Search the Community

Showing results for tags 'egg'.

-

HI guys, I’m currently assisting my mother with a PPI complaint with Barclaycard (formerly an egg card taken out Online in Q1 of 2004). I would really appreciate if someone could categorically tell me that EGG had the PPI box pre-ticked during Q1 of 2004 i.e. they have been successful in calming miss-sold PPI with egg. I would be especially over the moon if someone could tell me that it was not possible to proceed with the application if this box was not ticked as that seems of a complete own goal by egg. Barclaycard have offered us quite a chunk of a refund due to Plevin, but my mother believes she did not knowingly apply of the PPI insurance, which would be the case if the box was pre-ticked. We are is still the early stages i.e. we stated that we believed we have been miss-sold to Barclays and the 1st letter had was this Plevin offer, but we still have not sent our evidence nor our full reasons of the miss-selling to Barclaycard as of yet. Note: Barclaycard have stated the application was made online, I have no way to confirm this, but I have a paper copy of the 15 year old agreement from egg which I found filed away. The card is still active and has PPI premiums ongoing although I have made her paid off the balance of the card (+£2000). Any Help is much appreciated.

HI guys, I’m currently assisting my mother with a PPI complaint with Barclaycard (formerly an egg card taken out Online in Q1 of 2004). I would really appreciate if someone could categorically tell me that EGG had the PPI box pre-ticked during Q1 of 2004 i.e. they have been successful in calming miss-sold PPI with egg. I would be especially over the moon if someone could tell me that it was not possible to proceed with the application if this box was not ticked as that seems of a complete own goal by egg. Barclaycard have offered us quite a chunk of a refund due to Plevin, but my mother believes she did not knowingly apply of the PPI insurance, which would be the case if the box was pre-ticked. We are is still the early stages i.e. we stated that we believed we have been miss-sold to Barclays and the 1st letter had was this Plevin offer, but we still have not sent our evidence nor our full reasons of the miss-selling to Barclaycard as of yet. Note: Barclaycard have stated the application was made online, I have no way to confirm this, but I have a paper copy of the 15 year old agreement from egg which I found filed away. The card is still active and has PPI premiums ongoing although I have made her paid off the balance of the card (+£2000). Any Help is much appreciated. -

I cannot believe how useless FOS is: Investigator ruled against me because I must have accepted an online question that I wanted PPI: he sent me screenshots of questions re PPI but not my screenshots since i never seen them before. my gdpr did not contain them, my cca regulated agreement contained nothing about ppi… he says fos is not interested in cca agreement or what is in gdpr … cca is a matter for fca.. not fos disgraceful appalling service... i feel a need to complain about this investigator i have sent an email complaining about the fos guy essentially he has assumed that i saw an online form and replied i did want ppi… but he has not offered any evidence that i was offered or even accepted or declined

-

Hello all I banged off a ppi enquiry to every single company that I had ever borrowed from, in case, although I'm fairly sure I always declined any extra services. Egg/One Canada Square replied last to say that I did have ppi on a very old credit card back in the day. I complained and today got a letter saying that my complaint was upheld but there was nothing to refund as no premiums were ever applied, something like that. Does that sound sensible/likely? If I dig out some old statements will it show on them as a separate line? SAR? Thanks Micky

Hello all I banged off a ppi enquiry to every single company that I had ever borrowed from, in case, although I'm fairly sure I always declined any extra services. Egg/One Canada Square replied last to say that I did have ppi on a very old credit card back in the day. I complained and today got a letter saying that my complaint was upheld but there was nothing to refund as no premiums were ever applied, something like that. Does that sound sensible/likely? If I dig out some old statements will it show on them as a separate line? SAR? Thanks Micky -

Hi, when the whole PPI claim thing started i didn't really think i could claim on this account, but here are the details. I had an Egg card 8 or more (not sure) years ago which started around £500 limit, i had PPI, and they kept raising the limit until about 6 months down the line i had a £3000+ limit, anyway i abused this and got to a point where i couldn't pay off even the minimum monthly payments, so charges and interest grew until the balance was £10k, i told them i couldn't pay this and reached an agreement for a one time payment of £3k to close the account. Would it be possible to claim PPI on this account? I don't know if i have any old statments on the account as i think i threw them when it closed.

