Search the Community

Showing results for tags 'response'.

-

I fell behind on payment due to illness. Long and short of it is that FRF are threatening repossession. the vehicle is worth 1.5k. at auction it will get max £500. a trade garage who valued said they wiould pay the finance company 1.5 direct and deal direct. First Response tell me the garage would have to pay the full amount outstanding of 4k. if i VT i am liable for the balance after auction. i assume this is process. but if i am able to make the vakue of the vehicle does anyone know if other finace companies who have accepted this. has anyone had repossesion dealings with this company. Not the most customer friendly but it is what it is.

I fell behind on payment due to illness. Long and short of it is that FRF are threatening repossession. the vehicle is worth 1.5k. at auction it will get max £500. a trade garage who valued said they wiould pay the finance company 1.5 direct and deal direct. First Response tell me the garage would have to pay the full amount outstanding of 4k. if i VT i am liable for the balance after auction. i assume this is process. but if i am able to make the vakue of the vehicle does anyone know if other finace companies who have accepted this. has anyone had repossesion dealings with this company. Not the most customer friendly but it is what it is. -

Lowell recently sent me a 'letter before claim' giving me 14 days to contact them regarding a debt from 2011 or they would take me to court. This debt relates to a bank account, with NO overdraft facility that ended up going overdrawn. I received some advice and sent them a prove it letter and after a few weeks received the following as a response - imgur (dot) com/ a /E7JuE Along with the above letter they sent a copy of my bank statement from 2011 but there was no notice of default included in the package, which they state they did send but have not. Is there anywhere else I can go with this now? Any help appreciated! EDIT - Cannot post link to image. The letter basically says "Please find enclosed a copy of the statements and default notice as requested from the original creditor. As this account is a current account it is not regulated by the consumer credit act therefore the original creditor is not obliged to provide you with a copy of the agreement"

-

Hi all - this is a split off from a more general thread where following your Cash Cow advice I have sent off many CCA's This is a Natwest CC taken out in Mid 2004 - Balance around £2300 Currently paying £1 PCM Direct - Account in Default since 2010 The application was made online They have sent me 1) a covering letter telling me they can send me a copy agreement and "current" terms. 2) A current leaflet with the General Conditions 3) A letter regarding a replacement Credit card with no date 4) A signed credit agreement A6 size no mention of limits or APR's 5) A letter with a copy of the agreement with APR's on an Credit limit 6) A photocopy of some more terms with some minor variations in the Advances APR's 7) A copy of a current statement. I have no idea what most of this means and your guidance as to the next steps would be greatly appreciated.

-

Hi all - this is a split off from a more general thread where following your Cash Cow advice I have sent off many CCA's This is a RBS CC taken out in early 2005 - Balance around £700 Currently paying £1 to Moorcroft They acknowledge receipt of CCA but request "in line of their clients procedures" a hand signed request... they returned the old one for a signature.. The also ask the the PO gets made out to the client ( atm it just says xxx) On hold 30 days blah blah I gather this is all rubbish so what is my next move? Thanks again

-

No response from the dealer at all.

shedder101 posted a topic in Vehicle retailers and manufacturers

Hi I hope you can give some advice on my next step I need to take with a used car dealer and a problem I have had with a car I purchased from him. I purchased the car from him mid June 2012 the car was advertised on Autotrader with 12 month MOT and Tax. I agreed a trade in deal for my vehicle and paid the balance on my credit card. On the test drive the car was driven by him and we went around the block. The car had full history and a new MOT and was I thought a good purchase. On the way home I noticed a jerking from the gearbox at low speed this was worse after the trip home some 50 miles, however the car only judder when pulling off after that the car drove normally. I contacted the dealer the next day as I had left my sunglasses in my old vehicle and mentioned the juddering to him and my concerns, he said they all do it don’t worry about it. He sent me back my glasses in the post. I was informed at the end of June by an official my road tax was about to expire, I said no it’s to 2013 as had been advertised but they were correct and I had to tax the vehicle at the post office for £250 I continued to be concerned about the gearbox over the next few days and did some research on the internet in to its cause, following the points raised on the forums I checked the service history and noticed a gearbox service had been missed and contacted my local main dealer for advice. The said servicing was vital for correct operation of the gearbox; I checked prices and found the main dealer to be very competitive on cost so booked the car in with them for the service. I informed the used car dealer in writing about my concerns as well as complaining I had paid for road tax the car was advertised with, this letter was sent recorded delivery. No response from the dealer at all. When the main dealer had the car the service was performed and a car check by them they informed me that the front brakes of the car were in a dangerous condition and they refused to test drive the car until they were replaced also the rear brakes were binding and corroded and needed replacing. Also several other minor faults were listed on the receipt. Not knowing the best action I had the car back from the main dealer and wrote again, recorded, to the used dealer with a copy of the invoice showing the faults from the main dealer and asking for a response about what he was going to do about it. No response from the dealer at all. I have obtained three quotes for the brake work to be repaired and sent him copies of them and told him I needed a response in the next seven days or I will go ahead and get the car repaired and send him the bill, or for him to collect the car and get it repaired as I won’t drive the car as it is dangerous. No response from the dealer at all. I intend to get the car fixed next week and the only upside is the gearbox is considerably improved but I am out £151 to get it fixed, what this long winded way round text and I apologise for its length but I wanted to make sure you had all the facts, is, what do I do after that. Send another letter to the dealer, contact the credit card company and say what, or take him to small claims court. Any help would be appreciated. -

Hi, my 19 year old son who has recently been diagnosed with depression got himself into a muddle with his banking due to inexperience and the ease of contactless payments. He was paying charges of £80 per month for the majority of a year and was unable to get himself out of the financial mess he had got himself in. Once I became aware I advised him to speak to the bank HSBC and ask them to give him an authorised overdraft so he could limit his charges and get himself out if the situation he found himself in. He contacted HSBC and as he failed a credit score (no surprise there, he has never had credit) they refused to give him an authorised overdraft. He buried his head the sand a little longer and then finally took my advice to contact the Financial Ombudsman. HSBC initially denied to the FOS that he had made a call to them explaining his financial situation and asking for help but after we supplied a telephone bill detailing the date and the fact that he was on the phone for in excess of an hour they agreed that he had made contact. The FOS requested the conversation. However HSBC did not submit a recording of the phone call they supplied hand written notes. These notes failed to mention that he was experiencing financial hardship. Therefore the FOS said that he had no case. He stressed that he did state this in the phone call but the FOS decided that as it was not mentioned in the notes submitted by HSBC then that was the end of the matter. My son has paid in excess of £800 in charges on a paultry income and it feels that he has no redress against HSBC. Can they not be forced to submit the original recording?

