Search the Community

Showing results for tags 'county court'.

-

Hi, I am extremely worried about the possible eviction. I have mortgage with Birmingham Midshires. I live in the property with my mother who is 68, wife and four children age from 1 to 6. Back in 2009 I had mortgage arrears for which court granted the suspended repossession order on the terms that I pay £100 towards the arrears every month. which I did. After some time the lender capitalized the arrears. After few years i got in arrears again but situation got worse because how the payment team at lender dealt with my account. I made complaint on 2 occasions. My complaint was resolved by awarding me the payment of £100 on one occasion and another time £250. February last year I was in arrears, I contacted the lender but ended up in dispute on the way my account was being handled. I complaint to financial ombudsman. They contacted me and lender few time. Until today i don't know the outcome. Now i have received a letter from court for hearing on 23rd Jan. The lender has applied to the court for the decision on to "The Claimant respectfully requests that the court make the following Order" "The Claimant permission to apply for a Warrant of Possession pursuant to CPR 83.2(3)(a) and that permission shall remain valid for 6 years from the date permission is granted". The arrears are around £13k. I am in a position to make ongoing monthly payment as well as substantial amount towards arrears. Can you please advise what the lender is asking the court? Are they asking for eviction warrant? I am very worried because if the y get the eviction order on the hearing on 23rd i have no where to take my children to. Please help how can I defend this as well as is this hearing for eviction? If so, how soon this can happen? Have i lost all now? Thanks.

Hi, I am extremely worried about the possible eviction. I have mortgage with Birmingham Midshires. I live in the property with my mother who is 68, wife and four children age from 1 to 6. Back in 2009 I had mortgage arrears for which court granted the suspended repossession order on the terms that I pay £100 towards the arrears every month. which I did. After some time the lender capitalized the arrears. After few years i got in arrears again but situation got worse because how the payment team at lender dealt with my account. I made complaint on 2 occasions. My complaint was resolved by awarding me the payment of £100 on one occasion and another time £250. February last year I was in arrears, I contacted the lender but ended up in dispute on the way my account was being handled. I complaint to financial ombudsman. They contacted me and lender few time. Until today i don't know the outcome. Now i have received a letter from court for hearing on 23rd Jan. The lender has applied to the court for the decision on to "The Claimant respectfully requests that the court make the following Order" "The Claimant permission to apply for a Warrant of Possession pursuant to CPR 83.2(3)(a) and that permission shall remain valid for 6 years from the date permission is granted". The arrears are around £13k. I am in a position to make ongoing monthly payment as well as substantial amount towards arrears. Can you please advise what the lender is asking the court? Are they asking for eviction warrant? I am very worried because if the y get the eviction order on the hearing on 23rd i have no where to take my children to. Please help how can I defend this as well as is this hearing for eviction? If so, how soon this can happen? Have i lost all now? Thanks. -

Hi I hope you are all well. I have recently received a county court claim from VCS. It was for parking on the premises shared by a few different businesses. I went to the gym that evening and had to park a bit further out, not realising that there were boundaries set for the different businesses on the premises. The signage looks exactly the same unless scrutinised up close. I cam out out of the gym and found a ticket stuck to my window. I queried it with the staff at the gym a few days later and they said there was nothing that they could do. Lots of their members had received these fines. Their advice was to write them a letter or ignore it. Needless to say, I never parked there again but that didnt help the fact that I already received a CN from them. I have completed the details below and also logged onto MCOL and did the AOS Please advise what next step should be. I have also received a letter from VCS so looks like they are going it alone, without a solicitor. Thanks WS Name of the Claimant ? Vehicle Control Services claimants Solicitors: No Solicitor listed on claim form Date of issue –08 May 2018 What is the claim for – 1.The claim against the defendant is for breach of contract in respect to breaching the terms and conditions set on Private land. The Defendant was issued with a charge notice (CN) and has failed to settle their outstanding liabilities. 2.At all material times the defendant was the registered keeper and/or driver of the vehicle identified in the provided particulars of claim. 3.It is alleged that the defendant breached the terms and conditions of entering private land as detailed in the particulars of claim (to follow). 4.The claimant seeks the recovery of the CN and interest under section 69 of the conty court act of 1984 at the rate of 8% at the same rate up to the date of judgement or earlier payment. I will provide the defendant with separate detailed particulars within 14 days. What is the value of the claim? £185 Has the claim been issued by the Private parking Company or was the PCN assigned and it is the Debt purchaser who has issued the claim ? Claim has been issues by PCN (Parking Company) Were you aware the account had been assigned – did you receive a Notice of Assignment? N/A I also found the below CPR 31.14 to send to VCS.. I will get that in the post tomorrow unless you need more information from me.. Do I need to send a copy to the court as well and do you recommend recorded delivery of the CPR 31.14? Thanks __________________________________ To VCS [Your address] . [Their address [solicitors] . [Date] . Dear Sir or Madam, . Re: (Claimant's name) v (Your name) Case No: . CPR 31.14 Request . On (date) I received the claim formicon in this case issued by you out of the (Name) county courticon. . I confirm having returned my acknowledgement of service to the court in which I indicate my intention to contest all of your claim. . Please treat this letter as my request made under CPR 31.14 for the disclosure and the production of a verified and legible copy of [each of the following / the] document(s) mentioned in your Particulars of Claim: . 1. the contract between [parking company name] and the landowner that assigns the right to enter into contracts with the public and make claims in their own name,. . 2.proof of planning permission granted for signage etc under the Town and Country Planning Act 2007 . 3.copies of the notice to driver, notice to keeper and any other correspondence from [insert Claimant Name] & [insert Solicitors Name} to the defendant that they intend to rely upon in court. . You should ensure compliance with your CPR 31 duties and ensure that the document(s) I have requested are disclosed at your earliest convenience.. . Your CPR 31 duties extend to making a reasonable and proportionate search for the originals of the documents I have requested, the better for you to be able to verify the document's authenticity and to provide me with a legible copy. . Further, where I have requested a copy of a document, the original of which is now in the possession of another person, you will have a right to possession of that document if you have mentioned it in your case. You must take immediate steps to recover and preserve it for the purpose of this case. . Where I have mentioned a document and there is in your possession more than one version of that same document owing to a modification, obliteration or other marking or feature, each version will be a separate document and you must provide a copy of each version of it to me. Your obligations extend to making a reasonable and proportionate search for any version(s) to include an obligation to recover and preserve such version(s) which are now in the possession of a third party. . In accordance with CPR 31.15© I undertake to be responsible for your reasonable copying costs incurred in complying with this CPR 31.14 request. . If you are unable to comply with this request within 14 days and believe that you will never be able to comply with this request please confirm in your response. . You are reminded that as this case is yet to be allocated to a track, CPR31:14 does apply, a refusal to comply because you 'think' at this stage you dont have too will be used against you in any filed defence. . Yours faithfully . TYPE YOUR NAME DO NOT SIGN IT

