Search the Community

Showing results for tags 'county court'.

-

Hi Redroy. Any luck with obtaining these hire costs back yet? Am asking as it seems I am in the exact same position as you are right now. Ive been told by OCL solicitors that third party are Hi Redroy, any luck with this yet? I am in exact same position as you was last year. Have been told by OCL solicitors that third party are disputing the excessive car hire amount and want to know why i chose to take an expensive car out of hire. I feel trapped as i explained to OCL that One Call insurance deferred me to the hire company and made it seem all seemingless and painless. Now its been 7 months and I am dealing with a court mitigation with third party regarding costs for car hire and injury. This was a 100 percent non fault claim.

-

Papers from SAR shows shockingly very high charges from 2009 to 2013 within period I lost my job and was struggling financially, can I seek refund from OC? Just after calling OC and asking for complaint procedure and address, I received letter stating small % of charges will be refunded but paid directly to Lowell? What's your opinion guys?

- 22 replies

-

- 1

-

-

- county court

- defending

- (and 1 more)

-

I am a small independent skincare maker. I purchased the service of MyHermes to collect and deliver 4 parcels of wholesale skincare goods to a stockist, and 3 were lost. * 2 parcels had their last scan at the Hermes depot Jun 1st '18, and haven't been seen since. * 1 parcel made it to the destination OK. * 1 parcel was said to have been delivered but was never received, and at some point I was told the delivery scan happened on the other side of town to where the parcel was supposed to go. MyHermes say they've conducted multiple sweeps of the warehouse and can't find them, and have offered me £50 only as a 'good will gesture', which is insulting. I have taken the case through the small claims procedure and it’s been moved from different courts/online to court / different judges etc, and finally now there is a hearing date. I was hoping to settle this without a hearing as I don’t have a lawyer. Hermes claim as the contents is liquids they don’t cover them in their terms. I labelled the boxes as ‘Skincare’ and they took them anyway. And it’s beside the point what the contents were since the boxes were lost/stolen. I'm claiming for the wholesale price of these goods. The case is for around £4,600 including the court costs. I have to pay another £355 hearing fee now, on top of the few hundred I’ve already paid to make the small claims case. Do I continue? Can I go to a hearing without a lawyer and be successful? Do I have any chance? I’m just so sick of all this. I have only a few days (until the 8th March) to pay the hearing fee so I need to decide ASAP whether this is worth it. I would so so appreciate some help or support from someone who knows much more about this than me!

I am a small independent skincare maker. I purchased the service of MyHermes to collect and deliver 4 parcels of wholesale skincare goods to a stockist, and 3 were lost. * 2 parcels had their last scan at the Hermes depot Jun 1st '18, and haven't been seen since. * 1 parcel made it to the destination OK. * 1 parcel was said to have been delivered but was never received, and at some point I was told the delivery scan happened on the other side of town to where the parcel was supposed to go. MyHermes say they've conducted multiple sweeps of the warehouse and can't find them, and have offered me £50 only as a 'good will gesture', which is insulting. I have taken the case through the small claims procedure and it’s been moved from different courts/online to court / different judges etc, and finally now there is a hearing date. I was hoping to settle this without a hearing as I don’t have a lawyer. Hermes claim as the contents is liquids they don’t cover them in their terms. I labelled the boxes as ‘Skincare’ and they took them anyway. And it’s beside the point what the contents were since the boxes were lost/stolen. I'm claiming for the wholesale price of these goods. The case is for around £4,600 including the court costs. I have to pay another £355 hearing fee now, on top of the few hundred I’ve already paid to make the small claims case. Do I continue? Can I go to a hearing without a lawyer and be successful? Do I have any chance? I’m just so sick of all this. I have only a few days (until the 8th March) to pay the hearing fee so I need to decide ASAP whether this is worth it. I would so so appreciate some help or support from someone who knows much more about this than me! -

Hi, just had this arrive over the weekend In order for us to help you we require the following information:- Name of the Claimant ? Hoist Finance UK Holdings Date of issue – 19th Feb 2019 Particulars of Claim 1. The claim is for the sum of £5xxx.xx in respect of monies owing under an agreement with the account number: 12345 pursuant to the consumer credit act 1974 (CCA). 2.The debt was legally assigned by Hoist Portfolio Holding (EX Aqua) to the claimant and notice has been served. 3.The defendant has failed to make contractual payments under the terms of the agreement. A default notice has been served upon the defendant pursuant to s.87(1) CCA The claimant claims 1. The sum of £5xxx.xx 2. costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ? No Have you changed your address since the time at which the debt referred to in the claim was allegedly incurred? No Did you inform the claimant of your change of address? N/A What is the total value of the claim? £5xxx.xx Is the claim for - a Bank Account (Overdraft) or credit card or loan or catalogue or mobile phone account? Credit Card When did you enter into the original agreement before or after April 2007 ? After Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ? Yes Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Not sure Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure Why did you cease payments? Down turn in business What was the date of your last payment? Mid 2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Was in DMP but had trouble with them. Thanks

-

Any help appreciated I bought a car on HP in 2003, It was beyond my means and I only made 4 repayments -the car was repossed in 2005. I had a company called Marlin ringing me at work constantly and I was bullied into paying £15pm - I moved house and changed banks and the payments stopped in 2013. In 2015 I had letters from Cabot requesting money - over the years I have argued with them over the debt. They say it was assigned to them in 2016 yet I have statements from the original HP company in 2007 showing the balance - so how can they have it assigned if it was still with the original lender. It was due to become statute barred on 01/02/19 - however Mortimer issued an online claim on 27/12/18 - I defended and requested a SAR - they have only sent me 2 out of 9 pages of the credit agreement - which includes PPI and Gap insurance. There are various inconsistencies in the paperwork, dates amounts etc. Do I stand a chance in court of getting the claim in my favour or should I just negotiate with the Solicitor on a reduced amount?

