Search the Community

Showing results for tags 'lloyds bank'.

-

I opened an account in 2007 with Lloyds bank whilst I was 16 years old and living in the south of the country with my girlfriend at the time. I then moved back to the north of the country but did not change my home address and all my mail was withheld from me for about a year. I had gone overdrawn on my account by £5.40 and did not know of this because my mail was being withheld and had no cause for concern. (I should have changed my address). September 2008 I received a letter from Lloyds TSB demanding I pay £479.03 of the £679.03 balance in full in a couple of weeks. Due to my financial situation I was unable to pay. In October 2008 I received a letter from a solicitors demanding that I pay the full amount £686.69 outstanding balance. They also state in the letter that if the payment was not paid in full I would receive a CCJ, which inevitably happened. I chose to bury my head in the sand at this point only being young and unable to make such a massive payment upfront. Later in January 2015 I set up a repayment plan of £5 a week to Lowel and managed to get the outstanding balance of £767.72 down to £162.72 thus paying £605. On my credit report it states that I have had a CCJ. What I am wondering is, what is the likelihood of reclaiming these charges? What steps do I need to take to reclaim? Will the CCJ be attached to my credit history permanently? Any other advise would be most appreciated.

-

Hello all, I have received a claim from 1st Credit in regards to an alleged Lloyds TSB Loan. Unfortunately the claim form came whilst I was on Holiday and so I have missed the date in which to respond. As advised by your Set Aside section, I have contacted both the court, and their representative. Whilst it bugs me to pay the Application fee (as I had no chance to respond) I want to still defend this. So any advice will be appreciated. Just to advise, I have not sent any letters as of yet, however, I did a SARs a year or so ago and so have a lot of paperwork that may be helpful. Name of claimant: 1st Credit (Finance) Ltd. Date of issue: 03 Aug 2016 Date of acknowledgement was the 22nd, I never seen the letter until the 25th and logged straight into acknowledge but judgement had already be served (23rd). What is the claim: The claimant is the assignee of a Lloyds Bank PLC debt in the sum of xxxx assigned on the xx/11/15. The statutory notices were sent to the defendant. The debt is a loan account first opened by the original creditor on or about xx/xx/2010 under the reference xxxxx. The defendant used the credit facilities. On the xx/xx/2012 the account defaulted with an outstanding balance of xxxx. The claimant and its predecessors in title demanded repayment of the sum due. In breach of contract the defendant failed to repay the sums due. What is the value of the claim? around 9,000 including their costs and fees. Claim is for Loan and was entered into after 2007 It has been assigned and it is the 1st credit issuing the claim. I received a chasing letter from 1st credit advising that the debt had been assigned with a copy of an suspect notice of assignment from Lloyds TSB. The reason I say it is suspect is that the address has extra letters in, which are then replicated on the 1st Credit Letter - almost as it had been printed from the same details. These letter have never been on any letters from Lloyds. Did you receive a Default Notice from the original creditor: Not that I can recall, I know I never received the annual letters for two years of so. Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? I think these maybe the letters I refer to above. I never received for two years then they were sent. I do not have the date they were last sent but I can find out. Why did you cease payments? Serious debt issues, I lost job, and then went self employed, then had a knee operation. What was the date of your last payment? Nov 2011 Was there a dispute with the original creditor that remains unresolved? No I advised Lloyds numerous times I was struggling and in financial difficulties, but they kept hitting me with charges. Late payment, charges, then taking money from my overdraft, taking me over my planned O/D resulting in more charges. What you need to do now. I have a copy of the CCA - however, I am not sure on what information I should receive as part of this req I will Send a CPR31.14 request to the solicitor named on the claim form for copies of documents mentioned/implied within the claim form. Request 1 - Loans/Credit Cards Thanks in advance

Hello all, I have received a claim from 1st Credit in regards to an alleged Lloyds TSB Loan. Unfortunately the claim form came whilst I was on Holiday and so I have missed the date in which to respond. As advised by your Set Aside section, I have contacted both the court, and their representative. Whilst it bugs me to pay the Application fee (as I had no chance to respond) I want to still defend this. So any advice will be appreciated. Just to advise, I have not sent any letters as of yet, however, I did a SARs a year or so ago and so have a lot of paperwork that may be helpful. Name of claimant: 1st Credit (Finance) Ltd. Date of issue: 03 Aug 2016 Date of acknowledgement was the 22nd, I never seen the letter until the 25th and logged straight into acknowledge but judgement had already be served (23rd). What is the claim: The claimant is the assignee of a Lloyds Bank PLC debt in the sum of xxxx assigned on the xx/11/15. The statutory notices were sent to the defendant. The debt is a loan account first opened by the original creditor on or about xx/xx/2010 under the reference xxxxx. The defendant used the credit facilities. On the xx/xx/2012 the account defaulted with an outstanding balance of xxxx. The claimant and its predecessors in title demanded repayment of the sum due. In breach of contract the defendant failed to repay the sums due. What is the value of the claim? around 9,000 including their costs and fees. Claim is for Loan and was entered into after 2007 It has been assigned and it is the 1st credit issuing the claim. I received a chasing letter from 1st credit advising that the debt had been assigned with a copy of an suspect notice of assignment from Lloyds TSB. The reason I say it is suspect is that the address has extra letters in, which are then replicated on the 1st Credit Letter - almost as it had been printed from the same details. These letter have never been on any letters from Lloyds. Did you receive a Default Notice from the original creditor: Not that I can recall, I know I never received the annual letters for two years of so. Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? I think these maybe the letters I refer to above. I never received for two years then they were sent. I do not have the date they were last sent but I can find out. Why did you cease payments? Serious debt issues, I lost job, and then went self employed, then had a knee operation. What was the date of your last payment? Nov 2011 Was there a dispute with the original creditor that remains unresolved? No I advised Lloyds numerous times I was struggling and in financial difficulties, but they kept hitting me with charges. Late payment, charges, then taking money from my overdraft, taking me over my planned O/D resulting in more charges. What you need to do now. I have a copy of the CCA - however, I am not sure on what information I should receive as part of this req I will Send a CPR31.14 request to the solicitor named on the claim form for copies of documents mentioned/implied within the claim form. Request 1 - Loans/Credit Cards Thanks in advance -

