Search the Community

Showing results for tags 'satisfied'.

-

Hi Just received my credit file and after getting into a bad financial situation I have a total of 19 defaults on my credit file!, 11 are due to drop of this year and 3 next year the rest are around 2022, for the latter do you think my credit file will improve If I pay them of so they are marked as satisfied? or should I just wait, none of them are chasing me for payment at the minute Just edited to add one is for a mobile phone debt that I was paying for 2 years at £35 per month, it says I owe £550.00 now

Hi Just received my credit file and after getting into a bad financial situation I have a total of 19 defaults on my credit file!, 11 are due to drop of this year and 3 next year the rest are around 2022, for the latter do you think my credit file will improve If I pay them of so they are marked as satisfied? or should I just wait, none of them are chasing me for payment at the minute Just edited to add one is for a mobile phone debt that I was paying for 2 years at £35 per month, it says I owe £550.00 now -

I have an ancient Myjar default from 2012 from when they tried to pursue £1055 against £50 borrowed. It went through a few DCAs who sent standard threat letters which were easily seen off with section 77 requests but no court action was ever taken, and it should have gone SB in March. I was looking forward to it being gone from my file on today's Noddle update, however instead I've found that 1 week before the default reached 6 years, it was suddenly marked 'satisfied' and it now appears as a satisfied closed account rather than having dropped off my file altogether, where presumably it will sit until 2024. Obviously it's new status is far less damaging than the active default, but not as good as it having disappeared and when I'm so close to having a clean sheet on my credit file I don't want this thing hanging around on it in any form. How can they mark it as satisfied when it has never been acknowledged?

I have an ancient Myjar default from 2012 from when they tried to pursue £1055 against £50 borrowed. It went through a few DCAs who sent standard threat letters which were easily seen off with section 77 requests but no court action was ever taken, and it should have gone SB in March. I was looking forward to it being gone from my file on today's Noddle update, however instead I've found that 1 week before the default reached 6 years, it was suddenly marked 'satisfied' and it now appears as a satisfied closed account rather than having dropped off my file altogether, where presumably it will sit until 2024. Obviously it's new status is far less damaging than the active default, but not as good as it having disappeared and when I'm so close to having a clean sheet on my credit file I don't want this thing hanging around on it in any form. How can they mark it as satisfied when it has never been acknowledged? -

A friend of mine had a CCJ that was satisfied after he sold his house, we were talking about it and it seems there were £200 a month admin fees were being added to the account before it went to CCJ. The question is can he go back and SAR the company and claim back the Fees or is it too late. He settled the CCJ earlier this year, the CCJ was over 6 years old and attached to his house. Thanks

-

Good afternoon folks, I have been looking around for advice on the following as i am trying to clean up my credit files folowing completion of an IVA in August 2016. In summary, IVA started in June 2010, settled in August 2016. One of the creditors has finally updated the credit file at Equifax as below :- You can see that there is no default date on this entry, which should be the start date for the IVA. Is this entry going to stay on there for another 6 years from the settlement date, which should also be the date for te end of the IVA? If i have the default date corrected will the entry then disappear ? This creditor, Nationwide, seems to be reluctant to assist. Urkood.

Good afternoon folks, I have been looking around for advice on the following as i am trying to clean up my credit files folowing completion of an IVA in August 2016. In summary, IVA started in June 2010, settled in August 2016. One of the creditors has finally updated the credit file at Equifax as below :- You can see that there is no default date on this entry, which should be the start date for the IVA. Is this entry going to stay on there for another 6 years from the settlement date, which should also be the date for te end of the IVA? If i have the default date corrected will the entry then disappear ? This creditor, Nationwide, seems to be reluctant to assist. Urkood.

-

I have a charge order placed on my house by Bristol & Wessex Water for £1800. They recently sent me a letter stating that if I don't pay the full amount they will be taking legal action and apply for an order for sale. I then will be sent an order to vacate my property within 28 days. My house is owned outright with no mortgage and currently valued around £200K. I am living on a small private pension with no chance of paying back the debt. I went to the CAB who told me that I will end up homeless and living on the streets as there is no social housing available for single men. The Water company placed a CCJ on my credit record so it's impossible for me to borrow money to pay back the debt and keep my house. I could never understand why there were homeless people on the streets, but I do now. I will be joining them soon. What an idiot I was buying a house. If I had a council house I would have nothing to worry about and a safe roof over my head. I know a chap near here who lives in a housing association bungalow. He owes banks £73k and will not end up homeless. Comments welcome.

