Search the Community

Showing results for tags 'egg'.

-

Hi Firstly, those in debt finding it hard to see light at the end of the tunnel, don't be disheartened, it can be done. After 8 years, I am within 9 months of being debt free. however, this hasn't been without issues and I could do with some advice on what should be my last issue.... Sorry for the length, just don't know best course of action... thanks in advance for any help I defaulted on an Egg credit card, they sold the debt to Arc Europe. Barclaycard bought Egg. Barclaycard transferred the debt to Moorcroft. I have consistently paid the agreed monthly amount. However, during the transfer from Arc to Moorcroft 3 payments went to Arc totalling c£250. In July 2016, Moorcroft sent me a letter stating an incorrect outstanding balance, incorrect by the same c£250 exactly. In November 2016, I wrote the following to Moorcroft (names & reference no's excluded, and amounts rounded to avoid identification).. In reply to your letter dated dd/07/2016 stating the balance was £x. I disagree with this balance, my balance is £y. This represents a difference of c£250, which equates to monthly payments of £z. My account transferred from ARC to Moorcroft in September 2011. At this time, my balance with ARC was £6k, before my September 2011 payment. This is confirmed in your letter dated dd/10/2011. I am not aware of missing any payments, can you provide a full breakdown of the account including any interest or charges applied please? Today, I believe the balance is £a. I will not pay any additional balance until I receive a full breakdown of the account including any interest or charges applied. Please do provide a full breakdown of the account including any interest or charges applied. Today, they have responded with (pleasantries have been excluded) Our client has advised that they have a balance of c£900 on their system. a letter is attached from our client as confirmation. The attached letter (on very poor Barclaycard letterhead and unprofessional format) says dd/12/2016 Dear Sir/Madam RE : My name - Account No. my account number Thanks for contacting us. Unfortunately, statements are no longer produced on the above account. I can confirm that the outstanding balance of the Account As of today is c£900. I trust this information is of assistance to you. Any queries, contact us, we are here to help. So in summary, I know why we disagree with the balance. Moorcroft won't acknowledge this. Moorcroft have created a fictitious letter from Barclaycard trying to pass it off as from Barclaycard. The debt is no longer on my credit file, it is clean. I suspect if I contact Barclaycard they won't recognise the account. All payments since Sept 11 have been paid to Moorcroft using their reference number, except the 3 made to ARC. what do I do? 1) stop payments immediately 2) report Moorcroft to FCA 3) subject access request to Moorcroft 4) send Moorcroft a firm letter as per - you are wrong. payments have been made to Moorcroft not Barclay - you are fraudulent. you should create fictitious letters using someone else letterhead. - offer 10% of the correct balance to go away? help please....

-

Hi First post here. I have an old debt with Egg from around 2000 for roughly £2900. I was on a CAB plan paying £1 token payment for a while at the time but stopped paying , I never heard anything for years and now Capquest own the debt . I think I might remember paying them £10 a month 3-4 years ago for a while but due to financial hardship stopped paying. Though I cant be certain on this as I cant seem to find any details at the moment. They have recently sent me letters again and have refered it to Drydens Fairfax who have given me to the 30th Nov to offer a payment proposal otherwise court action. Which means I`ll have to send them a ltter either today or tomorrow .What should I do , offer £5 a month or something or play hardball. I don't really want a CCJ as I already have one from Drydens at £10 a month for another card debt. I wish I had know of the Statute Barred act before I may(possibly) have paid Capquest 3-4 years ago as it was probably unenforceable back then. thanks Tired and Weary

-

Hello I am new to the site always been a watcher and reader. Recently requested a CCA on account that is managed by idem (previously EGG) because it was pre 2007. They have sent through a copy but I am unsure where I stand to whether it is enforceable. I have a scanned copy in PDF Please can someone help me I have been quite successful on negotiating F&F on other accounts and am trying to finalise on others with Barclaycard (Link), PRA Virgin Active. RS1.pdf

-

Good evening I am hoping somebody can help me with advise. My wife currently owns a house with her mum. Her mum moved out about 9 years ago when she remarried and instead of selling my wife went onto the mortgage and became 50% owner. they have had an offer on the house and are in the process of selling. The solicitor today rang to say we they aware of a charging order in mother in laws name. She didn't have a clue about it but so far has managed to find out the following: The DCA is Cabot. They have said that she needs to speak with the Solicitors 'Wright Hassall' (seems a really apt name!!!!) She contacted solicitors and they have said that the original debt was with Egg (apparently. Until MIL said she has never had an egg credit card, they mentioned two other potential creditors it could be) The charging order was on the 16/12/2013 for a fee of £6,113.25. The last payment (or default, she can't remember) on this account is 02/07/2007. The account balance was £5066.25 She has never had a credit card so obviously wants to dispute this in its entirety. She didn't live at the address the letters were sent to so was unaware of the judgements. I have told her that she needs to request a CCA from the solicitors etc. The problem is, the house sell. Obviously they don't want to pay this, but will not be able to sell the house if they dispute it. Can they dispute it retrospectively? really really really appreciate the advice given

