Search the Community

Showing results for tags 'ltd'.

-

Received a claim? Yes Issue Date: 15-12-2017 Amount approx: 1979.25 Claimant: Cabot Financial (UK) LTD Solicitor: Mortimer Clarke Solicitors LTD Original Credit: Capital One Particulars of Claim: 1.By an agreement between CAPITAL ONE BANK (EUROPE) PLC & the Defendant on or around 08/10/2015 (the Agreement) CAPITAL ONE BANK (EUROPE) PLC agreed to issue the Defendant with a credit card. 2.The Defendant failed to make the minimum payments due & the Agreement was terminated, 3.The Agreement was assigned to the Claimant. THE CLAIMANT THEREFORE CLAIMS 1794.25 Stat Barred? No Have sent: Acknowledged the Claim, Sent a CCA request, Sent a CPR 31.14 request Have also file my defence. Well i had a letter back from their solicitors this is word to word and don't they proof check before sending out? also i know about Cabot Financial (UK) Ltd are unlicensed. Which means its an offence to under take debt collecting activity contrary to the Financial Services and markets Act 2000 and technically they aren't unlicensed they are unauthorised. "We confirm receipt of your defence. We can confirm that we acknowledged your request for documentation pursuant to civil Procedure part 31.14 and consumer credit act 1974, in the letter you sent to you on the 28/12/2017 (copy enclosed) In response to your assertion that our client is not authorised by the Financial Conduct Authority ('FCA'), the FCA register shows Cabot Financial (Europe) Limited permission as lapsed because, with the permission of the FCA, it has been made an appointed representative of Cabot Credit Management Group Limited. Cabot Credit Management Group Limited is a principal regulated firm and with the permission of the FCA, has .appointed its operational company, Cabot Financial (Europe) Limited, as appointed representative to perform debt recovery and/or debt administration activities on its behalf. Please find enclosed a copy of the Notice of Assignment and Statement of Account for your records. Our client's position is the documents provided evidences how the balance accrued and how a balance remained outstanding when the Agreement was assigned to our client. In response to your request for a copy of the Deed of Assignment, our client considers that it has no statutory obligation to provide you with any further documents in relation to the assignment. It has complied with its statutory obligations by sending you the Notice of Assignment in accordance with section 136 of the law of Property Act 1925. Furthermore, the Deed of Assignment is a confidential document client and the original creditor. We are instructed that the Deed of does not contain any personal details relating to you and is not disclosure. We can confirm that the remainder of your defense has been referred to your client for its instruction and we will contact you with a response as soon as possible. In the meantime, the Matter has been placed on hold." As you can see they are on about Cabot Financial (Europe) Limited, and not Cabot Financial (UK) LTD, also no Deed of assignment, or the original agreement, all they sent was the letter from capital one saying that they sold the account to cabot credit management group, and the letter Cabot sent to say they now own my account from Capital One and 3 pages of payments made to Capital one. What should be my next move? to me it seems they don't have the paper work to back their claim or am i wrong. And is there any other letters i can send to ask about the Deed of assignment and the original agreement?

