Search the Community

Showing results for tags 'termination'.

-

Hi All, I am looking for some help, my husband has recently passed his driving test but only has an automatic licence and we are in the process of changing our car. We have already been accepted for finance for a new car with another company with better rates. We took out HP finance with Advantage Finance in July 2016, the agreement was for 54 months. If my calculations are correct we have made 29 payments back which is over the 50% they state you need to pay before you can proceed with a VT. I have sent an email and letter to inform them I was to terminated with immediate effect and I am awaiting their reply. (I have attached a copy of the letter/email sent) I have never been in this situation before and want to know what my next steps should be? I have never been in arrears with them, never missed a payment or been late with a payment. I just made a payment for the car on the 26th January 2019 (this would have been payment 29), should I still make my payment in February on should I cancel my direct debit? I have been reading quite a few threads lately on dealing with Advantage when proceeding with a VT and I am petrified they try and charge us extra for scratches etc. that were already on the car when we originally purchased it. I will take lots of photos before it goes back, I have had it professionally valeted and washed also. Any help is much appreciated.

Hi All, I am looking for some help, my husband has recently passed his driving test but only has an automatic licence and we are in the process of changing our car. We have already been accepted for finance for a new car with another company with better rates. We took out HP finance with Advantage Finance in July 2016, the agreement was for 54 months. If my calculations are correct we have made 29 payments back which is over the 50% they state you need to pay before you can proceed with a VT. I have sent an email and letter to inform them I was to terminated with immediate effect and I am awaiting their reply. (I have attached a copy of the letter/email sent) I have never been in this situation before and want to know what my next steps should be? I have never been in arrears with them, never missed a payment or been late with a payment. I just made a payment for the car on the 26th January 2019 (this would have been payment 29), should I still make my payment in February on should I cancel my direct debit? I have been reading quite a few threads lately on dealing with Advantage when proceeding with a VT and I am petrified they try and charge us extra for scratches etc. that were already on the car when we originally purchased it. I will take lots of photos before it goes back, I have had it professionally valeted and washed also. Any help is much appreciated. -

