Search the Community

Showing results for tags 'monument'.

-

Hi Everyone I have been charged by Monument £1020 on late payment and overlimit fees. My credit limit is only £250 and I owe them about £1075. Last week I sent them the letter from this website requesting statements along with my £10 cheque. Yesterday I received a letter back from them giving me a spreadsheet with all the charges. They also gave me my £10 cheque back! Can anyone advise what I need to do now?? Should I print off the template letter on this site, asking for the £1020 to be refunded?

-

Hi do you have the contact details for Monument please?

-

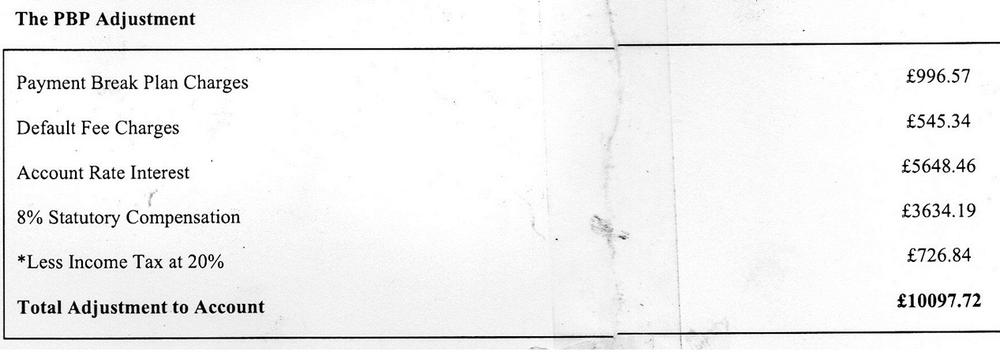

I have received a letter from monument about PBP. It was totally unsolicited, and I have not applied for anything (PPI or the like)or contacted Monument in any way for years. This letter came totally out of the blue and I dismissed it along with all the other letters I have received from them over the years. I ripped it up and put it in the bin. The Short Story My monument account was pulled many years ago , I can't even remember the dates it was so long ago, leaving an unpaid balance of around £3,600 which remained unpaid. The Long Story I have just fished this letter out of the bin as yesterday, I received a cheque in the amount of just over £6,800. The letter I received last week referred to PBP - Payment Break Plan and looks to be a letter of 'without admission of liability'. I have scanned part of this and attached it to this post. It would appear than an adjustment of just over £10,000 has been credited to my account, and the cheque I have received looks to be the difference between the amount of the adjusted credit, and the outstanding balance as mentioned above. I'm just wondering if this is legit or maybe a ruse on the part of Monument to track down their un-paying debtors. I have seen other posts here mentioning refunded PBP - which I never knew I had, but these are dating back to 2014/2015. Obviously we're now at the latter part of 2016, and they 'look' to be still paying out. The letter states they will apply the adjustment values to any outstanding debt from the account, and should this result in your account going into credit, we will issue you a cheque within 28 days - which looks to be the same as others have posted here. I'm not sure whether to put this cheque in the bank or leave it be as I really can't afford to be snared in this way. Any input would be greatly appreciated. Thanks.

-

Hi, I have had a Monument credit card for about 15 years and have been paying PBP for most of this time. I actually cancelled it in 2010 when I realised that my balance was never coming down due to the amount I was paying in, what I assumed at the time was PPI (I just paid the minimum payment by DD each month). The card balance was always around £3000. I had a letter from Monument about 6 weeks ago advising that I may be due a refund of PBP and directing me to their website. I simply entered the details on the letter and that was that. Today I have received a letter from them, without admission of liability and as a gesture of goodwill, stating a total adjustment to my account of over £16k! I actually paid the card off and closed the account in January of this year (the balance was still around £2800!). I have tried all day to contact them but the line has been constantly busy. Does anyone know whether this seems a realistic figure - my limit on the card was approx £3500 and I hadn't used it for about the past 7 years. Thanks in advance.

