Search the Community

Showing results for tags 'required'.

-

Barclays have just told me that the contract is terminated and even paying the arrears in full will not stop the car from being repossessed. Today was the last day for surrender... Anyone know how long it will be before they get a court order or any options available... I pleaded with them on Friday, and though the arrears are only £540, they will take the car and put it in auction where I am due to lose about 2k of the value and that will still be owed to them... HELP PLEASE ! Barclays Partner Finance are in the process of repo my dads car. They have terminated the contract - however the 1/3 rule is very close.. . if its 1/3 of the value still owed against interest upto repo then fine, if based on original term then not... HELP. + they say they will probably go to court proceedings to recover car, but hinted they might just sent a recovery company in.. . no idea of timescales however = would be really good to have an idea, days or weeks? My father (80) purchased a car on HP from CarSupermarket. With his wife having poor health, he decided in Aug to suddenly goto India for 3 months for treatment. With cashflow being tight, he missed Aug and Sept payments. I took over paying and on a 220/month contract, I began paying 80/week except for when I paid 220. Barclays Partner Finance (BPF) were told this is what I am doing, but they couldn't confirm if they were happy as I wasn't the named person on the contract. My father, out in India then, in Oct suffered a stroke himself and was unable to speak and was receiving physio out in India. BPF then sent a termination letter and advising that the car needs to be surrendered or court proceedings will begin. I managed to get my father to ring them and agree that I could speak on his behalf. BPF said you are £504 in arrears and the contract is terminated. I said I can borrow that amount and get it restored to the normal T&Cs - but they rejected it, stating its been in arrears since Aug so NOTHING can be done to restore the contract. PROBLEMS: 1) Car Supermarket when doing the original contract with my father, put the car into my name not his...surely some kind of contract breach 2) I was willing to pay all the arrears, but that was not deemed satisfactory. 3) The car is now to be repossessed and according to BPF - they will instruct their solicitors tomorrow to start doing this. 4) I have paid just under 4k so far, finance amount originally was £9,693. There is now £10,185 outstanding, though the true figure accounting for early settlement would be £7,990 - I don't know what figures to use to see if 1/3 has been paid. 5) no consideration given to the fact that my father is ill, and as such will likely have to stay at least a further 3 months in India as he is unfit to travel. I am totally in a tizz... I dare not risk telling dad his car is to be repossessed but don't know what to do. Please if anyone can help, H.

Barclays have just told me that the contract is terminated and even paying the arrears in full will not stop the car from being repossessed. Today was the last day for surrender... Anyone know how long it will be before they get a court order or any options available... I pleaded with them on Friday, and though the arrears are only £540, they will take the car and put it in auction where I am due to lose about 2k of the value and that will still be owed to them... HELP PLEASE ! Barclays Partner Finance are in the process of repo my dads car. They have terminated the contract - however the 1/3 rule is very close.. . if its 1/3 of the value still owed against interest upto repo then fine, if based on original term then not... HELP. + they say they will probably go to court proceedings to recover car, but hinted they might just sent a recovery company in.. . no idea of timescales however = would be really good to have an idea, days or weeks? My father (80) purchased a car on HP from CarSupermarket. With his wife having poor health, he decided in Aug to suddenly goto India for 3 months for treatment. With cashflow being tight, he missed Aug and Sept payments. I took over paying and on a 220/month contract, I began paying 80/week except for when I paid 220. Barclays Partner Finance (BPF) were told this is what I am doing, but they couldn't confirm if they were happy as I wasn't the named person on the contract. My father, out in India then, in Oct suffered a stroke himself and was unable to speak and was receiving physio out in India. BPF then sent a termination letter and advising that the car needs to be surrendered or court proceedings will begin. I managed to get my father to ring them and agree that I could speak on his behalf. BPF said you are £504 in arrears and the contract is terminated. I said I can borrow that amount and get it restored to the normal T&Cs - but they rejected it, stating its been in arrears since Aug so NOTHING can be done to restore the contract. PROBLEMS: 1) Car Supermarket when doing the original contract with my father, put the car into my name not his...surely some kind of contract breach 2) I was willing to pay all the arrears, but that was not deemed satisfactory. 3) The car is now to be repossessed and according to BPF - they will instruct their solicitors tomorrow to start doing this. 4) I have paid just under 4k so far, finance amount originally was £9,693. There is now £10,185 outstanding, though the true figure accounting for early settlement would be £7,990 - I don't know what figures to use to see if 1/3 has been paid. 5) no consideration given to the fact that my father is ill, and as such will likely have to stay at least a further 3 months in India as he is unfit to travel. I am totally in a tizz... I dare not risk telling dad his car is to be repossessed but don't know what to do. Please if anyone can help, H. -

Hi, I have received a PCN from Premier Park for parking in Exeter Road Car Park in Braunton, Devon. I parked in this carpark for 20 mins at 19:06 and it was dark. I did not realise that it was a paid car park as the notices were not that clear and lighting was low. 'Contrevention date': 2nd November, 2017. The issue date of the PCN: 8th November, 2017. The PCN requests £60 if paid by 14 days from issue date or £100 afterwards. I have googled around and this car park seems to have a history of this issue. I do not live any where near the car park, I cannot get images etc. From what I have read, Premier Park provides images in daylight or with a strong flash to 'prove' that they have enough lighting. I cannot provide this evidence, but even in the images that they have provided on the PCN form shows how dark it is. Could you provide me with any advice for a potential defence. Also, if I apeal to Premier Park (which I expect they will turn down) and then go to POPLA, will this mean that if I am refused, they will charge £100. Any advice is appreciated.

Hi, I have received a PCN from Premier Park for parking in Exeter Road Car Park in Braunton, Devon. I parked in this carpark for 20 mins at 19:06 and it was dark. I did not realise that it was a paid car park as the notices were not that clear and lighting was low. 'Contrevention date': 2nd November, 2017. The issue date of the PCN: 8th November, 2017. The PCN requests £60 if paid by 14 days from issue date or £100 afterwards. I have googled around and this car park seems to have a history of this issue. I do not live any where near the car park, I cannot get images etc. From what I have read, Premier Park provides images in daylight or with a strong flash to 'prove' that they have enough lighting. I cannot provide this evidence, but even in the images that they have provided on the PCN form shows how dark it is. Could you provide me with any advice for a potential defence. Also, if I apeal to Premier Park (which I expect they will turn down) and then go to POPLA, will this mean that if I am refused, they will charge £100. Any advice is appreciated. -