Any help appreciated I bought a car on HP in 2003, It was beyond my means and I only made 4 repayments -the car was repossed in 2005. I had a company called Marlin ringing me at work constantly and I was bullied into paying £15pm - I moved house and changed banks and the payments stopped in 2013. In 2015 I had letters from Cabot requesting money - over the years I have argued with them over the debt. They say it was assigned to them in 2016 yet I have statements from the original HP company in 2007 showing the balance - so how can they have it assigned if it was still with the original lender. It was due to become statute barred on 01/02/19 - however Mortimer issued an online claim on 27/12/18 - I defended and requested a SAR - they have only sent me 2 out of 9 pages of the credit agreement - which includes PPI and Gap insurance. There are various inconsistencies in the paperwork, dates amounts etc. Do I stand a chance in court of getting the claim in my favour or should I just negotiate with the Solicitor on a reduced amount? -

Hi I'm new to all this so I apologise in advance if i've made any mistakes. I had a contract with BT back in 2015 which I wanted to finish early due to the constant slow speeds I was getting after 2 months of being with them. At one point I cancelled my direct debits in protest until they sent an engineer out to have a look at why my internet was so slow. When an engineer was promised to be sent out I called to re-instate my direct debits and was asked which date I wanted them to come out. I asked for the start of the month which was agreed but a few weeks later I had a direct debit come out in the middle of the month. I questioned this and was told they couldn't do a specific date unless I agreed to estimated billing. This was not what I had earlier agreed and they were not willing to do anything about it so for me it was the final straw. I asked if I could end the contract early due to the poor service but was told I would have to pay the remainder off which was over £300. I refused to pay this obviously and was sent various debt collect letters which I ignored stupidly thinking they would eventually give up. Now after all this time I get a letter from the small claims court as Lowell acting of behalf of BT saying they want their £300. I've sent off the acknowledgement but i'm not sure what to do from here, do I defend or do I need to counterclaim? I feel BT were in breach of contract and according to their own terms they would look at ending a contract early due to poor service but I don't feel they ever really considered it. I would really appreciate any help please. Thank you

-

Hi Folks, Been disputing a debt with Cabot for some time and eventually it has been issued as a claim to which I have responded as per the guidance in the forum. Very helpful thank you. So back in December 2018 I filled out my AOC and then 31CPR and then my Defence. Today I received a letter from Cabot chasing the debt asking me to pay, are they allowed to send me a letter to collect when it has now been escalated to a court case? Where do I stand? Any thoughts, guidance, greatly and warmly received. Thanks.

-

Today I checked my credit file for the sheer hell of it. Personally I'm not bothered what it says as I don't borrow money. Made those mistakes years ago and now my file is at zero. However what I did find was a CCJ for £280 issued last October. Whoever the claimant was didn't write to me at my current address despite being on the electoral register and not at my previous one. They sneakily wrote to the old address so as to win by default. I have a very good idea who this, but it doesn't show on my credit file, just a claim number. I am guessing here but I think it may be a debt collector who has been harassing me for years over this alleged debt It was to Orange for a mobile contract which I had never has. ( I was the victim of ID fraud and they did other things too ). Despite many, many letters asking them for proof like the Deed of Assignment, Deed of Novation and a contract that proves I am the debtor and responsible, they have ignored me. To then sue me using an old address when they only wrote again only yesterday to my current one, I find this extremely bad practice that flies in the face of all the guidelines on debt collections. This is just spite of their behalf, nothing more. Today I wrote to that Mickey Mouse court called Northampton business centre where no judge ever sets foot and asked for the judgement to be set aside as I have not been notified and I have been denied my right to defend myself. Also I issued a counterclaim for a considerable sum as set down by a judge in a similar situation where PC World sued a man over a computer and filed an inaccurate and untruth report on his credit file. Now what will happen? Will my set aside be successful as it really is a bit cheeky to sue somebody deliberately using an old address so that you win by default. This smacks of a certain debt collector who we are all familiar with on this forum.