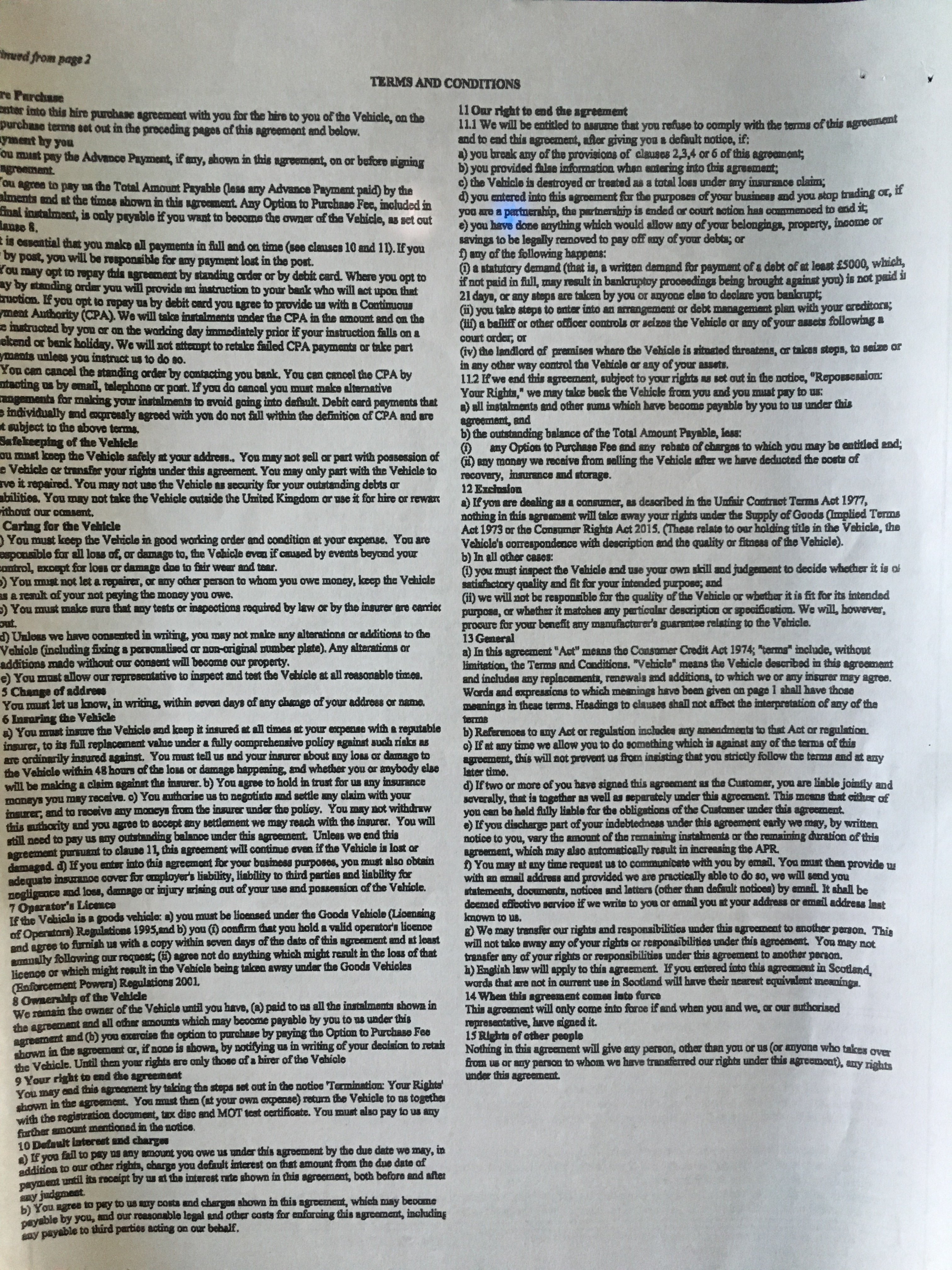

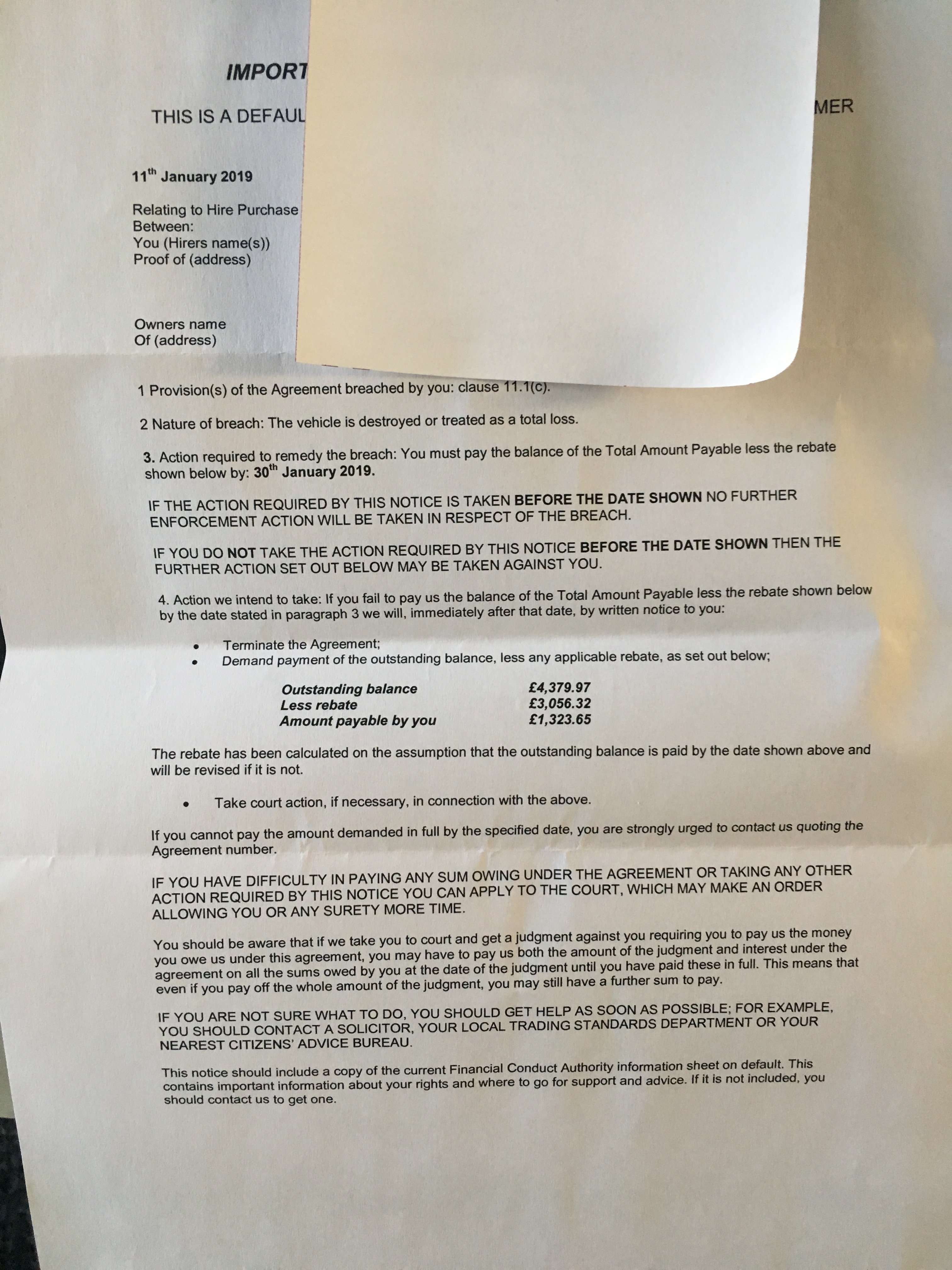

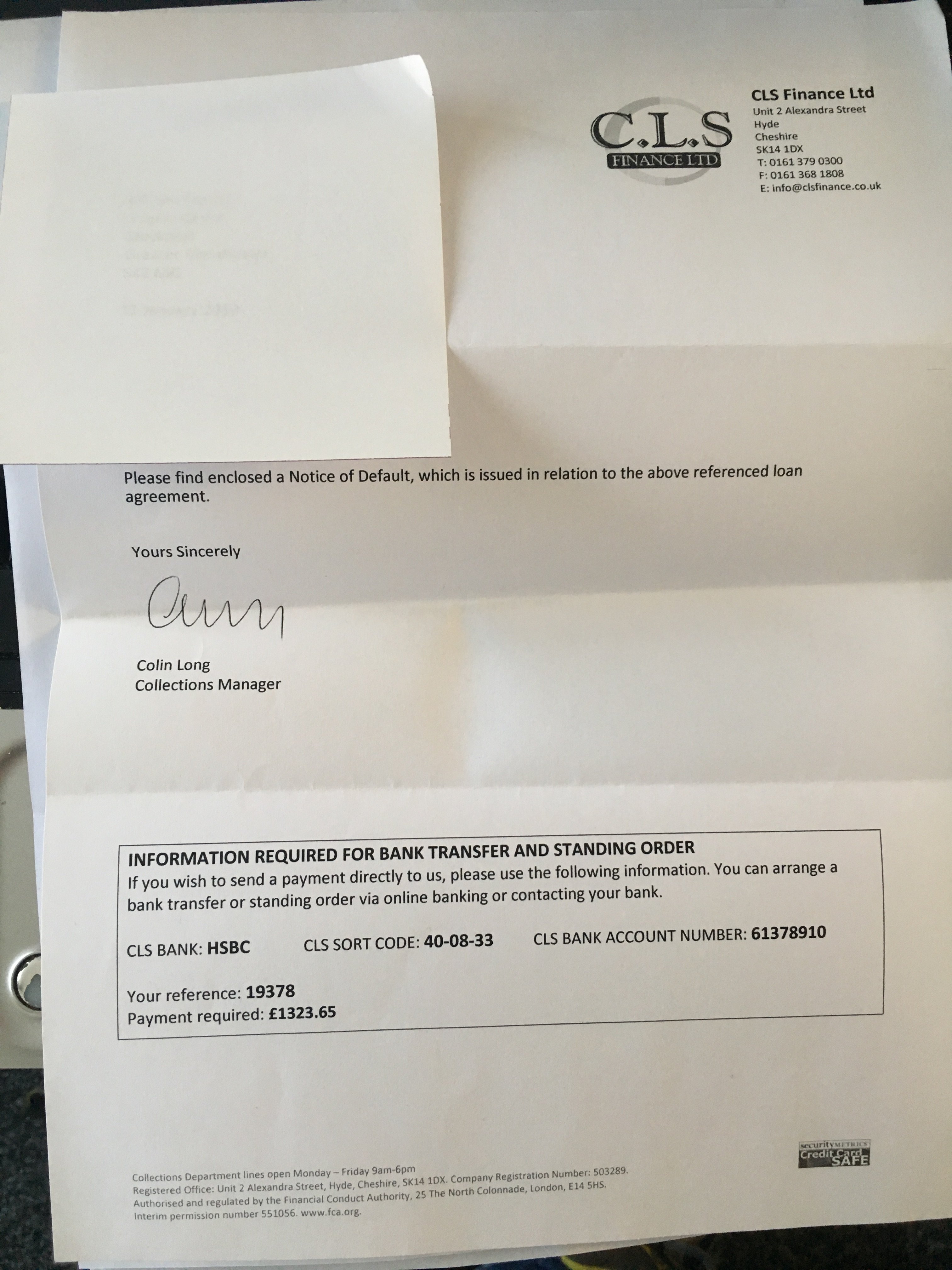

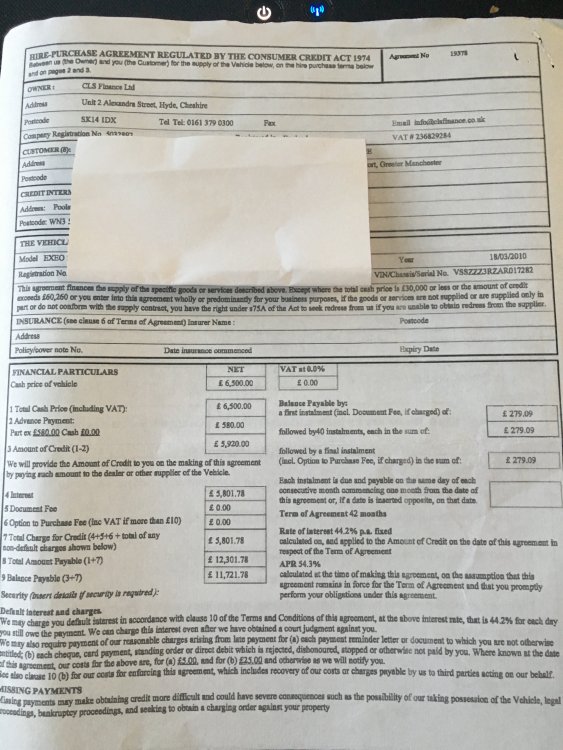

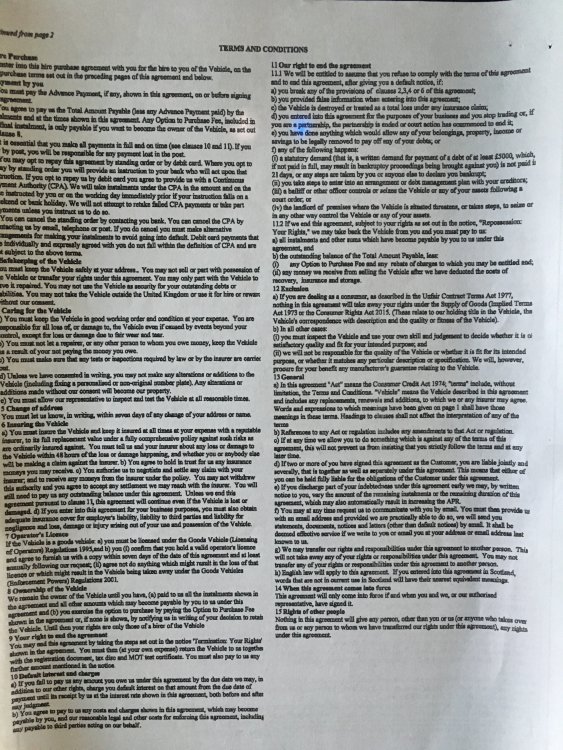

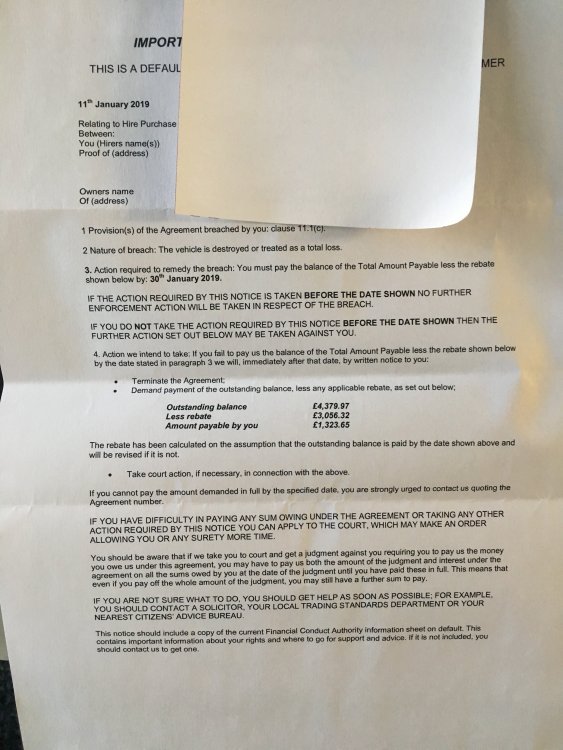

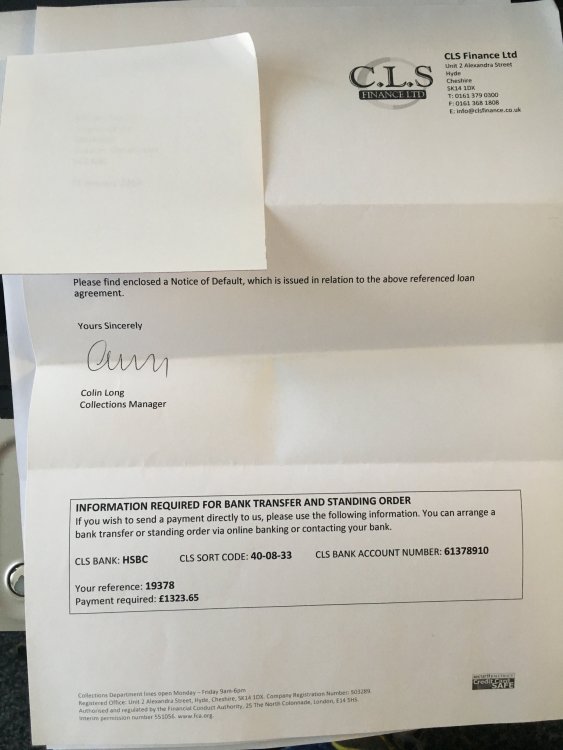

Hi All, I'm after some advise please, I took out a joint HP agreement last January with these, all payments up to date until I wrote off the vehicle in October, the insurance paid them a settlement figure and CLS advised them there was a £433 shortfall, as it was almost Christmas it slipped my mind, 11th Jan both my partner and I received a default notice for £1323, now this morning, received a termination letter stating 'subject to clause 9.2 of the agreement, you must now pay the full outstanding balance to us of £4379, can someone please advise where I stand with this? copies attached thanks

Hi All, I'm after some advise please, I took out a joint HP agreement last January with these, all payments up to date until I wrote off the vehicle in October, the insurance paid them a settlement figure and CLS advised them there was a £433 shortfall, as it was almost Christmas it slipped my mind, 11th Jan both my partner and I received a default notice for £1323, now this morning, received a termination letter stating 'subject to clause 9.2 of the agreement, you must now pay the full outstanding balance to us of £4379, can someone please advise where I stand with this? copies attached thanks

