Search the Community

Showing results for tags 'owed'.

-

I'm with Scottish Power pre-payment meter with key. Put £15 on card as usual. The gas meter read "error call help". So rang up and had the gas machine replaced with a new one. The person on the phone said they'll give me +£10 credit. Got new card in the mail later. Placed £5 to test. No extra +£10 credit, just the £5 I put on, and I still have the receipt of the original £15 and the old card. What are my options if they say they can't do anything about the £15? Not too bothered about the promised credit.

I'm with Scottish Power pre-payment meter with key. Put £15 on card as usual. The gas meter read "error call help". So rang up and had the gas machine replaced with a new one. The person on the phone said they'll give me +£10 credit. Got new card in the mail later. Placed £5 to test. No extra +£10 credit, just the £5 I put on, and I still have the receipt of the original £15 and the old card. What are my options if they say they can't do anything about the £15? Not too bothered about the promised credit. -

Hi, I work in sales and my contract was amended some months ago to give me 1% commission on all combined sales above a target figure. The target was designed to be easily achievable as my base salary was lower than I'd liked and I was effectively doing two jobs - both sales and IT. The commission became due so I requested it twice via email (no response) I then raised it again via telephone. I got sat down in a meeting with my manager and the finance guy, they tried to tell me it was not payable for several months longer and also that the company didn't have the money.. After numerous emails they said OK we will pay you x amount as soon as you agree, x being about 50% less than I was expecting! They are working out sales AFTER deducting tax, postage etc. they are saying that tax does not go to them, it goes to HMRC so it isn't considered part of a sales figure. My contract does not say whether sales are GROSS or NET, from several verbal discussions before I signed, I was under the impression sales were GROSS. The figure they suggest pays me approx. what I could get for doing the sales job elsewhere.. nothing more.. I also have effectively been on call and spent many extra unpaid hours.. I am sticking out for the full amount I think I'm owed and have given them 2 weeks to pay it - am I in the right? Thanks in advance.

Hi, I work in sales and my contract was amended some months ago to give me 1% commission on all combined sales above a target figure. The target was designed to be easily achievable as my base salary was lower than I'd liked and I was effectively doing two jobs - both sales and IT. The commission became due so I requested it twice via email (no response) I then raised it again via telephone. I got sat down in a meeting with my manager and the finance guy, they tried to tell me it was not payable for several months longer and also that the company didn't have the money.. After numerous emails they said OK we will pay you x amount as soon as you agree, x being about 50% less than I was expecting! They are working out sales AFTER deducting tax, postage etc. they are saying that tax does not go to them, it goes to HMRC so it isn't considered part of a sales figure. My contract does not say whether sales are GROSS or NET, from several verbal discussions before I signed, I was under the impression sales were GROSS. The figure they suggest pays me approx. what I could get for doing the sales job elsewhere.. nothing more.. I also have effectively been on call and spent many extra unpaid hours.. I am sticking out for the full amount I think I'm owed and have given them 2 weeks to pay it - am I in the right? Thanks in advance. -

Hi all, Santander have made an offer based only on the PPI amount and associated interest and no interest because... 'On a rolling line of credit account 8% out of pocket interest is only applied if the loan would have had a credit balance had the PPI not been included. ... This is in line with the requirements of the FOS and FCA' I believe this to be complete nonsense: I take a restitution approach with unjust enrichment. Had I had the PPI amount then I could have invested it and gained at least 8% interest. Has anyone challenged this and been succesful? Do you agree with me? How do you challenge their full and final offer? A letter first stating the argument I assume then ... FOS seem to be under pressure and likely take a while??? or... direct to county court? I have exactly the same argument presented to me for no interest offered on my Credit Card PPI.... Any advice would be helpful... thanks

Hi all, Santander have made an offer based only on the PPI amount and associated interest and no interest because... 'On a rolling line of credit account 8% out of pocket interest is only applied if the loan would have had a credit balance had the PPI not been included. ... This is in line with the requirements of the FOS and FCA' I believe this to be complete nonsense: I take a restitution approach with unjust enrichment. Had I had the PPI amount then I could have invested it and gained at least 8% interest. Has anyone challenged this and been succesful? Do you agree with me? How do you challenge their full and final offer? A letter first stating the argument I assume then ... FOS seem to be under pressure and likely take a while??? or... direct to county court? I have exactly the same argument presented to me for no interest offered on my Credit Card PPI.... Any advice would be helpful... thanks -