Today I checked my credit file for the sheer hell of it. Personally I'm not bothered what it says as I don't borrow money. Made those mistakes years ago and now my file is at zero. However what I did find was a CCJ for £280 issued last October. Whoever the claimant was didn't write to me at my current address despite being on the electoral register and not at my previous one. They sneakily wrote to the old address so as to win by default. I have a very good idea who this, but it doesn't show on my credit file, just a claim number. I am guessing here but I think it may be a debt collector who has been harassing me for years over this alleged debt It was to Orange for a mobile contract which I had never has. ( I was the victim of ID fraud and they did other things too ). Despite many, many letters asking them for proof like the Deed of Assignment, Deed of Novation and a contract that proves I am the debtor and responsible, they have ignored me. To then sue me using an old address when they only wrote again only yesterday to my current one, I find this extremely bad practice that flies in the face of all the guidelines on debt collections. This is just spite of their behalf, nothing more. Today I wrote to that Mickey Mouse court called Northampton business centre where no judge ever sets foot and asked for the judgement to be set aside as I have not been notified and I have been denied my right to defend myself. Also I issued a counterclaim for a considerable sum as set down by a judge in a similar situation where PC World sued a man over a computer and filed an inaccurate and untruth report on his credit file. Now what will happen? Will my set aside be successful as it really is a bit cheeky to sue somebody deliberately using an old address so that you win by default. This smacks of a certain debt collector who we are all familiar with on this forum. -

Hello, I have today received a letter from High Court Enforcement Group Ltd demanding payment for an old university tuition fee debt. I have recently changed address and I had no idea this had got to the court stage, so I didn't get a chance to respond to the claim. I would like to be able to get this case back in the court system because I would like to defend it. The reason I didn't pay the tution fees is that after one term I realised the course being taught was nothing like what they had detailed in all their marketing. I soon realised that this MA course was not going to help me any further with a career and would just add another £10,000 debt to my student debt already. Had I known that this was at the court stage I would gladly have defended the action against me. I know it's my fault I didn't inform the University of my new address but I am now on long term sick and awaiting treatment. I am in receipt of ESA and in the support group, I get the full benefit after the DWP changed their decision once they had received medical reports. I really hope at the very least my current circumstances will delay the debt process escalating further but I really don't know what to do. I have never been in this situation before and I know once it's at this stage it's very serious. I really didn't need this. I have just about managed to keep up with all my current bills and debts with minimal income but this is something else. Any help or advice would be very gratefully received. Jake

Hello, I have today received a letter from High Court Enforcement Group Ltd demanding payment for an old university tuition fee debt. I have recently changed address and I had no idea this had got to the court stage, so I didn't get a chance to respond to the claim. I would like to be able to get this case back in the court system because I would like to defend it. The reason I didn't pay the tution fees is that after one term I realised the course being taught was nothing like what they had detailed in all their marketing. I soon realised that this MA course was not going to help me any further with a career and would just add another £10,000 debt to my student debt already. Had I known that this was at the court stage I would gladly have defended the action against me. I know it's my fault I didn't inform the University of my new address but I am now on long term sick and awaiting treatment. I am in receipt of ESA and in the support group, I get the full benefit after the DWP changed their decision once they had received medical reports. I really hope at the very least my current circumstances will delay the debt process escalating further but I really don't know what to do. I have never been in this situation before and I know once it's at this stage it's very serious. I really didn't need this. I have just about managed to keep up with all my current bills and debts with minimal income but this is something else. Any help or advice would be very gratefully received. Jake -

Commission applies to High Court to appoint an Official Receiver to charity -Thrift Urban Housing Limited READ MORE HERE: https://www.gov.uk/government/news/commission-applies-to-high-court-to-appoint-an-official-receiver-to-charity

Commission applies to High Court to appoint an Official Receiver to charity -Thrift Urban Housing Limited READ MORE HERE: https://www.gov.uk/government/news/commission-applies-to-high-court-to-appoint-an-official-receiver-to-charity -

About two weeks ago (Jan 2019) I received a letter from DrysdensFairfax solicitors acting on behalf of CapQuest for a debt of £9900.07 which I want to defend on the basis of its being and unenforceable debt. The original credit agreement was with Virgin Money and dates from 2005 The original default letter dates from 2009. The debt has increased due to 'various court charges etc charges' that aren't itemised They issued court proceedings in 2014 which I defended, and they put a stay on the case.. they have recently requested for the stay to be lifted and a court date has been set for March 2019. I have objected to this for many reasons (it seems very poor professional practice to delay a case for no reason for almost 10 years. I currently have a completely clear credit record with no loans/credit cards/defaults of any kind on it. The court date of 1st March seems very soon for me to prepare my defence. Can I ask for it to be delayed. Any advice much appreciated. Thank you

About two weeks ago (Jan 2019) I received a letter from DrysdensFairfax solicitors acting on behalf of CapQuest for a debt of £9900.07 which I want to defend on the basis of its being and unenforceable debt. The original credit agreement was with Virgin Money and dates from 2005 The original default letter dates from 2009. The debt has increased due to 'various court charges etc charges' that aren't itemised They issued court proceedings in 2014 which I defended, and they put a stay on the case.. they have recently requested for the stay to be lifted and a court date has been set for March 2019. I have objected to this for many reasons (it seems very poor professional practice to delay a case for no reason for almost 10 years. I currently have a completely clear credit record with no loans/credit cards/defaults of any kind on it. The court date of 1st March seems very soon for me to prepare my defence. Can I ask for it to be delayed. Any advice much appreciated. Thank you -

Hi all, Firstly I wasn't quite sure which area to post this, so apologies if I've got the wrong place. Right, to my question. I won £6500 on an online casino last July and they are refusing to pay me. I have done all of the SAR, online mediation, contacting the CEO of the company, involving the gambling commission etc etc to no avail. The casino's stance is basically "take us to court". I'd love to as I've got a water-tight case, but the problem is that they're based in Malta with no UK service address. Questions: - Am I correct in thinking that I have to take them to court in Malta? and if yes.. - Does anybody know how to do this and if there are any solicitors who may specialise in these type of overseas disputes? - Any other general advise on how best to proceed? For info, the casino involved is Slotty Vegas and their parent company is Max Entertainment. Many thanks, Lee.

