Search the Community

Showing results for tags 'dpa'.

-

Hi, Please see attached. Your comments would be appreciated. convert-jpg-to-pdf.net_2018-05-04_20-06-00.pdf

-

Having some issues with O2 as of March this year as they have decided to link 2 accounts for another person with the same name and DOB as myself, however this other person has a middle name and i do not. I do not have any accounts with O2. 18/3/18 Received letter stating i was in breach of contract for not paying my O2 bill. 22/3/18 Received letter telling me they had stopped me making calls and texts. 23/3/18 Checked call credit report and O2 had already linked my address with the debtors in Janurary 18 and had both accounts listed. 23/3/18 Emailed call credit stating the incorrect information. 2/4/18 Received letter from O2 telling me they had disconnected my phone. 7/4/18 Requested credit report from Experian. 20/4/18 received letter from call credit stating that O2 had not bothered to respond to them, and are unable to amend the entries to my credit file without the permission of O2. 20/4/18 same letter as above also stating that the disputed entries will be supressed from my credit file, however, O2 can remove the suppression at any time. 21/4/18 complaint letter sent to Experian stating the incorrect accounts and linked addresses. 17/5/18 Received email from Experian telling me O2 had supplied the following details "The link is correct as the account was registered to the disputed address." 1/5/18 Received letter from Experian stating O2 had removed the accounts but not the linked addresses. 1/5/18 Complaint send to ICO about Experian knowingly registering wrong information on there systems even though it had been proved it was not me O2 were looking for. 5/6/18 sent SAR to Experian 5/6/18 SAR sent to O2 8/6/18 Received letter requesting what specific information i wanted from Experian. 11/6/18 Sent Experian an email stating i wanted the information between themselves and O2 to see what had been said about the matter. 11/6/18 Received email back from Experian stating that they had supplied the information the comparison data sets in the additional information i could request. No information regards conversations about themselves and O2. What O2 have done here is add accounts and linked addresses to a serial debtor on my credit report , opening the floodgates for all of these other companies to jump on the bandwagon adding CCJs , Defaults, Late payment accounts to my credit files. They are refusing to remove the wrong data from my Experian report and as stated above have not even replied to call credit about the issue. No reply as yet from the ICO as they are running 8 weeks behind about the Experian complaint. Next steps to take against O2 if anyone has any suggestions, AGAIN O2 are the ones that have opened the floodgates for all of the other comapnies to throw wrongful information onto my credit files without even bothering to do the correct checks. ***Please also note that my Experian credit report in April stated O2 were the source of the linked address, however my credit file in June states Experian are the source of the linked address*** Something funny going on i think. Thanks

Having some issues with O2 as of March this year as they have decided to link 2 accounts for another person with the same name and DOB as myself, however this other person has a middle name and i do not. I do not have any accounts with O2. 18/3/18 Received letter stating i was in breach of contract for not paying my O2 bill. 22/3/18 Received letter telling me they had stopped me making calls and texts. 23/3/18 Checked call credit report and O2 had already linked my address with the debtors in Janurary 18 and had both accounts listed. 23/3/18 Emailed call credit stating the incorrect information. 2/4/18 Received letter from O2 telling me they had disconnected my phone. 7/4/18 Requested credit report from Experian. 20/4/18 received letter from call credit stating that O2 had not bothered to respond to them, and are unable to amend the entries to my credit file without the permission of O2. 20/4/18 same letter as above also stating that the disputed entries will be supressed from my credit file, however, O2 can remove the suppression at any time. 21/4/18 complaint letter sent to Experian stating the incorrect accounts and linked addresses. 17/5/18 Received email from Experian telling me O2 had supplied the following details "The link is correct as the account was registered to the disputed address." 1/5/18 Received letter from Experian stating O2 had removed the accounts but not the linked addresses. 1/5/18 Complaint send to ICO about Experian knowingly registering wrong information on there systems even though it had been proved it was not me O2 were looking for. 5/6/18 sent SAR to Experian 5/6/18 SAR sent to O2 8/6/18 Received letter requesting what specific information i wanted from Experian. 11/6/18 Sent Experian an email stating i wanted the information between themselves and O2 to see what had been said about the matter. 11/6/18 Received email back from Experian stating that they had supplied the information the comparison data sets in the additional information i could request. No information regards conversations about themselves and O2. What O2 have done here is add accounts and linked addresses to a serial debtor on my credit report , opening the floodgates for all of these other companies to jump on the bandwagon adding CCJs , Defaults, Late payment accounts to my credit files. They are refusing to remove the wrong data from my Experian report and as stated above have not even replied to call credit about the issue. No reply as yet from the ICO as they are running 8 weeks behind about the Experian complaint. Next steps to take against O2 if anyone has any suggestions, AGAIN O2 are the ones that have opened the floodgates for all of the other comapnies to throw wrongful information onto my credit files without even bothering to do the correct checks. ***Please also note that my Experian credit report in April stated O2 were the source of the linked address, however my credit file in June states Experian are the source of the linked address*** Something funny going on i think. Thanks -

Not sure if this is the correct forum,but it's the only 1 closest to my query, it involves an employee. Last week when England knocked out Colombia, there were fans congregating in a town center , blocking the road, and 2 buses were blocked in. Several dozen fans were converging on one of the buses which was immediately outside the pub., rocking it, opening the entrance doors via the outside emergency door button. The driver attempted 3 or 4 times to gently shove a few fans off. 1 fan actually got onto the roof and was jumping on the roof. A harrowing experience for the several passengers on board, some of whom were young women. All the time this was happening, someone was filming the incident. All of a sudden, the video clip is on Youtube. The driver concerned is angry that this video clip is on youtube , uploaded by a local taxi firm. The driver never gave his permission for the video clip to be uploaded or for the drivers face to be shown. The taxi firm did not ask the bus company if they could upload it either. Not only was it embarrassing for the driver at the time of the incident, but it was also a shock for him when he saw the video clip on Youtube, which has gone viral, and has had over 66,000 hits. The bus driver asked me if there is a breach of the Data Protection Act 2018, and/or a breach of the GDPR. As I am not clued up much on both, I cannot give a positive answer So, any help and advice would be greatly appreciated. I will print it off and give it to the employee.