Hi All, I have read many many threads on here about SkillsTrain etc. and the issues about the course material, mis-selling of finance with CDF etc and i am in a similar boat. Let me explain my story here. In early 2010 i responded to an advert about receiving information on the Games Developer course with Train2Game. A lady came to my house shortly afterwards. At the time i was very stressed at work and was diagnosed with an acute anxiety disorder (thankfully that has gone now) because of my work and the pressures on me. The lady arrived at noon and started chatting about the course. Throughout the chat she kept asking me "is this something you are interested in?". I told her that i would need to think about it as i wasn't sure i could afford the £4500 that it would cost (£135 per month), especially with the way things at work were going. She started talking about all other things under the sun and ended up staying in my house for 7 hours. She didn't leave no matter how many times i said i would have to think about it. All the while my partner (now wife) was there witnessing this. She told me that she had 3 other appointments to attend but was missing them to sign me up, she kept looking at her watch, making me feel pressurised. The only way to get her out of my house was to sign up as it was now after 1800. She gave me a "pre contract information sheet" that i looked at, all the while regretting signing it. Straight away she called a finance company (CDF) who gave me the finance and i signed the agreement. As soon as i signed it she went to her car, gave me a laptop bag with a workbook and CD and then drove away. All this within 15 minutes. I made 1 payment but didn't start the course. I could not sleep from thinking about it. I did some research online a short while afterwards and saw the mountains of complaints about it and felt utterly sick about being pushed into the course. She told me that i was guaranteed a job after completing the course and that the course was accredited by Microsoft (which it isn't). She also told me i could use the course to get into university (which i couldn't). I stopped making payments because of what i had read about and my illness at the time, i couldn't deal with the stress of it. I have never received any correspondence, no calls, no letters, no material, no nothing up until last week when i got a letter from Cabot saying i owed £4320 for my course. Since receiving this letter, i have dug out the stuff that i was given including the agreement copies etc. The agreement says i should have been given the "per-contract information sheet" in good time beforehand, which i wasn't, i was given it 1 minute beforehand.. The contract agreement between me and CDF has my signature on it and a date but no signature and date for the CDF representative (salesperson) as it states it should have. So the agreement is basically a signature of my own with their company name on it. I really need help here as i cannot afford to pay this. I have received no goods or services at all. My credit file is slowly getting better and i cannot have this on my head. Should i go to CAB? Can anyone suggest a letter and wording to put in it for me to send to Cabot? I dont want to be in a financial mess again and i feel that this whole thing was forced on me. What should i do?

-

Hi I sold a phone via fb marketplace and he paid into my account. I sent the phone and I assume he has received it as he has now reported me as a [EDIT] to Natwest saying he has received nothing. I have no proof of post. The bank has blocked my access to online banking and use of my card I have no access to my monies. I spoke to them and they said that I am being investigated by the team I am outraged as obviously the person saying I am doing him over is in fact trying to do me over Any how. How will I get my account back and my monies? Also I hear fraud and think of the police. Is this guys games going to get me in trouble? Thanks

-

Hello, My partner has received a 'final notice' from marstons regards to a fine until today she had no knowledge of. After ringing the HMCTS, she found that the fine related to a judgement from April 2017 for not insuring a vehicle she was registered keeper for (she had reported as SORN but admits had no confirmation). Presumably as the vehicle was registered at a previous address then any court documents wouldve gone there. She ignored the first notice from Marstons today they put a 'final notice' through the door threatening that they can break in using a locksmith and remove goods for sale next time they visit. I have advised her that a statutory declaration needs to be done, which she will get signed by solicitor tomorrow afternoon and sent recorded delivery to court. am i correct? As this is deemed as a criminal charge, are they correct in implying they can break in if we are not home? Thanks Forgot to say the amount they are claiming to get back is £660

Hello, My partner has received a 'final notice' from marstons regards to a fine until today she had no knowledge of. After ringing the HMCTS, she found that the fine related to a judgement from April 2017 for not insuring a vehicle she was registered keeper for (she had reported as SORN but admits had no confirmation). Presumably as the vehicle was registered at a previous address then any court documents wouldve gone there. She ignored the first notice from Marstons today they put a 'final notice' through the door threatening that they can break in using a locksmith and remove goods for sale next time they visit. I have advised her that a statutory declaration needs to be done, which she will get signed by solicitor tomorrow afternoon and sent recorded delivery to court. am i correct? As this is deemed as a criminal charge, are they correct in implying they can break in if we are not home? Thanks Forgot to say the amount they are claiming to get back is £660 -

Name of the Claimant ? Cabot Financial UK Ltd Date of issue – 1 Jun 2017 What is the claim for – 1.By an agreement between IDEM Re Egg Banking Plc & the Defendant on or around 16/8/2005 ('the agreement') IDEM Re Egg Banking Plc agreed to loan the Defendant monies. 2. The Defendant did not pay the installments as they fell due & the Agreement was terminated. The Agreement was assigned to the Claimant. THE CLAIMANT THEREFORE CLAIMS 1397.53 What is the value of the claim? 1547.53 (inc fees of 150) Is the claim for - personal loan When did you enter into the original agreement before or after 2007? before - around 2003-4 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Cabot Were you aware the account had been assigned – did you receive a Notice of Assignment? NO Did you receive a Default Notice from the original creditor? No Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ?No Why did you cease payments? Payments were being taken by direct debit, unaware payments had stopped, no notices received for lack of payment at any time What was the date of your last payment? Exact date unknown at present, sometime prior to 2010 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management planicon? No financial problems, no need to contact creditor, no need for debt management. They stopped taking payments and did not inform us we were behind Hello I received a county court claim form in the post today from Cabot. I will fill out the details I know you need in the next post. I'm doing this for my wife, who is in bits now because of this form. I'm trying to calm her down but he is scared witless. She did take out a loan over 10 years ago with Egg, but that was sold to another company when Egg got out of the personal loan business and I think we only had one more letter from them after that. This is the only one we've received since. Bank accounts and direct debits have not changed in over 20 years and she always pays her debts on time. I don't think she has ever missed a payment for anything. I work at home and as such, very rarely ever leave the house. No-one has come knocking at the door about this - or any other - debt in the 10 years I've lived here. Can someone lease assist me, I have no idea what I'm doing and we cannot afford solicitors. Thank you in advance Ian

Name of the Claimant ? Cabot Financial UK Ltd Date of issue – 1 Jun 2017 What is the claim for – 1.By an agreement between IDEM Re Egg Banking Plc & the Defendant on or around 16/8/2005 ('the agreement') IDEM Re Egg Banking Plc agreed to loan the Defendant monies. 2. The Defendant did not pay the installments as they fell due & the Agreement was terminated. The Agreement was assigned to the Claimant. THE CLAIMANT THEREFORE CLAIMS 1397.53 What is the value of the claim? 1547.53 (inc fees of 150) Is the claim for - personal loan When did you enter into the original agreement before or after 2007? before - around 2003-4 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Cabot Were you aware the account had been assigned – did you receive a Notice of Assignment? NO Did you receive a Default Notice from the original creditor? No Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ?No Why did you cease payments? Payments were being taken by direct debit, unaware payments had stopped, no notices received for lack of payment at any time What was the date of your last payment? Exact date unknown at present, sometime prior to 2010 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management planicon? No financial problems, no need to contact creditor, no need for debt management. They stopped taking payments and did not inform us we were behind Hello I received a county court claim form in the post today from Cabot. I will fill out the details I know you need in the next post. I'm doing this for my wife, who is in bits now because of this form. I'm trying to calm her down but he is scared witless. She did take out a loan over 10 years ago with Egg, but that was sold to another company when Egg got out of the personal loan business and I think we only had one more letter from them after that. This is the only one we've received since. Bank accounts and direct debits have not changed in over 20 years and she always pays her debts on time. I don't think she has ever missed a payment for anything. I work at home and as such, very rarely ever leave the house. No-one has come knocking at the door about this - or any other - debt in the 10 years I've lived here. Can someone lease assist me, I have no idea what I'm doing and we cannot afford solicitors. Thank you in advance Ian -