-

Court bans mobility equipment boss for 6 years - Churchills Homecare READ MORE HERE: https://www.gov.uk/government/news/court-bans-mobility-equipment-boss-for-6-years

-

I owe one of my creditors £32000, (more than half of this is their solicitors costs) after speaking with Business Debtline and preparing a budget I offered them £440 per month. They got a order for me to attend court for questioning. I went to the court with the documents requested which were statments for all bank accounts, HMRC returns etc. Their solicitor was there and asked me questions regarding my income, (although they hadn't listed their questions before hand) After court the solicitor wrote and asked me to supply my bank staments since 2017, I replied they have seen all my current financial position and ability to pay. They have written back today to say they are trying to deal with this amicably and if I dont send through what they want they will get a court order and those further costs will be added on to my debt. Can they get a court order to see that far back?

I owe one of my creditors £32000, (more than half of this is their solicitors costs) after speaking with Business Debtline and preparing a budget I offered them £440 per month. They got a order for me to attend court for questioning. I went to the court with the documents requested which were statments for all bank accounts, HMRC returns etc. Their solicitor was there and asked me questions regarding my income, (although they hadn't listed their questions before hand) After court the solicitor wrote and asked me to supply my bank staments since 2017, I replied they have seen all my current financial position and ability to pay. They have written back today to say they are trying to deal with this amicably and if I dont send through what they want they will get a court order and those further costs will be added on to my debt. Can they get a court order to see that far back? -