-

11 years ago I was taken seriously ill and due to the illness I lost my job and ended up in a financial mess resulting in my house being repossessed. Thankfully my health has stabalised and I'm now starting to get to grips with my financial mess. Having checked my credit reports I noticed Natwest were reporting missed payments each month on two mortgages and a loan and hadn't recorded any of the defaults or CCJ's. I lodged a complaint with Natwest which they upheld due to inaccurate reporting of my credit file when one mortgage and loan had been paid off with a full a final settlement and the other mortgage had resulted in a repossession. To compensate me for inaccurate reporting over the past 8 years they've sent a cheque for £125 which I don't believe is adequate. However, whats more worrying is that they have now listed the mortgage shortfall as an outstanding mortgage even though the property was repossessed over 7 years ago. While I don't dispute the amount is outstanding I didn't think they could report the outstanding balance once the account had been defaulted and subsequently repossessed. Am I correct or are Natwest allowed to register the mortgage shortfall in this way on my credit file ? Thanks

-

As some of you know Scottish Power (SP) are terrible at everything they do! Story: Friend 1: I helped an SP customer get their account sorted, back-billing issues. Now that's sorted and redress was nice for the customer. Friend 2: I am currently helping sort their back-billing issues, some success so far. Now being smart a SAR was sent to SP for friend 2. In their name only . The data pack duly arrives within the 40 days, some items were missing, a quick email to SP sorted that out. Now its complicated, on listening to the cd's of the phone calls for friend 2, SP have sent friend 2 copies of all friend 1's calls, neither friend know each other, never met nor communicated with each other whatsoever. The only common thing is me. I am not the data subject for either account. So why have SP issued data for friend 1 to friend 2, can friend 2 now complain to the ICO and the Ombudsman in relation to the data breach. It clearly can be heard that the normal security questions being asked and confirmed! Your thoughts please

-

Aviva posted me some very insulting to me marketing material in february so I contacted them to complain. They claimed that I had opted to receive marketing some years before, when i lived at a previous address. After further correspondence where they failed to produce any evidence of htis supposed agreemnt or ticked box (never used web or paper forms to agree to anything) they admitted they did not ahve such an agreement, had mixed my personal data up with another person of a similar name as well and offered me £75 when I had requested £250 as that was a sum courts had agreed was a minimum under persuasive case precedent. The main problem is the peopel who deal with a complaint are limited in what they can offer and do not know much about the DPA or even what other departments have been up to. in my case it was Aviva Insurance UK Ltd that had passed on erroneous personal data to Aviva Equity release Ltd, a separate company, without any authorisation and they finally accepted that this was a breach of the DPA, apologised and have agreed to pay me the £250 demanded to avoid legal action. Next year the law changes on what is deemed consent when ticking (or not) boxes and who they can pass your details to without express consent so hopefully this will become a rarer instance but in the meanwhile if you have a complaint, be persistent, stick to your guns if you are right and dont accept a stock response that they dont have to think about. My complaint got to director level because they didnt initially think they could be wrong, ignored the Vidal Hall v Google decision and blamed me for their errors. You dont have to put up with rubbish from big companies.

Aviva posted me some very insulting to me marketing material in february so I contacted them to complain. They claimed that I had opted to receive marketing some years before, when i lived at a previous address. After further correspondence where they failed to produce any evidence of htis supposed agreemnt or ticked box (never used web or paper forms to agree to anything) they admitted they did not ahve such an agreement, had mixed my personal data up with another person of a similar name as well and offered me £75 when I had requested £250 as that was a sum courts had agreed was a minimum under persuasive case precedent. The main problem is the peopel who deal with a complaint are limited in what they can offer and do not know much about the DPA or even what other departments have been up to. in my case it was Aviva Insurance UK Ltd that had passed on erroneous personal data to Aviva Equity release Ltd, a separate company, without any authorisation and they finally accepted that this was a breach of the DPA, apologised and have agreed to pay me the £250 demanded to avoid legal action. Next year the law changes on what is deemed consent when ticking (or not) boxes and who they can pass your details to without express consent so hopefully this will become a rarer instance but in the meanwhile if you have a complaint, be persistent, stick to your guns if you are right and dont accept a stock response that they dont have to think about. My complaint got to director level because they didnt initially think they could be wrong, ignored the Vidal Hall v Google decision and blamed me for their errors. You dont have to put up with rubbish from big companies. -

In May 2018 the new General Data Protection Regulation will come into force. This is an EU wide regulation and although the UK will be leaving the EU, these new regulations will be implemented. http://tinyurl.com/zqfmm48 The above linkis from the ICO goes into some detail but it isn't very clear as yet. The one major change to consumers is the removal of the £10 fee although companies can charge for extra searches. I'm not 100% sure that the removal of fees relates to medical records as yet. If the NHS cannot charge the usual £50, that will be a big bonus. http://tinyurl.com/zrg22z4

-

Hello all, I was hoping someone here can help me regarding this issue. I took out a loan in 2011 with a Credit Union in Scotland. They have defaulted my credit file with the wrong info, including amount, default date and address. I've had both the ICO and FOS involved in this matter and am now tearing my hair out to get it resolved. A high level timeline of events: In August, I contacted the CU about the default and they gave no indication that this would happen. It was also not reported for 4 years after the fact. In September, I paid outstanding amount. They told me the default would be settled and closed. In October, wrote a letter and called the CU several times. They told me it would be marked as settled by November over the phone, no formal response. In November took to the FOS, couldn't do anything without a final response letter, until 8 weeks had past, and my letter was ignored by the CU. In December contacted the FOS and they sent a letter to the CU. In Jan, followed up with the FOS. Their letter had been ignored. They called called the CU. In Feb, they finally respond to the FOS stating the default was sorted and the FOS sided with them. I responded with a copy of my credit file and told them this was not the case (felt bad for the Girl totally deconstructed her email with DPA legislation etc, she clearly was worried in her response to me). The FOS, as part of the closure, say the default was fair to be recorded after 4 years.. .. guidance from the ICO states 3 - 6 months. I also complained to the ICO. However, the FOS reopened the case because the CU hadn't sorted the default. In March / Apr, Information gathering by myself, the FOS and Experian. In late April, FOS sides with me and awards compensation. ICO finally assign a case advisor. In May, wait two weeks for the response, then the CU say not happy with that, escalate within the FOS and I need to wait for an Ombudsman to be assigned.. .. as it was an investigator who made this decision. Today, ICO respond saying that they can't uphold the complaint as they deal with the org and not the individual, but are willing to be communicated further information. Email in progress.... but they also notify me that CU's aren't regulated under the CCA. So my questions really is... the distress this has caused has been over 9 months. I can't get a new car (which I could lose my job over), I need to sort out the Mortgage for my current residence (which means I could lose my home) and in all honesty I've spent hours on this. What can I do? The FOS is saying it now may take the ombudsman a while to respond. Bringing this whole incident to 10, possibly 11 months. The other thing I'm unsure of is if the CU isn't regulated by the CCA, what can actually be done? How can this be fair processing of consumer data? Thanks in advance and sorry for the long post!

