Search the Community

Showing results for tags 'unfair charges'.

Found 24 results

-

I have been personally dealing with my landlord for over a year now without any legal support to correct being overcharged for rent at my residence for 11 years. During my tenancy (before march 2013) I was issued with court costs as my landlord made applications to the court to recover rent arrears held on my account. I signed a tenancy agreement for a 1 Bedroom apartment in 2002. The rent was set and I never questioned it (Why would I??). In March 2013, I found out that from the start of my tenancy I was registered as a two bedroom tenant paying rent for a two bedroom accommodation. This came about as I received a letter from the council requesting payments from me to pay for an unused bedroom space. When I notified my landlord they adjusted my rent account to reflect the rent their tenant's would normally pay for a 1 bedroom property. In addition, they also debited payments from my credit balance to cover the outstanding court costs. I didn't agree to any of this nor was a new tenancy agreement issued to me. - (Do I still have a legally binding tenancy agreement contract with my landlord)? I used their complaint procedure to request returning the court costs to my rent account as I believed I should not be held liable. My initial complaint was overruled and was told by my landlord that they were justified in their actions as my rent account still would have been in arrears even after the adjustments. I used my old rent statements, with the correct rent charges to calculate any outstanding arrears before the court applications were submitted and found this not being the case. Again following their complaint procedures, I re-submitted a compliant insisting that the court costs transferred from my credit balance should be returned to my rent account. After nearly a year on, my landlord agreed and confirmed my calculations and produced a gesture of good will (GOGW) of £190 to draw a line in my complaint. I did not agree with the (GOGW) and issued my final formal complaint to return all court cost's. Eventually, (as of last month) my landlord refunded my account with the full court costs suggesting that refunding the full amount was way of compensation to me. I am in desperate need of sound advice as to what rights I have as a tenant, if I am being treated fairly, do I have any entitlement or due compensation, who should i contact for legal advice and generally just being in this position as I feel that my landlord is not being up front with their obligations.

I have been personally dealing with my landlord for over a year now without any legal support to correct being overcharged for rent at my residence for 11 years. During my tenancy (before march 2013) I was issued with court costs as my landlord made applications to the court to recover rent arrears held on my account. I signed a tenancy agreement for a 1 Bedroom apartment in 2002. The rent was set and I never questioned it (Why would I??). In March 2013, I found out that from the start of my tenancy I was registered as a two bedroom tenant paying rent for a two bedroom accommodation. This came about as I received a letter from the council requesting payments from me to pay for an unused bedroom space. When I notified my landlord they adjusted my rent account to reflect the rent their tenant's would normally pay for a 1 bedroom property. In addition, they also debited payments from my credit balance to cover the outstanding court costs. I didn't agree to any of this nor was a new tenancy agreement issued to me. - (Do I still have a legally binding tenancy agreement contract with my landlord)? I used their complaint procedure to request returning the court costs to my rent account as I believed I should not be held liable. My initial complaint was overruled and was told by my landlord that they were justified in their actions as my rent account still would have been in arrears even after the adjustments. I used my old rent statements, with the correct rent charges to calculate any outstanding arrears before the court applications were submitted and found this not being the case. Again following their complaint procedures, I re-submitted a compliant insisting that the court costs transferred from my credit balance should be returned to my rent account. After nearly a year on, my landlord agreed and confirmed my calculations and produced a gesture of good will (GOGW) of £190 to draw a line in my complaint. I did not agree with the (GOGW) and issued my final formal complaint to return all court cost's. Eventually, (as of last month) my landlord refunded my account with the full court costs suggesting that refunding the full amount was way of compensation to me. I am in desperate need of sound advice as to what rights I have as a tenant, if I am being treated fairly, do I have any entitlement or due compensation, who should i contact for legal advice and generally just being in this position as I feel that my landlord is not being up front with their obligations. -

Hi, I travel from Marks tey to London at least twice a week. 2 weeks ago I bought my return ticket and I believe I stupidly left the tickets in the self service ticket point. I realised as I got off the train and spoke to a member of the greater anglia team to explain my situation. They said they would have to fine me but advised me to pay half the fine of 23.60 as they did I would be able to appeal if I had proof of payment. They also said I could keep the single ticket I buy myself later in the day and include it in my appeal. I followed her instructions, printed my bank statements, kept all receipts and submitted the appeal. It was declined and I find this incredibly unfair, I'm a regular commuter, can prove so as I keep all tickets and can also prove I didn't purposely avoid paying for my train ticket as I have proof I paid at 8.10am before I boarded the train. Greater anglia are not out of pocket and I did not avoiding paying. Is there anything I can do to appeal this further? I didn't have to pay approx £130 for 1 days travel, especially as an incredibly inconvenienced regular commuter.

Hi, I travel from Marks tey to London at least twice a week. 2 weeks ago I bought my return ticket and I believe I stupidly left the tickets in the self service ticket point. I realised as I got off the train and spoke to a member of the greater anglia team to explain my situation. They said they would have to fine me but advised me to pay half the fine of 23.60 as they did I would be able to appeal if I had proof of payment. They also said I could keep the single ticket I buy myself later in the day and include it in my appeal. I followed her instructions, printed my bank statements, kept all receipts and submitted the appeal. It was declined and I find this incredibly unfair, I'm a regular commuter, can prove so as I keep all tickets and can also prove I didn't purposely avoid paying for my train ticket as I have proof I paid at 8.10am before I boarded the train. Greater anglia are not out of pocket and I did not avoiding paying. Is there anything I can do to appeal this further? I didn't have to pay approx £130 for 1 days travel, especially as an incredibly inconvenienced regular commuter. -

Hi All, Me, my Husband and daughter(18) rented three storage "garages" from a storage company three years ago. In February 2014 they had problems with leaky roof which caused damage to daughter's stuff in her garage, which they never compensated for saying beyond their control as rain is an act of God (????). They put the charges up this year (contract to run April 14 - March 15) which we weren't prepared to pay as they still haven't repaired the roof. We therefore gave a month notice and removed our stuff on the 25th April. On the 2nd of May they then issued three invoices, mine & husband's storage fee for 1st to 25th April at double the previous rate and daughter's at three times the rate! I recalculated at previous rate and paid on the 17th May. They weren't happy with this and sent me emails threatening court, I stated that charging double/treble amount not reasonable under Supply of Goods and Services act, and charging more to cover loss of profit for loss of custom not fair under Unfair Terms and Conditions in Consumer Contract Regs 1999. They have now made a claim using MCOL for the rest of money on all three invoices - but only showing Daughter and Husband as defendants not me! I think this is as they know that husband and daughter are not as hot as me on consumer rights - and don't have as much fire in their bellies, plus both work full time whereas I have time for research! Can anyone give me advice - I believe I have a relevant defence but I'm not trained so can't become the family's legal representative. If I go I won't be able to say anything as not a defendant - can I become a defendant??? Help! - and thanks in advance for any knowledge

-

Dear all I have received the informartion from Halifax on all charges on my current account and now need to know how to progress. Do I just highlight these and send to the bank or FOS? Do you have a letter template I can use? I am a single mother who works but have experienced payday loans excess charges and thus causing fees on my account and also passing to other companies who have taken too much. I am in serious debt and although work am making it hard to make ends meet. Halifax have refused to help me with any charges apart from cancelling these for 3 months but I want to claim back precvious charges. Please help - thanks so much

Dear all I have received the informartion from Halifax on all charges on my current account and now need to know how to progress. Do I just highlight these and send to the bank or FOS? Do you have a letter template I can use? I am a single mother who works but have experienced payday loans excess charges and thus causing fees on my account and also passing to other companies who have taken too much. I am in serious debt and although work am making it hard to make ends meet. Halifax have refused to help me with any charges apart from cancelling these for 3 months but I want to claim back precvious charges. Please help - thanks so much -

Hello! I have a problem with my last employer, owner of the care home I worked for. Due to certain mistake I've made I was put on garden leave, awaiting my disciplinary meeting. On the day I had my disciplinary I provided the statement, prior to the meeting and gave my notice. Chair of the meeting said they accept my notice, yet will go with the meeting as planned. Although I provided mitigating circumstances I was found guilty and chair of the disciplinary hearing said 'had you not resigned we would sack you for gross misconduct'. Few weeks after I received my final pay slip I opened it and BOOM - from my final wages a cost of £390 was deducted. It stated is for the training. I was working for that care home for over two months and was never given my contract of employment. The training they provided was mandatory prior starting work in care setting and it was in-house training. I don't agree with that charge and contacted CAB but after 1h20minutes on the phone they sent me to read some law documents from which I didn't understand a lot I need the information - was the deduction of training costs in that case unfair? Please, please help And in case it was unlawful for my ex employer to do so what legislation describes it? Many thanks in advance!!