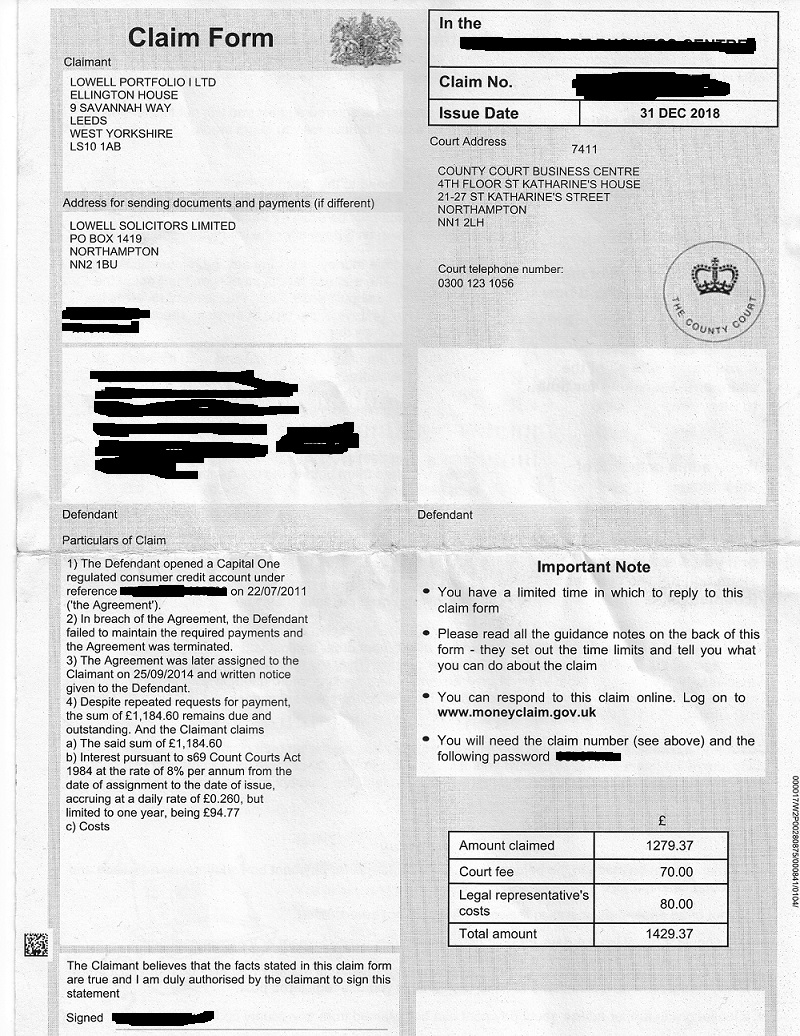

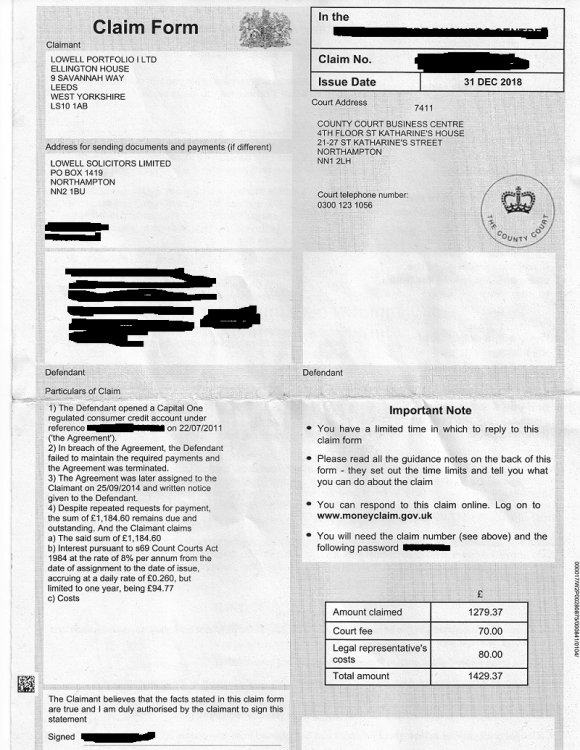

Hi I received County court claim back on Friday 4th January despite it states issue date 31 December 2018 it did not arrive in post until then but no matter what I assume date on paper work stands. I then received 15th January a warning from Lowell that they had sent it to court and I should receive something soon their letter was dated 7th January so that came very late. Okay I will get to the facts really hoping for your urgent help and assistance in this as I have suffered with sickness this month and also at same time struggled as had to keep work balance. I don’t want to use any excuses other then It was easier for me to hide this away and just wish for better things. But I did submit my AOS and full defence within the 2 weeks on Sunday 13th January and was received and noted by court on Monday 14th January. I did receive the proper letter regarding Lowell would submit to court and I had the 30 days before end of November 2018 so they followed rules for that. To try put facts about my debt down short basically was a credit card I took out with Capital One back in 2011. To be fair I am not 100% sure when my last payment was and if its statue barred. It was at a lower limit then years later was setup to £1000 limit. I fell into a dispute regarding some £12 charges etc and also had contact through phone and emails I then stopped payments and kept going up. I did not get proper response on my emails etc I was even trying to settle a solution. My fault for ignoring further letters with request for payments and debt was sold to solicitor Lowells in 2014. To cut to the chase I need to submit my defence tonight as I understand and I have not got CCA and CPR (31.14) letters sent off despite I have made them ready. Can I still get these sent off tomorrow morning with Royal mail 1st class recorded delivery and then attach £1 postal order for each? Also because of my dispute with Capital One I really wish to claim back all charges and the 8% interest etc but how do I deal with this now? Can I sent letter to them or does that has to go to Lowell? Hope for your assistance guys I would be so grateful. I have attached Claim Form and also I have done a draft Defence for me to submit tonight hope it looks okay? here is my defence draft Defence 1. The Defendant contends that the particulars of claim are vague and generic in nature. The Defendant accordingly sets out its case below and relies on CPR r 16.5 (3) in relation to any particular allegation to which a specific response has not been made. 2. Paragraph 1 is noted. I have had an agreement in the past with Capital One but any alleged balance is and remains in dispute for charges/services. 3. Paragraph 2 is denied I am unaware of any legal assignment or Notice of Assignment allegedly served over 1 year ago. 4. It is therefore denied with regards to the Defendant owing any monies to the Claimant, the Claimant has failed to provide any evidence of agreement/assignment/balance/breach requested by CPR 31. 14, therefore the Claimant is put to strict proof to: (a) show how the Defendant has entered into an agreement with the Claimant; and (b) show how the Defendant has reached the amount claimed for; and © show how the Claimant has the legal right, either under statute or equity to issue a claim; 5.As per Civil Procedure icon Rule 16.5(4), it is expected that the Claimant prove the allegation that the money is owed. 6. On the alternative, if the Claimant is an assignee of a debt, it is denied that the Claimant has the right to lay a claim due to contraventions of Section 136 of the Law of Property Act and Section 82A of the consumer credit icon Act 1974. 7. By reasons of the facts and matters set out above, it is denied that the Claimant is entitled to the relief claimed or any relief. Signed I am the Defendant - I believe that the facts stated in this form are true xxxxxxxxxx 27/01/2019 Defendant's date of birth x/x/19xx Address to which notices about this claim can be sent to you xxxxxxxxxxxx

-

I recently won a ccj against my brother. Once the ccj was given, with a debt of £40k my brother declared himself bankrupt. Prior to declaring himself bankrupt he transferred £30k to a third party bank account (he did not declare this when we were in court regarding the debt he owed me). The Official Receivers found this transaction. We are yet waiting to hear who this money was transferred to, my guess is another sibling. Also he transferred for nil value land and a house in Canada to his now ex wife, who he divorced just prior to going bankrupt. I am hoping these property transactions can be reversed as the total sum for both is around £45k. I am the only creditor so if any monies are received will the receivers reimburse themselves before paying me?