Hi I hope you are all well. I have recently received a county court claim from VCS. It was for parking on the premises shared by a few different businesses. I went to the gym that evening and had to park a bit further out, not realising that there were boundaries set for the different businesses on the premises. The signage looks exactly the same unless scrutinised up close. I cam out out of the gym and found a ticket stuck to my window. I queried it with the staff at the gym a few days later and they said there was nothing that they could do. Lots of their members had received these fines. Their advice was to write them a letter or ignore it. Needless to say, I never parked there again but that didnt help the fact that I already received a CN from them. I have completed the details below and also logged onto MCOL and did the AOS Please advise what next step should be. I have also received a letter from VCS so looks like they are going it alone, without a solicitor. Thanks WS Name of the Claimant ? Vehicle Control Services claimants Solicitors: No Solicitor listed on claim form Date of issue –08 May 2018 What is the claim for – 1.The claim against the defendant is for breach of contract in respect to breaching the terms and conditions set on Private land. The Defendant was issued with a charge notice (CN) and has failed to settle their outstanding liabilities. 2.At all material times the defendant was the registered keeper and/or driver of the vehicle identified in the provided particulars of claim. 3.It is alleged that the defendant breached the terms and conditions of entering private land as detailed in the particulars of claim (to follow). 4.The claimant seeks the recovery of the CN and interest under section 69 of the conty court act of 1984 at the rate of 8% at the same rate up to the date of judgement or earlier payment. I will provide the defendant with separate detailed particulars within 14 days. What is the value of the claim? £185 Has the claim been issued by the Private parking Company or was the PCN assigned and it is the Debt purchaser who has issued the claim ? Claim has been issues by PCN (Parking Company) Were you aware the account had been assigned – did you receive a Notice of Assignment? N/A I also found the below CPR 31.14 to send to VCS.. I will get that in the post tomorrow unless you need more information from me.. Do I need to send a copy to the court as well and do you recommend recorded delivery of the CPR 31.14? Thanks __________________________________ To VCS [Your address] . [Their address [solicitors] . [Date] . Dear Sir or Madam, . Re: (Claimant's name) v (Your name) Case No: . CPR 31.14 Request . On (date) I received the claim formicon in this case issued by you out of the (Name) county courticon. . I confirm having returned my acknowledgement of service to the court in which I indicate my intention to contest all of your claim. . Please treat this letter as my request made under CPR 31.14 for the disclosure and the production of a verified and legible copy of [each of the following / the] document(s) mentioned in your Particulars of Claim: . 1. the contract between [parking company name] and the landowner that assigns the right to enter into contracts with the public and make claims in their own name,. . 2.proof of planning permission granted for signage etc under the Town and Country Planning Act 2007 . 3.copies of the notice to driver, notice to keeper and any other correspondence from [insert Claimant Name] & [insert Solicitors Name} to the defendant that they intend to rely upon in court. . You should ensure compliance with your CPR 31 duties and ensure that the document(s) I have requested are disclosed at your earliest convenience.. . Your CPR 31 duties extend to making a reasonable and proportionate search for the originals of the documents I have requested, the better for you to be able to verify the document's authenticity and to provide me with a legible copy. . Further, where I have requested a copy of a document, the original of which is now in the possession of another person, you will have a right to possession of that document if you have mentioned it in your case. You must take immediate steps to recover and preserve it for the purpose of this case. . Where I have mentioned a document and there is in your possession more than one version of that same document owing to a modification, obliteration or other marking or feature, each version will be a separate document and you must provide a copy of each version of it to me. Your obligations extend to making a reasonable and proportionate search for any version(s) to include an obligation to recover and preserve such version(s) which are now in the possession of a third party. . In accordance with CPR 31.15© I undertake to be responsible for your reasonable copying costs incurred in complying with this CPR 31.14 request. . If you are unable to comply with this request within 14 days and believe that you will never be able to comply with this request please confirm in your response. . You are reminded that as this case is yet to be allocated to a track, CPR31:14 does apply, a refusal to comply because you 'think' at this stage you dont have too will be used against you in any filed defence. . Yours faithfully . TYPE YOUR NAME DO NOT SIGN IT -

Hi Guys, Today i got a letter to say welcome finance has won the court case and i need to pay full balance of £5000 even thou i got a loan of £2000, I did apply last month online for to hold it off for 28days but as i'm getting redundant and getting all stressed but i have to do 4 week notice period i cant afford the full balance is there a way i can get round this and pay little bit till i get another job? please help im stressed enough,

Hi Guys, Today i got a letter to say welcome finance has won the court case and i need to pay full balance of £5000 even thou i got a loan of £2000, I did apply last month online for to hold it off for 28days but as i'm getting redundant and getting all stressed but i have to do 4 week notice period i cant afford the full balance is there a way i can get round this and pay little bit till i get another job? please help im stressed enough, -

Here are the current court fees which take effect from today 22nd April 2014. http://hmctsformfinder.justice.gov.uk/courtfinder/forms/ex050-eng.pdf http://www.consumeractiongroup.co.uk/forum/showthread.php?421493-Court-fees-increase-from-22nd-April-2014 http://www.legislation.gov.uk/ukdsi/2015/9780111127490

-

Just got back from holiday and I have a court letter sitting waiting for me Stopped paying this a fair while ago due to lack of funds but unsure actually how long ago. I've had no contact with them directly for ages it may possibly be over 6 years but not sure. I've had letters and it's skipped round the DCAs who I've ignored. Letter is dated 7/5/15 I intend to acknowledge later today on MCOL and I will send Howard Cohen a CCA request as a matter of course. I'm also inclined to send Santander a SAR Request as well but imagine my time to do anything is now limited? Any advice other than the above greatly received

Just got back from holiday and I have a court letter sitting waiting for me Stopped paying this a fair while ago due to lack of funds but unsure actually how long ago. I've had no contact with them directly for ages it may possibly be over 6 years but not sure. I've had letters and it's skipped round the DCAs who I've ignored. Letter is dated 7/5/15 I intend to acknowledge later today on MCOL and I will send Howard Cohen a CCA request as a matter of course. I'm also inclined to send Santander a SAR Request as well but imagine my time to do anything is now limited? Any advice other than the above greatly received -

Hi, I'm new on here and could do with some help, please. 12 weeks ago my friend ordered some parts for a roof extension he was making. He was verbally promised that the parts would be with him within the week. He paid a 20% deposit at this point. 9 weeks later the parts arrived and he was happy with them. 2 weeks ago my friend received a voice message from the company threatening court action if he didn't pay up. He then wrote to them (recorded delivery) to request an invoice as he planned to pay. This weekend they eventually sent the invoice for the amount plus £185 Court fees and £20.31 interest. They claim that they previously sent him an invoice. There was no Letter Before Action or any mention of one (if this is important?) My friend feels that he hasn't done a thing wrong and doesn't feel that he has to pay the court fees or interest as all he ever wanted, and politely asked for, was an invoice. Please can I ask for some help? Does he have to complete the court form or can he just pay the fee he believes is owed? Thank you in advance. Here are the details of the claim: Received a claim? Yes Issue Date: 2-10-2014 Amount approx: £5079 Claimant: Roof Trusses Solicitor: A C Jones Original Credit: Particulars of Claim: We manufactured and supplied timber frame panels and roof trusses to Dolycoed, Dolfor, Newtown on 8th September 2014 on behalf of the defendants who had ordered these from us. Our invoice TF4-34647A for the balance of £4874.22 remains outstanding - this invoice should have been paid on delivery. Despite numerous requests for payment nothing has been forthcoming. Neither party are responding to voicemails, letters or emails. We are not aware of any reason why this has not been paid. Interest is now payable at a rate of 5% per month as per our conditions of Business/Sale which currently equates to £20.31 Stat Barred? No Have sent: Other Info: 12 weeks ago my friend ordered some parts for a roof extension he was making. He was verbally promised that the parts would be with him within the week. He paid a 20% deposit at this point. 9 weeks later the parts arrived and he was happy with them. 2 weeks ago my friend received a voice message from the company threatening court action if he didn't pay up. He then wrote to them (recorded delivery) to request an invoice as he planned to pay. This weekend they eventually sent the invoice for the amount plus £185 Court fees and £20.31 interest. They claim that they previously sent him an invoice. There was no Letter Before Action or any mention of one (if this is important?) My friend feels that he hasn't done a thing wrong and doesn't feel that he has to pay the court fees or interest as all he ever wanted, and politely asked for, was an invoice. Please can I ask for some help? Does he have to complete the court form or can he just pay the fee he believes is owed?