Hello all, I was hoping someone here can help me regarding this issue. I took out a loan in 2011 with a Credit Union in Scotland. They have defaulted my credit file with the wrong info, including amount, default date and address. I've had both the ICO and FOS involved in this matter and am now tearing my hair out to get it resolved. A high level timeline of events: In August, I contacted the CU about the default and they gave no indication that this would happen. It was also not reported for 4 years after the fact. In September, I paid outstanding amount. They told me the default would be settled and closed. In October, wrote a letter and called the CU several times. They told me it would be marked as settled by November over the phone, no formal response. In November took to the FOS, couldn't do anything without a final response letter, until 8 weeks had past, and my letter was ignored by the CU. In December contacted the FOS and they sent a letter to the CU. In Jan, followed up with the FOS. Their letter had been ignored. They called called the CU. In Feb, they finally respond to the FOS stating the default was sorted and the FOS sided with them. I responded with a copy of my credit file and told them this was not the case (felt bad for the Girl totally deconstructed her email with DPA legislation etc, she clearly was worried in her response to me). The FOS, as part of the closure, say the default was fair to be recorded after 4 years.. .. guidance from the ICO states 3 - 6 months. I also complained to the ICO. However, the FOS reopened the case because the CU hadn't sorted the default. In March / Apr, Information gathering by myself, the FOS and Experian. In late April, FOS sides with me and awards compensation. ICO finally assign a case advisor. In May, wait two weeks for the response, then the CU say not happy with that, escalate within the FOS and I need to wait for an Ombudsman to be assigned.. .. as it was an investigator who made this decision. Today, ICO respond saying that they can't uphold the complaint as they deal with the org and not the individual, but are willing to be communicated further information. Email in progress.... but they also notify me that CU's aren't regulated under the CCA. So my questions really is... the distress this has caused has been over 9 months. I can't get a new car (which I could lose my job over), I need to sort out the Mortgage for my current residence (which means I could lose my home) and in all honesty I've spent hours on this. What can I do? The FOS is saying it now may take the ombudsman a while to respond. Bringing this whole incident to 10, possibly 11 months. The other thing I'm unsure of is if the CU isn't regulated by the CCA, what can actually be done? How can this be fair processing of consumer data? Thanks in advance and sorry for the long post! -

Hi, I made a claim against a bank for some charges which had been applied to my mortgage account for the 'cleansing' by their solicitors of my Data following a DSAR in 2008. The finite detail of which is not relevant to this question I pose. The bank employed solicitors to defend my Claim (which I had repaid in full after a battle). 1) The solicitors advised me that the bank had admitted the charges should not have been applied ie. there was a mistake or the fact I was never advised of these charges, they were 'concealed.' However, the solicitors stated on a number of occasions when I pressed them that my 2008 charges which had been charged were now Time Barred and therefore would not be repaid citing s.2 Limitations Act 1980. - (6yrs rule) 2) I only discovered the charges in 2014 when investigating something else and they knew this. However, I went back to them and stated that under s.32 of the Limitations Act 1980 in the event of Mistake, Concealment or Fraud, Limitation is postponed, but they insisted s.2 applied as a result of my claim being a claim against the bank for breaching the DPA. They stated in response: "You have proposed an action against our client for a breach of the Data Protection Act 1998 and on that basis s.2 Limitations Act 1980 applies" So my question to you here is: Under what circumstances, when a claim is made for a breach in the Data Protection Act (they charged me over £1000 for a £10 statutory DSAR fee cost which breached the DPA regulations of charges for a DSAR) can a defence of s.2 Limitations Act apply which denies me the repayment, when s.32 can be ignored which entitles me to be repaid? I received the payments back on the basis of a 'commercial decision' being made (ie..it was costing them more in their own legal fees now that I had redeemed the mortgage and couldn't dump them on my mtg, than they were going to pay out) But that's not the issue here, I need to know exactly why they felt they could use s.2 legally to defend and not repay me, whilst ignoring s.32? To the layman it doesn't make sense, perhaps there is a particular legal reason why and that's what I need to know. Many thanks A1