-

I need help!! I have a parking fine with Blackpool council for £112 (this includes court fee etc) I had a visit today from Phoenix Commercial collections Bailiff handing me a "notice of bailiff having visited" letter, stating I owe them £311.44 I asked him how he came to that figure and he stated it was his companies guidelines for what they charge. I have spoken to Blackpool council who are refusing to accept my payment of the £112 direct to them, stating I have to deal with the bailiff direct now. I spoke to Phoenix who again are refusing this amount and state I have to pay the £311.44 I really do not know what to do or where to go from here as I am certainly not paying £311.44 as this is certainly not a correct charges amount. PLEASE HELP!! (the original parking fine was Dec 2012) Thanks

I need help!! I have a parking fine with Blackpool council for £112 (this includes court fee etc) I had a visit today from Phoenix Commercial collections Bailiff handing me a "notice of bailiff having visited" letter, stating I owe them £311.44 I asked him how he came to that figure and he stated it was his companies guidelines for what they charge. I have spoken to Blackpool council who are refusing to accept my payment of the £112 direct to them, stating I have to deal with the bailiff direct now. I spoke to Phoenix who again are refusing this amount and state I have to pay the £311.44 I really do not know what to do or where to go from here as I am certainly not paying £311.44 as this is certainly not a correct charges amount. PLEASE HELP!! (the original parking fine was Dec 2012) Thanks -

hi i took out a loan with quid24 for 100, with a repayment of £110 , unfortunatly wasnt able to pay it on time, and within 6 days of missed due date £190 of charges had been added, they claim the charges are for letters they have sent but i have only ever recieved emails which they claim to be the letters. anyway here it a converstion log i have had with them so far. please let me know what you think , i have tried throwing a few legal quotes here and there (although i have probably got them wrong lol ) i have paid them £110.38 thet still persistant that i owe them £189.62 and dont seem to be budging no matter what i do or say, only thing they have done is offered to clear the remaining for £89.62 ( - £100 of the debt) but i still think this is unfair. i have contacted the financial ombudsman who advised me they can charge whatever they want if thats what i signed in the contract, but they have told me they have written to quid24 telling them i have lodged a compaint and they have 8 weeks to sort it... anyways enough of me going on, heres the contact between me and quid24 so far. okz19@hotmail.co.uk |2011-10-24 20:13:05 I would like to cancel mu agreement with yourselves under the terms and conditions i have 14 days to cancel my agreement with yourselves so i would like to excercise this right, please accept this as my written confirmation as cancelment of my agreement . please contact me asap by phone on 07413610113 in regards to the matter and for full payment of the original amount borrowed , the transfer fee , and 14 days interest at 8%apr . I would like to thank you in advance for your help in regards to this matter. Regards, anthony smith okz19@hotmail.co.uksupport@quid24.com |2011-10-25 13:28:04 Dear Anthony, Thank you for the email. Please see Cancellation Rights in our Credit Agreement: You will have a right to cancel this Agreement for 14 days, beginning with the day after this Agreement is signed by us ("the Cancellation Period"). If you do not exercise your right to cancel within the Cancellation Period, you will not be able to cancel this agreement. You may exercise this right to cancel by giving notice in writing by sending a letter to us at Quid24 Limited, 2nd Floor, 145-157 St John Street, London, EC1V 4PY, United Kingdom or by e-mail to support@quid24.com. As the Credit Agreement was signed on 07/10/2011 at 01:21, the Cancellation Period ended on 21st October. You sent us the notification on 24th October, so you are no longer able to cancel this Agreement under the Financial Services (Distance Marketing) Regulations 2004. Please make sure that you have sufficient funds available and let us know when can we collect the repayment of £300. Kind regards, Quid24 Support http://www.quid24.comokz19@hotmail.co.uk |2011-10-25 16:11:19 Give me an account number and sortcode to pay onto i do not have a debit card to payvwith, also i.borrowed on the 10/10/11 not 07/10/11support@quid24.com |2011-10-25 16:29:21 Dear Anthony, Thank you for the email. The Credit Agreement was signed when you registered with us on the 7th October. And the Cancellation Period is for 14 days, beginning with the day after the Credit Agreement was signed by us. So the Cancellation Period was 14 days starting from 8th October. We can offer an alternative payment method only once. Please make us a bank transfer to cover your debt using the following details: Account name: Quid24 Limited; Account number: 23497062; Sort code: 20-30-89; Amount: £300; Ref: Smith 1804 Please do not forget to add the reference. Please note that if we have not received the payment by the time we have agreed, additional charges will be added. When you have made the payment, please notify us and send us a copy of the payment. Please let us know as soon as you have received a new card to update your details. Thank you. Kind regards, Quid24 Support http://www.quid24.comokz19@hotmail.co.uk |2011-10-25 17:25:39 I have made a payment of 110.38 the paymeny breakdown is as follows: £100 original loan £5.50 transfer fee ( altough all uk banks transfer instantly for free) £4.50 original interest fee £0.38 good will gesture 1months interest on £100 @ 8% apr as for my debit card number you will not need this as as far as i am concered my debt to yourselves has been paid However if you still believe i owe any outstanding balance i advise you to pursue the matter via court, as the rest of the balance you claim to be owed is clearly laid out on the online statement as charges for reminder letters that you have not sent, and if you had i would expect them to be printed in gold on 24c gold leaf paper as £70 for a standard piece of paper printed in black toner ink certainly would not be a justifiable cost which would then bring us to the unfair terms and conditions act of 1997. I thank you for your help in this matter anthony smith. support@quid24.com |2011-10-26 11:08:21 Dear Anthony, Thank you for the email. We have received your payment of £110.38, as your loan had increased up to £300, so £189.62 is currently outstanding. Please Make us another transfer of £189.62 as soon as possible, as otherwise your debt will be soon handed over to our debt collection partner and further debt collection fees will apply. Kind regards, Quid24 Support http://www.quid24.comokz19@hotmail.co.uk |2011-10-26 15:21:16 Get the message you aint getting another penny stop playing stupid . support@quid24.com |2011-10-26 15:41:53 Dear Anthony, Thank you for the email. Please note that your loan has increased up to £300. The outstanding balance currently is £189.62, as you have only repaid £110.38 to us. Please make us another transfer of £189.62 as soon as possible, as otherwise your debt will be soon handed over to our debt collection partner and further debt collection fees will apply. Kind regards, Quid24 Support http://www.quid24.comokz19@hotmail.co.uk |2011-10-27 18:01:47 May i remind you that under the unfair terms and conditions act 1997 that your terms and conditions for charging £190 for letters you have not sent is deemed an unfair charge and would also be deemed an unfair condition in a court of law. however if you wish to continue this matter and pass the accused debt to a debt collecter then i would also like to remove your right to ring me on any contact number and further contact is to be via email and post only , this right also moves with the debt so you are to inform any 3rd party you pass the matter on to that they also no longer have any right to contact me other than the methods stated. if anyone contacts me by any method other that post and email in regards to this matter they will be liable for damages in court under the communications act 2003. I would like to thank you for your yet more unhelpfulness, and hope not to hear from you in regards to this matter again.support@quid24.com |2011-10-31 12:45:02 Dear Anthony, Thank you for the email. You have agreed all the charges as these are stated in our credit agreement that you have read, agreed and electronically signed. Please note that these letters were sent via email. Kind regards, Quid24 Support http://www.quid24.comokz19@hotmail.co.uk |2011-11-04 14:43:11 its nice to see how it took you 4 days to reply, anyway i have just been in contact with with the financial ombudsman who are going to write to yourselves in regards to the matter. firstly letters were not sent emails were, there is a difference, a letter you print and post and email you type and click a send button. and secondly the dates the emails were sent do not match the dates they should have as stated in the terms and conditions. terms and conditions states LETTERS (not emails) would be sent after the account becomes 1, 2, 4, and 7 days over due EMAILS (not letters) were sent on 1st reminder 17th oct - the DUE DATE (not 1 day after) 2nd reminder 18th oct - 1 day over (not 2 like stated) 3rd reminder 20th oct - 3 days over (not 4 like stated) 4th reminder 23rd oct - 6 days over ( not 7 like stated) also it has been noted to the financial ombudsman that when i contacted you in regards to a repayment plan you refused to help until the 24th oct conveniently after you had finished charging the account with unfair and unjustified charges. support@quid24.com |2011-11-04 15:10:22 Dear Anthony, Thank you for the email. Please note that it did not take 4 office opening days to reply to you as our office opening hours are Mon-Fri 8.30am-5pm. You sent us the email on Thursday evening after the office was closed and we replied to you on Monday morning. So we replied to you on the second day. We have checked and the emails were sent out on the following dates: 1st reminder - 18th October, 2nd reminder - 19th October, 3rd reminder - 21st October and 4th reminder - 24th October. Please note that these were sent out straight after midnight when the charge was added. Reminder letters are sent out via email, not via post as emails will reach you straight away. We can only offer repayment plans to clients whose loan has gone seriously overdue and who are seriously in debt. Kind regards, Quid24 Support http://www.quid24.comokz19@hotmail.co.uk |2011-11-04 15:42:12 do you not think £300 for a £100 is not seriously overdue enough ? and why would you not think i was in serious debt, if i wasnt in debt i would of been able to obtain and overdraft from my bank or a cheaper method of borrowing? anyway heres my solution , i can offer £10 a month on starting thursday the 10th, and can offer this every 4 weeks, providing you stop adding interest and charges, however if you find this unacceptable and still want to challenge it, then i will have no option but to let the matter continue , and once 8 weeks has passed without any resolution from yourselves, the matter will be pursued with the financial ombudsman. support@quid24.com |2011-11-04 16:10:21 Dear Anthony, Thank you for the email. We are willing to freeze the loan and set up a repayment plan for up to 12 months. As currently the outstanding balance is £300 and if this would be divided into 12 equal payments then every month you would have to repay £25. Alternatively as a gesture of goodwill we can make you a settlement offer to repay £200 in one go before 23rd November 2011 (so we would waive more then half of the charges). Please let us know which of the above two offers suits you the best and let us know of the exact date(s) when we can collect the payment(s). Kind regards, Quid24 Support http://www.quid24.comsupport@quid24.com |2011-11-04 16:18:18 Dear Anthony, Please ignore the above email. As you have already repaid £110.38, the outstanding balance is £189.62 not £300. Please accept our apologies for the mistake. We are willing to freeze the loan and set up a repayment plan for up to 12 months. As currently the outstanding balance is £189.62 and if this would be divided into 12 payments then you would have to make 11x £16 and 1x £13.62 payments. Alternatively as a gesture of goodwill we can make you a settlement offer to repay £89.62 in one go before 23rd November 2011 (so we would waive more then half of the charges). Kind regards, Quid24 Support www.quid24.com as you can see i have not responded to them as i have come back to my senses and have decided i shouldnt have to pay them anything , and i retract my last email to them that i offered £10 a month , until i fully understant where i stand ! any help wil be much appreciated.