I recently won a ccj against my brother. Once the ccj was given, with a debt of £40k my brother declared himself bankrupt. Prior to declaring himself bankrupt he transferred £30k to a third party bank account (he did not declare this when we were in court regarding the debt he owed me). The Official Receivers found this transaction. We are yet waiting to hear who this money was transferred to, my guess is another sibling. Also he transferred for nil value land and a house in Canada to his now ex wife, who he divorced just prior to going bankrupt. I am hoping these property transactions can be reversed as the total sum for both is around £45k. I am the only creditor so if any monies are received will the receivers reimburse themselves before paying me? -

hello everyone. just started this thread for a colleague, who needs some advice and is not very good with computers. history of debt Barclaycard credit card 01/2008 debt management 08/2009 arranged with Barclays a reduced payment plan which was accepted while on the debt management plan. PRA GROUP was assigned the debt from Barclaycard 08/2015 Last payment made 02/2018 Name of the Claimant ? PRA Group Date of issue 17/01/2019 What is the claim for – 1.The claimant claims the sum of £1834.29 for an outstanding debt owed. 2.On 22.01.2008 the defendant entered into a an agreement with Barclays Bank PLC for a credit card under reference ….. 3.On the 06/2018 the defendant defaulted on the agreement with an outstanding balance of £2019.29. 4.On 17/08/2015 the debt of £2301.02 was assigned to PRA Group(UK) Ltd. Notices of assignment were sent to the defendant in accordance with S136 law of property act 1925. Payments of £434.52 were received up to 06/06/2018 and adjustments have been applied in the sum of £32.21. 5.AND THE CLAIMANT CLAIMS 1. The sum of £1834.29 A Barclaycard CC debt £1834.29 + court costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (pre action protocol) ?Yes What is the total value of the claim? £2019.29 what is the claim for:Barclaycard credit card When did you enter into the original agreement before or after April 2007 ? 01/2008 Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ?NO Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim.Debt purchaser PRA Were you aware the account had been assigned – did you receive a Notice of Assignment? I don't remember receiving this information Did you receive a Default Notice from the original creditor? No, after ringing Barclaycard they claim that the account was never defaulted. Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Just letters from PRA stating you are behind with your payments Why did you cease payments? Got into financial difficulties What was the date of your last payment?06/02/2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes I was on a debt management plan He has done the AOS on MCOL. CCA request ready to send to claimants CPR.31.14 ready to send to claimants solicitors Any help and advice appreciated. Donation will be made thank you

-

Hi everyone, following on from extremely similar cases, i requested documentation for service charges of a flat i own. Accordingly to regulations (Landlord and Tenant Act 1985 Section 21, as amended by the Commonhold and Leasehold Reform Act 2002 Section 152) they should have provided evidence within 21 days. 25 days later they sent me some receipts making up 25% of the charges. I asked them if that was all they had for that financial year and they confirmed this. So I had these checked and found usual irregularities like wrong calculations for shares and of course all the missing receipts and invoices for many of the services allegedly offered. For example, lift maintenance is £1000, divided by 10 flats they make it £15. Clearly wrong to me and you, but of course their calculators seem to consider maths an opinion. They don't dispute that these calculations are wrong, but they simply avoid addressing the problem. I asked for a refund of all undocumented charges and overcharged, same as I did with other financial years which they refunded. As soon as they received this request they sent another 3 receipts totalling £20 approx; this was well after the statutory 21 days. I rejected these receipt and told them that I was not in a position to accept any further documents because they had already confirmed that they didn't have anymore and the 21 days had passed long time ago. So they're now playing the ignore game and, as the 14 days I gave them are up tomorrow, I am drafting a lba. If you are still reading I thank you, I know it's a bit long but I wanted you to have a good picture. I have a feeling that this time I will end up taking them to court, so I don't want to make any mistake. My question is: Accordingly to the pre action protocol I should suggest an alternative dispute resolution service, however I don't want to give them an opportunity to get the Ombudsman involved, knowing that they are useless. Can I avoid mentioning ADR in my lba? If I do, could they claim that I haven't complied to the letter of the pre action protocol? Or by ticking yes to mediation on mcol I should be ok? Thanks for your help.

Hi everyone, following on from extremely similar cases, i requested documentation for service charges of a flat i own. Accordingly to regulations (Landlord and Tenant Act 1985 Section 21, as amended by the Commonhold and Leasehold Reform Act 2002 Section 152) they should have provided evidence within 21 days. 25 days later they sent me some receipts making up 25% of the charges. I asked them if that was all they had for that financial year and they confirmed this. So I had these checked and found usual irregularities like wrong calculations for shares and of course all the missing receipts and invoices for many of the services allegedly offered. For example, lift maintenance is £1000, divided by 10 flats they make it £15. Clearly wrong to me and you, but of course their calculators seem to consider maths an opinion. They don't dispute that these calculations are wrong, but they simply avoid addressing the problem. I asked for a refund of all undocumented charges and overcharged, same as I did with other financial years which they refunded. As soon as they received this request they sent another 3 receipts totalling £20 approx; this was well after the statutory 21 days. I rejected these receipt and told them that I was not in a position to accept any further documents because they had already confirmed that they didn't have anymore and the 21 days had passed long time ago. So they're now playing the ignore game and, as the 14 days I gave them are up tomorrow, I am drafting a lba. If you are still reading I thank you, I know it's a bit long but I wanted you to have a good picture. I have a feeling that this time I will end up taking them to court, so I don't want to make any mistake. My question is: Accordingly to the pre action protocol I should suggest an alternative dispute resolution service, however I don't want to give them an opportunity to get the Ombudsman involved, knowing that they are useless. Can I avoid mentioning ADR in my lba? If I do, could they claim that I haven't complied to the letter of the pre action protocol? Or by ticking yes to mediation on mcol I should be ok? Thanks for your help. -

