Search the Community

Showing results for tags 'affected'.

Found 24 results

-

Grenfell Tower fire: support for people affected READ MORE HERE: https://www.gov.uk/guidance/grenfell-tower-fire-june-2017-support-for-people-affected

Grenfell Tower fire: support for people affected READ MORE HERE: https://www.gov.uk/guidance/grenfell-tower-fire-june-2017-support-for-people-affected -

Health advice for residents affected by Saddleworth Moor fire READ MORE HERE: https://www.gov.uk/government/news/health-advice-for-residents-affected-by-saddleworth-moor-fire

-

Help for nursing students affected by loan overpayments READ MORE HERE: https://www.gov.uk/government/news/help-for-nursing-students-affected-by-loan-overpayments

-

A strain of influenza which hit Australia and affected 98,000 people, is set to come to Britain and could case our worst epidemic for fifty years. Will it or wont it.I am taking no chances how about you. The vulnerable groups include the over-65s, pregnant women, children from six to 24 months and those with long-term *illness such as *diabetes, heart disease and asthma. https://www.unilad.co.uk/health/deadly-flu-outbreak-in-uk-expected-to-kill-thousands/ Well i have not much time this morning to hang around. I am nipping off sharpish to the vets to have my Flu Injection. Adios must fly. Tawnyowl.

A strain of influenza which hit Australia and affected 98,000 people, is set to come to Britain and could case our worst epidemic for fifty years. Will it or wont it.I am taking no chances how about you. The vulnerable groups include the over-65s, pregnant women, children from six to 24 months and those with long-term *illness such as *diabetes, heart disease and asthma. https://www.unilad.co.uk/health/deadly-flu-outbreak-in-uk-expected-to-kill-thousands/ Well i have not much time this morning to hang around. I am nipping off sharpish to the vets to have my Flu Injection. Adios must fly. Tawnyowl. -

READ MORE HERE: https://www.gov.uk/government/publications/support-within-the-royal-air-force-community-for-those-affected-by-domestic-abuse

-

I bought a diesel Volkswagen Passat estate car around a year ago from a local car dealership. While my wife and I were out for a test drive, I made sure to ask the salesman if the car had been affected by the VW emissions scandal. The salesman told us that it was not as they had checked. However, I recently received a letter from Volkswagen stating that my car was indeed affected. We would not have bought the car had we known that it was affected. What are my rights in terms of the dealership? I have no written or recorded record of the conversation, but my wife and I were both present when he made the statement.

I bought a diesel Volkswagen Passat estate car around a year ago from a local car dealership. While my wife and I were out for a test drive, I made sure to ask the salesman if the car had been affected by the VW emissions scandal. The salesman told us that it was not as they had checked. However, I recently received a letter from Volkswagen stating that my car was indeed affected. We would not have bought the car had we known that it was affected. What are my rights in terms of the dealership? I have no written or recorded record of the conversation, but my wife and I were both present when he made the statement. -

Yahoo has said more than one billion user accounts may have been affected in a hacking attack dating back to 2013. The internet giant said it appeared separate from a 2014 breach disclosed in September, when Yahoo revealed 500 million accounts had been accessed. Yahoo said names, phone numbers, passwords and email addresses were stolen, but not bank and payment data. You should immediately change your password and security questions and answers. You should do this not just for your Yahoo account but also for any other accounts you have which may have used the same or similar info http://www.bbc.co.uk/news/world-us-canada-38324527 http://www.bbc.co.uk/news/technology-38327169

Yahoo has said more than one billion user accounts may have been affected in a hacking attack dating back to 2013. The internet giant said it appeared separate from a 2014 breach disclosed in September, when Yahoo revealed 500 million accounts had been accessed. Yahoo said names, phone numbers, passwords and email addresses were stolen, but not bank and payment data. You should immediately change your password and security questions and answers. You should do this not just for your Yahoo account but also for any other accounts you have which may have used the same or similar info http://www.bbc.co.uk/news/world-us-canada-38324527 http://www.bbc.co.uk/news/technology-38327169 -

https://www.theguardian.com/business/2016/nov/07/tesco-bank-freezes-transactions-online-attack As long as their money has not been stolen !

-

Hello all, I just joined this forum and I'm looking for advice on an issue where I really feel hard done by. Let me explain. Back in September 2014 my ex wanted a phone. We were out and at Carphone Warehouse she said she wanted a phone. However, at the time she didn't have her bank card with her, because the old one had expired and she was waiting for a replacement to come. Me being the gent I am decided to take out a contract in my name and gave my direct debit details. It wasa Vodafone contract. The man at the shop said that after 3 months, we can call Vodaphone and do a 1) transfer of direct debit and 2) transfer of account ownership. I said okay. Sadly the relationship ended pretty soon after that but for the first three month the direct debit was coming out of my account and she was putting money in my account. After three months there was a forced meeting where we called Vodafone at the same time and requested a complete transfer. Both direct debit and account were transferred from mine into her name (or so I thought). Fast forward to September 2016 and I got rejected for a mortage by a lender. I was a little baffled as to why so I logged onto creditscore and to my shock, it shows the Vodafone account from 2014 more than £800 in arrears. I called up Vodafone. I was angry. The account should never have been in my name. They told me that at time of transfer of account ownership they did a credit check on my ex and she failed it. So, the account bouced back to me. I was shocked. I was never told about this at all. As it turns out, my ex then cancelled the direct debit and didn't make any more payments. Problem is that account was in my name and I didn't even know. I wasn't called, e-mailed, written to. I thought after three months that account was no longer in my name. I wasn't using the phone, my ex was. The problem now is that my credit history shows major telecom arrears which I feel is really unfair. I disputed it and Vodafone told equifax that the account remained in my names so the credit history is correct. I'm livid because I feel this is not an accurate reflection of my payment history. I am struggling to buy a house now. Can you help?