Hello everyone, My father is paying a very large amount of CSA debt, payments which cover my brother and I up until the age of 18. However, I know that for me - this is incorrect. My mother was neglectful/ treated me very badly in my childhood, which resulted in me leaving home to live in a hostel before my 17th birthday. After I left home, she refused to declare details of her income so that I could claim EMA (education maintenance allowance) whilst I was at college- whilst continuing to claim family allowance for me as if I was still at home, resulting in me having no income whatsoever. Then when I started university, she refused to get involved with any of the forms I needed to complete. In both situations, it had to be noted that I was estranged from my mother and father in order to be eligible for support and move forward. I understand that these payments are forwarded from CSA to my mother, but of course I dont agree she should get payment for me from when I was 16 to 18. I am not raising this issue to defend my father, as bottom line is that he did not maintain us. But does anyone have any idea how CSA might deal with the matter regarding myself if I were to inform them? Thank you all, Jo.

-

Hello, I owe service charge backpayment to my management agent for my leasehold property. They took it to county court, then fast tracked to high court without informing me. I only knew when I received a demand for £2100 from the Sheriff's office. I offered to pay in instalments but they said their client wanted full payment, which I could not do. I sent them a copy of my Debt and Mental Health Evidence Form, they said their client rejected it. A Baliff visited my property when I was not in. I submitted an income and expenditure form (both mine and my wife's)to the sheriff's office, which clearly shows a minus. Even so I offered to pay £50 a month. I have now had an email saying they will forward this to their client and if it is rejected I will receive a visit from the Baliff without any prior notice. The amount has risen from £2100 to £3700 in just over 6 weeks, with interest at 41p a day. There is also a charge for a Baliff visit that never happened. I am worried sick. Please, if you can, please advise. I feel due process was not followed regarding the secrecy in taking this to court. I suffer from depression due to my debt issues and this is really affecting me

Hello, I owe service charge backpayment to my management agent for my leasehold property. They took it to county court, then fast tracked to high court without informing me. I only knew when I received a demand for £2100 from the Sheriff's office. I offered to pay in instalments but they said their client wanted full payment, which I could not do. I sent them a copy of my Debt and Mental Health Evidence Form, they said their client rejected it. A Baliff visited my property when I was not in. I submitted an income and expenditure form (both mine and my wife's)to the sheriff's office, which clearly shows a minus. Even so I offered to pay £50 a month. I have now had an email saying they will forward this to their client and if it is rejected I will receive a visit from the Baliff without any prior notice. The amount has risen from £2100 to £3700 in just over 6 weeks, with interest at 41p a day. There is also a charge for a Baliff visit that never happened. I am worried sick. Please, if you can, please advise. I feel due process was not followed regarding the secrecy in taking this to court. I suffer from depression due to my debt issues and this is really affecting me -

Hi all, I have a long winded situation. I have council tax debt that has gone up to £5,000. This has been going on from more than 8 years from a different house I lived at before moving in to my own house. The council has passed all dealing and account to solicitors who I have had a few email communication with confirming I will be making a £100 monthly payment towards the debt as well as paying £1200 of council tax on my current property yearly. The house is worth £285k today. Three different Charging Orders have been applied to the house for council tax debt as I have tried to keep up with paying for the council tax going forward and also paying for the debt owed from years back. It has been such a challenge as the type of work I do is contracts which is not too regular. I am currently not working, I have three children with the youngest a year old and oldest 8 years old. My Partner works part time. I have just had this bulky document come through the post. They are court papers. The Council are taking me to court to push for a sale of my house I live in to recover 5k of the money owed. This is very distressful and annoying to say the least. I have offered to be paying £100 towards the debt, who refused it contending that their client - the council - are not accepting this as it will take too long to pay off the money owed. The court date is for the 18th of October next month in the meantime, there is a job I am scheduled to commence on the 2nd of October too which will enable me make some bigger payment towards the debt. The issue now is, legally, where do I stand and how do I contest this as it stands. I have evidence of all the payments I have made so far and email correspondence What advice and how do I proceed, it can not be just and equitable to push for a sale of a house worth £285k over a 5k debt with children in the house!! I am not disputing the money owed either, I just need more time to come up with some of the money. I am not in receipt of any benefit from the state either. I await your responses and thanks in advance all.

