Search the Community

Showing results for tags 'request'.

-

Hi all, I have submitted a GDPR request to Cabot for an old credit card debt which I was paying of as part of a DMP I had until a couple of years ago (and stopped paying as I did ask for the CCA and cabot did not comply). Cabot provided all the information they “had”. They provided (as part of the GDPR the CCA ) however there is no mention or any confirmation that the debt was passed on to them or any correspondence made by them that they now owned my debt (i.e from the previous company, initially Egg, then “according to the notes I could find from Cabot “ idem but absolutely no mention of any communication of either purchasing the debt or correspondence made to me notifying that they were the “rightful” owner” … .not sure if the above makes sense .. I was under the impression that a Debt management company had to prove that they actually owned the “debt” and had to ensure the debtor was notified IF the debt was sold or no? Also it seems that several letters which I have received were not attached to the “GDPR” documentation (thought again they had to provide a copy of any correspondence sent?)

-

Hi, Im trying to unravel my late father's very complicated finances, as I'm his executor. I found a letter from Hoist Finance dated from last year stating they own the account, with an outstanding balance of £2131.92. When I phoned to say he'd died they told me it would be passed to 'Philips and Cohen' - this was mid-January and I've heard nothing (luckily). Having read these forums I then wrote to MBNA requesting all his account data but they replied stating the 'GDPR only applies to personal data relating to a living individual'. is this true?There's also a letter relating to another MBNA debt from Link Financial, so they have sold the two on. I need to know how old these are etc. Letters scanned and attached. The reason I'm confused is I've also written to Santander (using the same template letter) and have received all the loan info so they obviously have different rules! - I'm not willing to settle anything unless I know how old these debts are and what they relate to. We couldn't find any paperwork at my Father's house. Any advice as what to do next - I did send certified copy of probate certificate with my requests. Many thanks for reading! scan0041.pdf scan0040.pdf

-

Dear All, My neighbour plans to do a side extension which is only 90cm away from my side wall. I wrote to them in Nov. 2018, however they did not reply to me. Today I noticed they had started to take down some solid fences to prepare for the building work. What should I do now for their ignorance? Should I start to take formal process and take them to court? The are not easily approachable (this is why I write to them instead of speaking to them in person). (the letter is attached) Any advice would be appreciated! Thank you. ----------- Dear xxx We hope you are well. The County Council has informed us that you have planning permission granted to extend your property. I have been advised to check if The Party Wall Act is applicable to your building work. I have no objection of your building work whatsoever, of course. However, I believe that we may need to have a party wall agreement in place according to The Party Wall Act 1996 Section 6 (3 / 6m). Please bear with me if this is already under your consideration. It’d be great if you could let me know the following at your earliest convenience: When would you like to start your building work The depth of the foundation of your extension When you could provide a party wall notice We are happy to discuss appointing an independent party wall surveyor to make sure everything is fine. Surveyor Mr xxx has been recommended to us: .... .... For your information, I have enclosed a copy of the relevant section of the Act. I look forward to hearing from you soon. With best wishes