-

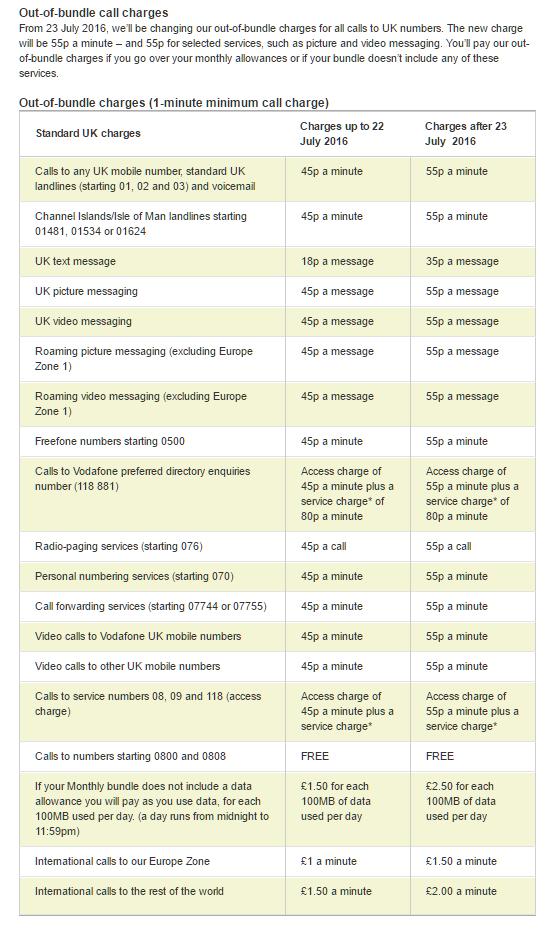

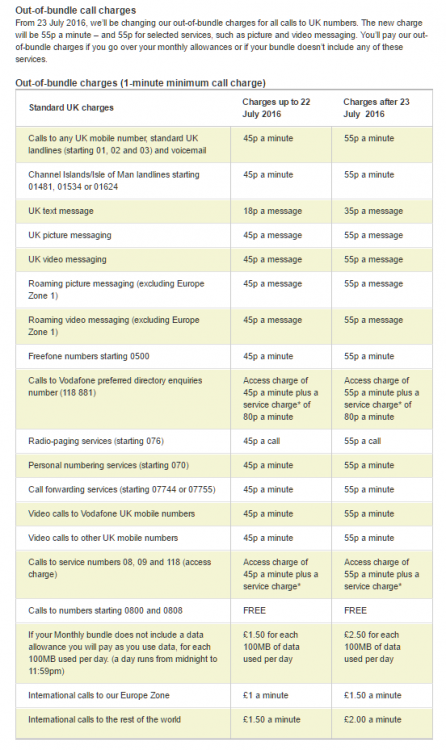

.thumb.jpg.bf2f59e5260173230834ce3ad8015900.jpg) Ladies & Gents, Yet another reason why any Vodafone Customers must think about if Voda is the right choice for them. New Charges are listed below at this link;

Ladies & Gents, Yet another reason why any Vodafone Customers must think about if Voda is the right choice for them. New Charges are listed below at this link;