Good evening I am hoping somebody can help me with advise. My wife currently owns a house with her mum. Her mum moved out about 9 years ago when she remarried and instead of selling my wife went onto the mortgage and became 50% owner. they have had an offer on the house and are in the process of selling. The solicitor today rang to say we they aware of a charging order in mother in laws name. She didn't have a clue about it but so far has managed to find out the following: The DCA is Cabot. They have said that she needs to speak with the Solicitors 'Wright Hassall' (seems a really apt name!!!!) She contacted solicitors and they have said that the original debt was with Egg (apparently. Until MIL said she has never had an egg credit card, they mentioned two other potential creditors it could be) The charging order was on the 16/12/2013 for a fee of £6,113.25. The last payment (or default, she can't remember) on this account is 02/07/2007. The account balance was £5066.25 She has never had a credit card so obviously wants to dispute this in its entirety. She didn't live at the address the letters were sent to so was unaware of the judgements. I have told her that she needs to request a CCA from the solicitors etc. The problem is, the house sell. Obviously they don't want to pay this, but will not be able to sell the house if they dispute it. Can they dispute it retrospectively? really really really appreciate the advice given -

Hi All Its been along time since I have been back and needed help from you wonderful guys but back I am Basically like alot of you guys I had a credit card with egg that over the months and years has been passed for DCA to DCA, having CCA'd them along time ago with no response I have done nothing with it. Which wasnt a problem until now. I have been offered a job, something I have wanted to do all my life, couldnt believe it when I got it was over the moon. But.... they do a full vetting and blindly thinking they would only do the normal employer credit check (which I am fine on) they contacted me today to say they had done a full one and need me to explain a default I have on there, the one from egg. Thinking this was all over have stupidly mislaid all my paperwork, but from memory I CCA'd one of the first DCA's sometime ago with no response therefore I ignored the debt and correspondence from the other DCA's it kept being passed to. My question is this, they have failed to produce the CCA before is it fair that now its been taken over by Marlin that they could leave a footprint on my CRA report. From my report it follows like this: Barclaycard closed the account Jan 2013 marked DA (Debt assigned) default date of Feb 2010 (showing now zero balance) Marlin put default marker on June 2013 with the following on 2 CRA files Call Credit Opening Balance £xxxx Current Balance £xxxx Equifax Opening Balance £0 Current balance (Closed 4 March 2010 (balance £xxxx)) If there is anyone out there who could help me as I have to explain to my potential new employers asap about this default. Would I have to go down the CCA route again with Marlin which I didnt want to do because of the time scales ie statute barred etc but if I have to I will. Thanks in advance guys for any help you can give xxx

Hi All Its been along time since I have been back and needed help from you wonderful guys but back I am Basically like alot of you guys I had a credit card with egg that over the months and years has been passed for DCA to DCA, having CCA'd them along time ago with no response I have done nothing with it. Which wasnt a problem until now. I have been offered a job, something I have wanted to do all my life, couldnt believe it when I got it was over the moon. But.... they do a full vetting and blindly thinking they would only do the normal employer credit check (which I am fine on) they contacted me today to say they had done a full one and need me to explain a default I have on there, the one from egg. Thinking this was all over have stupidly mislaid all my paperwork, but from memory I CCA'd one of the first DCA's sometime ago with no response therefore I ignored the debt and correspondence from the other DCA's it kept being passed to. My question is this, they have failed to produce the CCA before is it fair that now its been taken over by Marlin that they could leave a footprint on my CRA report. From my report it follows like this: Barclaycard closed the account Jan 2013 marked DA (Debt assigned) default date of Feb 2010 (showing now zero balance) Marlin put default marker on June 2013 with the following on 2 CRA files Call Credit Opening Balance £xxxx Current Balance £xxxx Equifax Opening Balance £0 Current balance (Closed 4 March 2010 (balance £xxxx)) If there is anyone out there who could help me as I have to explain to my potential new employers asap about this default. Would I have to go down the CCA route again with Marlin which I didnt want to do because of the time scales ie statute barred etc but if I have to I will. Thanks in advance guys for any help you can give xxx -

Debt from June 2002 £8,500 sold by Barclays to Arrow Global. I have been dealing with Capquest until Nov 2015, and paying £5 per month, when I asked for a copy of my agreement and had reply from Capquest in Feb 2016, saying account on hold whilst they request the documentation from Arrow. I heard nothing more until last week when I had a letter from Wescot asking if I was the person they referred to and to contact them. I did nothing. Then a letter today from Arrow saying that Westcot is now managing my debt and asking me to contact Wescot. Odd thing is I have always dealt via a friends address to avoid embarassment and the last two letters came to my address not my friends. What do i do?