-

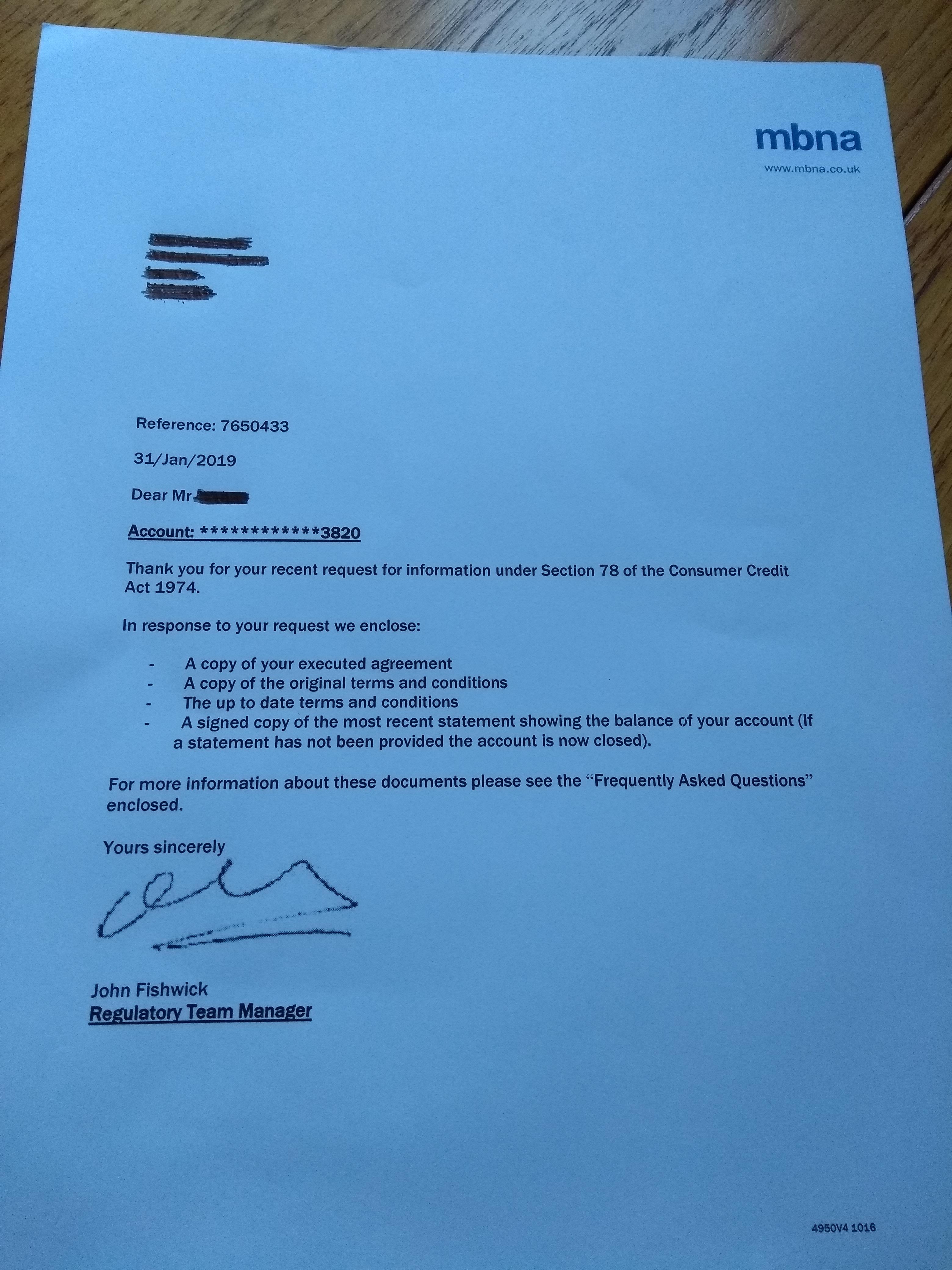

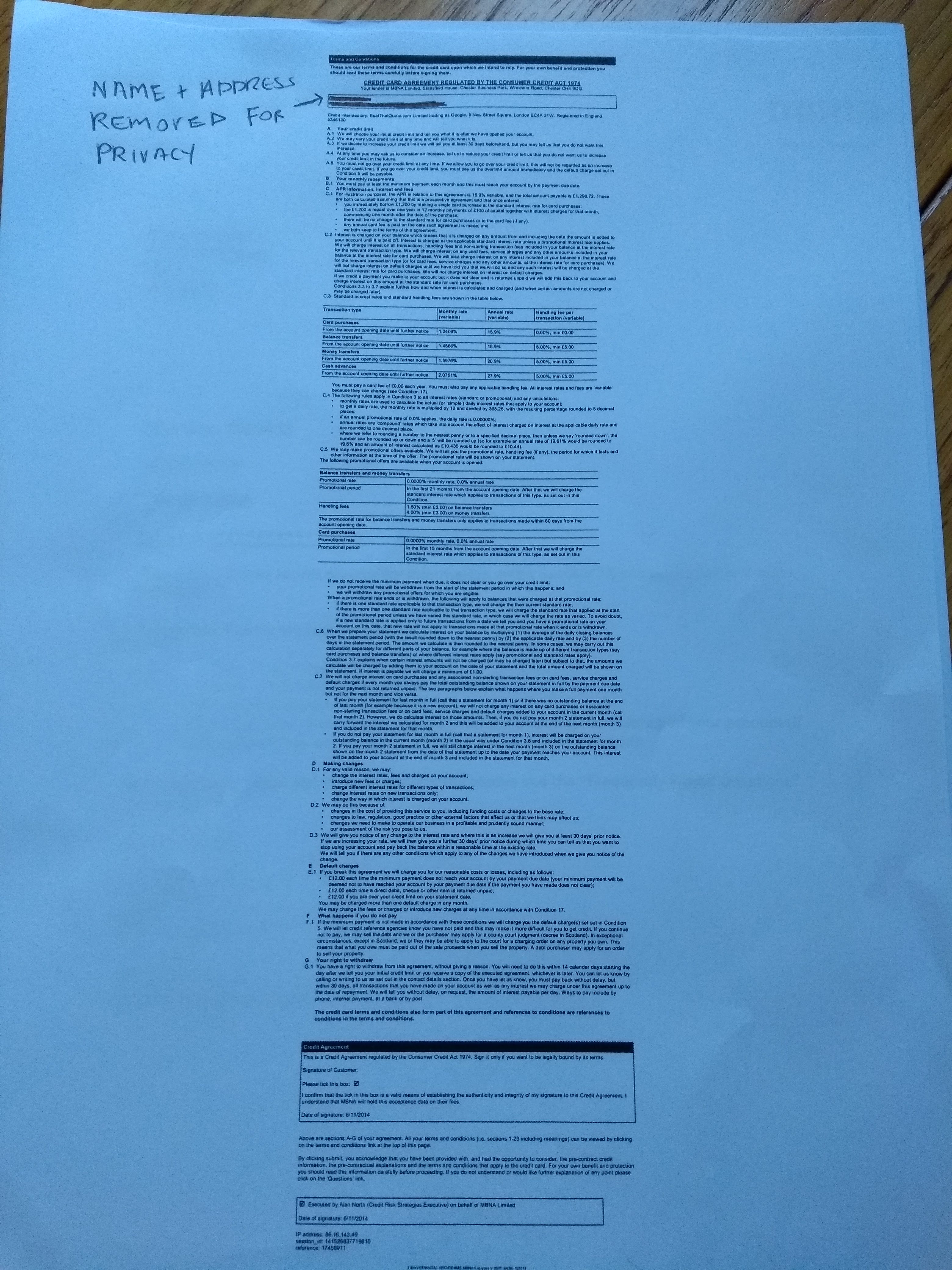

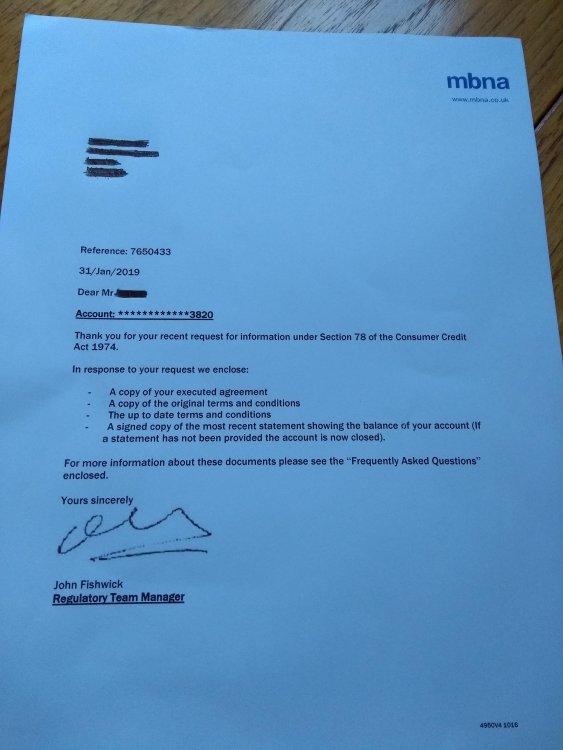

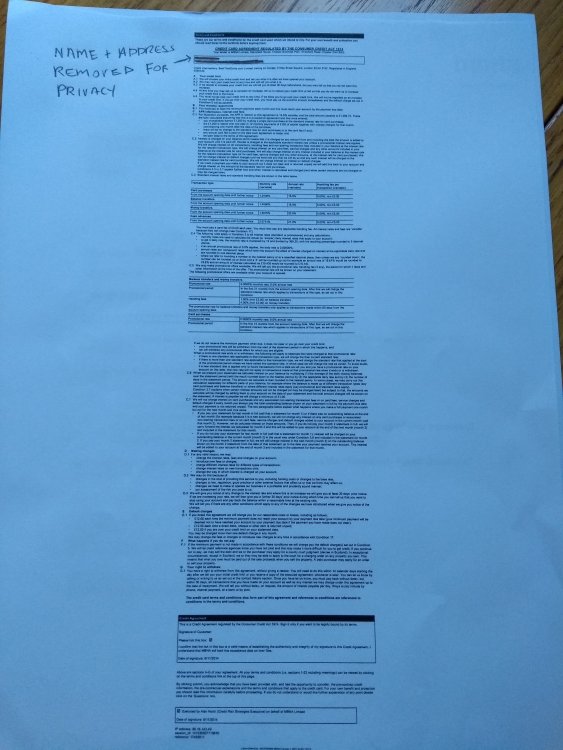

Had the following back from MBNA in response to a CCA request. 2 sets of T&C's, one current, and one supposedly from the time they card was taken out (not sure how I'd actually verify that) A summary statement showing current balance And a "copy executed agreement" Have uploaded the covering letter and the redacted "copy executed agreement". Basically, is this valid? This card was taken out in late 2014, and from what I've read it seems like it probably is a valid an enforceable response to my request, but would like to be sure before taking next step (MBNA bluntly rejected a recent full and final offer of around 60% of balance, claiming they never accept such offers. I should also mention that the debt is still with MBNA and no payments have been made for 3 months now. Current balance is a around £10.5k. Borrowing from family and selling a few things I reckon I could raise £8k tops. It doesn't seem like MBNA would accept this as a full and final, and all the while the interest mounts up.