A couple of weeks ago I had to call a locksmith out (from a call centre number). My key would not turn what appeared to be a jammed deadlock. Using airbags to partially hold open part of the door he used an angle grinder to try and cut through the deadlock but unfortunately the blade was too short by about 2mm. He then decided to use a hammer and chisel with a great amount of force for about 30 - 40 minutes. He aborted the job and I was left locked out. The next day another locksmith came round and used a paddle to hole part of the door open sufficiently enough for him to be able to drill through the lock and gain entry. Once in it was clear that there was quite a lot of damage caused to the UPVCS frame, the wooden frame and to the edge of the door. I complained to the first company who denied that their "engineer" used a hammer even though several of my neighbours signed to say that they had heard the hammering. They are denying responsibility saying " Firstly, I wish to clarify my point regarding the liability of any damaged caused. Each sub-contractor that works for us is required to have Public Liability Insurance to cover himself on jobs should accidental damage be caused. Therefore, if any damage was caused by our engineer Danny, then it would be the engineer personally liable for making further arrangements through his personal insurance. Naturally Keytek would assist as and where required should any of our locksmiths cause damage while on site. Surely my contract was between the Company and not the subcontractor they chose to appoint to the job. All helpful advice welcome. Thanks

A couple of weeks ago I had to call a locksmith out (from a call centre number). My key would not turn what appeared to be a jammed deadlock. Using airbags to partially hold open part of the door he used an angle grinder to try and cut through the deadlock but unfortunately the blade was too short by about 2mm. He then decided to use a hammer and chisel with a great amount of force for about 30 - 40 minutes. He aborted the job and I was left locked out. The next day another locksmith came round and used a paddle to hole part of the door open sufficiently enough for him to be able to drill through the lock and gain entry. Once in it was clear that there was quite a lot of damage caused to the UPVCS frame, the wooden frame and to the edge of the door. I complained to the first company who denied that their "engineer" used a hammer even though several of my neighbours signed to say that they had heard the hammering. They are denying responsibility saying " Firstly, I wish to clarify my point regarding the liability of any damaged caused. Each sub-contractor that works for us is required to have Public Liability Insurance to cover himself on jobs should accidental damage be caused. Therefore, if any damage was caused by our engineer Danny, then it would be the engineer personally liable for making further arrangements through his personal insurance. Naturally Keytek would assist as and where required should any of our locksmiths cause damage while on site. Surely my contract was between the Company and not the subcontractor they chose to appoint to the job. All helpful advice welcome. Thanks -

Hi CAG, I am hoping for some advice, if you could be so kind. I took out a BC in Jan 2011, and due to a serious marriage break-up, problems with alcohol and depression I lost my job in late 2012, needless to say the last thing on my mind was managing my debt. In a panic I ended up on another forum which I am sure you will know which seems to offer stupid advice. I wrote to BC and asked for a copy of the CCA, they replied with a reconstituted copy of the terms and conditions but no copy of the agreement. Literally a month later they sold the debt (£2000) to Hoist and I do believe I received a notice of assignment, although I cannot be 100% sure. I challenged Hoist to produce a copy of the CCA and a copy of the notice of assignment, they failed to produce any documentation and it all went quiet. Then last year RobisonWay starting trying to collect the debt on behalf of Hoist Around June 2016 I received a letter from RW saying they may pass my account to Cohens for court action I replied explaining BC and Hoist had failed to supply any copy of a CCA and if they wished to instigate legal proceedings then I would defend based on the fact none of the companies could produce a copy of the CCA and under civil procedure rules they would need to supply a copy after issuing a LBA. I challenged them for a copy of the CCA and notice of assignment and they replied they would write to Hoist/BC to get it and were suspending collection activity. About 2 months later I finally received the exact same reconstituted copy of the terms and conditions (which BC had sent me over 2 years previously) and still no copy of a CCA, I emailed RW and told them what they had sent was utter junk and did not fulfill what I had requested, they wrote to em again saying they would suspend activity. I have now received another letter from them in which they claim my credit card application was online and as such does not need a signature, this is UNTRUE, when I applied for the BC in 2011 it was via an application which was received in the post. They have included a copy of the notice of assignment from MKLDP LLP to Hoist and something called "barclaycard cas mart application retrieval" which contains the date the card was applied for, my address, etc but it appears to be an internal document which appears to simply be where they have imputed the postal application on to their system after approval. At least that's what it appears to be. I am currently wondering what should be my next course of action, If I could pay the £2000 off I would, but since my marriage break-up, problems with alcohol, depression and my job loss I have been struggling on benefits which is incredibly hard to do. When I was drinking I could not care about them, but now I am sober and trying to rebuild my life I am worried about this situation. Sorry for such a long-winded post, but if anyone could offer any advice I would be eternally grateful.

-

At the start of the year we had a new bathroom fitted. We purchased all the furnishings so the quote was for labour only. Due to my wife being allergic to dust it was agreed that the fitting would take place whilst we was on holiday. 75% of the labour charge has been paid to him to date On our return home we was shocked to see our new bathroom. The quality of work in our opinion is below standard, fittings haven't been fitted correctly, damaged has occured to several furnishings, we have had a leak going through our living room ceiling and a second leak on the outside wall due to incorrect exterior pipe work being fitted. The bathroom is dangerous in parts. The fitter says he doesn't have personal liability insurance and was too busy to come back for a while to deal with any of the issues. Several months on we are still in the same position. The fitter believes his work is to a high standard. He admits breaking fittings and admits parts of the bathroom are dangerous but thinks the 25% remainder of the balance will cover it, but it doesn't. We have had 8 different companies come to look at the bathroom and everyone of them says it isn't fitted correctly and the bathroom needs pulling out and starting again. I have had no choice but to take this matter to a small claims court. Initially the fitter replied to us when I made our intentions known and said he was willing to resolve issues and the reason for not being able to contact him for 6 months is because he had phone problems. I believe he was deliberately avoiding us. When I have told him about the leaks etc he has said he is happy to proceed down the small claims court route. I am wanting an independent assessor to come take a look at the bathroom and provide me with a report that will support my claim. How do I go about this? Thanks in advance for any help