-

Name of the Claimant ? MARLIN CAPITAL EUROPE LTD Date of issue – 27 MAY 2015 What is the claim for – By an agreement between Egg Banking plc (EGG) & the defendant on or around 29/10/2005 (the agreement ) EGG agreed to issue the defendant with a credit card. The defendant failed to make the minimum payments due & the agreement was terminated. The agreement was assigned to the claimant on 31/01/2013. THE CLAIMANT THEREFORE CLAIMS 1. 4000 2. interest pursuant to section 69 of the county court act 1984, namely 1400 & continuing until judgment or sooner payment at the rate of 0.93 What is the value of the claim? £6200(including court/solicitors fees) Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? credit card When did you enter into the original agreement before or after 2007? 29/10/2005 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Don't know, was aware of Barleys taking over Did you receive a Default Notice from the original creditor? Dont remember Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? Loss of job and family problems What was the date of your last payment? not sure sometime 2009 Was there a dispute with the original creditor that remains unresolved? no Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? no I've received county court claim form. I've put as much information which i can find or know at the moment. Do i have any chance of defending this claim? I already have a ccj fron Cabot this year

Name of the Claimant ? MARLIN CAPITAL EUROPE LTD Date of issue – 27 MAY 2015 What is the claim for – By an agreement between Egg Banking plc (EGG) & the defendant on or around 29/10/2005 (the agreement ) EGG agreed to issue the defendant with a credit card. The defendant failed to make the minimum payments due & the agreement was terminated. The agreement was assigned to the claimant on 31/01/2013. THE CLAIMANT THEREFORE CLAIMS 1. 4000 2. interest pursuant to section 69 of the county court act 1984, namely 1400 & continuing until judgment or sooner payment at the rate of 0.93 What is the value of the claim? £6200(including court/solicitors fees) Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? credit card When did you enter into the original agreement before or after 2007? 29/10/2005 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Don't know, was aware of Barleys taking over Did you receive a Default Notice from the original creditor? Dont remember Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? Loss of job and family problems What was the date of your last payment? not sure sometime 2009 Was there a dispute with the original creditor that remains unresolved? no Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? no I've received county court claim form. I've put as much information which i can find or know at the moment. Do i have any chance of defending this claim? I already have a ccj fron Cabot this year -

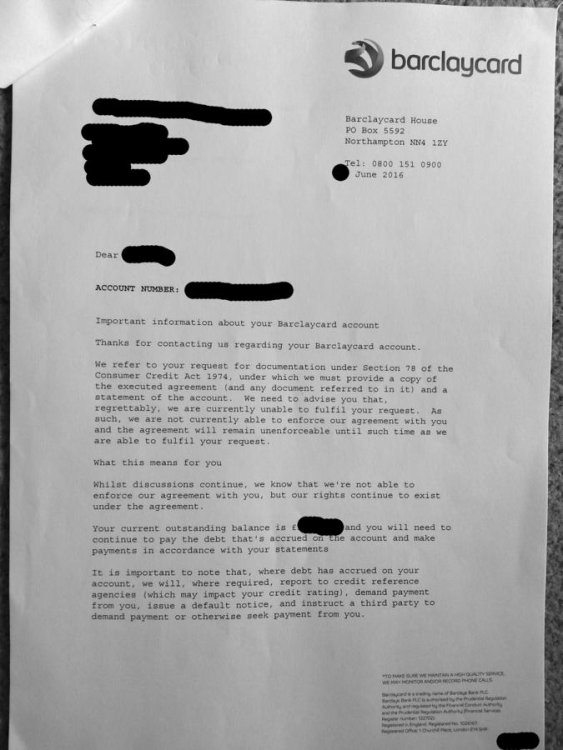

I have an old Egg credit card which went into default a number of years ago after I had to close my business. I have been paying £1 per month for a couple of years now. The payments are going through Capquest. Last time they asked for a financial update i asked for a copy of the original loan agreement. As I understand it Barclaycard took over Egg cards a number of years ago. I have attached a copy of the letter with details blanked out - the outstanding is around £3000. In the letter B/card state that they cannot currently fulfil my request, and as a result the outstanding is unenforceable. What should I do now? Should I stop payments until they can prove the liability? Should I offer them £100 in full and final? The default obviously still shows on my credit file. Many thanks TW