-

Hi, I'm looking for general advice and a heads up on what the outcome might be of my issues with nPower, based on the experience of people who know better! I've lived in my current (rented) property for almost 4 years in that time I've lived with 5 different flatmates; flatmate A from August 2013 to March 2014; flatmate B from March 2014 to September 2014; flatmate C from September 2014 to March 2015; flatmate D from March 2015 to February 2016 and flatmate E has been with me since February (2016). The gas/electric bills have always been in my flatmate's name and we'd been with nPower for both gas and electricity up 'til March 2015 when we tried to switch. The electricity switch went fine, but we were told that nPower were objecting to the gas account move. I phoned nPower and asked what was going on, knowing that flatmate D had submitted a final meter reading before moving out. nPower told me that they did not supply gas to the property and could not find any gas account linked to my address. They recommended I phoned the National Grid to find out who was supplying me, which I did and they too said it seemed that nobody was supplying me (which was odd because I was getting gas). I checked again with nPower who insisted it was not them and was unable to make any progress. We received no gas bills up until October 2015, when I received 13 months' worth of estimated gas bills from nPower, totalling more than £500, along with a letter 'welcoming' me to nPower. This was all in my name, for the first time, when I logged into the account online, there was a new account for me, as well as the old account which would have been in flatmate D's name both attributed to me. I made an initial payment of £155.32, knowing that we were liable for some of the money and set about speaking to nPower to clarify what was going on and to get accurate bills. Within a month of this, nPower has passed my details on Richburns debt collection agency who sent me a letter stating their intention to seek a warrant to enter my property. At this stage, I'd logged an official complaint to nPower and understood that my account was on hold and as such, the collections process should have been paused. I sent Richburns a letter stating this and highlighting the customer service and billing issues it was well publicised that nPower were guilty of, they replied to tell me that they'd passed the matter back to nPower. Following this, I received a letter from nPower again threatening to seek a warrant and also to place a default on my credit record. At this point (25/01/16) I phoned the customer service team who assured me there was a hold on the account and no further bills would be issued until we understood what was going on and that the threats would not be carried out as there was a complaint logged. After this I received a bill and I made a second phone call, seeking an update (01/02/16), where I was told that there was indeed a hold (until 31/05/16) and the bill shouldn't have been issued, as the matter had been passed to the 'specialist' billing team who could generate an accurate bill. I was told that everything would be investigated and I'd receive an email to confirm everything, and to disregard the bill. No such email materialised and the bill wasn't reversed, as promised. I heard nothing and chased with another phone call on 05/02/16 when I was told that the complaint had been closed on 25/01/16. At this point I discovered nPower had raised 3 different complaint numbers and muddled everything up - the one complaint was closed , that all issues were all consolidated into one. After being given the correct complaint number, I was asked why I was disputing the bill. Prior to this call I'd done some reading and come across the backbilling policy that nPower were signed up to and knew that some of the bill should not have been chased I raised this, and explained that I was seeking an accurate bill as opposed to ridiculous estimates (we had given a meter reading to bring everything up to date 02/02/16). The guy on the phone said as far as he could see, I'd been contacted to say everything had been investigated. This had not happened; no letter, no emails, no missed calls. He went on to say there was an accurate bill which had been recently generated, which I logged into my online account and saw, but I'd had no email to alert me to it before this phone call. At this point the bill had ballooned to £625 with costs from debt collection visits and calls. I again raised the fact that it was not accurate as they needed to remove the 'backbilled' amount and he said they'd investigate to write off that one month. I told him that I wanted to go away and check that this latest bill was indeed accurate, given that I'd only just seen it and that I wanted the charges removed because they should never have passed the account to collections, which he did actually do after the call; crediting that £57.50 to the account. He said he'd get the backbilling team to investigate the outstanding amount and come back to me with an up-to-date bill. During this phone call I said I'd be seeking compensation given their failing to bill me for over a yea r and then seeking 13 months' of bills in one go, as well as their abysmal customer service given that Id had to do so much chasing and been kept so misinformed. The guy said he'd note that I was seeking compensation but warned that I couldn't claim for phone calls/time; just the backbilling and the customer service. He asked if I had an amount in mind and I said I'd wait to see what they offered. I heard nothing from nPower for the next two weeks and having given the compensation some real thought, I sent an email to nPower informing them that I was seeking £400 compensation. The email was as follows: To whom it may concern, On Friday 5th February, having spent 40 minutes on hold, I spent 20 minutes speaking to Sam, one of you customer service advisors, seeking an update on billing issues with my gas account (ref. XYZ). Sam assured me that he'd add a 'miscellaneous credit' to my account to reimburse me for fees relating to debt collection agencies - who should never have been approached. This has now happened. He also said he'd pass my account onto the back-billing team to remove a bill from September 2014, which was only actually billed in October 2015, and that I'd receive a new bill taking this into account. I am still awaiting any update on this, some 15 days later. I also made Sam aware that I would be seeking compensation for the total lack of customer service I'd received and for the fact that I'd been billed 13 months' worth of bills in October 2015, having received nothing for over a year and despite me trying to make payments. Sam asked if I had a figure in mind and I said I would wait to hear from you. Having heard nothing, and having spent time over the past two weeks reflecting on the impact of this saga on me, I am now writing to inform you that I seek £400 total in compensation, for the reasons outlined below. I expect a prompt response outlining what is going on with my account and when and how I should expect to receive compensation from you. Yours faithfully, MY NAME 1. Billing delays Your website states: We will provide compensation