-

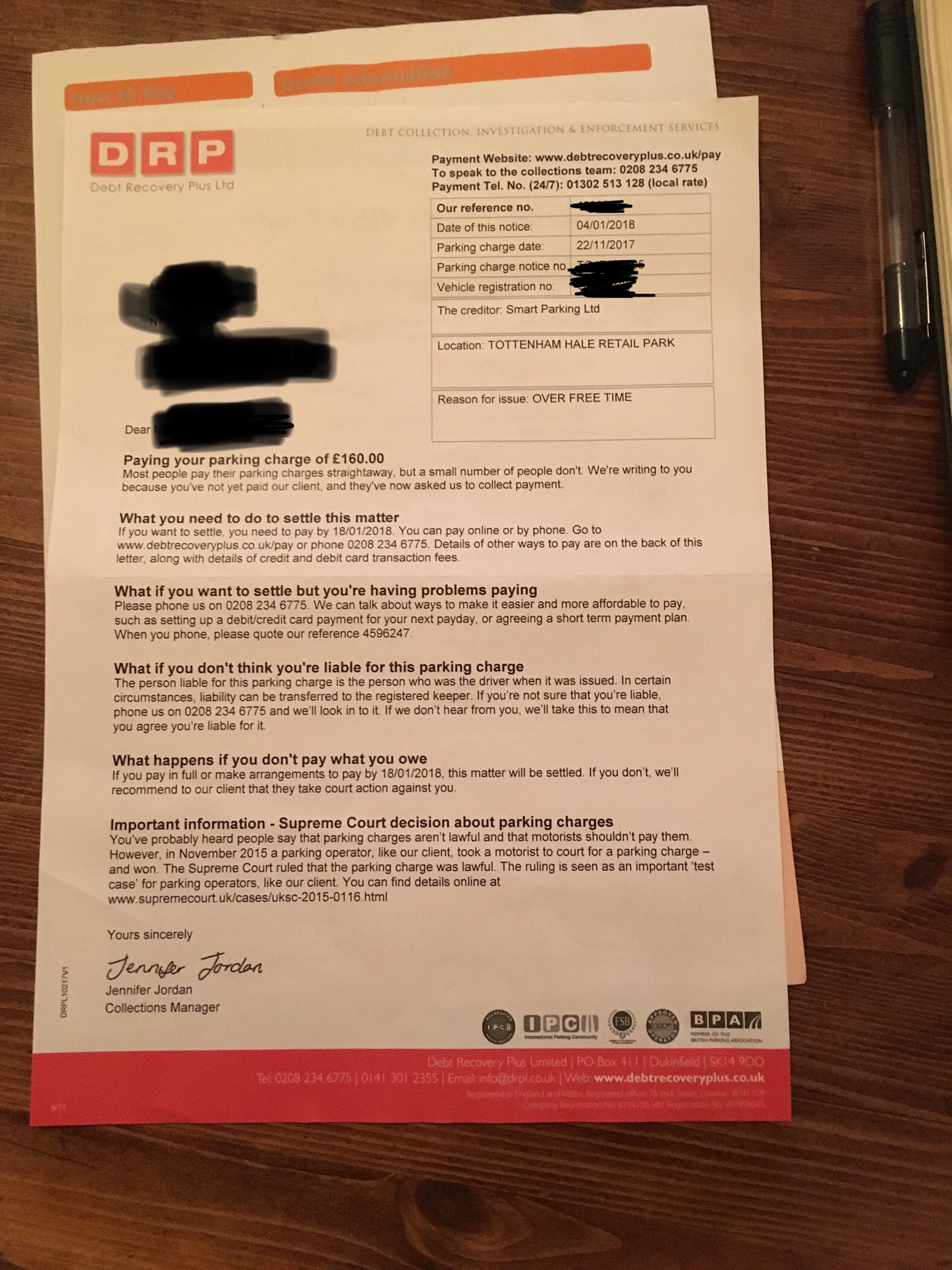

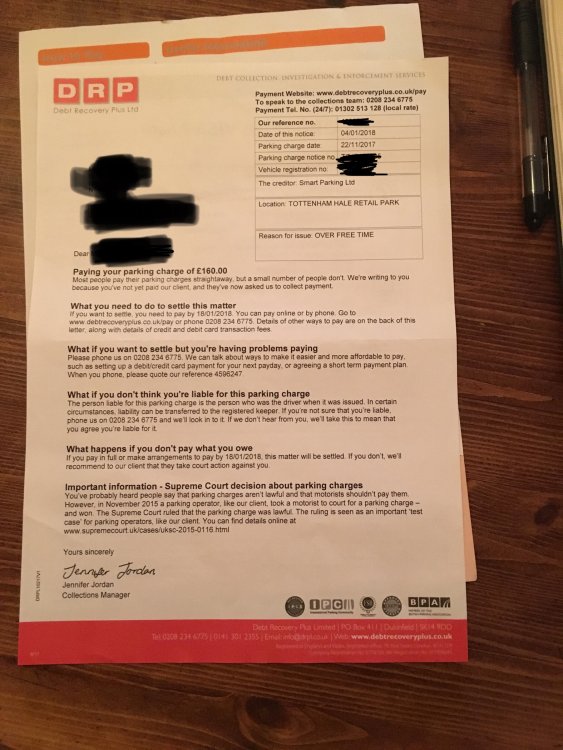

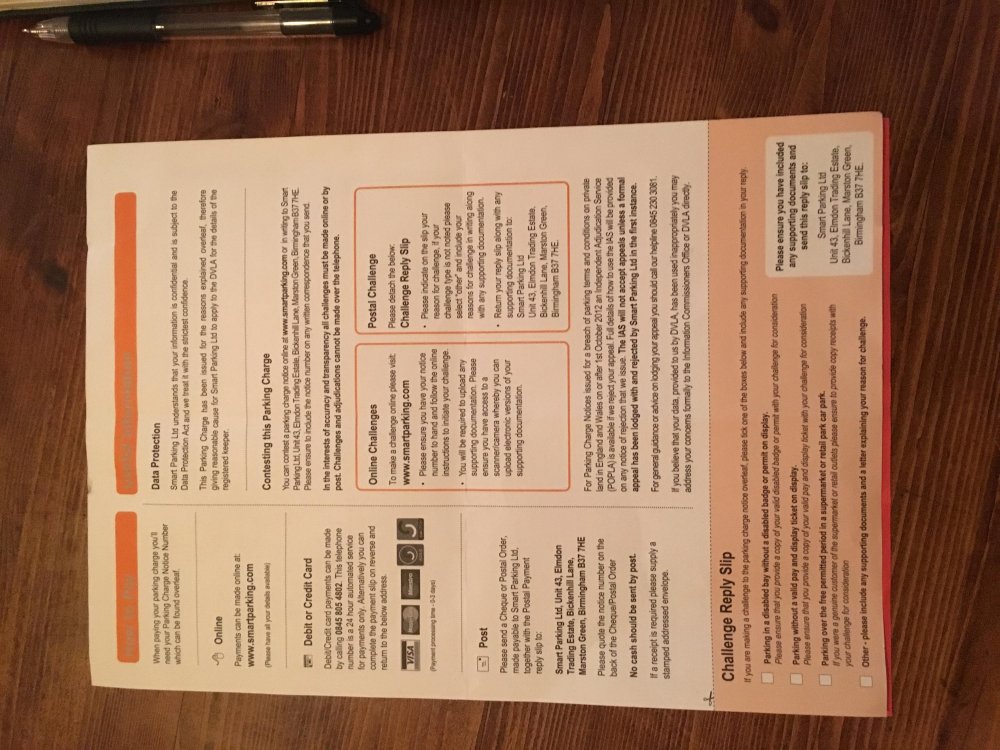

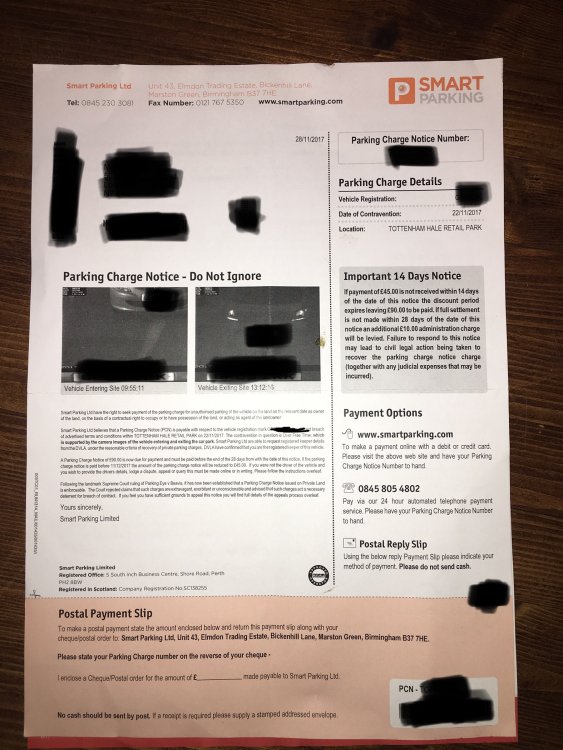

For tickets received through the post (Notice to Keeper) please answer the following questions. 1 Date of the infringement 2 Date on the NTK 22 November 2017 3 Date received Letter says it was sent on 28 November 2017, but only received letter just before Christmas. 4 Does the NTK mention schedule 4 of The Protections of Freedoms Act 2012? No mention of POFA in NTK, it is mentioned in follow up letter from debt recovery agency. 5 Is there any photographic evidence of the event?Yes 6 Have you appealed? Have you had a response? No 7 Who is the parking company? Smart Parking Ltd For either option, does it say which appeals body they operate under. There are two official bodies, the BPA and the IAS. If you are unsure, please check here. Original PCN mentions IAS, but your link says BPA If you have received any other correspondence, please mention it here. Received letter from debt recovery agency, saying charge is now £160.

For tickets received through the post (Notice to Keeper) please answer the following questions. 1 Date of the infringement 2 Date on the NTK 22 November 2017 3 Date received Letter says it was sent on 28 November 2017, but only received letter just before Christmas. 4 Does the NTK mention schedule 4 of The Protections of Freedoms Act 2012? No mention of POFA in NTK, it is mentioned in follow up letter from debt recovery agency. 5 Is there any photographic evidence of the event?Yes 6 Have you appealed? Have you had a response? No 7 Who is the parking company? Smart Parking Ltd For either option, does it say which appeals body they operate under. There are two official bodies, the BPA and the IAS. If you are unsure, please check here. Original PCN mentions IAS, but your link says BPA If you have received any other correspondence, please mention it here. Received letter from debt recovery agency, saying charge is now £160.

-

Hi I took out a door step loan in 10/2010 due to my younger sister having a stroke I defaulted in the same year I have not paid or recognised this debt since in 2014 it was assigned to lowell who marked it on my credit file as a new debt. Today I received a letter saying despite previous letters I have not made an agreement they are giving me 30 days notice before court have included a load of paperwork for me to fill out about financial situation other debts and am I seeking debt help or who I plan to pay. They say that because they took over the debt in 2014 the six year rule started when the took over the debt. The original debt no-one appears on my credit file as it went statute barred either the end of 2016 or early 2017. How do I fight this if it comes to court

-

Ill start with how and what it has come to for me to post on here. Around this time last year my nan went into end of life care at a pilgrims hospice in kent. At the time I was temporarily living with my mum who lives in Hertfordshire for work. There was no long term vision so I never changed my permanent address. I do have a dart charge account but before working there and due to other reasons I hadnt actually been to Hertfordshire often thus using the dartford crossing, overlooking the fact Id got