Search the Community

Showing results for tags 'real'.

Found 17 results

-

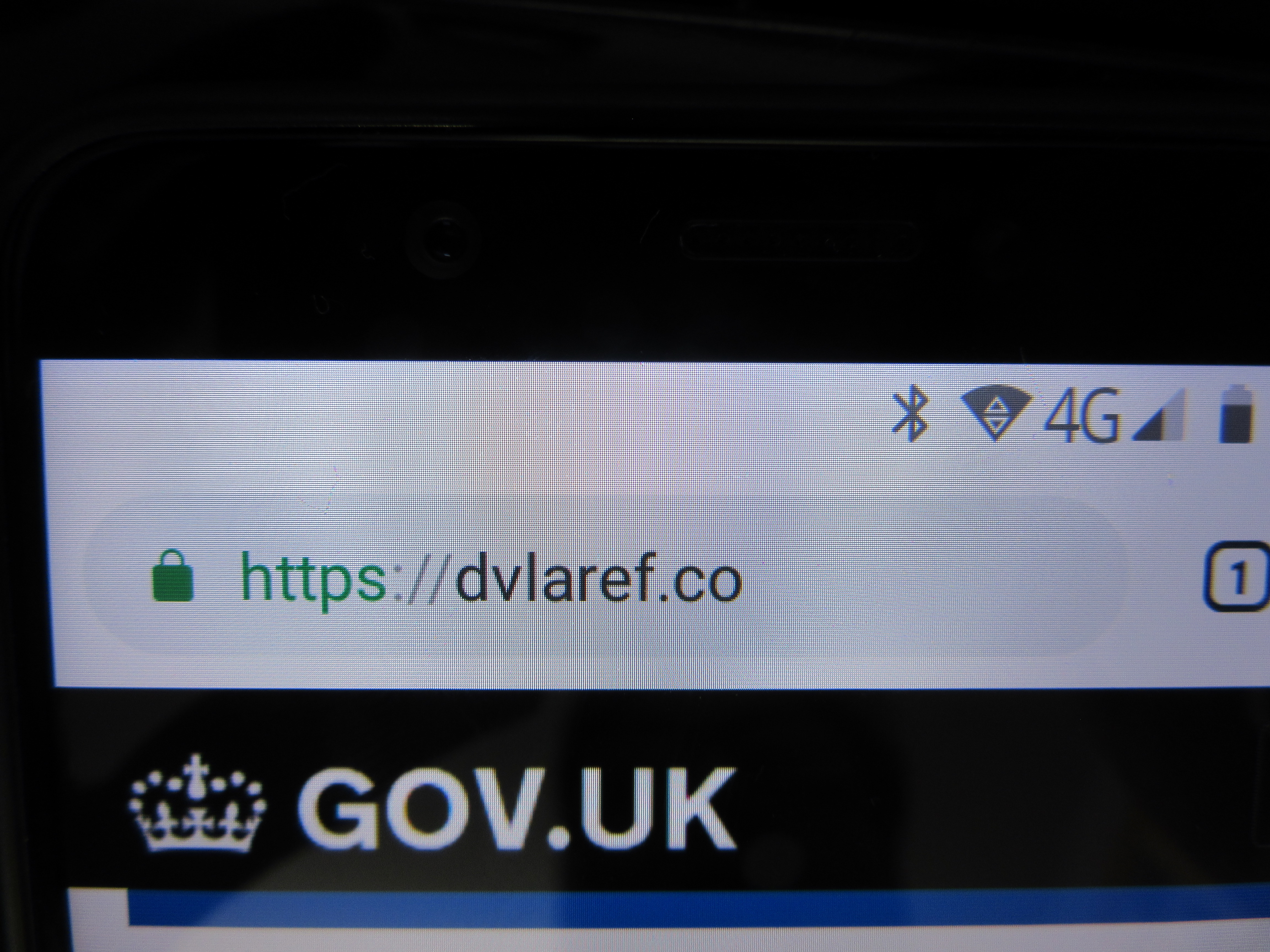

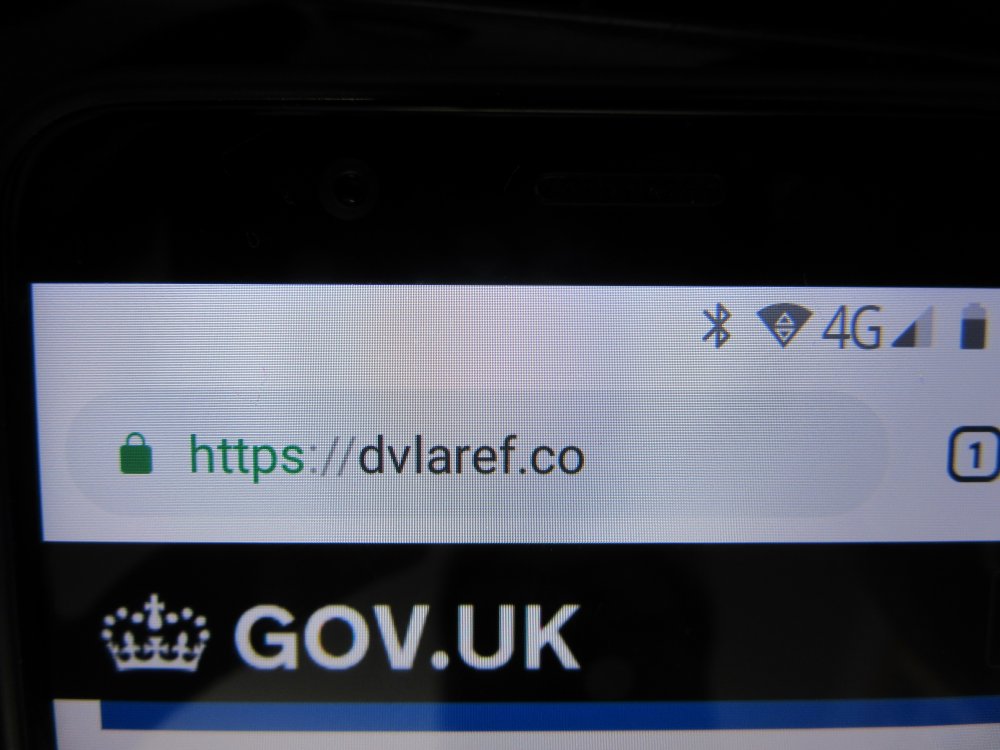

I am due to road tax refund but received this message on my phone. It seems a bit suspect. Has anyone else had this message. Many thanks for any adivce! LT

-

A friend has chosen a business name which someone else claims copyright on: Name Of Business© How can I check if they have the copyright or have just added the © symbol? I Googled it and found a Gov site but that only lets you check TM's.

-

I have an agreement with Jacobs to pay 2016-17 council tax, well I did have until they have demanded the balance with in 7 days. My agreement was for £20 per week, in May 17 I asked to reduce this to £60 and pay monthly. They agreed and confirmed by mail for three months then I would have to pay £80 per month starting in August 17. I have paid may, June, July as agreed but because the July payment was paid in three weekly amounts but the full 60.00 was with them by the agreed date 16th and one extra week towards Augusts payment (my mum actually gave me the money to pay July and the extra 20.00) they sent me letter saying I have broken my weekly arrangement therefore full balance due. I sent three emails which reminded them of the new monthly agreement and payment was not due until 16th August 17, I finally got a response today, which I find quite rude, it states:: ""You did not pay your account as we agreed and you have been making your payments sporadically which we do not allow as we are not able to monitor your case. You have not maintained your original arrangement, nor have you maintained the weekly arrangement which we set to cater for your incoming payments. You are not able to decide when you are paying parts of your arrangement nor are you able to pay £20.00 and then reduce your payment for that month without having this confirmed by a member of our team. If you are having issues you are advised to contact our office before your arrangement defaults and we will look into your account and endeavour to assist you in the best way we can."" IT THEN IGNORES WHAT IS STATED ABOVE AND THE FINAL PARAGRAPH SAYS:: "All of the above is stated in the arrangement terms and conditions which we have provided to you upon setting your arrangement. Unfortunately as your arrangement has defaulted for a third time we have no other option but to insist that your remaining balance of £433.00 is paid in full within the next 7 days, We have attached a list of all of our payment methods for your perusal. I have paid on time I have proof. I have not made the payments as they state apart from the July one which wad sent over in weekly amounts but on time. This agreement has not defaulted previously, I had a previous one that did but that's all paid up. The reply email does not make sense, Can they demand the full balance like this when I have paid what was due. if I wanted to pay an extra amount to reduce the balance, I would have to ask permission first as they state I can't decide when to pay them. surely paying them is the main priority. Please advise me what if any can I do to stop them adding fees and sending their enforcement officer to take goods.