I have a charge order placed on my house by Bristol & Wessex Water for £1800. They recently sent me a letter stating that if I don't pay the full amount they will be taking legal action and apply for an order for sale. I then will be sent an order to vacate my property within 28 days. My house is owned outright with no mortgage and currently valued around £200K. I am living on a small private pension with no chance of paying back the debt. I went to the CAB who told me that I will end up homeless and living on the streets as there is no social housing available for single men. The Water company placed a CCJ on my credit record so it's impossible for me to borrow money to pay back the debt and keep my house. I could never understand why there were homeless people on the streets, but I do now. I will be joining them soon. What an idiot I was buying a house. If I had a council house I would have nothing to worry about and a safe roof over my head. I know a chap near here who lives in a housing association bungalow. He owes banks £73k and will not end up homeless. Comments welcome. -

Hi, We have a credit card debt with MBNA taken out in 2008 which defaulted in 2013. It is showing on CRA as 'satisfied' with MBNA, but then appeared as Aktiv Captial, who chased through 2013 - 2015. The debt is now with PRS Group and we have had a letter asking for payment or Court Action will ensue. If the debt is showing 'satisfied' can PRS still push for payment, or is this 'satisfied' because the debt has been bought? We wrote to Aktive in 2013 asking for CCA, they sent us photocopied version, scribbled numbers over and no sig. Do we just ignore PRS? We have had one succesfully thrown out case with another card company who folded at Court, can we do the same again? Thanks skywalker

-

Hi everyone I'm trying to sort out my credit file so i can apply for a mortgage. In the past I was careless with money but for the past couple of years I have been responsible. I have 4 defaults on my file, one is for a capital one card. The account was opened in 2009 and since 2010 the card was not used and I was paying off the minimum payment each month (by automatic payment) My bank card had to be changed when i got married and I didn't update the payment method and I had arrears letters which I stupidly ignored. I did not hear anything for a good while and the debt got sold to Lowell in 2014 The default date is 14/6/2014 and the debt is fully satisfied. I paid it off in full recently Is there any way i can get this removed from my credit file? This is my most recent default and I don't want to wait until 2020 to apply for a mortgage (I will be nearly 40 at that time) Recently for the past 12 months I have accounts with vanquis, aqua, jd william, very, littlewoods, ee, vodaphone, o2 that are all upto date with no late payments. I am rebuilding my credit file but I will find it difficult to get a mortgage with these defaults on here. Thanks

-

.thumb.jpg.bf2f59e5260173230834ce3ad8015900.jpg) Many questions have been raised about Credit Files. A lot of confusion exists about how to interpret elements of a CR (Credit Report) However, don't fear, the wonderful people at Experian have helpfully explained when you should see "Settled" or "Satisfied" on your CRA Report. This includes accounts that have been subject to arrears but not defaulted. So if you default on an account, once paid off this will change to "Satisfied" Please remember that when negotiating a Payment Plan at a discounted rate, the Creditor has the legal right to change this status to "Partially Satisfied" Settled Vs Satisfied.pdf

Many questions have been raised about Credit Files. A lot of confusion exists about how to interpret elements of a CR (Credit Report) However, don't fear, the wonderful people at Experian have helpfully explained when you should see "Settled" or "Satisfied" on your CRA Report. This includes accounts that have been subject to arrears but not defaulted. So if you default on an account, once paid off this will change to "Satisfied" Please remember that when negotiating a Payment Plan at a discounted rate, the Creditor has the legal right to change this status to "Partially Satisfied" Settled Vs Satisfied.pdf -

this could be a very stupid questions but I notice on my CRA files some loans/debts show as settled whilst others show as satisfied. Which is better? I ask as I have an aqua card debt I need to pay and want to request a full and final settlement figure but part of my request is also asking that the debt be shown as nothing else owing on it.

this could be a very stupid questions but I notice on my CRA files some loans/debts show as settled whilst others show as satisfied. Which is better? I ask as I have an aqua card debt I need to pay and want to request a full and final settlement figure but part of my request is also asking that the debt be shown as nothing else owing on it. -