-

GDPR, In 2018 I sent a request for CCA/Prove it letter to Idem they never replied or sent the info back. However they kept sending letters/calling to contact them etc, duly ignored as the CCA request was not fulfilled. About 10 weeks ago they sent a letter stating that as they could not get hold of me they decided to pass ALL my details to a company called “callresolve”. After 5 weeks I received a letter from callresolve stating that my details were passed on to them by Idem and that they will send someone over. About 2 weeks ago a lovely (sarcasm!) gent arrived at the house, all with a long black coat (not making this one up I swear) and a lovely badge from “Callresolve” anyhow, as he did not look like your average postman, I asked what he wanted. He said before he could tell me he had to “confirm” my details… I said “ah ok that would be good” and he started “if I could confirm the address” (yes that was right on the front door), I looked at the house number and pointed out at the street sign outside…. He said it was process, then (and this is where it gets quite interesting) he asked for my Date of Birth (to which I replied , I had one and I was happy with it). Anyway at that point I also added that he could “Jog on” and to ensure his coat would not get stuck on the porch. The question is, as Idem ignored any “prove it letter” or even CCA and without my authorization they passed on my private details to a third party. Are they in breach of GDPR guidance. As I thought under the new regulation ALL information can only be passed to third parties with someone’s explicit agreement (I never gave that agreement to Idem. I also got rather annoyed and called Idem, told them that I was still awaiting for the CCA and prove of debt (i.e deed) they said they were not obliged (rightly so I believe, ) to send me the deed of assignment however I asked them if they could confirm and send the confirmation of when they told me of their “Ownership” of the debt, they stated as it was sent in 2009 they did not have a copy (?) Could someone confirm what information I could ask for and if anything else I should be weary of? Idem seem to have got hold of a phone number which I seldom use, and also an email address which I used to set up a DMP years ago (but was still going on last year but NOT for Idem)….are they under obligation to let me know how they got hold of my data and who provided to them? Is there a template for GDPR ? and also what is the process to lodge a complain and to whom? The ICO (from what I can read, would limit itself to “remind” Idem to comply with requirements) Hope the above makes sense!

-

Hi all, I received a letter today from BWLegal in relation to a debt of £704.80 original debt was with The Money Shop, payday loan of just over £100.00. The debt is due to be made SB in March. The letter is threatening to take me to court and place a CCJ on my credit file. I have typed the below letter and would appreciate any feedback you could give. This will be the first letter they have received from me, I have not made any contact with them previously. I have also typed out the content of the letter I received from them today. 16th January 2019 CCA Request removed please do not post our template requests. The Below is a rough outline of the letter received today Dear MR XXXXXX We have been instructed by PRAC Financial Ltd to commence legal action in the form of issuing a claim against you in the county court, without further notice, in respect of the above debt. If payment or response is not received before the 14th February 2019. If you dispute this debt please tell us why so we can help resolve this matter. Estimated Claim Such legal action may result in you being liable for court fees, solicitors costs and statutory interest which are listed below: Principal Debt: £708.74 Estimated Interest: £118.37 Estimated Court Fees: £60.00 Estimated Solicitors cost: £70.00 Enclosures Enclosed with this letter are: Information Sheet Reply Form Income & Expenditure form Particulars of the debt On 20 February 2013 you entered into an agreement with Instant Csh Loans Ltd t/a The Money Shop to provide you with a fixed sum Loan agreement account. You failed to make payment in accordance with the terms of the agreement and it was later terminated and has since been assigned to our client on the 9th December 2016. Notice of this assignment has previously been given to you. Our client is not currently applying any interest, fees or charges to your account. Any help with my CCA Request letter is greatly appreciated, I want to make sure I have the correct sections quoted etc. Thanks in advance regards Veteran6224

Hi all, I received a letter today from BWLegal in relation to a debt of £704.80 original debt was with The Money Shop, payday loan of just over £100.00. The debt is due to be made SB in March. The letter is threatening to take me to court and place a CCJ on my credit file. I have typed the below letter and would appreciate any feedback you could give. This will be the first letter they have received from me, I have not made any contact with them previously. I have also typed out the content of the letter I received from them today. 16th January 2019 CCA Request removed please do not post our template requests. The Below is a rough outline of the letter received today Dear MR XXXXXX We have been instructed by PRAC Financial Ltd to commence legal action in the form of issuing a claim against you in the county court, without further notice, in respect of the above debt. If payment or response is not received before the 14th February 2019. If you dispute this debt please tell us why so we can help resolve this matter. Estimated Claim Such legal action may result in you being liable for court fees, solicitors costs and statutory interest which are listed below: Principal Debt: £708.74 Estimated Interest: £118.37 Estimated Court Fees: £60.00 Estimated Solicitors cost: £70.00 Enclosures Enclosed with this letter are: Information Sheet Reply Form Income & Expenditure form Particulars of the debt On 20 February 2013 you entered into an agreement with Instant Csh Loans Ltd t/a The Money Shop to provide you with a fixed sum Loan agreement account. You failed to make payment in accordance with the terms of the agreement and it was later terminated and has since been assigned to our client on the 9th December 2016. Notice of this assignment has previously been given to you. Our client is not currently applying any interest, fees or charges to your account. Any help with my CCA Request letter is greatly appreciated, I want to make sure I have the correct sections quoted etc. Thanks in advance regards Veteran6224 -