-

hello any advise would be greatly appreciated. 6 months ago we bought a Audi a3 on finance over a 4year contract after a few weeks the Audi started cutting out while driving and would roll to a complete stop RAC called out recovered to a garage after a week no faults were found and we collected the car this started happening on a weekly basis after an hour or so the car would start and go until it cut out again. we got in contact with the car sales garage they agreed to cover any costs as long as it was not caused through wear/tear rang finance company and made a complaint. after 5 & half months 3 different garages including Audi themselves and multiple RAC call outs nobody can find a reason to why this is happening. call finance company to ask if I could vt the finance to which they informed me they hadn't started the complaints procedure the first time I complained (about 15 calls ago) and I only had 10 days left to be within the 6 months fix or replace policy. the last 2 weeks of jumping through hoops more fault finding ideas, diagnostic tests, road test through main dealer (still no solutions) and letters from previous garages for evidence of fault as requested by them. I received a call today saying as there not enough evidence to prove a fault they are going to close the complaint and allow me to voluntary terminate the finance agreement and there will be a bill of 5250 pound plus cost of recovering the vehicle as its unsafe to drive.:-x:-x I have no idea where or what to do at the moment so any advise on this would be great. thank you for taking the time to read this

hello any advise would be greatly appreciated. 6 months ago we bought a Audi a3 on finance over a 4year contract after a few weeks the Audi started cutting out while driving and would roll to a complete stop RAC called out recovered to a garage after a week no faults were found and we collected the car this started happening on a weekly basis after an hour or so the car would start and go until it cut out again. we got in contact with the car sales garage they agreed to cover any costs as long as it was not caused through wear/tear rang finance company and made a complaint. after 5 & half months 3 different garages including Audi themselves and multiple RAC call outs nobody can find a reason to why this is happening. call finance company to ask if I could vt the finance to which they informed me they hadn't started the complaints procedure the first time I complained (about 15 calls ago) and I only had 10 days left to be within the 6 months fix or replace policy. the last 2 weeks of jumping through hoops more fault finding ideas, diagnostic tests, road test through main dealer (still no solutions) and letters from previous garages for evidence of fault as requested by them. I received a call today saying as there not enough evidence to prove a fault they are going to close the complaint and allow me to voluntary terminate the finance agreement and there will be a bill of 5250 pound plus cost of recovering the vehicle as its unsafe to drive.:-x:-x I have no idea where or what to do at the moment so any advise on this would be great. thank you for taking the time to read this -

Hi We had a car for 4 years with VW - the lease ended in March 2018 - they collected the car in September 2018. We have today been presented with a bill for £1368 from a solicitor (Blake Morgan) acting on behalf of VW - they have listed to damages and the cost but it is outrageous - any ideas how this can be challenged?

-

My wife has a CCJ to the value of roughly £800 from vodafone, containing what i presume would be a large value of early termination fees. She has made one payment towards this, as she only became aware of it last month (dont ask, burying the head in the sand...) Now, ive seen some members on here stating that OFCOM are against early termination fees being included in a CCJ/default? Is that correct? maybe dx100uk you know more? as its one of your posts referencing termination charges and mobile contracts that i have referenced

-

Hi Everyone, I would really appreciate your help here, as I think the Post Office home insurance are mis-advising people. I am moving out of my housing association flat to a house I just bought with my girlfriend. I have a 6 week overlap for the two properties so we can renovate and decorate prior to moving in. I already have contents insurance for the new house. My flat was covered for the last 6 years by the Post Office, I told them I am moving and have to cancel the insurance as there is already insurance at the new house, so they can't insure it. As such they have to cancel insurance at the flat as I won't be living there and can't transfer the insurance to my new property. However, they are still wanting to charge me an £35 early cancellation fee. Surely this isn't right, as they can no longer legally provide a service to me? Are they [causing problems] people like me out of £35? Many thanks in advance!

Hi Everyone, I would really appreciate your help here, as I think the Post Office home insurance are mis-advising people. I am moving out of my housing association flat to a house I just bought with my girlfriend. I have a 6 week overlap for the two properties so we can renovate and decorate prior to moving in. I already have contents insurance for the new house. My flat was covered for the last 6 years by the Post Office, I told them I am moving and have to cancel the insurance as there is already insurance at the new house, so they can't insure it. As such they have to cancel insurance at the flat as I won't be living there and can't transfer the insurance to my new property. However, they are still wanting to charge me an £35 early cancellation fee. Surely this isn't right, as they can no longer legally provide a service to me? Are they [causing problems] people like me out of £35? Many thanks in advance! -

As i understand it I can Voluntary Termination at any time but will be liable to 50% of the total agreement. I intend to VT my HP agreement however I am £93.00 away from 50%. If I send notification of VT on Monday along with a cheque for £93.00 would this be accepted?

-

hi, could somebody explain the purpose of a termination notice? i have been served a termination notice 14 days after being served a default notice which i believe to be correct. however i have been served another default notice which is dated the same day as the termination notice. also i am still receiving threats of fees and charges and am wondering the point of the termination notice.

hi, could somebody explain the purpose of a termination notice? i have been served a termination notice 14 days after being served a default notice which i believe to be correct. however i have been served another default notice which is dated the same day as the termination notice. also i am still receiving threats of fees and charges and am wondering the point of the termination notice. -

i am writing on behalf of my wife. she was employed as a manager for just over 6 months, her employer phoned her up just under a week ago and told her they was terminating her contract as of immediate effect. This was done without any probation meetings and no meetings prior to raise any concerns. I don't want to go into much detail as at the moment she has just started by raising this problem with ACAS. The employer has since claimed via a letter a fictitious probation meeting took place AFTER the dismissal via phone call! This was probably done by them to distract from they acted unprofessional and possibly against employment law. She had disclosed all her health problems at the original job interview and recently was found to have some other problems arise during her employment. She has had time off because of her disclosed health problems but these have been for hospital appointments and she was told to put them in as sometimes sick and sometimes annual leave. Just before the phone call terminating her employment she had informed her Line manager she was going to the GP as she has been under a significant amount of stress with her job, within 10 minutes of notifying the line manage she received the call from the owner of the company terminating her contract. The doctor who assesses her gave her a fit for work note stated work related stress. i would like to point out that they are not going down the health route for sacking as that would be discrimination and they was made aware of that by my wife about 5 months into her employment after they was complaining about time off for appointments. She told her employers she was going to acas as she felt she had not been treated fairly to which the owner said they have a lot of businesses and have a lot of solicitors that they can seek advice from if she chooses to go down that route. anyway i went off course a little but i felt i needed to share a little info as a lead up to my question. As she has already seeking advice from acas under the new data protection rules would/should she make a SAR request to see exactly what info they have or wait until it goes to tribunal? is there a template for an SAR request with the new rules listed and also what can she ask for... also is it possible to ask for any emails, possible taped phone conversations although my wife was never told of any phone conversations that were being recorded, texts, correspondants etc which my wifes name is included in. any info would be greatly appreciated thank you

