Search the Community

Showing results for tags 'application'.

-

Hi There, Been playing games with MBNA for months now on CCA etc and they passed onto PRA Group to chase, they have come back now and said the application was done digitally! Not sure where I stand now or what I can do? Thank you in advance for your help. Regards Steve H

-

I recently went on Nat West website to inquire about a loan, I progressed it but decided not to go any further as the interest rate was too high so I didn't apply for credit. I then discovered that Nat West had placed a hard search on my file for a credit application. I disputed this with Equifax as I had not made the application, they told me to take it up with Nat West who then told me that is how they do things. surely this isnt right or is it? any guidance would be appreciated.

I recently went on Nat West website to inquire about a loan, I progressed it but decided not to go any further as the interest rate was too high so I didn't apply for credit. I then discovered that Nat West had placed a hard search on my file for a credit application. I disputed this with Equifax as I had not made the application, they told me to take it up with Nat West who then told me that is how they do things. surely this isnt right or is it? any guidance would be appreciated. -

Credit Score Went Down After Application Declined

Zinnia posted a topic in Credit Reference Agencies

Hi Guys In November, I applied for a post office credit card and was declined despite having near perfect scores with Experian and Equifax. I used an eligibility checker first and it showed that I had a 95% chance of being approved so I felt confident to apply. However, while filling out the application form I did notice that there were no fields to enter information as a self-employed person but I proceeded anyway by entering info about my self-employed status so it may be that they only approve those that are employed. I received a letter from them confirming the decline but they didn't give a reason. It said that they used Experian. For several years I have had an Aqua card and they have increased my credit limit quite substantially. Over the last 6 months they have sent me a letter every month encouraging me to apply for a loan for up to £5,000 using the loan code they sent. I want to apply for a loan because the rate is 3X lower than their credit card rate. However, I'm concerned about my credit score being negatively affected again I wonder if someone could tell me how much time I should allow before applying for credit/loan again. Your advice would be appreciated. -

Hello everyone, I have recently issued a small claim against a company, but do not want to go through with it any further. The defendant did issue a defence and requested for Mediation, but subsequently changed their mind. I was wondering if I can still issue a Notice of discontinuance (N279) form before the case being allocated to a track? If yes, which court do I write down? Should I send this via post to the Money Claims centre in Manchester or via email? I have been utilising the new beta Money Claims service, which does not provide information on the matter. I was wondering if anyone could assist me? I'm new to this and this is my first small claims case.

Hello everyone, I have recently issued a small claim against a company, but do not want to go through with it any further. The defendant did issue a defence and requested for Mediation, but subsequently changed their mind. I was wondering if I can still issue a Notice of discontinuance (N279) form before the case being allocated to a track? If yes, which court do I write down? Should I send this via post to the Money Claims centre in Manchester or via email? I have been utilising the new beta Money Claims service, which does not provide information on the matter. I was wondering if anyone could assist me? I'm new to this and this is my first small claims case. -

Could you offer some advise on my situation please? I moved into a property in December 2010, and the Water bill was put into my name. I left this property at some point during 2014, at which point i had made no payments towards the water or been in contact with the water company. I've made good the debt now, ive actually cleared all my debts! My question is regards to the default date. The company placed the default in January 2016. They then applied for and won a CCJ by default in August 2016. I've raised a complaint as i believe the default should have been dated between March-July 2011. That is correct i assume? In regards to the CCJ, I have asked that they agree to have it set aside, as if they had placed the default on the correct date then it would have been statute barred. Im confident on my first point, how do you feel the second point (CCJ set aside) will be? I've already paid any monies i owe to them, but if they had placed the default correctly then it would have been statute barred before the date that they actually applied for it

Could you offer some advise on my situation please? I moved into a property in December 2010, and the Water bill was put into my name. I left this property at some point during 2014, at which point i had made no payments towards the water or been in contact with the water company. I've made good the debt now, ive actually cleared all my debts! My question is regards to the default date. The company placed the default in January 2016. They then applied for and won a CCJ by default in August 2016. I've raised a complaint as i believe the default should have been dated between March-July 2011. That is correct i assume? In regards to the CCJ, I have asked that they agree to have it set aside, as if they had placed the default on the correct date then it would have been statute barred. Im confident on my first point, how do you feel the second point (CCJ set aside) will be? I've already paid any monies i owe to them, but if they had placed the default correctly then it would have been statute barred before the date that they actually applied for it -