I have an agreement with Jacobs to pay 2016-17 council tax, well I did have until they have demanded the balance with in 7 days. My agreement was for £20 per week, in May 17 I asked to reduce this to £60 and pay monthly. They agreed and confirmed by mail for three months then I would have to pay £80 per month starting in August 17. I have paid may, June, July as agreed but because the July payment was paid in three weekly amounts but the full 60.00 was with them by the agreed date 16th and one extra week towards Augusts payment (my mum actually gave me the money to pay July and the extra 20.00) they sent me letter saying I have broken my weekly arrangement therefore full balance due. I sent three emails which reminded them of the new monthly agreement and payment was not due until 16th August 17, I finally got a response today, which I find quite rude, it states:: ""You did not pay your account as we agreed and you have been making your payments sporadically which we do not allow as we are not able to monitor your case. You have not maintained your original arrangement, nor have you maintained the weekly arrangement which we set to cater for your incoming payments. You are not able to decide when you are paying parts of your arrangement nor are you able to pay £20.00 and then reduce your payment for that month without having this confirmed by a member of our team. If you are having issues you are advised to contact our office before your arrangement defaults and we will look into your account and endeavour to assist you in the best way we can."" IT THEN IGNORES WHAT IS STATED ABOVE AND THE FINAL PARAGRAPH SAYS:: "All of the above is stated in the arrangement terms and conditions which we have provided to you upon setting your arrangement. Unfortunately as your arrangement has defaulted for a third time we have no other option but to insist that your remaining balance of £433.00 is paid in full within the next 7 days, We have attached a list of all of our payment methods for your perusal. I have paid on time I have proof. I have not made the payments as they state apart from the July one which wad sent over in weekly amounts but on time. This agreement has not defaulted previously, I had a previous one that did but that's all paid up. The reply email does not make sense, Can they demand the full balance like this when I have paid what was due. if I wanted to pay an extra amount to reduce the balance, I would have to ask permission first as they state I can't decide when to pay them. surely paying them is the main priority. Please advise me what if any can I do to stop them adding fees and sending their enforcement officer to take goods. -

Summer has arrived and Thunderstorms are around. If you would like to track Storms moving around Great Britain this is for you. You can close into your town see strikes in real time and even time the thunder before it reaches you. As you zoom in, you can even see the strikes in nearby streets. At this moment 03-14am I notice just off the coast of South East of Britain is getting a beating. Anyway the link you will soon get used to it.Just turn the sound on, and as you close in you will see the lightning strikes and track the thunder before it reaches you . Strange things interest this old owl.And what am I doing up this time of day. https://www.lightningmaps.org/?lang=en#y=53.8559;x=-3.0294;z=3;t=2;m=sat;r=0;s=0;o=3;b=0.00;n=0;d=2;dl=2;dc=0;

Summer has arrived and Thunderstorms are around. If you would like to track Storms moving around Great Britain this is for you. You can close into your town see strikes in real time and even time the thunder before it reaches you. As you zoom in, you can even see the strikes in nearby streets. At this moment 03-14am I notice just off the coast of South East of Britain is getting a beating. Anyway the link you will soon get used to it.Just turn the sound on, and as you close in you will see the lightning strikes and track the thunder before it reaches you . Strange things interest this old owl.And what am I doing up this time of day. https://www.lightningmaps.org/?lang=en#y=53.8559;x=-3.0294;z=3;t=2;m=sat;r=0;s=0;o=3;b=0.00;n=0;d=2;dl=2;dc=0; -