a new car since the last time I had been there. As I also ride motorbikes and more often ride that and wouldnt pay dart charge manually. When my nan went into hospice for end of life care over the space of a couple of weeks there were five occasions i used my car and didn't pay the dart charge fee. My dad would open my post delivered to his address, but in the circumstances with his mum and my nan being so unwell and eventually passing away. The fines were sent to equita. This is where the trouble started... Originally the five penalties added up to a sum of £10, but through equita LTD they amounted to £190 each! Once I became aware of these I got in contact immediately and tried to resolve/explain the situation and set up a payment plan as id never had anything like this before. I ended up having five separate 'accounts' with them, I asked for have one set date a month for an individual payment to be paid by either standing order or direct debit to make things easier for both parties. But they insisted this they couldn't do this so on five separate times of each month a different amount would need to be paid. But being paid weeks, working long hours and with other financial commitments it was difficult. One week with no warning I had missed a £20 by a day, with no warning I had an enforcement agent at my dads door, demanding 3 of the 5 accounts in full plus his £235 fee. I ended up working nights paying him £100 a week. I even payed him £175 while on holiday which was a birthday treat from my girlfriend. After this and paying over £700 in such a short space of time, I called the office number, on hold for over an hour sometimes purely just to ask for a single payment date and a statement of all the money I had paid. With no exaggeration there has been over 20 times I have been hung up on or spoken to either rudely, patronising and even aggressively I have been told they have no record of what I have paid. At the end of November I called and made a payment which apparently cleared of my 'accounts' as the last two payments were made on the 25 and 29 of the month I asked if anyone would be in the office to pay on those dates in December, the lady on the phone told me there wouldn't but it would be fine to pay the end of the first week in jan. Which with luck was actually my pay day and all was well... Until Jan 3rd 2018 when I received a call from the same enforcement agent I had paid hundreds of pounds in the summer saying he had visited the address demanding the full amount plus £235. I had no warning, only recently I have received texts on the 24th and 28th as a reminder, but no one at equita was working!!! And i had been told friday the 5th would be fine. Since they have continued to hang up, will not discuss anything as its not their problem its the enforcement agents. I even have a couple of phone calls recorded proving this. Yet I still have an agent demading now over £500! Any ideas where I go??? Sorry for such a long threat but I thought it would be better to get it all in that reply filling the gaps later Thanks Also, A point I have missed. On four or five occasions asking for the statement and reciepts which they promised to send. Every single time I have only received what seems to be a generic print out of that I owe them money, with no statement or payments!!