to any customer who we incorrectly back billed from July 2010 to 31st December 2015, to a value not less than £100 per customer We will provide compensation to any customer currently affected by late invoice for 12 months or more as at 31st December 2015, to a value not less than £100 per customer I received 13 months' of bills (from September 2014 to October 2015) and an immediate demand for payment in October 2015 having received no bills, and even being told Npower didn't supply my gas, throughout that period. Given that I meet both your criteria for redress, I am seeking compensation from Npower for billing delays. TOTAL SOUGHT FOR BILLING DELAYS: £100 2. General customer service My issue was not resolved within 10 working days as per your complaints policy [here I included a link to their complaints policy page] to-date it has actually taken more than 90 days since first contact and I have not been informed of progress throughout; rather I’ve sent 2 letters, countless emails and made 3 phone calls (spending more than an hour on hold) to chase updates and unfulfilled promises Such chaos has there been around my account, that even when I've tried to make payments in the past year, I was told I was not on your system and had no gas account with you; I was not receiving bills and it was impossible to make any payment given there being no account according to your team You state [here I included a link to their page which details what they're doing as of the latest December 2015 issue] We will identify and repay any customer who we incorrectly back billed from July 2010 to 31st December 2015 and yet I had to point this issue out to you; you did not identify any issues with my account until I raised the back-bill in my phone call with Sam on 05/02/2016 - in fact you were still seeking payment for the out-of-date bill at that point, contravening the Energy UK guidelines which you signed up to You raised multiple complaints (X, Y and Z) and made no contact to let me know anything had been resolved (even if it your ‘resolution’ was just consolidating two complaints into one), leading to total confusion and delaying communication with customer services about my issues A pitiful level of care and attention has been given to my communications as is evident in your reply dated 20/01/2016 , when the copying and pasting of my email was blatant (you failed to replace ‘my’ with ‘your’) and you mis-spelled basic information such as the address [i copied and highlighted the errors here] All of the above suggests my issues have been handled with nowhere near the level of care and importance they should have been, especially given your repeated promises to the Ombudsman that you will handle and resolve complaints more effectively. TOTAL SOUGHT FOR ABYSMAL CUSTOMER SERVICE: £150 3. Inconvenience and stress Such was the stress of this episode, and particularly the threat of entry to my property from Richburns (acting on Npower’s behalf) to seek a disputed debt, I spent several months taking high value items including a MacBook computer and family heirlooms including jewellery to work everyday to avoid them being taken away in my absence I have experienced serious anxiety, triggering asthma which I have not suffered from since childhood, which has massively impacted by wellbeing and quality of day-to-day life TOTAL SOUGHT FOR INCONVENIENCE AND STRESS: £50 4. Failure to uphold the Data Protection Act and unnecessarily passing my details into Richburns Debt Collection agency The Data Protection Act of 1998 states that: Personal data shall be accurate and, where necessary, kept up to date In passing inaccurate data on me on to Richburns and wrongly seeking payment for a disputed debt, I believe you contravened this act and risked damage to my reputation I am aware that following intervention by The Guardian's Consumer Champions, [here I inserted a link to a Guardian Consumer Champion's article] you previously awarded £100 in compensation to a customer who wrongfully received a visit from a debt collection agency acting on your instruction and I expect the same in this instance TOTAL SOUGHT FOR MISHANDLING OF DATA: £100 TOTAL SOUGHT FOR ALL OF THE ABOVE: £400. The week after this, I logged into my online account and saw lots of 'transfers' and 'reversed bills' applied, making my balance £0. I submitted a meter reading and it became approx. £19. As expected, nPower failed to reply to my email within the 7 working days they state they will. I received a voicemail from a different customer service team member on 01/03/16 asking me to call back, which I did today, speaking to someone who had no idea what was going on. He informed me that the backbilling team had sent the query back to them because they weren't sure which account the questions were around; but I only have one (gas) account with nPower! He agreed this was odd but explained that they wanted to just credit the account with £60 to save the backbilling team investigating, but hadn't done so yet because of the 'goodwill gesture' of £400 that I was seeking. He explained he could do the £60 reversal for the backbilling and give me a goodwill gesture of £30, to which my response was 'Are you joking?!'. He claimed it was a reasonable amount. I told him that the nPower website states that in response to the latest (December 2015) issues with the Ombudsman, any customer still affected by backbilling would receive no less than £100 in compensation, and he told me he wasn't aware of it but could offer £40 to make it £100. I told him this would not do, because the backbilling is seperate to the compensation; as I understand it they CANNOT charge me for that month that they billed me for some 13 months later. Any compensation I seek should be seperate to this. I also highlighted the issues I'd experienced (he hadn't read the LONG email i sent) and explained why I was seeking £400; it not being some random amount I'd plucked out of thin air. He said he'd log that I wouldn't accept the £40 and that now the matter would be passed on to Stage 2 for the complaint to be reviewed and I stressed that they need to look at my email again. As I understand it, the bill is going back to the backilling team to figure out what needs to be written off and I have to wait to hear regarding my complaint. I also asked him why my account went back to £0 and he said it was because they'd credited payments from old accounts to the new account so it was up to date. I presume he refers to payments flatmate C and/or D made before they stopped billing us. Is it not ridiculous that they've just figured out we might not even owe them anything!? I'm still not clear whether we do or don't, because billing is still on hold given the lock from the complaint. I'm utterly exhausted with all this. All I want is some fair compensation, and the mess to be resolved so that I can switch suppliers. As I understand it, there's every chance that Stage 2 will involve another laughable offer and then it'll likely go to deadlock and I'll need to complain to the Ombudsman. I guess I'm looking for advice - have I done everything I need to? What else can I do at this point? Also should I expect to have to go to the Ombudsman? Any help very much appreciated. Thank you!