Hi, I'm new on here and could do with some help, please. 12 weeks ago my friend ordered some parts for a roof extension he was making. He was verbally promised that the parts would be with him within the week. He paid a 20% deposit at this point. 9 weeks later the parts arrived and he was happy with them. 2 weeks ago my friend received a voice message from the company threatening court action if he didn't pay up. He then wrote to them (recorded delivery) to request an invoice as he planned to pay. This weekend they eventually sent the invoice for the amount plus £185 Court fees and £20.31 interest. They claim that they previously sent him an invoice. There was no Letter Before Action or any mention of one (if this is important?) My friend feels that he hasn't done a thing wrong and doesn't feel that he has to pay the court fees or interest as all he ever wanted, and politely asked for, was an invoice. Please can I ask for some help? Does he have to complete the court form or can he just pay the fee he believes is owed? Thank you in advance. Here are the details of the claim: Received a claim? Yes Issue Date: 2-10-2014 Amount approx: £5079 Claimant: Roof Trusses Solicitor: A C Jones Original Credit: Particulars of Claim: We manufactured and supplied timber frame panels and roof trusses to Dolycoed, Dolfor, Newtown on 8th September 2014 on behalf of the defendants who had ordered these from us. Our invoice TF4-34647A for the balance of £4874.22 remains outstanding - this invoice should have been paid on delivery. Despite numerous requests for payment nothing has been forthcoming. Neither party are responding to voicemails, letters or emails. We are not aware of any reason why this has not been paid. Interest is now payable at a rate of 5% per month as per our conditions of Business/Sale which currently equates to £20.31 Stat Barred? No Have sent: Other Info: 12 weeks ago my friend ordered some parts for a roof extension he was making. He was verbally promised that the parts would be with him within the week. He paid a 20% deposit at this point. 9 weeks later the parts arrived and he was happy with them. 2 weeks ago my friend received a voice message from the company threatening court action if he didn't pay up. He then wrote to them (recorded delivery) to request an invoice as he planned to pay. This weekend they eventually sent the invoice for the amount plus £185 Court fees and £20.31 interest. They claim that they previously sent him an invoice. There was no Letter Before Action or any mention of one (if this is important?) My friend feels that he hasn't done a thing wrong and doesn't feel that he has to pay the court fees or interest as all he ever wanted, and politely asked for, was an invoice. Please can I ask for some help? Does he have to complete the court form or can he just pay the fee he believes is owed? -

Name the issuing court: Glasgow Sheriff Court Who Is The Claimant: Cabot Financial UK limited Who Are the Solicitors: Nolans What type of action? Simple What is the claim for – On 14/10/2013 the Respondent entered a credit card agreement with New Day Ltd under which the Respondent borrowed money from them repayable on demand. The said agreement was an agreement under the Consumer Credit Act 1974. The date of termination was 31/03/2017. The Respondent failed to pay as agreed on demand and is in breach of contract with the said New Day Ltd and the supplier assigned all rights in the said debt to Cabot Financial UK Ltd on 19/04/2017 and the Claimants have advised Respondent of the same. The last payment to the account was 02/02/2017. The said sum of £1778.81 is the sum sued for. The Claimants have made frequent requests to the Respondent to make payment of the said sum but the Respondent had refused or delayed to do so. Last Date Of Service:- 09/01/2019 Last Date For Response:- 30/01/2019 What Documents are listed in Box E2: Simply states No Defence – No evidence required No stateable Defence (Rule 4.4 breach) – no evidence required Defence on Prescription – Copy statement of account only. (Agreement must be admitted to plead prescription. So agreement not required) Is the claim for a Overdraft, credit card, loan account, hp Agreement, Catalogue or mobile phone debt : - Credit card BOX D5 what has the claimant state: The Claimants request that the court order the respondant to pay the sum of .£1778.81 from your knowledge: answer the following: When did you enter into the original agreement before or after 2007? After Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser - Cabot Were you aware the account had been assigned – did you receive a Notice of Assignment? Not sure Did you receive a Default Notice from the original creditor? I think so Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Don't think so When was you last payment:- 02/02/2017 (according to the form) Hi All, Looking for some guidance and advice please, if possible. Around 5 years ago I took out an Aqua Credit card. Unfortunately, I was unable to keep up the payments and defaulted. The account was sold on to Cabot Financial, and as a result I received a number of letters from a law firm called Nolans (which I ignored) I have now received a Simple Procedure Notice of Claim. Any advice gratefully received. Many thanks, Pete

Name the issuing court: Glasgow Sheriff Court Who Is The Claimant: Cabot Financial UK limited Who Are the Solicitors: Nolans What type of action? Simple What is the claim for – On 14/10/2013 the Respondent entered a credit card agreement with New Day Ltd under which the Respondent borrowed money from them repayable on demand. The said agreement was an agreement under the Consumer Credit Act 1974. The date of termination was 31/03/2017. The Respondent failed to pay as agreed on demand and is in breach of contract with the said New Day Ltd and the supplier assigned all rights in the said debt to Cabot Financial UK Ltd on 19/04/2017 and the Claimants have advised Respondent of the same. The last payment to the account was 02/02/2017. The said sum of £1778.81 is the sum sued for. The Claimants have made frequent requests to the Respondent to make payment of the said sum but the Respondent had refused or delayed to do so. Last Date Of Service:- 09/01/2019 Last Date For Response:- 30/01/2019 What Documents are listed in Box E2: Simply states No Defence – No evidence required No stateable Defence (Rule 4.4 breach) – no evidence required Defence on Prescription – Copy statement of account only. (Agreement must be admitted to plead prescription. So agreement not required) Is the claim for a Overdraft, credit card, loan account, hp Agreement, Catalogue or mobile phone debt : - Credit card BOX D5 what has the claimant state: The Claimants request that the court order the respondant to pay the sum of .£1778.81 from your knowledge: answer the following: When did you enter into the original agreement before or after 2007? After Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser - Cabot Were you aware the account had been assigned – did you receive a Notice of Assignment? Not sure Did you receive a Default Notice from the original creditor? I think so Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Don't think so When was you last payment:- 02/02/2017 (according to the form) Hi All, Looking for some guidance and advice please, if possible. Around 5 years ago I took out an Aqua Credit card. Unfortunately, I was unable to keep up the payments and defaulted. The account was sold on to Cabot Financial, and as a result I received a number of letters from a law firm called Nolans (which I ignored) I have now received a Simple Procedure Notice of Claim. Any advice gratefully received. Many thanks, Pete -

I had a new boiler fitted by a shade greener on 16/12/14 when i say fitted it was a very windy day when it was fitted and they left a Couple of jobs to finish of like fitting the weatherseal to the flue and clearing all the brick dust they had covered everything in my attic with' these jobs i was told would be done the next day but they were not Finally after many facebook messages and phonecalls a fitter was sent to return on his way home from work when it was dark he refused to go up the ladders as it was dark and there was nobody to foot the ladders and he only had the bottom half of a henry hoover and a brush which he said himself would not sort the job out He never came back despite many phonecalls to Everlasting boilers Just after Xmas my boiler broke down I rang the 24 hour helpline to be told somebody would ring me back to sort the problem out 48 hours later still no phonecall i rang up another gas fitter who asked me for the error code and told me to turn the boiler off and then back on again to sort the problem out - This fixed it it would appear that I was forgotton about for both the finishing off work AND the clean up work and also the "24 hour care" this was the case until about 2 weeks ago when some jumped up git rang my mobile and told me i had to pay or they would come rip the boiler out I told them that i wanted the unfinished work completed before I agreed to start paying for it but his answer was "see you in court"! Today a county court summons has appeared for the grand total of £5170.52 for the boiler I have no issues with paying for it BUT the agreement says payments start after the work has been completed but it still hant been completed so where do i stand please Thanks in advance