Ill start with how and what it has come to for me to post on here. Around this time last year my nan went into end of life care at a pilgrims hospice in kent. At the time I was temporarily living with my mum who lives in Hertfordshire for work. There was no long term vision so I never changed my permanent address. I do have a dart charge account but before working there and due to other reasons I hadnt actually been to Hertfordshire often thus using the dartford crossing, overlooking the fact Id got a new car since the last time I had been there. As I also ride motorbikes and more often ride that and wouldnt pay dart charge manually. When my nan went into hospice for end of life care over the space of a couple of weeks there were five occasions i used my car and didn't pay the dart charge fee. My dad would open my post delivered to his address, but in the circumstances with his mum and my nan being so unwell and eventually passing away. The fines were sent to equita. This is where the trouble started... Originally the five penalties added up to a sum of £10, but through equita LTD they amounted to £190 each! Once I became aware of these I got in contact immediately and tried to resolve/explain the situation and set up a payment plan as id never had anything like this before. I ended up having five separate 'accounts' with them, I asked for have one set date a month for an individual payment to be paid by either standing order or direct debit to make things easier for both parties. But they insisted this they couldn't do this so on five separate times of each month a different amount would need to be paid. But being paid weeks, working long hours and with other financial commitments it was difficult. One week with no warning I had missed a £20 by a day, with no warning I had an enforcement agent at my dads door, demanding 3 of the 5 accounts in full plus his £235 fee. I ended up working nights paying him £100 a week. I even payed him £175 while on holiday which was a birthday treat from my girlfriend. After this and paying over £700 in such a short space of time, I called the office number, on hold for over an hour sometimes purely just to ask for a single payment date and a statement of all the money I had paid. With no exaggeration there has been over 20 times I have been hung up on or spoken to either rudely, patronising and even aggressively I have been told they have no record of what I have paid. At the end of November I called and made a payment which apparently cleared of my 'accounts' as the last two payments were made on the 25 and 29 of the month I asked if anyone would be in the office to pay on those dates in December, the lady on the phone told me there wouldn't but it would be fine to pay the end of the first week in jan. Which with luck was actually my pay day and all was well... Until Jan 3rd 2018 when I received a call from the same enforcement agent I had paid hundreds of pounds in the summer saying he had visited the address demanding the full amount plus £235. I had no warning, only recently I have received texts on the 24th and 28th as a reminder, but no one at equita was working!!! And i had been told friday the 5th would be fine. Since they have continued to hang up, will not discuss anything as its not their problem its the enforcement agents. I even have a couple of phone calls recorded proving this. Yet I still have an agent demading now over £500! Any ideas where I go??? Sorry for such a long threat but I thought it would be better to get it all in that reply filling the gaps later Thanks Also, A point I have missed. On four or five occasions asking for the statement and reciepts which they promised to send. Every single time I have only received what seems to be a generic print out of that I owe them money, with no statement or payments!! -

Hello, I have today received a letter from SCS Law who claim they've been instructed by Highview Parking Limited to recover an alleged penalty charge notice incurred by myself/my vehicle. Incensed by the content of this letter, I sought to establish what the address of the alleged contravention was supposed to have taken place it turns out to be my local gym where I've been a member for nearly 20 years and as such a legitimate user of their car park. I initially contacted Highview Parking to enquire about the reason for the letter and/or alleged contravention was advised by a lady to write to their Appeals Team who're based in Barnet. A second call to SCS Law drew a complete blank as the gentleman on the line advised that the firm had not been given any details on the alleged offence and had only been instructed by Highview to send out to me an initial notification letter. Now, knowing how some of these cases can be won and lost through technicalities and not wanting to allow my heated emotions overrule any logical thinking on my part, I'd be grateful for any advice on how I should proceed with this please, e.g. how and who to contact, my line of argument, etc. Thank you.

Hello, I have today received a letter from SCS Law who claim they've been instructed by Highview Parking Limited to recover an alleged penalty charge notice incurred by myself/my vehicle. Incensed by the content of this letter, I sought to establish what the address of the alleged contravention was supposed to have taken place it turns out to be my local gym where I've been a member for nearly 20 years and as such a legitimate user of their car park. I initially contacted Highview Parking to enquire about the reason for the letter and/or alleged contravention was advised by a lady to write to their Appeals Team who're based in Barnet. A second call to SCS Law drew a complete blank as the gentleman on the line advised that the firm had not been given any details on the alleged offence and had only been instructed by Highview to send out to me an initial notification letter. Now, knowing how some of these cases can be won and lost through technicalities and not wanting to allow my heated emotions overrule any logical thinking on my part, I'd be grateful for any advice on how I should proceed with this please, e.g. how and who to contact, my line of argument, etc. Thank you. -

Hi, this is one for people who really know their contract law, specifically the consumer credit act. This is the scenario: I have a builder do me an extension. Our contract states the work will cost £100k. In order to get s75 CCA protection, I get the builder to give me 4 invoices. Invoice 1- foundations, £25k (price shown on the contract) Invoice 2- Roof, £25k (price shown on the contract) Invoice 3- Walls, £25k (price shown on the contract) Invoice 4, decorations £25k (price shown on the contract). £100 was paid for each invoice using a credit card. The transaction I made on each card was for the invoices, not for the contract. Each invoice takes the pricing from the contract. Does anyone, who has a legal mind with a speciality in contract law, know if I can expect cover under s75 CCA in this situation? thanks

Hi, this is one for people who really know their contract law, specifically the consumer credit act. This is the scenario: I have a builder do me an extension. Our contract states the work will cost £100k. In order to get s75 CCA protection, I get the builder to give me 4 invoices. Invoice 1- foundations, £25k (price shown on the contract) Invoice 2- Roof, £25k (price shown on the contract) Invoice 3- Walls, £25k (price shown on the contract) Invoice 4, decorations £25k (price shown on the contract). £100 was paid for each invoice using a credit card. The transaction I made on each card was for the invoices, not for the contract. Each invoice takes the pricing from the contract. Does anyone, who has a legal mind with a speciality in contract law, know if I can expect cover under s75 CCA in this situation? thanks -

Hi everyone I hope I've posted this in the correct forum as I'm back again just looking for advise and general pointing in the right direction. I've received a letter (PDF attached) and presume at this stage all I can do is send a CCA request to Link? Do I send a SAR to Link and MBNA or just to MBNA as they were the original creditor? Regards Suss Link.pdf