Hi all, I have a long winded situation. I have council tax debt that has gone up to £5,000. This has been going on from more than 8 years from a different house I lived at before moving in to my own house. The council has passed all dealing and account to solicitors who I have had a few email communication with confirming I will be making a £100 monthly payment towards the debt as well as paying £1200 of council tax on my current property yearly. The house is worth £285k today. Three different Charging Orders have been applied to the house for council tax debt as I have tried to keep up with paying for the council tax going forward and also paying for the debt owed from years back. It has been such a challenge as the type of work I do is contracts which is not too regular. I am currently not working, I have three children with the youngest a year old and oldest 8 years old. My Partner works part time. I have just had this bulky document come through the post. They are court papers. The Council are taking me to court to push for a sale of my house I live in to recover 5k of the money owed. This is very distressful and annoying to say the least. I have offered to be paying £100 towards the debt, who refused it contending that their client - the council - are not accepting this as it will take too long to pay off the money owed. The court date is for the 18th of October next month in the meantime, there is a job I am scheduled to commence on the 2nd of October too which will enable me make some bigger payment towards the debt. The issue now is, legally, where do I stand and how do I contest this as it stands. I have evidence of all the payments I have made so far and email correspondence What advice and how do I proceed, it can not be just and equitable to push for a sale of a house worth £285k over a 5k debt with children in the house!! I am not disputing the money owed either, I just need more time to come up with some of the money. I am not in receipt of any benefit from the state either. I await your responses and thanks in advance all. -

Hello, Back in January 2015 i started a new job and with it came a company car, i got all the details and immediately called HMRC to inform them of this. Fast forward a few months and in August 2015 i left the company,returned the company car and again immediately called HMRC to inform them of this. Started a new job with a new company in September 2015 which didn't come with a company car. I get a letter from HMRC in September 2015 to say that i have underpaid tax so i call them up and they say its to do with the company car i used to have in the old job, they said they will adjust my tax code to make sure i pay back what i owe in the next financial year. I never really argued and said ok. Fast forward to now and i am still paying it back and my tax code has changed at least twice because of it all. Surely i shouldn't be paying back tax on a company car i returned back in August 2015 and even informed HMRC of all the changes??

-

Hi there. I want some advice on what to do next and will start from the very beginning so that I have all the details in the right order. Over a month ago my Dad and myself worked with companies that can help you claim back PPI, we went with different companies and never heard anything back. I only have a credit card but my Dad and my Mum (who has passsed on) had a lot of loans and a mortgage about 17 years ago. This was cleared off in 2009 and the loan was with Blemain Finance. my Dad had a lot more than me. Unfortunately about 3 weeks ago my Dad had an accident which required him to be in hospital for just under 3 weeks about a week into his time in hospital my sister got a letter that was addressed to my Dad but it was her address on the letter and she said in this letter there was a lot of charges and money owed back to my Dad. One was over £200 and then there was another sum of over £300 so altogether it was over £500. I mentioned the name Blemain Finance because for years I know my parents paid them for the loan they had for the mortgage, it's the first name that came to mind and my sister said yes. Unfortunately my sister cannot find that letter now but is still looking to try and find it. I don't want my Dad to lose out on this letter I called the PPI company that was in charge of his claim and they said they knew nothing about it, they had heard no word from anyone and they actually never contacted Blemain Finance so they can't explain it at all. They just advised to wait and perhaps another letter would be sent out and whatever letter or offer was sent would be sent to my Dad, they said they wouldn't know about any kind of offer that was offered. I then asked for advice on another forum and a kind member of that forum directed me to here because I have no way of contacting Blemain Finance directly and I can see on this forum that other people are having this same trouble too. I can only go from memory, I'm sure the Bank of Scotland/Halifax were involved in the mortgage too, I think in 2009 a good 18,000 was owed and paid to them. My parents sold their house and I know that £18,000 was paid to clear the debt with Blemain Finance. I've no idea what was paid over the years. My Dad says it was a good 17 years all in. Can anyone advise me on the best steps to take from now on? My sister did say yes it said Blemain Finance on the letter but obviously I never seen the actual letter, it could have been another company acting on their behalf. Also bare in mind that the debt was cleared in 2009, the £18,000 was paid but I've no idea the total paid for all those years prior The offer was over £500 but with all that money paid to them and some of the horror stories I've read on here I can't help but feel that there could be a lot more owed to my Dad. What would be the best course of action for my Dad to take to not only see about the £500+ owed but to see if that sum is actually right and if more money is owed to him. If anyone can give me advice on what to do and how to do it I would be very grateful. The only thing I can't explain is how the letter was sent to my sister's address. What can we do to not only contact them but to see if over those 17 years and what my parent's paid and if there is anything owed back to my Dad? Thanks