Hi, my 19 year old son who has recently been diagnosed with depression got himself into a muddle with his banking due to inexperience and the ease of contactless payments. He was paying charges of £80 per month for the majority of a year and was unable to get himself out of the financial mess he had got himself in. Once I became aware I advised him to speak to the bank HSBC and ask them to give him an authorised overdraft so he could limit his charges and get himself out if the situation he found himself in. He contacted HSBC and as he failed a credit score (no surprise there, he has never had credit) they refused to give him an authorised overdraft. He buried his head the sand a little longer and then finally took my advice to contact the Financial Ombudsman. HSBC initially denied to the FOS that he had made a call to them explaining his financial situation and asking for help but after we supplied a telephone bill detailing the date and the fact that he was on the phone for in excess of an hour they agreed that he had made contact. The FOS requested the conversation. However HSBC did not submit a recording of the phone call they supplied hand written notes. These notes failed to mention that he was experiencing financial hardship. Therefore the FOS said that he had no case. He stressed that he did state this in the phone call but the FOS decided that as it was not mentioned in the notes submitted by HSBC then that was the end of the matter. My son has paid in excess of £800 in charges on a paultry income and it feels that he has no redress against HSBC. Can they not be forced to submit the original recording? -

hi all, sent a cca to restons recently regarding an alleged arrow debt, they refuse to give any detail other than amount allegedly owed. Received this pathetic response from restons - Re: Arrow Global Limited v. Yourself Original Creditor and Product Type: Santander - Asda Store Card Dear Madam, We write further to receiving your recent email, seeking documentation pursuant to S77-79 of the Consumer Credit Act 1974. We are under no obligation to provide the requested documents to you as we are not the Creditor; we are a firm of solicitors. We have not been informed of any properly constituted request having been made pursuant to the CCA 1974. Even if a properly constituted request has been made, the Credit Agreement is only unenforceable until such a time as the request is complied with. It does not mean that the debt is indefinitely irrecoverable. Your email is written in a format that we are familiar with and that is circulated on consumer based websites. You may be encouraged to use this template in order to avoid the repayment of a legitimate debt. It is our belief that you do not fully understand the nature of the allegations raised within your email. We trust this clarifies our position. We now require your proposals towards the outstanding balance. As such, please complete a financial statement on our website at restons by no later than 13 April 2017; failing which, we are instructed to issue legal proceedings against you. Yours Sincerely Miss N Didsbury ---- anyone give me the best way to respond to this claptrap, needless to say they haven't responded within the statutory time limit to the cca request. appreciate the help if poss, i'm helping a disabled friend who can't take their harrassment any more.

-

Hi All, Like many others on this forum, I've been having a lot of trouble with Harlands/CRS/X4L and wish for it to stop. I've been putting off posting here for a while and simply been following the advice given to everyone else by ignoring the threats from CRS and Harlands and replying in writing. I signed up for a 12-month contract on the 3rd November 2015, and after 12 months decided to cancel my direct debit on the 22nd November 2016 after fulfilling my 12-month obligation. Initially I ignored the letters from Harlands demanding payment, however after they threatened to pass my 'debt' of £171 onto CRS, I decided to reply with a letter to them explaining that I'd fulfilled my 12-month obligation but offered to pay the £9.99 to cover the cancellation period which I had missed, and to stop further demands otherwise they'd be reported to TS etc, etc. In the meantime, my 'debt' was passed onto CRS, and Harlands replied with a letter simply stating that they could not cancel the agreement as they were simply the direct debit company acting on their behalf and to get in touch with X4L directly. So I did just that, basically sending the same letter to X4L head offices, offering to pay the £9.99 but nothing more, and again to stop CRS/Harlands contacting my otherwise I'd report them to TS and the CMA. However, on Tuesday I received this response via email: I'm a bit confused by all of this as they just seem to be passing the buck onto one another, and I'm a bit confused as to what steps I should take next, as CRS have since begun Texting me and sending me Emails demanding I ring them. Anything I should say to X4L in response to this? Any advice would be GREATLY appreciated. Many thanks

Hi All, Like many others on this forum, I've been having a lot of trouble with Harlands/CRS/X4L and wish for it to stop. I've been putting off posting here for a while and simply been following the advice given to everyone else by ignoring the threats from CRS and Harlands and replying in writing. I signed up for a 12-month contract on the 3rd November 2015, and after 12 months decided to cancel my direct debit on the 22nd November 2016 after fulfilling my 12-month obligation. Initially I ignored the letters from Harlands demanding payment, however after they threatened to pass my 'debt' of £171 onto CRS, I decided to reply with a letter to them explaining that I'd fulfilled my 12-month obligation but offered to pay the £9.99 to cover the cancellation period which I had missed, and to stop further demands otherwise they'd be reported to TS etc, etc. In the meantime, my 'debt' was passed onto CRS, and Harlands replied with a letter simply stating that they could not cancel the agreement as they were simply the direct debit company acting on their behalf and to get in touch with X4L directly. So I did just that, basically sending the same letter to X4L head offices, offering to pay the £9.99 but nothing more, and again to stop CRS/Harlands contacting my otherwise I'd report them to TS and the CMA. However, on Tuesday I received this response via email: I'm a bit confused by all of this as they just seem to be passing the buck onto one another, and I'm a bit confused as to what steps I should take next, as CRS have since begun Texting me and sending me Emails demanding I ring them. Anything I should say to X4L in response to this? Any advice would be GREATLY appreciated. Many thanks -