-

Hi all : haven't posted in a while. Had letter out of the blue yesterday from Global Debt Recovery Ltd (New Malden) Client Jefferson (Insurance Product) sum of just under £100.00. We are today appointed as agents for the collection.......basically giving me options how to pay etc Never heard of this company and quite frankly don't recall any insurance owing. Any advice on how to respond please kind regards

-

Hi all I wonder if you can help (provide guidance). I received a CCJ 8 years ago from Yorkshire Bank for a visa card. I paid £20.00 per month for six years and then stopped. I received various letters from Mortimer Clarke which I ignored and subsequently they went to court and got an attachment of earnings. This was paid for several months until I left the company and am now working for myself. The court has today written to me to say the attachment of earnings is dismissed. I need to know really what my next step should be - the original debt was just under £10k and it is now £9,800 so I have made very little impact into this debt. Should I contact Mortimer Clarke and continue to pay a nominal amount or is there anyway I can fight this. The original credit agreement goes back to 1995 (but I never requested this orginally). Any advice would be grateful. Thanks Bump

Hi all I wonder if you can help (provide guidance). I received a CCJ 8 years ago from Yorkshire Bank for a visa card. I paid £20.00 per month for six years and then stopped. I received various letters from Mortimer Clarke which I ignored and subsequently they went to court and got an attachment of earnings. This was paid for several months until I left the company and am now working for myself. The court has today written to me to say the attachment of earnings is dismissed. I need to know really what my next step should be - the original debt was just under £10k and it is now £9,800 so I have made very little impact into this debt. Should I contact Mortimer Clarke and continue to pay a nominal amount or is there anyway I can fight this. The original credit agreement goes back to 1995 (but I never requested this orginally). Any advice would be grateful. Thanks Bump -

I have received a County Court claim form for Lowell Portfolio 1 Ltd for an old BT debt 10 years + for £290 incl. fees and costs Can anyone point me in the right direction to a Defence Template I can use I have already requested further information from Lowell as I do not acknowledge the debt as it is so old and have since had other accounts with BT over the years but yet to receive a reply I have till the 13th Dec to submit my defence Thank you

-

Please don't fall into their trap like I and others have done. We were approached by Falcon Management Services last year after a company went into liquidation owing us a substantial amount of money. This company contacted us as they were aware we were on the creditors list (not sure where they get this info) and there seemed to be a light at the end of the tunnel that we may get our money back. Of course they had inside information of fraudulent behaviour on the part of the director. It all seemed plausible as we suspected him of wrong doing. For a one off fee they guaranteed they would get our money back or the fee would be refunded. That was the hook. Be warned you will not get your money back and they will pursue you quite aggressively demanding more money from you and threats of various actions if you do not pay within the next few hours. I like to think we are not gullible and knowledgeable enough not to be taken for a ride. But they prey on you when you are when are dealing with the anger, upset and financial loss you have already suffered and entice you with false promises. Article in the Express on Monday 10th of April about Falcon Management services Ltd in the Crusader section http://www.express.co.uk/finance/crusader/790244/the-crusader-debt-collector-trader-falls-victim-get-back-money-owed Hope this post saves someone else from being even further out of pocket and being harassed by them

-

Re: Awful experience with mylhd BUYERS BEWARE - I have had an abysmal association with My 'LHD' UK Ltd. I paid a 20% deposit for a Mercedes SLK and, even repeated warning bells of being ignored and not receiving replies to e-mails or telephone messages, did not prevent me from being duped by this Company. Luckily, because of the Company's inefficiency and lack of professionalism, information it provided about its Euro Bank Account were inaccurate and the final payment for the car did not go through and the payment was rejected by the Company's Bank, albeit €346 short. Sadly I did not see this forum until after I had paid the deposit and I hope that by posting other unsuspecting potential buyers will pick up these threads as I am surprised at the online sales activity still enjoyed by such a Company. Despite being assured by the Company Director that my deposit would be returned if my requirements could not be satisfied, he did not honour his word. I was advised that I was protected by the Distance Selling Regulations, so I issued a Summons through the Courts, but the Company lodged what I can only describe as a completely fabricated defence which made it clear to me the course that the Proceedings would take. Also, one must bear in mind that the Company could possibly go into voluntary liquidation in which case any claim would be lost. So, I closed the case down and decided to cut my losses. An expensive lesson, but one I will never forget.

-

Good afternoon all, like to say big thanks for this forum reading through all the cases I have managed up until this point not to ask for advise..... I have been through letter receiving from Lowell, phones calls, sending CCA & CPR requests, creating my witness statement/defence etc (attached to this for background) I have my court date 21st November 7 Lowell have paid the allocation fee which I checked with the court today. This is for a debt with Aqua credit card around £1200 original debt. My question is....... .They have supplied my old credit card statements but I still haven't received the signed CCA agreement I have asked for or the default notice? Does that help me in court? They have even put on their defence they haven't got it but will continue to ask for it from the original creditors? Suppose what I am asking is without me receiving it then surely even if they did turn up with it at court then they can't enforce a CCJ? Could be wrong but wanted to gather some thoughts from other members? Anything else you need to know please let me know. Thanks

Good afternoon all, like to say big thanks for this forum reading through all the cases I have managed up until this point not to ask for advise..... I have been through letter receiving from Lowell, phones calls, sending CCA & CPR requests, creating my witness statement/defence etc (attached to this for background) I have my court date 21st November 7 Lowell have paid the allocation fee which I checked with the court today. This is for a debt with Aqua credit card around £1200 original debt. My question is....... .They have supplied my old credit card statements but I still haven't received the signed CCA agreement I have asked for or the default notice? Does that help me in court? They have even put on their defence they haven't got it but will continue to ask for it from the original creditors? Suppose what I am asking is without me receiving it then surely even if they did turn up with it at court then they can't enforce a CCJ? Could be wrong but wanted to gather some thoughts from other members? Anything else you need to know please let me know. Thanks -

Hi everyone I received this hand delivered letter today from Debt Management Services LTD. They say they are acting on behalf of Bradford and Bingley, I had a mortgage with them over 21 years ago and my house was repossessed. I have made payments on the account over the years but not anything in the last 4 years. The letter says they want to discuss any problems I may be having with the outstanding account. In order to bring my account upto date they want me to contact them. I can't find out much about them on the net, are they debt collectors or bailiffs ? Any help or info would be greatly appreciated, thanks.