I have just received a letter from Mortimer Clarke stating that they act on behalf of their client Marlin Europe II Limited asking for details of my financial circumstances for a debt that they say a county court claim was issued on April 2014. It also has a claim number at the top of the letter and if I don't respond they will lift the stay and request Judgement. I have never had any claim form for this debt and I have logged on to MCOL and there is nothing on there with that claim number. I also went on to my credit file and it says the debt they are talking about is with Cabot for a different amount. I'm not sure what to do.

I have just received a letter from Mortimer Clarke stating that they act on behalf of their client Marlin Europe II Limited asking for details of my financial circumstances for a debt that they say a county court claim was issued on April 2014. It also has a claim number at the top of the letter and if I don't respond they will lift the stay and request Judgement. I have never had any claim form for this debt and I have logged on to MCOL and there is nothing on there with that claim number. I also went on to my credit file and it says the debt they are talking about is with Cabot for a different amount. I'm not sure what to do. -

I'll try to cut a long story short. Yesterday a good friend with own business wanted cash to buy car today. No time to go to bank due to work pressure, so online transferred £7000 to me. I rang Lloyds to make sure ok to withdraw £7000 and they said yes with my id. I went to branch with my driving licence to withdraw cash. Computer said "no". Branch official needed paper statement from my friend. Friend and I met at branch around 4.15pm. Friend had brought statement showing online transfer but bank wanted actual bank statement. Friend and I walk to his Barclays bank to get statement but he'd left his bank card at home (10 miles away). They couldn't help him get a statement without bank card!!! Back to Lloyds. Offered to show clerk phone statement but not good enough as she wanted paper receipt. Couldn't offer us internet access to print it out. Branch closed at 5pm. Back to my house to online transfer £7000 back to friend. Computer said "no" again I rang enquiry line. Several questions later (which I correctly answered) I was told go back to branch with photo id in order to allow transaction to go through!!! Tried logging onto internet banking to check my statement and it's been frozen. Rang enquiry line and was told go to branch with photo id!!! Branch closed today (Good Friday). So car sale fallen through for friend. The two of us will turn up tomorrow at my branch so wish me luck

-

PRA DCA Lloyds card Debt -they say un-en but now issued LBA

Brunowales posted a topic in Lloyds Bank

Hi Can someone please advise on whether a DCA can reconstitute a CCA and DN for a credit card taken out in 1999 and if they can use it to enforce in court. Many Thanks -

I have two cases with LTSB which are quite complex so please bear with me. Case 1: LTSB credit card debt pre 2007 - CCJ obtained by defaul at Northampton in 2011. I intially defended and it went to a full hearing which I couldn't attend due to family issues and my ental state at the time. They sent some big-time lawyer to the case which added £4K to the CCJ bringing it to near £19K with no interest payable. Got a variation order and have been paying £50 a month since 2012 without missing a month. Debt now approx £16.5K. I got a leteer last week from Lloyds saying they are passing the debt on to Moorcroft to collect. Why would they do that? It's not like I'm going to pay Moorcroft over a Court order? I'll obviously ignore Moorcrap, but am wondering what Lloyds are doing here? this CCJ dosen't show on ANY of my credit files or trustonline but does exist - I phoned the relevant court to see if there's been any movement on the CCJ and there hasn't. LTSB contacted me back in 2014 to tell me that their solicitor has been changed and that the court has been infomed. Well the court knew nothing about that when I phoned them a couple of weeks back so wonder if I can use that in some way? Case 2 Loan with LTSB - CCJ obtained 2011 - not defended as post 2007 - going through a bad time as above. Had the CCJ varied to pay £25 per month which I've paid without fail since. Got a letter from Asset Link in early July this year saying that they have bought the debt from Lloyds. In the same envelope was a letter from Lloyds saying the same thing. Contacted the court [Northampton] to see if there was any movement and they said no, everything was the same as 2011. Well, on a whim a couple of weeks ago, I phoned them back again and was told that the claimant was now Asset Link and had been since 2011 I was on the phone for over an hour with this guy telling me that I had obviously made a mistake and that LTSB were NEVER claimants. Finally he found a note on the file which was a bulk order from a judge changing the claimant from LTSB to Asset Link on a lot of accounts - not just mine. If I hadn't contacted the court, I would have known nothing about this - surely some CPR has been broken here? I have also contacted Asset Link asking for the original credit agreement from LTSB and the current statement of my account. They replied saying it would take them up to 30 days to get the info - it's been over 50 days now so it looks like they don't have it. Their solicitors have also contacted me telling me it's important to keep up my regular payments to the new claimant. I'm sorely tempted to just give up on these two debts. The total is just over £20K and even paying £75 a month as I have been, will take me over 20 years to pay. I'm self employed on low income, don't drive and have little in the way of assets for bailiffs to seize and I rent my home - so in all honesty, what have I got to lose? If you need any letters posted up, just let me know. Thanks for reading and I appreciate any help and advice you give.