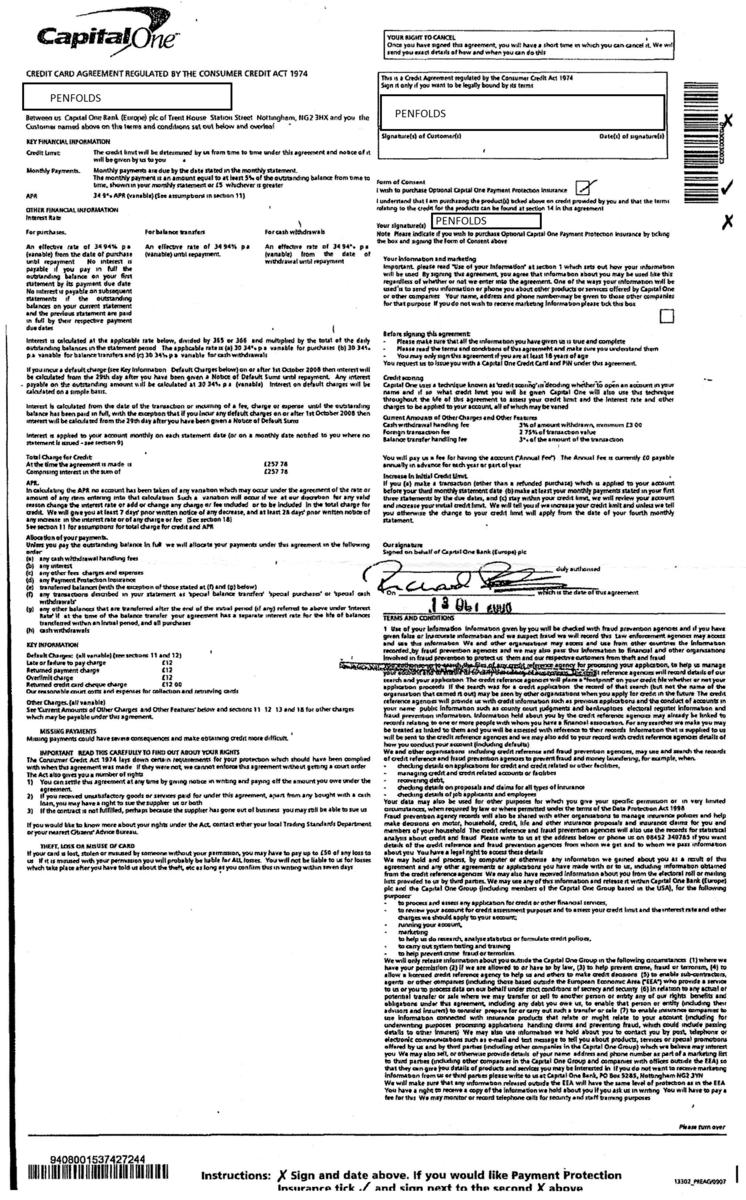

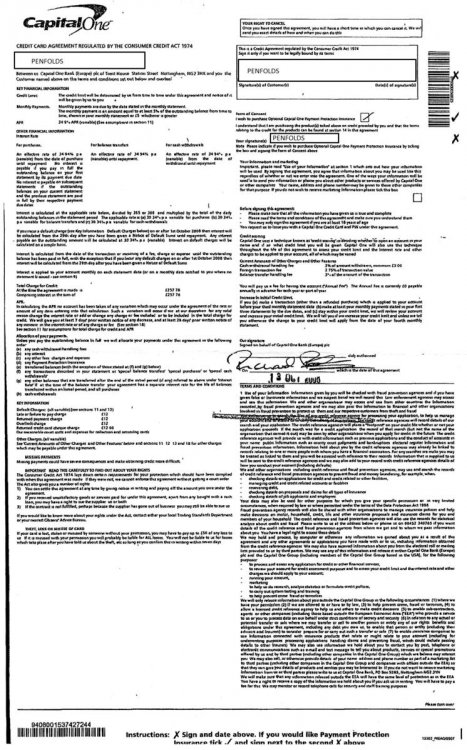

Hi All, I have recently defended a claim by Shoosmiths on behalf of Capquest for a Cpaital One credit card taken out in Oct 2008, the last payment made was in Jan 2012. The claim was stayed at the end of Jan 2017 after filing a defence. Before filing the defence Capquest was sent a CCA request, a copy was also sent to Shoosmiths with a CPR31.14 request, which Shoosmiths remain in breach of. However today Capquest has sent a response to the CCA request (attached). They have also sent somebody elses application for a Barclays Sky Card which includes their name, address, DOB, household income, home, mobile and work telephone numbers and applicants signature. Any advice greatly appreciated, please advise if defence or CPR 31.14 request needs uploading. Thanks Penfolds

Hi All, I have recently defended a claim by Shoosmiths on behalf of Capquest for a Cpaital One credit card taken out in Oct 2008, the last payment made was in Jan 2012. The claim was stayed at the end of Jan 2017 after filing a defence. Before filing the defence Capquest was sent a CCA request, a copy was also sent to Shoosmiths with a CPR31.14 request, which Shoosmiths remain in breach of. However today Capquest has sent a response to the CCA request (attached). They have also sent somebody elses application for a Barclays Sky Card which includes their name, address, DOB, household income, home, mobile and work telephone numbers and applicants signature. Any advice greatly appreciated, please advise if defence or CPR 31.14 request needs uploading. Thanks Penfolds

-

In 1996, I applied for the then student loan for as 2 years course. Once I finished my University, and for a long while, I didn't get any jobs where my earning reached the threshold necessary to start paying it back. I then moved to Australia and live there almost close to 4 years. I hadn't heard anything from the SLC (Student Loan Company) since 1997. When I got back from Australia, I suffered a stroke and since then I have completely forgotten about this loan. However, last week, I got a letter making demands to pay the loan back? Isn't this supposd to be statute barred? (No communcations since 1997?) Also I am going to be 51 and I was under the impression that the loan gets written off once you are that age? The long and the short of it is that my daughter needs to apply for a student loan and my wife has been able to fill-in her side and I am supposed to do mine, but it keep saying error and that I must contact them by phone. I am not sure what to do next? Is this statute barred or not? Thank you for your help