I took out a money claim to recover money owed. The Defendant hired a Solicitor who sent and acknowledgement and applied for extra time, 28 days, to file a defence, I made no objection to this application and the court never put it in front of a judge for ratifying. However, 28 days later when the date specified by the Solicitor on their sample order had passed, no defence had been filed, so I applied for the judgement to be made by default as no defence has been filed. The Solicitor then called me (4 days past filing date) requesting further information so that they could begin to put together their defence... (BEGIN to??!) and I pointed out that I had already applied for Judgement as they were now out of time (CPR 12.3 (2)a "The Claimant may obtain Judgement by Default where acknowledgement of service has been filed but a defence has not been filed and the time for filing has expired). The Solicitor said that the extra 21 days dont start until they are rubber stamped by a judge. Today I received notification from the Court that the request for judgement has been returned by the judge for referral to a District Judge. So, my question is: Where extra time is requested and not challenged, is it accepted that the extra time is granted by agreement? Or can this defendant solicitor continue to delay filing until they get a rubber stamp agreeing extra time? My reading of the rules that where extra time is agreed 28 days would be given, would apply where no challenge is made to the request for extra time. How do I challenge this and stop them late filing please?

-

Hi all My mother died in September and I've been putting off applying for a probate grant but I've made an attempt at completing application for probate form, (PA1) https://www.gov.uk/government/publications/apply-for-probate-form-pa1 and Inheritance Tax IHT205(2011) https://www.gov.uk/government/publications/inheritance-tax-return-of-estate-information-iht205-2011. I've read HMRC guidance notes but I think I'm missing something when completing the online version IHT205 because it flags up that my mother's estate could be liable for Inheritance Tax. I've carefully assessed Mum's assets and liabilities and assumed that once these were entered online it would automatically make the deductions but it doesn't appear to do this. My mother and father took out an equity release mortgage which amounts to £175,000, the property has been valued for probate at £375,000 so I would assume that the mortgage and any other liabilities should be deducted from the property value and other assets. Does anyone know what I'm doing wrong? Should I deduct the liabilities from the assets myself before adding them to the online application? If not, I'll give HMRC Helpline a ring in the morning. Thanks for reading, hope this makes sense.

-

A friend has been charged £27.56 in service/ call charges when applying for PIP over the telephone. I am aware that Esther McVey had been challenged regarding call charges with 08 numbers and I see that the government website has been changed to 0800 numbers now. However, I cannot see when the website was updated. Is there any chance of claiming these charges back from DWP/PIP as they are extortionate for vulnerable people who do not understand the implications of service charges on top of call charges?

-

Hi all. I am completely new here and just looking for some advice please. I bought a house in 2015 with no issues all went through with no problems. I went to view a new house on Sunday and approached a mortgage advisor who was going to go through our finances etc and see affordability for the new place, financially i knew it wouldnt be an issue. The advisor contacted me today to advise that I have an active CCJ on my account from 2014. And that due to this he couldn’t get us the mortgage that we needed. I download my credit report and there is a CCJ which I have never seen. My credit score is in the excellent category so I never had any idea that anything was wrong, I’ve never been refused credit in the time since it has been issued. I contacted the court who issued it today and they advised the company who lodged the case, I called them as I was already in a payment plan with them months before the date of the CCJ being filed. They have advised that I can settle the balance and the CCJ will show as satisfied which is better than active. Does anyone know if It’s too late to dispute the CCJ after 4 years of it being on file as I was making regular monthly payments to the student loan company before it was actually issued I did receive papers asking if I agreed to the amount owed and I stated that I did and was already in agreement to pay it back, i then received a letter advising to continue with the arrangement - no mention of a CCJ being issued. If I pay the CCJ and it shows as satisfied does this make my chances any better of securing a better mortgage or is it a lost cause now. Thanks for taking the time to read. Ps sorry if I’ve done this wrong or it’s posted in the wrong section . Nelly

-

Hi all, I'm hoping someone can advise, back in October I applied for a loan through Admiral but the application was unsuccessful. My credit score (i use Clearscore) went down this month with a note saying: What changed in July 2018 : Hard Search performed by Admiral Loans for Credit Application The October application is showing the exact same information - why would they simply perform another hard search without my consent? and is there anything i can do about it? Thank you H x

Hi all, I'm hoping someone can advise, back in October I applied for a loan through Admiral but the application was unsuccessful. My credit score (i use Clearscore) went down this month with a note saying: What changed in July 2018 : Hard Search performed by Admiral Loans for Credit Application The October application is showing the exact same information - why would they simply perform another hard search without my consent? and is there anything i can do about it? Thank you H x -

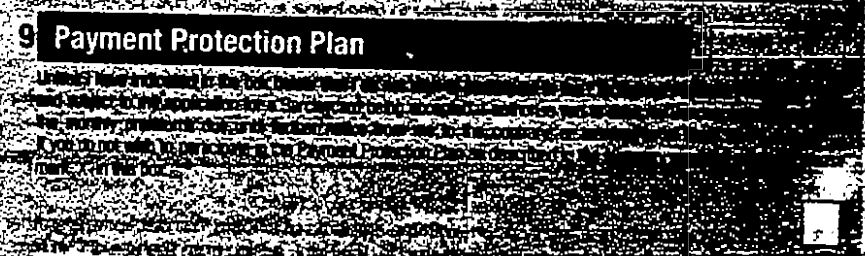

Does anyone have a Barclaycard application form from 1990 please? I know it's a long shot, but sadly the copy they have sent me is unhelpfully more or less illegible for the relevant section, and I need the exact wording. What I can discern from it reads like you have to indicate in the box to opt out, rather than the usual indicate to opt in. The final sentence appears to say and the section is titled Here's how it looks:

Does anyone have a Barclaycard application form from 1990 please? I know it's a long shot, but sadly the copy they have sent me is unhelpfully more or less illegible for the relevant section, and I need the exact wording. What I can discern from it reads like you have to indicate in the box to opt out, rather than the usual indicate to opt in. The final sentence appears to say and the section is titled Here's how it looks:

-

Hi all, firstly I'm posting on behalf of my step son & GF, as they are unsure of how to respond to/progress with their currently situation. Background BF / GF living with GF's parents. GF becomes pregnant. Both 'kicked out' - asked to find alternative accommodation. Accepted as 'Homeless' by the Local Authority, and that they have a 'priority need'. Currently in emergency Council-owned accommodation (pretty decent actually) in the centre of town. GF doesn't drive, BF has small mbike only. BF employed locally. GF was in college locally before pregnancy but now not. They have made applications to the Local Authority allocation scheme for housing, placed an interest bid on a property they were matched with, within the local area. Upon visiting, found it in poor condition, at the far end of a maze-type newish estate, and around 1.5 miles outside of the town centre. Please see attached the Local Authority letter, informing them that if they reject this property then the Council will discharge their obligation to house them. Since this letter has been received there has been a significant change of circumstances - BIRTH. GF has giving birth at 27 weeks ! A lovely baby girl, who is doing really well - as is mum GF & daughter are in a NICU approx 90 mins away from home town and will be for a substantial length of time. Clearly there will be a significantly increased requirement for local hospital interaction in the short term. Issue: BF & GF want to reject the visited property, but are worried the Council will them wash its hands of their housing requirement. Their reasoning is mainly that the location will leave GF isolated from amenities and her support network. Clearly the latter is now more important than it was at the start of the application, due to the significant change in circumstances. So, how do they proceed...? I'm presuming they should write to the Housing Advice and Homeless Manager specified on the attached letter, but what should they say..? Is there something standard available, or should they just blurt it all out and hope for the best..? Can the Local Authority really remove them from their care following such a change in circumstances....? Look forward to your comments... CLST1 2018-06-05.pdf

Hi all, firstly I'm posting on behalf of my step son & GF, as they are unsure of how to respond to/progress with their currently situation. Background BF / GF living with GF's parents. GF becomes pregnant. Both 'kicked out' - asked to find alternative accommodation. Accepted as 'Homeless' by the Local Authority, and that they have a 'priority need'. Currently in emergency Council-owned accommodation (pretty decent actually) in the centre of town. GF doesn't drive, BF has small mbike only. BF employed locally. GF was in college locally before pregnancy but now not. They have made applications to the Local Authority allocation scheme for housing, placed an interest bid on a property they were matched with, within the local area. Upon visiting, found it in poor condition, at the far end of a maze-type newish estate, and around 1.5 miles outside of the town centre. Please see attached the Local Authority letter, informing them that if they reject this property then the Council will discharge their obligation to house them. Since this letter has been received there has been a significant change of circumstances - BIRTH. GF has giving birth at 27 weeks ! A lovely baby girl, who is doing really well - as is mum GF & daughter are in a NICU approx 90 mins away from home town and will be for a substantial length of time. Clearly there will be a significantly increased requirement for local hospital interaction in the short term. Issue: BF & GF want to reject the visited property, but are worried the Council will them wash its hands of their housing requirement. Their reasoning is mainly that the location will leave GF isolated from amenities and her support network. Clearly the latter is now more important than it was at the start of the application, due to the significant change in circumstances. So, how do they proceed...? I'm presuming they should write to the Housing Advice and Homeless Manager specified on the attached letter, but what should they say..? Is there something standard available, or should they just blurt it all out and hope for the best..? Can the Local Authority really remove them from their care following such a change in circumstances....? Look forward to your comments... CLST1 2018-06-05.pdf -