I had a new boiler fitted by a shade greener on 16/12/14 when i say fitted it was a very windy day when it was fitted and they left a Couple of jobs to finish of like fitting the weatherseal to the flue and clearing all the brick dust they had covered everything in my attic with' these jobs i was told would be done the next day but they were not Finally after many facebook messages and phonecalls a fitter was sent to return on his way home from work when it was dark he refused to go up the ladders as it was dark and there was nobody to foot the ladders and he only had the bottom half of a henry hoover and a brush which he said himself would not sort the job out He never came back despite many phonecalls to Everlasting boilers Just after Xmas my boiler broke down I rang the 24 hour helpline to be told somebody would ring me back to sort the problem out 48 hours later still no phonecall i rang up another gas fitter who asked me for the error code and told me to turn the boiler off and then back on again to sort the problem out - This fixed it it would appear that I was forgotton about for both the finishing off work AND the clean up work and also the "24 hour care" this was the case until about 2 weeks ago when some jumped up git rang my mobile and told me i had to pay or they would come rip the boiler out I told them that i wanted the unfinished work completed before I agreed to start paying for it but his answer was "see you in court"! Today a county court summons has appeared for the grand total of £5170.52 for the boiler I have no issues with paying for it BUT the agreement says payments start after the work has been completed but it still hant been completed so where do i stand please Thanks in advance -

I'm posting this on behalf of an elderly gentleman who has absolutely no computer skills. In March he received a Parking fine from Premier Park for 15mins in a local carpark. He swears the machine wasn't working on the day but has no independent witnesses. He spent 15mins looking at the instructions including when he went out of the carpark to see where the nearest phone box was. when he realised it was too far he came back and drove out. I'll attach the correspondence to this post. I helped him draft letters based on forums we'd looked at. Premier Park were useless to say the least. Unfortunately he didn't get his POPLA appeal in in time (i.e. by a few days and although POPLA state appeals might be submitted late, they don't make it easy), and there is a letter attached showing how they were less than useless with this also. We are now at the County Court stage. Is it worth fighting it further or just paying the £235? 1. the claim has been filed in Exeter and the gentleman has a heart condition so cannot travel that far, his nearest court is in Liverpool. he was served on the 3rd. does the 14days mean he can apply to change courts. 2. Is it possible to have the charge reduced? the first time Premier Park even mention checking the machine to see if it works is the their court statement, if he'd known before maybe he might have thought there was an issue with the coin and paid the original £60/£100. He's still adamant it wasn't working. 3. I didn't include the POPLA complaint form as it's the same as the original letter. Thanks in advance Popla complaint redacted 15:6.pdf Popla complaint ADR redacted 18:7.pdf Premier Park Case.pdf

I'm posting this on behalf of an elderly gentleman who has absolutely no computer skills. In March he received a Parking fine from Premier Park for 15mins in a local carpark. He swears the machine wasn't working on the day but has no independent witnesses. He spent 15mins looking at the instructions including when he went out of the carpark to see where the nearest phone box was. when he realised it was too far he came back and drove out. I'll attach the correspondence to this post. I helped him draft letters based on forums we'd looked at. Premier Park were useless to say the least. Unfortunately he didn't get his POPLA appeal in in time (i.e. by a few days and although POPLA state appeals might be submitted late, they don't make it easy), and there is a letter attached showing how they were less than useless with this also. We are now at the County Court stage. Is it worth fighting it further or just paying the £235? 1. the claim has been filed in Exeter and the gentleman has a heart condition so cannot travel that far, his nearest court is in Liverpool. he was served on the 3rd. does the 14days mean he can apply to change courts. 2. Is it possible to have the charge reduced? the first time Premier Park even mention checking the machine to see if it works is the their court statement, if he'd known before maybe he might have thought there was an issue with the coin and paid the original £60/£100. He's still adamant it wasn't working. 3. I didn't include the POPLA complaint form as it's the same as the original letter. Thanks in advance Popla complaint redacted 15:6.pdf Popla complaint ADR redacted 18:7.pdf Premier Park Case.pdf -

Today I checked my credit file for the sheer hell of it. Personally I'm not bothered what it says as I don't borrow money. Made those mistakes years ago and now my file is at zero. However what I did find was a CCJ for £280 issued last October. Whoever the claimant was didn't write to me at my current address despite being on the electoral register and not at my previous one. They sneakily wrote to the old address so as to win by default. I have a very good idea who this, but it doesn't show on my credit file, just a claim number. I am guessing here but I think it may be a debt collector who has been harassing me for years over this alleged debt It was to Orange for a mobile contract which I had never has. ( I was the victim of ID fraud and they did other things too ). Despite many, many letters asking them for proof like the Deed of Assignment, Deed of Novation and a contract that proves I am the debtor and responsible, they have ignored me. To then sue me using an old address when they only wrote again only yesterday to my current one, I find this extremely bad practice that flies in the face of all the guidelines on debt collections. This is just spite of their behalf, nothing more. Today I wrote to that Mickey Mouse court called Northampton business centre where no judge ever sets foot and asked for the judgement to be set aside as I have not been notified and I have been denied my right to defend myself. Also I issued a counterclaim for a considerable sum as set down by a judge in a similar situation where PC World sued a man over a computer and filed an inaccurate and untruth report on his credit file. Now what will happen? Will my set aside be successful as it really is a bit cheeky to sue somebody deliberately using an old address so that you win by default. This smacks of a certain debt collector who we are all familiar with on this forum.

Today I checked my credit file for the sheer hell of it. Personally I'm not bothered what it says as I don't borrow money. Made those mistakes years ago and now my file is at zero. However what I did find was a CCJ for £280 issued last October. Whoever the claimant was didn't write to me at my current address despite being on the electoral register and not at my previous one. They sneakily wrote to the old address so as to win by default. I have a very good idea who this, but it doesn't show on my credit file, just a claim number. I am guessing here but I think it may be a debt collector who has been harassing me for years over this alleged debt It was to Orange for a mobile contract which I had never has. ( I was the victim of ID fraud and they did other things too ). Despite many, many letters asking them for proof like the Deed of Assignment, Deed of Novation and a contract that proves I am the debtor and responsible, they have ignored me. To then sue me using an old address when they only wrote again only yesterday to my current one, I find this extremely bad practice that flies in the face of all the guidelines on debt collections. This is just spite of their behalf, nothing more. Today I wrote to that Mickey Mouse court called Northampton business centre where no judge ever sets foot and asked for the judgement to be set aside as I have not been notified and I have been denied my right to defend myself. Also I issued a counterclaim for a considerable sum as set down by a judge in a similar situation where PC World sued a man over a computer and filed an inaccurate and untruth report on his credit file. Now what will happen? Will my set aside be successful as it really is a bit cheeky to sue somebody deliberately using an old address so that you win by default. This smacks of a certain debt collector who we are all familiar with on this forum. -

Hi Folks, Been disputing a debt with Cabot for some time and eventually it has been issued as a claim to which I have responded as per the guidance in the forum. Very helpful thank you. So back in December 2018 I filled out my AOC and then 31CPR and then my Defence. Today I received a letter from Cabot chasing the debt asking me to pay, are they allowed to send me a letter to collect when it has now been escalated to a court case? Where do I stand? Any thoughts, guidance, greatly and warmly received. Thanks.