Hi, when the whole PPI claim thing started i didn't really think i could claim on this account, but here are the details. I had an Egg card 8 or more (not sure) years ago which started around £500 limit, i had PPI, and they kept raising the limit until about 6 months down the line i had a £3000+ limit, anyway i abused this and got to a point where i couldn't pay off even the minimum monthly payments, so charges and interest grew until the balance was £10k, i told them i couldn't pay this and reached an agreement for a one time payment of £3k to close the account. Would it be possible to claim PPI on this account? I don't know if i have any old statments on the account as i think i threw them when it closed. -

Hi guys I'd like your thoughts on this. I have a Barclaycard / ex-Egg account - that defaulted back in 2012. In middle of last year it was sold to Hoist and then Robinson Way came chasing. It's a familiar story. Last payment on this was February 2012 (default was Nov. 2012), so I'm thinking "you sods!". I sent CCA request which has taken them months to comply with (I have all the time in the world!). I finally received a recon from them this week, with an I&E sheet attached and 30 days complete it (keeps clock ticking ). Reading between the lines, I don't think they have a clue when this agreement commenced, but nor do I, to be honest. There isn't a date specified anywhere. On the bottom of the Egg recon it states "04_2006", but this only appears to be a copy of T&Cs, so probably isn't a compliant recon anyway. They certainly don't appear to have a copy of the original agreement, so from that perspective, I'm hoping this account is from pre-April 2007. All I know is that it's from around that time and could well be 2006, or could be a year later. With the six year anniversary of the last payment coming up next week, I'm hoping that I'll also have the SB option in my locker too. I'd prefer to eat up another few months though before I would feel confident having to rely on this should they issue a claim. I don't know if it affects anything, but I did enter into conversation with one of these Dor-2-Dor callers a few months after the last payment - they called to the house and caught me on the hop. How would you recommend I respond to the recon they sent me? I'm ideally looking to string them along for a little while longer if possible, although they might even keep sending begging letters for a few months without any form of prompting anyway. Cheers! Sham

-

Hi, I unsuccessfully claimed against Barclaycard for a mis-sell of egg card PPI back in 2015 (I was successful against Canada Square for my Egg loan) My Reasons were: the box was pre-ticked and having a relationship with Egg I had spoken to someone over the phone first who had advised that I must go online to apply, and as with the loan my chances were improved if I took out PPI. In addition I had a generous sick pay scheme and redundancy scheme at work. I then sent off a SAR to barclaycard requesting all of my statement information as well as the original application. They returned a ream of lovely dot matrix print outs (that they insisted I go into a branch to collect) and a reconstruction of my application.. .none of which was of any use to me in my hunt for further information, so I left the claim at that point. I recently became aware of a "failed SAR" and what it meant, so I sent another request to Barclays for the information, pointing out that they had failed to provide the relevant information requested. I have now had another ream of much easier to decipher a4 paper (delivered to my flat this time), this includes all of my statements as well as some information on my claim. This following stood out for me: Again they haven't provided my application, this time not even a reconstruction, just a page of settings & values, again it says "Y" for PPI and I am sure that this was pre-ticked The PPI rate climbed from 54p to 79p in the £ (with a mid range in the middle) within a very short space of time with no notification. I also have "finance charges" which I have asked for further explanations on, but I suspect were put in place when PPI took me over my limit as this was applied before payments were calculated Then the final and most worrying item, there is data about when my claim was filed and "settled", the settled date is correct, the claimed date is years out, which seems to indicate a lackadaisical approach to reviewing these claims, and a total lack of due care and diligence on their part, I can't believe that my claim was actually looked into bar data entry & sending out standard letters based on this information. In addition I now have the details of my exact sick pay offering as well as the letter sent when AXA were replaced as the underwriter of the insurance, this was the first inkling I had of this being optional and I turned off PPI soon afterwards. Given all this new info, and the fact that BC failed to hand some of it over at the first time of asking, am I right in thinking I could ask them to review my claim again even though the 6 months has long passed.

Hi, I unsuccessfully claimed against Barclaycard for a mis-sell of egg card PPI back in 2015 (I was successful against Canada Square for my Egg loan) My Reasons were: the box was pre-ticked and having a relationship with Egg I had spoken to someone over the phone first who had advised that I must go online to apply, and as with the loan my chances were improved if I took out PPI. In addition I had a generous sick pay scheme and redundancy scheme at work. I then sent off a SAR to barclaycard requesting all of my statement information as well as the original application. They returned a ream of lovely dot matrix print outs (that they insisted I go into a branch to collect) and a reconstruction of my application.. .none of which was of any use to me in my hunt for further information, so I left the claim at that point. I recently became aware of a "failed SAR" and what it meant, so I sent another request to Barclays for the information, pointing out that they had failed to provide the relevant information requested. I have now had another ream of much easier to decipher a4 paper (delivered to my flat this time), this includes all of my statements as well as some information on my claim. This following stood out for me: Again they haven't provided my application, this time not even a reconstruction, just a page of settings & values, again it says "Y" for PPI and I am sure that this was pre-ticked The PPI rate climbed from 54p to 79p in the £ (with a mid range in the middle) within a very short space of time with no notification. I also have "finance charges" which I have asked for further explanations on, but I suspect were put in place when PPI took me over my limit as this was applied before payments were calculated Then the final and most worrying item, there is data about when my claim was filed and "settled", the settled date is correct, the claimed date is years out, which seems to indicate a lackadaisical approach to reviewing these claims, and a total lack of due care and diligence on their part, I can't believe that my claim was actually looked into bar data entry & sending out standard letters based on this information. In addition I now have the details of my exact sick pay offering as well as the letter sent when AXA were replaced as the underwriter of the insurance, this was the first inkling I had of this being optional and I turned off PPI soon afterwards. Given all this new info, and the fact that BC failed to hand some of it over at the first time of asking, am I right in thinking I could ask them to review my claim again even though the 6 months has long passed. -