-

Canada Square Operations are citing the Financial Conduct Authority's regulatory review in light of the Supreme Court’s decision in Plevin as a justification for being unable to consider my claim for mis-sold PPI on an Egg credit card until such time as the FCA publishes its guidance. Let me be clear, it's not that Canada Square Operations have rejected my claim but have said they will revisit it in light of any additional rules / guidance deemed necessary by the FCA. Rather, they have said they won't even consider it until the FCA publishes its conclusions. Now, it seems to me this is a nonsense for the following reasons: [1] I've completed and returned a FOS questionnaire which makes clear the basis on which I think the PPI was mis-sold – essentially, I applied for the credit card online and was unable to proceed with my application if I unticked a pre-ticked box requesting PPI. This being the case, it seems clear to me that the PPI was mis-sold and whatever the FCA guidance might / might not turn out to be apropos Plevin and the role of undisclosed commissions is irrelevant. [2] Notwithstanding [1], I applied for this credit card in October 1999, ie long before Section 140A of the Consumer Credit Act 1974 kicked in, and the account was settled in full long before April 2008 when the legislation began to apply regardless of when an agreement was entered into. In these circumstances, it seems to me nonsensical for Canada Square Operations to refuse to consider my claim and instead invite me to go straight to the FOS, whereby they would, I believe, incur a fee in excess of £500 to investigate a complaint which I am confident would be upheld. Aside from the annoyance / inconvenience it would cause me [waiting for the Ombudsman's ruling], I can't see what possible motivation Canada Square Operations could have for taking this course of action. With this in mind, I'm minded to write back making the very same points I've made above but, before doing so, would welcome the thoughts and opinions of my fellow CAGgers. Thanks in anticipation Fred_Funk

-

Hi Would like some advice about 2 loans that I took out in 2005 with egg to consolidate credit cards, car purchase etc after getting a mortgage in 2004. Both loans were for just under £25k each and it was more or less implied that if I took out PPI that the loans would be easier to be accepted for and that I would be able to claim if I was not able to work for any reason even though I was self employed. Roll onto end of 2008 where my ex wife and I started having relationship problems and I started struggling to make the repayments but feeling that I had a duty to repay I struggled on trying to keep the repayments up to date even when I could not carry on working at the end of 2009 when I became a single parent. By March/April 2010 I could not make the payments so the loans went into default officially. I spent the next 6 years struggling to bring up my kids as a single parent and have been chased to repay the loans via lots of different debt collection companies but was never in the position to pay anything So now in 2016 the loans have both been removed from my credit report (such a relief as can start rebuilding my credit worthiness). I did receive a questionnaire for both loans from Canada Square Operations in 2013 about my PPI but because of my financial situation I just filed them as I was worried that it was a ploy to get me to pay money to them that I could not afford. It does state in the covering letter that they that the loans where now being administered by Britannica Recoveries but does not say the debt had been sold to them. It also lists the reasons that they think I would be entitled to a refund for and they are for it being implied that by taking PPI I would get the loans and that when self employed I could only claim if I could not work at all. My question is would it be worthwhile sending in the questionnaire now to apply for a refund. Many thanks in advance Allister

Hi Would like some advice about 2 loans that I took out in 2005 with egg to consolidate credit cards, car purchase etc after getting a mortgage in 2004. Both loans were for just under £25k each and it was more or less implied that if I took out PPI that the loans would be easier to be accepted for and that I would be able to claim if I was not able to work for any reason even though I was self employed. Roll onto end of 2008 where my ex wife and I started having relationship problems and I started struggling to make the repayments but feeling that I had a duty to repay I struggled on trying to keep the repayments up to date even when I could not carry on working at the end of 2009 when I became a single parent. By March/April 2010 I could not make the payments so the loans went into default officially. I spent the next 6 years struggling to bring up my kids as a single parent and have been chased to repay the loans via lots of different debt collection companies but was never in the position to pay anything So now in 2016 the loans have both been removed from my credit report (such a relief as can start rebuilding my credit worthiness). I did receive a questionnaire for both loans from Canada Square Operations in 2013 about my PPI but because of my financial situation I just filed them as I was worried that it was a ploy to get me to pay money to them that I could not afford. It does state in the covering letter that they that the loans where now being administered by Britannica Recoveries but does not say the debt had been sold to them. It also lists the reasons that they think I would be entitled to a refund for and they are for it being implied that by taking PPI I would get the loans and that when self employed I could only claim if I could not work at all. My question is would it be worthwhile sending in the questionnaire now to apply for a refund. Many thanks in advance Allister -