-

Hi all, I've noticed that there are some real horror-show complaints about Advantage Finance on this forum, and I'm here to add to this in my own small way. I would like to mention in advance that I believe some of this stuff to sound implausible, but there is written proof of everything I say here. So, a quick summary of this would be: 1. I bought a car from a dealer, using Advantage for finance for £3000 of the £4000 price. 2. I made several payments on time by DD. 3. I notified them that there were several issues with the car; a - the parking sensors have never been reliable, and this nearly caused a couple of incidents before I realized they were intermittent b - the brakes make a clunking noise and squeal when applied - this wasn't apparent on the test-drive, but has been getting worse c - the brakes also caused one of the tyres to be damaged, and this had to be replaced d - the power steering pump clunks sporadically 4. I got reports on all of these faults from a local Kwik-Fit, and Advantage paid to have the brakes repaired. This did not resolve the issue, however, as the issue persists, and this has also been the subject of another report by the same Kwik-Fit. Advantage refused to pay for the replacement tyre. 5. Some arguments were had with Advantage staff about the car, which I notified them that I wanted to return as faulty as I was within the 6 months, I was unhappy with the number of faults. They refused, and they spoke to me pretty badly. I reminded them that they are a finance company and that I am their customer - they shouldn't be treating everybody who owes them money as if they're some sort of criminal: we're their customer and their sole revenue stream. 6. I sent another report to Advantage from the garage detailing faults 5 months in and they didn't respond. I chased again, they still didn't respond. They have since admitted that this is an accurate description of what happened: I tried to get in contact, they didn't come back to me. This will be important later. 7. I rearranged all my finances and now have all my direct debits paid out of one specific bank account. I provided these details to Advantage in writing 3 weeks before the next payment was due. They wrote back saying that they were declining to accept these details as they weren't provided in a way which they approved. I said I thought providing them in writing was sufficient and that I wanted all future payments to be taken from the account I had specified. At this point in time I was not in arrears and they had loads of time to arrange the direct debit. I genuinely felt like they were treating me the way they were because of the previous arguments over my attempt to return the car as faulty; it always felt like I was being drawn into an argument. 8. I received a call from Advantage I was told again that they were not accepting the direct debit information. said, and I quote: "I sent the same details to providers of my car insurance, home insurance, car tax, and lots of other companies. gave them to you in loads of time and if it's good enough for the DVLA then I don't see why it's not good enough for you. now you're deliberately inconveniencing me and trying to justify it by quoting some technicality." The agent tried to tell me off for swearing at her, I said that in the context I used the word I wasn't swearing AT her, and she hung up. I then received a letter from Advantage which demanded a written apology for my conduct and threatened me with police action for the virulent verbal abuse I had subjected their member of staff to. I ignored this threat, of course. 9. Advantage set up a direct debit with my bank, using the details I had provided to them. This was confirmed by my bank, in writing: they set up the direct debit, they were fully capable of taking payment on the agreed payment date. Advantage then sent me confirmation in writing that they had set up the direct debit, and would be taking payment. 10. I then received a Termination notice in the mail which said that since I had refused to make payment they had cancelled the agreement and would be going to court in order to repossess my car. I called them and was told this was an administration error, that this letter should never have been sent out. 11. Advantage did not take payment on the agreed DD date. I then found a note on my doormat from some collection 'agent' saying he'd been to collect the car, and I wasn't home. This note demanded that I surrender the car. 12. I did not surrender the car, and I told Advantage I would be making a complaint through the FOS. 13. I complained to the FOS, citing: a - Advantage's refusal to deal with the fact that the car was faulty when sold b - Advantage's refusal to allow me to reject a car as faulty, despite my provision of several garage reports within six months of purchase c - Advantage refusing to take payment, despite setting up the Direct Debit d - Advantage lodging a default notice against me, and putting this on my credit file despite the fact I had never once refused to pay them, and despite the fact that they had full access to the payment, having a direct debit established and then not taking the money, and despite the fact that I can prove that there were funds in the account more than sufficient to cover the direct debit amount. I provided all of this detail in writing to the FOS, I was sure that my case was strong because I had shown good faith continued to make payments even when Advantage refused to uphold their obligations relating to the faults on the car and my rejection of said car, proved that I had not only provided the details with time to spare but that Advantage had used them to set up a direct debit and then not taken payment. How could I lose? 14. The FOS adjudicator somehow came to the conclusion that even though Advantage had complete access to the money and didn't take it, they were within their rights to cancel the agreement, and not only am I the one being "obstructive" (she somehow thought that even though it was Advantage refusing to respond to me, which they admitted, it was all my fault for "refusing to engage with Advantage", see point #6), but that I'm also liable for the entire balance of the agreement. Advantage have done nothing wrong, apparently, and I'm the one in the wrong, because I had an argument with one of Advantage's people on the phone a year ago. She also described this as a "favourable" outcome for me, which actually made me burst out laughing. 15. My bank manager told me he's never seen anything like this, and said that he's never seen before a case where the FOS have found in favor of a company who have outright refused to take payment, even after sending me confirmation that they would be taking payment. He was also the guy who provided me with the proof that the direct debit was set up with more than enough time to take payment on the agreed date. 16. I'm absolutely sure that a financial agreement includes two-way obligations, and that both parties need to be held to the same standards. I'm agreeing to make payments, and they're agreeing to facilitate that. I don't honestly see how Advantage can cancel an agreement in this way, for no good reason, and I'm still being held over the fire. I'm not up on breach-of-contract law, but this seems to me to be a clear breach, and now I'm faced with either finding the money to repay in full, entering into another agreement with the company who have already screwed me over at even worse terms than before, or having my car taken away and being liable for any disparity between whatever price they sell it for and the balance on the agreement. 17. I'm amazed that I can put my finances in order, so that part of my salary is automatically transferred into a separate account meant for the purpose of paying my bills, and now I find myself with a huge debt and a default against my name. Can anyone advise on what my next course of action might be?