I got letter from solicitors, on behalf of Robinsons Way acting as agents for HPH (ex Barclaycard) on a debt they say originates from a legal agreement from 2004. This I believe relates to an old Egg debt, but BCard bought my Egg debt in 2011/12. I was paying Egg card small amount monthly, Egg stopped taking payments (not me defaulting) when BCard bought debt. Bcard wrote to me said I needed to change SO to their details and quote my Bcard as a reference!!! I didnt have BCard, it was an Egg card. I wrote and told them, they didnt reply, I didnt resume payments (Never made any payments to Bcard). That was in 2011/2012 not too sure of last payment date - have to scroll thru old bank statements, but never made any payments to BCard. Had various letters from Bcard, Robinson Way and other companies over the ensuing years, debt been passed off from one co to another. Now just received a Letter of Claim from solicitors saying they have legal agreement between me and original creditor (who they seem to be implying was BCard as no mention of Egg), and the date of that agreement. Said their "client" (think they mean BCard) purchased the account and it was legally assigned in July 17, Notice of Assignment sent to me - I not received! I have drafted a letter asking for a copy of the CCA, a full breakdown of the costs involved in the debt, and a copy of the Notice of Assignment. Will send recorded delivery tomorrow. I know they have 14 days to supply a legible true copy of the CCA -. My main thought is why has it taken them so long to initiate legal action if they have a good case? Any thoughts or advice please on what else I can do, Sorry for War and Peace!!

-

Hi Ive received out of the blue a court claim form from Arrow Global saying that I owe nearly £22k to Egg but Ive not heard anything for at least 10 years until now. Please can you advise me whats the best course of action as Ive acknowledged the claim on moneyclaim to get another 14 days on this. Can this debt be Statute Barred because of the age of it? I need to file my defence before 18 October before 4pm online. Ive sent a CCA request to Arrow & their Solicitor Restons and had a reply from both of them to say theyve requested CCA paperwork from Egg but so far I havent received anything since 4 October. I look forward to hearing from anyone soon. Thanks!

Hi Ive received out of the blue a court claim form from Arrow Global saying that I owe nearly £22k to Egg but Ive not heard anything for at least 10 years until now. Please can you advise me whats the best course of action as Ive acknowledged the claim on moneyclaim to get another 14 days on this. Can this debt be Statute Barred because of the age of it? I need to file my defence before 18 October before 4pm online. Ive sent a CCA request to Arrow & their Solicitor Restons and had a reply from both of them to say theyve requested CCA paperwork from Egg but so far I havent received anything since 4 October. I look forward to hearing from anyone soon. Thanks! -

Had an old egg card that I defaulted on back in 2010. Agreed payment of £1/month with egg then was informed barclaycard had assumed the debt. Continued to make my payments but they suddenly started getting rejected by barclaycard. Eventually cancelled the standing order. Last successful payment was may 2012 so about 9 months until it is statute barred. Now out of the blue had a letter to my old address (new occupant there has sent it on to me) saying Robinson Way on behalf of Hoist are instructed to recover the debt. First question is whether or not to ignore the letter as they still haven't quite found me? Can they start proceedings without having my correct address? From reading other posts on the forum it seems highly likely they wont be able to provide a true copy of my signed agreement they wont be able to take any enforcement action in which case making contact with them now would head off any likelihood of court proceedings that i dont know about. Any advice will be greatly appreciated.

-

Hello- background: debt dates to 2005 with a pre-approved credit card, the limit being increased and increased unasked unti 2008 when BAM! Then i set up a debt management plan with the CCCS, and paid into that until feb 2012 and not a penny since. A couple of weeks ago i got a phishing letter from wescot addressed to me at this address asking if the address was correct and saying if they didn't hear back they'd assume it was, no detail as to what it was for. I didn't reply. Today, letter from wescot saying they have been instructed by their client arrow global ltd-egg, to make contact with me to discuss the outstanding balance (£19,900) and telling me it is essential to contact them within the next 10 days to prevent further action. Now... what do you advise here? how likely are they to produce a CCA after so long? It's months away from being statute barred.. should i ignore it? I haven't heard anything for the last 3 years, i *think* they must have been given new address by old landlord getting sick of them constantly writing there. They don't have any certainty of my current address, are they likely to push for a CCJ under these circumstances? Advice gratefully received!