-

Have you ever tried to make a subject access request to Lloyds bank and been told that they don't keep data longer than six years? Well basically it's a lie – but you wouldn't expect anything else from Lloyds bank. They use an archiving service in Andover and you can get data going back at least 2001. Their address is: – DSAR Unit Lloyds TSB Customer Service recovery Charlton Place C46 Andover SP10 1RE And they even have a telephone number: – 0345 0707124 Although I don't know whether people are prepared to speak to you. Apparently the same archiving service is used to store data relating to TSB, Lloyds TSB, RSP, Halifax Bank of Scotland. In other words all the usual suspects who have ripped you off over the years and then try to obstruct you from getting a full data disclosure. You should still contact their head offices or your branch for your data disclosure, but when they come back to you and say that there is only six years then that is the time to start objecting and to make complaints to the information Commissioner. You can make an SAR request directly to the data centre as well, of course.

Have you ever tried to make a subject access request to Lloyds bank and been told that they don't keep data longer than six years? Well basically it's a lie – but you wouldn't expect anything else from Lloyds bank. They use an archiving service in Andover and you can get data going back at least 2001. Their address is: – DSAR Unit Lloyds TSB Customer Service recovery Charlton Place C46 Andover SP10 1RE And they even have a telephone number: – 0345 0707124 Although I don't know whether people are prepared to speak to you. Apparently the same archiving service is used to store data relating to TSB, Lloyds TSB, RSP, Halifax Bank of Scotland. In other words all the usual suspects who have ripped you off over the years and then try to obstruct you from getting a full data disclosure. You should still contact their head offices or your branch for your data disclosure, but when they come back to you and say that there is only six years then that is the time to start objecting and to make complaints to the information Commissioner. You can make an SAR request directly to the data centre as well, of course. -

Hello, ive got a claim against me from cabot for an alledged debt on a credit card. Ive done the acknowledgment on mcol, sent off the cca and cpr etc. this is my defence, is this ok to go onto mcol please. letter from court dated 17/01/2017. acknowledged on mcol on 24/01/2017. needs defence by 18/02/2017?? Actual particulars on letter are…. The claimant claims payment of the overdue balance due form the defendant under a contract between the defendant and Lloyds, dated on or around 06/12/2002 and assigned to the claimant on 24/06/2016. Particulars….is then gives an account number. Particulars of Claim 1.The claimant claims payment of the overdue balance due from the Defendant under a contract between the defendant and Lloyds bank dated on or about 06/12/2002 2. The defendant did not pay the instalments as they fell due & the agreement was terminated. 3. And apparently its been assigned to the claimant, for the sum of 4282.90 with possible court costs = £xxxx.00. Defence The Defendant contends that the particulars of claim are vague and generic in nature. The Defendant accordingly sets out its case below and relies on CPR r 16.5 (3) in relation to any particular allegation to which a specific response has not been made. 1.Paragraph 1 is accepted. in that I have, in the past, entered into an agreement with Lloyds Bank, however I do not recall the exact details, as it is over 15 years ago, I have requested the claimant verify the exact details of this claim by way of a CPR 31.14. The claimant has refused to provide me with a copy of the agreement, stating they are not obligated to do so by virtue of the consumer credit Act 1974. 2.The Claimant alleges that I the Defendant did not pay the instalments as they fell due. The claimant is put to strict proof to evidence such breach by way of a Default Notice pursuant to CCA1974 section 87 (1) 3. Paragraph 3 is denied. I am unaware of any legal assignment or Notice of Assignment allegedly served pursuant to the Law of Property Act and Section 82A of the consumer credit Act 1974. The Claimant has yet to provide a copy of the Notice of Assignment its claim relies upon. On the 26/01/2017 I made a legal request by way of a section of a CPR 31:14 request to the Claimant. The Claimant has failed to comply to this date, no statement of the alleged account has been received. The claimant has failed to provide any evidence of agreement/contract/breach as requested by CPR 31.14 and a Section 78 request and therefore is in default of this request and as such unable to enforce this agreement or request any relief until compliance. Therefore the Claimant is put to strict proof to: (a) show how the Defendant has entered into an agreement/contract; and (b) show how the Defendant has reached the amount claimed for; and © show and evidence the nature of breach and service of a Default Notice; (d) show how the Claimant has the legal right, either under statute or equity to issue a claim. 5. As per Civil Procedure Rule 16.5(4), it is expected that the Claimant prove the allegation that the money is owed. 6. As the Claimant is an assignee of a debt, it is denied that the Claimant has the right to lay a claim due to contraventions of Section 136 of the Law of Property Act and Section 82A of the consumer credit Act 1974. 7. By reason of the facts and matters set out above, it is denied that the Claimant is entitled to the money claimed.

-

hi everyone , I received a letter this morning from Lloyds "Jaimie graham director ,collections,and recoveries " the letter stated that Lloyds were passing my debt to a debt collection agency "Moorcroft group plc "they have instructed Moorcroft to contact me, to enable me to make future payments to them , I have been paying the debt back, £1:00 every month since before june 2013 as that was the information I was given to do by the national debt helpline, they said that as long as I,m paying something there is nothing they can do. what to do ? if moorcoft get in touch can I tell them to go away in army language or be polite l.o.l.??. can I ask for the original agreement ?? help on this would be great. thanks

-

Hi, First post so please be gentle I recently made a claim for PPI for an old Lloyds Credit Card that ran from 2006 - 2008. I did it all via initially the telephone and then using the standard PPI reclaim form. My reasoning for the reclaim was the firstly I was entitled to Full-Pay SSP and also I have type-1 Diabetes so it's unlikely the PPI would have been relevant to me, none of which was explained at the point of the CC application. Lloyds have now said they have upheld the complaint but the figures are extremely weird. I've attached the refund letter but they are stating I only had 0.01p of PPI which I find hard to believe and they are refunding me £298 or so. I didn't request a SAR but now I'm thinking I probably should to work out if what they are saying is correct. Also they've said they'll pay the amount within 28 days, I assume I can still contest this even after they've deposited the money into my account. Thanks!