Hi all, I've noticed that there are some real horror-show complaints about Advantage Finance on this forum, and I'm here to add to this in my own small way. I would like to mention in advance that I believe some of this stuff to sound implausible, but there is written proof of everything I say here. So, a quick summary of this would be: 1. I bought a car from a dealer, using Advantage for finance for £3000 of the £4000 price. 2. I made several payments on time by DD. 3. I notified them that there were several issues with the car; a - the parking sensors have never been reliable, and this nearly caused a couple of incidents before I realized they were intermittent b - the brakes make a clunking noise and squeal when applied - this wasn't apparent on the test-drive, but has been getting worse c - the brakes also caused one of the tyres to be damaged, and this had to be replaced d - the power steering pump clunks sporadically 4. I got reports on all of these faults from a local Kwik-Fit, and Advantage paid to have the brakes repaired. This did not resolve the issue, however, as the issue persists, and this has also been the subject of another report by the same Kwik-Fit. Advantage refused to pay for the replacement tyre. 5. Some arguments were had with Advantage staff about the car, which I notified them that I wanted to return as faulty as I was within the 6 months, I was unhappy with the number of faults. They refused, and they spoke to me pretty badly. I reminded them that they are a finance company and that I am their customer - they shouldn't be treating everybody who owes them money as if they're some sort of criminal: we're their customer and their sole revenue stream. 6. I sent another report to Advantage from the garage detailing faults 5 months in and they didn't respond. I chased again, they still didn't respond. They have since admitted that this is an accurate description of what happened: I tried to get in contact, they didn't come back to me. This will be important later. 7. I rearranged all my finances and now have all my direct debits paid out of one specific bank account. I provided these details to Advantage in writing 3 weeks before the next payment was due. They wrote back saying that they were declining to accept these details as they weren't provided in a way which they approved. I said I thought providing them in writing was sufficient and that I wanted all future payments to be taken from the account I had specified. At this point in time I was not in arrears and they had loads of time to arrange the direct debit. I genuinely felt like they were treating me the way they were because of the previous arguments over my attempt to return the car as faulty; it always felt like I was being drawn into an argument. 8. I received a call from Advantage I was told again that they were not accepting the direct debit information. said, and I quote: "I sent the same details to providers of my car insurance, home insurance, car tax, and lots of other companies. gave them to you in loads of time and if it's good enough for the DVLA then I don't see why it's not good enough for you. now you're deliberately inconveniencing me and trying to justify it by quoting some technicality." The agent tried to tell me off for swearing at her, I said that in the context I used the word I wasn't swearing AT her, and she hung up. I then received a letter from Advantage which demanded a written apology for my conduct and threatened me with police action for the virulent verbal abuse I had subjected their member of staff to. I ignored this threat, of course. 9. Advantage set up a direct debit with my bank, using the details I had provided to them. This was confirmed by my bank, in writing: they set up the direct debit, they were fully capable of taking payment on the agreed payment date. Advantage then sent me confirmation in writing that they had set up the direct debit, and would be taking payment. 10. I then received a Termination notice in the mail which said that since I had refused to make payment they had cancelled the agreement and would be going to court in order to repossess my car. I called them and was told this was an administration error, that this letter should never have been sent out. 11. Advantage did not take payment on the agreed DD date. I then found a note on my doormat from some collection 'agent' saying he'd been to collect the car, and I wasn't home. This note demanded that I surrender the car. 12. I did not surrender the car, and I told Advantage I would be making a complaint through the FOS. 13. I complained to the FOS, citing: a - Advantage's refusal to deal with the fact that the car was faulty when sold b - Advantage's refusal to allow me to reject a car as faulty, despite my provision of several garage reports within six months of purchase c - Advantage refusing to take payment, despite setting up the Direct Debit d - Advantage lodging a default notice against me, and putting this on my credit file despite the fact I had never once refused to pay them, and despite the fact that they had full access to the payment, having a direct debit established and then not taking the money, and despite the fact that I can prove that there were funds in the account more than sufficient to cover the direct debit amount. I provided all of this detail in writing to the FOS, I was sure that my case was strong because I had shown good faith continued to make payments even when Advantage refused to uphold their obligations relating to the faults on the car and my rejection of said car, proved that I had not only provided the details with time to spare but that Advantage had used them to set up a direct debit and then not taken payment. How could I lose? 14. The FOS adjudicator somehow came to the conclusion that even though Advantage had complete access to the money and didn't take it, they were within their rights to cancel the agreement, and not only am I the one being "obstructive" (she somehow thought that even though it was Advantage refusing to respond to me, which they admitted, it was all my fault for "refusing to engage with Advantage", see point #6), but that I'm also liable for the entire balance of the agreement. Advantage have done nothing wrong, apparently, and I'm the one in the wrong, because I had an argument with one of Advantage's people on the phone a year ago. She also described this as a "favourable" outcome for me, which actually made me burst out laughing. 15. My bank manager told me he's never seen anything like this, and said that he's never seen before a case where the FOS have found in favor of a company who have outright refused to take payment, even after sending me confirmation that they would be taking payment. He was also the guy who provided me with the proof that the direct debit was set up with more than enough time to take payment on the agreed date. 16. I'm absolutely sure that a financial agreement includes two-way obligations, and that both parties need to be held to the same standards. I'm agreeing to make payments, and they're agreeing to facilitate that. I don't honestly see how Advantage can cancel an agreement in this way, for no good reason, and I'm still being held over the fire. I'm not up on breach-of-contract law, but this seems to me to be a clear breach, and now I'm faced with either finding the money to repay in full, entering into another agreement with the company who have already screwed me over at even worse terms than before, or having my car taken away and being liable for any disparity between whatever price they sell it for and the balance on the agreement. 17. I'm amazed that I can put my finances in order, so that part of my salary is automatically transferred into a separate account meant for the purpose of paying my bills, and now I find myself with a huge debt and a default against my name. Can anyone advise on what my next course of action might be? -

Hello, A number of PCNs from Smart Parking were delivered to my address in the last few weeks, for an alleged breach of the terms of parking at Matalan in Sutton, Surrey. This was subsequently followed by a Notice of Intended Court Action letter from Debt Recovery Plus (DRP), stating the reason for the PCN being issued as: "Overstayed Paid Time". Earlier this week, another letter was received from SCS Law who claim to act on behalf of Smart Parking Ltd who have allegedly instructed this law firm to recover the PCN charges. The letter then goes on to state that Smart Parking are entitled to the outstanding sum under contract law, adding: "When your vehicle parked at the above mentioned site(s), the driver of the vehicle agreed to be bound by the terms and conditions of parking which was displayed on signage throughout the site(s). The driver of the vehicle breached the terms and conditions of parking on each of the above stated occasions for the reason stated. For each contravention, a parking charge notice was issued, for which the sums owed remain outstanding. We refer you to the Supreme Court decision in ParkingEye Ltd v Beavis [2015] UKSC 67. In this case, the Supreme Court found that parking charge notices do not contravene the penalty rule or Unfair Terms in Consumer Contract Regulations 1999 provided they protect a legitimate interest. Unless payment is made within the next 14 days, we are instructed to issue court proceedings to recover the same and any of our client's legal costs, without further recourse to you". I visited the Matalan store last weekend and discussed my issue with a member of staff, with the hope Matalan would intervene and request for the PCN to be cancelled, being a regular customer of the store. The member of staff was not very helpful but did advise me to contact Smart Parking directly for any resolution and also pointed out that Smart Parking were no longer the contracted to manage the car park. I would now appreciate the kind assistance of our very valued forum members to advice on how to fight this PCN successfully and have provided some relevant pictures from the car park, if this helps construct a solid defence. Thank you.

Hello, A number of PCNs from Smart Parking were delivered to my address in the last few weeks, for an alleged breach of the terms of parking at Matalan in Sutton, Surrey. This was subsequently followed by a Notice of Intended Court Action letter from Debt Recovery Plus (DRP), stating the reason for the PCN being issued as: "Overstayed Paid Time". Earlier this week, another letter was received from SCS Law who claim to act on behalf of Smart Parking Ltd who have allegedly instructed this law firm to recover the PCN charges. The letter then goes on to state that Smart Parking are entitled to the outstanding sum under contract law, adding: "When your vehicle parked at the above mentioned site(s), the driver of the vehicle agreed to be bound by the terms and conditions of parking which was displayed on signage throughout the site(s). The driver of the vehicle breached the terms and conditions of parking on each of the above stated occasions for the reason stated. For each contravention, a parking charge notice was issued, for which the sums owed remain outstanding. We refer you to the Supreme Court decision in ParkingEye Ltd v Beavis [2015] UKSC 67. In this case, the Supreme Court found that parking charge notices do not contravene the penalty rule or Unfair Terms in Consumer Contract Regulations 1999 provided they protect a legitimate interest. Unless payment is made within the next 14 days, we are instructed to issue court proceedings to recover the same and any of our client's legal costs, without further recourse to you". I visited the Matalan store last weekend and discussed my issue with a member of staff, with the hope Matalan would intervene and request for the PCN to be cancelled, being a regular customer of the store. The member of staff was not very helpful but did advise me to contact Smart Parking directly for any resolution and also pointed out that Smart Parking were no longer the contracted to manage the car park. I would now appreciate the kind assistance of our very valued forum members to advice on how to fight this PCN successfully and have provided some relevant pictures from the car park, if this helps construct a solid defence. Thank you. -

My rent is payable weekly (tenancy agreement states rent is to be paid weekly to landlord's bank account) which I do. I have been told that the landlord should still provide a rent book as it is paid weekly - is that correct? Thank you.

My rent is payable weekly (tenancy agreement states rent is to be paid weekly to landlord's bank account) which I do. I have been told that the landlord should still provide a rent book as it is paid weekly - is that correct? Thank you. -

I took virgin media to CICAS and they lied about the contract. They told CICAS the screen shot of the t&cs I provided was from an old contract from someone else while the screen shot they provided is from my contract (by this time they had changed my online profile and had updated my contract to show new t&cs). I did not have the original contract copy at that moment but later, after CICAS decided in their favour, I found out the email they had sent me which had the contract I signed and could prove my stance was right. The only proof they gave was fake screen shots which I can prove now was fake. CICAS would not listen to me as their decision is final. Can someone help me legally and take them to court. I do not want to spend more money on them unless I have some legal advise. They not only broke their T&Cs with me but also lied to CICAS deliberately as I had pointed out to them in a call that my online profile shows the old t&cs and after three weeks they changed those. I am sure they have done it to 100s of thousands of people and ripping them off. It's a big [problem] I can tell. Please note I am no more looking for the contract I signed as I have it in my email when they originally sent it to me.