-

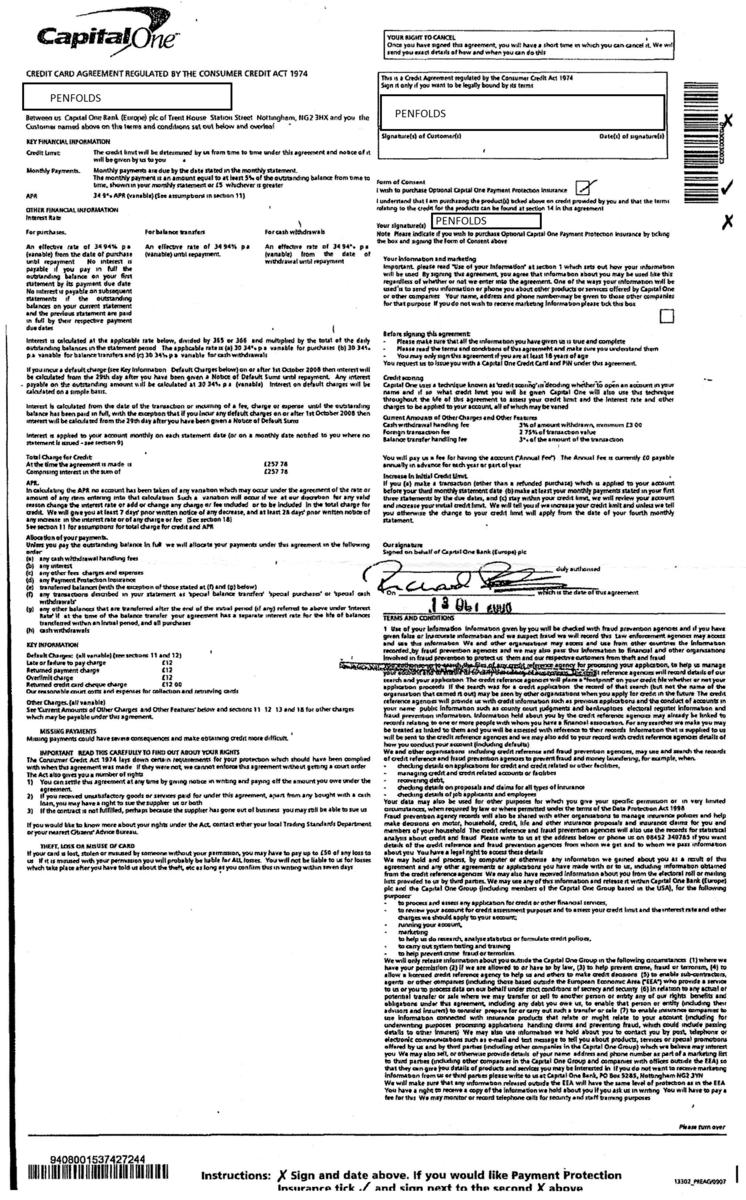

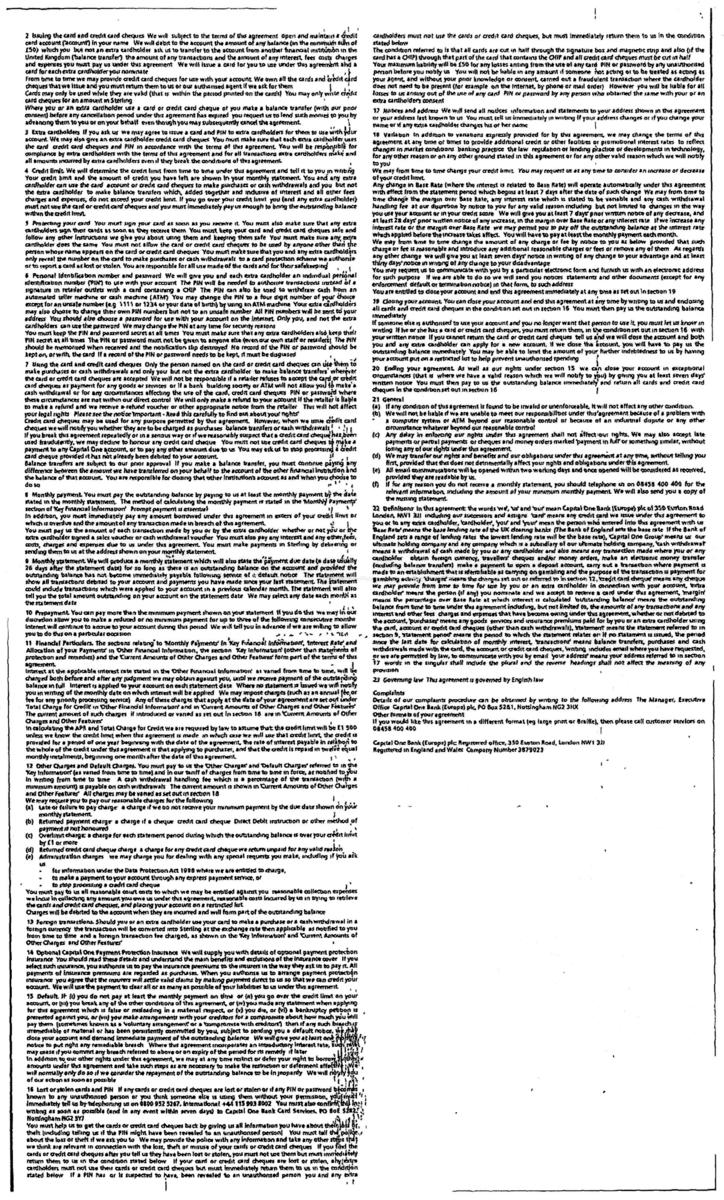

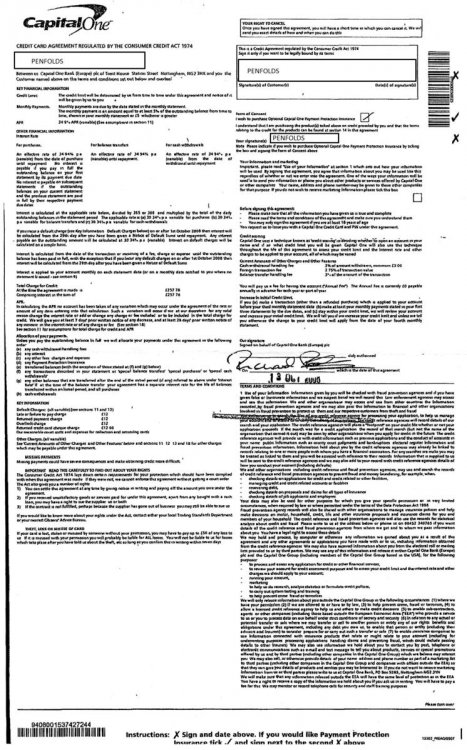

Hi All, I have recently defended a claim by Shoosmiths on behalf of Capquest for a Cpaital One credit card taken out in Oct 2008, the last payment made was in Jan 2012. The claim was stayed at the end of Jan 2017 after filing a defence. Before filing the defence Capquest was sent a CCA request, a copy was also sent to Shoosmiths with a CPR31.14 request, which Shoosmiths remain in breach of. However today Capquest has sent a response to the CCA request (attached). They have also sent somebody elses application for a Barclays Sky Card which includes their name, address, DOB, household income, home, mobile and work telephone numbers and applicants signature. Any advice greatly appreciated, please advise if defence or CPR 31.14 request needs uploading. Thanks Penfolds

Hi All, I have recently defended a claim by Shoosmiths on behalf of Capquest for a Cpaital One credit card taken out in Oct 2008, the last payment made was in Jan 2012. The claim was stayed at the end of Jan 2017 after filing a defence. Before filing the defence Capquest was sent a CCA request, a copy was also sent to Shoosmiths with a CPR31.14 request, which Shoosmiths remain in breach of. However today Capquest has sent a response to the CCA request (attached). They have also sent somebody elses application for a Barclays Sky Card which includes their name, address, DOB, household income, home, mobile and work telephone numbers and applicants signature. Any advice greatly appreciated, please advise if defence or CPR 31.14 request needs uploading. Thanks Penfolds