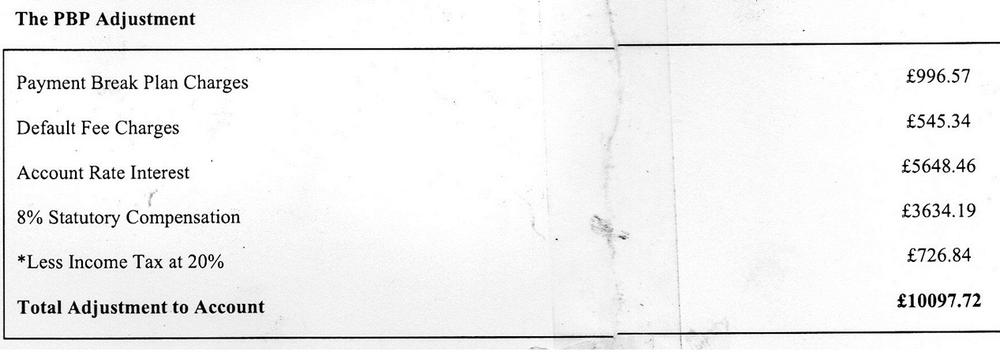

I have received a letter from monument about PBP. It was totally unsolicited, and I have not applied for anything (PPI or the like)or contacted Monument in any way for years. This letter came totally out of the blue and I dismissed it along with all the other letters I have received from them over the years. I ripped it up and put it in the bin. The Short Story My monument account was pulled many years ago , I can't even remember the dates it was so long ago, leaving an unpaid balance of around £3,600 which remained unpaid. The Long Story I have just fished this letter out of the bin as yesterday, I received a cheque in the amount of just over £6,800. The letter I received last week referred to PBP - Payment Break Plan and looks to be a letter of 'without admission of liability'. I have scanned part of this and attached it to this post. It would appear than an adjustment of just over £10,000 has been credited to my account, and the cheque I have received looks to be the difference between the amount of the adjusted credit, and the outstanding balance as mentioned above. I'm just wondering if this is legit or maybe a ruse on the part of Monument to track down their un-paying debtors. I have seen other posts here mentioning refunded PBP - which I never knew I had, but these are dating back to 2014/2015. Obviously we're now at the latter part of 2016, and they 'look' to be still paying out. The letter states they will apply the adjustment values to any outstanding debt from the account, and should this result in your account going into credit, we will issue you a cheque within 28 days - which looks to be the same as others have posted here. I'm not sure whether to put this cheque in the bank or leave it be as I really can't afford to be snared in this way. Any input would be greatly appreciated. Thanks.

-

Hi guys I rang the DWP about a change in my circumstances. The guy on the phone told me I had to send some evidence in but the address he gave me sounded really weird- I wonder if anyone knows if this is right?: FREEPOST DWP ESA 36 Thankyou

-

I keep reading that money doesn't exist. What does this mean ?

-

The ONS has today estimated that there are 5 million cases of fraud a year, with at least half being online. Much of this was not included in previous crime survey stats which showed reductions in crime. I have always believed that crime has not reduced, but it has simply changed or Police don't investigate it. Most shoplifting is not reported and is dealt with on a civil basis. Fraud reporting has been made difficult, with Police not investigating in most cases. When i look locally, in the last year or so, i believe crime has increased. A local newsagent was burgled, a cashpoint was broken into, there have been raids on several properties growing canabis. The Police do seem to be able to catch the criminals more quickly from intelligence, CCTV etc. The newsagent burglars were caught within a few weeks and came from about 40 miles away. They were obviously rubbish criminals, as they had already been to prison for similar crimes.

-

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) Over the past few months a large number of Facebook pages have been set up (mainly by Sovereign Citizen/Freeman on the Land activists). A common feature of these pages is the use of highly dubious methods of 'beating the bailiff'. The most common feature, and one that is sadly costing debtors dearly is the advice to refuse to speak or correspond with the enforcement agent and instead, to pay the amount of the actual 'debt' (Liability Order, parking penalty notice, court fine) direct to the creditor (minus bailiff fees of course). From further reading it would appear that the reason for refusing to 'engage' with the enforcement company is that by 'engaging' the debtor becomes a 'joinder' and therefore is agreeing to a 'contract' being entered into (a daft Freeman on the Land theory and one that has no basis in law whatsoever). A rather worrying suggestion that I have seen on quite a few of these sites recently is the advice to debtors to make a complaint about bailiff fees to the Magistrate's Court under the provision of Regulation 1 of the Magistrates Courts Act 1980. This is novel idea and one that again is being sold by 'Guru's' and has no basis whatsoever in law. Of course as with all such scams, there is no evidence whatsoever of any court 'successes'. This is despite the highly inaccurate 'claims' on these Facebook pages that once the summons is laid before the Justice of the Peace that the Justice will either issue a summons directed to the bailiff requiring him to appear before the magistrates' court to answer the information or more ludicrously; that a warrant would be issued ordering the bailiff to be arrested and brought to court to answer the charges. A copy of a recent 'template' is provided in the following post.