-

Hi there, I am hoping someone can help me - I tried unsuccessfully in Sept 2015 with Egg to get PPI back on 3 loan accounts and a credit card. These were taken out in 2004 and ran for many years before I paid them off - I believe early 2010. My reason is a simple one - I was diagnosed with Ulcerative Colitis in 1992 which is a lifelong chronic disease - I've had many operations and hospital stays/visits over the years, my last visit being as recent as 2 years ago. Certainly on the last loan, it was done on the phone and I was told I couldn't have the loan without taking out the insurance. I was stuck and therefore had to take it. The other applications were online at the time and I believe I never selected this product at all - at that time, these types of things were pointless for me as I couldn't get cover for the one thing I was always ill with. I dragged out the paperwork again last night and have 2 separate rejection letters from them - one relating to the loan accounts and one relating to the credit card - both from Canada Square. There is a glaring error on both which I am hoping will help me resurrect or at least re-submit. Both letters refer to 'my questionnaire' - the issue is I never filled one in - I sent a hand written letter to them with approx 3 or 4 sentences. They asked me to verify identity which was fine and then the next paperwork was we are looking at your case, followed by a rejection letter for both several weeks later. Does anyone think this is worth pursuing with them to re-open on the basis I did not fill in a questionnaire and therefore they did not have the required information to make an informed decision? I am planning on putting a letter together later today saying just that, but would like to post it here later on for advice to see if I have done it right. Any advice or thoughts are truly welcome - I'm so ill at the moment, so any money I can get from anywhere would really help me out. Okay - this is the letter that I have come up with - any advice gratefully received; Dear Sir/Madam, I am writing to you to request that my original claim reference numbers COM/261626/2015 and COM/071766/2014 are re-opened based on the following information; No questionnaire was ever provided to me to complete. You refer in your letters dated 17th and 21st September 2015 on both claims to ‘your questionnaire’ implying I completed one - which I did not. The information I provided you in my original letter dated July 2015 provided minimal information and as such you would not have had all information required to make an accurate assessment of my case. This would have included the following items being missing from my claim; Employment history and benefits available from those employers - of which I can provide proof. Details of my existing Medical condition - for which I can provide extensive documentation and proof. Your staff member who completed the questionnaire without my knowledge has failed me as a customer. I was not aware of this questionnaire at any point, I have no visibility of the contents of this questionnaire. Since vital information was missing from your assessment or was provided incorrectly by a member of your staff, it has distorted the outcome of your decision and should be reviewed as a matter of urgency. Based on the above information, I am convinced that I have not been treated fairly by your Company in this matter at all. Based on the information above, I insist that these cases are reviewed by a responsible person who can deal with the matter correctly and ascertain all the facts before making any decision. I am willing to provide both a completed questionnaire and further documentation that may be required by yourselves to review this matter accurately. To ensure that this matter is dealt with to my satisfaction, a copy of this letter has been sent to your CEO by signed for post; Mr Andrew Nettleton Citigroup Centre, Canada Square, London E14 5LB

Hi there, I am hoping someone can help me - I tried unsuccessfully in Sept 2015 with Egg to get PPI back on 3 loan accounts and a credit card. These were taken out in 2004 and ran for many years before I paid them off - I believe early 2010. My reason is a simple one - I was diagnosed with Ulcerative Colitis in 1992 which is a lifelong chronic disease - I've had many operations and hospital stays/visits over the years, my last visit being as recent as 2 years ago. Certainly on the last loan, it was done on the phone and I was told I couldn't have the loan without taking out the insurance. I was stuck and therefore had to take it. The other applications were online at the time and I believe I never selected this product at all - at that time, these types of things were pointless for me as I couldn't get cover for the one thing I was always ill with. I dragged out the paperwork again last night and have 2 separate rejection letters from them - one relating to the loan accounts and one relating to the credit card - both from Canada Square. There is a glaring error on both which I am hoping will help me resurrect or at least re-submit. Both letters refer to 'my questionnaire' - the issue is I never filled one in - I sent a hand written letter to them with approx 3 or 4 sentences. They asked me to verify identity which was fine and then the next paperwork was we are looking at your case, followed by a rejection letter for both several weeks later. Does anyone think this is worth pursuing with them to re-open on the basis I did not fill in a questionnaire and therefore they did not have the required information to make an informed decision? I am planning on putting a letter together later today saying just that, but would like to post it here later on for advice to see if I have done it right. Any advice or thoughts are truly welcome - I'm so ill at the moment, so any money I can get from anywhere would really help me out. Okay - this is the letter that I have come up with - any advice gratefully received; Dear Sir/Madam, I am writing to you to request that my original claim reference numbers COM/261626/2015 and COM/071766/2014 are re-opened based on the following information; No questionnaire was ever provided to me to complete. You refer in your letters dated 17th and 21st September 2015 on both claims to ‘your questionnaire’ implying I completed one - which I did not. The information I provided you in my original letter dated July 2015 provided minimal information and as such you would not have had all information required to make an accurate assessment of my case. This would have included the following items being missing from my claim; Employment history and benefits available from those employers - of which I can provide proof. Details of my existing Medical condition - for which I can provide extensive documentation and proof. Your staff member who completed the questionnaire without my knowledge has failed me as a customer. I was not aware of this questionnaire at any point, I have no visibility of the contents of this questionnaire. Since vital information was missing from your assessment or was provided incorrectly by a member of your staff, it has distorted the outcome of your decision and should be reviewed as a matter of urgency. Based on the above information, I am convinced that I have not been treated fairly by your Company in this matter at all. Based on the information above, I insist that these cases are reviewed by a responsible person who can deal with the matter correctly and ascertain all the facts before making any decision. I am willing to provide both a completed questionnaire and further documentation that may be required by yourselves to review this matter accurately. To ensure that this matter is dealt with to my satisfaction, a copy of this letter has been sent to your CEO by signed for post; Mr Andrew Nettleton Citigroup Centre, Canada Square, London E14 5LB -