-

Dear all, I'd greatly appreciate advice as I'm wanting to take ES Parking to court for breaching the DPA by claiming my details in the first place from the DVLA. I know this is going to be a long journey and lots of work but I'm willing to do it for the good of others and perhaps to teach them a lesson to stop harassing people when there is no basis for their claim. I've been through the following so far: Stage 1: Letter before claim: __________________________________________________________________________ (Sent mid December) Letter Before Claim (Ref number: XX111111) Dear ES Parking In May 2016 you issued me with a parking charge for stopping/parking in a publicly accessible road where no contract was formed and for which there were no road markings (provided courtesy of your own witness statement). It has been established that there can be no liability as you do not follow the protocols of the POFA and so it is not possible for a contract to be created. You have continued to pursue speculative charges despite it being firmly established that no charge could ever be due. I refer to case C8GF4C12 ES Parking Enforcement v Ms A. Manchester, in front of DH Iyah on 29/11/2016. It was established that there was inadequate signage and that you lost the case on the grounds that signage is forbidding. You obtained my personal details from the DVLA for the purpose of pursuing a parking charge, However, there was never any possibility this charge could be valid. My name and address information (together with other information) is classified as personal data within the meaning of s1(1) of the Data Protections Act (DPA). As there is no possibility that any monies were owed to you by myself, then attempting to charge a parking charge is caused harassment and personal distress to myself, is using it in ways which violate principles 1 and 2 of the DPA, and s13 of the DPA provides for financial compensation for this. The case of Vidal-Hall v Google Inc [2014] EWHC 13 (QB) provides authority that misuse of personal data is a tort and that damages may be non-pecuniary. The case of Halliday v Creation Consumer Finance Ltd [2013] All ER (D) 199 provides authority that a reasonable sum for compensation would be £750. I am therefore claiming £500 from yourself for misuse of my personal data under s13 of the DPA. You have 14 days to remit this amount to myself. After that time I will file a claim without further correspondence. The rules on pre-action conduct are here https://www.justice.gov.uk/courts/procedure-rules/civil/rules/pd_pre-action_conduct I believe I have provided you with all necessary information. I am willing to consider alternative dispute resolution and suggest the Consumer Ombudsman. Yours Sincerely __________________________________________________________________________ Stage 2: Claim filed with MCOL with the following details: In May 2016 ES Parking breached the Data Protection Act by accessing my details from the DVLA without reasonable cause. It has been proven on numerous cases including C8GF4C12 ES Parking Enforcement v Ms A. Manchester, in front of DH Iyah on 29/11/2016 that they have no grounds for pursuing a parking charge. I am claiming damages of £750 for misuse of my personal data under s13 of the DPA. I attempted to resolve this out of court with a letter before claim for which I have received no reply. __________________________________________________________________________ I've now received a defence which is attached I'm willing to fight them to the death on this and money is no objective, this is purely about principle - ultimately this is going to cost me money because of time off.ClientDefenceDPA.pdf

Dear all, I'd greatly appreciate advice as I'm wanting to take ES Parking to court for breaching the DPA by claiming my details in the first place from the DVLA. I know this is going to be a long journey and lots of work but I'm willing to do it for the good of others and perhaps to teach them a lesson to stop harassing people when there is no basis for their claim. I've been through the following so far: Stage 1: Letter before claim: __________________________________________________________________________ (Sent mid December) Letter Before Claim (Ref number: XX111111) Dear ES Parking In May 2016 you issued me with a parking charge for stopping/parking in a publicly accessible road where no contract was formed and for which there were no road markings (provided courtesy of your own witness statement). It has been established that there can be no liability as you do not follow the protocols of the POFA and so it is not possible for a contract to be created. You have continued to pursue speculative charges despite it being firmly established that no charge could ever be due. I refer to case C8GF4C12 ES Parking Enforcement v Ms A. Manchester, in front of DH Iyah on 29/11/2016. It was established that there was inadequate signage and that you lost the case on the grounds that signage is forbidding. You obtained my personal details from the DVLA for the purpose of pursuing a parking charge, However, there was never any possibility this charge could be valid. My name and address information (together with other information) is classified as personal data within the meaning of s1(1) of the Data Protections Act (DPA). As there is no possibility that any monies were owed to you by myself, then attempting to charge a parking charge is caused harassment and personal distress to myself, is using it in ways which violate principles 1 and 2 of the DPA, and s13 of the DPA provides for financial compensation for this. The case of Vidal-Hall v Google Inc [2014] EWHC 13 (QB) provides authority that misuse of personal data is a tort and that damages may be non-pecuniary. The case of Halliday v Creation Consumer Finance Ltd [2013] All ER (D) 199 provides authority that a reasonable sum for compensation would be £750. I am therefore claiming £500 from yourself for misuse of my personal data under s13 of the DPA. You have 14 days to remit this amount to myself. After that time I will file a claim without further correspondence. The rules on pre-action conduct are here https://www.justice.gov.uk/courts/procedure-rules/civil/rules/pd_pre-action_conduct I believe I have provided you with all necessary information. I am willing to consider alternative dispute resolution and suggest the Consumer Ombudsman. Yours Sincerely __________________________________________________________________________ Stage 2: Claim filed with MCOL with the following details: In May 2016 ES Parking breached the Data Protection Act by accessing my details from the DVLA without reasonable cause. It has been proven on numerous cases including C8GF4C12 ES Parking Enforcement v Ms A. Manchester, in front of DH Iyah on 29/11/2016 that they have no grounds for pursuing a parking charge. I am claiming damages of £750 for misuse of my personal data under s13 of the DPA. I attempted to resolve this out of court with a letter before claim for which I have received no reply. __________________________________________________________________________ I've now received a defence which is attached I'm willing to fight them to the death on this and money is no objective, this is purely about principle - ultimately this is going to cost me money because of time off.ClientDefenceDPA.pdf -

I am suing both a Parking company and a Supermarket company. Suing them for my time prepping and Appealing. Im also suing them for Breaches of the DPA. One of the reasons for their breach, I have been told, is that the Parking Company passed on my details to a Debt Recovery Company AFTER a POPLA appeal was started but BEFORE the POPLA decision was made. (I won the POPLA Appeal). I have been told this was a breach of the DPA but for the life of me I cannot find any reference to passing on of details anywhere. Can anyone help? By the way. The parking company obtained my details and sent me a PCN as Keeper 6 months after the alleged parking contravention knowing there was no keeper liablility.