Over the past few months a large number of Facebook pages have been set up (mainly by Sovereign Citizen/Freeman on the Land activists). A common feature of these pages is the use of highly dubious methods of 'beating the bailiff'. The most common feature, and one that is sadly costing debtors dearly is the advice to refuse to speak or correspond with the enforcement agent and instead, to pay the amount of the actual 'debt' (Liability Order, parking penalty notice, court fine) direct to the creditor (minus bailiff fees of course). From further reading it would appear that the reason for refusing to 'engage' with the enforcement company is that by 'engaging' the debtor becomes a 'joinder' and therefore is agreeing to a 'contract' being entered into (a daft Freeman on the Land theory and one that has no basis in law whatsoever). A rather worrying suggestion that I have seen on quite a few of these sites recently is the advice to debtors to make a complaint about bailiff fees to the Magistrate's Court under the provision of Regulation 1 of the Magistrates Courts Act 1980. This is novel idea and one that again is being sold by 'Guru's' and has no basis whatsoever in law. Of course as with all such scams, there is no evidence whatsoever of any court 'successes'. This is despite the highly inaccurate 'claims' on these Facebook pages that once the summons is laid before the Justice of the Peace that the Justice will either issue a summons directed to the bailiff requiring him to appear before the magistrates' court to answer the information or more ludicrously; that a warrant would be issued ordering the bailiff to be arrested and brought to court to answer the charges. A copy of a recent 'template' is provided in the following post. -

I've been itching to buy trainer the a long time. I've had an exercise bike for a few years but I was getting fed up with it, partly because bits of it was time to wear out but also because it didn't really replicate cycling at all well. I was looking for a trainer and although I really wanted something that is generally compatible and in the majority, I was put off by the noise tests of the Wahoo Kickr and most of the other more common trainers. In the end, I saved up and settled for the Elite Real Muin because it was apparently so incredibly quiet. I was also looking for a virtual trainer. The Elite Real Muin arrived today. Here are some initial thoughts: – It’s well built Looks fantastic Extremely quiet The instructions are rubbish You can work it out without the instructions, eventually. Here are my main criticisms: – Firstly the software is extremely poor. It looks as if it was designed quite a few years ago. It’s clunky and frankly it’s badly behaved. In particular, the Ant connection is extremely finicky. You have to use the supplied Elite dongle to get any kind of connection at all. This is fair enough of course but the connection is unreliable and constantly drops out. I don’t think this is a function of the dongle or of the trainer. I think it is a function of the software because when I tried the dongle with other software such as Veloreality and Zwift the dongle was recognised without any problem and without having to reset it. As soon as I went back to the Elite software, there were problems. Looking at the Elite troubleshooting guide, there is so much time spent advising on Ant problems that it is clearly an issue. In fact looking around the Internet, I have noticed a number of people complaining about it. I noticed that DCRainmaker has talked about Elite’s commitment to the Ant standard, but this is not strictly true because Elite user own private Ant standard. In fact Elite only use private Ant for their power signal. The Cadence signal is a standard protocol and for instance, Veloreality had no problem receiving it and using it. Another nuisance about Elite’s implementation of Ant is that there seems to be no pairing. In other words the Elite software will automatically pair with whatever signal is being produced. Nice and easy, you might think – but actually it’s just an added problem because if you already have a Garmin Ant sensor on your crank arm, the Elite software doesn’t know which signal to use and so it uses neither of them and simply stops working. The only remedy for this is to remove your Garmin cadence sensor while you are using the trainer and then put it back when you have finished. Not a huge problem – but just a nuisance and once again points to a shabby and half-hearted implementation and lack of a customer facing approach from Elite. Surely it would only take a small bit of programming to make the Elite software pair and recognise a particular signal – but they certainly haven’t done it yet. Even when the software is receiving the Ant signal correctly, the stats are sometimes all over the place. I had finished a short session and had dismounted from the bike, but there was still a substantial wattage showing and also a cadence rpm of 64 and this continued for several minutes. The lag between cycling effort and what comes up on the screen makes it extremely difficult to ride virtually. On another occasion, I started pedaling and produced something like 1800 W traveling at 647 km/h! It’s not possible to know what is causing this but it might be glitches in the Ant signal. There were no such problems with the cadence readings In Veloreality or in Zwift and not only that, when I stopped pedaling, the cadence rate returned to 0 very quickly. With the Elite software, the cadence rate generally failed to return to 0 at all. I sort of feel that a lot of these problems would be ironed out if Elite implemented a standard Ant + on its trainers. I know that there are rumours that they are proposing to abandon private Ant – but frankly these rumours have been going on for at least a couple of years – and when I contacted Elite, they told me they had no plans. The trainer is great, but the software is extremely poor and I think that most people are paying this level of money to use the virtual training aspects and I suspect that many people will be disappointed. Elite needs to sort this out – but maybe they’re making enough money without having to bother. Incidentally, I have tried this on two powerful desktop computers and also a similarly specified laptop. All three of them passed the Elite tests as to whether they were suitable computers, without any problem. I forgot to add that Elite provide their own cadence sensor, which although is on an open protocol, has to be plugged in with a wire into the trainer. This is fine, but the problem is that for some reason or other known best to them, Elite have designed the cadence sensor in the most extraordinary shape so that is enormously difficult to get the receptor part close enough to the magnet without the rest of the body of the unit hitting the pedal. I suppose they wanted to do something a bit individual – but it means that they have come away from all the acquired wisdom of cadence sensor manufacturers going back several years. They’ve decided to try and reinvent the wheel – or the cadence sensor in this case and frankly it is just another thing that doesn’t quite work properly or easily.