-

Hi everyone, haven't been on here for a while but wondered if anyone could lend an ear to this; I defaulted on a Lloyds Credit Card 3 years ago; it was linked to my bank account and I have never tried to hide my address from Lloyds, and still use the current account. I became a student again for a while and didn't hear anything about the card, until recently when I became aware that Cabot were chasing me at an old address. I've since received a forwarded letter sent to my old address from Shoosmiths, giving me 14 days to reach settlement before taking action, but the 14 days had expired by the time I received the letter. I have now asked for all letters to my old address to be forwarded to me. I would actually like to sort out the debt and reach a full and final settlement, and really don't want to get the CCJ; I wrote to Cabot and asked them to write to me at my new address; which they should have been supplied by the OC anyway, and have heard nothing. What is the general opinion on this; should I try and CCA Cabot now, or wait for the CCJ and apply to have it struck out? I don't want to confuse things further, but do want it sorted.

Hi everyone, haven't been on here for a while but wondered if anyone could lend an ear to this; I defaulted on a Lloyds Credit Card 3 years ago; it was linked to my bank account and I have never tried to hide my address from Lloyds, and still use the current account. I became a student again for a while and didn't hear anything about the card, until recently when I became aware that Cabot were chasing me at an old address. I've since received a forwarded letter sent to my old address from Shoosmiths, giving me 14 days to reach settlement before taking action, but the 14 days had expired by the time I received the letter. I have now asked for all letters to my old address to be forwarded to me. I would actually like to sort out the debt and reach a full and final settlement, and really don't want to get the CCJ; I wrote to Cabot and asked them to write to me at my new address; which they should have been supplied by the OC anyway, and have heard nothing. What is the general opinion on this; should I try and CCA Cabot now, or wait for the CCJ and apply to have it struck out? I don't want to confuse things further, but do want it sorted. -

Millions of people who have basic bank accounts may be paying higher fees than necessary.. Basic bank accounts are designed for people who do not already have a bank account and are ineligible for a standard current account .While eight million people have basic accounts, around half of them are still liable to pay fees for failed payments. Completely fee-free basic accounts have been available since January 2016, following an industry agreement. Vulnerable customers who have such accounts are not charged for failed payments, or for going overdrawn. The Treasury figures show that 3.7 million people have accounts that do not conform to the agreement, struck between the government and the banking industry, in 2014. Of those, 3.6 million bank with Lloyds, the rest being RBS customers All the other seven big High Street banks do not charge fees for basic account customers http://www.bbc.co.uk/news/business-38289654

-

http://www.thisismoney.co.uk/money/saving/article-2895425/Lloyds-life-misery-insisting-DEAD.html

http://www.thisismoney.co.uk/money/saving/article-2895425/Lloyds-life-misery-insisting-DEAD.html -

Evening all. I've been away from the forums a while, busy getting on with life but a few recent events have brought me back. Thanks largely to this site I have been able to get my debts largely under control, dealt with or paid off. Advice and information supplied on here has not only helped me claim money back, compensation and in some cases get debts written off but most of all it has given me a bedrock of confidence when dealing with the sharks, and conmen that work in this field. That said having felt like I'd largely dealt with my debt problem for these recent events to occur is more than a little annoying and upsetting. This thread may take some typing but please stick with it. I'm also looking for advice but also just trying to understand the legalities. Now Firstly, I have read around various threads covering selling CCJ debts etc but I have to honestly say I've struggled to fully comprehend the situation. here's my most recent story. in amongst the many financial issues I encountered during the crash of circa 2008 were 2 debts to LLoyds. One for a credit card and one a personal loan. In late 2010 and then early 2011 LLoyds secured CCJ's on these debts (yes I didn't challenge and over the years have wished I'd found this site much earlier (. the CCJ's were awarded and relatively nominal payments set £1.00 on the 2k credit card debt and £50.00 a month on the 15K loan. All interest was stopped.) Lloyds then secured what I thought was a CO on my house but now understand is a restriction as the house is jointly owned with my ex wife. So for years I was making payments and then as my situation improved I made additional payments and all seemed well until firstly last month I get a letter from Lloyds and a company called Asset Link Capital saying they have sold my account with the balance blah blah. so far heard no more even though they indicated in the letters that I would hear from a solicitor if the account is subject to a ccj or CO (it is only subject to CCJ). Now this week I've had a letter from 'LLOYDS' (though the return address, surprise surprise, is Moorcroft) telling me they have transferred (notice doesn't say sold) the other debt to Moorcroft. This account is subject to a CCJ and also the CO/restriction. Oddly the balance they claim to have transferred is some £373 higher than the balance they told me was on the account @ 24/06/2016, if add in payments made since it is probably 673 higher. So far no attempt has been made to ask for higher payments but I cannot imagine there is any other motive. my questions are firstly can they demand more without returning to the court? If they do try to go through the court can I request the matter is transferred to a local court as I am disadvantaged by it being impractical for me to attend a court hundreds of miles away? Also can they actually sell an account like this? It almost feels like as these CCJ's are about to drop of my file (one in October and one in January) that they have decided to stress and pressure me again. If I'd never found this site I'd probably be a wreck now after receiving these letters. So guys, any thoughts, either specific to my cases or just generally about the wonderful way creditors and DCA's treat people?