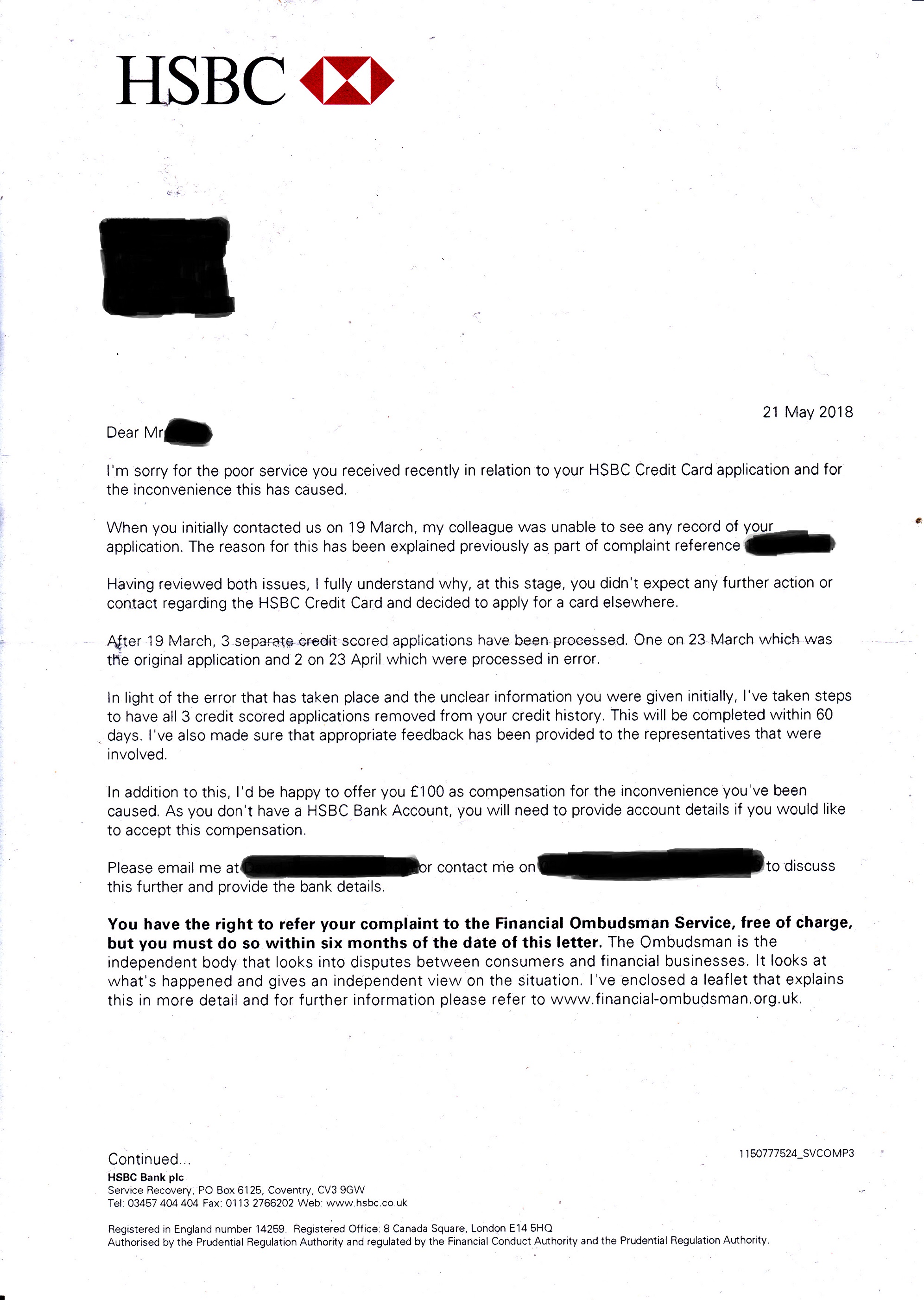

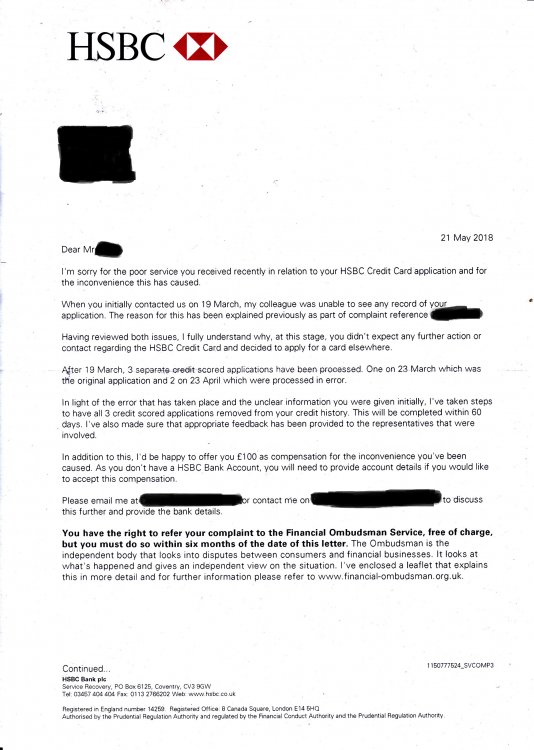

I was wondering what people were thinking of the letter I received from HSBC regarding a recent credit card application I had with them. In March I applied for a HSBC credit card in order to do a balance transfer after checking playing like Money Saving to see how eligible I was and came back 90/95%. After getting the reference number saying my application was being processed I left it at that expecting an email within the 5 days they would let me know. After over a week I heard nothing I called them to check. It was on this occasion I was told they had no record of my application. Unfortunately I didn't make a note of the first reference number but I never needed this before . After speaking to them they said the issue was I said that I had an account with them when I said I didn't. I have a mortgage with them and never thought of this as an account as such like an current account. It was only when I I was on the phone to them I looked at my mortgage reference number I never realised the 14 digit number was a sort code and account number together. I told them I was going to leave it then and got a credit card through the Post Office paid in 3 days! SI left it and then I got a letter from HSBC telling me my application had been unsuccessful. Funny that considering they said I hadn't applied. A month or so later I got a letter saying you have been successful in my credit card application! I didn't apply again and it appears that they randomly reapplied for me hence the attached letter. To me it seems they are running a little scared as they are offering me £100 in compensation. Yes this would be nice but I would think banks usually offer a minimum compensation and I'm wondering if I take this to the Financial Ombudsman may they be in bigger trouble and have to compensate me much more. Just wondering what peoples views on this are?

-

Fully digital divorce application launched to the public England and Wales READ MORE HERE: https://www.gov.uk/government/news/fully-digital-divorce-application-launched-to-the-public

Fully digital divorce application launched to the public England and Wales READ MORE HERE: https://www.gov.uk/government/news/fully-digital-divorce-application-launched-to-the-public -

Hi I've just got a letter from HMRC regarding tax credit checks saying that they think my payments maybe wrong. I am on JSA and due to mental health problems applied for PIP taking the advice of my support worker. They want to see all my details,proofs of children living with me and proof of all my job searches since September. There was no change in my circumstances.The only change is my eldest turning 18 in January but continuing non-advanced education. They requested my details from 05/04/17. I have almost all the information they are asking for but receipts of spendings. Should I be worried?Is this a common process?

-