Just wondered if anyone can advise me on what line I should pursue. I am currently in the early stages of court proceedings on another thread for an Egg loan - which led to me reading other things on this site, particularly lots of stuff about Egg cards. Can anyone advise me on whether or not I have anything worth pursuing. Will summarise; In 99 or 2000 took out an Egg card online which ran ok for many years. I know I had PPI and account ran up and down to around £11k. A few years into the account i questioned the need for the PPI and they stopped it. (not sure of exact dates) Account balance eventually dropped to about £4k and last year i asked them questions about the PPI but was told I was wasting my time as the application was done online and i'd ticked the box! I got into financial difficulties early this year, did an 'income and expenditure exercise and offered each of my creditors a monthly payment pro rata. Egg ignored my letters for 3 months (but managed hundreds of phone calls, 3 further letters of their own, texts etc) and then issued a Default Notice! 6 weeks later they sent a further letter terminating my account and handed it to a DCA called DLC. They agreed to the monthly amount that i'd offered Egg within a matter of days!! I'm assuming that the debt was probably sold on. My question is this - Does anybody have an opinion on what I should be doing now/next? Should I be issuing anything to Egg or DLC at this stage or should I let sleeping dogs lie? Any advice gratefully received.

-

Hi I'm currently on a DMP and paying off my Egg card through Cabot financial. Can I still put in a PPI claim and if so then who do I contact??

-

Hi I know it's Christmas but really hope someone can help me out urgently, I've had a claim through from cabot financial with 'right hassle' acting on their behalf for a very old Egg account. I submitted the AOS now need to put together a defence in the next 2-3 days and submit by thursday next week (i think that's the deadline having used the 33 day from service calc). Claim details/points Claimant - CABOT FINANCIAL (UK) LIMITED Address for docs & payments - WRIGHT HASSALL LLP Date of issue – 24/11/14 POC - POC ATTACHED but I can type this out if need be. [ATTACH=CONFIG]54992[/ATTACH] - Not sure if important but POC seems to include a mistake or two: using # symbols instead of £, also they quote a #19,***.** balance for the debt (far in excess of the c14K at close of account!?) and then go on to ask for interest of exactly the same total: "The Claimant therefore claims the sum of #19,***.** interest under s89 County Courts Act 1984 and costs." surely this is wrong and a basis to defend/strike out? Claim Value - ALMOST £20,000 Original Creditor - EGG (Card Account closed 2006) Type of Account - CREDIT CARD ACCOUNT Agreement entered pre-2007? - Yes 2004 Account assigned by Debt Purchaser? - Yes, by CABOT (bought from Egg 2009) Notice of Assignment? NOT SURE if I have a properly worded NOA: - had a letter from EGG (OC) late 2009 stating "We hereby give notice of the transfer of the debt due to us by you.. ..On XXX 2009 your account was sold to Cabot Financial.. .Any further communications and payments must therefore be addressed to Cabot...etc." -had a "Welcome to Cabot" letter stating similar (is that acceptable as an NOA) Default Notice from the original creditor? - YES 2006 but not sure if correct Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? - YES BUT NOT EVERY YEAR (not in 2011 & 2012) Why did you cease payments? - BUSINESS IN TROUBLE SO SEVERE FINANCIAL DIFFICULTIES What was the date of your last payment? - to the OC May/June 2006 (can check exact date if needed) - to the DCA not sure either late 2008 or very early 2009 Was there a dispute with the original creditor that remains unresolved? Possibly - PPI charged when not asked for, this was refunded (2004) but can I use this? - CCA request to ARC in early 2009 recorded post, responded with a copy of a signed Egg Agreement but not the entire terms, very brief 2 pages - pretty sure I wrote back "account in dispute" as requested docs not supplied but what if I can't find letter/postal proof? Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? YES, I wrote to them saying that I had severe financial issues asking for account to be put on hold, that I had been in touch with National Debtline (gave them the ref number) and had been making recent smaller payments, They wrote back saying no can do. PPI - as mentioned above never requested/applied for but charged at the start of the account, I lodged a complaint and was refunded the 2 charges. Interest - The interest has been accruing since the account moved on and has grown from c£14k to almost £20k, surely this is wrong when there are no details as to how they have come by an interest rate, what terms do they rely on etc? Can anyone help me out with some advice please, am I on the right track with some of my thoughts above? Most urgently I'm not sure if i should send any further CCA requests to Cabot or WH or even Egg? Too late for a CPR31.14? If i can get the letters into the post tomorrow morning they will reach the DCA/OC by Monday morning recorded delivery which gives almost a week - but I need to send them by 12pm tomorrow so if anyone is out there please advise. Many thanks. GF2k