-

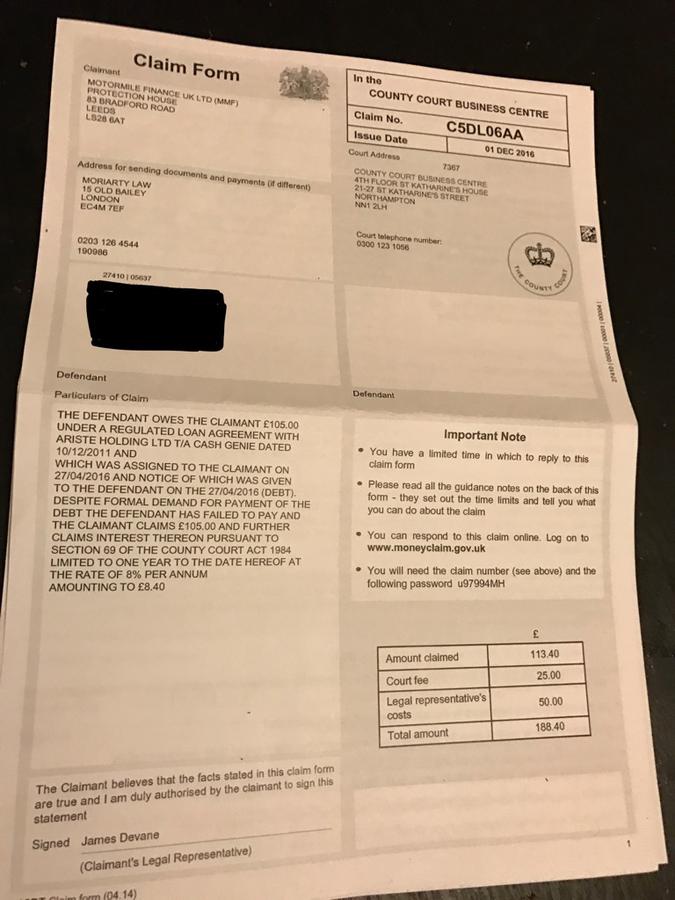

I was gong through bad time financially few years ago and I built up some debts using payday loans such as Cash Genie. Or Motormile finance. I received a letter from Moriarty Law saying they're sending me county court papers for £105 I still owe Cash Genie from 2011. I also received county court claim form and I attached a copy. My main problem that I work for financial institution so if I get CCJ I'll be forced to quit my job. Can they really take you to county for only £105??? Now they increased it to £188 with court fees and theirs. This is looks serious and I'm worried! Any advice is appreciated guys! Thanks in advance Angela.

I was gong through bad time financially few years ago and I built up some debts using payday loans such as Cash Genie. Or Motormile finance. I received a letter from Moriarty Law saying they're sending me county court papers for £105 I still owe Cash Genie from 2011. I also received county court claim form and I attached a copy. My main problem that I work for financial institution so if I get CCJ I'll be forced to quit my job. Can they really take you to county for only £105??? Now they increased it to £188 with court fees and theirs. This is looks serious and I'm worried! Any advice is appreciated guys! Thanks in advance Angela.

-

My contract with Virgin Media was terminated on the 4th May due to the fact that they broke contract by way of serious issues with my broadband which they admitted they had trouble fixing and gave me permission to leave without charge or penalty. I've received my final bill to say I am owed a refund of around £15. I was told initially it was to be refunded within 14 days of cancelled contract. Its now over 14 days and I've not receive the monies due. Any advice please.

-

Hello all. A while back I defaulted on a Vodafone account, and now owe them a four figure sum. I haven't been able to clear the debt due to low income and focusing on priority debts. I can't remember if I received a default notice or not (the default is on my credit reports) but the amount that is in the letter of assignment is double than what is owed. The amount owed is on the default on the credit reports and the previous letters received from Vodafone, I'm 100% sure that the amount I was originally told I owed is correct. What I don't understand is that amount on the letter of assignment is exactly double of the true value of the debt. The default was placed in June last year so I can't understand why or how the amount owed can double in 9 months when the service was cancelled before June 2016. Can they legally double a debt when they sell it to Lowells? Any advice regarding this would be appreciated.