-

Hi guys, just a quick query. Over the last year i was stupid enough to have severaql payday loans to which i was not able to pay. First was with MiniCredit which is being dealt with, and sure most people that use this site are aware of the issues with this company. The Second loan is with CFO Lending. Both have issued me with several charges to my account, including missed payment charges and interest charged per day. On this site and others I have seen stated that the amount that people have to pay is "amount borrowed plus one month's interest" I've informed both companies of this to which they say this is not the case, i have tried to do some research on this matter online and have failed to find any other reference to this on any other sites other than forums, this does not appear (from what i can see) within Consumer Credit Act 1974 or any amendments and does not seem to appear under any OFT guidelines. I don't doubt in the slightest that this information is correct but i can find any law that would back up this. Where would i find these laws or guidelines which states this amount of charges applied to accounts? Dont get me wrong I know I am liable to these debts and will pay these back, but I think i should only be paying what is lawful.

-

Hi, This is my first time claiming back a deposit so I have a few questions and would really appreciate some advice! I just moved out of a shared house a couple of weeks ago. My tenancy ended on June 30th, and I left the property on June 29th. As it was a student house and term was over, a couple of my housemates moved out a few weeks before the end of tenancy, however myself and another housemate, while not actively staying in the house, still had our belongings there and so had not yet moved out of the property. Myself and the other remaining housemate planned on returning to the property on June 29th, the day before our final day of tenancy to collect the rest of our belongings, return our keys and clean the property. However, when we returned on june 29th we discovered that our landlady had come to the property the day before (june 28th, 2 days before the end of our tenancy), and having found that the oven was not cleaned and that there was still a few items in the fridge she ordered a cleaner to come in and is taking this charge out of our deposits. We had planned on fully cleaning everything on june 29th, which was the day before the end of our tenancy, and our landlord knew that neither of us had fully moved out yet as our rooms still had our belongings in them and we had not returned our keys. My landlord also did not call us to say she was going to get a cleaner in, or else we would have told her we were coming the next day and would clean it then. My first question is, is our landlord allowed to charge us for cleaning even though our tenancy had not yet ended, and we had not yet moved out? Secondly, I read that the deposit is supposed to be returned within 10 days of the tenancy ending, and the deadline for that was today, so that hasn't happened. One of my housemates rang up the landlord to ask about the deposits and the landlord said that she will not return the deposits until she has proof that we have paid our last utility bills. This is the first time she has mentioned this to us. I have paid all our bills, but the only proof I have of this is the internet banking transfer I made to British Gas. Just to be clear, the utility accounts are in my name and have nothing to do with the landlord. So my second question, is my landlord allowed to withhold our deposits until she has proof that we have paid our final utility bills? I have a feeling she's just trying to delay paying us. Finally, do you think we have been charged unfairly for the cleaning (as already mentioned) and do you think I should take her to small claims court and send a letter informing her I am doing this? If I send her the proof that we've paid our utility bills like she wants, is it reasonable for me to ask for our deposits to be returned within 7 days of her receipt of this letter, bearing in mind she has already gone past the 10 days deadline? And finally, should I ask for proof that our deposits were put into a protection scheme (as I stupidly did not do this when we originally paid our deposits). Sorry for the ramble, any advice/answers would be very much appreciated. Thanks!