-

Can a 'Reply Card' ever be a legal Agreement? Part of my SAR's request came a little photocopy purporting to be 'it'. No details other than my personal ones and a Declaration with Credit Agreement Regulated by CCA1974.....I am applying for a Providian Visa card..... (I can scan it later if necessary). No interest rate etc. Dated Oct 2002. Also, actual statements were not included, only a list of usage and payments made each month (quite adequate for reclaiming charges). But I'm sure I used to see, stamped on my actual statements, something about Payment Break Plan. Of course, I now know that is same as PPI! When I looked in the T&C's (they kindly included a recent copy of these) it had, in small print, that the PBP would incur a charge of 0.89% of the balance each month. Question 1. Is this a 'hidden' charge added to the APR charged each month so you don't realise it's there? Or, should I be less cynical and presume that I opted out without realising?? Question 2. How on earth do you calculate that???! Sneaky or what??!

-

I had a disputed Credit Card account with Monument and the alleged debt which i disputed became statute barred. I haven't heard anything from Monument for a couple of years, however I received a letter this morning. Dear drob Thank you for your recent correspondence ( I haven't corresponded with them recently) We have reviewed your account and can confirm that yoy subscribed to the Payment Break Plan product. Without admission of liability, and as a gesture of goodwill we are prepared to adjust your account with the fees plus compound interest. Payment Break Plan Charges: £179.04 Account Rate Interest: £86.72 8% Statutory Compensation £35.80 Total Adjustment to Account £408.96 I am just wondering if I should be cheeky and ask for the cash, should they be applying the Payment Break Plan refund as an adjustment???

-

I had a Monument Credit Card and was receiving statements from them on a monthly basis. At the beginning of this year they passed the debt on to a DC who I wrote to and claimed the debt is Statute Barred (it was over 7 years since last payment had been made and I live in Scotland anyway). I haven't heard from the DC since (about 3 months now) Last month monument sent me a letter asking if I wanted to claim PBP, as I am disabled and was unable to work when I took the credit card out, I sent them an email to stake my claim on the 9th Sept which they have acknowledged. Can they offset any PBP against a statute barred debt and send it to the DC?? Im pretty sure they said the debt had been sold to Capquest. All advise is welcome

-

Hi I had a Monument Credit Card, which was opened in 2004, this month i started gettting letters from NCO Europe saying to pay up, i have sent one letter and they have replied with a bit strange wording, i have listed them below and was wondering if you could help me draft a response the specifics i am looking is for quotes from the law, example under such law and under section and subsection etc., i wonder if you could help., thanks in advance. 1) their response "I can confirm that our letter dated 12th May 2015, confirms that your monument account has now been passed to NCO to manage the collection of the balance outstanding, This is your notice of assignment, however, i do acknowledge that you have requested the Deed of Assignment A Deed of Assignment is a document in which a debtor appoints a trustee to take charge of the property to pay debts, partly or wholly. It allows one party(the assignor) to transfer ownership of something they own, such as a house or endowment policy, to someone else(the assignee). Therefore, it is not applicable to your account and it is not possible to provide." What they say above is it right?, what can i quote in law to make them agree for a deed of assignment. 2)"We have not purchased this balance therefore we are unable to provide a Deed of Novation" they have not purchased it???? 3)"NCO Europe is managing the above account on behalf of Arrow Global. The account was purchased by Arrow Global from Monument on 22nd December 2014. As per the original terms and conditions with Monument they reserve the right to pass or sell your account to a third party to manage. The account was sold to arrow global and they have appointed NCO Europe to manage it on their behalf" they are managing does it not make them a party and under law they have to provide documentation for this, they say i have to make a CCA request which i do not want to as it will reset the account, can you please advise. Hope to hear from you soon. a image of the letter below

-

HI, I have received a final response letter from Monument, regarding a Payment break plan I use to have attached to a credit card. I last paid a payment on the 6/10/2006, the credit card account is statute barred. I did receive letters from Arrow Global and after asking them to prove the debt, not heard from them since. The problem is I have not made any claim against Monument or authorised a third party to do so in my name. Their letter states in response to my recent correspondence with them. I am concerned this will reset the time on the statute barred debt, some advice would be very welcome.