Hello all. A while back I defaulted on a Vodafone account, and now owe them a four figure sum. I haven't been able to clear the debt due to low income and focusing on priority debts. I can't remember if I received a default notice or not (the default is on my credit reports) but the amount that is in the letter of assignment is double than what is owed. The amount owed is on the default on the credit reports and the previous letters received from Vodafone, I'm 100% sure that the amount I was originally told I owed is correct. What I don't understand is that amount on the letter of assignment is exactly double of the true value of the debt. The default was placed in June last year so I can't understand why or how the amount owed can double in 9 months when the service was cancelled before June 2016. Can they legally double a debt when they sell it to Lowells? Any advice regarding this would be appreciated. -

Having received funds to pay my charging order, Marlin owe me the outstanding amount but are refusing to pay claiming they do not have enough details about me to do so. I have provided everything I can and feel as though they are trying to get as much info as possible not just what is required. Should I now issue a claim as I have spent weeks sending them more and more info?

-

Hi Looking for some advice please. I was a customer of First Utility they stopped being able to issue me with a bill after almost a year I referred the case to the Energy Ombudsman and the complaint was resolved to my satisfaction. During this time I switched my supply (October 2015), I agreed a final amount with F/Utility of £111.52 & this was paid. Today I received a letter from their credit management company stating that I owe them £112.50. I'm reluctant to respond to the letter to be honest but I don't want the situation to blow up. Surely F/Utility should have made contact with me if I owed them money!? Thank you

Hi Looking for some advice please. I was a customer of First Utility they stopped being able to issue me with a bill after almost a year I referred the case to the Energy Ombudsman and the complaint was resolved to my satisfaction. During this time I switched my supply (October 2015), I agreed a final amount with F/Utility of £111.52 & this was paid. Today I received a letter from their credit management company stating that I owe them £112.50. I'm reluctant to respond to the letter to be honest but I don't want the situation to blow up. Surely F/Utility should have made contact with me if I owed them money!? Thank you -

I took out a payday loan with quickquid for around £200, couldn't pay back as I lost my job and fast forward to now, I owe ARC Europe £333.80, what is the best way to deal with this? Thanks.

-

My first contribution to this site. I owe the Co-operative Bank money on a credit card and had problems with repayments. They were being quite unpleasant about it (I had asked for a 'breathing space') in one week claimed to have passed my debt onto a collection agency and then said they were taking me to court. I wrote to the CEO Niall Booker and he sorted things out and I received an apology and a cheque for £75. its worth going straight to the top. I also discovered that Phil Burrows who I received a lot of post from doesn't actually work there anymore! Is this normal for a bank to continue using the name of an ex-employee on their letters? Does Phil Burrows know?

My first contribution to this site. I owe the Co-operative Bank money on a credit card and had problems with repayments. They were being quite unpleasant about it (I had asked for a 'breathing space') in one week claimed to have passed my debt onto a collection agency and then said they were taking me to court. I wrote to the CEO Niall Booker and he sorted things out and I received an apology and a cheque for £75. its worth going straight to the top. I also discovered that Phil Burrows who I received a lot of post from doesn't actually work there anymore! Is this normal for a bank to continue using the name of an ex-employee on their letters? Does Phil Burrows know? -

Hi Everyone Im hoping for some help on this please. I took out finance december 2015 on a vehicle, immediately fell into difficulties in January and had the car repossessed. I was in complete communication with the finance company, met the transporter to recover the car and kept talking with them throughout. They explained that there may be a shortfall from the resale of the vehicle which i appreciated I heard nothing for a month or so, but expecting there to be some shortfall emailed the company to find out what happened next . I then had a letter sent to my address from their solicitors saying a CCJ had been registered and that I had to reply to the CCJ that would be sent. Next thing I received was a CCJ had been awarded to the claimant asking for £392 a month to cover the balance of almost £8k - when only £9k was borrowed, the car was returned in immaculate condition and was resold almost immediately for over £8k (internet search showed this) I found out that despite having my correct address, the ccj was sent to my previous address. Where do i stand in having to pay back almost 90% of the finance despite no longer having the vehicle? And where do i stand that I have never had the oppurtunity to represent myself in court to explain that the vehicle was returned due to the fact that the finance company explained the shortfall would only be small and manageable? Thanks in advance