Hi, I'm looking for general advice and a heads up on what the outcome might be of my issues with nPower, based on the experience of people who know better! I've lived in my current (rented) property for almost 4 years in that time I've lived with 5 different flatmates; flatmate A from August 2013 to March 2014; flatmate B from March 2014 to September 2014; flatmate C from September 2014 to March 2015; flatmate D from March 2015 to February 2016 and flatmate E has been with me since February (2016). The gas/electric bills have always been in my flatmate's name and we'd been with nPower for both gas and electricity up 'til March 2015 when we tried to switch. The electricity switch went fine, but we were told that nPower were objecting to the gas account move. I phoned nPower and asked what was going on, knowing that flatmate D had submitted a final meter reading before moving out. nPower told me that they did not supply gas to the property and could not find any gas account linked to my address. They recommended I phoned the National Grid to find out who was supplying me, which I did and they too said it seemed that nobody was supplying me (which was odd because I was getting gas). I checked again with nPower who insisted it was not them and was unable to make any progress. We received no gas bills up until October 2015, when I received 13 months' worth of estimated gas bills from nPower, totalling more than £500, along with a letter 'welcoming' me to nPower. This was all in my name, for the first time, when I logged into the account online, there was a new account for me, as well as the old account which would have been in flatmate D's name both attributed to me. I made an initial payment of £155.32, knowing that we were liable for some of the money and set about speaking to nPower to clarify what was going on and to get accurate bills. Within a month of this, nPower has passed my details on Richburns debt collection agency who sent me a letter stating their intention to seek a warrant to enter my property. At this stage, I'd logged an official complaint to nPower and understood that my account was on hold and as such, the collections process should have been paused. I sent Richburns a letter stating this and highlighting the customer service and billing issues it was well publicised that nPower were guilty of, they replied to tell me that they'd passed the matter back to nPower. Following this, I received a letter from nPower again threatening to seek a warrant and also to place a default on my credit record. At this point (25/01/16) I phoned the customer service team who assured me there was a hold on the account and no further bills would be issued until we understood what was going on and that the threats would not be carried out as there was a complaint logged. After this I received a bill and I made a second phone call, seeking an update (01/02/16), where I was told that there was indeed a hold (until 31/05/16) and the bill shouldn't have been issued, as the matter had been passed to the 'specialist' billing team who could generate an accurate bill. I was told that everything would be investigated and I'd receive an email to confirm everything, and to disregard the bill. No such email materialised and the bill wasn't reversed, as promised. I heard nothing and chased with another phone call on 05/02/16 when I was told that the complaint had been closed on 25/01/16. At this point I discovered nPower had raised 3 different complaint numbers and muddled everything up - the one complaint was closed , that all issues were all consolidated into one. After being given the correct complaint number, I was asked why I was disputing the bill. Prior to this call I'd done some reading and come across the backbilling policy that nPower were signed up to and knew that some of the bill should not have been chased I raised this, and explained that I was seeking an accurate bill as opposed to ridiculous estimates (we had given a meter reading to bring everything up to date 02/02/16). The guy on the phone said as far as he could see, I'd been contacted to say everything had been investigated. This had not happened; no letter, no emails, no missed calls. He went on to say there was an accurate bill which had been recently generated, which I logged into my online account and saw, but I'd had no email to alert me to it before this phone call. At this point the bill had ballooned to £625 with costs from debt collection visits and calls. I again raised the fact that it was not accurate as they needed to remove the 'backbilled' amount and he said they'd investigate to write off that one month. I told him that I wanted to go away and check that this latest bill was indeed accurate, given that I'd only just seen it and that I wanted the charges removed because they should never have passed the account to collections, which he did actually do after the call; crediting that £57.50 to the account. He said he'd get the backbilling team to investigate the outstanding amount and come back to me with an up-to-date bill. During this phone call I said I'd be seeking compensation given their failing to bill me for over a yea r and then seeking 13 months' of bills in one go, as well as their abysmal customer service given that Id had to do so much chasing and been kept so misinformed. The guy said he'd note that I was seeking compensation but warned that I couldn't claim for phone calls/time; just the backbilling and the customer service. He asked if I had an amount in mind and I said I'd wait to see what they offered. I heard nothing from nPower for the next two weeks and having given the compensation some real thought, I sent an email to nPower informing them that I was seeking £400 compensation. The email was as follows: To whom it may concern, On Friday 5th February, having spent 40 minutes on hold, I spent 20 minutes speaking to Sam, one of you customer service advisors, seeking an update on billing issues with my gas account (ref. XYZ). Sam assured me that he'd add a 'miscellaneous credit' to my account to reimburse me for fees relating to debt collection agencies - who should never have been approached. This has now happened. He also said he'd pass my account onto the back-billing team to remove a bill from September 2014, which was only actually billed in October 2015, and that I'd receive a new bill taking this into account. I am still awaiting any update on this, some 15 days later. I also made Sam aware that I would be seeking compensation for the total lack of customer service I'd received and for the fact that I'd been billed 13 months' worth of bills in October 2015, having received nothing for over a year and despite me trying to make payments. Sam asked if I had a figure in mind and I said I would wait to hear from you. Having heard nothing, and having spent time over the past two weeks reflecting on the impact of this saga on me, I am now writing to inform you that I seek £400 total in compensation, for the reasons outlined below. I expect a prompt response outlining what is going on with my account and when and how I should expect to receive compensation from you. Yours faithfully, MY NAME 1. Billing delays Your website states: We will provide compensation to any customer who we incorrectly back billed from July 2010 to 31st December 2015, to a value not less than £100 per customer We will provide compensation to any customer currently affected by late invoice for 12 months or more as at 31st December 2015, to a value not less than £100 per customer I received 13 months' of bills (from September 2014 to October 2015) and an immediate demand for payment in October 2015 having received no bills, and even being told Npower didn't supply my gas, throughout that period. Given that I meet both your criteria for redress, I am seeking compensation from Npower for billing delays. TOTAL SOUGHT FOR BILLING DELAYS: £100 2. General customer service My issue was not resolved within 10 working days as per your complaints policy [here I included a link to their complaints policy page] to-date it has actually taken more than 90 days since first contact and I have not been informed of progress throughout; rather I’ve sent 2 letters, countless emails and made 3 phone calls (spending more than an hour on hold) to chase updates and unfulfilled promises Such chaos has there been around my account, that even when I've tried to make payments in the past year, I was told I was not on your system and had no gas account with you; I was not receiving bills and it was impossible to make any payment given there being no account according to your team You state [here I included a link to their page which details what they're doing as of the latest December 2015 issue] We will identify and repay any customer who we incorrectly back billed from July 2010 to 31st December 2015 and yet I had to point this issue out to you; you did not identify any issues with my account until I raised the back-bill in my phone call with Sam on 05/02/2016 - in fact you were still seeking payment for the out-of-date bill at that point, contravening the Energy UK guidelines which you signed up to You raised multiple complaints (X, Y and Z) and made no contact to let me know anything had been resolved (even if it your ‘resolution’ was just consolidating two complaints into one), leading to total confusion and delaying communication with customer services about my issues A pitiful level of care and attention has been given to my communications as is evident in your reply dated 20/01/2016 , when the copying and pasting of my email was blatant (you failed to replace ‘my’ with ‘your’) and you mis-spelled basic information such as the address [i copied and highlighted the errors here] All of the above suggests my issues have been handled with nowhere near the level of care and importance they should have been, especially given your repeated promises to the Ombudsman that you will handle and resolve complaints more effectively. TOTAL SOUGHT FOR ABYSMAL CUSTOMER SERVICE: £150 3. Inconvenience and stress Such was the stress of this episode, and particularly the threat of entry to my property from Richburns (acting on Npower’s behalf) to seek a disputed debt, I spent several months taking high value items including a MacBook computer and family heirlooms including jewellery to work everyday to avoid them being taken away in my absence I have experienced serious anxiety, triggering asthma which I have not suffered from since childhood, which has massively impacted by wellbeing and quality of day-to-day life TOTAL SOUGHT FOR INCONVENIENCE AND STRESS: £50 4. Failure to uphold the Data Protection Act and unnecessarily passing my details into Richburns Debt Collection agency The Data Protection Act of 1998 states that: Personal data shall be accurate and, where necessary, kept up to date In passing inaccurate data on me on to Richburns and wrongly seeking payment for a disputed debt, I believe you contravened this act and risked damage to my reputation I am aware that following intervention by The Guardian's Consumer Champions, [here I inserted a link to a Guardian Consumer Champion's article] you previously awarded £100 in compensation to a customer who wrongfully received a visit from a debt collection agency acting on your instruction and I expect the same in this instance TOTAL SOUGHT FOR MISHANDLING OF DATA: £100 TOTAL SOUGHT FOR ALL OF THE ABOVE: £400. The week after this, I logged into my online account and saw lots of 'transfers' and 'reversed bills' applied, making my balance £0. I submitted a meter reading and it became approx. £19. As expected, nPower failed to reply to my email within the 7 working days they state they will. I received a voicemail from a different customer service team member on 01/03/16 asking me to call back, which I did today, speaking to someone who had no idea what was going on. He informed me that the backbilling team had sent the query back to them because they weren't sure which account the questions were around; but I only have one (gas) account with nPower! He agreed this was odd but explained that they wanted to just credit the account with £60 to save the backbilling team investigating, but hadn't done so yet because of the 'goodwill gesture' of £400 that I was seeking. He explained he could do the £60 reversal for the backbilling and give me a goodwill gesture of £30, to which my response was 'Are you joking?!'. He claimed it was a reasonable amount. I told him that the nPower website states that in response to the latest (December 2015) issues with the Ombudsman, any customer still affected by backbilling would receive no less than £100 in compensation, and he told me he wasn't aware of it but could offer £40 to make it £100. I told him this would not do, because the backbilling is seperate to the compensation; as I understand it they CANNOT charge me for that month that they billed me for some 13 months later. Any compensation I seek should be seperate to this. I also highlighted the issues I'd experienced (he hadn't read the LONG email i sent) and explained why I was seeking £400; it not being some random amount I'd plucked out of thin air. He said he'd log that I wouldn't accept the £40 and that now the matter would be passed on to Stage 2 for the complaint to be reviewed and I stressed that they need to look at my email again. As I understand it, the bill is going back to the backilling team to figure out what needs to be written off and I have to wait to hear regarding my complaint. I also asked him why my account went back to £0 and he said it was because they'd credited payments from old accounts to the new account so it was up to date. I presume he refers to payments flatmate C and/or D made before they stopped billing us. Is it not ridiculous that they've just figured out we might not even owe them anything!? I'm still not clear whether we do or don't, because billing is still on hold given the lock from the complaint. I'm utterly exhausted with all this. All I want is some fair compensation, and the mess to be resolved so that I can switch suppliers. As I understand it, there's every chance that Stage 2 will involve another laughable offer and then it'll likely go to deadlock and I'll need to complain to the Ombudsman. I guess I'm looking for advice - have I done everything I need to? What else can I do at this point? Also should I expect to have to go to the Ombudsman? Any help very much appreciated. Thank you! -