-

Hi fellow caggers, looking a bit of advice for my partner She opened a Halifax Rewards account in 2002 with her Ex husband They separated in 2011 and there was an OD on the account He sub sequentially left all the debt to her, he managed to remove himself from the account by paying a small amount, I will say he was a Halifax employee. The last payment into the account was feb 13 by my partner and the account was defaulted on her credit report in Dec 13 It was sold onto Hoist and is being managed by Wescot, we have not acknowledged the debt and sent them a prove it in January which they still havent complied with and the account is on hold My partner never received a termination notice and we have sub sequentially SAR'd Halifax and received a mountain of paperwork today. I can upload any thing that you need to see Looking through it there is no reference to a termination notice and have noticed from an initial balance of ~£300 the debt stands at ~£800 which is all charges Can she challenge Halifax to remove the default? Also can she reclaim the charges under BCOBS?

Hi fellow caggers, looking a bit of advice for my partner She opened a Halifax Rewards account in 2002 with her Ex husband They separated in 2011 and there was an OD on the account He sub sequentially left all the debt to her, he managed to remove himself from the account by paying a small amount, I will say he was a Halifax employee. The last payment into the account was feb 13 by my partner and the account was defaulted on her credit report in Dec 13 It was sold onto Hoist and is being managed by Wescot, we have not acknowledged the debt and sent them a prove it in January which they still havent complied with and the account is on hold My partner never received a termination notice and we have sub sequentially SAR'd Halifax and received a mountain of paperwork today. I can upload any thing that you need to see Looking through it there is no reference to a termination notice and have noticed from an initial balance of ~£300 the debt stands at ~£800 which is all charges Can she challenge Halifax to remove the default? Also can she reclaim the charges under BCOBS? -

This 3rd party mobile provider contacted me (Unsolicited) around Feb 2017 telling me that my small business contract with o2 was coming to an end. As an O2 "Partner" they had all my information and could provide me with a great deal. I stupidly signed a 3year contract with a "Deal Incentive" whereby they would pay a sum to me to reduce my line rental to £25 a month, I got 1 payment in April then nothing until in Jan 2018 I sent them a letter of contract cancellation due to "Material Breach of Contract". My bill rose from £35 to £92 for 3gb of data and no phone !! Despite several letters and calls to o2 to cancel this contract I am still waiting. Beware of this company please, I will keep you updated !!

-

Hi all, Im just after some advice…. I am currently in a IVA and when it was accepted allowances were made for my car payment to black horse. To cut a long story short, things have changed rapidly and my income has stayed the same, well it’s actually due to go down and my expenditure is going to rise. This means that I can no longer afford the vehicle that the allowance was made for. Im ok with that, My dad is going to gift me an old car to be able to run, and on completing my income and expenditure form, if I get rid of the current PCP vehicle then I can still afford to live etc and afford my payment to my IVA. I have spoke to my IP and they have said that I can terminate the agreement with BH and the negative debt will be passed on to my IVA as it was taken out before the IVA was accepted. (So I get all that) However…… I have spoke to BH over the last couple of days and they have told me that I must write a letter Voluntary Surrendering the vehicle, drive it to an auction house and they will pass the liabilities to my IVA. BUT. The figure is massive! I purchased a car on a PCP plan for £31,650.98 with zero deposit The total I would have to pay would be £38,207.62 (including balloon) My monthly payments are 47 payments of £455.46 followed by a final payment of £16,801.00 I have currently been in the agreement for 12 months (again circumstances changed quickly due to no fault of my own) So that is £5465.52 I have paid. My current settlement on the Vehicle is £28,846.49 The vehicle is worth currently £24,000ish trade value. They have said I need to Voluntary Surrender the car and my liability is £14093.75 which will be passed on to the IVA. BUT how is this if my settlement is £28,846.49, shouldn’t it be closer to £4846.49? Is this the same as a Voluntary Termination? or is that more expensive/cheaper? Im just a bit stumped how my settlement can be 29k and they get 24k back and still want the remaining settlement including interest when I no longer pay monthly or have the vehicle? I need to get this sorted, as my insurance for the car is due in a week and I do not want to/can afford to insure it. Please advise and thank you in advance Also just to add, as this might change things quite a bit, I received a letter from BH when I did my IVA saying that they intend to terminate my agreement on 27th March 2018 under section 76(1) of the consumer credit act 1974 as I had made a application for a voluntary arrangement.

Hi all, Im just after some advice…. I am currently in a IVA and when it was accepted allowances were made for my car payment to black horse. To cut a long story short, things have changed rapidly and my income has stayed the same, well it’s actually due to go down and my expenditure is going to rise. This means that I can no longer afford the vehicle that the allowance was made for. Im ok with that, My dad is going to gift me an old car to be able to run, and on completing my income and expenditure form, if I get rid of the current PCP vehicle then I can still afford to live etc and afford my payment to my IVA. I have spoke to my IP and they have said that I can terminate the agreement with BH and the negative debt will be passed on to my IVA as it was taken out before the IVA was accepted. (So I get all that) However…… I have spoke to BH over the last couple of days and they have told me that I must write a letter Voluntary Surrendering the vehicle, drive it to an auction house and they will pass the liabilities to my IVA. BUT. The figure is massive! I purchased a car on a PCP plan for £31,650.98 with zero deposit The total I would have to pay would be £38,207.62 (including balloon) My monthly payments are 47 payments of £455.46 followed by a final payment of £16,801.00 I have currently been in the agreement for 12 months (again circumstances changed quickly due to no fault of my own) So that is £5465.52 I have paid. My current settlement on the Vehicle is £28,846.49 The vehicle is worth currently £24,000ish trade value. They have said I need to Voluntary Surrender the car and my liability is £14093.75 which will be passed on to the IVA. BUT how is this if my settlement is £28,846.49, shouldn’t it be closer to £4846.49? Is this the same as a Voluntary Termination? or is that more expensive/cheaper? Im just a bit stumped how my settlement can be 29k and they get 24k back and still want the remaining settlement including interest when I no longer pay monthly or have the vehicle? I need to get this sorted, as my insurance for the car is due in a week and I do not want to/can afford to insure it. Please advise and thank you in advance Also just to add, as this might change things quite a bit, I received a letter from BH when I did my IVA saying that they intend to terminate my agreement on 27th March 2018 under section 76(1) of the consumer credit act 1974 as I had made a application for a voluntary arrangement. -