Letter completely out of the blue from Canada Square : regarding commission paid on PPI (they had rejected the claim previously) "following a Supreme Court decision and new rules and guidance from the Financial Conduct Authority you can now make a new type of complaint to us about the sale of your PPI policy" I am assuming this is as a result of the recent landmark Plevin judgment?? There was a form to send back Does this also apply to previously settled PPI claims?? thanks as always

-

Hi I had a letter a couple of months back from Robinson Way regarding a Barclaycard account. I have never had a Barclaycard called them immediately and they told me that it was an egg card. I did have an Egg card several years back and this went in to a DMP but then the DMP Company went in to liquidation and hadn't been paying. I did make payments hug these were returned 'suspense' so didn't make it to the right person. I have checked my Experian and this account has dropped off my file. I don't know if it would be considered SB. How would I find this information out? They have written to me this week offering a 50% discount and then today offering 10 days to contact them before they start litigation proceedings. I cannot afford any negative points on my credit report at the moment so am not sure how to proceed. What would you advise?

-

Hey Guys. I was called by a company called Cabot on 15/08/2017 re debt. They didn't go into detail as i was on holiday. I ended up coming back later than planned and ended up coming back on 28th. Since then we have had some family emergencies so was unable to deal with stuff. I called them yesterday and they said they where calling in regards to an Egg loan (which i dont remember). They said they couldn't discuss things as the case had gone through to their sister company a Solicitors firm called Mortimer Clarke. I called Mortimer Clarke today. They said they cannot deal with the case as it was being claimed through the courts. I asked for details re the loan. All they could provide was: 1. a date the original loan was taken out (Dec 2007), 2. The default date. 3. The last payment date. They cant tell me: A. how much the loan was for B. Probably not be able to get the original credit agreement. C. Statement on the account D. How much the last payment was E. How much the default amount was I said if i put in a CCA request formally then do they have to provide. She said they may not have it. Although she was hesitant and trying to avoid the topic of the Agreement. I got an email address to send the formal CCA to. They said a bulk court claim had been put in and they couldn't do anything with the claim now until i respond to paperwork. I haven't lived at the address they said the details where sent to for about 2 to 3 years so haven't received anything. The girl provided me with a number for the court but no name so asked me to call them for a copy of the paperwork. I asked to put the account on hold and explained the situation about traveling but they where not having any of it. What do i do? Please help!

-

Hi there, I was really hoping for some help and advise on whether there is any way forward with this complaint. I complained to Canada Square about an egg credit card taken out in March 2001. I know that I did not opt in to take PPI - that the box was pre ticked, as I was also advised on the phone that the box had to be pre ticked to complete the application when I questioned it. They rejected my complaint as my personal circumstances meant I had no cover (significant sick pay or savings etc). I don't see how this is relevant. I took it to FOS and they rejected my complaint. I have questioned it and they say their records show it was opt in at this time. But I know this isn't true. Can anyone give any advice on how to proceed with this?