Hi All Received a letter from Mortimer Clarke today regarding a debt to Cabot Financial. Letter claims their client obtained a judgement against me on 04/02/2016. First paragraph says "Because you have failed to pay the judgement debt in accordance with the terms of the judgement our client is now entitled to take action to enforce the judgement order against you. Our client has instructed us to apply to the County Court for an Attachment to Earnings order to be made against you." Final paragraph says "If you do not contact us within 7 days , then our client has instructed us to apply for an Attachment of Earnings Order against you." Notes: 1. I have checked Trust Online for my current and previous 3 addresses and there are no ccjs registered against me. 2. I did not receive any correspondence threatening to take me to court, advising I was being taken to court or asking if I wished to defend and finally I did not receive a judgement. 3. The letter makes no mention which court they obtained the judgement from or any judgement reference number. 4. The debt is from 2007 and I believe it may well be statute barred now. Can anyone provide any thoughts or advice on how I should proceed at this point? kind regards

Hi All Received a letter from Mortimer Clarke today regarding a debt to Cabot Financial. Letter claims their client obtained a judgement against me on 04/02/2016. First paragraph says "Because you have failed to pay the judgement debt in accordance with the terms of the judgement our client is now entitled to take action to enforce the judgement order against you. Our client has instructed us to apply to the County Court for an Attachment to Earnings order to be made against you." Final paragraph says "If you do not contact us within 7 days , then our client has instructed us to apply for an Attachment of Earnings Order against you." Notes: 1. I have checked Trust Online for my current and previous 3 addresses and there are no ccjs registered against me. 2. I did not receive any correspondence threatening to take me to court, advising I was being taken to court or asking if I wished to defend and finally I did not receive a judgement. 3. The letter makes no mention which court they obtained the judgement from or any judgement reference number. 4. The debt is from 2007 and I believe it may well be statute barred now. Can anyone provide any thoughts or advice on how I should proceed at this point? kind regards -

posted on behalf of a friend after checking her credit file because she was turned down for credit. it showed she had a CCJ. and has applied to for courts for it to be set aside on the basis she knows nothing about it today she has received a letter off cabots solicitors confirming it was for a mobile phone and papers were sent to previous address. it states that the is no prospect of setting this aside and invites her to withdraw her action whats the next step https://www.photobox.co.uk/my/photo/full?photo_id=10030744201[/img]