Hi, This is my first time claiming back a deposit so I have a few questions and would really appreciate some advice! I just moved out of a shared house a couple of weeks ago. My tenancy ended on June 30th, and I left the property on June 29th. As it was a student house and term was over, a couple of my housemates moved out a few weeks before the end of tenancy, however myself and another housemate, while not actively staying in the house, still had our belongings there and so had not yet moved out of the property. Myself and the other remaining housemate planned on returning to the property on June 29th, the day before our final day of tenancy to collect the rest of our belongings, return our keys and clean the property. However, when we returned on june 29th we discovered that our landlady had come to the property the day before (june 28th, 2 days before the end of our tenancy), and having found that the oven was not cleaned and that there was still a few items in the fridge she ordered a cleaner to come in and is taking this charge out of our deposits. We had planned on fully cleaning everything on june 29th, which was the day before the end of our tenancy, and our landlord knew that neither of us had fully moved out yet as our rooms still had our belongings in them and we had not returned our keys. My landlord also did not call us to say she was going to get a cleaner in, or else we would have told her we were coming the next day and would clean it then. My first question is, is our landlord allowed to charge us for cleaning even though our tenancy had not yet ended, and we had not yet moved out? Secondly, I read that the deposit is supposed to be returned within 10 days of the tenancy ending, and the deadline for that was today, so that hasn't happened. One of my housemates rang up the landlord to ask about the deposits and the landlord said that she will not return the deposits until she has proof that we have paid our last utility bills. This is the first time she has mentioned this to us. I have paid all our bills, but the only proof I have of this is the internet banking transfer I made to British Gas. Just to be clear, the utility accounts are in my name and have nothing to do with the landlord. So my second question, is my landlord allowed to withhold our deposits until she has proof that we have paid our final utility bills? I have a feeling she's just trying to delay paying us. Finally, do you think we have been charged unfairly for the cleaning (as already mentioned) and do you think I should take her to small claims court and send a letter informing her I am doing this? If I send her the proof that we've paid our utility bills like she wants, is it reasonable for me to ask for our deposits to be returned within 7 days of her receipt of this letter, bearing in mind she has already gone past the 10 days deadline? And finally, should I ask for proof that our deposits were put into a protection scheme (as I stupidly did not do this when we originally paid our deposits). Sorry for the ramble, any advice/answers would be very much appreciated. Thanks! -

Hi Everyone Can anyone provide any advice on how I should complain and attempt to get the original Business Loan Repayment Insurance Cost and subsequent Bank Charges back on the following:- In 2004 we had a Limited Company who banked with Lloyds TSB, when we needed to consolidate the debt of the the Overdrafts with this bank. We took out a loan for £40,000 plus a charge of 7017.00 for Business Loan Repayment Insurance and a £400.00 Arrangement Fee, this was secured by a Guarantee and Charge over our Property. We had many problems during the period up until 2009 when we allowed our company to be struck off by Companies House. We paid all outstanding Creditors off. We had many Bank Returned Fees during the period 2004 - 2009 which added to this Limited Companies demise. We started a Partnership in the same business and Lloyds provided a New Loan ro clear the outstanding Bank Accounts of the old Limited Company. This amounted to a New Loan with the same Guarantors as with the old Limited Company, the loan was for £70,000 with a £1,000.00 Arrangement Fee. This was the amount outstanding plus a small working Overdraft. The outstanding figure would have been £7,000 less if we had not been forced to take out the Business Loan Repayment Insurance in 2004, and I note they never pushed this Insurance for the New Loan with the New Partnership. When they closed the old Limited Companies Accounts they ommitted to open the New Partnership Accounts and as such we where paying continued excessive Interest and Charges on the Old LC Accounts even though it had been closed. One of our old customers paid an outstanding invoice via BAC's to the old LC Account and the Bank transfered this into cyberspace and we have never received into our new account, even though we have complained about it many times. The banks actions over the years have caused the new partnership considerable financial hardship and continue to do so. Please Help!

Hi Everyone Can anyone provide any advice on how I should complain and attempt to get the original Business Loan Repayment Insurance Cost and subsequent Bank Charges back on the following:- In 2004 we had a Limited Company who banked with Lloyds TSB, when we needed to consolidate the debt of the the Overdrafts with this bank. We took out a loan for £40,000 plus a charge of 7017.00 for Business Loan Repayment Insurance and a £400.00 Arrangement Fee, this was secured by a Guarantee and Charge over our Property. We had many problems during the period up until 2009 when we allowed our company to be struck off by Companies House. We paid all outstanding Creditors off. We had many Bank Returned Fees during the period 2004 - 2009 which added to this Limited Companies demise. We started a Partnership in the same business and Lloyds provided a New Loan ro clear the outstanding Bank Accounts of the old Limited Company. This amounted to a New Loan with the same Guarantors as with the old Limited Company, the loan was for £70,000 with a £1,000.00 Arrangement Fee. This was the amount outstanding plus a small working Overdraft. The outstanding figure would have been £7,000 less if we had not been forced to take out the Business Loan Repayment Insurance in 2004, and I note they never pushed this Insurance for the New Loan with the New Partnership. When they closed the old Limited Companies Accounts they ommitted to open the New Partnership Accounts and as such we where paying continued excessive Interest and Charges on the Old LC Accounts even though it had been closed. One of our old customers paid an outstanding invoice via BAC's to the old LC Account and the Bank transfered this into cyberspace and we have never received into our new account, even though we have complained about it many times. The banks actions over the years have caused the new partnership considerable financial hardship and continue to do so. Please Help! -

Hi i went to get a ticket from a machine in an ncp car park,the machine would not take my money,then it stated that only credit cards... i went to get my credit card and received a ticket within 1 minute of looking and parking. please help:mad2:

-

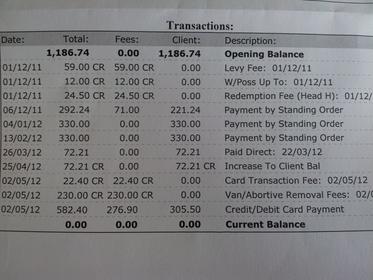

Dear CAG Forum users, I've been following this forum for quite some time but this is my first post. Last week I had the misfortune of a bailiff visit to my property whilst I was away working - to collect Council Tax arrears. He managed to raise the attentions of my landlady, who lives a few doors away, and made a number of verbal threats which clearly distressed her. Luckily, through a series of telephone calls, I managed to sort the matter out remotely and simply paid what I was told I owed in full over the phone as I didn't want the situation to go any further. In the previous week, I had received a letter from the Council stating that I owed £305.50 from last year's Council Tax bill and that this would be collected via Direct Debit. I thought no more about it. I've since made a complaint to the Council in question regarding the way in which they handled this matter. I requested a statement of my account, once settled, from Bristow and Sutor. This arrived today and I've included a copy of it as an attachment here: You'll see that a Bailiff had visited previously, after which I set up an arrangement. I made some errors in my accounting, and thinking the amount owing had been paid in full, I cancelled the payment arrangement I had in place. This was a silly mistake on my part I guess. Bristow and Sutor did not write to me about it and the next I heard was from the Council stating that the amount outstanding would be taken by DD. I thought the matter had been solved. Looking at this breakdown, I've paid in the region of £347.90 in fees in order to sort this out. I am not sure which of these fees are legal and which are not. Can Bailiffs really charge all these? For example, the debit card processing fee of 4% - this appears to me to be paying for the priviledge of paying with money! Certain sites on the internet indicate that these fees are fraudulent for various reasons and may consitute theft. Is this true? Aside from my complaint to the Council, which I doubt will result in a satisfactory conclusion from my point of view, does the forum know of any other way to get any of this money back? I look forward to any responses and advice I might get. All the best.