-

I am a defendant in a fast track case. I have the other parties documents I requested copies of from their disclosure by list. There are other docs I know of the existence of and want the other party to disclose them as I think they have left them out because they will hurt their case. I have written to them requesting these be disclosed but have not heard back or received supplemental disclosure of these docs. I don't expect to hear back as they refuse to communicate with me regarding this litigation. I am planning to apply for a Specific Disclosure order and cannot find much guidance online on how to go about this. I want them to disclose specific documents, rather than to do an additional search as I think these should have been found and disclosed within the search they already carried out. There are 11 docs in total I want them to disclose. Some of the docs are mentioned by them in emails they disclosed, some are police records they can get through a subject access request, they have disclosed the Crime Ref numbers of these incidents and referred to them in letters they disclosed. My questions are: 1. What do I put in the draft order? 2. What do I put in my supporting evidence/information to support the application? 3. How do I refer to the places that bought these documents existence to light? Many thanks

I am a defendant in a fast track case. I have the other parties documents I requested copies of from their disclosure by list. There are other docs I know of the existence of and want the other party to disclose them as I think they have left them out because they will hurt their case. I have written to them requesting these be disclosed but have not heard back or received supplemental disclosure of these docs. I don't expect to hear back as they refuse to communicate with me regarding this litigation. I am planning to apply for a Specific Disclosure order and cannot find much guidance online on how to go about this. I want them to disclose specific documents, rather than to do an additional search as I think these should have been found and disclosed within the search they already carried out. There are 11 docs in total I want them to disclose. Some of the docs are mentioned by them in emails they disclosed, some are police records they can get through a subject access request, they have disclosed the Crime Ref numbers of these incidents and referred to them in letters they disclosed. My questions are: 1. What do I put in the draft order? 2. What do I put in my supporting evidence/information to support the application? 3. How do I refer to the places that bought these documents existence to light? Many thanks -

On the 20th September I posted off nine CCA requests all by signed for post. Of these only one company NCO (Amex ) have sent a copy of the CCA which I posted up under the AMEX sub forum. Two have replied and said they have asked the original creditors to supply the CCA and one has returned my request and postal order and asked me to write to the creditor directly. So five have not responded at all, what is my next move ? Is there a template letter I can send ? Mine is outdated as it has a reference to the defunct OFT. Thanks Everett.

-

I took out a Unsecured Personal Loan with Halifax online in December 2011. I was NEVER asked questions like, can you afford the payments, are you employed/unemployed, and I certainly was not asked about my income. This have got so bad I am currently on an IVA - Halifax increased the IVA from 5 years to 6 years forcing me to pay for longer. I am now wondering if bankruptcy is the best option. Do I have a claim that Halifax lent to me irresponsibly without going through my finances first?

I took out a Unsecured Personal Loan with Halifax online in December 2011. I was NEVER asked questions like, can you afford the payments, are you employed/unemployed, and I certainly was not asked about my income. This have got so bad I am currently on an IVA - Halifax increased the IVA from 5 years to 6 years forcing me to pay for longer. I am now wondering if bankruptcy is the best option. Do I have a claim that Halifax lent to me irresponsibly without going through my finances first? -

Good day all Just one question I have emigrated to SE Asia. I wish to get all my charges back from the bank but I will need to SAR them. I know it is 40 days from the date of posting but the post takes about 21 days to arrive from this country. Do the 40 days rule still come into it and when I request the SAR should I ask them to include the Proof Of Posting slip with the SAR to ensure they don't get more days than they should. Might seem a little petty but the bank have been very petty with me over the years and I estimate around £3,000 of charges from Bank accounts, Loan Accounts and Mortgage Many thanks in advance.

-

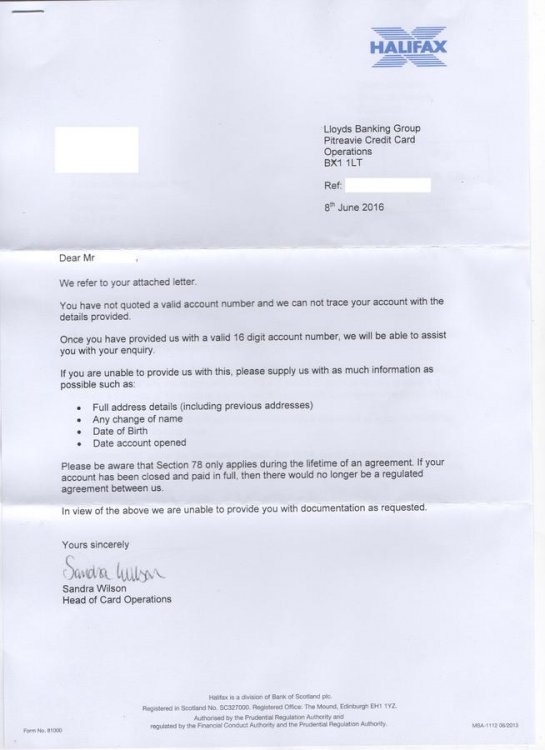

Good afternoon I have today received a response from IDEM after sending them a CCA letter regarding a HSBC credit card They have sent me a reconstituted copy and statement and their letter says that this is all they need to provide and that the debt once again becomes enforceable. There is nothing enclosed that shows my signature. is this now enforceable without the signature and if not what should my next move be Many thanks