-

Hi, I issued a Section 10 notice (Data Protection Act) on a non-credit related matter relating to the processing of inaccurate personal information held about me. The organisation a) failed to respond within the 21 days (upheld by the ICO) and b) when they did eventually respond, have refused to comply with my Section 10. Most grateful for any guidance on next steps - e.g. how I might go about enforcing compliance through the courts, procedurally. And is their failure to respond within the 21-day timeframe actionable, e.g. distress in light of Vidal-Hall v. Google? Many thanks.

Hi, I issued a Section 10 notice (Data Protection Act) on a non-credit related matter relating to the processing of inaccurate personal information held about me. The organisation a) failed to respond within the 21 days (upheld by the ICO) and b) when they did eventually respond, have refused to comply with my Section 10. Most grateful for any guidance on next steps - e.g. how I might go about enforcing compliance through the courts, procedurally. And is their failure to respond within the 21-day timeframe actionable, e.g. distress in light of Vidal-Hall v. Google? Many thanks. -

I recently checked my Credit Reference File and saw that a default was on my account for a Cahoot flexi loan, the default was incorrect in that the last payment date and default date were some 18 months apart and the original debt was incurring interest, making the amount outstanding an additional £4 K. I approached Santander on 2 occasions and they refused to remove the default, so I then moved on to the ICO, who upheld my complaint and instructed Santander to put things right. The debt would be statute barred and should thus disappear, this happened on my Noddle file but still was showing on my Experian file, this has prevented me from a re-financing deal due to adverse credit being shown. I got back to the ICO and once again they contacted Santander, who stated they had removed one but had forgotten about the other CRA's, to say I am annoyed is an understatement Is there any way to get compensation for this as I see ICO cannot penalise them?

-

After some advice and any feedback from anybody who has needed to seek a court order to have their data ceased being processed. I have issued a S. 10 notice that was delivered by hand to the director of a small company, they have so far attempted to involve a third party to put pressure on me to back off but have failed to abide by the notice. I have also sent a Subject access request which I am expecting them to ignore as well. Being a small company this could just be down to not knowing what to do etc however I am now in the position of having to decide my next steps. Has anyone pursued a S.10 notice as far as the courts ?

After some advice and any feedback from anybody who has needed to seek a court order to have their data ceased being processed. I have issued a S. 10 notice that was delivered by hand to the director of a small company, they have so far attempted to involve a third party to put pressure on me to back off but have failed to abide by the notice. I have also sent a Subject access request which I am expecting them to ignore as well. Being a small company this could just be down to not knowing what to do etc however I am now in the position of having to decide my next steps. Has anyone pursued a S.10 notice as far as the courts ? -

Had an issue over a water bill for some time which has resulted in non payment. Due to my somewhat poor state of health I've not had the energy to deal with things as well as I could do. So I've done the worst thing possible and ignored it until today. Searchlight Collections attended my property this afternoon. I was not at home at the time. The agent spoke to someone who came to my property to collect some belongings, they do not live here. They are a completely different gender to me also. From what I've been told the doorstepper had the cheek to ask for me and state that I owed money for a water bill and to make contact with them. They left a menacing looking card with a box ticked next to "An application for a bailiff or HCEO to seize possessions" ... I have nothing of value, I don't drive on medical grounds so really that course of action is not going to end well for anyone. They are also lacking a defaulted CCJ against me so I don't see how they could even do this without one! They handed this over to the girl at the property and left. They did not enter the property at any point. I received a phonecall from the lady in question and said that if he'd not gone to politely tell them that I was busy and not to be disturbed. Needless to say I'm rather angry that this clown has breached the DPA in this manner. Therefore I want to follow that up. I've no interest in discussing the account with Searchlight. I'd be happy to speak to water company directly however and get the billing issue resolved. How should I proceed in this? I don't want any compensation as such. However I do want to raise the pulse-rates for them a little bit. Thinking a letter asking them what they were doing and copy of their complaints procedure? Then threaten the ICO but actually raise the matter with them anyway? Tyia

Had an issue over a water bill for some time which has resulted in non payment. Due to my somewhat poor state of health I've not had the energy to deal with things as well as I could do. So I've done the worst thing possible and ignored it until today. Searchlight Collections attended my property this afternoon. I was not at home at the time. The agent spoke to someone who came to my property to collect some belongings, they do not live here. They are a completely different gender to me also. From what I've been told the doorstepper had the cheek to ask for me and state that I owed money for a water bill and to make contact with them. They left a menacing looking card with a box ticked next to "An application for a bailiff or HCEO to seize possessions" ... I have nothing of value, I don't drive on medical grounds so really that course of action is not going to end well for anyone. They are also lacking a defaulted CCJ against me so I don't see how they could even do this without one! They handed this over to the girl at the property and left. They did not enter the property at any point. I received a phonecall from the lady in question and said that if he'd not gone to politely tell them that I was busy and not to be disturbed. Needless to say I'm rather angry that this clown has breached the DPA in this manner. Therefore I want to follow that up. I've no interest in discussing the account with Searchlight. I'd be happy to speak to water company directly however and get the billing issue resolved. How should I proceed in this? I don't want any compensation as such. However I do want to raise the pulse-rates for them a little bit. Thinking a letter asking them what they were doing and copy of their complaints procedure? Then threaten the ICO but actually raise the matter with them anyway? Tyia -

Group, I’m seeking help / advice on section 35 of the DPA 1998 Act: 35. Disclosures required by law or made in connection with legal proceedings etc. (1) Personal data are exempt from the non-disclosure provisions where the disclosure is required by or under any enactment, by any rule of law or by the order of a court. (2) Personal data are exempt from the non-disclosure provisions where the disclosure is necessary— (a) for the purpose of, or in connection with, any legal proceedings (including prospective legal proceedings), or (b) for the purpose of obtaining legal advice, or is otherwise necessary for the purposes of establishing, exercising or defending legal rights. Could someone please advise if sub-section 1 above could be applied as follows ? If a creditor does not respond to an information request made under section 77-79 of the CCA 1974 Act then a SAR could be made for the information and if they continue to withhold the information then a court order could be sought to enforce the SAR which the creditor must comply with or else confirm they do not have the information ? I hope this makes sense – any help / guidance would be appreciated. Many thanks.