Hi Everyone Im hoping for some help on this please. I took out finance december 2015 on a vehicle, immediately fell into difficulties in January and had the car repossessed. I was in complete communication with the finance company, met the transporter to recover the car and kept talking with them throughout. They explained that there may be a shortfall from the resale of the vehicle which i appreciated I heard nothing for a month or so, but expecting there to be some shortfall emailed the company to find out what happened next . I then had a letter sent to my address from their solicitors saying a CCJ had been registered and that I had to reply to the CCJ that would be sent. Next thing I received was a CCJ had been awarded to the claimant asking for £392 a month to cover the balance of almost £8k - when only £9k was borrowed, the car was returned in immaculate condition and was resold almost immediately for over £8k (internet search showed this) I found out that despite having my correct address, the ccj was sent to my previous address. Where do i stand in having to pay back almost 90% of the finance despite no longer having the vehicle? And where do i stand that I have never had the oppurtunity to represent myself in court to explain that the vehicle was returned due to the fact that the finance company explained the shortfall would only be small and manageable? Thanks in advance -

Hi, I am after some help please. I had a debt that I have been paying off to `Newman Debt recovery` from back in 2007. I have been paying off £10 a month as agreed with them. Well the payment I paid in Dec 2016 was paid, but then paid back into my account, and the same happened to my Jan 2017 payment. I dug out the paperwork, and according to the last letter I have back from 12th Sept 2007, the remaining balance was £882.18. So by my calculations, the last accepted payment that was not returned I have paid till Nov 2016 makes the total paid of £1100 ( £10 per month). This means I have paid £217.82 more then I needed to. I have tried to E-mail them but their e-mail just bounces back. Tried to Phone them, but not getting much joy either. What are my chances of get this money back and what options have I got to try and recover this over payment? Thank you in advance Jon.

Hi, I am after some help please. I had a debt that I have been paying off to `Newman Debt recovery` from back in 2007. I have been paying off £10 a month as agreed with them. Well the payment I paid in Dec 2016 was paid, but then paid back into my account, and the same happened to my Jan 2017 payment. I dug out the paperwork, and according to the last letter I have back from 12th Sept 2007, the remaining balance was £882.18. So by my calculations, the last accepted payment that was not returned I have paid till Nov 2016 makes the total paid of £1100 ( £10 per month). This means I have paid £217.82 more then I needed to. I have tried to E-mail them but their e-mail just bounces back. Tried to Phone them, but not getting much joy either. What are my chances of get this money back and what options have I got to try and recover this over payment? Thank you in advance Jon. -

Hi all, I reclaimed my PPI from a number of lenders a few years ago using the great advice and letters etc on here, eternally grateful for that! But.... I've had a few calls from claim companies over the last few months and they claim that a lot of lenders knowingly underpaid on PPI claims and that more is owed. I was wondering if there's any truth to that and, if so, would it be a case of following the same process as previously to claim the extra owed? Thanks, Nick

Hi all, I reclaimed my PPI from a number of lenders a few years ago using the great advice and letters etc on here, eternally grateful for that! But.... I've had a few calls from claim companies over the last few months and they claim that a lot of lenders knowingly underpaid on PPI claims and that more is owed. I was wondering if there's any truth to that and, if so, would it be a case of following the same process as previously to claim the extra owed? Thanks, Nick -

Hi all. Very briefly, my friend worked for an employer last year who paid him by bank transfer and never gave him a pay slip. My friend resigned at Christmas and since then has sent letters to the employer asking for payment for 2 days worked, 2 days bank holiday pay and 2 days holiday pay. He has since asked me to help him make a claim against his ex-employer. Evidence-wise, we have this: Original advert in local paper Bank Statements showing 7 bank transfers made to my friend's bank account starting on 11.9.2015 and ending 18.12.2015 totalling £4718 Copies of letter and email sent to employer Proof of receipt of letter. He is owed money for the last 2 days he worked (21&22 December 2015), 2 days holiday pay and 2 days bank holiday pay. He works this out as £9 x 8 hours x 6 days=£432 Is this the correct amount or do we work out the Tax and NI he would have had deducted? (although his employer, apparently, never paid his NI or Tax) My question is, do you think that we have enough evidence to proceed? And, if so, is an LBA the next move, detailing the above information? Thank you in advance, B