Evening, I requested a SAR from Co-op, I had a loan from them several years ago. I gave my name, address from when I made the application and the reference number from the loan. They have replied to me saying they are unable to verify my signature(s) after checking my records. They have asked my to provide photographic ID in order to investigate the matter further. Is this normal? Has anyone experienced this with Co-op? I've requested SAR from other places with no issues. Many thanks

Evening, I requested a SAR from Co-op, I had a loan from them several years ago. I gave my name, address from when I made the application and the reference number from the loan. They have replied to me saying they are unable to verify my signature(s) after checking my records. They have asked my to provide photographic ID in order to investigate the matter further. Is this normal? Has anyone experienced this with Co-op? I've requested SAR from other places with no issues. Many thanks -

Happy New Year to all! I have contacted HSBC using their online contact form about PPI that i took out with an old Marbles credit card. They have replied giving a credit card number and the start date, the also confirm PPI was paid. Reading other posts I see its best to start with a SAR request, can anyone advise the current address for making SAR requests or is it the standard complaints address : HSBC UK Bank plc, Complaints Department, POBox 5207, Coventry, CV3 8FB Thanks in advance

-

My dear Dad who served in WWII and worked all his life developed vascular dementia after suffering a stroke and eventually ended up in a care home. We applied for NHS Continuing Care and was passed from pillar to post as is the case for many. The only asset he had was the ex-council house which I helped him to buy [he had lived there for over 40 years at the time] with my mother. We bought the house as joint tenants in 1985. On my mother's death in 1991 we failed to inform the Land Registry of her death [not clued up at all about these things] so the house was then jointly owned by myself and my Dad. My Dad went into a care home in 2006. The local authority [LA] rejected the claim for NHS Continuing Care and took all my Dad's pension leaving him with a few pounds each week. As I was the joint owner of the property with my Father the LA kept sending me bills for the shortfall in his weekly care home fees. Upon my Dad's death in 2007 the LA continued to chase me for the shortfall in the care home fees amounting to thousands of pounds despite my stating I was pursuing a claim for NHS Continuing care. Earlier and unbeknown to me the LA had put a charging order on the house [sending 3 letters - one to my deceased mother, one to my father who was in the care home and one to me [living 200 miles away] we didn't pick up the letters until after the deadline for objecting had passed as we were obviously up and down the motorway visiting my father in the care home. Since then I have completed various questionnaires and sent loads of emails to no avail and no resolution of this issue. The demands for payment from the Finance Dept. stopped in 2014. I've not heard anything since. My questions are: 1. Does the charging order made by the LA against the property have an expiry date? I have seen something about 12 years? 2. If the Finance Dept. has stopped chasing me for payment - where do I stand now? Is the debt written off after x number of years? I maintain my father was fully entitled to NHS Continuing Care and I will continue to fight this - he died in 2007 - I haven't heard anything further from my last appeal I think in 2014 - it is very wearing. Meanwhile I can't sell the house [the charge on the house means the LA will get their hands on the money to which I vehemently object] and am letting the property out to tenants which is a whole new world of pain. I also foolishly paid someone to act as my advocate and of course he took the money and did - feel very let down that he could take advantage of people when they are at such a low ebb. I know I'm not the only person to fall prey to this person. Any advice gratefully received. Thank you.

My dear Dad who served in WWII and worked all his life developed vascular dementia after suffering a stroke and eventually ended up in a care home. We applied for NHS Continuing Care and was passed from pillar to post as is the case for many. The only asset he had was the ex-council house which I helped him to buy [he had lived there for over 40 years at the time] with my mother. We bought the house as joint tenants in 1985. On my mother's death in 1991 we failed to inform the Land Registry of her death [not clued up at all about these things] so the house was then jointly owned by myself and my Dad. My Dad went into a care home in 2006. The local authority [LA] rejected the claim for NHS Continuing Care and took all my Dad's pension leaving him with a few pounds each week. As I was the joint owner of the property with my Father the LA kept sending me bills for the shortfall in his weekly care home fees. Upon my Dad's death in 2007 the LA continued to chase me for the shortfall in the care home fees amounting to thousands of pounds despite my stating I was pursuing a claim for NHS Continuing care. Earlier and unbeknown to me the LA had put a charging order on the house [sending 3 letters - one to my deceased mother, one to my father who was in the care home and one to me [living 200 miles away] we didn't pick up the letters until after the deadline for objecting had passed as we were obviously up and down the motorway visiting my father in the care home. Since then I have completed various questionnaires and sent loads of emails to no avail and no resolution of this issue. The demands for payment from the Finance Dept. stopped in 2014. I've not heard anything since. My questions are: 1. Does the charging order made by the LA against the property have an expiry date? I have seen something about 12 years? 2. If the Finance Dept. has stopped chasing me for payment - where do I stand now? Is the debt written off after x number of years? I maintain my father was fully entitled to NHS Continuing Care and I will continue to fight this - he died in 2007 - I haven't heard anything further from my last appeal I think in 2014 - it is very wearing. Meanwhile I can't sell the house [the charge on the house means the LA will get their hands on the money to which I vehemently object] and am letting the property out to tenants which is a whole new world of pain. I also foolishly paid someone to act as my advocate and of course he took the money and did - feel very let down that he could take advantage of people when they are at such a low ebb. I know I'm not the only person to fall prey to this person. Any advice gratefully received. Thank you. -