-

Hi folks, hope someone can give me some advice please. I missed a month's direct debit for my electricity supply from edf; they cancelled the direct debit and gradually I fell behind. I used their online chat application and 'spoke' to an operative - I said that as I'm paid weekly I'd be able to repay the outstanding amount at £25 per week, ie £100 every four weeks. The lady said I had to pay by direct debit, £100 a month I said I'd rather pay weekly and she said that she would note that on my account. I set up a standing order and have paid £25 every Friday for the last probably 4 months. The outstanding was about £400-ish, sorry I can't remember exactly. I started getting letters from edf saying I had this outstanding balance that needed to be paid off, then would come home from work to notes through the door from debt collectors saying they'd tried to gain access. This morning I had a letter through the post from Resolvecall saying that they are applying for a warrant to come into my home and fit a prepayment meter and the hearing is on 12 October at my local court house. The amount they say is outstanding is £431.41 I read the meter and sent it to edf last week to see where I was the bill was in the region of £600. Resolvecall letter is dated 25 September and I read the meter before that so their info is out of date. I'm paying this as quick as I can and now I'm worried sick. What should I do please? Thanks in advance

Hi folks, hope someone can give me some advice please. I missed a month's direct debit for my electricity supply from edf; they cancelled the direct debit and gradually I fell behind. I used their online chat application and 'spoke' to an operative - I said that as I'm paid weekly I'd be able to repay the outstanding amount at £25 per week, ie £100 every four weeks. The lady said I had to pay by direct debit, £100 a month I said I'd rather pay weekly and she said that she would note that on my account. I set up a standing order and have paid £25 every Friday for the last probably 4 months. The outstanding was about £400-ish, sorry I can't remember exactly. I started getting letters from edf saying I had this outstanding balance that needed to be paid off, then would come home from work to notes through the door from debt collectors saying they'd tried to gain access. This morning I had a letter through the post from Resolvecall saying that they are applying for a warrant to come into my home and fit a prepayment meter and the hearing is on 12 October at my local court house. The amount they say is outstanding is £431.41 I read the meter and sent it to edf last week to see where I was the bill was in the region of £600. Resolvecall letter is dated 25 September and I read the meter before that so their info is out of date. I'm paying this as quick as I can and now I'm worried sick. What should I do please? Thanks in advance -

Hi, My partner has been paying off a nominal monthly amount to Link Financial since the card debt was sold to them by MBNA. Sent Link a CCA in June but have had no reply. Sent a SARN request to MBNA and had a reply with only the attached request form copy and a second page with the terms and conditions. From reading other posts I think that this is invalid and therefore unenforceable. Would one of you more experienced people be good enough to have a look at give me your opinion. It seems to refer to paragraphs that don't exist and there is no lending limit or interest rate shown. We have since (last week) written to Link re their failure to supply a valid CCA and await their response! What is our next move please? L CCA Request Load.pdf

Hi, My partner has been paying off a nominal monthly amount to Link Financial since the card debt was sold to them by MBNA. Sent Link a CCA in June but have had no reply. Sent a SARN request to MBNA and had a reply with only the attached request form copy and a second page with the terms and conditions. From reading other posts I think that this is invalid and therefore unenforceable. Would one of you more experienced people be good enough to have a look at give me your opinion. It seems to refer to paragraphs that don't exist and there is no lending limit or interest rate shown. We have since (last week) written to Link re their failure to supply a valid CCA and await their response! What is our next move please? L CCA Request Load.pdf -

Hi all, I have received a form N244A notice of hearing of application today for a hearing scheduled for 20 Oct 17. This is in relation to a Tomlin Order that i had been paying monthly since april 15. In may this year i was signed off from work due to ill health and only receive statutory sick pay at approx £400 per month. (i am still off work) I contacted all my creditors and informed them and all were happy with token payments (TPP set up via stepchange) I contacted pestons to tell them and offered them a reduced payment of £20 per month until i was back in work when i would continue with the agreed 200 a month. They wanted bank statements, employers letters, GP letters and various other bits of paper. i didn't supply them with any of it - they already have too much info on me in my opinion. This is the reason for the N244A arriving today. Can i apply to the court for a variation at this stage or have i missed the boat on that one? If so do i need to do anything or wait until the imminent CCJ is served on me? Any advice will be greatly appreciated.

Hi all, I have received a form N244A notice of hearing of application today for a hearing scheduled for 20 Oct 17. This is in relation to a Tomlin Order that i had been paying monthly since april 15. In may this year i was signed off from work due to ill health and only receive statutory sick pay at approx £400 per month. (i am still off work) I contacted all my creditors and informed them and all were happy with token payments (TPP set up via stepchange) I contacted pestons to tell them and offered them a reduced payment of £20 per month until i was back in work when i would continue with the agreed 200 a month. They wanted bank statements, employers letters, GP letters and various other bits of paper. i didn't supply them with any of it - they already have too much info on me in my opinion. This is the reason for the N244A arriving today. Can i apply to the court for a variation at this stage or have i missed the boat on that one? If so do i need to do anything or wait until the imminent CCJ is served on me? Any advice will be greatly appreciated. -

Hi all, I'm new to this site but I really need help. a few years ago I got myself into a right pickle with debt. I was young and stupid and when it came to having to pay, I couldn't. I have had letters from collection 'enforcement officers' which I haven't given a second thought, letters have been binned etc and we've since moved house. Yesterday morning two men knocked my door and handed me a form from the local sheriff court advising that I will be taken to court in order to recoup the money owed to the collection agency. They did not introduce themselves (later found them to be capquest agents from a clause in the paperwork) and I did not acknowledge the debt or confirm who I was in relation to the person they were looking for. What do I do? Where do I stand with this? The debt was bought by capquest in December 2012 from original creditor Very and I have had zero contact with either since defaulting on payment to Very in November 2012.