-

I dont quite understand what the problem here is, claimant on DLA, partner is a carer, claim income support/child tax credits etc. Do not claim Mortgage relief (barred for whatever reason it was at the time of the claim some years ago) October, the Atos form arrives re assessment, form filled in and sent back (recorded), nothing heard from since. No medical sought (as yet) Roll forward 2 months and a letter drops through the door from the Benefit Integrity Centre in Ilford (about 100miles from the claimants address) withan Income Support from A2/04/12 . Form states that claimant has been getting income support for some time now and they need make sure they're getting the right amount of money. The enclosed letter from the Integrity Centre was dated 7th December and they want it back by the 20th December, just under two weeks. It is 33 pages long, has questions that were not asked the same or were not on the original form filled out about 6 years ago when the claim was first made, some of the questions seem almost intrusive. Some of the questions require quite accurate information, the claimant is currently not really well enough to answer the questions, some of the paperwork required needs a bank statement obtaining/ share amounts calculating etc. All this within 13 days or the threat of money being stopped? Seems a little unfair. They also want 'where to pay the money into' which they already have the details re accounts/sort codes, so why the need for these details? In part5 it asks ' Do you or your partner have any of the following' and ' You must answer for every item in the list. Tell us about accounts even if they are not in credit. but then go on to give just one line and £ amount for the bank accounts? Does this mean the claimant has to say 'Yes' to the bank accounts and then add how much is in each one credit wise and put the total in the box? If this is the case, the accounts are all but one overdrawn. Also, it asks for saving, there is a running float of around £1k in the account that the DWP payments are put in to, this would not be 'savings' but more of there before it gets used (which it does every month. They also want details of the mortgage but this was before the initial claim was made by some 4 years and no mortgage relief is being claimed (they are disallowed by the rules) so why is this relevant? why do they need to know? any help/advice would be much appreicated, the time limit given for the form (sent on 7th, received on 9th and want it back by 20th) seems a little strict.

I dont quite understand what the problem here is, claimant on DLA, partner is a carer, claim income support/child tax credits etc. Do not claim Mortgage relief (barred for whatever reason it was at the time of the claim some years ago) October, the Atos form arrives re assessment, form filled in and sent back (recorded), nothing heard from since. No medical sought (as yet) Roll forward 2 months and a letter drops through the door from the Benefit Integrity Centre in Ilford (about 100miles from the claimants address) withan Income Support from A2/04/12 . Form states that claimant has been getting income support for some time now and they need make sure they're getting the right amount of money. The enclosed letter from the Integrity Centre was dated 7th December and they want it back by the 20th December, just under two weeks. It is 33 pages long, has questions that were not asked the same or were not on the original form filled out about 6 years ago when the claim was first made, some of the questions seem almost intrusive. Some of the questions require quite accurate information, the claimant is currently not really well enough to answer the questions, some of the paperwork required needs a bank statement obtaining/ share amounts calculating etc. All this within 13 days or the threat of money being stopped? Seems a little unfair. They also want 'where to pay the money into' which they already have the details re accounts/sort codes, so why the need for these details? In part5 it asks ' Do you or your partner have any of the following' and ' You must answer for every item in the list. Tell us about accounts even if they are not in credit. but then go on to give just one line and £ amount for the bank accounts? Does this mean the claimant has to say 'Yes' to the bank accounts and then add how much is in each one credit wise and put the total in the box? If this is the case, the accounts are all but one overdrawn. Also, it asks for saving, there is a running float of around £1k in the account that the DWP payments are put in to, this would not be 'savings' but more of there before it gets used (which it does every month. They also want details of the mortgage but this was before the initial claim was made by some 4 years and no mortgage relief is being claimed (they are disallowed by the rules) so why is this relevant? why do they need to know? any help/advice would be much appreicated, the time limit given for the form (sent on 7th, received on 9th and want it back by 20th) seems a little strict. -