-

Dear CAG Restons have written to me: That they have been instructed to review my payment plan. That I should provide my financial information and breakdown again. That they want to determine if the payment arrangement I have with them is affordable. Please advise, if I am correct in understanding: a. I am required to remain compliant to the actual order by the court. (in the court order it states, "the claimant had objected to the rate of payment you have offered. The court has therefore decided at the rate which you should pay.") This is via monthly instalments of £5/month until the debt is settled. b. That I do not have an "arrangement" so to speak, with Restons. I have an order from the court. The background information is self-explanatory in the reply I have sent to them, as copied below. Dear Sir/ Madam Your ref: xxxxx Amount claimed: £15541.85 Letter dated xx March 2017 by Miss H xxx Further to your letter as attached: 1. Please note that my understanding is that you had obtained a CCJ and the court had ordered, directing me to pay £5 a month until this debt is settled. 2. This was ordered at CC Business Centre, Northampton on the x of Feb 2016, for a total sum of £15541.85 including interest and court costs, owed to your clients. 3. I have attached the copy of the order for ease of reference. The claim no. is xxxxxx 4. Yourselves had further obtained a charging order against my home which I had not contested. This is dated x April 2016. (I do not have or own any other properties.) 5. I have remained compliant to, as directed by the court and I understand, that the onus is on me to continue to make the payments at £5 per month. 6. Please explain, why the outstanding balance is shown to be greater than that on the court order. I have made payments to cover the payment due date, of the 28 of Feb 2017 (13 payments x £5 = £65), prior to when you have written to me, with £15709.41 as the balance amount in your letter dated the 10th of March 2017. I am not in agreement with the outstanding sum you state. 7. Please also note this as a formal complaint. In your letter dated 10 March 2017, you have stated and informing me about legal/recovery actions, even though I have remained compliant with the court order. This has caused me a lot of distress and is now affecting my health to an extent, that I am having sleepless nights. I have experienced extreme anxiety. I have tried to call Miss H xxxxx who is named on this letter, numerous times on the telephone number 01925426100 and have also left a message to return my call, but to no avail. 8. I will continue to make the monthly payments of £5. 9. Ref offer of a discounted settlement: a. Further to your second letter dated the 13th of March, 2017, with a discount of 20% available to me, against the outstanding sum, via three equal monthly instalments of £4089.30, please be advised, that I am unable to take up this offer. b. However, if you were to accept a sum of £1555 to settle and close this account, I may be able to get some help from a relative abroad. I may be able to make this payment before the end of April 2017. I shall await your confirmation on this. c. Another debt collection agency had offered to me a discounted settlement, in February 2017 for £400 against an actual balance of £4000. I did manage to settle this account with a plea to reduce my associated stress and burden, to a relative abroad. I can attempt to do the same, for a sum of £1555 to settle the account with MFS portfolio, if you were to advise so. Please note that there will not be a time limit for I to repay such a cash advance to me. Therefore, it will not add to my current level of stress. Your Sincerely

Dear CAG Restons have written to me: That they have been instructed to review my payment plan. That I should provide my financial information and breakdown again. That they want to determine if the payment arrangement I have with them is affordable. Please advise, if I am correct in understanding: a. I am required to remain compliant to the actual order by the court. (in the court order it states, "the claimant had objected to the rate of payment you have offered. The court has therefore decided at the rate which you should pay.") This is via monthly instalments of £5/month until the debt is settled. b. That I do not have an "arrangement" so to speak, with Restons. I have an order from the court. The background information is self-explanatory in the reply I have sent to them, as copied below. Dear Sir/ Madam Your ref: xxxxx Amount claimed: £15541.85 Letter dated xx March 2017 by Miss H xxx Further to your letter as attached: 1. Please note that my understanding is that you had obtained a CCJ and the court had ordered, directing me to pay £5 a month until this debt is settled. 2. This was ordered at CC Business Centre, Northampton on the x of Feb 2016, for a total sum of £15541.85 including interest and court costs, owed to your clients. 3. I have attached the copy of the order for ease of reference. The claim no. is xxxxxx 4. Yourselves had further obtained a charging order against my home which I had not contested. This is dated x April 2016. (I do not have or own any other properties.) 5. I have remained compliant to, as directed by the court and I understand, that the onus is on me to continue to make the payments at £5 per month. 6. Please explain, why the outstanding balance is shown to be greater than that on the court order. I have made payments to cover the payment due date, of the 28 of Feb 2017 (13 payments x £5 = £65), prior to when you have written to me, with £15709.41 as the balance amount in your letter dated the 10th of March 2017. I am not in agreement with the outstanding sum you state. 7. Please also note this as a formal complaint. In your letter dated 10 March 2017, you have stated and informing me about legal/recovery actions, even though I have remained compliant with the court order. This has caused me a lot of distress and is now affecting my health to an extent, that I am having sleepless nights. I have experienced extreme anxiety. I have tried to call Miss H xxxxx who is named on this letter, numerous times on the telephone number 01925426100 and have also left a message to return my call, but to no avail. 8. I will continue to make the monthly payments of £5. 9. Ref offer of a discounted settlement: a. Further to your second letter dated the 13th of March, 2017, with a discount of 20% available to me, against the outstanding sum, via three equal monthly instalments of £4089.30, please be advised, that I am unable to take up this offer. b. However, if you were to accept a sum of £1555 to settle and close this account, I may be able to get some help from a relative abroad. I may be able to make this payment before the end of April 2017. I shall await your confirmation on this. c. Another debt collection agency had offered to me a discounted settlement, in February 2017 for £400 against an actual balance of £4000. I did manage to settle this account with a plea to reduce my associated stress and burden, to a relative abroad. I can attempt to do the same, for a sum of £1555 to settle the account with MFS portfolio, if you were to advise so. Please note that there will not be a time limit for I to repay such a cash advance to me. Therefore, it will not add to my current level of stress. Your Sincerely -

Hi, just had this arrive over the weekend In order for us to help you we require the following information:- Name of the Claimant ? Hoist Finance UK Holdings Date of issue – 19th Feb 2019 Particulars of Claim 1. The claim is for the sum of £5xxx.xx in respect of monies owing under an agreement with the account number: 12345 pursuant to the consumer credit act 1974 (CCA). 2.The debt was legally assigned by Hoist Portfolio Holding (EX Aqua) to the claimant and notice has been served. 3.The defendant has failed to make contractual payments under the terms of the agreement. A default notice has been served upon the defendant pursuant to s.87(1) CCA The claimant claims 1. The sum of £5xxx.xx 2. costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ? No Have you changed your address since the time at which the debt referred to in the claim was allegedly incurred? No Did you inform the claimant of your change of address? N/A What is the total value of the claim? £5xxx.xx Is the claim for - a Bank Account (Overdraft) or credit card or loan or catalogue or mobile phone account? Credit Card When did you enter into the original agreement before or after April 2007 ? After Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ? Yes Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Not sure Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure Why did you cease payments? Down turn in business What was the date of your last payment? Mid 2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Was in DMP but had trouble with them. Thanks

-

Hi all, I received a County Court Claim (Northampton) 4 days ago for a couple of pre-1998 student loans that I'd successfully deferred until 2013 . My account was not in default at the time, but when Erudio took over, I decided to ignore their deferral form because of all the personal info they were demanding, and later because of all the stories I heard about their dodgy practices. long story short, I've never replied to any of their correspondence, but unfortunately I ignored a PAP from Drydens recently, and now I have a County Claim form. My address hasn't changed, but I'm guessing that they're going for a default judgement as I've never sent them anything. I intend to defend the claim, but not sure whether my ignoring their letters previously will look bad if it goes to court? Many thanks in advance for any help on this matter.

Hi all, I received a County Court Claim (Northampton) 4 days ago for a couple of pre-1998 student loans that I'd successfully deferred until 2013 . My account was not in default at the time, but when Erudio took over, I decided to ignore their deferral form because of all the personal info they were demanding, and later because of all the stories I heard about their dodgy practices. long story short, I've never replied to any of their correspondence, but unfortunately I ignored a PAP from Drydens recently, and now I have a County Claim form. My address hasn't changed, but I'm guessing that they're going for a default judgement as I've never sent them anything. I intend to defend the claim, but not sure whether my ignoring their letters previously will look bad if it goes to court? Many thanks in advance for any help on this matter. -

Guys, I am about to send defence to Northampton County Court, please I need your help. Claim issued 14/09/18, received it on 18/09/18 and acknowledged it same day on 18/09/18. I think I have till wed 17/10/18 to file my defence? Please correct me if I'm wrong. Claim is about HBOS overdraft of current account I held since 2003, I believe it's status barred judging from when it was closed... od fees was up to 100 pounds I couldn't maintain payment. I held 2 overdrawn current account but upon challenging for second account they recently sent me letter stating account closed balance is zero. If I had challenged Lowell for the one they raised claim for maybe they'd dropped it as well. But i didn't I just bin their letters as believe it's statute barred. Other points: 1, Account number they've been quoting is wrong 2, Despite signing for it and cashing statutory 1 pound, they have not responded to all my signed for letters dated 21/22 sept 18 : CCA, Cpr 31.14, etc. SAR to HBOS no reply yet many thanks for any help in advance