-

Hello I recently sent a SAR to Barclay for an Egg Credit Card I held from 2001. The account is no longer open but I am currently paying off the balance. I have been searching through the information that was sent to me but all I have received are microfische versions of the statements. I have all the balances from month to month but unable to ascertain whether I was paying PPI on this account. I do know that I applied for this account online and I had transferred the balance over from another card when I first opened it. I have noticed the card had something called Egg Rewards and stating it had up to 10% Insurance savings built in. I am not sure whether this is anything to do with PPI? Any help would be greatly apprtiated Dagenham Dave

-

So here's the latest in my Egg adventures. I've had a letter from Barclaycard referring to an EGG debt, to an old address. It's attached here. It refers to a default that hasn't appeared on my file as yet. I'm fairly certain (although I don't think I have a record) that the account was defaulted in 2004. Here's the fun part - it was from an Egg credit card, Now this. Do I CCA Barclaycard for the Egg details instead? Egg_Barclaycard_default_26-02-17.pdf

-

My Daughter has be hassled by Shoosmiths/ARC over an alleged debt with Egg, this started in March 2011 several DCA's have written and to each we have sent a S78 request, and had nothing returned other than a blank 'example' agreement. A couple of years ago Shoosmiths issued court papers to which I filed a defence on her behalf, pointing out that S78 had not been complied with and that a multitude of DCA's and solicitors had written a range of letters alleging debts but for a number of varying amounts. Shoosmiths responded by withdrawing the court application, out off the blue today we get a letter threatening an application for Summary Judgment, and wanting us to set up an agreement for repayment with them. My Daughter had a nervous breakdown several years ago 2007/8 and genuinely has no recollection of these debts and I have been managing them on her behalf, in may cases PPI has more than covered the debt but Shoosmiths have been particularly difficult to deal with and if this is a genuine debt then it will almost certainly have PPI attached to it, but apart from a bare minimum of information they have given me nothing to work with. I feel like calling their bluff, but the amount they are claiming is around £2k0 and if genuine is not a single debt but a number rolled into one, or has a significant amount of charges added. What would be my best course of action? Thanks in advance.

My Daughter has be hassled by Shoosmiths/ARC over an alleged debt with Egg, this started in March 2011 several DCA's have written and to each we have sent a S78 request, and had nothing returned other than a blank 'example' agreement. A couple of years ago Shoosmiths issued court papers to which I filed a defence on her behalf, pointing out that S78 had not been complied with and that a multitude of DCA's and solicitors had written a range of letters alleging debts but for a number of varying amounts. Shoosmiths responded by withdrawing the court application, out off the blue today we get a letter threatening an application for Summary Judgment, and wanting us to set up an agreement for repayment with them. My Daughter had a nervous breakdown several years ago 2007/8 and genuinely has no recollection of these debts and I have been managing them on her behalf, in may cases PPI has more than covered the debt but Shoosmiths have been particularly difficult to deal with and if this is a genuine debt then it will almost certainly have PPI attached to it, but apart from a bare minimum of information they have given me nothing to work with. I feel like calling their bluff, but the amount they are claiming is around £2k0 and if genuine is not a single debt but a number rolled into one, or has a significant amount of charges added. What would be my best course of action? Thanks in advance.

-

Hi There. My wife has just received through the post an attachment of earnings form from the MCOL Business centre. A CCJ was awarded in default as was sent to a previous address. My wife only found out about it when she received a Noddle credit profile change notification. She spoke to Robinson Way who advised it was issued at a previous address. She gave them our new address and interestingly the attachment of earnings form has come through to our current address. Details of the debt: Original creditor was Egg (so suspect any CCA would be "interesting" to say the least) Default was issued in 2012 according to her credit report Original agreement was taken out we think in about 2006. Balance was about 1650 CCJ balance was just over 2.5k (plus now another £110 attachment of earnings fee added) We are convinced the debt is statute barred as my wife is convinced she hasn't paid anything towards this for a long time. I know we need to look at getting this set aside but unfortunately we cannot afford the fee to do so, and we don't fall into the category where we can have the fees waived. Is there any other way around this? Surely they would have records and would know when the last payment was made, so if so then is this not an abuse of court process by submitting the claim? Any advice on next steps would be greatly appreciated.

Hi There. My wife has just received through the post an attachment of earnings form from the MCOL Business centre. A CCJ was awarded in default as was sent to a previous address. My wife only found out about it when she received a Noddle credit profile change notification. She spoke to Robinson Way who advised it was issued at a previous address. She gave them our new address and interestingly the attachment of earnings form has come through to our current address. Details of the debt: Original creditor was Egg (so suspect any CCA would be "interesting" to say the least) Default was issued in 2012 according to her credit report Original agreement was taken out we think in about 2006. Balance was about 1650 CCJ balance was just over 2.5k (plus now another £110 attachment of earnings fee added) We are convinced the debt is statute barred as my wife is convinced she hasn't paid anything towards this for a long time. I know we need to look at getting this set aside but unfortunately we cannot afford the fee to do so, and we don't fall into the category where we can have the fees waived. Is there any other way around this? Surely they would have records and would know when the last payment was made, so if so then is this not an abuse of court process by submitting the claim? Any advice on next steps would be greatly appreciated. -