Hi I know it's Christmas but really hope someone can help me out urgently, I've had a claim through from cabot financial with 'right hassle' acting on their behalf for a very old Egg account. I submitted the AOS now need to put together a defence in the next 2-3 days and submit by thursday next week (i think that's the deadline having used the 33 day from service calc). Claim details/points Claimant - CABOT FINANCIAL (UK) LIMITED Address for docs & payments - WRIGHT HASSALL LLP Date of issue – 24/11/14 POC - POC ATTACHED but I can type this out if need be. [ATTACH=CONFIG]54992[/ATTACH] - Not sure if important but POC seems to include a mistake or two: using # symbols instead of £, also they quote a #19,***.** balance for the debt (far in excess of the c14K at close of account!?) and then go on to ask for interest of exactly the same total: "The Claimant therefore claims the sum of #19,***.** interest under s89 County Courts Act 1984 and costs." surely this is wrong and a basis to defend/strike out? Claim Value - ALMOST £20,000 Original Creditor - EGG (Card Account closed 2006) Type of Account - CREDIT CARD ACCOUNT Agreement entered pre-2007? - Yes 2004 Account assigned by Debt Purchaser? - Yes, by CABOT (bought from Egg 2009) Notice of Assignment? NOT SURE if I have a properly worded NOA: - had a letter from EGG (OC) late 2009 stating "We hereby give notice of the transfer of the debt due to us by you.. ..On XXX 2009 your account was sold to Cabot Financial.. .Any further communications and payments must therefore be addressed to Cabot...etc." -had a "Welcome to Cabot" letter stating similar (is that acceptable as an NOA) Default Notice from the original creditor? - YES 2006 but not sure if correct Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? - YES BUT NOT EVERY YEAR (not in 2011 & 2012) Why did you cease payments? - BUSINESS IN TROUBLE SO SEVERE FINANCIAL DIFFICULTIES What was the date of your last payment? - to the OC May/June 2006 (can check exact date if needed) - to the DCA not sure either late 2008 or very early 2009 Was there a dispute with the original creditor that remains unresolved? Possibly - PPI charged when not asked for, this was refunded (2004) but can I use this? - CCA request to ARC in early 2009 recorded post, responded with a copy of a signed Egg Agreement but not the entire terms, very brief 2 pages - pretty sure I wrote back "account in dispute" as requested docs not supplied but what if I can't find letter/postal proof? Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? YES, I wrote to them saying that I had severe financial issues asking for account to be put on hold, that I had been in touch with National Debtline (gave them the ref number) and had been making recent smaller payments, They wrote back saying no can do. PPI - as mentioned above never requested/applied for but charged at the start of the account, I lodged a complaint and was refunded the 2 charges. Interest - The interest has been accruing since the account moved on and has grown from c£14k to almost £20k, surely this is wrong when there are no details as to how they have come by an interest rate, what terms do they rely on etc? Can anyone help me out with some advice please, am I on the right track with some of my thoughts above? Most urgently I'm not sure if i should send any further CCA requests to Cabot or WH or even Egg? Too late for a CPR31.14? If i can get the letters into the post tomorrow morning they will reach the DCA/OC by Monday morning recorded delivery which gives almost a week - but I need to send them by 12pm tomorrow so if anyone is out there please advise. Many thanks. GF2k -

as above, CCA'd egg on 16/07/08. They responded with an unsigned agreement and nothing else, no terms, no other info. Wrote back to them to tell them account in dispute as they have failed to provide etc. put in the dispute letter the usual about "you may not pass this account on" etc but they've completely ignored it and sent a letter back saying the account is now closed and will be passed to a DCA for collection what do I do now?