Dear CAG Forum users, I've been following this forum for quite some time but this is my first post. Last week I had the misfortune of a bailiff visit to my property whilst I was away working - to collect Council Tax arrears. He managed to raise the attentions of my landlady, who lives a few doors away, and made a number of verbal threats which clearly distressed her. Luckily, through a series of telephone calls, I managed to sort the matter out remotely and simply paid what I was told I owed in full over the phone as I didn't want the situation to go any further. In the previous week, I had received a letter from the Council stating that I owed £305.50 from last year's Council Tax bill and that this would be collected via Direct Debit. I thought no more about it. I've since made a complaint to the Council in question regarding the way in which they handled this matter. I requested a statement of my account, once settled, from Bristow and Sutor. This arrived today and I've included a copy of it as an attachment here: You'll see that a Bailiff had visited previously, after which I set up an arrangement. I made some errors in my accounting, and thinking the amount owing had been paid in full, I cancelled the payment arrangement I had in place. This was a silly mistake on my part I guess. Bristow and Sutor did not write to me about it and the next I heard was from the Council stating that the amount outstanding would be taken by DD. I thought the matter had been solved. Looking at this breakdown, I've paid in the region of £347.90 in fees in order to sort this out. I am not sure which of these fees are legal and which are not. Can Bailiffs really charge all these? For example, the debit card processing fee of 4% - this appears to me to be paying for the priviledge of paying with money! Certain sites on the internet indicate that these fees are fraudulent for various reasons and may consitute theft. Is this true? Aside from my complaint to the Council, which I doubt will result in a satisfactory conclusion from my point of view, does the forum know of any other way to get any of this money back? I look forward to any responses and advice I might get. All the best.

-

Hi All, Had a Capital One credit card with 200 pounds limit - at one point in 2007 it went upto 220 and over the course of a few months it escalated to 550! i wasn't aware of these charges as i didn't receive most of the paper work - also i was abroad for some of the time... i then partially settled it in 2008 - but was unaware that it will still be set as a default in 2007 and will not come off my credit file until end of 2013... I sent a letter in feb 2012 to the executive response team at Cap1 requesting for the default to be removed as it's ruining my life and that of my family - The amount increased from £200, simply because of the over limit “unfair” fee charges of £20 in addition to late payment charges of a further £20 plus purchase interest and cash interest – all of this eventually added up to £550 without my knowledge. Earlier today i rung them and understood that they sent a letter to my old address stating that this will be their last correspondence with me and any future communication will have to go through the financial ombudsman... and they have now cleared the balance off my credit report and instead of it saying "Partial settlement" which i settled back in 2008 - it will now state fully settled but the DEFAULT will remain till end of 2013... Is there anything i can do here to remove this DEFAULT??? Basically this default is of a small amount has ruined my Life and that of my family!!! Thank you in advance for your help..

-

I have just attempted to start the process of small claim court action - and where you inpit the address, as SL's address is in Scotland it wont let me continue... Can anyone advise me on what to do? STANDARD LIFE WAS BOUGHT BY BARCLAYS recently - should i be suing barclays instead? Also, if anyone else has issues with SL id love to hear - i have many letters ive sent that might help you! Xenia

-

Please can someone give me some sound advice...... 5 yrs ago i paid for my double glazing with interest free finance from GE Money. About 2 yrs ago I got into difficulty paying my direct debit on time, and although it was always paid it was often late, and GE Money always let me know this with numerous letters/reminders to myself, my wife, and both of us at the same time ! Now my 5 yrs is up and GE Money have informed me that I still owe £600 for late payment charges etc, so my payments will continue, interest free for another 10 months. I have no problems with making these payments and even contacted them and asked if I could settle the account with one payment if they were willing to discount it a bit, even by just 25%, to which they said No Way ! I have to pay the full amount as it was an interest free account. As I've said, I can afford the payments but it just drives me mad that they are so pedantic and unhelpful, So, the crux of the matter is, Can I in anyway reclaim these charges, simply for the satisfaction of getting them back !!??? Any advice, ie am i wasting my time, will be gratefully received, Many thanks B68

-

Hello to you all, I wonder if anyone can help. Some time ago, I went after A & L for unfair bank charges. They were bouncing £1 standing orders and charging me a fortune. It ended up about £350 + on charges. The case was stayed until the Office of Fair Trading V Abbey case was settled. I have now received a General Form of Judgement of Order. It states that the matter is listed for directions when the court will consider striking out the claim following of the decision of the Supreme Court test case (office of fair trading v Abbey National) and if the claimant (me) objects to the claim being struck out, written notice is required. I only got the letter this week and if I need to respond, it must be by Tuesday next week. Can anyone enlighten me on what I should now do? Grateful thanks to any help advice offered. I am bricking this as I am only on working tax credits at the moment and this sounds quite serious.

Hello to you all, I wonder if anyone can help. Some time ago, I went after A & L for unfair bank charges. They were bouncing £1 standing orders and charging me a fortune. It ended up about £350 + on charges. The case was stayed until the Office of Fair Trading V Abbey case was settled. I have now received a General Form of Judgement of Order. It states that the matter is listed for directions when the court will consider striking out the claim following of the decision of the Supreme Court test case (office of fair trading v Abbey National) and if the claimant (me) objects to the claim being struck out, written notice is required. I only got the letter this week and if I need to respond, it must be by Tuesday next week. Can anyone enlighten me on what I should now do? Grateful thanks to any help advice offered. I am bricking this as I am only on working tax credits at the moment and this sounds quite serious. -

I've been with littlewoods for years, set a direct debit for monthly payment from the very beginning. cos i am quite a careless person, in case i forget, i always set direct debit for payments . When i stopped receiving any catalogues or statements, i shopped elsewhere even left some credit in my Littlewoods account for a long time. Last christmas i shopped again from Littlewoods, with direct debit setting and credit left, i did not even think about the payment issue. On 2nd March 2011, I received a phone call from Littlewoods informed me that i had arrears totally 50 pounds, i was so confused and could not access the internet at that time, I requested a full statements to be sent and promised to pay after i find out what's happening to my account. Unfortunately , i did not receive anything after that and i totally forget about this. Most importantly, i was Not told there had been charges or there would be charges to my account whatsoever. Until few days before, on 8th April, I finally could access the internet, I logged on littlewoods to check my account, and was so shocked to find out my balance turned out to be 86 pounds! I called them right away, spoke with an adviser. According to her reply, littlewoods might remove my direct debit information since there were no activities for a year which i totally have no idea about that. Moreover, i was told that there were five charges added on my account but she could not tell me when did the charges start or how frequent they added those charges. I insisted to talk to the manager, she then promised to get the manager to call me back. But no calls from anyone that day or any following days. I filed a complaint on 8th April after the phone call, got an email back on 10th April said my complaint would pass to a manager. I was hoping the problem would be solved. But to my greatest anger, this morning when i logged on littlewoods, i found that there was another charge been added to my account again just yesterday 11th April, the total amount shows now 98pounds in arrears. Instead of giving me a definite answer, they just keep putting charges to my account. Here's my statement below. As you can see, within around one month period, they put 4 charges to my account, the most recent one was after i talked to them filed a complaint failed to get any response, Balance b/f from last statement PAYMENT NOT RECEIVEDOther Items 03/03/2011 Debt Collection Telephone Call Fee12.00 19/03/2011 Missed Minimum Payment Fee12.00 Pending ItemsAdjustments To Your Account 28/03/2011 Debt Collection Letter Fee12.00 4WK 11/04/2011 Debt Collection Letter Fee12.00 4WK According to this trend, every 10 days they claim to have sent a letter , which i have never ever received a single, would charge me 12 pounds, soon there will be hundreds of pounds arrears on my account!! It is so unfair!!! I am so frustrated guys!! I cant believe that's the way Littlewoods treat their customers, that's totally outrageous. Please, someone help me! Give me some advice to deal with them! Really drive me mad! Is it even legal???:sad::sad: Your time of reading this and any useful replies are very much appriciated !!