-

hello everyone. just started this thread for a colleague, who needs some advice and is not very good with computers. history of debt Barclaycard credit card 01/2008 debt management 08/2009 arranged with Barclays a reduced payment plan which was accepted while on the debt management plan. PRA GROUP was assigned the debt from Barclaycard 08/2015 Last payment made 02/2018 Name of the Claimant ? PRA Group Date of issue 17/01/2019 What is the claim for – 1.The claimant claims the sum of £1834.29 for an outstanding debt owed. 2.On 22.01.2008 the defendant entered into a an agreement with Barclays Bank PLC for a credit card under reference ….. 3.On the 06/2018 the defendant defaulted on the agreement with an outstanding balance of £2019.29. 4.On 17/08/2015 the debt of £2301.02 was assigned to PRA Group(UK) Ltd. Notices of assignment were sent to the defendant in accordance with S136 law of property act 1925. Payments of £434.52 were received up to 06/06/2018 and adjustments have been applied in the sum of £32.21. 5.AND THE CLAIMANT CLAIMS 1. The sum of £1834.29 A Barclaycard CC debt £1834.29 + court costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (pre action protocol) ?Yes What is the total value of the claim? £2019.29 what is the claim for:Barclaycard credit card When did you enter into the original agreement before or after April 2007 ? 01/2008 Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ?NO Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim.Debt purchaser PRA Were you aware the account had been assigned – did you receive a Notice of Assignment? I don't remember receiving this information Did you receive a Default Notice from the original creditor? No, after ringing Barclaycard they claim that the account was never defaulted. Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Just letters from PRA stating you are behind with your payments Why did you cease payments? Got into financial difficulties What was the date of your last payment?06/02/2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes I was on a debt management plan He has done the AOS on MCOL. CCA request ready to send to claimants CPR.31.14 ready to send to claimants solicitors Any help and advice appreciated. Donation will be made thank you

-

I received a court claim form on the 7/11/18 (issue date 5/11/18) for unpaid water charges amount totaling £5,095 for the period 1/4/2007 to 31/3/2019 I have lived at the property for longer but never actually paid anything for water rates, due to being unemployed and not being to afford it. have been i receipt of yearly water bills and various uk search limited letters for amount owing. recently shulmans got involved and sent a few letters before court action. all of which i have ignored due to large debt amount. I have rung up northampton county court to verify if the claim form was send by them. they acknowledged the letter and told me the service date is 10/11/2018. Any advice on how to proceed would be very much appreciated as i'm unsure of what i can do and how to go about it. I rang southern water yesterday and enquired to my account and was told it had gone over to their litigation team. I have not rung their litigation team as of yet as i dont want to say the wrong thing. Thank you in advance for any help offered

-

Hi there, Is there anyone out there who can help me? We have a former GMAC mortgage that went over to mortgage Express. We were keeping up with the mortgage until I finally succumbed to my illness and disability. We are currently five months in arrears which works out to be £4250. I was working part time and my wife was working full time and up to earlier in the year keeping up with our mortgage. We thought we had sorted ourselves out with my working part time and my wife getting a full time job a while ago. I had an operation several years ago, that resulted in damage to my spine, this means I take 35 tablets a day, and have fentanyl (type of morphine) patches, oramorph (another type of morphine). I am stuck in a wheelchair now, I am typing from a special bed installed in our bedroom that is like a hospital bed. All this means I cannot really work a lot now. I am waiting for the first of five operations at the start of August so will be out of any sort of working fulltime loop for a few years. I will be able to work part time and an employer is willing to let me do this fitting around all my issues. My wife works fulltime, but had to take a few months off without pay due my being in and out of hospital. overall a loss of income. We have managed to stabilise our position, but need to sort out the mortgage arrears. We were in arrears a few years ago with MX and it was hell. Four of five phone calls a day, refusal to accept a deal, threats of a home visit etc. we changed our phone number, managed to pay off the debt and were debt free for three years. How can I write a letter offering an extra £150.00 a month, which we can pay and try to forestall any action? We had a knock at the door which was out of the blue. It was an advisor and valuer from them. We told him to go away, we were only going to deal with Mortgage Express in writing as our last experience told us they bullied on the phone, never agreed a deal, and kept on phoning us. Despite our telling him to go away, he came back four times, each time was when our neighbours were coming home from work. He would stand outside the house and with a raised voice tell us he was there to deal with our mortgage arrears. our neighbours know our business. Can someone point me towards a letter template our help me out with one to send them as soon as possible? I just want to stop and action which the valuer told us they would do, that being taking us to court for repossession. I know the court might end up giving possession and then stay it, but it is a worry I could do without. I get full DLA, I am as previously stated in a wheelchair. I have four outpatient’s appointments a week, which I know is not MX’s fault, but being thrown out of the house will result in my ending up in hospital. Please help.

Hi there, Is there anyone out there who can help me? We have a former GMAC mortgage that went over to mortgage Express. We were keeping up with the mortgage until I finally succumbed to my illness and disability. We are currently five months in arrears which works out to be £4250. I was working part time and my wife was working full time and up to earlier in the year keeping up with our mortgage. We thought we had sorted ourselves out with my working part time and my wife getting a full time job a while ago. I had an operation several years ago, that resulted in damage to my spine, this means I take 35 tablets a day, and have fentanyl (type of morphine) patches, oramorph (another type of morphine). I am stuck in a wheelchair now, I am typing from a special bed installed in our bedroom that is like a hospital bed. All this means I cannot really work a lot now. I am waiting for the first of five operations at the start of August so will be out of any sort of working fulltime loop for a few years. I will be able to work part time and an employer is willing to let me do this fitting around all my issues. My wife works fulltime, but had to take a few months off without pay due my being in and out of hospital. overall a loss of income. We have managed to stabilise our position, but need to sort out the mortgage arrears. We were in arrears a few years ago with MX and it was hell. Four of five phone calls a day, refusal to accept a deal, threats of a home visit etc. we changed our phone number, managed to pay off the debt and were debt free for three years. How can I write a letter offering an extra £150.00 a month, which we can pay and try to forestall any action? We had a knock at the door which was out of the blue. It was an advisor and valuer from them. We told him to go away, we were only going to deal with Mortgage Express in writing as our last experience told us they bullied on the phone, never agreed a deal, and kept on phoning us. Despite our telling him to go away, he came back four times, each time was when our neighbours were coming home from work. He would stand outside the house and with a raised voice tell us he was there to deal with our mortgage arrears. our neighbours know our business. Can someone point me towards a letter template our help me out with one to send them as soon as possible? I just want to stop and action which the valuer told us they would do, that being taking us to court for repossession. I know the court might end up giving possession and then stay it, but it is a worry I could do without. I get full DLA, I am as previously stated in a wheelchair. I have four outpatient’s appointments a week, which I know is not MX’s fault, but being thrown out of the house will result in my ending up in hospital. Please help. -