An interesting story for general practice this morning. The post on the BBC website today links patient satisfaction with GP antibiotic prescribing levels. http://www.bbc.co.uk/news/health-35008128 As a practice manager I've seen this myself, people wanting to complain that their request for antibiotics (ABx) has been refused, normally accompanied by "well, Dr. X always gave them to me..." We have a nickname for GP's who prescribe appropriately, Dr. No! Because it seems they spend much of their day saying just that. You find that most younger GP's are quickly labelled as a Dr. No and they quiclky develop a whole tranche of patients who don't want to see them and would sooner see the older, 'easier' GP. Is it down to GP's who are less strong willed in the past changing public perception and expectations? I think it might be, it's far 'easier' to give someone what they want, but is it clinically appropriate? No, of course not. It was only in August this year that GP's were threatened by NICE with being disciplined for prescribing too many ABx(http://www.bbc.co.uk/news/health-33961241) So, what's your take on it? Are you left feeling short changed when you leave the surgery empty handed? Are you happy that your GP is one of the stronger, more clinically adept ones who prescribe appropriately or would you prefer one that NICE want disciplined/struck off?

-

Hi all, Back after a long break, good to see some of the old familiar names are still here.... My OH has a very complicated credit history. Lots of accounts are being paid off under a plan which was originally put in place by CAB, then taken over by me once i discovered CAG. She has just received an 'offer' from our good friends at Lowell - a discount of 75% to pay off an old bank debt. on receipt of payment they will 'update your credit file to show the account as partially satisfied and we will close your account'. Now, would I be right in thinking that 'partially satisfied' is absolutely no use to us, and we should ignore this offer like all the rest? Just to avoid the obvious questions, this loan is certainly pre-2007; we are not currently paying anything, and i don't remember without digging into the mountain of files when the last payment or acknowledgement was. All i need is an opinion on the 'partially satisfied' gambit.

-

Good afternoon all This is my first post on this forum. I received a letter from the lowell group saying they had checked my credit file and see no reason for not paying and that they believe i work etc etc and that they will be applying for CCJ. Two days later i receive a letter offering me a discount of 75% saying they will mark as partially satisfied and close my account. Now i have not made a payment or acknowledged the debt since 2007, but on looking at my credit file it says default November 2009. Would I be correct in thinking that it will not be statute barred until November 2015? Thanks

-

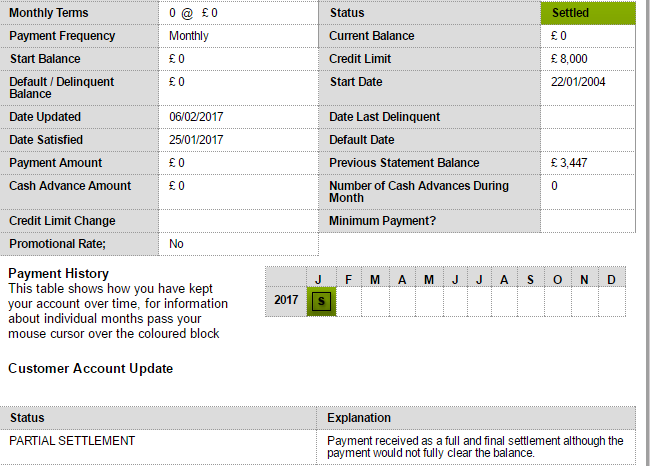

I received a letter from one of the debt companies that have taken over a debt I had for £165 they offered me a settlement payment of £50 so I took this offer and I have paid the £50 The guy I spoke to was rude and very unhelpful! He told me that this account would show up as Settled instead as Satisfied .. If I were to pay the £165 then it would be satisfied, he then went on to ask me a number of questions as to why I could afford to pay £50 but yet I can not pay £165. So I am wondering what the difference between Satisfied & Settled is ?

-

I had a financial based company take money out my account without my consent or permission and they only offered me 50% refund for this membership fee. I complained and continued for weeks complaining without any email responses and got advice and support from the Ombudsman and after some communication I had with rogue company the FO contacted them and although the company was unwilling to resolve my issue with me they got the full refund plus some compensation as it took 7 weeks and some stress to get a full refund. At the same time my bank had on 3 occasions given me incorrect information about my debit card and was complaining to them and given a tenner but then got FO back involved who wrote a letter to bank and they decided to give me further compensation for the confusing information they had provided me. I was delighted with them as they listened to me for ages and helped me to try to tackle the complaints I had and my aim was never for extra money I started out complaining out of principle and just wanted to give up at times as it was too stressful and time consuming, but the FO seemed to do what I just wasn't able to do myself and much beyond what I had initially seeked and wished for.