I've been with littlewoods for years, set a direct debit for monthly payment from the very beginning. cos i am quite a careless person, in case i forget, i always set direct debit for payments . When i stopped receiving any catalogues or statements, i shopped elsewhere even left some credit in my Littlewoods account for a long time. Last christmas i shopped again from Littlewoods, with direct debit setting and credit left, i did not even think about the payment issue. On 2nd March 2011, I received a phone call from Littlewoods informed me that i had arrears totally 50 pounds, i was so confused and could not access the internet at that time, I requested a full statements to be sent and promised to pay after i find out what's happening to my account. Unfortunately , i did not receive anything after that and i totally forget about this. Most importantly, i was Not told there had been charges or there would be charges to my account whatsoever. Until few days before, on 8th April, I finally could access the internet, I logged on littlewoods to check my account, and was so shocked to find out my balance turned out to be 86 pounds! I called them right away, spoke with an adviser. According to her reply, littlewoods might remove my direct debit information since there were no activities for a year which i totally have no idea about that. Moreover, i was told that there were five charges added on my account but she could not tell me when did the charges start or how frequent they added those charges. I insisted to talk to the manager, she then promised to get the manager to call me back. But no calls from anyone that day or any following days. I filed a complaint on 8th April after the phone call, got an email back on 10th April said my complaint would pass to a manager. I was hoping the problem would be solved. But to my greatest anger, this morning when i logged on littlewoods, i found that there was another charge been added to my account again just yesterday 11th April, the total amount shows now 98pounds in arrears. Instead of giving me a definite answer, they just keep putting charges to my account. Here's my statement below. As you can see, within around one month period, they put 4 charges to my account, the most recent one was after i talked to them filed a complaint failed to get any response, Balance b/f from last statement PAYMENT NOT RECEIVEDOther Items 03/03/2011 Debt Collection Telephone Call Fee12.00 19/03/2011 Missed Minimum Payment Fee12.00 Pending ItemsAdjustments To Your Account 28/03/2011 Debt Collection Letter Fee12.00 4WK 11/04/2011 Debt Collection Letter Fee12.00 4WK According to this trend, every 10 days they claim to have sent a letter , which i have never ever received a single, would charge me 12 pounds, soon there will be hundreds of pounds arrears on my account!! It is so unfair!!! I am so frustrated guys!! I cant believe that's the way Littlewoods treat their customers, that's totally outrageous. Please, someone help me! Give me some advice to deal with them! Really drive me mad! Is it even legal???:sad::sad: Your time of reading this and any useful replies are very much appriciated !! -

Hi, I would like to reclaim PPI and payment penalties on debts I am still paying off from 1999. The debts were transferred to collection agencies. My question is how do I go about reclaiming my PPI? Do I write to the original lender or the debt collection agencies? Is it possible some of these debts are unenforcible and if so how would I go about doing all 3 ie PPI, unfair charges and unenforceable agreements? Sorry for all the questions but new to this and really confused! Thanks

-

So... Last July (2009) I began having visits from a Rossendales Bailiff over a Magistrates Liability Order/Distress warrant for unpaid council tax. I immediately called them and asked what the balance I owed was. The reply was a disheartening £875.91. I stated that I was out of work and could afford to pay £50 a month from my jobseekers allowance, but was told this wouldn't fly, they said I had two accounts outstanding(??), the first charge was £473.11 and the second was £402.80. I was told that if I paid the £473.11 by the end of the month they would accept installments on the lower amount. I borrowed money from my partner and her father (which I am still paying off) and applied for a Budgeting Loan from the DWP. I promptly paid the £473.11 (plus a hidden admin charge for paying with a debit card) on 28/7/09. I received a receipt from this. The folllowing month I paid £202.80 and received a receipt saying that my balance was now £200. It was only then that I discovered some earlier correspondence from Rossendales (my partner would often leave unopened mail on the table and it simply got buried with other paperwork). The previous letters from Rossendales stated that the balances owed were £402.80 & £204.11 (including first visit & second visit charges) totalling £606.91 NOT the £875.91 they were claiming in July. Since I had already paid a total of £677.51 (proven in my bank statement) I had already paid £70 more than I needed to. I called them to ask where their figures came from and requested a breakdown of their charges before I paid them any more cash, they said that my account details were still with the bailiff in charge. I called him and he said that I had to call head office. This went back and forth several times until I said that I refuse to pay any more money until I had the paperwork I was legally entitled to. In November (two months after the phone calls) I received another letter stating that they agreed to accept installments and I did not adhere to them. I now owed £389.00 plus a further £110.00 should a van be sent to my address. Again, I called them and was given the same old spin. I didn't pay and didn't hear from them again until May this year, when the same notices were posted through the communal door of my block (not even in sealed envelopes) and left in the foyer for any Tom, Dick and Harry to see. I ignored these, because, as far as I'm concerned, I didn't receive them. More recently I've had handwritten notices posted through the door for me to "contact the bailiff in charge and discuss the o/s court warrant". I should also add that one of these pieces of paper had somebody elses credit card details written on the back!!! For the last month I have been receiving phone calls from the bailiff, but I'm still reluctant to pay until I receive a breakdown of charges. Rossendales slogan states that they are "Proud to be Professional". What an absolute joke they are!

So... Last July (2009) I began having visits from a Rossendales Bailiff over a Magistrates Liability Order/Distress warrant for unpaid council tax. I immediately called them and asked what the balance I owed was. The reply was a disheartening £875.91. I stated that I was out of work and could afford to pay £50 a month from my jobseekers allowance, but was told this wouldn't fly, they said I had two accounts outstanding(??), the first charge was £473.11 and the second was £402.80. I was told that if I paid the £473.11 by the end of the month they would accept installments on the lower amount. I borrowed money from my partner and her father (which I am still paying off) and applied for a Budgeting Loan from the DWP. I promptly paid the £473.11 (plus a hidden admin charge for paying with a debit card) on 28/7/09. I received a receipt from this. The folllowing month I paid £202.80 and received a receipt saying that my balance was now £200. It was only then that I discovered some earlier correspondence from Rossendales (my partner would often leave unopened mail on the table and it simply got buried with other paperwork). The previous letters from Rossendales stated that the balances owed were £402.80 & £204.11 (including first visit & second visit charges) totalling £606.91 NOT the £875.91 they were claiming in July. Since I had already paid a total of £677.51 (proven in my bank statement) I had already paid £70 more than I needed to. I called them to ask where their figures came from and requested a breakdown of their charges before I paid them any more cash, they said that my account details were still with the bailiff in charge. I called him and he said that I had to call head office. This went back and forth several times until I said that I refuse to pay any more money until I had the paperwork I was legally entitled to. In November (two months after the phone calls) I received another letter stating that they agreed to accept installments and I did not adhere to them. I now owed £389.00 plus a further £110.00 should a van be sent to my address. Again, I called them and was given the same old spin. I didn't pay and didn't hear from them again until May this year, when the same notices were posted through the communal door of my block (not even in sealed envelopes) and left in the foyer for any Tom, Dick and Harry to see. I ignored these, because, as far as I'm concerned, I didn't receive them. More recently I've had handwritten notices posted through the door for me to "contact the bailiff in charge and discuss the o/s court warrant". I should also add that one of these pieces of paper had somebody elses credit card details written on the back!!! For the last month I have been receiving phone calls from the bailiff, but I'm still reluctant to pay until I receive a breakdown of charges. Rossendales slogan states that they are "Proud to be Professional". What an absolute joke they are! -