-

Hi please see below the response from BH airlines to my delay flight claim - seems to be saying, yes the aircraft was broke but we are only a charter company so tough! Also interesting interpretation of BH holidays terms and conditions. Whats next then SC court? any views gratefully received: Thank you for contacting BH AIR Customer Service Department and thus giving us the chance to review your complaint. Thank you for your patience while the case was being reviewed. First of all, we would like to apologize for the inconveniences you faced due to the delay of your flight. We do realize that any delay could be quite frustrating and we strive to avoid such occurrences. Unfortunately, delays in aviation do happen and in such cases we try to at least minimize them as much as possible. We would like to take this opportunity to explain that your return flight was delayed due to a combination of factors which made it very difficult for the airline's ground-handling agent to predict how long it would be delayed for. We can advise that your flight was unfortunately adversely affected by a series of cumulative delays to the aircraft on earlier rotations. The root cause of your delay was a technical problem to the aircraft on a previous rotation. We naturally regret to hear that the end of your holiday was marred by the above delay. *We can advise that the track record of BH Airlines on timekeeping is very good, but unfortunately sometimes delays do occur for reasons beyond our control. As a charter airline BH Air has less flexibility than other airlines (such as e.g. Lufthansa or Air France) to replace an aircraft in order to comply with its initial schedule. Preventing this delay would have led us to making „intolerable sacrifices” in the light of the capacities of BH Air’s undertaking at the time of the flight, which sacrifices (as per the rationale of the European court judgment on Case C-294/10 (Eglītis-Ratnieks v. Latvijas Republikas Ekonomikas ministrija) we have no legal obligation to make. Evident from the above, the delay of the flight was caused by circumstances which we could not avoid even where we took all reasonable measures within the capacity of our airline. Furthermore, we would like to advise you that BH Air operated the flight on the basis of an aircraft lease arrangement but not a contract of carriage with you and the members of your family as passengers. The flight schedule announced was for reference only. As stated on Balkan Holidays website – flight timings and routings are only provisional and may be subject to change! Hence, the Airline had no contractual obligation vis-à-vis you and your family to comply with any specific flight schedule and may not be responsible for any flight delay. For that reason and reasons mentioned above, we may not honour your claim for compensation under Regulation No 261/2004 or otherwise. That being said, we would like to take this one last chance to apologize for all inconveniences caused. We always strive to give our passengers only the best customer service and so your feedback as it is highly appreciated. We hope that they will give us the chance to welcome you on board our aircraft in the future and give you the customer service you deserve! Kindest regards, BH Air Claims Team

Hi please see below the response from BH airlines to my delay flight claim - seems to be saying, yes the aircraft was broke but we are only a charter company so tough! Also interesting interpretation of BH holidays terms and conditions. Whats next then SC court? any views gratefully received: Thank you for contacting BH AIR Customer Service Department and thus giving us the chance to review your complaint. Thank you for your patience while the case was being reviewed. First of all, we would like to apologize for the inconveniences you faced due to the delay of your flight. We do realize that any delay could be quite frustrating and we strive to avoid such occurrences. Unfortunately, delays in aviation do happen and in such cases we try to at least minimize them as much as possible. We would like to take this opportunity to explain that your return flight was delayed due to a combination of factors which made it very difficult for the airline's ground-handling agent to predict how long it would be delayed for. We can advise that your flight was unfortunately adversely affected by a series of cumulative delays to the aircraft on earlier rotations. The root cause of your delay was a technical problem to the aircraft on a previous rotation. We naturally regret to hear that the end of your holiday was marred by the above delay. *We can advise that the track record of BH Airlines on timekeeping is very good, but unfortunately sometimes delays do occur for reasons beyond our control. As a charter airline BH Air has less flexibility than other airlines (such as e.g. Lufthansa or Air France) to replace an aircraft in order to comply with its initial schedule. Preventing this delay would have led us to making „intolerable sacrifices” in the light of the capacities of BH Air’s undertaking at the time of the flight, which sacrifices (as per the rationale of the European court judgment on Case C-294/10 (Eglītis-Ratnieks v. Latvijas Republikas Ekonomikas ministrija) we have no legal obligation to make. Evident from the above, the delay of the flight was caused by circumstances which we could not avoid even where we took all reasonable measures within the capacity of our airline. Furthermore, we would like to advise you that BH Air operated the flight on the basis of an aircraft lease arrangement but not a contract of carriage with you and the members of your family as passengers. The flight schedule announced was for reference only. As stated on Balkan Holidays website – flight timings and routings are only provisional and may be subject to change! Hence, the Airline had no contractual obligation vis-à-vis you and your family to comply with any specific flight schedule and may not be responsible for any flight delay. For that reason and reasons mentioned above, we may not honour your claim for compensation under Regulation No 261/2004 or otherwise. That being said, we would like to take this one last chance to apologize for all inconveniences caused. We always strive to give our passengers only the best customer service and so your feedback as it is highly appreciated. We hope that they will give us the chance to welcome you on board our aircraft in the future and give you the customer service you deserve! Kindest regards, BH Air Claims Team -

Received this in the post today Along with my original CCA letter. Any advice? I dont know what details they have as I have moved a number of times since then. If it was a credit card I would have thought capquest would have the details Just double checked on my Noodle account. It is listed in my closed accounts (if it is that one) and is shown as settled in Dec 2010 with no missed payments. Edit: it cant be that one on the account as my card limit was £1000 and have been paying £6.52 for years and my outstanding balance is shown as £1211.14 and the account is settled properly. Edit 2: Is it worth doing a SAR with CapQuest to see what they have on file and amounts?

-

Good afternoon I have received the attached response following a CCA letter. Is this contact or not as they are now saying the debt has become enforceable. If not correct what do I need to do now. Below is my original post re this Many thanks http://www.consumeractiongroup.co.uk/forum/showthread.php?467679-Unable-to-pay-DMP-as-now-unemployed CCA return.pdf

-

Hi, I sent a CCA request to the DC/Solicitor in feb 2016 Just received a response in October which is basically a copy of the online application? no agreement on terms or repayments just my address details, job details, credit limit, no signed agreement Is the above enforceable? is there a letter I can send back to this? the amount is for £6k+ - any help much appreciated