-

hi can anyone give me some advice. Monument have written to me to day that they are refunding me for the payment break plan but I still have a balance with them and they are going to off set this. Just want to know if they can do this or should I get the refund direct? thank you x

-

It's been a while since I had to use the advice on this forum, which is a very positive thing! Anyway, I am currently trying to help a relative claim back PPI from Barclays and PBP from Monument. 1. Barclays have replied to state that apparently the relevant box was ticked and so there can be no claim. I reckon there's more than a hint of male bovine excrement about that statement but am unsure how to proceed. Exact wording from the letter is; "Following my investigation I have identified that your application for PPI was submitted by post. This means that at the point of applying for PPI we did not give you any advice." Then goes on to explain all the details that provided eligibility. Basically I am aware that the 'you ticked the box' excuse is being rolled out, but don't know where to go from here. 2. Monument replied that 'without admission of liability' they could offer of a few hundred pounds. Firstly, they seem to have worked this out based on only 3 years data when (I will have to double check) I think the account is much older than that. Secondly, they say "Refunds will only be offered on condition that any monies still owed from the original debt are offset by the refund." - This account is still being paid off and the refund will not offset the full amount - but surely they can't do that!? Also, is 'PBP' just a stinkweed by any other name? It seems like they're trying to use the different term for legal squirming room. So, that's my situation and any advice on how to proceed would be most welcome. Thanks km1988

It's been a while since I had to use the advice on this forum, which is a very positive thing! Anyway, I am currently trying to help a relative claim back PPI from Barclays and PBP from Monument. 1. Barclays have replied to state that apparently the relevant box was ticked and so there can be no claim. I reckon there's more than a hint of male bovine excrement about that statement but am unsure how to proceed. Exact wording from the letter is; "Following my investigation I have identified that your application for PPI was submitted by post. This means that at the point of applying for PPI we did not give you any advice." Then goes on to explain all the details that provided eligibility. Basically I am aware that the 'you ticked the box' excuse is being rolled out, but don't know where to go from here. 2. Monument replied that 'without admission of liability' they could offer of a few hundred pounds. Firstly, they seem to have worked this out based on only 3 years data when (I will have to double check) I think the account is much older than that. Secondly, they say "Refunds will only be offered on condition that any monies still owed from the original debt are offset by the refund." - This account is still being paid off and the refund will not offset the full amount - but surely they can't do that!? Also, is 'PBP' just a stinkweed by any other name? It seems like they're trying to use the different term for legal squirming room. So, that's my situation and any advice on how to proceed would be most welcome. Thanks km1988 -

Can anyone tell me if the most recent contact for old Monument accounts is still R. Raphael & Sons PLC Albany Court Yard, 47-48 , Piccadilly, London, W1J 0LR Thanks in advance for any help.

-

Hi all, I know everyone on these forums are very savvy regarding PPI matters, and there seem to be some experts also. My late father owed "Monument" money but once Death Certificate was issued then it was resolved (no will, no assets). I have now received a letter saying they owe PPI, or PBP as they like to call it. However, their dealings look suspicious as essentially they say "We will not give you money unless there is some left over what is owed." Why should I pay what is owed? This does not seem fair. They also want me to sign a "Statutory Declaration" and I fear that if I sign that they may be charging me for what is owed. Please, is there any way to get the full amount of money they owe? It is over £1000 pounds. Here are the letters below, I hope you can help: [ATTACH=CONFIG]55404[/ATTACH][ATTACH=CONFIG]55405[/ATTACH]