-

Hi CAG, thanks for taking the time to read this. I'll keep it snappy. I recently worked for Lloyds bank but left on 20th June 2016 because I emigrated to Spain, where I now live. I had worked at Lloyds for 6 years. This past weekend (29th October 16) I went back to my old UK address to pick up my post and discovered that at the end of July Lloyds sent a letter informing me they had erroneously paid me my 2015 deferred bonus, and a second letter dated 24th October, stating my 'debt' has been passed on to DrydensFairfax solicitors. The bonus in question was £10k after tax, based on my 2015 performance. £2k was paid on March 20th with the remaining payable £8k on June 20th. The 2k march payment is not disputed, but they want the £8k back I was aware of the deferral system and after discussions with my boss (who i had a great relationship with) delayed my resignation until March 20th, which we both thought was the cut of date, meaning I would mean i would pick up my full bonus on June 20th - my last day as I was on 3 months notice, which I did. I have since checked the small print on one of my letters and it did indeed stipulate that if you are serving your notice period on 1st June 16 you are not entitled to the remainder of the 2015 bonus. So it appears me and my boss were indeed wrong about the date you needed to be not serving notice on to receive the second installment of the bonus, and lloyds made a mistake when they paid it to me. From what I've read this seems to fit the criteria for Estoppel. Discussion with my manager led me to believe this money was mine if i resigned on March 20th, and I have since spent the money (and quote a bit more!) on emigration. If i'm right, then I don't know how to put this in motion. I've not replied to anything yet. I have not had any calls or messages from DrydensFairfax directly, just 2 letters from Lloyds, with the second one asking me to contact drydens to payback the £8k I don't really want to do nothing and risk a court order of black mark on my credit record Thanks again for reading. Any help/advice/thoughts would be hugely appreciated Nick

Hi CAG, thanks for taking the time to read this. I'll keep it snappy. I recently worked for Lloyds bank but left on 20th June 2016 because I emigrated to Spain, where I now live. I had worked at Lloyds for 6 years. This past weekend (29th October 16) I went back to my old UK address to pick up my post and discovered that at the end of July Lloyds sent a letter informing me they had erroneously paid me my 2015 deferred bonus, and a second letter dated 24th October, stating my 'debt' has been passed on to DrydensFairfax solicitors. The bonus in question was £10k after tax, based on my 2015 performance. £2k was paid on March 20th with the remaining payable £8k on June 20th. The 2k march payment is not disputed, but they want the £8k back I was aware of the deferral system and after discussions with my boss (who i had a great relationship with) delayed my resignation until March 20th, which we both thought was the cut of date, meaning I would mean i would pick up my full bonus on June 20th - my last day as I was on 3 months notice, which I did. I have since checked the small print on one of my letters and it did indeed stipulate that if you are serving your notice period on 1st June 16 you are not entitled to the remainder of the 2015 bonus. So it appears me and my boss were indeed wrong about the date you needed to be not serving notice on to receive the second installment of the bonus, and lloyds made a mistake when they paid it to me. From what I've read this seems to fit the criteria for Estoppel. Discussion with my manager led me to believe this money was mine if i resigned on March 20th, and I have since spent the money (and quote a bit more!) on emigration. If i'm right, then I don't know how to put this in motion. I've not replied to anything yet. I have not had any calls or messages from DrydensFairfax directly, just 2 letters from Lloyds, with the second one asking me to contact drydens to payback the £8k I don't really want to do nothing and risk a court order of black mark on my credit record Thanks again for reading. Any help/advice/thoughts would be hugely appreciated Nick -

Hi on 30th August 2016 I received a letter from Lloyds Bank, signed by Jamie Graham informing me Lloyds have transferred my outstanding credit card debt to Moorcroft and they have instructed them to contact me. I defaulted on my credit card debt with Lloyds 7 years ago and for 6 years 6 months I have been paying £10.00 a month direct to Lloyds Bank. Today I received a letter from Moorcroft (signed by A.J. Martin) telling me that despite fact earlier this week I paid Moorcroft the monthly £10.00 unless I contact Moorcroft within 7 days they will 'recommence collection activity if we cannot agree a repayment plan that you can afford and maintain.' I cannot afford to pay more than £10 a month and have paid this amount to Lloyds - the debtors for over six years now. I feel Moorcroft are using intimidation tactics in order to get me to contact them. I checked my credit rating with Noddle and note this credit card debt is no longer showing so it must be over 6 years old. Any advice would be much appreciated. Hecuba