-

Hi all Hoping you may be able to help me, I was stupidly heavily in debt in 2011 with 16 different payday loan companies (all clear and debt free since then) , I am now in the process of emailing them all regarding irresponsible lending, so far I have had generic responses but nothing further at the moment. I have received this from 247 moneybox and would like some advice on how to respond - not shocked with the response to be honest! Dear.... Hope that you are well. Please find below a copy of our complaints procedure. We are aware that there are many forums and templated letters available on the internet to exploit any previous credit commitments under the wholly subjective banner of affordability. We have seen some legitimate claims upheld in the press such as with the lender Cash Genie. However, to compare our actions with their reported behaviour is inappropriate. We are confident that the required assessments were carried out prior to the advance of all loans. We have had relatively few instances where customers have ultimately look to take recourse with the Financial Ombudsman Service and our record there is good as we are able to substantiate fully the information on which lending decisions were based. Our relationship was based on responsible lending in addition to responsible borrowing. We provided you with all the facts about our product and the charges and costs involved. We treated you as a rational individual able to make a credible decision as to whether to borrow or not. For our part of the relationship we acted on the information available to us at the time and the prevailing regulations and guidance at the time. I am your personal account manager and would be happy to discuss any of the above with you over the phone. I am available on 0207 183 8078 between 08:30 and 18:00 Monday to Friday. If you would prefer, please do feel free to provide a number and time at which I can reach you directly. Kind regards, Shahan Warning: Late repayment can cause you serious money problems. For help, go to moneyadviceservice.org.uk 247Moneybox 20-22 Wenlock Road London N1 7GU Complaints Procedure Customer satisfaction is of utmost importance to 247Moneybox. Please do not hesitate to contact us if you are dissatisfied with our service in anyway. We hope that it never comes to this, however should you wish to make a formal complaint in writing, please address your letter to: Customer Services Department 247Moneybox 20-22 Wenlock Road London N1 7GU If you have a complaint, please write to our Customer Services Department at the address set out above, e-mail us at Upon receipt of your complaint we will do our best to resolve your complaint by the end of the next business day. If we can't do this, we will send you a prompt written acknowledgement of your complaint within 5 working days and tell you who is dealing with it. In addition, we will provide you with a copy of our complaints procedure. If we need to investigate your complaint further to respond fully, we will tell you and keep you regularly updated. We will send you our final response as soon as possible but within eight weeks of receiving your complaint. Our final response will explain that you will have ultimate recourse to the Financial Ombudsman Service if you remain dissatisfied. We will enclose a leaflet (or provide a link to information) from the Financial Ombudsman Service with our final response to assist you if you decide to pursue this further course of action. If looking to do so, you will need to contact the Financial Ombudsman Service within six months of receiving our final response. If you want to make a complaint to our trade association (BCCA), their contact details can be found at the end of this procedure. Our trade association will liaise with us to ensure your complaint is investigated fully and a response is sent out to you.

Hi all Hoping you may be able to help me, I was stupidly heavily in debt in 2011 with 16 different payday loan companies (all clear and debt free since then) , I am now in the process of emailing them all regarding irresponsible lending, so far I have had generic responses but nothing further at the moment. I have received this from 247 moneybox and would like some advice on how to respond - not shocked with the response to be honest! Dear.... Hope that you are well. Please find below a copy of our complaints procedure. We are aware that there are many forums and templated letters available on the internet to exploit any previous credit commitments under the wholly subjective banner of affordability. We have seen some legitimate claims upheld in the press such as with the lender Cash Genie. However, to compare our actions with their reported behaviour is inappropriate. We are confident that the required assessments were carried out prior to the advance of all loans. We have had relatively few instances where customers have ultimately look to take recourse with the Financial Ombudsman Service and our record there is good as we are able to substantiate fully the information on which lending decisions were based. Our relationship was based on responsible lending in addition to responsible borrowing. We provided you with all the facts about our product and the charges and costs involved. We treated you as a rational individual able to make a credible decision as to whether to borrow or not. For our part of the relationship we acted on the information available to us at the time and the prevailing regulations and guidance at the time. I am your personal account manager and would be happy to discuss any of the above with you over the phone. I am available on 0207 183 8078 between 08:30 and 18:00 Monday to Friday. If you would prefer, please do feel free to provide a number and time at which I can reach you directly. Kind regards, Shahan Warning: Late repayment can cause you serious money problems. For help, go to moneyadviceservice.org.uk 247Moneybox 20-22 Wenlock Road London N1 7GU Complaints Procedure Customer satisfaction is of utmost importance to 247Moneybox. Please do not hesitate to contact us if you are dissatisfied with our service in anyway. We hope that it never comes to this, however should you wish to make a formal complaint in writing, please address your letter to: Customer Services Department 247Moneybox 20-22 Wenlock Road London N1 7GU If you have a complaint, please write to our Customer Services Department at the address set out above, e-mail us at Upon receipt of your complaint we will do our best to resolve your complaint by the end of the next business day. If we can't do this, we will send you a prompt written acknowledgement of your complaint within 5 working days and tell you who is dealing with it. In addition, we will provide you with a copy of our complaints procedure. If we need to investigate your complaint further to respond fully, we will tell you and keep you regularly updated. We will send you our final response as soon as possible but within eight weeks of receiving your complaint. Our final response will explain that you will have ultimate recourse to the Financial Ombudsman Service if you remain dissatisfied. We will enclose a leaflet (or provide a link to information) from the Financial Ombudsman Service with our final response to assist you if you decide to pursue this further course of action. If looking to do so, you will need to contact the Financial Ombudsman Service within six months of receiving our final response. If you want to make a complaint to our trade association (BCCA), their contact details can be found at the end of this procedure. Our trade association will liaise with us to ensure your complaint is investigated fully and a response is sent out to you. -

HI I sent CCA to Lowells for 3 different accounts. I had no response this was in 2014. I have now received pre-legal assessment letters. I have kept the post office recipts as I sent recoreded with 1 pound postal order. I also sent to Bryan Carter as well. (he respoded was on hold until could get info) never heard back from any of the creditors until now??? How do I prove I sent CCA if it goes to court? and do I need to send another CCA as its been 2 years?? Any help thanks

HI I sent CCA to Lowells for 3 different accounts. I had no response this was in 2014. I have now received pre-legal assessment letters. I have kept the post office recipts as I sent recoreded with 1 pound postal order. I also sent to Bryan Carter as well. (he respoded was on hold until could get info) never heard back from any of the creditors until now??? How do I prove I sent CCA if it goes to court? and do I need to send another CCA as its been 2 years?? Any help thanks -