-

Hello everyone, After splitting with my ex partner in 2008 I defaulted on my then Egg c/c. Since then I haven't made a payment or made contact. Egg was taken over by Barclaycard and they started chasing me via letters for payment. Recently MKDP have started sending letters demanding payment. They have threatened to send round a debt collection guy to collect payment, and gave me 14 days to settle. When this happened I found this forum and sent them a letter requesting the original credit agreement, as suggested on here. Today they replied saying they are unable to resolve my query ATM. They are conducting a review which may include liaising with my original creditor. What would be the correct next step please? Thank you in advance. Russ

-

I have received a claim form from Restons / Arrow global dated 10th December. Date of issue – top right hand corner of the claim form – this in order to establish the time line you need to adhere to. The are claiming just short of £4000 for an old loan debt The loan started in 2005 and should have completed in 2010. I was in a serious amount of difficulty in 2009. I used the advice from another forum (cant recall which sorry) to send a number of template CCA request letters and the account has been in dispute without payments since June 2009. I believe that I should send a CPR31.14. Also, I should acknowledge the claim online within 14 days and send a defence within 28 days. It will be difficult for me to find the money quickly and hopefully the court date is later in the year to give me more time so I am very stressed right now.

I have received a claim form from Restons / Arrow global dated 10th December. Date of issue – top right hand corner of the claim form – this in order to establish the time line you need to adhere to. The are claiming just short of £4000 for an old loan debt The loan started in 2005 and should have completed in 2010. I was in a serious amount of difficulty in 2009. I used the advice from another forum (cant recall which sorry) to send a number of template CCA request letters and the account has been in dispute without payments since June 2009. I believe that I should send a CPR31.14. Also, I should acknowledge the claim online within 14 days and send a defence within 28 days. It will be difficult for me to find the money quickly and hopefully the court date is later in the year to give me more time so I am very stressed right now. -

Sent a claim for PPI on EGG credit card : had paperwork as I had sent a SAR request. Statute barred debt £6k. Reasons given are several and it's their final response. Application was March 2002. They say the CRP policy box was not pre-ticked (online application) They say I was fully informed and it was my decision to take it and it was up to me to decide if suitable for my needs? and that the policy document would have been supplied to me which would have explained everything many thanks the letter was dated 14th September : received 17th September Is it worth sending to FOS.

Sent a claim for PPI on EGG credit card : had paperwork as I had sent a SAR request. Statute barred debt £6k. Reasons given are several and it's their final response. Application was March 2002. They say the CRP policy box was not pre-ticked (online application) They say I was fully informed and it was my decision to take it and it was up to me to decide if suitable for my needs? and that the policy document would have been supplied to me which would have explained everything many thanks the letter was dated 14th September : received 17th September Is it worth sending to FOS. -

Hi caggers, I have received a letter from Mortimer Clarke which I originally thought was to do with an alleged Barclaycard debt but now realise relates to an alleged Egg debt. The letter contains income and expenditure forms and a Direct Debit mandate for me to complete and states that if no reasonable offer if made within 14 days then they will issue a claim in the County Court. I sent a s.77/78 request to Egg in 2010 and received nothing so assumed they had no agreement form to support the demands they were making of me for payment. Should I reply to this Mortimer Clarke letter and if so how? Any help much appreciated. Cheers.

-

Hi Everyone, I had a debt management plan about 10 years ago, which is long since pretty much paid off / written off etc aside from two things which I would like to ask advice on. Firstly, I pay Collect Direct £45.00 a month on a standing order. I no longer have any idea what it is for but believe it may have been for an Egg credit card I have received no correspondence whatsoever from Collect Direct for about 8 years and I have no idea how to contact them or find out how much I may still owe. Nor do I really want to open that can of worms really as life has moved on. I would ideally like to stop paying them because I feel I could continue paying £45.00 forever and I don't know how much I really may owe. Is it advisable to stop paying them or just continue? If I stop paying them, what might the implications be? Secondly, I also have a CCJ from Tesco finance. This was a CCJ given in 2005 and no longer shows on my credit file. I pay £57.00 a month and at that rate it will take me longer than my entire working life to pay back what the debt was. Again my question is, what would the implications be of failing to pay a CCJ or should I just carry on. I could never afford to pay off the full amount. Is there anything else that I could do to try and get rid of this noose? Many thanks in advance for any advice.

-

Brief description, £11,343 - Egg Loan (original loan was £15k), Aktiv Kapital (UK) Ltd (Not showing on my credit report) - when was you last payment? Through dmp once every month So they have sent refusal letter and a response to a CCA request. whilst awaiting the cca, collection has been removed AK 75% discount offer letter