Hi All, I'm hoping there's someone on here that can help? I'm just in from work and a lovely letter through the door from IRS an investigation and recovery company on behalf of Peugeot Finance. I'm crying as I type this as I don't know what to do, They're not chasing me, but my husband, he has missed 3 payments on his van and due to him burying his head I assume, theyve handed it over to this lot and they've added their charges of £300 for a doorstep visit. My husband is away to a work course this weekend and I won't speak to him till tomorrow. I'm a scared what they will do and I just don't have £700 to give them if they come back. I've never had to deal with debt collectors before and I'm upset beyond words. Advice please as to what I can do to stop them repossessing the van. Can they do that for £400 arrears? Please please help me. Grumpy x

Hi All, I'm hoping there's someone on here that can help? I'm just in from work and a lovely letter through the door from IRS an investigation and recovery company on behalf of Peugeot Finance. I'm crying as I type this as I don't know what to do, They're not chasing me, but my husband, he has missed 3 payments on his van and due to him burying his head I assume, theyve handed it over to this lot and they've added their charges of £300 for a doorstep visit. My husband is away to a work course this weekend and I won't speak to him till tomorrow. I'm a scared what they will do and I just don't have £700 to give them if they come back. I've never had to deal with debt collectors before and I'm upset beyond words. Advice please as to what I can do to stop them repossessing the van. Can they do that for £400 arrears? Please please help me. Grumpy x -

Ikea is sprucing up its offer by selling cheap six foot Christmas trees in a bid for more festive business as analysts claim as much as 62pc of the high street is already on sale Famed for its flat-pack beds and the meatballs in its restaurants, Ikea is branching out in the festive rush by selling real Christmas trees - for five pounds. The Swedish out of town giant yesterday revealed its tactics for trying to entice shoppers away from the high street - offering customers a £20 coupon if they forked out £25 for a real, 6 foot Nordmann fir. Ikea said rivals were selling trees for as much as £79.99 elsewhere in Britain, with the average price £48. Brigit Hartelius, deputy country manager for the UK, told the Daily Telegraph it was all part of giving customers an "affordable Christmas". But more cynical analysts said it was simply part of the cut and thrust at Christmas as competition for shoppers hots up. Last week, accountants PriceWaterhouseCoopers said 62 per cent of the high street was already on sale or running promotions amid fears hard-pressed families coping with rising energy bills will cut back this Christmas. More: http://www.telegraph.co.uk/finance/personalfinance/consumertips/household-bills/10506222/Christmas-offers-best-gifts-cheap-presents-real-Christmas-trees-best-Christmas-trees-Ikea-Hawkes.html

Ikea is sprucing up its offer by selling cheap six foot Christmas trees in a bid for more festive business as analysts claim as much as 62pc of the high street is already on sale Famed for its flat-pack beds and the meatballs in its restaurants, Ikea is branching out in the festive rush by selling real Christmas trees - for five pounds. The Swedish out of town giant yesterday revealed its tactics for trying to entice shoppers away from the high street - offering customers a £20 coupon if they forked out £25 for a real, 6 foot Nordmann fir. Ikea said rivals were selling trees for as much as £79.99 elsewhere in Britain, with the average price £48. Brigit Hartelius, deputy country manager for the UK, told the Daily Telegraph it was all part of giving customers an "affordable Christmas". But more cynical analysts said it was simply part of the cut and thrust at Christmas as competition for shoppers hots up. Last week, accountants PriceWaterhouseCoopers said 62 per cent of the high street was already on sale or running promotions amid fears hard-pressed families coping with rising energy bills will cut back this Christmas. More: http://www.telegraph.co.uk/finance/personalfinance/consumertips/household-bills/10506222/Christmas-offers-best-gifts-cheap-presents-real-Christmas-trees-best-Christmas-trees-Ikea-Hawkes.html -