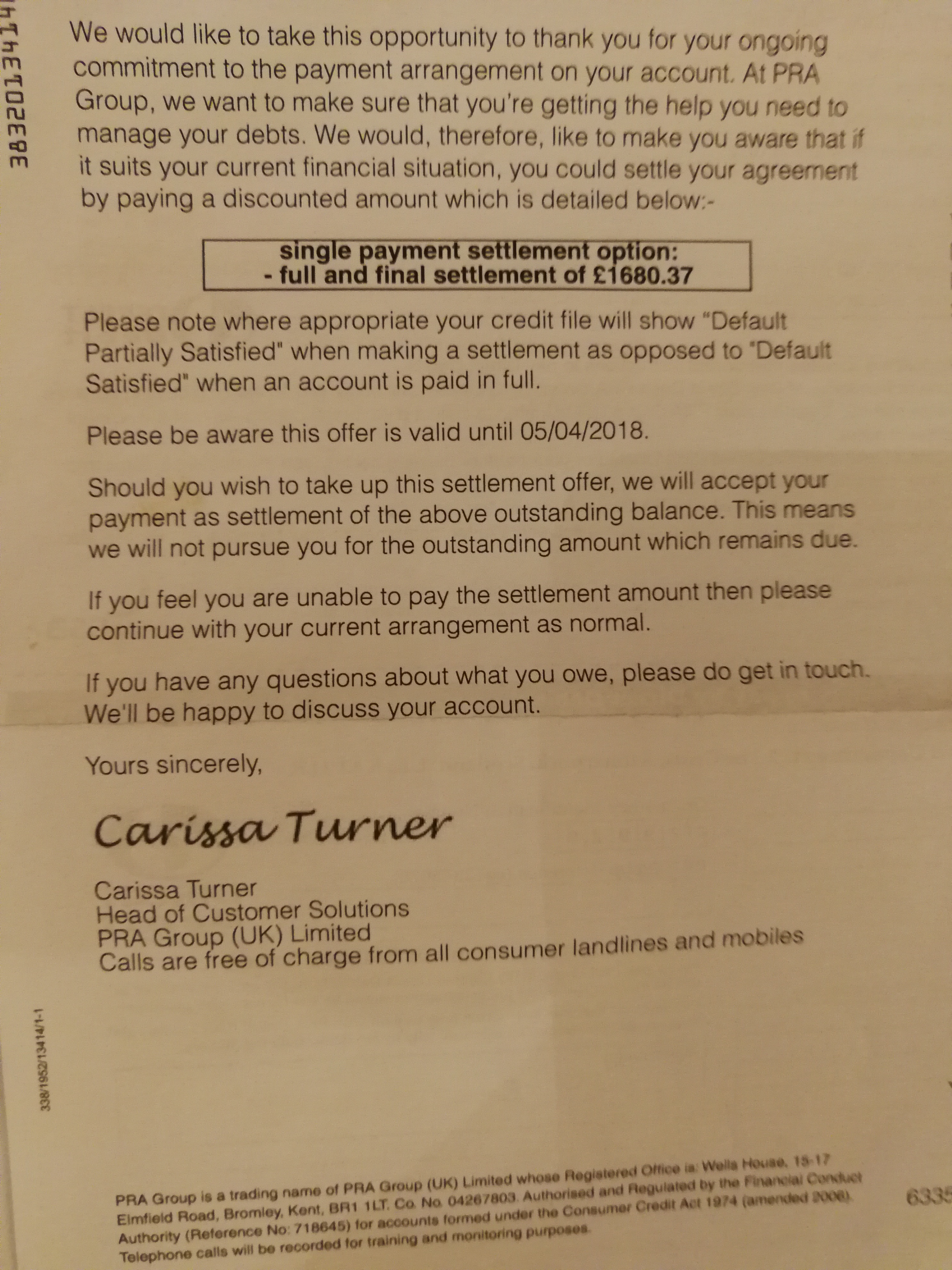

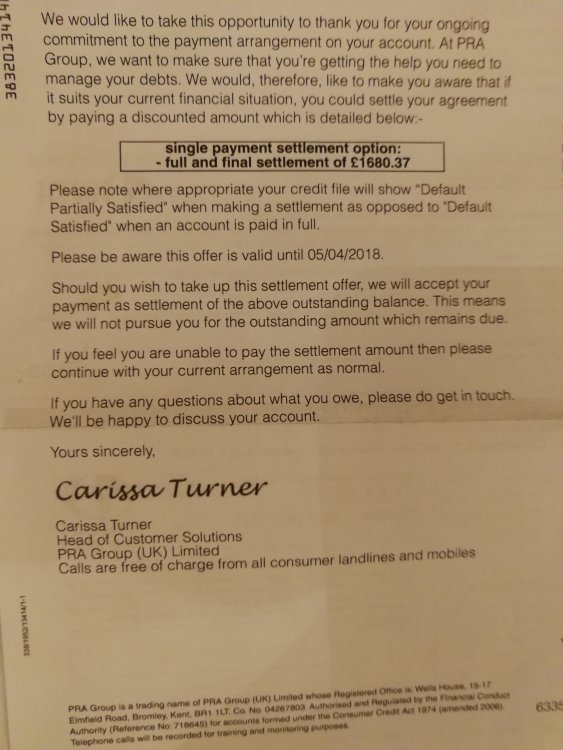

Name of the Claimant ? PRA Group Date of issue 19/12/2018 What is the claim for – 1.The claimant claims the sum of £4793.79 for an outstanding debt owed. 2.On 20.01.2005 the defendant entered into a an agreement with Barclays Bank PLC for a credit card under reference ….. 3.On the 06/05/2011 the defendant defaulted on the agreement with an outstanding balance of £5041.31. 4.On 17/08/2015 the debt of £5041.31 was assigned to PRA Group(UK) Ltd. Notices of assignment were sent to the defendant in accordance with S136 law of property act 1925. Payments of £232.96 were received up to 20/03/20108 and adjustments have been applied in the sum of £14.56. 5.AND THE CLAIMANT CLAIMS 1. The sum of £4793.79 An Egg CC debt £4793.79 + court costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ?Yes What is the total value of the claim? £5058.79 what is the claim for: egg credit card When did you enter into the original agreement before or after April 2007 ? 2005 should I request the CCA I believe they won't have a problem proofing I owe this debt? Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ?No it came off about a year ago Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim.Debt purchaser PRA Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes sure I did ! Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure Why did you cease payments? Had a brain injury What was the date of your last payment?19/12/2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes How shall I defend / respond to this they seem to be using bully tactics and fishing for me to pay up the full amount which I don't have. in March last year they sent me a full and final settlement letter asking for £1680.37 I counter offered £1200 they refused it and said they would only take £1945 which is bizarre. PLEASE SEE ATTACHMENT, I questioned this on another forum and was told the wording is not right and the balance should be zero. If you have not already done so – send a CCA Request to the claimant for a copy of your agreement (except for Overdraft/ Mobile/Telephone accounts) Will Do ! Particulars of Claim An Egg CC debt £4793.79 + court costs I went into arrears in 2010 after a head injury and have been making monthly payments. Egg was bought by Barclaycard since then and then they assigned/sold the debt to the PRA group 17/08/2015. I have been paying without missing a payment but have not done their constant requests for income and expenditure. I got a letter November 13th say my account had been transferred to the investigations and litigation department which I ignored. Thanks for your help I don't have long to respond to this claim

Name of the Claimant ? PRA Group Date of issue 19/12/2018 What is the claim for – 1.The claimant claims the sum of £4793.79 for an outstanding debt owed. 2.On 20.01.2005 the defendant entered into a an agreement with Barclays Bank PLC for a credit card under reference ….. 3.On the 06/05/2011 the defendant defaulted on the agreement with an outstanding balance of £5041.31. 4.On 17/08/2015 the debt of £5041.31 was assigned to PRA Group(UK) Ltd. Notices of assignment were sent to the defendant in accordance with S136 law of property act 1925. Payments of £232.96 were received up to 20/03/20108 and adjustments have been applied in the sum of £14.56. 5.AND THE CLAIMANT CLAIMS 1. The sum of £4793.79 An Egg CC debt £4793.79 + court costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ?Yes What is the total value of the claim? £5058.79 what is the claim for: egg credit card When did you enter into the original agreement before or after April 2007 ? 2005 should I request the CCA I believe they won't have a problem proofing I owe this debt? Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ?No it came off about a year ago Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim.Debt purchaser PRA Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes sure I did ! Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure Why did you cease payments? Had a brain injury What was the date of your last payment?19/12/2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes How shall I defend / respond to this they seem to be using bully tactics and fishing for me to pay up the full amount which I don't have. in March last year they sent me a full and final settlement letter asking for £1680.37 I counter offered £1200 they refused it and said they would only take £1945 which is bizarre. PLEASE SEE ATTACHMENT, I questioned this on another forum and was told the wording is not right and the balance should be zero. If you have not already done so – send a CCA Request to the claimant for a copy of your agreement (except for Overdraft/ Mobile/Telephone accounts) Will Do ! Particulars of Claim An Egg CC debt £4793.79 + court costs I went into arrears in 2010 after a head injury and have been making monthly payments. Egg was bought by Barclaycard since then and then they assigned/sold the debt to the PRA group 17/08/2015. I have been paying without missing a payment but have not done their constant requests for income and expenditure. I got a letter November 13th say my account had been transferred to the investigations and litigation department which I ignored. Thanks for your help I don't have long to respond to this claim