New rules for taxation of termination payments READ MORE HERE: https://www.gov.uk/government/news/new-rules-for-taxation-of-termination-payments

-

I have a vehicle on finance from Trax Motor Finance which is just short of the halfway mark. Due to ill health I a no longer able to drive it so I sent a request to voluntary terminate using a letter template from this site. I sent I recorded and they have signed for it and acknowledged it via email. I know that there will be some liability left to see the agreement to the half way mark and have detailed this in the VT sent to them. They are insisting that I contact them via phone to sort out the details but I have replied on several occasions that I will only communicate via email or letter so that I have a paper trail and that I am not contactable by phone as I am currently in hospital. I have sent a second recorded letter reiterating the request with a copy of the original request which they have also acknowledged and again insist that I contact them by phone about my voluntary surrender. I have replied very sternly and pointed out many times that under no circumstances do I want to voluntary surrender and pointed out many times that it is a voluntary termination request . They say that they cannot communicate via letter or email due to data protection. I then pointed out to them that I have received several communications from them via email and letter discussing personal and financial business so data protection has nothing to do with it when it suits them. I have threatened them with the FCA as I am getting nowhere with them and I have a car that will be rotting away on my drive if they do not take it away but what else can I do now as they are refusing my VT request unless I speak to them on the phone.

I have a vehicle on finance from Trax Motor Finance which is just short of the halfway mark. Due to ill health I a no longer able to drive it so I sent a request to voluntary terminate using a letter template from this site. I sent I recorded and they have signed for it and acknowledged it via email. I know that there will be some liability left to see the agreement to the half way mark and have detailed this in the VT sent to them. They are insisting that I contact them via phone to sort out the details but I have replied on several occasions that I will only communicate via email or letter so that I have a paper trail and that I am not contactable by phone as I am currently in hospital. I have sent a second recorded letter reiterating the request with a copy of the original request which they have also acknowledged and again insist that I contact them by phone about my voluntary surrender. I have replied very sternly and pointed out many times that under no circumstances do I want to voluntary surrender and pointed out many times that it is a voluntary termination request . They say that they cannot communicate via letter or email due to data protection. I then pointed out to them that I have received several communications from them via email and letter discussing personal and financial business so data protection has nothing to do with it when it suits them. I have threatened them with the FCA as I am getting nowhere with them and I have a car that will be rotting away on my drive if they do not take it away but what else can I do now as they are refusing my VT request unless I speak to them on the phone. -

Recently employed on a three month probation contract in an industry I had not previously worked in. My employer recruited me based upon my skills and achievements at a far larger organisation with the intention of modernising their working practices. On my first day of working I had my role & responsibilities but received no targets, objectives, training or guidance and was told "off you go". Due to the small size and skills of the workforce obtaining information became difficult but I managed to understand the business set-up and started collating information, completed any tasks assigned and even sourced potential new business from a former employer. My manager has now decided with 3 weeks to go that "I am not a fit for their business as they work a different way to what I am used to " (they were pretty backward) I actually feel aggrieved at this decision as: - I had two monthly reviews where my performance or lack off was not discussed. - The reviews were at short notice (I had prepared from experience),not documented and new objectives not set. - Information & improvements submitted had not been read by other employees even after prompting. - The manager had been made aware that I could not tie down the necessary employees to get information,yet nothing happened - All tasks that were assigned were completed or in progress within timescales. - My termination meeting was again at short notice and out of the blue as I had no indication I was not performing. - The "not fit" reason was very weak and when I enquired in which areas they would not discuss it. I believe throughout that they have acted below what I would expect from a company and to dismiss me without following employment guidelines is very poor. Acas have been consulted and they agree that guidelines have not been followed and suggest that I follow procedure and appeal. Has anyone else experienced anything similar and what was the outcome? I would not want to work for this company again but they have left me at short notice with no income at the end of this month. If I knew I was under performing I would have tried to address this or look for another position.

-

I have a car I've paid over half of and wish to return. I emailed them Friday to a previous correspondence address, no reply, I called them yesterday morning and "no one was available right now in VT department" they gave me a direct email address, still no reply. I want this returned by 20th as I'm going away, can I force them in to a speed up? What is reasonable notice? also does mileage penalty apply to the halves rule? The wording in my document says "You have the right to end this agreement. To do so, you should write to the person you made your payments to. They will then be entitled to the return of the goods and to half the total amount payable under this agreement, that is £11891.97. If you have already paid as least this amount plus any overdue instalments and have taken reasonable care of the goods, you will not have to pay any more." That seems pretty clear to me there is no more to pay?

I have a car I've paid over half of and wish to return. I emailed them Friday to a previous correspondence address, no reply, I called them yesterday morning and "no one was available right now in VT department" they gave me a direct email address, still no reply. I want this returned by 20th as I'm going away, can I force them in to a speed up? What is reasonable notice? also does mileage penalty apply to the halves rule? The wording in my document says "You have the right to end this agreement. To do so, you should write to the person you made your payments to. They will then be entitled to the return of the goods and to half the total amount payable under this agreement, that is £11891.97. If you have already paid as least this amount plus any overdue instalments and have taken reasonable care of the goods, you will not have to pay any more." That seems pretty clear to me there is no more to pay? -

Good Afternoon everyone, Having had a read of these forums I have seen how helpful you have been with offering advice to other people so decided to register and post my own situation to see if you can offer me any advice. I am currently a private tenant through a letting agent. I originally signed an Assured Shorthold Tenancy Agreement on the 1st October 2016, which was a 12 month agreement with a 6 Month break clause. This agreement was signed by both myself and my Girlfriend at the time, so this original tenancy has not yet ended. On the 12 June 2017 (3 and a half months before the tenancy end date) I was contacted by the letting agent to re sign a new agreement which would run from 1st October 2017 for a further 12 months, with a 6 month break clause, so this is still a month away from actually commencing. The tenancy is still in the names of both myself and my girlfriend at the time (with myself listed as the lead tenant). Since signing the tenancy agreement on the 12th June 2017 I have had a change in circumstances, in that myself and my girlfriend are no longer together (this happened in the last week). As such I am now in a rather dire situation where I face having to pay a minimum of another 7 months worth of rent (£1200 per month) which on my own I simply cannot afford to do, I don't earn enough on my own to cover the cost of this and council tax/other bills etc. I was wondering if anyone would be able to advise me where I stand legally with regards to now cancelling the tenancy agreement due to start on the 1st October 2017. From what I understand this is only possible with the landlords consent and I would be liable for any costs incurred to re let the property, however as I am the current tenant, at the end of the current agreement I only needed to give 30 days notice, so would this apply? I wanted to know what (if anything) I can do to cancel the AST from the 1st October. Any advice or help would be greatly appreciated. Thanks Jamie