Hi All I bought a new Audi A5 under a HP agreement in 2012, the final lumps sum payment is due in March 2016. I have just discovered my engine IS affected by the VW emissions cheat device. As I understand it, the finance company is liable as well as VW, will be quicker and easier to deal with the finance company than join a class action against VW Under the CCA 1974, can I claim against my HP finance company on the grounds that: 1. The vehicle was not as described (i.e. emissions etc. not as quoted) 2. the vehicle is not fit for purpose (emissions cheat device fitted (knowingly) and Mileage, emissions, fuel consumption not as quoted) Is there any template for this type of letter? Any advice would be most welcome as a £10K final payment is due soon, thanks John

Hi All I bought a new Audi A5 under a HP agreement in 2012, the final lumps sum payment is due in March 2016. I have just discovered my engine IS affected by the VW emissions cheat device. As I understand it, the finance company is liable as well as VW, will be quicker and easier to deal with the finance company than join a class action against VW Under the CCA 1974, can I claim against my HP finance company on the grounds that: 1. The vehicle was not as described (i.e. emissions etc. not as quoted) 2. the vehicle is not fit for purpose (emissions cheat device fitted (knowingly) and Mileage, emissions, fuel consumption not as quoted) Is there any template for this type of letter? Any advice would be most welcome as a £10K final payment is due soon, thanks John -

An interesting read today as follows "As a landlord, agent or solicitor, if you have used a High Court Enforcement Officer who did not follow the proper process, you could find that you’re liable for a significant claim for damages. In recent years, there has been a large increase in the use of High Court Enforcement Officers (HCEO) to evict residential tenants, which is no great surprise, as HCEOs can frequently enforce far more quickly than a County Court Bailiff (CCB) can. How could the eviction be illegal? At present, HCEOs can only use a standard writ of possession to evict trespassers, i.e. “persons unknown” such as squatters. For an HCEO to evict a tenant who remains in a property after a possession date, they MUST obtain permission from the County Court under Section 42 of the County Court Act 1984 to transfer enforcement of the order for possession to the High Court. Without this permission, any writ of possession enforced is invalid and any action taken under it will be illegal. Are illegal evictions taking place? In the last 18 months the High Court enforcement sector has seen a quantity of small ‘franchise’ bailiff firms, many operating under the authority of a single authorised High Court Enforcement Officer. Some of these firms are offering guaranteed seven day evictions of residential tenants, which does not allow time to obtain court permission to transfer up. It is our understanding that some of these firms may be applying for the writ of possession, without having previously obtained permission from the County Court to transfer up the order for possession to the High Court for enforcement, perhaps because they are not aware of this legal requirement. If any of these firms are evicting tenants under a writ of possession but without court permission to transfer up, then those evictions will have been conducted illegally. Exposure to claims for damages Whilst it is understandable that every landlord wants possession of their property without the lengthy delays regularly quoted by the County Court Bailiffs, the potential cost implications for a landlord for incorrectly evicting a tenant can be huge - claims for damages might come from both the tenants, as well as the local authority that had to rehouse them in emergency accommodation. As well as claiming for considerable damages from the landlord, the tenant may also make a claim against the bailiff company that evicted them and the authorised HCEO personally. If you think you may be affected If you have used the services of one of these ‘franchise’ HCEO firms, it would be prudent to now demand to see the court order allowing the HCEO to undertake the eviction. Be advised that this is NOT the writ of possession, but is a separate standard court order. If the HCEO cannot produce this, you could be looking at a claim for damages landing on your doormat any day soon. It would also be prudent to ask the HCEO company for details of their insurers." Story from Scoop today here http://www.scoop.it/t/lacef-news Info in full from here http://thesheriffsoffice.com/articles/are-you-evicting-tenants-illegally