-

Hi I received a county court claim from Lowell Portfoloio on 12th December 2018 regarding a debt with Vodafone, I made AOS on 18th December. POC 1) The defendant entered into an agreement with Vodafone under the account reference ******** ('the Agreement'). 2) The defendant failed to maintain the required payments and the service was terminated. 3) The Agreement was later assigned to the Claimant on 28/02/2018 and notice was given to the Defendant. 4) Despite repeated requests for the payment, the sum of £xxxx remains due and outstanding. And the Claimant claims a) The said sum of £xxxx b) Interest pursuant to s69 county courts Act 1984 at the rate of 8% per annum from the date of assignment to the date of issue, accusing at a daily rate of £0.251, but limited to one year, being £71.76 c) Costs I would really appreciate some advise for the next stage. Many thanks. Roland

-

Hello About 3 years ago I had an issue with my pension provider and as a result placed an SAR with them, however they employed delay tactics and required various forms and ID documents to be completed. I know I should have done but never pursued the request. However under the new GDPR I submitted another SAR on the 30 May, recorded mail and signed for by them. They never acknowledged my request and never acknowledged a reminder I sent to them. Needless to say they have not complied. I intend to issue a claim in the County Court as well as reporting them to the ICO. I have issued a LBA informing them I will start proceedings after the 14 days of the date of my LBA and at the same time report them to the ICO. Question is, what will be the nature of the claim, I am not after the £'s, I just want the breach against them to be recorded and I want my personal data from them. Also should I report them to the ICO before pursuing a Court claim?

Hello About 3 years ago I had an issue with my pension provider and as a result placed an SAR with them, however they employed delay tactics and required various forms and ID documents to be completed. I know I should have done but never pursued the request. However under the new GDPR I submitted another SAR on the 30 May, recorded mail and signed for by them. They never acknowledged my request and never acknowledged a reminder I sent to them. Needless to say they have not complied. I intend to issue a claim in the County Court as well as reporting them to the ICO. I have issued a LBA informing them I will start proceedings after the 14 days of the date of my LBA and at the same time report them to the ICO. Question is, what will be the nature of the claim, I am not after the £'s, I just want the breach against them to be recorded and I want my personal data from them. Also should I report them to the ICO before pursuing a Court claim? -

Hi all, Bit of back story to my questions: I'm a director of a webhosting company, and one of our payment processors we use is called Payza, which is similar to Paypal and very useful for people who live in countries not serviced by Paypal. Around about the 21st of March, the U.S. Department of Justice (DoJ) has filed a lawsuit against digital payment processor Payza for allegedly operating an unlicensed money service business that processed more than $250 million in transactions. Now looking at Payza's structure, they operate under several shady layers it seems. The company uses terms such as "servicing" companies, but all are ultimately falling under a UK Ltd company called MH Pillars Ltd. MH Pillars Ltd has had a few address changes recently, but now the latest registered address for them is an accountant's office. I tried to withdraw funds from our "ewallet" on the 21st of March, and a few small transactions went through, now I have nearly £5000 still stuck in my "ewallet" and the site is not allowing withdrawals. Each day the withdrawal requests remain "Pending" with a due date that just keeps on extending. Their support team no longer respond to emails, and they are not active on their Social Media accounts on Twitter and Facebook anymore. Anyone have suggestions please? What are the merits of sending a LBA to their accountants, and then a county court claim to their accountants as well? Would I just be wasting my money as accountants could just turn around and say nothing to do with us!

-

Papers from SAR shows shockingly very high charges from 2009 to 2013 within period I lost my job and was struggling financially, can I seek refund from OC? Just after calling OC and asking for complaint procedure and address, I received letter stating small % of charges will be refunded but paid directly to Lowell? What's your opinion guys?

- 22 replies

-

- 1

-

-

- county court

- defending

- (and 1 more)

-

Hi guys/gals its been awhile since I posted and needed any help so bare with me. Lowell have bought an old Vanquis debt, I have had loads of letters and ignored them, I haven't had any contact with them on the phone either so I've not acknowledged any thing. On Saturday received court papers, I have registered with money claim AOS as I want to defend. I was told about a 3 letter process to send to Lowells solicitor but don't know what the letters are. Any help greatly appreciated, thanks.

-

Hi everyone, following on from extremely similar cases, i requested documentation for service charges of a flat i own. Accordingly to regulations (Landlord and Tenant Act 1985 Section 21, as amended by the Commonhold and Leasehold Reform Act 2002 Section 152) they should have provided evidence within 21 days. 25 days later they sent me some receipts making up 25% of the charges. I asked them if that was all they had for that financial year and they confirmed this. So I had these checked and found usual irregularities like wrong calculations for shares and of course all the missing receipts and invoices for many of the services allegedly offered. For example, lift maintenance is £1000, divided by 10 flats they make it £15. Clearly wrong to me and you, but of course their calculators seem to consider maths an opinion. They don't dispute that these calculations are wrong, but they simply avoid addressing the problem. I asked for a refund of all undocumented charges and overcharged, same as I did with other financial years which they refunded. As soon as they received this request they sent another 3 receipts totalling £20 approx; this was well after the statutory 21 days. I rejected these receipt and told them that I was not in a position to accept any further documents because they had already confirmed that they didn't have anymore and the 21 days had passed long time ago. So they're now playing the ignore game and, as the 14 days I gave them are up tomorrow, I am drafting a lba. If you are still reading I thank you, I know it's a bit long but I wanted you to have a good picture. I have a feeling that this time I will end up taking them to court, so I don't want to make any mistake. My question is: Accordingly to the pre action protocol I should suggest an alternative dispute resolution service, however I don't want to give them an opportunity to get the Ombudsman involved, knowing that they are useless. Can I avoid mentioning ADR in my lba? If I do, could they claim that I haven't complied to the letter of the pre action protocol? Or by ticking yes to mediation on mcol I should be ok? Thanks for your help.

Hi everyone, following on from extremely similar cases, i requested documentation for service charges of a flat i own. Accordingly to regulations (Landlord and Tenant Act 1985 Section 21, as amended by the Commonhold and Leasehold Reform Act 2002 Section 152) they should have provided evidence within 21 days. 25 days later they sent me some receipts making up 25% of the charges. I asked them if that was all they had for that financial year and they confirmed this. So I had these checked and found usual irregularities like wrong calculations for shares and of course all the missing receipts and invoices for many of the services allegedly offered. For example, lift maintenance is £1000, divided by 10 flats they make it £15. Clearly wrong to me and you, but of course their calculators seem to consider maths an opinion. They don't dispute that these calculations are wrong, but they simply avoid addressing the problem. I asked for a refund of all undocumented charges and overcharged, same as I did with other financial years which they refunded. As soon as they received this request they sent another 3 receipts totalling £20 approx; this was well after the statutory 21 days. I rejected these receipt and told them that I was not in a position to accept any further documents because they had already confirmed that they didn't have anymore and the 21 days had passed long time ago. So they're now playing the ignore game and, as the 14 days I gave them are up tomorrow, I am drafting a lba. If you are still reading I thank you, I know it's a bit long but I wanted you to have a good picture. I have a feeling that this time I will end up taking them to court, so I don't want to make any mistake. My question is: Accordingly to the pre action protocol I should suggest an alternative dispute resolution service, however I don't want to give them an opportunity to get the Ombudsman involved, knowing that they are useless. Can I avoid mentioning ADR in my lba? If I do, could they claim that I haven't complied to the letter of the pre action protocol? Or by ticking yes to mediation on mcol I should be ok? Thanks for your help.