Hi all, I know everyone on these forums are very savvy regarding PPI matters, and there seem to be some experts also. My late father owed "Monument" money but once Death Certificate was issued then it was resolved (no will, no assets). I have now received a letter saying they owe PPI, or PBP as they like to call it. However, their dealings look suspicious as essentially they say "We will not give you money unless there is some left over what is owed." Why should I pay what is owed? This does not seem fair. They also want me to sign a "Statutory Declaration" and I fear that if I sign that they may be charging me for what is owed. Please, is there any way to get the full amount of money they owe? It is over £1000 pounds. Here are the letters below, I hope you can help: [ATTACH=CONFIG]55404[/ATTACH][ATTACH=CONFIG]55405[/ATTACH] -

Hi just wondered if anyone can help i made a claim for ppi well PBP from a old Monument account, bit strange really just found my old card one day and then found this forum then within a couple of days all this happens i made a call to monument made a claim for pbp they said yeah no probs we will deal with your claim you need to do nothing, and to be honest so far after 3 weeks i have spoke to them only twice then the other day a letter arrived dated 05/08/2014 Final Response Says Dear Mr I write further to your recent correspondence we have reviewed your account and can confirm you subscribed to the payment break plan ("PBP") product Without admission of liability, we are prepared to refund to you these fees plus compound interest (at today,s account interest rate of 28.82%) from the date of the fee, as shown below: Charges £624.54 Account rate interest £417.27 8% statutory compensation £477.46 less income tax at 20% £95.49 Total Refund £1423.78 (charges plus interest) Now i thought great happy days Then i remembered didnt i owe them a couple of hundred pounds so i called them up at customer relations and the lady said a cheque was rasied on the 06/08/2014 for £963.00 (about that) because you owed us money on the account (big jump from £200) which was being chased by a third party company called JCIA now the reason for my long boring post is, is this legal ?? can they take this money without first showing me what i owed them second take money from me to pay a third party company that they sold the debt to ?? i would have thought they should be made to pay me and then i do a deal with JCIA who i do recall sending me a letter once 5 years ago if anyone knows if Monument can do this please let me know Cheers

-

Hello everyone, new here and looking for some advice. I think I may have actually overloaded my brain over the last few days reading through all the different threads. I hope I'm posting in the correct place (first post) my query relates to a default placed on my credit file in Feb 2011 by Raphaells Bank (CCRT). This was originally a Monument credit card, default amount is £1533, credit limit was £750. My question is, who do I send my request to for the original agreement, as I don't think Monument actually exist anymore?

-

Hi there I'll try to be brief. Many years ago (15 if not more) I had a Monument credit card. When things became difficult a couple of payments were missed the debt was passed to C.A.R.S. to recover. About 12 months ago I entered into a DMP with Payplan and C.A.R.S. were added to the list of creditors. Payplan notified me that they were returning the payments so I called C.A.R.S. and they said that they no longer held the account and it was with Jepherson Capital. I phoned them and they too know nothing about it. I subsequently removed C.A.R.S. from the plan as they were just returning my payments. I have no had a letter from C.A.R.S. asking for the balance which is £1556. Naturally I'm not going to pay it but I would like some advice as to what to do now. This debt has been passed from pillar to post. Should I send a CCA letter (I think that's what it is) and if I do what am I looking for. I am hoping there will be discrepancies as the original debt is so old but I'm not sure how to go about getting something sorting. Many thanks

-

I will try to be brief with this question/problem. In 2008 my friend who had a Monument Credit Card suffered a heart attack and could not work. There is a vague recollection of Monument accepting the situation and providing a payment break or suchlike. Friend continued with regular payments until July 2011 when he got a letter out of the blue from C.A.R.S He telephoned Monument who said they no longer would be dealing with it and in future he would have to deal with C.A.R.S After a telephone convo with C.A.R.S (July 2011) he agreed to pay a set amount on the same date each month and he continues to get monthly statements from Monument. This month after checking his bank statements he noticed (since last November 2012) C.A.R.S have been erractic in taking their payments. They are ignoring the agreed date and two payments were taken out in the same month. This led to some checking and I discovered the only communication he has ever had from C.A.R.S was the initial letter (kept for ref) and a telephone call in July 2011. At that time he believed he was agreeing to a direct debit but now learns they got their payments via a credit debit on his card. Having read scary stories on recurring debit card payments, my friend would ideally like to stop C.A.R.S from using his debit card in this way. Now the obvious thing is to contact C.A.R.S but wanted some advice on how to proceed. Thanks in advance of any replies.