Hi All, I recently moved house and my previous landlord is attempting to take most of my deposit. There were a two issues brought up during my tenancy that I admit are my fault and will owe compensation towards: 1) The bath room tiles did develop some stubborn mould in places. 2) The kitchen table at the premises (the only piece of furniture not owned by myself) has been damaged on its legs by my cat’s claws. But after an independent inventory inspection on the day I left the inspector told me there was nothing much to worry about, the table had existing chips and damage to it before I moved in and even though my cats have damaged it further, there was no photographic proof of the state of the legs before I moved in - only the slight chipped tabletop and that I should only pay £70-£80 towards repair. Prior to this, at his request I bought the landlord a new table after being asked to with only the specification of a suitable replacement wood table between £100 and £200 and after searching for and purchasing a more than suitable table, I get a demand to view said table on the day of its delivery and it was rejected as it was not an exact match (which I was never told to find) and blew £100+ on a table I don't need. This shows my willingness to make amends for the extra damage I admit has been caused to the table since I moved in, but I realise now I was stupid even considering to buy a NEW table when my cats only caused extra damage, the existing table was damaged BEFORE we even moved in and the inventory even specifies this. But now he wants £453 from my £500: £10 Clean cat hairs off lounge blind £10 Clean faint grubby markings off kitchen blind £5 Clean two sticky tab marks £25 to replace 5 light bulbs. £60 Tile grout discoloured (action taken: Refinish grout) £110 Bathroom Tile grout discoloured (action taken: Rake out joints, refinish grout + reseal) £38 - 3” of heating oil on a 250 gallon tank = 16 Gallons = 76 litres at 0.5p litre (not mentioned on inventory report or told to leave any in there) £195 Table damage I emailed the Agent and Landlord explaining what I agreed with, and mostly, what I did not as follows: I will not be paying the £38 for 3" of oil as the day I moved in I tried to use the heating and was told by the Landlords mother that I was not allowed to use it until I had ordered some more oil and so I turned the heating off. At no time was I told there was any amount in the tank on my arrival, nor was I told at any time I had to leave a certain amount, and there is no mentioned in my copy of the report from the inspector that there is any discrepancy, if I'd have known I would have left some. I was not allowed to use any oil when I moved in, and I left none as I moved out. 5 Light bulbs do not cost £25 - even taking in to account screwing them in. I will pay £10 for these and that's still including a small fee for "labour". I completely refuse to pay that much for the table to be repaired for the reasons given above. I asked to receive proof of the final cost of the work carried out on the tiles as I believe £170 is pushing it for the damage the inspector described to me as minimal. I said I believed £270 is a fair and honest price and is the maximum I am prepared to pay given the information I have been presented with. Bearing in mind that if the kitchen and bathroom tile work isn't as expensive as listed above when I am presented with the proof I expect this to be even less or I shall be taking action. My landlord responded with the following: The cost represents a tiler for one day plus materials. I have carried out the work myself and my rates are much higher. However, to keep in line with industry rates I have used the lower rate of a tiler, and have not included a management fee. The work could have been carried out by the tenant to minimise his costs, but he chose to leave it to me. I have also lost revenue whilst the work has been carried out, and this is not reflected in my costs, so I believe that I have been very generous. The boiler was in fact used for 3-4 weeks before any further supplies were delivered. However, AA inventories reported the level of oil as part of their initial property review, and the reported level should be reflected on departure from the property. AA inventories did not report against the level in their last report but was confirmed as approx 3". As above I have used the actual cost of the oil to replenish that used. I have not charged a management fee to replenish the oil on behalf of the tenant. Note: (The heating was not in use – I half froze to death wearing gloves and hats indoors for the first month until I got paid) The tenant had the opportunity to replace bulbs and chose not to. In addition to the purchase price of the bulbs the cost includes travel and time to purchase. The tenant will find that he too will incur similar costs for the same. On arrival the table was almost perfect with only a small amount of marks showing to the top face. The table top has further marking to its top face and extensive damaged to its legs caused by cats sharpening their claws. This is reported in the AA inventories report. My last inspection of some months prior to the tenant leaving identified the table damage and it was agreed that he should find a suitable replacement of the same size, style, quality, and finish. The table is a very good quality Victorian pine unit and an estimate of replacement cost was agreed at approx £200. At no time was he under pressure to purchase anything quickly. A very similar unit is for sale in Claire antiques centre for £235. The table Mr Sawyers chose as a replacement was not the same size, style, quality, or finish. He chose not to take my advice regarding its suitability prior to purchase, and my mother inspected the table in addition to my inspection via a mobile phone photograph. The proposed replacement, once discussed, was agreed to be unsuitable, and its rejection was completely avoidable by the tenant. The cost listed is for repair of the existing table to minimise costs to the tenant. The cost represents 1 days labour and materials for a tradesman. I have not included a management fee to organise its repair. Please refer to the AA inventories report. The table was in near perfect condition, and my repair costs are very reasonable and reflect today's tradesman rates. The house including the kitchen was left spotless by the outgoing previous tenant. The same cannot be said of any part of now. The tenant chose to leave the property in a condition requiring considerable effort and cost to recover its condition. The option to avoid cost was entirely his, and he chose to leave the premises in a sub standard condition, requiring costs to be incurred on his part. The costs identified are extremely reasonable, fair, and justified. They could have been far higher and I am extremely disappointed by his threatening attitude, when he alone is to blame for the costs. I do not agree that £270 is a fair price, and will not accept the tenants offer. As above my costs are extremely fair and reasonable, I hope that the tenant recognises the fact and settles without delay. If we cannot reach agreement by Friday 29th October I will withdraw my current offer, and seek to recover my full costs through legal channels. I sincerely hope that we do not have to resort to a legal resolution to this dispute, and that common sense will prevail on the tenant’s part. Any advice guys, the inventory inspector said nothing to worry about, the place was clean and the guy even said the kitchen was left “cleaner than when we moved in”. Yes I am to blame for the extra table leg damage but I can’t help but feel he is taking me for a ride asking for £195 on appox £235 table? If that was the case why offer to leave the table in for me when he knew I had cats and took the place unfurnished. Any advice would be greatly appreciated. Thank you, Chris.