-

name of the claimant ? pra group (uk) limited date of issue – 05 sept 2016 AOS done 7th sept .filing the defence? by 4pm Friday 7th October what is the claim for – the reason they have issued the claim? 1. the claimant claims the sum of £1900 for debt and interest. 2.on 0i/12/89 the defendant entered into an agreement with lloyds for an overdraft under reference (here is bank sortcode and account number). 3.on 03/11/09 the defendant defaulted on the agreement with an outstanding balance of £1500. 4.on 24/06/13 the debt of £1500 assigned to aktiv kapital portfolio as, oslo zug branch who itself assigned the debt to pra group (uk) ltd 5.on 31/12/14. notices of assignment were sent to the defendant in accordance with s136 law of property act 1925. payments of £10 received up to 17/07/13 and the claimant claims 1. the sum of £1500 2. statutory interest pursuant to section 69 of the county courts act 1984 at a rate of 8% per annum from 17/07/13 to 02/09/16 £376.33 and thereafter at a daily rate of 0.33 until judgement or sooner payment. what is the value of the claim? £2,070.00 is the claim for a current account (overdraft) or credit/loan account or mobile phone account? current account (overdraft) when did you enter into the original agreement before or after 2007? before has the claim been issued by the original creditor or was the account assigned and it is the debt purchaser who has issued the claim. PRA GROUP were you aware the account had been assigned – did you receive a notice of assignment? no did you receive a default notice from the original creditor? dont know was in psychiatric hospital have you been receiving statutory notices headed “notice of default sums” – at least once a year ? no why did you cease payments? originally in 2009 i lost my job due to mental illness and could not repay my overdraft. a repayment plan was subsequently agreed with lloyds of £5 a month as i was unable to work (still ill) what was the date of your last payment? july 2013.i maintained the repayments to that date after that i continued to try to make the repayments by standing order but the payments were returned. was there a dispute with the original creditor that remains unresolved? no did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? yes. details provided and monthly repayments agreed and always made until they started being returned to account. if you have not already done so – send a cca request to the claimant for a copy of your agreement (except for overdraft/ mobile/telephone accounts) i have not done this as claim relates to overdraft. is this right? Send a CPR31.14 request to the solicitor named on the claim form for copies of documents mentioned/implied within the claim form. There are two different versions - one for Loans/Credit cards the other for Current accounts Request 1 - Loans/Credit Cards Request 2 - Current accounts i have read this and adapted it as best i can and will post it registered delivery tomorrow. i am new to this site. i have received a claim form from pra group for an overdraft with lloyds that i had when i had a breakdown in 2009 and was taken into hospital and lost my job. was making payments to lloyds of £5 per month from dec 2009 to july 2013 after that the standing orders were returned to me by lloyds. i also had a loan with lloyds and that was transferred to different debt purchaser and i continued to make repayments on that to date. so no i didnt know the overdraft debt had been transferred. i did not receive notice. i have read the guidelines on posting and i hope i am complying with them. any help at all on dealing with this claim would be very much appreciated. i have read that there are posts on the legal success forum that will help draft a defence. i .looking through this now. have i done the right things so far please. sorry about the caps. its.just that red font isnt coming up. i am trying to make my answers stand out for ease of reading

-

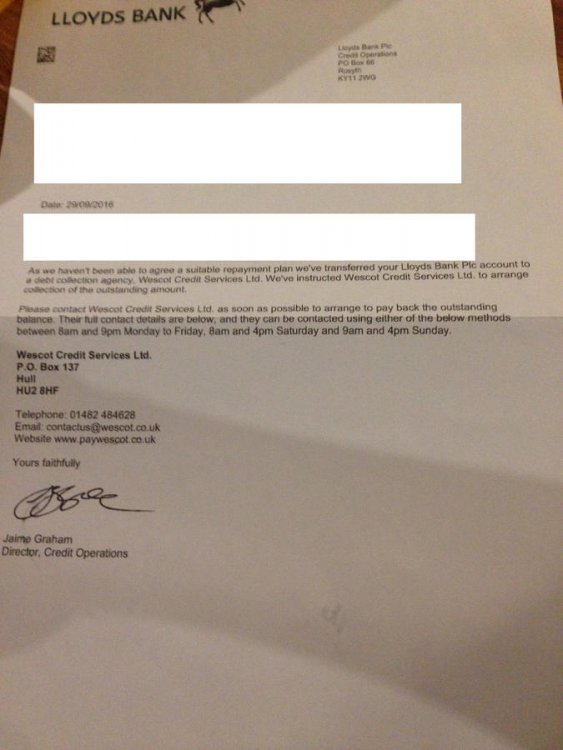

Hi, I am looking for some advice, I received the attached letter from Westcot and/or Lloyds in regards to an outstanding debt of just under £1000.00 I have in the past had a Lloyds credit card (at least over 4 years ago) and do not possess the statements or the card anymore. I do not recall leaving any outstanding debt on the card. I also received letters a few months ago from Moorcroft chasing this debt which I ignored as I thought it was fraudulent. I have not received any contact from Lloyds in regards to this debt, would they not contact me first? I am concerned this will ruin my credit rating but I am not even sure that I owe any debt… What would be the best course of action from here? Thanks

-

Hi there, not been on here for a long while. Have had a letter out of the blue from Lowell on a Lloyds credit card account that was defaulted in October 2010. Obviously this is about to drop off my history but obviously as they've renewed their interest in me I'm wondering my next move. Their reason for contacting me was to offer me a discount of 75%, now this obviously smells to me of them not having a prescribed agreement (the card was taken out pre 2007). I've had a look through my papers and it seems that for some reason I have never claimed charges on this account. Now I can obviously type up a CCA to see what they have, as I said it has been a while so on top of the actual signed agreement what else should I expect? With regards to sending a SAR am I still able to claim charges this far back? Any links to templates would be gratefully received! (I'm a bit rusty in here) Thanks in advance...

-

Lloyds Bank Old debt on closed current accounts advice

Jaffa__ posted a topic in General Debt Issues

Hi I have 2 debts with Lloyds both managed by Apex but now owned by Cabot The debts are for £4K and £10K they are 8 years old and are for closed current accounts. I pay £1 pm I was originally in £60K of debt with various lenders but have brought it down over the years with Partial settlements, My 2 Questions are Q1; I do not remember a £10K current account debt and have asked for a copy of the original contract on both accounts, they have replied by saying they will send me a statement but do NOT need to send a copy of my signature as its a current account and not a loan... is this correct?? Q2; Assuming due to age the debt it is no longer on my credit file what % is usually acceptable for a partial settlement? Thanks -

Hi, I had a default with Lloyds TSB a few years back, which Lowell took over. A few days ago I received a letter through the post from court saying Lowell want this debt paid and I have 14 days to respond. The original debt was made up of charges (because of an unplanned overdraft), The total amount owed is around £1400 and I just refused to pay it and buried my head. Is there anything I can do about this now or should I just accept and pay it in installments? Really don't want a CCJ. Thanks