Hi Firstly, those in debt finding it hard to see light at the end of the tunnel, don't be disheartened, it can be done. After 8 years, I am within 9 months of being debt free. however, this hasn't been without issues and I could do with some advice on what should be my last issue.... Sorry for the length, just don't know best course of action... thanks in advance for any help I defaulted on an Egg credit card, they sold the debt to Arc Europe. Barclaycard bought Egg. Barclaycard transferred the debt to Moorcroft. I have consistently paid the agreed monthly amount. However, during the transfer from Arc to Moorcroft 3 payments went to Arc totalling c£250. In July 2016, Moorcroft sent me a letter stating an incorrect outstanding balance, incorrect by the same c£250 exactly. In November 2016, I wrote the following to Moorcroft (names & reference no's excluded, and amounts rounded to avoid identification).. In reply to your letter dated dd/07/2016 stating the balance was £x. I disagree with this balance, my balance is £y. This represents a difference of c£250, which equates to monthly payments of £z. My account transferred from ARC to Moorcroft in September 2011. At this time, my balance with ARC was £6k, before my September 2011 payment. This is confirmed in your letter dated dd/10/2011. I am not aware of missing any payments, can you provide a full breakdown of the account including any interest or charges applied please? Today, I believe the balance is £a. I will not pay any additional balance until I receive a full breakdown of the account including any interest or charges applied. Please do provide a full breakdown of the account including any interest or charges applied. Today, they have responded with (pleasantries have been excluded) Our client has advised that they have a balance of c£900 on their system. a letter is attached from our client as confirmation. The attached letter (on very poor Barclaycard letterhead and unprofessional format) says dd/12/2016 Dear Sir/Madam RE : My name - Account No. my account number Thanks for contacting us. Unfortunately, statements are no longer produced on the above account. I can confirm that the outstanding balance of the Account As of today is c£900. I trust this information is of assistance to you. Any queries, contact us, we are here to help. So in summary, I know why we disagree with the balance. Moorcroft won't acknowledge this. Moorcroft have created a fictitious letter from Barclaycard trying to pass it off as from Barclaycard. The debt is no longer on my credit file, it is clean. I suspect if I contact Barclaycard they won't recognise the account. All payments since Sept 11 have been paid to Moorcroft using their reference number, except the 3 made to ARC. what do I do? 1) stop payments immediately 2) report Moorcroft to FCA 3) subject access request to Moorcroft 4) send Moorcroft a firm letter as per - you are wrong. payments have been made to Moorcroft not Barclay - you are fraudulent. you should create fictitious letters using someone else letterhead. - offer 10% of the correct balance to go away? help please....

-

Hello I am new to the site always been a watcher and reader. Recently requested a CCA on account that is managed by idem (previously EGG) because it was pre 2007. They have sent through a copy but I am unsure where I stand to whether it is enforceable. I have a scanned copy in PDF Please can someone help me I have been quite successful on negotiating F&F on other accounts and am trying to finalise on others with Barclaycard (Link), PRA Virgin Active. RS1.pdf

-

Good evening I am hoping somebody can help me with advise. My wife currently owns a house with her mum. Her mum moved out about 9 years ago when she remarried and instead of selling my wife went onto the mortgage and became 50% owner. they have had an offer on the house and are in the process of selling. The solicitor today rang to say we they aware of a charging order in mother in laws name. She didn't have a clue about it but so far has managed to find out the following: The DCA is Cabot. They have said that she needs to speak with the Solicitors 'Wright Hassall' (seems a really apt name!!!!) She contacted solicitors and they have said that the original debt was with Egg (apparently. Until MIL said she has never had an egg credit card, they mentioned two other potential creditors it could be) The charging order was on the 16/12/2013 for a fee of £6,113.25. The last payment (or default, she can't remember) on this account is 02/07/2007. The account balance was £5066.25 She has never had a credit card so obviously wants to dispute this in its entirety. She didn't live at the address the letters were sent to so was unaware of the judgements. I have told her that she needs to request a CCA from the solicitors etc. The problem is, the house sell. Obviously they don't want to pay this, but will not be able to sell the house if they dispute it. Can they dispute it retrospectively? really really really appreciate the advice given