I took virgin media to CICAS and they lied about the contract. They told CICAS the screen shot of the t&cs I provided was from an old contract from someone else while the screen shot they provided is from my contract (by this time they had changed my online profile and had updated my contract to show new t&cs). I did not have the original contract copy at that moment but later, after CICAS decided in their favour, I found out the email they had sent me which had the contract I signed and could prove my stance was right. The only proof they gave was fake screen shots which I can prove now was fake. CICAS would not listen to me as their decision is final. Can someone help me legally and take them to court. I do not want to spend more money on them unless I have some legal advise. They not only broke their T&Cs with me but also lied to CICAS deliberately as I had pointed out to them in a call that my online profile shows the old t&cs and after three weeks they changed those. I am sure they have done it to 100s of thousands of people and ripping them off. It's a big [problem] I can tell. Please note I am no more looking for the contract I signed as I have it in my email when they originally sent it to me. -

Would very much appreciate some guidance in putting together an appeal for county court. Mainly in terms of putting paperwork together. All. help would be greatly appreciated. Martin

Would very much appreciate some guidance in putting together an appeal for county court. Mainly in terms of putting paperwork together. All. help would be greatly appreciated. Martin -

Hi all new to the forum. I apologise if this is the wrong sub forum. I have recently decided to get my credit in order. I have for a long time buried my head in the sand and in the process ended up with 2 ccjs and iva i didnt make a payment to after careful 3rd party talks decided it wouldnt be right, numerous defaults. I have made the first steps Got my credit File from Experian and Equifax these show the following ACTIVE 297 - o2 325 - o2 116 - Indigo Michael (Safety net credit) Paid off in full this month account closed. Closed (with a default balance) 400 - O2 765 - Lowell Portfolio ( Provident) 872 - Lowell Portfolio (VODAFONE) 241 - Motormile Finance (Lending Stream) 285 - PRA Group 216 - APS OVERDRAFT (cashplus credit card) 304 - o2 441 - o2 204 - Lowell Portfolio 258 - CFO Lending (now with Motormile finance) 390 - Vanquis 1,361 - CCJ - 20-08-2012 473 - CCJ - 21/2/2013 0 - IVA - 21/12/15 Im am looking for best advise to get this ^ problem in order, paying them all off in full although my preffered option is one I just aint capable of at the present time. CCJ 1 This was taken out by Swansea Council without my knowledge and only after getting my credit file was I aware it even existed. I had moved from Swansea 2 years prior to the judgement and signed the house over to my ex partner at her address. CCJ 2 this was for a advertising debt for a limited company I was running and am unsure as to why or how they gained a judgement in my name when I never signed a directors guarantee etc. IVA I signed up to an IVA but after careful consideration and persistant messing about by the managing company Knightsbridge I decided to pull out of letting them handle my debts and here I am.

-

I've received a notice stating that my landlord is offering me suitable alternative accommodation and I shall be required to move. That was two weeks ago. 1 Previously the landlord has written to me stating that they cannot require me to move and will not require me to move. 2 No alternative has in fact been offered. I've done the obvious and emailed pointing out the above and also expressing surprise at receiving a notice without warning. I have had a reply stating that they have noted what I have written. Now, what do I do? I am a Housing Association tenant and have lived in my flat for over twenty years. They want me to move so that they can sell the property and move me to a cheaper area. Any advice appreciated, please.

I've received a notice stating that my landlord is offering me suitable alternative accommodation and I shall be required to move. That was two weeks ago. 1 Previously the landlord has written to me stating that they cannot require me to move and will not require me to move. 2 No alternative has in fact been offered. I've done the obvious and emailed pointing out the above and also expressing surprise at receiving a notice without warning. I have had a reply stating that they have noted what I have written. Now, what do I do? I am a Housing Association tenant and have lived in my flat for over twenty years. They want me to move so that they can sell the property and move me to a cheaper area. Any advice appreciated, please. -

Hi there I've had an Amex card (Amex BA rewards card) for several years. Back in September 2015 I sent a letter to tell them I had moved house and provided our new address. However I was getting my monthly statements on line by email so did not question whether they had updated my postal address on their records. In September 2016 I set up a standing order to cover £1000 per month payment but unbeknown to me the instruction failed. Even though Amex had my phone number and email contact details they did not let me know payments were not being received. Instead they wrote to me at my previous address. What's important here to understand is that up until this point Amex always contacted me via their online messaging system and my overseas mobile (due to the fact we lived overseas and this was an easy and immediate way to reach us). My expectation was therefore always that if Amex needed me urgently this is how they would contact me. Amex claim they never received my letter requesting they change my address. In January of this year (2017) I received an email from someone claiming to be a debt recovery agent for Amex. I thought it prudent to check with Amex this person was legitimate and also ascertained from Amex direct that they had cancelled my account and referred it to their debt collection agency. I immediately paid the missing payments and have continued to pay £1000 per month whilst I decide how to move forward. So my question is this? Even though Amex have cancelled my account they are continuing to charge interest on the balance each month. Which means that the payment I am making is mostly going to servicing the interest. I want to clear the original amount I owe them but do not think it is fair that I should have to pay interest when my account is cancelled. Should I talk to the debt collection agent and propose this? Or do I need to take a different approach (Ombudsman?). All advise greatly appreciated! Thanks in advance

-

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) The following regulation has been discussed for many months, and was finally laid before Parliament a few days ago (11th April). It comes into effect on 6th May 2017. The Road Vehicles (Registration and Licensing) (Amendment) Regulations 2017 http://www.legislation.gov.uk/uksi/2017/554/made

The following regulation has been discussed for many months, and was finally laid before Parliament a few days ago (11th April). It comes into effect on 6th May 2017. The Road Vehicles (Registration and Licensing) (Amendment) Regulations 2017 http://www.legislation.gov.uk/uksi/2017/554/made -

Good evening a couple of weeks ago I received court forms from Nottingham regarding CABOT. I have had a terrible time with this company, 3 times writing to ask for the creditors original signed credit agreement to no avail. I put a defence in to the money online tool (no idea what Im doing really) and stated that this company had harassed me (calls at work etc) and not supplied me with the credit agreement etc. Ive now received a letter from a company called Restons solicitors telling me my defence wont hold water and that I have 14 days to sort it Letter dated 28th March Ive been very ill since Friday so done nothing yet. Could someone please advise me as Ive no idea who Restons are or if they are real Thanking you in advance