Good Afternoon everyone, Having had a read of these forums I have seen how helpful you have been with offering advice to other people so decided to register and post my own situation to see if you can offer me any advice. I am currently a private tenant through a letting agent. I originally signed an Assured Shorthold Tenancy Agreement on the 1st October 2016, which was a 12 month agreement with a 6 Month break clause. This agreement was signed by both myself and my Girlfriend at the time, so this original tenancy has not yet ended. On the 12 June 2017 (3 and a half months before the tenancy end date) I was contacted by the letting agent to re sign a new agreement which would run from 1st October 2017 for a further 12 months, with a 6 month break clause, so this is still a month away from actually commencing. The tenancy is still in the names of both myself and my girlfriend at the time (with myself listed as the lead tenant). Since signing the tenancy agreement on the 12th June 2017 I have had a change in circumstances, in that myself and my girlfriend are no longer together (this happened in the last week). As such I am now in a rather dire situation where I face having to pay a minimum of another 7 months worth of rent (£1200 per month) which on my own I simply cannot afford to do, I don't earn enough on my own to cover the cost of this and council tax/other bills etc. I was wondering if anyone would be able to advise me where I stand legally with regards to now cancelling the tenancy agreement due to start on the 1st October 2017. From what I understand this is only possible with the landlords consent and I would be liable for any costs incurred to re let the property, however as I am the current tenant, at the end of the current agreement I only needed to give 30 days notice, so would this apply? I wanted to know what (if anything) I can do to cancel the AST from the 1st October. Any advice or help would be greatly appreciated. Thanks Jamie -

Hi Hope someone can advise if they have done this before. I am nearly 3 years into paying a 4 year hire purchase with first response I have been told as I have paid 50% off I can hand his car back via VT. If I was to trade my car in for a new car I would be £1500 in negative equality. I have been accepted by car finance for a much better deal but said I would be better to refinance than VT, of course they are gonna say that as they are a car finance company but told me if I do this I would struggle to get car finance. I have already been approved so would this show up on record to them? Would it really affect my chances getting car finance with them? They are trying to get me to trade in and add what is left to a new loan which bumps up monthly payments quite a bit Really just wondering if I VT can car finance then revoke my successful application. I am paying well above odds for my current car as credit score was bad but now it's better I want a newer car at a cheaper monthly price Any help appreciated please

Hi Hope someone can advise if they have done this before. I am nearly 3 years into paying a 4 year hire purchase with first response I have been told as I have paid 50% off I can hand his car back via VT. If I was to trade my car in for a new car I would be £1500 in negative equality. I have been accepted by car finance for a much better deal but said I would be better to refinance than VT, of course they are gonna say that as they are a car finance company but told me if I do this I would struggle to get car finance. I have already been approved so would this show up on record to them? Would it really affect my chances getting car finance with them? They are trying to get me to trade in and add what is left to a new loan which bumps up monthly payments quite a bit Really just wondering if I VT can car finance then revoke my successful application. I am paying well above odds for my current car as credit score was bad but now it's better I want a newer car at a cheaper monthly price Any help appreciated please -

Dear All Almost two years ago received a claim from Restons for £2,500 but with no details. Filed defence requesting details of claim and made a CCA request. Cabot didn't come back until a week ago, with copies of some documents, containing terms and conditions, and copy of agreement, stating that they are now entitled to obtain Judgment. Have to see if it is genuine. I have noticed that they have not provided copy of Deed of assignment, I requested. Not sure if important? Also it appears that the authorisation of Cabot Financial has lapsed with the FCA, which is the name they've used on the Claim form. Does this mean that the claim is not valid and they have to reapply? Also, over half of the amount they are claiming consists of bank charges. Not sure if Default or Termination notices are relevant if they have bought any debts. Please help

Dear All Almost two years ago received a claim from Restons for £2,500 but with no details. Filed defence requesting details of claim and made a CCA request. Cabot didn't come back until a week ago, with copies of some documents, containing terms and conditions, and copy of agreement, stating that they are now entitled to obtain Judgment. Have to see if it is genuine. I have noticed that they have not provided copy of Deed of assignment, I requested. Not sure if important? Also it appears that the authorisation of Cabot Financial has lapsed with the FCA, which is the name they've used on the Claim form. Does this mean that the claim is not valid and they have to reapply? Also, over half of the amount they are claiming consists of bank charges. Not sure if Default or Termination notices are relevant if they have bought any debts. Please help -

Hello, I have a car that is on HP from Advantage Finance. I have contacted them regarding a Voluntary Termination of the HP, and am currently awaiting a reply from the company regarding what I need to do next. Meanwhile, a few questions popped up in my head: 1. Would this affect my credit rating? 2. I have not serviced the car in a while (about 10k miles overdue), and the car has a couple of minor dents and scratches. If I fix the cosmetic issues and service the car now, will they still charge me for damages incurred, etc.? 3. Is there anything I need to watch out for with regards to doing this? Ive read that finance companies tend to draw the whole process out aslong as possible so that payments continue for a while. Would be nice to hear from people who have gone through this process so I know what to look out for. Thanks for replying. M

Hello, I have a car that is on HP from Advantage Finance. I have contacted them regarding a Voluntary Termination of the HP, and am currently awaiting a reply from the company regarding what I need to do next. Meanwhile, a few questions popped up in my head: 1. Would this affect my credit rating? 2. I have not serviced the car in a while (about 10k miles overdue), and the car has a couple of minor dents and scratches. If I fix the cosmetic issues and service the car now, will they still charge me for damages incurred, etc.? 3. Is there anything I need to watch out for with regards to doing this? Ive read that finance companies tend to draw the whole process out aslong as possible so that payments continue for a while. Would be nice to hear from people who have gone through this process so I know what to look out for. Thanks for replying. M -

Virgin Media Early termination fees

steven4064 posted a topic in Broadband and other Internet issues

I had an issue with Virgin Media about early termination fees when I was helping out a friend. The way he was treated was grossly unfair - details don't matter now. However, I wrote to Ofcom about it and they said that they consider early termination fees to be fair PROVIDED they only cover lost profit - actual cost of providing the service has to be deducted for the charge to be fair. This is because, if you cancel, they are saving this amount. I wrote to Virgin Media and told them what Ofcom had said. I asked them to tell me how much it cost them to supply the service my friend was terminating so that we could calculate the fair early termination fee. We've not heard from them since. The reason for this is that the information I was asking for is highly commercial (they wouldn't want Sky or anyone else knowing this) and there is no way they will divulge it. If they think you might pursue them for this information (which you have a right to do - find my thread on getting similar commercial information from Welcome Finance), they will just go away. This is not just for Virgin Media but for any ISP, Cable TV or phone service that charges early termination fees. Enjoy! -

Hi, my wife is 28 months into a 36 month PCP agreement with Ford. The car is becoming unaffordable for her and has contacted the finance company to discuss VT. they have said she can as she has paid in excess of 50% but are stating excess mileage charges will apply. because she was sold this car with 6000 miles allowed which was never suitable, she has gone over that and would owe around £550 in mileage. if VT'ing the car is this amount still payable? ford are telling her it is. there are mixed views over the internet.