Thanks for everything you do here – I hope you might be able to help with Opos and Kapama. Although I've read lots of threads about them, I'm struggling with some particular parts of my situation. Brief background – in 2013, lots of foolish unaffordable payday loans to pay more payday loans, including a written off Wonga. Most now dealt with, with my credit file looking like it will be clear by 2020. A few monthly payments still going, including to Opos for a MiniCredit debt purchased by Kapama - notice of assignment issued in late January 2015. The initial Minicredit loan was £450, with Kapama/Opos demanding over £1600. I've been making £20 monthly payments for 18 months, and so have nearly paid the original balance. There is no default listed for MiniCredit on my credit file. The loan is listed as an 'advance against income' with Kapama as the lender and an arrangement to pay – with over £1200 outstanding. I've come to a point where I'm reviewing my financial situation in mind of - first, a reduced income coming up because I'll be retraining in a new career - second, I want to be in a position to get a mortgage when my file is clear. That in mind, the £20 a month is no longer affordable, but as a default hasn't been recorded on that loan, I'm really concerned Opos/Kapama would register one if I stopped the arrangement now, setting back my file several (important) years. Having read through forums and taken a friend's advice, I sent them an email last week referring to the FCA ruling regarding MiniCredit's lending (link not here) but have not received a reply. The crux of that was that if the debt hadn't been transferred to Kapama by December 2014 it should be written off –*they say it was, but I have the notice of assignment – which was sent by email at the end of January 2015. The main questions I have: Can they register a default now? Should/can I stop making payments? They're currently being taken from a debit card by Opos. How should I proceed? Should I continue to complain on the grounds of that FCA ruling? Do you have any contacts at Opos/Kapama better than the general enquires address? I know there's a bit of duplication there - but as I've paid back so much of the original loan, the credit file listing and the potential relevance of MiniCredit's shutdown, I'm really not sure where I stand. Thanks in advance – I really appreciate it.

Thanks for everything you do here – I hope you might be able to help with Opos and Kapama. Although I've read lots of threads about them, I'm struggling with some particular parts of my situation. Brief background – in 2013, lots of foolish unaffordable payday loans to pay more payday loans, including a written off Wonga. Most now dealt with, with my credit file looking like it will be clear by 2020. A few monthly payments still going, including to Opos for a MiniCredit debt purchased by Kapama - notice of assignment issued in late January 2015. The initial Minicredit loan was £450, with Kapama/Opos demanding over £1600. I've been making £20 monthly payments for 18 months, and so have nearly paid the original balance. There is no default listed for MiniCredit on my credit file. The loan is listed as an 'advance against income' with Kapama as the lender and an arrangement to pay – with over £1200 outstanding. I've come to a point where I'm reviewing my financial situation in mind of - first, a reduced income coming up because I'll be retraining in a new career - second, I want to be in a position to get a mortgage when my file is clear. That in mind, the £20 a month is no longer affordable, but as a default hasn't been recorded on that loan, I'm really concerned Opos/Kapama would register one if I stopped the arrangement now, setting back my file several (important) years. Having read through forums and taken a friend's advice, I sent them an email last week referring to the FCA ruling regarding MiniCredit's lending (link not here) but have not received a reply. The crux of that was that if the debt hadn't been transferred to Kapama by December 2014 it should be written off –*they say it was, but I have the notice of assignment – which was sent by email at the end of January 2015. The main questions I have: Can they register a default now? Should/can I stop making payments? They're currently being taken from a debit card by Opos. How should I proceed? Should I continue to complain on the grounds of that FCA ruling? Do you have any contacts at Opos/Kapama better than the general enquires address? I know there's a bit of duplication there - but as I've paid back so much of the original loan, the credit file listing and the potential relevance of MiniCredit's shutdown, I'm really not sure where I stand. Thanks in advance – I really appreciate it. -

Hi Everyone , i was hoping for some advice , after looking through documentation it seems i was REALLY naive when i took out the credit for my car , i had finance on 10.12.2014 for a renault megane 2007 1.9 DCI To cut it short they charged me £2,350 for the car and the loan amount by credit for cars was £5500 !! i was paying £150 a month , ive paid £2,300 off it , but with all the numerous problems ive had to pay for with the car from the start i stopped paying last month last payment i made was on 17th june and i had to pay via "shopper@worldpay.com a Guy from avelo emailed me 10th june saying i needed to contact them urgently to discuss arrears (he was a negotiations case handler) i gave him a email back and told them when id make a payment he replied saying "sorry our systems have not been updated and could i ask how you will be making a payment ? and can we have your current phone number" i didnt give him my number but id updated them with my new address and he replied back "thank you ive updated our systems and "are you willing to continue paying £175 per month starting from next month?" i never replied then today i had a different person who was "Trainee Case Handler" asking me to contact the office to discuss arrears (the same like before) The reason i am not making payments is because i cannot afford to , the advice im looking for is Can they take the car away from me ? (on the documents i signed it stated that they could not take the goods if payments totalling £1997 have been made then they may not take the goods back against my wishes unless we get a court order) this is the Credit4Cars agreement i signed 2 years ago , also i have noticed that they charged me £375 for a "Stronghold Protector payment assurance system" they said they can disable my car with it as they reckon a device has been attached , the reason why i say they reckon because when i was late with a payment with C4C they threatened me they were going to disable it , i was not in a good way then and snapped back and replied "be my guest as i dont care" (they did this 3 times to me but never disabled it and also when i asked a mechanic to look for it he said he couldnt see anything , when i chose the car the people at trade center where i bought the car said because i have a tracking device my insurance would go down now when i queried with them what make it was for my insurance they would not tell me so i was paying a LOT more than i should have for my insurance , sorry to have gone on and on its just that the cars wheel bearing has gone and it will cost me £200 tomorrow and if they are going to take back the vehicle then i wont get it fixed , thanks for your time any advice appreciated