-

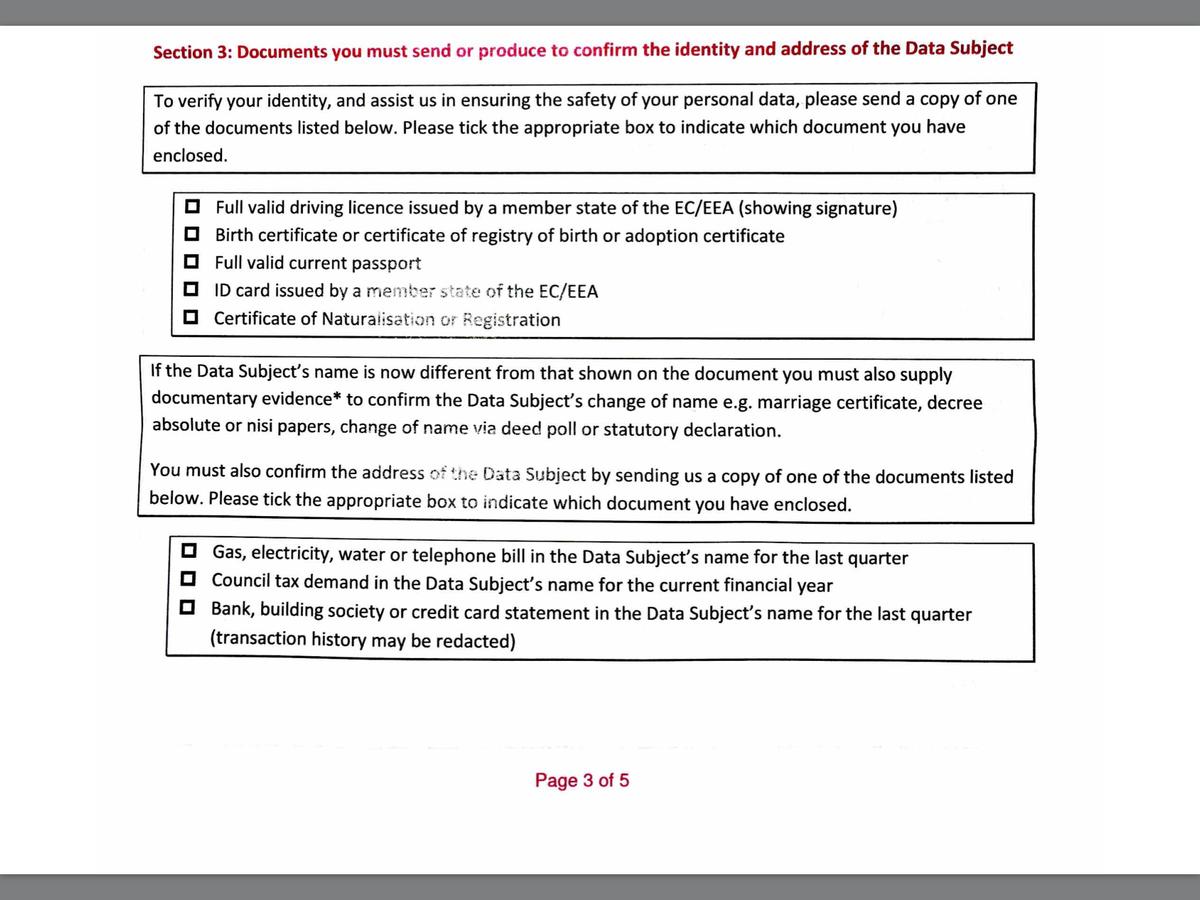

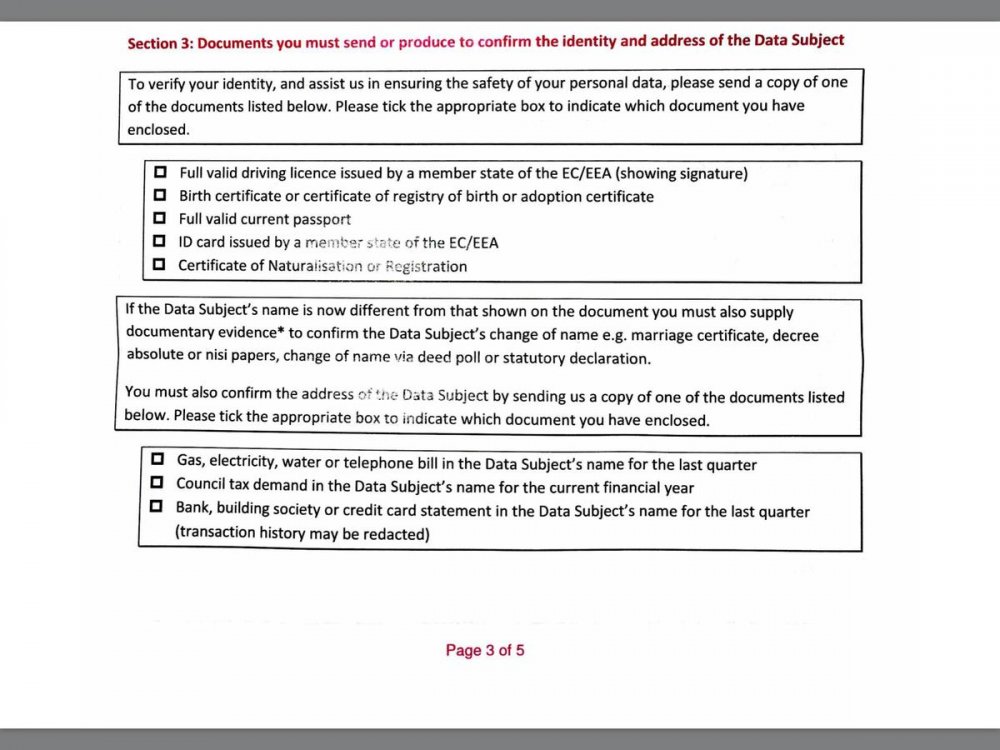

I've just sent off (with the £10 postal order) a Formal DSAR request to 1st Crud. All info required to be supplied, including a signature was provided in my formal and detailed letter. I've just received one of their 'please fill out this 5 page form' before we are obliged to do anything, however I'm not happy with what they are requesting I provide. There is no way I am ever going to provide them a copy of my driving licence, or bank statements and I'm back on here for some advice. I've been completing DSAR requests for approx 10 years, and apart from (almost) starting legal action with BC whilst some have been a struggle to get all info from and in a timely manner most have been compliant and not made me jump through too many hoops. (Oh apart from the DWP completely ignoring me for over 2 months! Still ongoing - but I class them in a different category to the CC companies and DCAs etc). Have the rules changed? I am now legally obliged to provide any of the following on the attached picture? Considering I've lived at the same address for over 10 years, and they've contacted me for 3-4 different companies at this same address, and threatened legal action to me at the same address, and supplied alleged CCA agreements, I would think that they should be fairly confident of my identity? Can I take this route, or will they likely play up and delay provision even though I don't (I think) have to legally provide the documents they have requested I send? Thanks ME_TOO

I've just sent off (with the £10 postal order) a Formal DSAR request to 1st Crud. All info required to be supplied, including a signature was provided in my formal and detailed letter. I've just received one of their 'please fill out this 5 page form' before we are obliged to do anything, however I'm not happy with what they are requesting I provide. There is no way I am ever going to provide them a copy of my driving licence, or bank statements and I'm back on here for some advice. I've been completing DSAR requests for approx 10 years, and apart from (almost) starting legal action with BC whilst some have been a struggle to get all info from and in a timely manner most have been compliant and not made me jump through too many hoops. (Oh apart from the DWP completely ignoring me for over 2 months! Still ongoing - but I class them in a different category to the CC companies and DCAs etc). Have the rules changed? I am now legally obliged to provide any of the following on the attached picture? Considering I've lived at the same address for over 10 years, and they've contacted me for 3-4 different companies at this same address, and threatened legal action to me at the same address, and supplied alleged CCA agreements, I would think that they should be fairly confident of my identity? Can I take this route, or will they likely play up and delay provision even though I don't (I think) have to legally provide the documents they have requested I send? Thanks ME_TOO