Hi, my wife is 28 months into a 36 month PCP agreement with Ford. The car is becoming unaffordable for her and has contacted the finance company to discuss VT. they have said she can as she has paid in excess of 50% but are stating excess mileage charges will apply. because she was sold this car with 6000 miles allowed which was never suitable, she has gone over that and would owe around £550 in mileage. if VT'ing the car is this amount still payable? ford are telling her it is. there are mixed views over the internet. -

Evening all, I could do with a bit of advice please. In January 2016 the wife and I took finance out on a car with Advantage finance. Unfortunately our circumstances have changed dramatically in that time and we can no longer afford to run the vehicle. We have been in contact with StepChange debt charity and they have gone through our finances and the only logical way forward for us out of a bit of a mess is to Voluntarily terminate the agreement and give the car back. We will still owe money on the vehicle as we haven't paid half the finance agreement, but StepChange have said we will deal with that once Advantage have got the car back. The advice I need is on the collection of the vehicle. The vehicle has no major damage to it - no dents or rust etc. There is a little scratch in the door which was there when we bought the car. Advantage have been really pushy on the phone to my wife already - to the point of bullying. I can understand from their point of view, in that they lent the money in good faith, but we are not burying our heads in the sand here, we are trying to do the best thing. On the phone they said any any marks or damage to the car would be charged. It is a 10 year old car, so of course it has the odd blemish here and there and, as I said, a scratch. What constitutes 'fair wear and tear'? Can I argue it at all if I don't agree with their assessment? What should I do if the person that comes to collect the car puts on his inspection sheet that it has a scratch etc? I am tempted not to sign it, or sign it as I am accepting they are taking the car but not accepting there is any 'damage' to it. As I said the car is in as good, if not better, condition than when we got it. The other thing is they are coming to collect the car Friday. They have said they are going to charge £80 to collect the vehicle. Now, StepChange have said they are not legally allowed to charge to collect the vehicle. I have read online that they are not allowed to charge. Does anyone have a definate answer as to if they can or can not charge to collect this car. In the grand scheme of things £80 is a drop in the ocean to be honest, but it is more a point of principle. Any advice would be most appreciated.

Evening all, I could do with a bit of advice please. In January 2016 the wife and I took finance out on a car with Advantage finance. Unfortunately our circumstances have changed dramatically in that time and we can no longer afford to run the vehicle. We have been in contact with StepChange debt charity and they have gone through our finances and the only logical way forward for us out of a bit of a mess is to Voluntarily terminate the agreement and give the car back. We will still owe money on the vehicle as we haven't paid half the finance agreement, but StepChange have said we will deal with that once Advantage have got the car back. The advice I need is on the collection of the vehicle. The vehicle has no major damage to it - no dents or rust etc. There is a little scratch in the door which was there when we bought the car. Advantage have been really pushy on the phone to my wife already - to the point of bullying. I can understand from their point of view, in that they lent the money in good faith, but we are not burying our heads in the sand here, we are trying to do the best thing. On the phone they said any any marks or damage to the car would be charged. It is a 10 year old car, so of course it has the odd blemish here and there and, as I said, a scratch. What constitutes 'fair wear and tear'? Can I argue it at all if I don't agree with their assessment? What should I do if the person that comes to collect the car puts on his inspection sheet that it has a scratch etc? I am tempted not to sign it, or sign it as I am accepting they are taking the car but not accepting there is any 'damage' to it. As I said the car is in as good, if not better, condition than when we got it. The other thing is they are coming to collect the car Friday. They have said they are going to charge £80 to collect the vehicle. Now, StepChange have said they are not legally allowed to charge to collect the vehicle. I have read online that they are not allowed to charge. Does anyone have a definate answer as to if they can or can not charge to collect this car. In the grand scheme of things £80 is a drop in the ocean to be honest, but it is more a point of principle. Any advice would be most appreciated. -

Hello I am hoping to receive some initial guidance/advice on the following situation in relation to my daughters nursey place. In brief summary; We were hoping to secure a place at a nursey, where our son had spent 2 very pleasant years before moving to reception at school proper. We received and she signed the registration forms as attached. ( I hope) As you may, in reviewing attached, see, Jxx, as a lecturer, was unsure what her hours would be and was happy, after discussions with a deputy manager, that the situation was flexible and we could amend the dates time in due course to suit our needs. As it happened the number of days reduced from 3 to 2. We contacted the Nursery immediately on hearing this. We were astonished that they were going to charge for 3 days for the T&C's 3 month notice period. We attempted to negotiate with no success. I can upload this correspondence if it will help? As the uncooperative and entirely inflexible attitude of the nursery had destroyed our original high standing of the establishment, we have decided to withdraw our daughter completely. We are now being told that we will have to pay in full anyway for the sessions we will not use for a 3 month notice period. This amounts to somewhere near £1000. on top of the deposit! This all appears a little unfair. Particularly in noting the following; we have not both signed the form the paragraph about making every effort to accommodate changes the fact the T&C's are separate The fact that we have even noted on the form the level of uncertainty the fact that we were assured a change in dates due course would be accommodated they are apparently oversubscribed and the place will most likely be filled anyway In any case I’d love to hear thoughts and advice where possible Many thanks Juzz

-

I signed up to EE a while back on 24 month contract, got a shared contract deal, basically got a phone for myself and my partner under the same contract. However, I was diagnosed with a heart condition earlier this year, I moved from being Employed to being on Disability Benefit, this had a major effect on my finances as you could imagine due to the decrease in my income. I rang EE, explained this, not really much could be done, so I cancelled the contract. I now have a bill for around £1200, this being termination charges and line rental charges. Spoke to EE today after hearing nothing from them in a couple of months, they've confirmed the balance was passed to a Debt Collection Agency however was passed back to them. (I've never had no contact from a Debt Collection Agency so not sure why that was), they've said the debt is due to be written off in August, at which there will be a default issued however I'll still owe them the money. In the meantime, I'll continue to get late payments issued on my Credit Report. I'm just wondering where I stand right now, I can't afford to pay the £1200 of termination charges, the fact it's £1200 I find crazy, they have confirmed there's nothing they can do about the charges. Any help would be appreciated. Thank you