-

Hi I have a debt with Monument that I have been paying off for a number of years at £50 per month. The original credit limit on the card was £500. The current balance with Monument is £1,980!!! I realise I should have checked this much sooner, but stupidly I didn't. It appears that each month they continue to add interest to the debt, and charges too. I want to get rid of this debt once and for all, and I am hoping someone could give me some advice on how to reduce the final balance before I clear it. I've tried calling them numerous times to discuss it, but the call center operatives are dreadful - they cannot deviate from their script, as is the line to wherever the call centre is. Any advice would be gratefully received. Thanks, Mike.

Hi I have a debt with Monument that I have been paying off for a number of years at £50 per month. The original credit limit on the card was £500. The current balance with Monument is £1,980!!! I realise I should have checked this much sooner, but stupidly I didn't. It appears that each month they continue to add interest to the debt, and charges too. I want to get rid of this debt once and for all, and I am hoping someone could give me some advice on how to reduce the final balance before I clear it. I've tried calling them numerous times to discuss it, but the call center operatives are dreadful - they cannot deviate from their script, as is the line to wherever the call centre is. Any advice would be gratefully received. Thanks, Mike. -

Hi Today i received a letter from a DCA called C.A.R.S (Creditlink Account Recovery Solutions), they state that they will be attempting to visit me at home within the next week to 'Establish Reasons For Non-Payment' to an old Monument Credit Card (balance of £620.21) which must date back to at least 4 years ago. I have responded by sending them a letter back requesting all communication to be made via letter and no doorstep callers and will immediately follow up with a CCA request. However i've just looked at my Credit Report which lists everything but for some reason this debt is nowhere to be seen on it, what does this mean and is it to my advantage ? many thanks

Hi Today i received a letter from a DCA called C.A.R.S (Creditlink Account Recovery Solutions), they state that they will be attempting to visit me at home within the next week to 'Establish Reasons For Non-Payment' to an old Monument Credit Card (balance of £620.21) which must date back to at least 4 years ago. I have responded by sending them a letter back requesting all communication to be made via letter and no doorstep callers and will immediately follow up with a CCA request. However i've just looked at my Credit Report which lists everything but for some reason this debt is nowhere to be seen on it, what does this mean and is it to my advantage ? many thanks -

Did anyone have this ?

-

So today I have finally decided to take the plunge and tackle monument. I had a card several years ago with monument that spiralled out of my control and went to arrow global. They are chasing me via a company called rockwell for an amount of £1100, the limit on my card was £500. I have spoken to monument and they have stated my balance is £497 and that they have sold it to arrow global who claim they have not added anything to the balance. So I am pretty confused and arrow global are looking into it. I seem to remember I was pressured in to taking the payment break plan and I also remember a lot of charges. I have sent a SAR today which I understand is the first step in the process. If someone could be so kind as to give me a bit of advice as to what to do when I receive all of my statements it would be very much appreciated. Ideally I would like to claim back the PPI and the charges plus contractual compound interest. Thanks in advance!

-

Hi Everyone, Just looking for a bit of advice so thought this might be the place to come.... I took out a Monumnet card in 2004, and unknowingly payed their infamous 'Payment Break Plan'. I have tried to claim back the Payment Break Plan, but they have only offered me back the last 6years money. I have sent them a SAR and like others on here have received the last 6years paperwork, a copy of the original 'reply' card - not the signed credit agreement, and a copy of up to date terms and conditions. In their terms and conditions it states that if the payment break plan is required it needs to be added on via the call centre or in writing, neither of which I did but was added anyway! I had also called Monument and asked about removing the Payment Break Plan but was told they don't take it off! I discovered this was a lie when in 2009 I called to make a substantial payment and advised I would be paying the balance by the end of the week that the advisor said she would remove it! I have appealed to the FOS but so far they are about as much use as a chocolate teapot and have upheld the offer from Monument. My argument is, if they cannot provide proof that I originally added it on (which I didn't), how can they refuse to refund my money?? I have now also found statements going back to 2005 showing the plan, but the FOS has said these are irrelevant until they find out if Monument have proof whether or not I added it on - which no doubt they'll say they don't! If they say they haven't got proof that I added the plan are they liable to refund my money? With SAR should they have sent me a copy of my signed credit agreement and terms that were applicable at the time? Sorry it's been a long post but i'm losing patience with them at very rapid rate!!!