I've been asked by a neighbour to see if I can find any contact details for a mortgate broker called Key Consultants, who I'm told provided advice and / or an intruduction prior to her obtaining a secured loan and PPI from a company called National Home Loans. She's been advised she may be able to claim PPI compensation, however the mortgage company has rejected her initial approach and stated that a 3rd party provided advice upon which her application was based. I've serched for 'Key Consultants' online and on the companies house website, and come up with a large number of possibles, but nothing conclusive. Can anyone point me in the right direction ? Many thanks in advance.

I've been asked by a neighbour to see if I can find any contact details for a mortgate broker called Key Consultants, who I'm told provided advice and / or an intruduction prior to her obtaining a secured loan and PPI from a company called National Home Loans. She's been advised she may be able to claim PPI compensation, however the mortgage company has rejected her initial approach and stated that a 3rd party provided advice upon which her application was based. I've serched for 'Key Consultants' online and on the companies house website, and come up with a large number of possibles, but nothing conclusive. Can anyone point me in the right direction ? Many thanks in advance. -

Hi we recently asked our landlord for recognition of our tenants association. We received the below late reply, after formally requesting recognition. Would this be grounds to send them a SAR as they say they have evidence on file? Also what would the best way to go about this, we have years of email trails so they shouldn't need to ID us. Thanks in anticipation Desamax Dear M ********, Upon receipt of your email dated **.**.18 I discussed the matter with our solicitors who confirmed that with the evidence we hold on file neither yourself or M****** are fit to be part of this proposed association. This is irrespective of our own views on the matter generally. I will pass on your email dated 13th instant to our solicitors for their perusal.

Hi we recently asked our landlord for recognition of our tenants association. We received the below late reply, after formally requesting recognition. Would this be grounds to send them a SAR as they say they have evidence on file? Also what would the best way to go about this, we have years of email trails so they shouldn't need to ID us. Thanks in anticipation Desamax Dear M ********, Upon receipt of your email dated **.**.18 I discussed the matter with our solicitors who confirmed that with the evidence we hold on file neither yourself or M****** are fit to be part of this proposed association. This is irrespective of our own views on the matter generally. I will pass on your email dated 13th instant to our solicitors for their perusal. -

Hi thanks to a member on here telling me to CCA Barclaycard I am looking for help. What makes it unenforceable I keep looking and some people say they have to produce original paperwork, others say they can send a revised one, being taken out in 1999 does it need to show my signature? Any help would be more than appreciated. X

-

Hi Caggers! I have a friend who is at the end of her tether with Scottish Power. She has a Gas Key for prepayment, however, has not used gas for approximately 6-9 years, possibly longer. This was due to the boiler breaking down and this was the only usage of gas, therefore she only uses electric immersion for the water heating. SP sent an invoice for money owing and after she quizzed them due to none usage they told her it was for X amount of standing charges for the gas meter. The agent for SP told her to ignore the bill due to none usage of gas and therefore she accepted that until she received another demand. Once the next agent told her a different story she requested the gas meter to be removed from her house. This request was made approximately 6+ years ago and was never actioned, until April 2018.Now of course they are demanding the standing charges for the last 6+ years at approximately £465. After numerous calls chasing up the removal and she was always told they were going to send somebody to do the removal. After many years of waiting they now sent her a bill for the entire periods of standing charges, which she disputes as she requested the removal, common sense eh? Now due to the hassle factor she has agreed to pay weekly when she tops up with her Electric Key to stop the hassle, but they do not appear to register these payments against her account as they have now issued a DC to chase her for the 'debt'. Now she contacts SP to inform them she has already made 3 payments to the account which they confirmed, but since then they know nothing of these payments and the DC keeps hassling her. Firstly, can she fight SP to actually cancel this debt in the first place as her request for removal was ignored? Secondly, how can we get this monster of a company to realise her payments already made need to be linked to her 'gas account' although she never buys gas? Any help would be greatly appreciated. regards stuscfc