Hi, I had a default with Lloyds TSB a few years back, which Lowell took over. A few days ago I received a letter through the post from court saying Lowell want this debt paid and I have 14 days to respond. The original debt was made up of charges (because of an unplanned overdraft), The total amount owed is around £1400 and I just refused to pay it and buried my head. Is there anything I can do about this now or should I just accept and pay it in installments? Really don't want a CCJ. Thanks -

hi everyone just trying to sort my debt mess out at the moment to be honest I'm struggling to keep up with things and seem to think of nothing else every day just trying not to let it crush me. Ok hear goes, had a letter from LLoyds saying they passed my debt on to Marlin Financial Services ( Debt is a current account over draft for £5000 this was at the height of my debt problems and the over draft started at £2000 and I applied online for extra overdraft and was granted each time until it reached £5000). Then yesterday had a letter from Marlin saying they now had the debt and I have 5 days to reply to them and fill in a debt planner? There has been nothing paid on the account for 5 years as every month there was high charges and interest on the account, I went in to the branch and told them I was struggling to pay this back as the charges were height and I had money problems, I was given the phone and I spoke to someone from LLoyds in India ?? And they said they would put all charges and interest on hold for 6 months and then review thing which I agreed but the following month I got the same charges on the account so went back again and sat with the same woman and she put me on the phone to India again and this time they said that nothing had been put down that an agreement had been made and I must make the payment to the account??? This is where i stopped paying and changed accounts. Sorry it's long winded but trying to give you the full story. I have had a look around other threads and I think I need to send a SAR to LLoyds but what will I need to send to Marlin I'm a bit confused as this is an overdraft debt? Everyone here are great and all help is grateful and appreciated Thanks mw

hi everyone just trying to sort my debt mess out at the moment to be honest I'm struggling to keep up with things and seem to think of nothing else every day just trying not to let it crush me. Ok hear goes, had a letter from LLoyds saying they passed my debt on to Marlin Financial Services ( Debt is a current account over draft for £5000 this was at the height of my debt problems and the over draft started at £2000 and I applied online for extra overdraft and was granted each time until it reached £5000). Then yesterday had a letter from Marlin saying they now had the debt and I have 5 days to reply to them and fill in a debt planner? There has been nothing paid on the account for 5 years as every month there was high charges and interest on the account, I went in to the branch and told them I was struggling to pay this back as the charges were height and I had money problems, I was given the phone and I spoke to someone from LLoyds in India ?? And they said they would put all charges and interest on hold for 6 months and then review thing which I agreed but the following month I got the same charges on the account so went back again and sat with the same woman and she put me on the phone to India again and this time they said that nothing had been put down that an agreement had been made and I must make the payment to the account??? This is where i stopped paying and changed accounts. Sorry it's long winded but trying to give you the full story. I have had a look around other threads and I think I need to send a SAR to LLoyds but what will I need to send to Marlin I'm a bit confused as this is an overdraft debt? Everyone here are great and all help is grateful and appreciated Thanks mw -

I opened a Club Lloyds account prior to Xmas, primarily for the benefits it advertised. Under doctor’s orders, I am currently abroad to reduce my stress levels. I have a large sum of money in my account, and have been trying to use the time to move this to other accounts I have that it will earn interest on. Each time I try to make a transaction, either using online banking or via debit card, to other accounts in my name which are already set up with my online banking, Lloyds block them and make me call their Fraud Team. I am making the calls from abroad, I think the shortest call to date has been around 30 minutes, each time I am made to answer questions from my credit file and a trace is left on my file each time they make me do this. Yesterday, at circa 3pm, I tried for the second time to move a large sum to an account I hold with RCI bank, the payment, for the second time was blocked. The call time I made to the Fraud team was in excess of 1 hour. The end result of the call was that my account is totally blocked and Lloyds are forcing me to return to the UK to present myself and ID to a Lloyds branch before I can access my money. This is my normal day-to-day banking account which I can no longer access, check that payments are being made into it, or make ad hoc bill payments or move money. The guy I spoke to in the fraud team, his attitude towards me inflamed the situation, he refused to let me speak to a manager, pass the call to a manager, or get a manager to call me back. He lied to me and told me he would put me through to customer services to make a complaint, he didn’t he put me back into the long queue to wait again for the Fraud team. Directly after this, I called the Complaints team. again a long wait to speak to someone., before starting on a 2-hour call with them. After they liaised with Fraud I was told that there was no block on my online banking (with me accessing my account while they were still on the line to ensure this was the case) that all I had to do was call Fraud again to go through more credit file checks to get the payment authorised. The complaint I had changed from initially being about the block on my account and enforced return to the UK, to about the conduct and attitude with ....., the Fraud team member. I was offered compensation of £160 to cover the cost of in excess of 3 hours of international mobile calls. I did not accept this to close the complaint, I elevated the complaint to a higher level (.......), where we went over everything, double-checked everything, and it was left in his hands to investigate further while I was left to go through the rigmarole regarding my transfer with the Fraud team again. This whole scenario which started at 3pm, concluded with the termination of this call after 6pm. 9 am this morning I went online to check my bank account before getting up the courage to tackle another call with the Fraud dept…..my online access was blocked. The start of many phone calls was to the complaints department to speak to either of the two people from the day before, this was not possible and I was put into the ‘care’ of a lady called ..... informed me that my account was blocked and that I would have to return to the UK, etc, before it would be unblocked. To cut a long story short, she confirmed with me the address of 3 branches in Edinburgh that I could do so, with me informing her that I wanted to make face-to-face contact with the manager of the branch to address my issues, and that I would be pursing costs for flights, transfers, accom, time off work etc. She refused my request to speak with someone senior and she terminated the call with me. started to look at flights to find the first available one is not until next Saturday, a week away. started to try to get contact details for the branch so I could phone to ensure a manager would be there, to make sure they could do everything that had to be done (from their side and from mine), and to make an appointment. You would think this would be easy, but being Lloyds, no it is not… .there is only an 0845 no provided, extortionate to call from abroad, and I was forced to call the call center. On doing so I was informed that there are in fact no Lloyds branches in Scotland, that the branch we were looking at was a Bank of Scotland one, with no telephone number for customers, as are all branches apparently, that I cannot talk to anyone in branch directly and that if I wished to make contact I had to do it via an agent in the call center, who then tried to call it for me with no joy. This call terminated after 1pm today, another 4 hours of my life wasted.