Hi everyone I received this hand delivered letter today from Debt Management Services LTD. They say they are acting on behalf of Bradford and Bingley, I had a mortgage with them over 21 years ago and my house was repossessed. I have made payments on the account over the years but not anything in the last 4 years. The letter says they want to discuss any problems I may be having with the outstanding account. In order to bring my account upto date they want me to contact them. I can't find out much about them on the net, are they debt collectors or bailiffs ? Any help or info would be greatly appreciated, thanks. -

Purchased a clutch mail order on 11/5/2015, it had a 4yr 40,000 mile warranty. just over 2yrs and 20,000 miles the clutch was juddering violently in reverse and pulling away .they offer a no quibble guarantee for parts only so no claims for the labour charge. "parts will be replaced irrespective as to whether there is a fault or not. If you cannot be without your vehicle simply purchase a new replacement second item from us and we will refund you for the first item upon its return". sound really good customer service ! NOT. Sent it back on 26/7/2017 at a cost of £15 non re-fundable to them, no reply or refund for weeks called them, they said due to holidays and staff shortage a delay had occurred. on the 31st aug 2017 received letter saying "i refer to the above and to your returned goods for which you seek replacement, which I am unable to offer because your parts display no manufacturing defect, just fair wear and tear. Whats the point in having a four yr warrant if when you send it back they just refuse it as wear and tear. when the cluch was removed by a professional garage they said that the dmf bearing showing excessive play causing severe juddering going foreward or reverse. the offer a no quibble guarantee then take it back. I need to stop these people from robbing me can you help please.

-

Hello All, I have just received a 'Parking Charge Notice' from HX Car Park Management Ltd. According to the contravention the: 'Pay and Display Ticket was face down' and they are requesting £60 (if paid within 14 days) or £100 (if paid within 28 days). There are no ticket machines in the car park and on arrival to the car park you pay cash to an attendant, he gives you a piece of square, coloured paper with the date printed on it (which they have photographed as evidence). Each day you're provided with a different colour. With hindsight, I stupidly didn't realise that I needed to place the dated ticket face upwards. I was under the impression that you couldn't park there without going past the parking attendant. Worryingly, I could potentially be liable for at least another three days as I'm not sure if I placed the coloured ticket 'face up' on the following days. Any advice would be most appreciated as this could potentially be an anxiety inducing £240.00 in total (almost a week's wage for me). All the best, Amy

Hello All, I have just received a 'Parking Charge Notice' from HX Car Park Management Ltd. According to the contravention the: 'Pay and Display Ticket was face down' and they are requesting £60 (if paid within 14 days) or £100 (if paid within 28 days). There are no ticket machines in the car park and on arrival to the car park you pay cash to an attendant, he gives you a piece of square, coloured paper with the date printed on it (which they have photographed as evidence). Each day you're provided with a different colour. With hindsight, I stupidly didn't realise that I needed to place the dated ticket face upwards. I was under the impression that you couldn't park there without going past the parking attendant. Worryingly, I could potentially be liable for at least another three days as I'm not sure if I placed the coloured ticket 'face up' on the following days. Any advice would be most appreciated as this could potentially be an anxiety inducing £240.00 in total (almost a week's wage for me). All the best, Amy -

Good afternoon! My husband has received the above two documents (I am hopefully attaching redacted scans to this post) and, as he's currently in hospital, I need to try and deal with them in his absence. I presume we should respond in some way, although I'm not totally convinced that this debt is his - he says he doesn't recall taking out a credit card with Home Retail Group. I certainly don't want to phone them or email them! It's clearly not statute-barred, as it dates from 2012. My hubby says that he can recall getting "some guff or other" (his words!) from Lowell in the past, but because he didn't know what they were talking about, he ignored it. Therefore, I haven't a hope of identifying what might have been received previously, or not. Your always excellent advice would be very much appreciated as to my next step. Scan Lowell 2.pdf Scan Lowell 1.pdf

-

Hi I have received a Magistrates Liability Order for 2 people who do not live at my address and the debt relates to a different address they have advised they will be taking goods in the next few days !!! Help I cannot get any advice

Hi I have received a Magistrates Liability Order for 2 people who do not live at my address and the debt relates to a different address they have advised they will be taking goods in the next few days !!! Help I cannot get any advice -