-

Group, Could someone please point me in the right direction for info on how to apply for a court order to enforce a SAR. Thanks in advance.

-

Hi everyone. I have a comparitively small debt of £350 for gas and electricity supplied by Eon at a property I moved out of a year ago. Eon have got PastDue to "manage" and recover the debt but it has not (as far as I can tell) been assigned to them. I have followed previous Forum advice and told them I will only communicate with them in writing and offered them in writing £10 a month. They have now come back to me asking for confirmation that I owned or occupied the previous property; dates that I entered and vacated the property and confirmation of my date of birth. They say they need this information to comply with the DPA. Now I must confess I'm not a leading expert on the Data Protection Act but I thought the act was there to safeguard personal information that companies held on people NOT as a tool to extract info companies do not have about you. If these people are properly acting for Eon shouldn't Eon be able to confirm dates when we were taking energy from them. They were properly informed when we vacated the property last year. I would welcome any thoughts members have please.

Hi everyone. I have a comparitively small debt of £350 for gas and electricity supplied by Eon at a property I moved out of a year ago. Eon have got PastDue to "manage" and recover the debt but it has not (as far as I can tell) been assigned to them. I have followed previous Forum advice and told them I will only communicate with them in writing and offered them in writing £10 a month. They have now come back to me asking for confirmation that I owned or occupied the previous property; dates that I entered and vacated the property and confirmation of my date of birth. They say they need this information to comply with the DPA. Now I must confess I'm not a leading expert on the Data Protection Act but I thought the act was there to safeguard personal information that companies held on people NOT as a tool to extract info companies do not have about you. If these people are properly acting for Eon shouldn't Eon be able to confirm dates when we were taking energy from them. They were properly informed when we vacated the property last year. I would welcome any thoughts members have please. -

Here goes, long painful story......... At the beginning of June, I upgraded my account with Vodafone and paid an early upgrade fee. My new phone was duly delivered within a few days. I logged into my account a few days later and was offered a further upgrade. I thought that this was odd as I'd just upgraded, however the website stated I could upgrade again - for free. I contacted Vodafone (upgrade dept) who confirmed to me that indeed I could upgrade again. I did not do anything about this at the time. A few days later, I received a call from vodafone sales department wondering why I hadn't gone with the upgrade. I told the advisor that I was still thinking about it. About a week later I logged into my account and the offer to upgrade free of charge was still there. I telephoned the upgrade department to take advantage of this and the order was put through and I was advised that the new phone would be delivered to my work address 2 days later. The phone did not arrive. I phoned your vodafone upgrades and was advised that the order was stuck in the system and that someone would sort this out and the phone would be delivered within a few days. This did not happen. After about 2 weeks of me contacting vodafone and speaking to numerous advisors and the complaints department I was told that my complaint had been logged and I should receive the new phone within a few days. I made in excess of 7 or 8 calls to vodafone offices regarding this and still did not receive the phone. On Thursday 2nd July around 4pm - my phone stopped working. It said 'NO SERVICE'. I telephoned Vodafone to be advised that I needed to do a SIM swap and that this needed to be done in a shop. My local shop had closed at 5.30pm so I then travelled to Manchester (8 miles away), to do this - I cannot be without my phone as I use it for work. I was very angry about this but travelled to Manchester to arrange the SIM swap. After speaking to an assistant at the shop, he did not wish to do the SIM swap due to 'too many outstanding orders and issues on my account'. He gave me a PAYG SIM with a small amount of credit so that I could contact vodafone customer relations office to get this sorted. I rang back at approximately 8pm that evening and after spending over an hour on the phone was told that my issue would be sorted the next day and I would receive a call back at 1130am the following day. This did not happen. So now no-one can contact me as my number is out of use. I've lost clients as they could not contact me. Numerous family and friends had been trying to contact me and were unsuccessful as my number was not working. Around 2pm on Friday 3rd July, my son's phone rang from my number, he answered the call only to be told by the caller (Mr Davies) - I don't know anyone called Mr Davies, that he had been given my phone number by the Vodafone upgrade department! I was absolutely speechless as you can imagine and enraged! Mr Davies had contacted my son as he'd had so many missed calls from my son (who is ill!) and wondered who it was. Mr Davies had also given my number out to his family and friends also! I telephoned vodafone complaints department and after spending nearly 2 hours on the phone in my works time, was told that it would be sorted that day. This did not happen. Mr Davies had also received text alerts from my bank and credit card giving sensitive information and account balances. Surely, This is a MAJOR DPA breach. It is vodafones duty to protect my data and they have failed! Mr Davies received numerous calls and text from my contacts wanting to know who the hell he was and where was I???!!!!!!! Having got nowhere with vodafone customer relations department, I went into the Vodafone store in Stockport to speak to someone who I foolishly thought could help me. I was advised by the shop assistant 'there are too many issues on your account and we can't deal with it'. He told me to call customer again. Which I did. After a further 2 and a half hours on the phone distressed, upset and very angry I was promised that this had been passed to a manager and someone would call me back before 9pm. I was also told they would block the number This did not happen! I then phoned Vodafone again and got through to an Egyptian call centre worker to told me that he would block my account. This did not happen until midnight on 3rd July! I received a call from an operator on 4 July to be advised that my complaint is being dealt with and I would receive my number back and my account would be closed and I would also receive compensation for the DPA breach, breach of privacy, inconvenience and also for the 15plus hours I've spent trying to sort this out with their call centres around the world! I have not managed to speak to the same person twice - It's ridiculous! I've been advised by vodafone customer relations today that if I send my phone back then they will cancel my account. They've offered me nothing else. I want my account cancelling, a full apology, a full investigation, copies of all of the phone recordings theyhave as well as a data subject access request and also financial recompense for the DPA breach, breach of privacy, massive inconvenience they have caused me by having to change my phone number and mobile provider I am outraged that they can just transfer my number to a random stranger and not even apologise. I am also outraged that despite on several occasions vodafone admitting that there's been a DPA breach and breach of privacy they have not offered me a mutually satisfactory resolution I've lost work clients and have had a major inconvenience as I've had to change my number. The upset, stress and inconvenience vodafone have caused is incomprehensible! I've been advised by iCO that I do have a good case but any further advice would be much appreciated. Thanks!!