Hi All, I recently moved house and my previous landlord is attempting to take most of my deposit. There were a two issues brought up during my tenancy that I admit are my fault and will owe compensation towards: 1) The bath room tiles did develop some stubborn mould in places. 2) The kitchen table at the premises (the only piece of furniture not owned by myself) has been damaged on its legs by my cat’s claws. But after an independent inventory inspection on the day I left the inspector told me there was nothing much to worry about, the table had existing chips and damage to it before I moved in and even though my cats have damaged it further, there was no photographic proof of the state of the legs before I moved in - only the slight chipped tabletop and that I should only pay £70-£80 towards repair. Prior to this, at his request I bought the landlord a new table after being asked to with only the specification of a suitable replacement wood table between £100 and £200 and after searching for and purchasing a more than suitable table, I get a demand to view said table on the day of its delivery and it was rejected as it was not an exact match (which I was never told to find) and blew £100+ on a table I don't need. This shows my willingness to make amends for the extra damage I admit has been caused to the table since I moved in, but I realise now I was stupid even considering to buy a NEW table when my cats only caused extra damage, the existing table was damaged BEFORE we even moved in and the inventory even specifies this. But now he wants £453 from my £500: £10 Clean cat hairs off lounge blind £10 Clean faint grubby markings off kitchen blind £5 Clean two sticky tab marks £25 to replace 5 light bulbs. £60 Tile grout discoloured (action taken: Refinish grout) £110 Bathroom Tile grout discoloured (action taken: Rake out joints, refinish grout + reseal) £38 - 3” of heating oil on a 250 gallon tank = 16 Gallons = 76 litres at 0.5p litre (not mentioned on inventory report or told to leave any in there) £195 Table damage I emailed the Agent and Landlord explaining what I agreed with, and mostly, what I did not as follows: I will not be paying the £38 for 3" of oil as the day I moved in I tried to use the heating and was told by the Landlords mother that I was not allowed to use it until I had ordered some more oil and so I turned the heating off. At no time was I told there was any amount in the tank on my arrival, nor was I told at any time I had to leave a certain amount, and there is no mentioned in my copy of the report from the inspector that there is any discrepancy, if I'd have known I would have left some. I was not allowed to use any oil when I moved in, and I left none as I moved out. 5 Light bulbs do not cost £25 - even taking in to account screwing them in. I will pay £10 for these and that's still including a small fee for "labour". I completely refuse to pay that much for the table to be repaired for the reasons given above. I asked to receive proof of the final cost of the work carried out on the tiles as I believe £170 is pushing it for the damage the inspector described to me as minimal. I said I believed £270 is a fair and honest price and is the maximum I am prepared to pay given the information I have been presented with. Bearing in mind that if the kitchen and bathroom tile work isn't as expensive as listed above when I am presented with the proof I expect this to be even less or I shall be taking action. My landlord responded with the following: The cost represents a tiler for one day plus materials. I have carried out the work myself and my rates are much higher. However, to keep in line with industry rates I have used the lower rate of a tiler, and have not included a management fee. The work could have been carried out by the tenant to minimise his costs, but he chose to leave it to me. I have also lost revenue whilst the work has been carried out, and this is not reflected in my costs, so I believe that I have been very generous. The boiler was in fact used for 3-4 weeks before any further supplies were delivered. However, AA inventories reported the level of oil as part of their initial property review, and the reported level should be reflected on departure from the property. AA inventories did not report against the level in their last report but was confirmed as approx 3". As above I have used the actual cost of the oil to replenish that used. I have not charged a management fee to replenish the oil on behalf of the tenant. Note: (The heating was not in use – I half froze to death wearing gloves and hats indoors for the first month until I got paid) The tenant had the opportunity to replace bulbs and chose not to. In addition to the purchase price of the bulbs the cost includes travel and time to purchase. The tenant will find that he too will incur similar costs for the same. On arrival the table was almost perfect with only a small amount of marks showing to the top face. The table top has further marking to its top face and extensive damaged to its legs caused by cats sharpening their claws. This is reported in the AA inventories report. My last inspection of some months prior to the tenant leaving identified the table damage and it was agreed that he should find a suitable replacement of the same size, style, quality, and finish. The table is a very good quality Victorian pine unit and an estimate of replacement cost was agreed at approx £200. At no time was he under pressure to purchase anything quickly. A very similar unit is for sale in Claire antiques centre for £235. The table Mr Sawyers chose as a replacement was not the same size, style, quality, or finish. He chose not to take my advice regarding its suitability prior to purchase, and my mother inspected the table in addition to my inspection via a mobile phone photograph. The proposed replacement, once discussed, was agreed to be unsuitable, and its rejection was completely avoidable by the tenant. The cost listed is for repair of the existing table to minimise costs to the tenant. The cost represents 1 days labour and materials for a tradesman. I have not included a management fee to organise its repair. Please refer to the AA inventories report. The table was in near perfect condition, and my repair costs are very reasonable and reflect today's tradesman rates. The house including the kitchen was left spotless by the outgoing previous tenant. The same cannot be said of any part of now. The tenant chose to leave the property in a condition requiring considerable effort and cost to recover its condition. The option to avoid cost was entirely his, and he chose to leave the premises in a sub standard condition, requiring costs to be incurred on his part. The costs identified are extremely reasonable, fair, and justified. They could have been far higher and I am extremely disappointed by his threatening attitude, when he alone is to blame for the costs. I do not agree that £270 is a fair price, and will not accept the tenants offer. As above my costs are extremely fair and reasonable, I hope that the tenant recognises the fact and settles without delay. If we cannot reach agreement by Friday 29th October I will withdraw my current offer, and seek to recover my full costs through legal channels. I sincerely hope that we do not have to resort to a legal resolution to this dispute, and that common sense will prevail on the tenant’s part. Any advice guys, the inventory inspector said nothing to worry about, the place was clean and the guy even said the kitchen was left “cleaner than when we moved in”. Yes I am to blame for the extra table leg damage but I can’t help but feel he is taking me for a ride asking for £195 on appox £235 table? If that was the case why offer to leave the table in for me when he knew I had cats and took the place unfurnished. Any advice would be greatly appreciated. Thank you, Chris. -

I'm at a bit of a loss with how to proceed with this letter that I received today from Marstons. The history behind it is that I had a Magistrates Court fine for a car without tax that wasn't even my car ! (someone else registered it in my name and forged my signature). I accepted the fine for £448.34, and set up a standing order from my account to pay monthly amounts of £50. The payments finished April this year, and I never heard anything about it until this letter today, that claimed the amount outstanding is £323.34 !! So I phoned up Marstons, and explained that the court fine was paid off, to no avail. I checked my bank account for proof, and saw that every payment for £50 was taken out, but the final payment of £48.34 wasn't, why I don't know since I set up the standing order correctly. So in effect, I still owe £48.34, which is fine, i'm happy to pay what I ought to. Marstons seem to have added a compliance fee of £75, and an Attendance fee of £200 !!!! Can they demand this of me ?? I have never had a visit, call or letter or any communication until today, via a letter. I would like to know the best way to approach this - I cannot afford almost 3/4 of the original fine for "fees" again !! If I was just contacted by someone, i'd have paid the outstanding £48.34 which was the last and only payment missed BTW !

I'm at a bit of a loss with how to proceed with this letter that I received today from Marstons. The history behind it is that I had a Magistrates Court fine for a car without tax that wasn't even my car ! (someone else registered it in my name and forged my signature). I accepted the fine for £448.34, and set up a standing order from my account to pay monthly amounts of £50. The payments finished April this year, and I never heard anything about it until this letter today, that claimed the amount outstanding is £323.34 !! So I phoned up Marstons, and explained that the court fine was paid off, to no avail. I checked my bank account for proof, and saw that every payment for £50 was taken out, but the final payment of £48.34 wasn't, why I don't know since I set up the standing order correctly. So in effect, I still owe £48.34, which is fine, i'm happy to pay what I ought to. Marstons seem to have added a compliance fee of £75, and an Attendance fee of £200 !!!! Can they demand this of me ?? I have never had a visit, call or letter or any communication until today, via a letter. I would like to know the best way to approach this - I cannot afford almost 3/4 of the original fine for "fees" again !! If I was just contacted by someone, i'd have paid the outstanding £48.34 which was the last and only payment missed BTW ! -

Hi. I really don't know much about the differences between all these different agreements, but basically I lived in a house where the landlord, moved away, his tenant (and friend) remained in the house and I moved in. We had a license agreement between the three of us. They then turned quite nasty after I said I wanted to leave (after 6 months) being very horrible indeed (details of which I won't go in to!). I moved out over a month ago, I didn't want them to have my new address here so gave them my parents (the letting agency have been helping me, although they have no contractual obligation, they felt they were harrassing me, and didn't want them to have my new address either, the Landlord and other tenant refused to use my work address.) However my mum has received a letter from them today, with a cheque for about £115 (my deposit was £375) with deductions for £80 to have the lock changed (which was not in my agreement), £50 for cutlery (WHAT!!!) and stupid things like £5 for batterys from remotes (really petty!) and £85 for cleaning, even though the letting agent who carried out the inspection said everything was fine! They have said they can provide receipts, which is fair, but I don't see why I should incur these charges. I took pictures of everywhere before I left, but they are on my digital camera so don't know how these would hold up if it did go further. Any advice?? I'm so glad to be out of there and really want this all to be over, I'm starting to think that I don't actually care about the money, but why should they get to keep it??? Many thanks in advance for your help!!!