I had a financial based company take money out my account without my consent or permission and they only offered me 50% refund for this membership fee. I complained and continued for weeks complaining without any email responses and got advice and support from the Ombudsman and after some communication I had with rogue company the FO contacted them and although the company was unwilling to resolve my issue with me they got the full refund plus some compensation as it took 7 weeks and some stress to get a full refund. At the same time my bank had on 3 occasions given me incorrect information about my debit card and was complaining to them and given a tenner but then got FO back involved who wrote a letter to bank and they decided to give me further compensation for the confusing information they had provided me. I was delighted with them as they listened to me for ages and helped me to try to tackle the complaints I had and my aim was never for extra money I started out complaining out of principle and just wanted to give up at times as it was too stressful and time consuming, but the FO seemed to do what I just wasn't able to do myself and much beyond what I had initially seeked and wished for. -

I was made bankrupt in 2008 & am cleaning up my credit file - there are a number of CCJs which do not show as satisfied despite the subject of the CCJ being satisfied on my credit agreements file - can I get the court to mark them as satisfied by my bankruptcy?

-

I apologise in advance if this is posted in the wrong section, or the info i need is posted elsewhere on the forum. Details are as follows: I had a loan to be paid back over 12 months. I made the first payment on time. Before the second payment was due, i recieved a notice of acceleration, quoting the previous issuing of a notice of default (which was definitely not received, and there would be no reason to issue) Because of the notice of acceleration, i suspected my bank account was about to be raided to recover the balance outstanding, so i wrote to my bank and the lender, to cancel my CPA. I also took the precaution to cancel my debit card and get a replacement. I complained to the lender to ask why my account was defaulted while i was up to date with payments and i was in compliance with all the terms of my loan. They could not give me any sort of answer to explain this, and in the 12 months or so since then, i have had no correspondence whatsoever. I have registered with Noddle recently to check my credit file and noticed the loan is shown under the closed account section, and is shown as having a default date, but the loan is marked as satisfied. My question, if anyone can help, is why would they mark the loan as satisfied and closed? I suspect the loan has been sold on, but my experience of this is pretty much zero so i really have no clue what this all means. I have been placing the loan repayment funds to one side, in case they or a DCA raise their head and request payment.

I apologise in advance if this is posted in the wrong section, or the info i need is posted elsewhere on the forum. Details are as follows: I had a loan to be paid back over 12 months. I made the first payment on time. Before the second payment was due, i recieved a notice of acceleration, quoting the previous issuing of a notice of default (which was definitely not received, and there would be no reason to issue) Because of the notice of acceleration, i suspected my bank account was about to be raided to recover the balance outstanding, so i wrote to my bank and the lender, to cancel my CPA. I also took the precaution to cancel my debit card and get a replacement. I complained to the lender to ask why my account was defaulted while i was up to date with payments and i was in compliance with all the terms of my loan. They could not give me any sort of answer to explain this, and in the 12 months or so since then, i have had no correspondence whatsoever. I have registered with Noddle recently to check my credit file and noticed the loan is shown under the closed account section, and is shown as having a default date, but the loan is marked as satisfied. My question, if anyone can help, is why would they mark the loan as satisfied and closed? I suspect the loan has been sold on, but my experience of this is pretty much zero so i really have no clue what this all means. I have been placing the loan repayment funds to one side, in case they or a DCA raise their head and request payment. -

Hello all, Has anyone encountered this before? I have an CCJ that was satisfied over 2 yearsago, yet showing on my credit reports as unsatisfied. Due to an previous issueregarding this judgement, I contacted HM Courts and Tribunal Service to getthis rectified over two months ago, and have had no response from them. I also have contacted the credit reference agencies, one of them hascorrected this while the other has informed, that the Registry Trust has saidthat the CCJ isn’t satisfied and that I have to contact the local court. I havecontacted the local court who have admitted that the CCJ is satisfied, but isat a loss as to why the Registry Trust wasn’t informed, as this is an automaticprocess. The local court will contact the Registry Trust to correct this. I am rather annoyed as I have had an job offer withdrawn because of thiserror. Any advice, would be most appreciated.