-

Hi, I've spoken to the ICO about this a few times, but they've told me that they don't deal with individual complaints when it comes to "Internet Media". 192.com persist to put my personal information up on their site publicly, despite having written to them on several occasions to request that my name isn't used to promote their company. Anyhow, I'm sat here, another year later, another release of the Voter Role and voila... There I am again... What do I do with these email exchanges I have between myself and them getting my name removed. What do I do about the ICO. Despite filling in their form here: 1) http://statics.192.com/rel-4b316/downloads/C01.pdf 2) The emails which are obviously automated i.e. 10 in a row (spaced out over a week last year when I had the same issue), all reading the exact same (yet with different fonts). I've had a thought about this. Never once did I give them permission to sue my details to promote their business. As a director of a company, I'm in two minds whether to pop them a surprise "consultancy invoice" in place of the usually yearly opt out (which I didn't even opt in to). Any thoughts on that? This is driving me moggy. Cheers, A

-

Lowell Portfolio / EE Limited / Possible DPA Breach?

Micael1000 posted a topic in Other Institutions

Good Afternoon All I had an EE (formally T-Mobile) contact that I ran in trouble with and got a default placed on my credit file. EE Limited then sold the debt to Lowell Portfolio, however even though EE had sold the account and were nothing to do with it anymore and Lowell Portfolio ‘legally’ owned the debt, EE Limited continued to update the default on my credit file for a further 5 consecutive months (I have proof of this from the CRA). I have been advised that what should have happened is that the default should have been taken over straight away by Lowell and it was Lowell responsibility to update it on my credit file, however EE continued to update it for 5 months, it then disappeared off my credit file and the CRA confirmed that EE had removed it and then 2 months later Lowell added there default. My question is, ‘Has DPA been breached, and is it worth making a complaint to the ICO?’ Many Thanks [/size][/size] -

Can anybody help.... at my wits end with this. I have been requesting my Subject Access Request from an organisation since last October, despite paying the fee, providing ID and numerous promises to send it to me, I've had nothing. I've complained to the ICO who have told the organisation they must comply promptly (two months ago...still nothing). The ICO have advised me to take this to the county court to get court order and possibly damages. I've been to my local County Court yesterday but they do not know what form I need. The ICO will not advise which form, they have a booklet on their site, which they admit is out of date. Even though I've told them I don't need advice on the claim just the bliddy form number, they can't/won't advise. I'm desperate to avoid going to a solicitor and incurring costs for what should be a relatively simple action.

-

I've asked the London Ambulance Service for a recording of a 999 call made on behalf of my late father. They have said that they can provide this but there would be a charge of £50. My understanding was that the maximum charge was £10 unless, of course, there are special rules for the NHS. Could anyone clarify?

-

A few weeks ago my car was parked on a residential road overnight, during the night the car was severely scratched with keys on all 4 sides (bonnet, boot, drivers and passenger sides) causing approximately £2000 of damage. I reported the incident to the police, who sent officers out to take a look and log the incident. 4 days later I received a call to let me know they would be making enquiries, knocking on doors, looking for witnesses and for any cctv. The following day I received a letter (dated 2 days prior to the call) saying there was very little that could be done so the case would be closed. I called them back to ask what had actually been done, apparently they had made the enquiries and found nothing so closed the case. I decided to take a walk round the area and knock on some doors myself, in doing so found a local business with infrared CCTV cameras, pointing in the direction of the space my car had been parked. Having spoken with the company they kindly reviewed the tapes, verified my identity as owner of the vehicle and found very clear, detailed video of the incident taking place and the face of the criminal. They offered the CCTV to the police to follow up but are unable to let me view the videos myself, apparently due to DPA. I've since spoken with the Police who have been unable to identify the perpetrator as yet but are circulating this internally to see if anyone recognises them. They have however said that if no-one does they will close the case and not take the matter further. If the police are unable to identify the criminal, how can I get the image to confirm whether or not I recognise them, was it personal??, was it a random drunk??, and further to circulate it more widely to bring the offender to justice? Additionally, i'm told there is a strong possibility that if they do manage to identify him then unless they are a persistent offender there is a strong possibility of a 'police caution' I have read through the DPA as posted on the ICO and there doesn't seem to be any reason why I should not view this video, does anyone have any view on this, or otherwise how I might go about persuading the private company to release a copy to me without risk to themselves? If the criminal is actually identified, through whatever means, how could I go about bringing a private prosecution to recover my losses for the damage, rather than them getting off with a 'caution' ? Many thanks in advance for your advice. Sorry for the long post but - 'Extremely annoyed at being so out of pocket and potentially Mr Scott-free strolling around without a care in the world for their actions'

A few weeks ago my car was parked on a residential road overnight, during the night the car was severely scratched with keys on all 4 sides (bonnet, boot, drivers and passenger sides) causing approximately £2000 of damage. I reported the incident to the police, who sent officers out to take a look and log the incident. 4 days later I received a call to let me know they would be making enquiries, knocking on doors, looking for witnesses and for any cctv. The following day I received a letter (dated 2 days prior to the call) saying there was very little that could be done so the case would be closed. I called them back to ask what had actually been done, apparently they had made the enquiries and found nothing so closed the case. I decided to take a walk round the area and knock on some doors myself, in doing so found a local business with infrared CCTV cameras, pointing in the direction of the space my car had been parked. Having spoken with the company they kindly reviewed the tapes, verified my identity as owner of the vehicle and found very clear, detailed video of the incident taking place and the face of the criminal. They offered the CCTV to the police to follow up but are unable to let me view the videos myself, apparently due to DPA. I've since spoken with the Police who have been unable to identify the perpetrator as yet but are circulating this internally to see if anyone recognises them. They have however said that if no-one does they will close the case and not take the matter further. If the police are unable to identify the criminal, how can I get the image to confirm whether or not I recognise them, was it personal??, was it a random drunk??, and further to circulate it more widely to bring the offender to justice? Additionally, i'm told there is a strong possibility that if they do manage to identify him then unless they are a persistent offender there is a strong possibility of a 'police caution' I have read through the DPA as posted on the ICO and there doesn't seem to be any reason why I should not view this video, does anyone have any view on this, or otherwise how I might go about persuading the private company to release a copy to me without risk to themselves? If the criminal is actually identified, through whatever means, how could I go about bringing a private prosecution to recover my losses for the damage, rather than them getting off with a 'caution' ? Many thanks in advance for your advice. Sorry for the long post but - 'Extremely annoyed at being so out of pocket and potentially Mr Scott-free strolling around without a care in the world for their actions'