Hi Caggers! I have a friend who is at the end of her tether with Scottish Power. She has a Gas Key for prepayment, however, has not used gas for approximately 6-9 years, possibly longer. This was due to the boiler breaking down and this was the only usage of gas, therefore she only uses electric immersion for the water heating. SP sent an invoice for money owing and after she quizzed them due to none usage they told her it was for X amount of standing charges for the gas meter. The agent for SP told her to ignore the bill due to none usage of gas and therefore she accepted that until she received another demand. Once the next agent told her a different story she requested the gas meter to be removed from her house. This request was made approximately 6+ years ago and was never actioned, until April 2018.Now of course they are demanding the standing charges for the last 6+ years at approximately £465. After numerous calls chasing up the removal and she was always told they were going to send somebody to do the removal. After many years of waiting they now sent her a bill for the entire periods of standing charges, which she disputes as she requested the removal, common sense eh? Now due to the hassle factor she has agreed to pay weekly when she tops up with her Electric Key to stop the hassle, but they do not appear to register these payments against her account as they have now issued a DC to chase her for the 'debt'. Now she contacts SP to inform them she has already made 3 payments to the account which they confirmed, but since then they know nothing of these payments and the DC keeps hassling her. Firstly, can she fight SP to actually cancel this debt in the first place as her request for removal was ignored? Secondly, how can we get this monster of a company to realise her payments already made need to be linked to her 'gas account' although she never buys gas? Any help would be greatly appreciated. regards stuscfc -

Good afternoon everyone, I sent off a CCA Request to Santander regarding a Debenhams store card, and got the following back. Does this mean they do not have an original copy on file. The card was originally run by GE Money and sold on to Max Recovery after I took out an IVA in 2012, or should I have written to GE Money or Max Recovery. Any help appreciated. img004.pdf img002.pdf img003.pdf

-

Hi there, Yesterday I received a letter from Lowell & 118 (together in one envelope) that Lowell are now the new owners of a 12 month unsecured loan I stopped paying in November 2015. During this period I also defaulted on 4 loans with 4 different payday companies however by now I have taken care of all but this one. I fully intend to take care of the last of my mess which rules out the PROVE IT route but there are a few stumbling blocks before I can do so. After checking my credit report I notice a second default has been placed on my account. How do I go about getting this removed? After also checking my credit file I notice that the original default placed on my account by 118 was not placed until 28 months after the account went delinquent despite ICO guidlines which state that 'accounts should be defaulted 3-6 months from last payment date'. How do I go about getting the original default accurately recorded to early 2016? (Giving me a clean slate in early 2022) I would like to thank you ever so much for taking the time to read through this thread and any input will be greatly appreciated.

Hi there, Yesterday I received a letter from Lowell & 118 (together in one envelope) that Lowell are now the new owners of a 12 month unsecured loan I stopped paying in November 2015. During this period I also defaulted on 4 loans with 4 different payday companies however by now I have taken care of all but this one. I fully intend to take care of the last of my mess which rules out the PROVE IT route but there are a few stumbling blocks before I can do so. After checking my credit report I notice a second default has been placed on my account. How do I go about getting this removed? After also checking my credit file I notice that the original default placed on my account by 118 was not placed until 28 months after the account went delinquent despite ICO guidlines which state that 'accounts should be defaulted 3-6 months from last payment date'. How do I go about getting the original default accurately recorded to early 2016? (Giving me a clean slate in early 2022) I would like to thank you ever so much for taking the time to read through this thread and any input will be greatly appreciated. -

Is the new GDPR SAR template suitable for a medical records request from a GP without any specific alterations? Thanks.

-

I personally know somebody who got a mortgage with an IVA so I know its possible as that's more frowned upon. I appreciate I won't get as good a deal having a DMP to my name though. Been in DMP for about 5 years. So defaults will be gone within 2 years. Cabot (was Halifax) £2300 Cabot (was Halifax)£3250 CashEuroNet (aka Quick Quid) £770 Instant Cash Loans (aka Payday uk)£305 Link (was Co-op) £5700 Moorcroft (aka Home Retail Group) £132 Nationwide (as is) £4200 Although one of these does not even appear on any of my credit reports.

-

Good evening all, I've done a bit of research trying to close accounts which led me to requesting CCA's to Cabot. I sent two for two different accounts which they took off Halifax (1 x CC & 1 x Current Acc Overdraft). I posted the following to them: Dear Sir/Madam Account No: With reference to the above agreement, I require you to supply the following documentation before I will correspond with you further on this matter. 1. You must supply me with a true copy of the alleged agreement you refer to. This is my right under your obligation to supply a copy of the agreement, under the legislation contained within s.78 (1) Consumer Credit Act 1974. 2. A full statement of account. 3. A signed true copy of the deed of assignment of the above referenced agreement that you allege exists. 4. A copy of any other documents referred to in the agreement. I understand that under the Consumer Credit Act 1974 (sections 77-79) , I am entitled to receive a copy of any credit agreement and a statement of account when I request it. I enclose a payment of £1 which is the fee payable under the Consumer Credit Act 1974. I understand a copy of any credit agreement along with a statement of account should be supplied within 12 working days. I understand that, under the Consumer Credit Act 1974, creditors are unable to enforce an agreement if they fail to comply with the request for a copy of the agreement and statement of account. A speedy response would be appreciated to resolve the matter amicably. I look forward to hearing from you soon. Yours faithfully THE LETTERS WERE RECEIVED ON 17TH/18TH JULY AND TODAY I RECEIVED THE FOLLOWING LETTERS: Thank you for your CCA request etc etc... We currently do not have this information on file. However I have requested the relevant details, which include a copy of the credit agreement, statement of account and relevant terms and conditions from the original lender. You have requested a copy of the Deed of Assignment. Please be advised that the DOA is a confidential document between Cabot and the original lender. It does not contain any personal details relating to you or your account and is not available for disclosure. We sent you a Notice of Assignment for your account to your address, which is sufficient to confirm our ownership of this account. Only the courts can request this... Blah blah blah. A couple of things here... I asked for a true copy, they are referring to simply a copy. If they do obtain a copy, is this enforceable? Also is it acceptable what they are saying about disclosing the DOA to me? I don't ever recall being sent a Notice of Assignment, if I did, is this sufficient to confirm ownership and enforceable? I have been currently paying towards what they are claiming, on a monthly basis via DMP. The next payment is due in a couple of days. Should I continue paying or is it advisable to stop until they wholly action my request? Thanks in advance and any help/advice/feedback is much appreciated! I'm looking to get a mortgage by the end of the year so I can get my son into the school I/he wants. Many thanks.