-

MBNA recently transferred my credit card debt to Idem Servicing without notice, (yes I do understand this can be done, & I do understand that under the 1926 act the full notional balance is transferred regardless of what Idem Servicing paid for it). Not wishing to be in the clutches of a DCA I decided to make a settlement offer of some 55% of the notional balance and about twice what Idem paid for it, working on the basis of the max they would have paid 30% for a debt situation that is now nearly six years old). Despite several tries at written dialogue all I have received in return is a standard letter stating no offer will be accepted until I complete a full financal statement, and boy is this full, it ask what I would consider to be the normal questions, plus items like what do you spend on petfood, sweets, footware etc.! They also want to know why the offer is being made, amount being offered, (already stated), and the source of the offer funds. Also the reference now used is not the cc number but their own, which they describe as a 'loan account'. In the past, I have made offers to creditors of full and final settlements and after negotiation have had them agreed at around this rate (50 - 60%) of the orginal debt amount, without resorting to disclosing so much (any) information. I could understand completing this form if negotiating a monthly payment figure but this is not the case. I should also add the amount I have been paying monthly amounts to more than I would be paying in terms of a minimum payment if the credit card was active. The question I have is would you consider this to be normal practise, or are they 'fishing' to leverage up my monthly payment? Any other suggestions gratefully received as well. As a bit of background IDEM recently accquired two tranches of cc debt from MBNA one at 55 million, the other at 11.8 million. They are part of the Paragon group who are a mortgage and loans company, although if you look at the groups balance sheet you will see the DCA arm (IDEM) contributed 27% of their last group profits, their investment partners (i.e. they have put up a proportion of the money) for debt accquisition are Carval Investors, and Arrow Global, technically this is called a 'shared upside purchase'.

MBNA recently transferred my credit card debt to Idem Servicing without notice, (yes I do understand this can be done, & I do understand that under the 1926 act the full notional balance is transferred regardless of what Idem Servicing paid for it). Not wishing to be in the clutches of a DCA I decided to make a settlement offer of some 55% of the notional balance and about twice what Idem paid for it, working on the basis of the max they would have paid 30% for a debt situation that is now nearly six years old). Despite several tries at written dialogue all I have received in return is a standard letter stating no offer will be accepted until I complete a full financal statement, and boy is this full, it ask what I would consider to be the normal questions, plus items like what do you spend on petfood, sweets, footware etc.! They also want to know why the offer is being made, amount being offered, (already stated), and the source of the offer funds. Also the reference now used is not the cc number but their own, which they describe as a 'loan account'. In the past, I have made offers to creditors of full and final settlements and after negotiation have had them agreed at around this rate (50 - 60%) of the orginal debt amount, without resorting to disclosing so much (any) information. I could understand completing this form if negotiating a monthly payment figure but this is not the case. I should also add the amount I have been paying monthly amounts to more than I would be paying in terms of a minimum payment if the credit card was active. The question I have is would you consider this to be normal practise, or are they 'fishing' to leverage up my monthly payment? Any other suggestions gratefully received as well. As a bit of background IDEM recently accquired two tranches of cc debt from MBNA one at 55 million, the other at 11.8 million. They are part of the Paragon group who are a mortgage and loans company, although if you look at the groups balance sheet you will see the DCA arm (IDEM) contributed 27% of their last group profits, their investment partners (i.e. they have put up a proportion of the money) for debt accquisition are Carval Investors, and Arrow Global, technically this is called a 'shared upside purchase'. -

Hello All, I was wondering if someone could help me. I have a number of Defaults on my file of which are now satisfied. I understand that these can possibly be removed by the company involved but they usually would not do this or would charge a fee. I was wondering if anyone may have a template of a letter I could send the companies concerned. Also if someone could possibly tell me the legal aspects surrounding satisfied defaults and removal. I understand that they are supposed to stay on my file for 6 years. However when I have paid off some of my debts the company have removed the default and marked as satisfied. I am a little confused! Thanks in advance! S