Hi all, Very sorry for the long post, hope it makes sense. I have seen quite a few posts here regarding Xercise4Less but every case seems to be different and i just want to check what i have done is correct. I was with the gym for approx. 2 years, i changed jobs and could no longer attend the gym so i went into the gym and spoke to a lady at the counter to cancel my membership this was around the 21st May, at this point there was no mention that i needed to go online to cancel and no mention that i needed 30 days to cancel my membership, the lady simply said that my membership has been cancelled. on the 25th May the following months membership come out (i had no issues with this, maybe it takes a few days to go through etc) , on the 14th June i received a letter saying they haven't received payment, i ignored this letter as i had cancelled my membership and paid on the 25th (probably my first mistake?) I dont have the letter but before the 1st July i received another letter saying i owed £34.99, i emailed them trying to explain as this way i have records, they emailed back on the 2nd saying i need to cancel on the website, which i then did (figured i had nothing to lose by trying) I sent 4 emails sent to Harlands with Xercise4Less copied in between 13/07 and 31/08, I received no replies from them then on the 02/08 I received a reply saying they don’t have any records of me emailing them, I emailed them back explain again all the issues saying I am happy to pay the £9.99. On the 28th July I received the next letter saying i owed £69.98, i phoned the gym, they told me i needed to speak to Harlands, Harlands said i had to pay or speak to the gym about my cancelling (i was going round in circles for a few days. My final email to them was from your messages boards to which they didn’t reply. If you confirm in writing that you'll accept the amount of £9.99 in settlement of all that I owe, I will pay you promptly. If you fail to accept my offer within 14 days or you demand any other payment, I will pay you nothing and my offer will be withdrawn. On the 12 August CRS got involved sending me a letter saying i owed £104.97 On the 12th August CRS sent another letter saying i owed £171.47 On 28th September CRS said i owed them £171.47 and gave me two options, Legal Action or Outsourced to external agents if i don't pay. On the 18th October CRS said i still owed them 171.47 saying it is now being passed to Zinc Ltd. Suggestions on what to do now? Currently I am just ignoring them, i have received only a couple of phone calls which i didn't answer.

-

Hi, I've recently had late payment charges on 2 LTSB credit cards. This pushed one of the cards over the limit incurring another £12 on top of that. When I made the next payment I did not include the late payment charges they'd added on to the minimum payments, so they added further charges. These cards were originally an accucard and an Easy card both of which LTSB bought out. I have noticed that the interest rates have crept up to much higher than when the cards were taken out also and when I received the last replacement card it stated "for details of the interest rate please refer to your original agreement. I'm therefore thinking it's time to challenge them for agreements. I've been reading up on the latest CCA info as I'm a bit rusty and things have moved on since I last did this. I'd really appreciate any advice, because it looks a bit confusing nowadays. Adding late payment charges onto the minimum payment really annoys me. How do they expect someone who has struggled to make the basic payment be able to pay all their add ons? Does anyone know please whether adding late payment charges onto minimum payments has been successfully challenged? I'm thinking of sending a standard CCA request letter with an added bit challenging the charges. Any further suggestions would be appreciated.

Hi, I've recently had late payment charges on 2 LTSB credit cards. This pushed one of the cards over the limit incurring another £12 on top of that. When I made the next payment I did not include the late payment charges they'd added on to the minimum payments, so they added further charges. These cards were originally an accucard and an Easy card both of which LTSB bought out. I have noticed that the interest rates have crept up to much higher than when the cards were taken out also and when I received the last replacement card it stated "for details of the interest rate please refer to your original agreement. I'm therefore thinking it's time to challenge them for agreements. I've been reading up on the latest CCA info as I'm a bit rusty and things have moved on since I last did this. I'd really appreciate any advice, because it looks a bit confusing nowadays. Adding late payment charges onto the minimum payment really annoys me. How do they expect someone who has struggled to make the basic payment be able to pay all their add ons? Does anyone know please whether adding late payment charges onto minimum payments has been successfully challenged? I'm thinking of sending a standard CCA request letter with an added bit challenging the charges. Any further suggestions would be appreciated. -

Hi all, Looking for some advise. As the title says got court action from Motormile on behalf of Cash Genie. Submitted my defence quite awhile back on the 25th august and have heard NOTHING at all. The claim history when logging in stands as below Claim History Your acknowledgment of service was received on 14/08/2017 at 01:07:10 Your defence was submitted on 24/08/2017 at 21:44:09 Your defence was received on 25/08/2017 at 08:02:45 Just wondered what happens now? Did / Do they have a timeframe they have to adhere by before it gets thrown out? Just looking for advise as i haven't got a clue. Many thanks

-

I received a PCN through the post (arrived today) for an offence committed on 29th July. I lent my car to my Mum for a weekend so she was the driver not me. She insists she paid but as it was a machine that asks for your registration she may well have entered it incorrectly, Im wondering if I can appeal on the grounds that the PCN wasn't issued until 15th August (17 days later) as stated on the letter. Can anyone advise please? Further details below... 1 Date of the infringement 29th July 2 Date on the NTK [this must have been received within 14 days from the 'offence' date] 15th August 3 Date received 17th August 4 Does the NTK mention schedule 4 of The Protections of Freedoms Act 2012? [y/n?] No 5 Is there any photographic evidence of the event? Yes, of her driving in and out of the car park. Total stay 1hr 2 mins. 6 Have you appealed? {y/n?] post up you appeal] Not yet Have you had a response? [Y/N?] post it up 7 Who is the parking company? Civil Enforcement Ltd 8. Where exactly [carpark name and town] Custom House Quay, Falmouth in a Tesco car park I believe.

-

Hi, Could I ask for some advice on how we should handle the following situation, that has recently cropped up. This problem started we believe way back in 2011, we went to the car phone warehouse to change a telephone that we had on contract with Orange. We were told that since Orange no longer supplied mobile phone services the mobile would be registered with EE the new Orange provider. We changed the telephone over and the assistant at car phone warehouse confirmed with Orange/EE that the old contract was now cancelled. Then some months later Orange sent us a bill for 3 months connection charges for the old telephone, we spoke to Orange a few times by telephone and they finally agreed to sort the account out and remove the charge since we no longer had that telephone. We then moved address, although both me and my partner still had EE phones so EE had full information of all of the addresses we had occupied. Now in 2017 my partner attempted to get a small item on credit and were shocked to find out that she had some sort of issue on her credit file, when we look at her credit record on a free credit database service, we were shocked to see that Orange had somehow and for some reason registered a debt of £125 against my partner causing issues on getting credit. we may need to get a small mortgage soon so we were really concerned about this. we have called EE and they quickly passed us over to Orange (although they are supposed to be the same company we thought) The Orange contact we were given was an email only service. The initial response we got back from them once we had highlighted it was that they could not find anything on their system to do with our account. Also EE had said they could not see anything in their records pertaining to this debt. We emailed Orange a second time and told them to look harder since it appeared that Clear score had something registered against my partner for, a mobile phone issue. after taking her d.o.b etc they looked again and this time they found something but could not be specific about when it occurred? At first they telephoned my partner and said said the issue occurred in 2011, at an address which we did live at in 2011, then when she advised them that we did not owe the money since it was from an old mobile that had been transferred by them to EE, and that the debt should have expired anyway since it was 6 years ago. The person at Orange then emailed her to inform her that the issue occurred in 2014 (he had appeared to change his mind?) but that the address it occurred at was the old address (we did not reside at this address in 2014). they advised us that they could do nothing about the issue and that we would have to speak to EE customer service, we again spoke to EE customer service who again told us they could do nothing since it was with Orange Credit team ?? We emailed the Orange credit team yet again and they said that the debt had been passed to a DCA, and asked us if we had received any letters from said DCA (Arrow Global Limited). We advised EE that we were extremely disappointed and that we want them to escalate it, we have heard nothing yet and now we are considering what actions to take moving forward. We have not communicated with the DCA since we have no contract with them and don't want to put ourselves in any situation that means we are in contract with them. Could anyone give us some advice on how we could/should proceed with this. Any help would be appreciated. Many Thanks, John.