Good evening I am hoping somebody can help me with advise. My wife currently owns a house with her mum. Her mum moved out about 9 years ago when she remarried and instead of selling my wife went onto the mortgage and became 50% owner. they have had an offer on the house and are in the process of selling. The solicitor today rang to say we they aware of a charging order in mother in laws name. She didn't have a clue about it but so far has managed to find out the following: The DCA is Cabot. They have said that she needs to speak with the Solicitors 'Wright Hassall' (seems a really apt name!!!!) She contacted solicitors and they have said that the original debt was with Egg (apparently. Until MIL said she has never had an egg credit card, they mentioned two other potential creditors it could be) The charging order was on the 16/12/2013 for a fee of £6,113.25. The last payment (or default, she can't remember) on this account is 02/07/2007. The account balance was £5066.25 She has never had a credit card so obviously wants to dispute this in its entirety. She didn't live at the address the letters were sent to so was unaware of the judgements. I have told her that she needs to request a CCA from the solicitors etc. The problem is, the house sell. Obviously they don't want to pay this, but will not be able to sell the house if they dispute it. Can they dispute it retrospectively? really really really appreciate the advice given -

Debt from June 2002 £8,500 sold by Barclays to Arrow Global. I have been dealing with Capquest until Nov 2015, and paying £5 per month, when I asked for a copy of my agreement and had reply from Capquest in Feb 2016, saying account on hold whilst they request the documentation from Arrow. I heard nothing more until last week when I had a letter from Wescot asking if I was the person they referred to and to contact them. I did nothing. Then a letter today from Arrow saying that Westcot is now managing my debt and asking me to contact Wescot. Odd thing is I have always dealt via a friends address to avoid embarassment and the last two letters came to my address not my friends. What do i do?

-

Name of the Claimant ? Arrow Global Date of issue – top right hand corner of the claim form – this in order to establish the time line you need to adhere to. 4th August 2016 Date of issue XX + 19 days ( 5 day for service + 14 days to acknowledge) = XX + 14 days to submit defence = XX (33 days in total) - 6th September What is the claim for – the reason they have issued the claim? Please type out their particulars of claim (verbatim) less any identifiable data and round the amounts up/down. The claimant claims payment of the overdue balance due from the defendent under a contract between the defendent and Egg dated on or about Mar 30 2006 and assigned to the claimant on Nov 30 2015. What is the value of the claim? £4000 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Unsecured loan When did you enter into the original agreement before or after 2007? Before Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. It is the debt purchaser who issued claim Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes Did you receive a Default Notice from the original creditor? Not sure Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? Financial difficulties What was the date of your last payment? June 2011 although they claim July Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? Yes Hi I received a claim form from Restons on behalf of arrow global. It's from a loan taken out in 2006. I got into financial difficulties in 2011 after entering into a reduced payment arrangement for a few months I stopped paying. I hadn't heard anything from them until recently. I have read lots of threads and have acknowledged the claim with intent to defend. I realise I have to send a CCA and CPR 31.14 Request. I would like to know whether I can ask for the notice of assignment, default notice, termination notice and statement of account if none of these documents are mentioned in the particulars of the claim? They only mention 'a contract'. Is this covered by the CCA request or should I put this in the CPR 31.14 Request too? Many thanks for your help

-

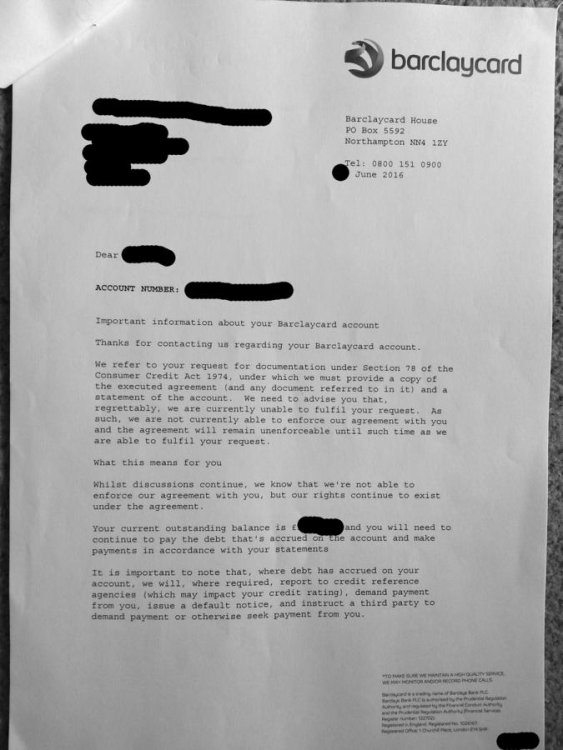

I have an old Egg credit card which went into default a number of years ago after I had to close my business. I have been paying £1 per month for a couple of years now. The payments are going through Capquest. Last time they asked for a financial update i asked for a copy of the original loan agreement. As I understand it Barclaycard took over Egg cards a number of years ago. I have attached a copy of the letter with details blanked out - the outstanding is around £3000. In the letter B/card state that they cannot currently fulfil my request, and as a result the outstanding is unenforceable. What should I do now? Should I stop payments until they can prove the liability? Should I offer them £100 in full and final? The default obviously still shows on my credit file. Many thanks TW