An interesting read today as follows "As a landlord, agent or solicitor, if you have used a High Court Enforcement Officer who did not follow the proper process, you could find that you’re liable for a significant claim for damages. In recent years, there has been a large increase in the use of High Court Enforcement Officers (HCEO) to evict residential tenants, which is no great surprise, as HCEOs can frequently enforce far more quickly than a County Court Bailiff (CCB) can. How could the eviction be illegal? At present, HCEOs can only use a standard writ of possession to evict trespassers, i.e. “persons unknown” such as squatters. For an HCEO to evict a tenant who remains in a property after a possession date, they MUST obtain permission from the County Court under Section 42 of the County Court Act 1984 to transfer enforcement of the order for possession to the High Court. Without this permission, any writ of possession enforced is invalid and any action taken under it will be illegal. Are illegal evictions taking place? In the last 18 months the High Court enforcement sector has seen a quantity of small ‘franchise’ bailiff firms, many operating under the authority of a single authorised High Court Enforcement Officer. Some of these firms are offering guaranteed seven day evictions of residential tenants, which does not allow time to obtain court permission to transfer up. It is our understanding that some of these firms may be applying for the writ of possession, without having previously obtained permission from the County Court to transfer up the order for possession to the High Court for enforcement, perhaps because they are not aware of this legal requirement. If any of these firms are evicting tenants under a writ of possession but without court permission to transfer up, then those evictions will have been conducted illegally. Exposure to claims for damages Whilst it is understandable that every landlord wants possession of their property without the lengthy delays regularly quoted by the County Court Bailiffs, the potential cost implications for a landlord for incorrectly evicting a tenant can be huge - claims for damages might come from both the tenants, as well as the local authority that had to rehouse them in emergency accommodation. As well as claiming for considerable damages from the landlord, the tenant may also make a claim against the bailiff company that evicted them and the authorised HCEO personally. If you think you may be affected If you have used the services of one of these ‘franchise’ HCEO firms, it would be prudent to now demand to see the court order allowing the HCEO to undertake the eviction. Be advised that this is NOT the writ of possession, but is a separate standard court order. If the HCEO cannot produce this, you could be looking at a claim for damages landing on your doormat any day soon. It would also be prudent to ask the HCEO company for details of their insurers." Story from Scoop today here http://www.scoop.it/t/lacef-news Info in full from here http://thesheriffsoffice.com/articles/are-you-evicting-tenants-illegally -

Do you want to know when your area is changing from DLA to PiPs? If so please read the attachment as you can see when and what areas are up next for the changes. I have also included the Welsh version as well for reference. Last updated on the 05/04/2015 first issued 05/04/2013 Timetable for PIP replacing DLA Updated: April 2015 Timetable by date and location. This is done by using the first 2 letters from your postcode so using the attachment you can see when your area is having the change from DLA to PIP's for example the following areas are due for the change in May of this year From May 2015 From 25 May, areas further extend to include postcodes beginning: BS; CB; CM; CO; DA; GL; MK; PA; RM; SN; SP and SS.

-

Hi I have been trying to build my credit rating back up and I have been succeeding. It had even moved back up to the "good" rating on Experian. Anyway I am now in a position where I could open a savings account and actually put money away. I decided to open an instant access savings account with Nat West, so no overdraft, not a current account but to my surprise they did a credit search that has left a footnote on my credit score and knocked my score back down to "fair" So it seems that by wanting to be a customer and hand money over to them I have now paid the price by my credit report being damaged. Is this usual for opening a savings account?

-

This has affected two family members recently. The Macmillan website has come up with recipes donated by various people involved with treating cancer. They know that cancer patients don't always feel like eating and that chemo affects your taste buds and the recipes are designed to be nutritious, tasty and tempting. I hope the link is useful. HB http://be.macmillan.org.uk/downloads/CancerInformation/LivingWithAndAfterCancer/MAC11668RecipesDD20120813.pdf

-

Have you been affected by the "Farringdon Floods"...? [ATTACH=CONFIG]55628[/ATTACH] [ATTACH=CONFIG]55629[/ATTACH] Remember that you may be entitled to compensation through your representative operator's refund scheme. Please remember that the TSGN and IKF (Thameslink, Southern & Great Northern) (Integrated Kent Franchise) are run by Govia so the process will normally be the same. Details available below; Latest update is that a full service will resume tomorrow, however this may change at short notice.