Hi All, Very new to all of this but essentially me and my partner got together a year ago and it turns out she has some minor debt. A fine from the courts for a theft which ended up a £120 fine. Now, this was two years ago (When she was 18) and they have decided to catch up to her now about it. The initial amount owed was £120 and has risen to £420 she has had no previous contact with them except for the court date, she received no warrant (Until today), and no notice of the debt to be owed. The Warrant we received today was stated as a "Distress warrant" And was of the value of £205 in the balance to be paid, £120 original court fine and £85 letter charges. But £420 was handwritten underneath and apparently that is how much we owe. I did read something about bailiffs and 180 days from when the warrant was issued but only had a moment to glance at that. The case history is marked as follows: July 2012 : Start Note Offence - Theft from a shop Date of sentence: June 2010 (Which is the £120 fine issued by the court) July 2012: Hold Case - Specific Period Hold Until July 2012 July 2012 - Misc Note Batch List Printed July 2012: Letter Sent - First HMCTS - First Bilingual Printed (I am assuming this would be the £85 letter charges) August 2012 - Bailiff Assigned Bailiff XX Assigned to case August 2012 - Misc Note Assigned cases List Printed August 2012 - Misc Note Activity Report / HMCS - Distress Warrant Printed August 2012 - Bailiff Unassigned Bailiff XX Unassigned August 2012 - Bailiff Assigned Bailiff XX Assigned to case August 2012 - Misc Note Assigned Cases List Printed Now, I am unsure where the additional £215 charges have come from to total debt to £420 but i wanted to know if you had any advice? There is no court stamp on the warrant and the only people we have spoken to is people from the main company which is Excel Civil Enforcement i can't seem to be able to gain information as to which court the case was assigned to. If needs be i can and will upload the document we recieved from the bailiff and black out all of the personal information so you can have a look at it. But from what i have stated here, is there any reason i should be suspicious? Thank you to anyone and everyone who helps me and my partner has just had a child and we are in our first tenancy so we are all over the place anyway at the moment! EDIT: Sorry, i also forgot to mention that he seemed twitchy about me paying in instalments, he wants payments done within this month. He won't allow any other way.

Hi All, Very new to all of this but essentially me and my partner got together a year ago and it turns out she has some minor debt. A fine from the courts for a theft which ended up a £120 fine. Now, this was two years ago (When she was 18) and they have decided to catch up to her now about it. The initial amount owed was £120 and has risen to £420 she has had no previous contact with them except for the court date, she received no warrant (Until today), and no notice of the debt to be owed. The Warrant we received today was stated as a "Distress warrant" And was of the value of £205 in the balance to be paid, £120 original court fine and £85 letter charges. But £420 was handwritten underneath and apparently that is how much we owe. I did read something about bailiffs and 180 days from when the warrant was issued but only had a moment to glance at that. The case history is marked as follows: July 2012 : Start Note Offence - Theft from a shop Date of sentence: June 2010 (Which is the £120 fine issued by the court) July 2012: Hold Case - Specific Period Hold Until July 2012 July 2012 - Misc Note Batch List Printed July 2012: Letter Sent - First HMCTS - First Bilingual Printed (I am assuming this would be the £85 letter charges) August 2012 - Bailiff Assigned Bailiff XX Assigned to case August 2012 - Misc Note Assigned cases List Printed August 2012 - Misc Note Activity Report / HMCS - Distress Warrant Printed August 2012 - Bailiff Unassigned Bailiff XX Unassigned August 2012 - Bailiff Assigned Bailiff XX Assigned to case August 2012 - Misc Note Assigned Cases List Printed Now, I am unsure where the additional £215 charges have come from to total debt to £420 but i wanted to know if you had any advice? There is no court stamp on the warrant and the only people we have spoken to is people from the main company which is Excel Civil Enforcement i can't seem to be able to gain information as to which court the case was assigned to. If needs be i can and will upload the document we recieved from the bailiff and black out all of the personal information so you can have a look at it. But from what i have stated here, is there any reason i should be suspicious? Thank you to anyone and everyone who helps me and my partner has just had a child and we are in our first tenancy so we are all over the place anyway at the moment! EDIT: Sorry, i also forgot to mention that he seemed twitchy about me paying in instalments, he wants payments done within this month. He won't allow any other way. -

Hi I have been a complete idiot and got hooked on gambling i have taken out so many pay day loans i went to payplan set up a dmp but i am having difficulty paying it as i took out more loans to feed my habbit. I have stopped but all are chasing me do I tell them about my addiction as they want to know why i cant pay. owe £7000 arrears on mortgage and have broken so many arrangements i think they will repossess my house. If they start proceedings what happens if I can prove i can pay a little back each month will they stop the repossession. I dont think they will agree to any more arrangements shoulld i tell them the truth

-

Hello all, I am not old, I am not young, but I would like to say, A real book made with real paper and bound and written with passion, proof read, edited, published, will stand the test of a thousand years of existence! Technology is my thing, however if I were to be sitting on a deserted island and there is no power and my batteries ran out, nothing beats a real tangible physical book!!!! a work of art an inspiration, a wonder - and its in front of you there ready to be read, now and forever! real books will never die..... Kindles I pads Phones etc are fine when you are on a train etc... but give me the real stuff all day everyday. khemist