-

Hi I need some advice about requesting a CCA ive got a ccj more than 4 yrs old I'm being threatened with a warrant of control from restons unless I fill in a expenditure form is there any point in requesting a CCA the original debt is from around 8yrs ago and I've never responded to any letters or paid anything Would like to get some info on this Thanks in advance

Hi I need some advice about requesting a CCA ive got a ccj more than 4 yrs old I'm being threatened with a warrant of control from restons unless I fill in a expenditure form is there any point in requesting a CCA the original debt is from around 8yrs ago and I've never responded to any letters or paid anything Would like to get some info on this Thanks in advance -

Hi I'm helping a family member with regard to a PPI claim. They don't know if they've ever had PPI and most of the accounts are closed. She has no statements and cannot afford to pay £10 for a SAR for all of them. I've noticed that banks have an online PPI checker. My question is - will the banks tell the truth? As you can see I'm very sceptical about banks. Thanks in advance.

-

Hi I've just received a 'Letter Of Claim' from Howard Cohen & Co. Solicitors stating their client as "HPH2 LTD (Ex Tesco Personal Finance PLC)" also referenced in the letter as "Hoist Portfolio Holding 2 Ltd" regarding it's 'intention to issue proceedings in the County Court'. It also says "Despite our client or it's agents, Robinson Way Limited..." I believe my first course of action is to issue a CCA Request to the debt collector / client? The problem is that I cant find a UK address for Hoist Portfolio Holding 2 LTD but have found a Jersey address. The UK arm appears to be Hoist Finance who in turn own Robinson Way. Which of these companies should I write to with the CCA request? It's in relation to an amount of c.£5,500 on a credit card agreement allegedly signed in April 2008 Thanks

Hi I've just received a 'Letter Of Claim' from Howard Cohen & Co. Solicitors stating their client as "HPH2 LTD (Ex Tesco Personal Finance PLC)" also referenced in the letter as "Hoist Portfolio Holding 2 Ltd" regarding it's 'intention to issue proceedings in the County Court'. It also says "Despite our client or it's agents, Robinson Way Limited..." I believe my first course of action is to issue a CCA Request to the debt collector / client? The problem is that I cant find a UK address for Hoist Portfolio Holding 2 LTD but have found a Jersey address. The UK arm appears to be Hoist Finance who in turn own Robinson Way. Which of these companies should I write to with the CCA request? It's in relation to an amount of c.£5,500 on a credit card agreement allegedly signed in April 2008 Thanks -

For anyone that might be interested a simple online process to obtain data they hold on you . https://www.gov.uk/guidance/request-your-personal-information-from-the-department-for-work-and-pensions

-

Hi guys Around 2 years ago, I asked Cabot for a CCA request for a loan i had. They said at the time that they couldnt find the documentation so it was not enforceable. Ive recently had a letter form them saying they have now found this CCA agreement and that the debt is now enforceable! Theyve sent me a reconsituted copy but im wondering if this is now a debt i have to pay? If you look at the scan ive added, it looks like the document is missing something, and also surely there would have been more than 1 page of t&c's?? Is there not a time limit that they have to provide me with the CCA or its not enforceable? i ve read they committed an offence but that doesnt really help me in this situation Anyone know if this is now a debt again? i cant find anything similar to this anywhere thanks Scan 1 copy.pdf

-

NRAM can i send an SAR to NRAM for details of a repo from 2011?

lisadp1970 replied to lisadp1970's topic in General

Hello I need to make a Subject Access Request to NRAM regarding the house repossession we went through back in 2011. I've looked on their website and it's very vague what I need to include. The mortgage and property was joint with my ex husband so does he have to agree to me doing this? I need these details urgently as my local council won't let me go on their housing register until I can prove the house was repossessed and not sold for profit. Thanks for any help Lisa -

I saw a film last week and did not like it at all. Left half way through the film and the theatre refused to refund me stating I had sat through more than 50% of the picture. I want to just go back and get my refund with BC. Any idea where to begin?