Hi, Could I ask for some advice on how we should handle the following situation, that has recently cropped up. This problem started we believe way back in 2011, we went to the car phone warehouse to change a telephone that we had on contract with Orange. We were told that since Orange no longer supplied mobile phone services the mobile would be registered with EE the new Orange provider. We changed the telephone over and the assistant at car phone warehouse confirmed with Orange/EE that the old contract was now cancelled. Then some months later Orange sent us a bill for 3 months connection charges for the old telephone, we spoke to Orange a few times by telephone and they finally agreed to sort the account out and remove the charge since we no longer had that telephone. We then moved address, although both me and my partner still had EE phones so EE had full information of all of the addresses we had occupied. Now in 2017 my partner attempted to get a small item on credit and were shocked to find out that she had some sort of issue on her credit file, when we look at her credit record on a free credit database service, we were shocked to see that Orange had somehow and for some reason registered a debt of £125 against my partner causing issues on getting credit. we may need to get a small mortgage soon so we were really concerned about this. we have called EE and they quickly passed us over to Orange (although they are supposed to be the same company we thought) The Orange contact we were given was an email only service. The initial response we got back from them once we had highlighted it was that they could not find anything on their system to do with our account. Also EE had said they could not see anything in their records pertaining to this debt. We emailed Orange a second time and told them to look harder since it appeared that Clear score had something registered against my partner for, a mobile phone issue. after taking her d.o.b etc they looked again and this time they found something but could not be specific about when it occurred? At first they telephoned my partner and said said the issue occurred in 2011, at an address which we did live at in 2011, then when she advised them that we did not owe the money since it was from an old mobile that had been transferred by them to EE, and that the debt should have expired anyway since it was 6 years ago. The person at Orange then emailed her to inform her that the issue occurred in 2014 (he had appeared to change his mind?) but that the address it occurred at was the old address (we did not reside at this address in 2014). they advised us that they could do nothing about the issue and that we would have to speak to EE customer service, we again spoke to EE customer service who again told us they could do nothing since it was with Orange Credit team ?? We emailed the Orange credit team yet again and they said that the debt had been passed to a DCA, and asked us if we had received any letters from said DCA (Arrow Global Limited). We advised EE that we were extremely disappointed and that we want them to escalate it, we have heard nothing yet and now we are considering what actions to take moving forward. We have not communicated with the DCA since we have no contract with them and don't want to put ourselves in any situation that means we are in contract with them. Could anyone give us some advice on how we could/should proceed with this. Any help would be appreciated. Many Thanks, John. -

For information Sussex Security Solutions Ltd have been struck of the register of companies as at 13 June 2017.

For information Sussex Security Solutions Ltd have been struck of the register of companies as at 13 June 2017. -

Hello, thanks for reading This matter relates to an old style loan of about 2k taken out in 1991/2 and consistently deferred until 2013, when I moved abroad to work (still earning under the threshold) and my deferral form went missing. I then forgot about it as got ill and depressed..(have medical evidence to back this up) Moved back to UK in 2014 and was unemployed for nearly a year.. so have never earned anything like the threshold limit. I also turned 50 in 2014 (am now 51) So, the long and short of it is, Student Loan Co wrote saying I was in arrears, then threatenign court action. . Now it has been passed to solicitors and a case has been opend at County Court I may have forgotten one deferrment form and defnitely sent one that they claim they never got. . But in any case, I turned 50 wouldnt the debt be wiped? And if I can prove I have never earned above the threshold, will they still have a case against me? How do I defend it? Is it now statute barred ? or has deferring it (until 2013, they claim was the last deferral) meant that it is no longer under the limitations act? I'd welcome your advice, have acknowledged service of court docs, giving myself 28 days to prepare to defend Abby

Hello, thanks for reading This matter relates to an old style loan of about 2k taken out in 1991/2 and consistently deferred until 2013, when I moved abroad to work (still earning under the threshold) and my deferral form went missing. I then forgot about it as got ill and depressed..(have medical evidence to back this up) Moved back to UK in 2014 and was unemployed for nearly a year.. so have never earned anything like the threshold limit. I also turned 50 in 2014 (am now 51) So, the long and short of it is, Student Loan Co wrote saying I was in arrears, then threatenign court action. . Now it has been passed to solicitors and a case has been opend at County Court I may have forgotten one deferrment form and defnitely sent one that they claim they never got. . But in any case, I turned 50 wouldnt the debt be wiped? And if I can prove I have never earned above the threshold, will they still have a case against me? How do I defend it? Is it now statute barred ? or has deferring it (until 2013, they claim was the last deferral) meant that it is no longer under the limitations act? I'd welcome your advice, have acknowledged service of court docs, giving myself 28 days to prepare to defend Abby