-

Hi all I decided to make a claim for PPI on my monument visa card after coming across some old statements which had payment break plan on them. I do remember querying it but was told at the time I had to have it order to get the card. I also had a few £24 charges. I got the card in 2003 and according to my credit report the account was settled in 2007 and it wasn't listed as monument visa but as barclaycard. I sent monument a SAR request end of july to an address in Leicester with a cheque for £10. (I have around 22 statements out of approx 43) Today i received a letter from barclays saying that they can't find my records with the info i provided. Am I right in thinking that if the account was settled in the last 6 years they should still have my records? Also i checked my account and the cheque has been cashed. should they have cashed it if they couldn't find my records? I thought the £10 fee was for the cost of copying. I am not sure what to do next. Can anybody help?

-

Hi Guys, I am hoping for some help with an issue we are having with CABOT. My husband recieved a letter about 2 years ago from Cabot stating he owed an outstanding debt to them for a monument card which was taken out in 2002 in his name. (We never got together until 2006 and he lived on his own at the time). After following some advise on this forum we have attempted to tackle this issue with cabot and have disputed this debt and not acknowledged it with them. We also recieved several other debt letters from capital one and O2 and it appears that he has had his ID stolen. We reported this to the police and obtained a crime reference number which we have issued to all companies and cabot are refusing to acknowledge the fact that he is not liable for this debt. We sent off a CCA request and recieved a reply card (does not look like a credit agreement to me) back from them by way of a credit agreement and the signature is not the same as the one my husband uses on all of his legal documents, additionally it states he was a student. My husband was in and out of hospital that year with ill health that we can prove. We have been going backwards and forwards with letters and even complained to the ombudsman who has referred the case back to cabot to resolve. The final response from cabot is attached for you to have a look at, as is the reply card they have sent by way of a CCA request. Additionally, they say the account was active until 2006, is this not statute barred now anyway? Confused and annoyed with these very arrogant people and I would welcome any advise you can offer to assist us in sorting this out. Thanks Peeps

-

Can anyone offer any advice, i contacted monument with regards to payment break plan which had been added to my credit card since 2001. i have worked out that i have paid over 11 years a total of £2650 to this plan plus the interest which totals approx £3,300. i have today received a final response letter from monument confirming that i have subscribed to this plan since jan 2001 but they are only prepared to offer me without admission a refund of these fees plus interest for the past 6 years, as this is their company policy. The total refund offer is for £1,990 including interest, which i believe is probably about £1,300 short of what i have actually paid in including the interest charged. My question is should i accept this offer or should i take it to the FOS, and chance losing the offer if they dont find in my favour. Does anyone else have the same sort of offer and if so have you taken any further action

Can anyone offer any advice, i contacted monument with regards to payment break plan which had been added to my credit card since 2001. i have worked out that i have paid over 11 years a total of £2650 to this plan plus the interest which totals approx £3,300. i have today received a final response letter from monument confirming that i have subscribed to this plan since jan 2001 but they are only prepared to offer me without admission a refund of these fees plus interest for the past 6 years, as this is their company policy. The total refund offer is for £1,990 including interest, which i believe is probably about £1,300 short of what i have actually paid in including the interest charged. My question is should i accept this offer or should i take it to the FOS, and chance losing the offer if they dont find in my favour. Does anyone else have the same sort of offer and if so have you taken any further action