Hi all. Very briefly, my friend worked for an employer last year who paid him by bank transfer and never gave him a pay slip. My friend resigned at Christmas and since then has sent letters to the employer asking for payment for 2 days worked, 2 days bank holiday pay and 2 days holiday pay. He has since asked me to help him make a claim against his ex-employer. Evidence-wise, we have this: Original advert in local paper Bank Statements showing 7 bank transfers made to my friend's bank account starting on 11.9.2015 and ending 18.12.2015 totalling £4718 Copies of letter and email sent to employer Proof of receipt of letter. He is owed money for the last 2 days he worked (21&22 December 2015), 2 days holiday pay and 2 days bank holiday pay. He works this out as £9 x 8 hours x 6 days=£432 Is this the correct amount or do we work out the Tax and NI he would have had deducted? (although his employer, apparently, never paid his NI or Tax) My question is, do you think that we have enough evidence to proceed? And, if so, is an LBA the next move, detailing the above information? Thank you in advance, B -

Hi, My ex (the mother to my son) has run away to Scotland (about 4 months ago) and left him behind with me and my girlfriend. We had a signed agreement (witnessed by a solicitor) that after a couple of months of moving up there she would pay £100 a month towards feeding/clothing/school etc, she paid twice then went silent, completely silent, doesn't even ring to speak to him anymore. So i got the CMS involved, I paid the extra to have it done as a collect and pay, as historically she has been bad with money. I know she was working as of two weeks ago, and had been up to that point at about 40 hours a week, but the CMS have claimed she should only pay NIL per week. I have the right to appeal, but I just want to know how? It might sound stupid and there is instructions on how to do it etc, but, I don't want to miss anything with this possible one chance to appeal and get it started. Can anyone advise on how and what to ask for them to do etc? I can't talk to my ex and I don't have anyone near her to see if she is working, but I'm almost positive she is, which is why I'm quite surprised they have come back with NIL. Cheers.

-

nb. subject should be freeholder not leaseholder Hi, in a nutshell we are trying to get information on ground rent owed to freeholder and monies we believe owed to my partner (leaseholder) from the freeholder and not sure what action to take next. Here's the timeline and more information: Dec 2013 Roof of my partner and her then husband (we'll call him Gru) leaks resulting in exterior and interior damage to property Freeholder refuses to make insurance claim as behind on ground rent despite not providing my partner and Gru with required invoices for ground rent Decision made to have work carried out by partner and Gru and pay contractors directly March 2014 Up to date on ground rent Freeholder makes insurance claim Insurance payout agreed by Gru and paid to freeholder - £975 Insurance payout not forwarded on. Not chased due to personal circumstance including partner not living at home. At some point a verbal agreement on paying ground rent was reached with Gru while he resided at the property which my partner was not party to. Still no invoices from freeholder for ground rent. My partner moved back into the property in February 2015 and Gru moved out. May 2015 Letter hand delivered to freeholder (he's local) requesting payment of insurance money June 2015 Second letter sent to freeholder, same as above August 2015 LBA sent to leaseholder threatening court action September 24th 2015 Email sent to leaseholder in last ditch effort to stave off court action September 25th 2015 Reply from freeholder intimating an amicable solution regards offsetting ground rent and insurance payout October 12th 2015 Chased freeholder for information October 19th 2015 Chased freeholder again for information October 19th 2015 Freeholder replied advising still looking for some of the information October 20th 2015 Polite confirmation What action should we take next? I'm aware it's good to show effort to mediate before jumping in with court action and freeholder has shown his desire to counter-sue for ground rent, even though he appears unable or unwilling to provide us with information on how much we owe for ground rent. Not even sure if he can hold onto the insurance money in lieu of ground rent. Any help and advice greatly appreciated. Thanks, Kris

nb. subject should be freeholder not leaseholder Hi, in a nutshell we are trying to get information on ground rent owed to freeholder and monies we believe owed to my partner (leaseholder) from the freeholder and not sure what action to take next. Here's the timeline and more information: Dec 2013 Roof of my partner and her then husband (we'll call him Gru) leaks resulting in exterior and interior damage to property Freeholder refuses to make insurance claim as behind on ground rent despite not providing my partner and Gru with required invoices for ground rent Decision made to have work carried out by partner and Gru and pay contractors directly March 2014 Up to date on ground rent Freeholder makes insurance claim Insurance payout agreed by Gru and paid to freeholder - £975 Insurance payout not forwarded on. Not chased due to personal circumstance including partner not living at home. At some point a verbal agreement on paying ground rent was reached with Gru while he resided at the property which my partner was not party to. Still no invoices from freeholder for ground rent. My partner moved back into the property in February 2015 and Gru moved out. May 2015 Letter hand delivered to freeholder (he's local) requesting payment of insurance money June 2015 Second letter sent to freeholder, same as above August 2015 LBA sent to leaseholder threatening court action September 24th 2015 Email sent to leaseholder in last ditch effort to stave off court action September 25th 2015 Reply from freeholder intimating an amicable solution regards offsetting ground rent and insurance payout October 12th 2015 Chased freeholder for information October 19th 2015 Chased freeholder again for information October 19th 2015 Freeholder replied advising still looking for some of the information October 20th 2015 Polite confirmation What action should we take next? I'm aware it's good to show effort to mediate before jumping in with court action and freeholder has shown his desire to counter-sue for ground rent, even though he appears unable or unwilling to provide us with information on how much we owe for ground rent. Not even sure if he can hold onto the insurance money in lieu of ground rent. Any help and advice greatly appreciated. Thanks, Kris -