-

Hi all Just after some advice really, I traded my car in on Friday for a BMW 118d which to be honest I am happy with apart from the fact that the drivers side window switch (its a master switch which controls passenger window/driver window and electric mirrors) when I enquired about the car I was told it had 6 months MOT on it but they would put through a new MOT. This they have done and they did change 2 rear tyres as these were advisories, the guy I spoke to also said that it needed a new window switch....... picked the car up on Friday and again it was mentioned that the switch was changed so didnt think anything of it. However on way home from garage try windows and it doesnt work, I didnt bother mentioning that day as it was late Friday and thought I would wait til Monday. I emailed the garage yesterday and no response, emailed again today and so far no response. Now its only a window so its not a major big deal I suppose but I paid £7.5k for the car (7k trade-in on mine) and my car was immaculate and everything worked. Am I being a biy picky bearing in mind the car is 6.5 years old or not? The good news is that £250 of the £500 extra I paid was on my credit card so I do think I have some comeback via that if necesssary. ANy advice much appreciated!

-

Brief background summary. I had a loan with bank, defaulted and they got judgement and charging order. Took bank to court for PPI on the loan, got default judgement and warrant of execution. Bank applied to get judgement and warrant set aside. We reached a compromise that they would reduce balance of judgement and charging order and amend the same accordingly. They have since sold debt without reducing the balance or amending judgement or charging order. Whats the best way to handle this? can I claim damages? Thanks in advance.

-

I paid them for a couple months via Monthly Standing Orders which i set up, this was after the Debt Management Company I used folded, I then stopped paying all of them recently ... I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them They are the only 1 from 5 to provide thus far, so tbh i still had a great result This is very true, i assumed info from a company like StepChange would be best i would get, not a mention or suggestion of doing CCA's came from them Sometimes their hands are tied to give certain aspects of advice and as I say CAG was a blessing in disguise when i read what people were saying about making CCA requests I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them, they are the only 1 from 5 to provide thus far, so tbh i have still had a great result ! Better late than never, very true

I paid them for a couple months via Monthly Standing Orders which i set up, this was after the Debt Management Company I used folded, I then stopped paying all of them recently ... I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them They are the only 1 from 5 to provide thus far, so tbh i still had a great result This is very true, i assumed info from a company like StepChange would be best i would get, not a mention or suggestion of doing CCA's came from them Sometimes their hands are tied to give certain aspects of advice and as I say CAG was a blessing in disguise when i read what people were saying about making CCA requests I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them, they are the only 1 from 5 to provide thus far, so tbh i have still had a great result ! Better late than never, very true -

Hi guys - really need some advice! I received a PCN for allegedly parking without a valid permit around three months ago, I foolishly disregarded this and thought nothing more of the matter. Imagine my surprise when I received the below correspondence - This is the first letter I have received with regards to this matter and was wondering how best to proceed?

-

I need some advice as to what I should do... here are the details of my situation. I purchased in to a property scheme run by a vendor in Nov 2008 , where you pay the vendor £2000 and for this they find a buy to let property for you where the rent covers the mortgage payment , the vendor takes care of the purchase of the property, they take care of the solicitor, all the management, (renting, any bills) all bills after two years you have the option to sell the property or to continue to use their services. The Solicitor used was in this with the vendor, the valuation from the surveyor showed that the property was worth more than what I was paying After three months after purchasing the property, the rents stopped coming in I started to chase the vendor who told me they were having some cash flow problems and I will get the rents to cover the mortgage, this went on for a two to three months and soon the vendor had disappeared. I visited the property I had purchased and asked the tenant for the rent and to pay me directly, and found out that that the rent came very short of the monthly mortgage payment , I got a local estate to come and value the property and they valued it less than £120K of the purchase price. I went to the police and told them about this, they said there is nothing they can do as this is a civil case I then instructed a solicitor to investigate and their findings showed that the property was bought and sold in a very short period less than a month, where the price sold at was over inflated by 120k, without any work done to the property. I told the mortgage company and told them there is no way I can afford the to pay the mortgage, this was around June 2009, The mortgage company repossessed the property and sold it in 2010, this is where the shortfall of 110K is. The conveyancing solicitor was part of a fraud, the solicitor is now no longer around, they were an LLP and I have tried to take them to court and sue them and claim damages from their indemnity insurance, but the indemnity insurers have said they will not cover this as this was a fraudulent act intentionally done by the solicitor. Now the bank has passed the debt to a number of debt collectors , this is the third one who is contacting me. To make things even worse, at the time, back in 2008 I actually bought three properties via this vendor, so I actually have three mortgage shortfalls that I need to deal with. I have been living with a lot of stress ever since this has happened, it is really getting me down, has affected my whole life, mentally, physically, affecting my family. I feel I have been let down by the whole system, I purchased these properties in good faith, thinking this will be an investment for the future but in reality it has been nothing but a nightmare. I need to find out what I can do to stop the debt or not pay the shortfall the debt collectors are asking for. Can anyone help and point me in the right direction

I need some advice as to what I should do... here are the details of my situation. I purchased in to a property scheme run by a vendor in Nov 2008 , where you pay the vendor £2000 and for this they find a buy to let property for you where the rent covers the mortgage payment , the vendor takes care of the purchase of the property, they take care of the solicitor, all the management, (renting, any bills) all bills after two years you have the option to sell the property or to continue to use their services. The Solicitor used was in this with the vendor, the valuation from the surveyor showed that the property was worth more than what I was paying After three months after purchasing the property, the rents stopped coming in I started to chase the vendor who told me they were having some cash flow problems and I will get the rents to cover the mortgage, this went on for a two to three months and soon the vendor had disappeared. I visited the property I had purchased and asked the tenant for the rent and to pay me directly, and found out that that the rent came very short of the monthly mortgage payment , I got a local estate to come and value the property and they valued it less than £120K of the purchase price. I went to the police and told them about this, they said there is nothing they can do as this is a civil case I then instructed a solicitor to investigate and their findings showed that the property was bought and sold in a very short period less than a month, where the price sold at was over inflated by 120k, without any work done to the property. I told the mortgage company and told them there is no way I can afford the to pay the mortgage, this was around June 2009, The mortgage company repossessed the property and sold it in 2010, this is where the shortfall of 110K is. The conveyancing solicitor was part of a fraud, the solicitor is now no longer around, they were an LLP and I have tried to take them to court and sue them and claim damages from their indemnity insurance, but the indemnity insurers have said they will not cover this as this was a fraudulent act intentionally done by the solicitor. Now the bank has passed the debt to a number of debt collectors , this is the third one who is contacting me. To make things even worse, at the time, back in 2008 I actually bought three properties via this vendor, so I actually have three mortgage shortfalls that I need to deal with. I have been living with a lot of stress ever since this has happened, it is really getting me down, has affected my whole life, mentally, physically, affecting my family. I feel I have been let down by the whole system, I purchased these properties in good faith, thinking this will be an investment for the future but in reality it has been nothing but a nightmare. I need to find out what I can do to stop the debt or not pay the shortfall the debt collectors are asking for. Can anyone help and point me in the right direction