Hi all, I'm new to this site but I really need help. a few years ago I got myself into a right pickle with debt. I was young and stupid and when it came to having to pay, I couldn't. I have had letters from collection 'enforcement officers' which I haven't given a second thought, letters have been binned etc and we've since moved house. Yesterday morning two men knocked my door and handed me a form from the local sheriff court advising that I will be taken to court in order to recoup the money owed to the collection agency. They did not introduce themselves (later found them to be capquest agents from a clause in the paperwork) and I did not acknowledge the debt or confirm who I was in relation to the person they were looking for. What do I do? Where do I stand with this? The debt was bought by capquest in December 2012 from original creditor Very and I have had zero contact with either since defaulting on payment to Very in November 2012. -

Hi there I have received a hand delivered envelope (I haven't signed for it, don't know if that makes any difference) containing a Simple Procedure Notice of Claim by Arrow Global for an Aqua credit card debt. I have never received one of these before and I am not entirely sure what it is. Is this a fishing expedition by Arrow to pressure me to respond - there are no court stamps on the letter or date to attend court. A Time to Pay application has been included. The amount they are asking for is more than the credit limit as on the card, I assume the balance is made up of fees/late payment charges. If I ignore it what will happen - is it likely to proceed to court? The balance is for £737.00. I took out the credit card in November 2014, Arrow say they purchased the debt from Aqua in August 2016 and that they have sent letters on 2 occasions in May 2017 to which they had no response - I do not recall ever receiving these letters. I did make repayments to the card, but same old story, I got into financial difficulty, they started adding on late payment fees and it all snowballed from there. I am unemployed at the moment and not claiming benefit as my live in partner works full time. I do not receive any tax credits, just child benefit for 1 child. Can anyone help me as I don't really know what to do here. I have until 14/09/2017 to respond. I have been reading the forums but there is so much information on there and I don't know where to start. Thank you.

Hi there I have received a hand delivered envelope (I haven't signed for it, don't know if that makes any difference) containing a Simple Procedure Notice of Claim by Arrow Global for an Aqua credit card debt. I have never received one of these before and I am not entirely sure what it is. Is this a fishing expedition by Arrow to pressure me to respond - there are no court stamps on the letter or date to attend court. A Time to Pay application has been included. The amount they are asking for is more than the credit limit as on the card, I assume the balance is made up of fees/late payment charges. If I ignore it what will happen - is it likely to proceed to court? The balance is for £737.00. I took out the credit card in November 2014, Arrow say they purchased the debt from Aqua in August 2016 and that they have sent letters on 2 occasions in May 2017 to which they had no response - I do not recall ever receiving these letters. I did make repayments to the card, but same old story, I got into financial difficulty, they started adding on late payment fees and it all snowballed from there. I am unemployed at the moment and not claiming benefit as my live in partner works full time. I do not receive any tax credits, just child benefit for 1 child. Can anyone help me as I don't really know what to do here. I have until 14/09/2017 to respond. I have been reading the forums but there is so much information on there and I don't know where to start. Thank you. -

Hi I received a claim form last year with regard to an apparent arrow global debt I owe. The debt was bought from a halifax credit card. I did a CCA and CPR request to them straight away. There was then a stay on proceedings while they got the relevant documentation together. They have now submitted a notice of application to get the stay lifted and for summary judgement to be made against me. However they do not appear to attached terms and conditions to the credit agreement, just something entitled 'Key Financial Information'. Please see attached document. They have also not supplied a copy of the default notice, just a computer database entry of it. I am going to base a defence on the fact they have not complied with the CCA request, due to the missing terms and conditions. So have not complied with section 78 of the CCA. Also that they have not supplied a copy of the default notice, therefor cannot prove that a compliant default notice has been served, pursuant to sections 87 and 88 of the CCA. Please could you have a look at the three attachments and let me know what you think. credit agreement, terms and conditions(supposed), and default notice database entry. Thanks CCA return.pdf