I definitely will. Thank you, I just wanted to know if there was anything that I'm missing or not doing correctly. For example, what would happen if the court finds that my friend has totalled up the total owed slightly incorrectly, maybe out by £50 or so? Do they then act upon this, etc?

-

Hi I was wondering whether anyone would be able to give me some advice. A couple of years ago I allowed a friend to order a PS3 from my catalogue and they received this without any problems. However she then started struggling to pay and I gave her leeway. A few occasions since I tried to get the money owed but it was one excuse after another and me being quite soft I let her off and tried to give her time. Once she asked if I could pass her onto my catalogue and she could sort a payment plan out with them. However after speaking to my catalogue they said the account is in my name and I am responsible for the debt. Over the last few days I have tried to ask her to pay again and she again said I should pass her to the catalogue. When I told her that it was paid off some time ago and she owes the money to me she said she wouldn't be paying me and I should have sorted this out years ago. I was wondering where I said on this, obviously I have proof the PS3 was delivered to her address. Would I be able to raise a court action against her or something? Thanks for reading this

-

Hi, my balance was £6,700 on my MBNA credit card and paid £4,409 which made my new balance £2,224 owed. My direct debit then paid the minimum of £67 which should of then made my newer balance £2,157 but this did not happen, instead, my balance owed went from £2,224 to £2,291, adding £67 to the debt rather than deducting it. I'm currently in a interest free offer and I have not used my card. This has never happened before, it's strange.

Hi, my balance was £6,700 on my MBNA credit card and paid £4,409 which made my new balance £2,224 owed. My direct debit then paid the minimum of £67 which should of then made my newer balance £2,157 but this did not happen, instead, my balance owed went from £2,224 to £2,291, adding £67 to the debt rather than deducting it. I'm currently in a interest free offer and I have not used my card. This has never happened before, it's strange. -

A while back we decided to pay a direct debit of 200£ to Spark energy our supplier. Since then we have regularly checked the meter and added the numbers into our account. We also had someone come around a couple of times to take the reading. Recently My boyfriend discovered that we had 800£ in our spark energy account. He contacted Spark energy to get a refund. they wanted another meter reading, which we gave them last night. Their reply was: "Thanks for that. The bill at the end of March wasn't charging for your gas so I corrected everything on your account so that it'll bill correctly going forward. As at the end of May, the credit balance is now £ 310.37. Would you like me to refund you about £300 and then set the direct debit at £100 per month as that's your average usage? Please bear in mind that refunds do take 28 working days to process. Alternatively, we could lower your direct debit to about £65 per month if you prefer." To me, this doesn't add up and sounds like a con. How could we have used 500£ of gas in the last 3 months, if our average according to them is 10£ a month. I know that back-billing only applies to bills that are over 12 months old, but can we fight this? get the Ombudsman involved? Thanks for your help

A while back we decided to pay a direct debit of 200£ to Spark energy our supplier. Since then we have regularly checked the meter and added the numbers into our account. We also had someone come around a couple of times to take the reading. Recently My boyfriend discovered that we had 800£ in our spark energy account. He contacted Spark energy to get a refund. they wanted another meter reading, which we gave them last night. Their reply was: "Thanks for that. The bill at the end of March wasn't charging for your gas so I corrected everything on your account so that it'll bill correctly going forward. As at the end of May, the credit balance is now £ 310.37. Would you like me to refund you about £300 and then set the direct debit at £100 per month as that's your average usage? Please bear in mind that refunds do take 28 working days to process. Alternatively, we could lower your direct debit to about £65 per month if you prefer." To me, this doesn't add up and sounds like a con. How could we have used 500£ of gas in the last 3 months, if our average according to them is 10£ a month. I know that back-billing only applies to bills that are over 12 months old, but can we fight this? get the Ombudsman involved? Thanks for your help