-

Hi all. Need some advice, please DH had an Egg credit card and we defaulted during a rather dark period of our lives. The account was passed on to Bryan Carter who took him to court in Jan 2011. We didn't contest it or turn up to the court date (which wasn't in our local court, but some 200 miles away) and a Charging Order was placed on our property. We're currently trying to sort our financial affairs out as we want to move next year. The "amount owing under judgement or order given on 18 June 2010 by the court, together with any interest becoming due and £268 the costs of the application" Surely, as the amount is under £5k, interest would not be payable? Is this just standard wording, or have the court given them carte blanche to charge us for that too? We have been paying £30 a month to Bryan Carter since 2011 but have never received any statements of account and we now want rid of this, so that we can start to repair our credit rating and get the charging order removed. Is it possible to attempt to fight this retrospectively? We have never asked for CCA's to prove liability or that the agreement was worded correctly; or for any statements of account on the original debt (and we know how bad these companies are for just plucking figures out of thin air! We're sure that the original debt was not this much) Is this worth doing now, or a bit pointless as it has already been through court? Alternatively, how open do you think they would be to accepting a full and final settlement for less than the amount outstanding? Many thanks for any help you can provide.

Hi all. Need some advice, please DH had an Egg credit card and we defaulted during a rather dark period of our lives. The account was passed on to Bryan Carter who took him to court in Jan 2011. We didn't contest it or turn up to the court date (which wasn't in our local court, but some 200 miles away) and a Charging Order was placed on our property. We're currently trying to sort our financial affairs out as we want to move next year. The "amount owing under judgement or order given on 18 June 2010 by the court, together with any interest becoming due and £268 the costs of the application" Surely, as the amount is under £5k, interest would not be payable? Is this just standard wording, or have the court given them carte blanche to charge us for that too? We have been paying £30 a month to Bryan Carter since 2011 but have never received any statements of account and we now want rid of this, so that we can start to repair our credit rating and get the charging order removed. Is it possible to attempt to fight this retrospectively? We have never asked for CCA's to prove liability or that the agreement was worded correctly; or for any statements of account on the original debt (and we know how bad these companies are for just plucking figures out of thin air! We're sure that the original debt was not this much) Is this worth doing now, or a bit pointless as it has already been through court? Alternatively, how open do you think they would be to accepting a full and final settlement for less than the amount outstanding? Many thanks for any help you can provide. -

Hi all. I'm not sure if I'm posting this in the right place, so please move the thread if not okay. Around 2006 after losing my job, I had difficulty meeting the payments on my Egg card. I paid them monthly out of my savings but when they ran out I could no longer pay. After defaulting on the account it was passed to a debt collector who settled for payments of £5 a month. They used to hassle me and ring constantly and also tried to demand more money each month. These were taken over by Apex Credit Management who seemed to do everything by the book. They send me regular statements, check my financial position every six months and make sure I can afford the payments, which are now £30. This debt is no longer on my Credit file, so is not affecting my status. What I need to know is: if I stop paying this each month, what will happen? I have received some great advice on here regarding other debts, so don't really want to continue to pay Apex if there is something I have missed. What should I have done when the debt was passed over? Thank you

-

Hi, I'm currently in default to egg for a loan after falling behind with payments after losing my job. they passed it onto capquest debt recovery who are useless. I set up a payment plan for £75 monthly, after making 6 payments by SO from bank capquest wrote and said they were taking further action due to non-payment. I was advised to cancel the payments and send off a copy of my bank statements showing the payments, which I did. They wrote acknowledging these and set up a new SO for £75 again. A payment left my account on 4 May but last week they sent me a letter saying they were now going to send a collector to my door due to me ignoring repeated requests for payments or a payment plan. I've tried speaking to them on the phone but they are bloody useless. Can anyone tell me what to do next, I'm not that great on the phone and if anyone comes to my door I'd panic and probably agree to whatever they asked for whether I could afford it or not. Any advice would be very much appreciated. Thanks

-

It depends if you are a fan of Apple or not whether you find this funny. Personally I find it hilarious: Independent

It depends if you are a fan of Apple or not whether you find this funny. Personally I find it hilarious: Independent -

Hi guys I am a newbie to this forum, but decided to join as I read some interesting stuff on here particularly regarding Marlin DCA. I have an existing credit card debt with Egg which last payment was made back in 2009. I received a letter this year from Marlin who are chasing the debt on behalf of BarclayCard. I wrote to Marlin on the 3rd March 2013 requesting a "true copy" of the original credit card agreement (s78 of the CCA). I then received a letter from Marlin on the 23rd March 2013 stating that "We do not hold a copy of your online agreement and have therefore applied for a copy from the original creditor and will forward upon receipt." A few questions: Is my letter of the 23rd March a valid CCA request or does it need to worded in a certain style? Should I have sent a failure to comply letter after 12+2 days or does it not matter too much? Based on the answers to my above questions, since it is now 13th May and I have not heard anything, is the agreement unenforceable? Thanks in advance.