-

Hi, I'm wondering if someone can advise as to what will happen after I was sent a certificate of satisfaction with regards to a CCJ. Some numpty added a nought to a payment I sent and they sent the cert as the computer said the debt was overpaid. I've been to the court with the certificate and the CCJ is now satisfied; the bank I owe the money to has since sent a letter I have to sign to say I still owe the money etc....what should I do? and if I don't sign what will THEY do? Thanks in advance for any advice. Mac

-

Hello All, Why do CRAs use terms like. a) Satisfied b) Settled What is the difference? All information/advice will as usual be gratefully received. "EXEMPLO DUCEMUS"

-

Hello I have 2 x Satisfied defaults on my credit file registered 2010 settled 2012 both are marked as satisfied. They have the wrong date of birth on them( just one day out). They were accounts taken out in my name by my ex wife. I do not want to go down the fraud route but the accounts were not opened by me have incorrect information. After i got divorced i noticed all the debt I had been left in due to my ex hiding bills and not paying stuff etc.. . I have asked the company JD Williams to remove these defaults and explained the situation they will not remove them. These are the last 2 items of adverse i need to remove before I apply for a mortgage I have now gone down the route of if they are my defaults where is the credit agreement and I have sent the necessary letter requesting copies of the original agreements. If as I suspect they cannot provide these documents can I ask them to remove the defaults? without a credit agreement how can there be a default. Also worth noting I settled the defaults earlier this year thinking I was doing the right thing. Any advice? Thanks

Hello I have 2 x Satisfied defaults on my credit file registered 2010 settled 2012 both are marked as satisfied. They have the wrong date of birth on them( just one day out). They were accounts taken out in my name by my ex wife. I do not want to go down the fraud route but the accounts were not opened by me have incorrect information. After i got divorced i noticed all the debt I had been left in due to my ex hiding bills and not paying stuff etc.. . I have asked the company JD Williams to remove these defaults and explained the situation they will not remove them. These are the last 2 items of adverse i need to remove before I apply for a mortgage I have now gone down the route of if they are my defaults where is the credit agreement and I have sent the necessary letter requesting copies of the original agreements. If as I suspect they cannot provide these documents can I ask them to remove the defaults? without a credit agreement how can there be a default. Also worth noting I settled the defaults earlier this year thinking I was doing the right thing. Any advice? Thanks -

Thinking about my debts,as I do constantly, I'm wondering if there would be any point in me trying to get a satisfied CCJ set aside on the basis that it was applied for in 2009 by which time I had been a resident of Spain for six years. The debt was one of many that my husband ran up unbeknown to me. I only found out about some of these when I managed to get a credit report earlier this year. The CCJ was showing on my file. It had already been settled by my husband and showed as settled on his file, but not on mine. He then wrote to the court and on an application to the trust online this week, I can now see that it shows as settled. However it is going to be on my file for another five years and I would like it removed if possible. If I did ask for it to be set aside, would this alert any debt collectors to my whereabouts? We also have two joint, defaulted debts with First Direct (now sold to Mkd Llp) which I had no knowledge of. I don't wish to contest these as they will hopefully become statute barred in two years, but again I had no contact about the debts despite First Direct knowing I had moved to Spain years earlier. At the time my husband had a UK address and I'm guessing that all correspondence went there. However First Direct knew I was living here and had previously telephoned me here on my Spanish land-line which they had, although never about the accounts being in arrears. Surely they should have contacted me before issuing defaults?

-

Hello, I'll try and make this short, sweet and to the point. In 2007 I went a few pence overdrawn with the nationwide. this amount grew with £30 charges being added every month. I spoke with Nationwide and came to an agreement to pay xx amount monthly, which I honoured. I then receive a letter from a debt collection company stating that I owe £154 (this included their charges). I phoned Nationwide and obviously wondered why this had been passed to a debt collectors when I was paying this monthly. Nationwide said that is was because I didn;t pay the interest associated with the debt/charges which i disagreed with as this had not been pointed out to me when I had made these monthy arrangments. They dismissd that claim and stated that it would had been discussed. So they slap a default on my credit file, I pay the £154 to the debt collectors (through gritted teeth) and the default has been classed as satisfied on my credit file. My question is do i have a case to get this satisfied defaut removed from my file and how would I go about doing this. Many Thanks Johnny

-

... Is there a difference on a credit file and if so, what is the difference and how detrimental is it to your credit score?