Hi I received a claim form last year with regard to an apparent arrow global debt I owe. The debt was bought from a halifax credit card. I did a CCA and CPR request to them straight away. There was then a stay on proceedings while they got the relevant documentation together. They have now submitted a notice of application to get the stay lifted and for summary judgement to be made against me. However they do not appear to attached terms and conditions to the credit agreement, just something entitled 'Key Financial Information'. Please see attached document. They have also not supplied a copy of the default notice, just a computer database entry of it. I am going to base a defence on the fact they have not complied with the CCA request, due to the missing terms and conditions. So have not complied with section 78 of the CCA. Also that they have not supplied a copy of the default notice, therefor cannot prove that a compliant default notice has been served, pursuant to sections 87 and 88 of the CCA. Please could you have a look at the three attachments and let me know what you think. credit agreement, terms and conditions(supposed), and default notice database entry. Thanks CCA return.pdf -

Hello I'm looking for advise. I live overseas for past 10 years. Yesterday at a friends address in UK where I receive my bank statements a letter arrived looking official. At my request my friend opened it. It is a Notice of Application for Attachments of Earnings Order. Judgement Creditor: Hoist Portfolio Holding 2 Limited. In the: Country Court Money Claims Centre. Amount 3,975.28 GB. The Judgement Debtor is under my maiden name and I've since been married, divorced and re-married. I have never heard of this company and no of no debt to them. They are not listed on companies house, but from research it seems they are linked to Robinson Way a DCA. There is no contact telephone number and only instruction to pay Howard Cohen & Co Solicitors, based in Leeds. Again they are not registered on Companies House. The form looks official with case number and reference number. The document is dated 17th May 2017 and says payment required in 8 days of notice or further action including a possible 14 days prison. I am very concerned especially as this is now logged at a friends address, where i have never lived but do get my UK bank statements sent to. Any advise gratefully received.

Hello I'm looking for advise. I live overseas for past 10 years. Yesterday at a friends address in UK where I receive my bank statements a letter arrived looking official. At my request my friend opened it. It is a Notice of Application for Attachments of Earnings Order. Judgement Creditor: Hoist Portfolio Holding 2 Limited. In the: Country Court Money Claims Centre. Amount 3,975.28 GB. The Judgement Debtor is under my maiden name and I've since been married, divorced and re-married. I have never heard of this company and no of no debt to them. They are not listed on companies house, but from research it seems they are linked to Robinson Way a DCA. There is no contact telephone number and only instruction to pay Howard Cohen & Co Solicitors, based in Leeds. Again they are not registered on Companies House. The form looks official with case number and reference number. The document is dated 17th May 2017 and says payment required in 8 days of notice or further action including a possible 14 days prison. I am very concerned especially as this is now logged at a friends address, where i have never lived but do get my UK bank statements sent to. Any advise gratefully received. -

Hi, I am in need of urgent advice. In April 2014 after losing a High Court case brought against myself and 8 others by our former employer, an interim charging order was made final. During the hearing I offered to pay the judgement debt (£8,000 + costs and interest of £120,000.00) by affordable monthly instalments of £100.00 but this was refused by the claimant who stated to the court that they had "no intention of applying for an order for sale but merely wanted to protect their interests". I subsequently made a number of instalment offers to the claimants but each offer was refused and indeed, my letters were often ignored by the claimant and their solicitor or they would take months to reply. In December 2016 I received a copy of an order issued by the High Court granting leave to the claimants to apply for an order for sale. The witness statement attached to the order was prepared by a solicitor who has subsequently been struck off for dishonesty and fraud! The statement also contain a number of factual mistakes and exaggerated the value of my home describing a different property to the one that I actually own. (using a Zoopla valuation as evidence of property value). The claimants issued their application for leave in the QBD of the High Court and the application was subsequently transferred to the Chancery Division where the order for leave was granted. the case was then transferred to the Central County court before being transferred again to Portsmouth County Court. At the hearing, the claimants failed to turn up and had written the day before to the court stating that they believed that they would not get a fair hearing (as one of my codefendant's partner had worked at the court 10 years previously!!!). The DJ was not impressed but would not dismissed the case as he believed that the claimants would only apply to reinstate proceedings. He subsequently transferred the proceedings to another County Court where the application will now be heard on 26th May (for directions). I am sorry that this preamble is so long winded! I need advice about what to do next. At the Portsmouth hearing the DJ alluded to the Human Rights Act (I assume he meant Article 8) although I am not sure how to use this during the hearing. My home is in joint names with my wife. My 20 year old daughter also resides with us. She is a full time university student and suffers with anxiety and dyslexsia. My wife works part time on a modest income. My income is also quite modest. The correct zoopla valuation for my home is £146K approx and my current interest only mortgage is £138K. After deduction of estate agents commission, solicitors and removal costs there is gross equity of about £2,000.00 (half of which presumably will have to be paid to my wife as she is not a party to the proceedings). The High court have never determined what my financial interest in the property actually is My interest only mortgage ends in about 6 years and, as I cannot afford to repay the loan, my family and I will have to move (possibly to a shared ownership property). I would welcome any advice and assistance that any cagger's can give to me about how to deal with this upcoming hearing (assuming that the claimant's turn up this time). In anticipation I appreciate any help that can be provided to me.