-

Some people who applied to the NHS low income scheme may have paid too much towards their health costs, due to an error in the scheme’s calculations. The error affects a small number of claims. The NHS is working to identify people who were affected and to make a payment to them. You may be entitled to a payment if you applied to the NHS low income scheme between October 2003 and September 2008, and all of the following apply to you: you or your partner were aged over 60, and you or your partner were registered blind, were ‘signed off’ by your doctor as incapable of work for at least 28 weeks, or were receiving Disability Living Allowance, Incapacity Benefit, Severe Disablement Allowance or Attendance Allowance, and you were issued with a partial help certificate, called HC3, which set out how much you had to pay towards NHS dental, optical, travel to receive treatment, wigs and fabric support costs, and you then paid NHS charges or costs for any of the above while the HC3 certificate was in force. You’re not affected by this and can’t claim a payment if any of the following apply to you: you were issued with a HC2 certificate for full help with health costs you applied to the low income scheme before October 2003 or after September 2008 you met the eligibility criteria and received a HC3 certificate but didn’t pay any NHS charges or costs while it was in force. If you think you’re affected, you can apply for a payment by calling 0300 330 1344. You’ll need to confirm that you applied to the NHS low income scheme during the affected period and that you paid NHS healthcare costs at that time. You’ll be sent an application form which you need to return by 31 March 2015. You can find more information on the NHS Business Services Authority website. FAQs on the redress scheme. The NHS low income scheme provides help with health costs for people who are on low incomes but don’t qualify for any other help. More about the NHS low income scheme. http://www.adviceguide.org.uk/england/news/whats_new_dec14_nhs_low_income_scheme_redress.htm

-

Russell Hobbs is recalling 15 different steam irons, due to safety fears over a faulty flex cable, which could fail and cause injury. The irons affected by the recall are: Russell Hobbs 18651 Russell Hobbs 18742 Russell Hobbs 19220 Russell Hobbs 19221 Russell Hobbs 18743 Russell Hobbs 19840 Russell Hobbs 18720 Russell Hobbs 15081 Russell Hobbs 19222 Russell Hobbs 19400 Russell Hobbs 20260 Russell Hobbs 18741 Russell Hobbs 20280 Russell Hobbs 20550-10 Russell Hobbs 20560-10 The recall affects those manufactured between October 2012 and June 2013. How do I know if my iron is affected? The model number can be found on the underside of the heel of the iron, where you will find a rectangular shaped label which contains a five digit code. If you have one of the steam irons listed, you will also need to check the second five digit code. If the last two digits of 'Code 2' are 12 and the first three digits are between 045 and 365, you have an affected iron. If the last two digits of 'Code 2' are 13 and the first three digits are between 001 and 195, you have an affected iron. Anyone who owns an affected iron is being advised to stop using it immediately and to contact Russell Hobbs on Freephone 0800 307 7616 or 0333 103 9663 from a mobile, who will advise you of how to return your iron for a replacement or full refund of the purchase price. No other Russell Hobbs steam irons are affected by this recall. http://www.which.co.uk/news/2014/12/russell-hobbs-irons-recalled-is-yours-affected-388071/

-

A friend received an email that their loan was being written off as per their new lending criteria. They received the following info in their email : What happens next We will automatically clear any outstanding debt you have with us and your balance will be set to zero. This will be done by the end of October 2014. You do not need to do anything. We are working with the relevant credit reference agencies to remove records relating to this loan from your credit report. We expect this will take between three to four weeks to be completed. This will be done automatically and there is no further action required from you. When he checked his credit file today the loan has not been removed but marked settled. This is not what their email says, it clearly say's records should be removed. Anyone else have the same problem?

A friend received an email that their loan was being written off as per their new lending criteria. They received the following info in their email : What happens next We will automatically clear any outstanding debt you have with us and your balance will be set to zero. This will be done by the end of October 2014. You do not need to do anything. We are working with the relevant credit reference agencies to remove records relating to this loan from your credit report. We expect this will take between three to four weeks to be completed. This will be done automatically and there is no further action required from you. When he checked his credit file today the loan has not been removed but marked settled. This is not what their email says, it clearly say's records should be removed. Anyone else have the same problem? -

From This is Money :- http://www.consumeractiongroup.co.uk/redirect.php?x=http://www.thisismoney.co.uk/money/news/article-2554472/Four-million-savers-short-changed-Aviva-compensation-Insurers-323million-bill-merger-blunder.html

From This is Money :- http://www.consumeractiongroup.co.uk/redirect.php?x=http://www.thisismoney.co.uk/money/news/article-2554472/Four-million-savers-short-changed-Aviva-compensation-Insurers-323million-bill-merger-blunder.html -

Can anyone please can tell me if I will be affected by the benefit cap: I get: housing benefit : £74.84 Jobseekers: £66.58 weekly I am single and in a 1 bedroom flat, so going by these will I be affected? any help would be great thanks as I am just worried that I will be affected btw I am in a Housing Association.

-

Following the confirmation of administration today,which will be from next week,We await a statement from administrators giving information to customers with pre orders which have been paid for.returns and warranties etc etc. Comets warranties were underwritten by The Warranty Group who will still have a responsibility to customers irrespective of Comet going into administration. Their website; http://uk.thewg.com/product-warranties/electrical/index.html Their Customer helpline number for the UK is 01594 863000 Customers with vouchers should use these ASAP. If you paid for goods by card you may be entitled to raise a claim under s75 of the Consumer Credit Act. Please feel free to post below if you have been affected. As reported by the BBC; http://www.bbc.co.uk/news/business-20164228 Comet's customer care team is handling customer inquiries on 0844 8009595. But dont hold your breath if what we have seen from their customer services for the last 3 years is anything to go by,

Following the confirmation of administration today,which will be from next week,We await a statement from administrators giving information to customers with pre orders which have been paid for.returns and warranties etc etc. Comets warranties were underwritten by The Warranty Group who will still have a responsibility to customers irrespective of Comet going into administration. Their website; http://uk.thewg.com/product-warranties/electrical/index.html Their Customer helpline number for the UK is 01594 863000 Customers with vouchers should use these ASAP. If you paid for goods by card you may be entitled to raise a claim under s75 of the Consumer Credit Act. Please feel free to post below if you have been affected. As reported by the BBC; http://www.bbc.co.uk/news/business-20164228 Comet's customer care team is handling customer inquiries on 0844 8009595. But dont hold your breath if what we have seen from their customer services for the last 3 years is anything to go by, -

News as at 5th.July suggests it could be next week before all issues are resolved.There are many reports of failed direct debits and some being duplicated.