Hi Everyone , i was hoping for some advice , after looking through documentation it seems i was REALLY naive when i took out the credit for my car , i had finance on 10.12.2014 for a renault megane 2007 1.9 DCI To cut it short they charged me £2,350 for the car and the loan amount by credit for cars was £5500 !! i was paying £150 a month , ive paid £2,300 off it , but with all the numerous problems ive had to pay for with the car from the start i stopped paying last month last payment i made was on 17th june and i had to pay via "shopper@worldpay.com a Guy from avelo emailed me 10th june saying i needed to contact them urgently to discuss arrears (he was a negotiations case handler) i gave him a email back and told them when id make a payment he replied saying "sorry our systems have not been updated and could i ask how you will be making a payment ? and can we have your current phone number" i didnt give him my number but id updated them with my new address and he replied back "thank you ive updated our systems and "are you willing to continue paying £175 per month starting from next month?" i never replied then today i had a different person who was "Trainee Case Handler" asking me to contact the office to discuss arrears (the same like before) The reason i am not making payments is because i cannot afford to , the advice im looking for is Can they take the car away from me ? (on the documents i signed it stated that they could not take the goods if payments totalling £1997 have been made then they may not take the goods back against my wishes unless we get a court order) this is the Credit4Cars agreement i signed 2 years ago , also i have noticed that they charged me £375 for a "Stronghold Protector payment assurance system" they said they can disable my car with it as they reckon a device has been attached , the reason why i say they reckon because when i was late with a payment with C4C they threatened me they were going to disable it , i was not in a good way then and snapped back and replied "be my guest as i dont care" (they did this 3 times to me but never disabled it and also when i asked a mechanic to look for it he said he couldnt see anything , when i chose the car the people at trade center where i bought the car said because i have a tracking device my insurance would go down now when i queried with them what make it was for my insurance they would not tell me so i was paying a LOT more than i should have for my insurance , sorry to have gone on and on its just that the cars wheel bearing has gone and it will cost me £200 tomorrow and if they are going to take back the vehicle then i wont get it fixed , thanks for your time any advice appreciated -

To cut a long story short.... I worked as a freelance contractor for a firm for 6 months in 2015. The long term contract was eventually cancelled by mutual consent and in October. In December I was sent a letter from my client stating that they strongly believed that I had not fulfilled any of my duties under the contract and wanted £4,000 withn 30 days or were threatening to take me to court for £12,000 + I spoke to a solicitor who advised me that unless it was a letter from a solicitors on the clients behalf, then I should not respond as the client was probably "fishing" to see if I would pay up. I received another letter in March, stating the same thing, at which point I requested a Subject Access Request (I did this as everything I did was controlled by work email I had no access to, including my contract and other personal documents) I received the SAR response as a set of transcripts of emails and other documentation (which according to the SAR code of practice is totally acceptable), HOWEVER also included was personal notes inbetween the emails, one of which states that due to a situation that occured the client thought I was going to use certain information to blackmail them. Yes they actually wrote that on the SAR response paperwork, twice, in two different places among the 36 pages of response I received. Now, my question is, are they allowed to comment with personal opinion and notation on an SAR response or should it be just the facts taken from documentation? I cannot find anything in my searches and thought one of you fine people on here would know. If not, what would be my next step in responding to it other than to ask for the information without the notation? Thanks in advance

To cut a long story short.... I worked as a freelance contractor for a firm for 6 months in 2015. The long term contract was eventually cancelled by mutual consent and in October. In December I was sent a letter from my client stating that they strongly believed that I had not fulfilled any of my duties under the contract and wanted £4,000 withn 30 days or were threatening to take me to court for £12,000 + I spoke to a solicitor who advised me that unless it was a letter from a solicitors on the clients behalf, then I should not respond as the client was probably "fishing" to see if I would pay up. I received another letter in March, stating the same thing, at which point I requested a Subject Access Request (I did this as everything I did was controlled by work email I had no access to, including my contract and other personal documents) I received the SAR response as a set of transcripts of emails and other documentation (which according to the SAR code of practice is totally acceptable), HOWEVER also included was personal notes inbetween the emails, one of which states that due to a situation that occured the client thought I was going to use certain information to blackmail them. Yes they actually wrote that on the SAR response paperwork, twice, in two different places among the 36 pages of response I received. Now, my question is, are they allowed to comment with personal opinion and notation on an SAR response or should it be just the facts taken from documentation? I cannot find anything in my searches and thought one of you fine people on here would know. If not, what would be my next step in responding to it other than to ask for the information without the notation? Thanks in advance -

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) At present, High Court Enforcement agents are only able to enforce judgments if they relate to non consumer credit debts and have a value of over £600. Judgements relating to consumer credit debts (typically, a debt relating to a bank loan, credit card debt, catalogue debt or any other finance agreement) may only be enforced by a County Court Bailiff. The High Court Enforcement industry has campaigned for many years for the law to be changed to allow them to enforce judgments in relation to 'consumer credit debts'. Earlier this year, the High Court Enforcement industry had their hopes raised that the law will be changed with the release of the Ministry of Justice's Civil Courts Structure Review that was chaired by Lord Justice Briggs. In the review, Justice Briggs stated that County Court enforcement is presently: “heavily localised, paper based, prone to error in form filling, and widely perceived to be slow, ineffective and expensive” A public Consultation was issued (now closed) and in the next few weeks a final report is due to be published. Today the Money Advice Trust issued the following release: http://www.moneyadvicetrustblog.org/2016/07/22/no-enforced-changes-some-thoughts-on-the-lord-justice-briggs-review/ A copy of their response to the Consultation is below: http://www.moneyadvicetrust.org/SiteCollectionDocuments/Policy%20consultation%20responses/Unilateral%20responses/Money%20Advice%20Trust%20response%20to%20the%20Civil%20Courts%20Structure%20Review%20Interim%20Report%20consultation%20paper.pdf

At present, High Court Enforcement agents are only able to enforce judgments if they relate to non consumer credit debts and have a value of over £600. Judgements relating to consumer credit debts (typically, a debt relating to a bank loan, credit card debt, catalogue debt or any other finance agreement) may only be enforced by a County Court Bailiff. The High Court Enforcement industry has campaigned for many years for the law to be changed to allow them to enforce judgments in relation to 'consumer credit debts'. Earlier this year, the High Court Enforcement industry had their hopes raised that the law will be changed with the release of the Ministry of Justice's Civil Courts Structure Review that was chaired by Lord Justice Briggs. In the review, Justice Briggs stated that County Court enforcement is presently: “heavily localised, paper based, prone to error in form filling, and widely perceived to be slow, ineffective and expensive” A public Consultation was issued (now closed) and in the next few weeks a final report is due to be published. Today the Money Advice Trust issued the following release: http://www.moneyadvicetrustblog.org/2016/07/22/no-enforced-changes-some-thoughts-on-the-lord-justice-briggs-review/ A copy of their response to the Consultation is below: http://www.moneyadvicetrust.org/SiteCollectionDocuments/Policy%20consultation%20responses/Unilateral%20responses/Money%20Advice%20Trust%20response%20to%20the%20Civil%20Courts%20Structure%20Review%20Interim%20Report%20consultation%20paper.pdf