Hi, I am extremely worried about the possible eviction. I have mortgage with Birmingham Midshires. I live in the property with my mother who is 68, wife and four children age from 1 to 6. Back in 2009 I had mortgage arrears for which court granted the suspended repossession order on the terms that I pay £100 towards the arrears every month. which I did. After some time the lender capitalized the arrears. After few years i got in arrears again but situation got worse because how the payment team at lender dealt with my account. I made complaint on 2 occasions. My complaint was resolved by awarding me the payment of £100 on one occasion and another time £250. February last year I was in arrears, I contacted the lender but ended up in dispute on the way my account was being handled. I complaint to financial ombudsman. They contacted me and lender few time. Until today i don't know the outcome. Now i have received a letter from court for hearing on 23rd Jan. The lender has applied to the court for the decision on to "The Claimant respectfully requests that the court make the following Order" "The Claimant permission to apply for a Warrant of Possession pursuant to CPR 83.2(3)(a) and that permission shall remain valid for 6 years from the date permission is granted". The arrears are around £13k. I am in a position to make ongoing monthly payment as well as substantial amount towards arrears. Can you please advise what the lender is asking the court? Are they asking for eviction warrant? I am very worried because if the y get the eviction order on the hearing on 23rd i have no where to take my children to. Please help how can I defend this as well as is this hearing for eviction? If so, how soon this can happen? Have i lost all now? Thanks.

Hi, I am extremely worried about the possible eviction. I have mortgage with Birmingham Midshires. I live in the property with my mother who is 68, wife and four children age from 1 to 6. Back in 2009 I had mortgage arrears for which court granted the suspended repossession order on the terms that I pay £100 towards the arrears every month. which I did. After some time the lender capitalized the arrears. After few years i got in arrears again but situation got worse because how the payment team at lender dealt with my account. I made complaint on 2 occasions. My complaint was resolved by awarding me the payment of £100 on one occasion and another time £250. February last year I was in arrears, I contacted the lender but ended up in dispute on the way my account was being handled. I complaint to financial ombudsman. They contacted me and lender few time. Until today i don't know the outcome. Now i have received a letter from court for hearing on 23rd Jan. The lender has applied to the court for the decision on to "The Claimant respectfully requests that the court make the following Order" "The Claimant permission to apply for a Warrant of Possession pursuant to CPR 83.2(3)(a) and that permission shall remain valid for 6 years from the date permission is granted". The arrears are around £13k. I am in a position to make ongoing monthly payment as well as substantial amount towards arrears. Can you please advise what the lender is asking the court? Are they asking for eviction warrant? I am very worried because if the y get the eviction order on the hearing on 23rd i have no where to take my children to. Please help how can I defend this as well as is this hearing for eviction? If so, how soon this can happen? Have i lost all now? Thanks. -

Hi i wonder if anyone can give me advice. I have received two summons from link financial ref to old defaulted ex barclay credit card debts. Can anyone give me any advice as to how to go about and what to do please? Any advice will be highly appreciated.

-

Hi, TL;DR version of events: I received a SJPN. I believe I technically am guilty of the charge, but had ignorantly committed the offence out of sheer financial desperation, having had no money and just started a new job. I'm desperate to avoid a criminal conviction. I contacted TfL's IAP to apologise, explained my circumstances, and I provided proof for everything possible and asked to settle this out of court, and that I'm happy to pay the necessary fine. Today they finally responded - with a very generic response to say they wish to proceed with the case... However, the Revenue Control Inspector's statement is factually incorrect, has the date incorrect. The date provided is a date on which I can prove I had a valid ticket. Do I stand a chance at fighting this as 'Not guilty' in court, on the basis that their evidence is incorrect? Complete story: On Thursday 26th July 2018 - I was caught using my mum's 60+ freedom pass by a Revenue Control Inspector on my way to work. I had just started a new job 10 days before, on the 16th July. I had used the card between 18th-26th July (until I was caught) for my commute to and from work. I could not afford a monthly travel card at the time I had been caught as I had been unemployed for past 8 months; maxed out two credit cards, and had been borrowing money from my family to afford rent and food already. I only intended on using the freedom pass until I received my first partial paycheque at the end of the month. I'm not denying - it was a stupid idea, and I obviously hugely regret having used a card I had no right to use. I'm not typically a dishonest person, and this was my first and only offence. 5 months later, just after christmas, I received a Single Justice Procedure Notice, charging me for not having a valid ticket in a compulsory ticket area; 'Contrary to Byelaw 17(1) of the Transport for London Railway Byelaws made under paragraph 26, schedule 11 of the Greater London Authority Act 1999.' Understanding I was guilty of the offence, despite it having been committed out of sheer desperation. I'm also desperate to try and avoid a criminal conviction as I’m currently unemployed, and in search of a job again, and wish to avoid anything that might damage my chances of re-employment. So I emailed TfL's IAP email address, explaining my financial circumstances, expressing that this was my first and only offence, apologising and pleading for any way for this matter to be settled without landing me a criminal record for it would really damage my chances of getting employed again- supplying bank statements, credit card statements, providing anything and everything to support the facts I had stated. ... Today, I finally received a totally generic sounding email response from one of the prosecutors at the IAP department: “On the 27th July 2018 you were approached at ***** ***** station after using a pass to enter that activated the monitors. You produced a 60+ Oyster card that you admitted belonged to your mother. These passes are not transferable and therefore was not valid for you to use…” “…Transport for London intend to continue with the matter listed against you and I would advise you to complete the paperwork and return within the required timescales” I noticed that in their email response they have the date of the incident incorrect, (She said 27th July 2018 instead of 26th July 2018. On the 26th I was caught and cautioned, on the 27th, I actually paid for my fare and can prove it) Furthermore, the Revenue Control Inspector's statement says the incident happened on the 27th instead of the 26th. It's only on the second page of the SJPN under the "Statement of facts" that they have the date correctly stated as the 26th July. Do I stand any chance in fighting this case as 'not guilty' in court, on the basis that the statement given by the Revenue Control Inspector is factually incorrect, and if they were to pull CCTV from the 27th - they'd find that I'd actually used a valid ticket on that date? Any help or suggestions would be massively appreciated. I have 5 days to respond to the SJPN letter Many thanks!