I opened a Club Lloyds account prior to Xmas, primarily for the benefits it advertised. Under doctor’s orders, I am currently abroad to reduce my stress levels. I have a large sum of money in my account, and have been trying to use the time to move this to other accounts I have that it will earn interest on. Each time I try to make a transaction, either using online banking or via debit card, to other accounts in my name which are already set up with my online banking, Lloyds block them and make me call their Fraud Team. I am making the calls from abroad, I think the shortest call to date has been around 30 minutes, each time I am made to answer questions from my credit file and a trace is left on my file each time they make me do this. Yesterday, at circa 3pm, I tried for the second time to move a large sum to an account I hold with RCI bank, the payment, for the second time was blocked. The call time I made to the Fraud team was in excess of 1 hour. The end result of the call was that my account is totally blocked and Lloyds are forcing me to return to the UK to present myself and ID to a Lloyds branch before I can access my money. This is my normal day-to-day banking account which I can no longer access, check that payments are being made into it, or make ad hoc bill payments or move money. The guy I spoke to in the fraud team, his attitude towards me inflamed the situation, he refused to let me speak to a manager, pass the call to a manager, or get a manager to call me back. He lied to me and told me he would put me through to customer services to make a complaint, he didn’t he put me back into the long queue to wait again for the Fraud team. Directly after this, I called the Complaints team. again a long wait to speak to someone., before starting on a 2-hour call with them. After they liaised with Fraud I was told that there was no block on my online banking (with me accessing my account while they were still on the line to ensure this was the case) that all I had to do was call Fraud again to go through more credit file checks to get the payment authorised. The complaint I had changed from initially being about the block on my account and enforced return to the UK, to about the conduct and attitude with ....., the Fraud team member. I was offered compensation of £160 to cover the cost of in excess of 3 hours of international mobile calls. I did not accept this to close the complaint, I elevated the complaint to a higher level (.......), where we went over everything, double-checked everything, and it was left in his hands to investigate further while I was left to go through the rigmarole regarding my transfer with the Fraud team again. This whole scenario which started at 3pm, concluded with the termination of this call after 6pm. 9 am this morning I went online to check my bank account before getting up the courage to tackle another call with the Fraud dept…..my online access was blocked. The start of many phone calls was to the complaints department to speak to either of the two people from the day before, this was not possible and I was put into the ‘care’ of a lady called ..... informed me that my account was blocked and that I would have to return to the UK, etc, before it would be unblocked. To cut a long story short, she confirmed with me the address of 3 branches in Edinburgh that I could do so, with me informing her that I wanted to make face-to-face contact with the manager of the branch to address my issues, and that I would be pursing costs for flights, transfers, accom, time off work etc. She refused my request to speak with someone senior and she terminated the call with me. started to look at flights to find the first available one is not until next Saturday, a week away. started to try to get contact details for the branch so I could phone to ensure a manager would be there, to make sure they could do everything that had to be done (from their side and from mine), and to make an appointment. You would think this would be easy, but being Lloyds, no it is not… .there is only an 0845 no provided, extortionate to call from abroad, and I was forced to call the call center. On doing so I was informed that there are in fact no Lloyds branches in Scotland, that the branch we were looking at was a Bank of Scotland one, with no telephone number for customers, as are all branches apparently, that I cannot talk to anyone in branch directly and that if I wished to make contact I had to do it via an agent in the call center, who then tried to call it for me with no joy. This call terminated after 1pm today, another 4 hours of my life wasted. -

My OH's elderly parents received a letter advising that their Gold account is being downgraded. When my OH discussed this with her mum, she was unaware that she had been paying a monthly fee etc so possibly a case of mis-selling. The letter also stated that they were downgrading account due to 80 year old age limit, yet they are 85 & 87 years old and therefore a bit late in advising. Now my OH's dad suffers from dementia and her mum is not very well and when mentioned about submitting a complaint she felt that she couldn't go through with it. Obviously my OH and I are disgusted with Lloyds and tried to assure her that all will be kept in writing. Can my OH submit a SAR on their behalf and deal with the complaint ? Any advice would be appreciated including relevant Lloyds SAR address. Thank-you

-

Hi there......posting on behalf of my husband Historic credit card debt card held 30 years Got into problems in the last few years and transferred to Robinson Way Payment arrangement in place and PPI already claimed back from LLoyds 6 years ago No charges ever reclaimed on Credit Card or Current account held for same amount of time. LLoyds have intermittently been chasing too last random contact was to a old previous address of my parents despite them having my current stating that the amount of interest had been accrued incorrectly by them refunding approx £600 back to the account and if the remaining balance was not cleared by X DATE (approx £1200) that a default would be applied to my credit file -this was SINCE i started paying Robinson Way direct. Unsure of if default applied need to check credit file to see what it shows. Response from Robinson way re CCA was they are making the necessary enquiries and let me know the outcome in due course and interestingly they will stop ALL collection activity on the account. I have cancelled the standing order to them. Balance £1127,98 Surely there is only liability to one creditor and if LLoyds have sold this on then they surely cant default my credit file. No response from LLoyds re SAR......should make interesting reading with 30 years of documentation Intending to reclaim all current account and credit card charges