Hi, TL;DR version of events: I received a SJPN. I believe I technically am guilty of the charge, but had ignorantly committed the offence out of sheer financial desperation, having had no money and just started a new job. I'm desperate to avoid a criminal conviction. I contacted TfL's IAP to apologise, explained my circumstances, and I provided proof for everything possible and asked to settle this out of court, and that I'm happy to pay the necessary fine. Today they finally responded - with a very generic response to say they wish to proceed with the case... However, the Revenue Control Inspector's statement is factually incorrect, has the date incorrect. The date provided is a date on which I can prove I had a valid ticket. Do I stand a chance at fighting this as 'Not guilty' in court, on the basis that their evidence is incorrect? Complete story: On Thursday 26th July 2018 - I was caught using my mum's 60+ freedom pass by a Revenue Control Inspector on my way to work. I had just started a new job 10 days before, on the 16th July. I had used the card between 18th-26th July (until I was caught) for my commute to and from work. I could not afford a monthly travel card at the time I had been caught as I had been unemployed for past 8 months; maxed out two credit cards, and had been borrowing money from my family to afford rent and food already. I only intended on using the freedom pass until I received my first partial paycheque at the end of the month. I'm not denying - it was a stupid idea, and I obviously hugely regret having used a card I had no right to use. I'm not typically a dishonest person, and this was my first and only offence. 5 months later, just after christmas, I received a Single Justice Procedure Notice, charging me for not having a valid ticket in a compulsory ticket area; 'Contrary to Byelaw 17(1) of the Transport for London Railway Byelaws made under paragraph 26, schedule 11 of the Greater London Authority Act 1999.' Understanding I was guilty of the offence, despite it having been committed out of sheer desperation. I'm also desperate to try and avoid a criminal conviction as I’m currently unemployed, and in search of a job again, and wish to avoid anything that might damage my chances of re-employment. So I emailed TfL's IAP email address, explaining my financial circumstances, expressing that this was my first and only offence, apologising and pleading for any way for this matter to be settled without landing me a criminal record for it would really damage my chances of getting employed again- supplying bank statements, credit card statements, providing anything and everything to support the facts I had stated. ... Today, I finally received a totally generic sounding email response from one of the prosecutors at the IAP department: “On the 27th July 2018 you were approached at ***** ***** station after using a pass to enter that activated the monitors. You produced a 60+ Oyster card that you admitted belonged to your mother. These passes are not transferable and therefore was not valid for you to use…” “…Transport for London intend to continue with the matter listed against you and I would advise you to complete the paperwork and return within the required timescales” I noticed that in their email response they have the date of the incident incorrect, (She said 27th July 2018 instead of 26th July 2018. On the 26th I was caught and cautioned, on the 27th, I actually paid for my fare and can prove it) Furthermore, the Revenue Control Inspector's statement says the incident happened on the 27th instead of the 26th. It's only on the second page of the SJPN under the "Statement of facts" that they have the date correctly stated as the 26th July. Do I stand any chance in fighting this case as 'not guilty' in court, on the basis that the statement given by the Revenue Control Inspector is factually incorrect, and if they were to pull CCTV from the 27th - they'd find that I'd actually used a valid ticket on that date? Any help or suggestions would be massively appreciated. I have 5 days to respond to the SJPN letter Many thanks! -

On his site people are frequently advised to follow CRA and take errant traders to the small claims court. Success rates appear to be most encouraging. Yesterday, I took a rouge motor trader to a SCC at the local sheriff court, and because of a major error by the sheriff, my claim was reduced by over 66%. What can i do ? Scottish Law

-

Noting the branding on a cinemas car park, I parked to watch a film. Not noticing any clear notifications to pay, they clearly are there. Naturally this is a Br2ttaN3a managed carpark. I now have two letters. 1. Letter before action from the dubious BW 2. A final 16 day demand before court. I have done the following but have had no response. 1. Recorded delivery letter to parking management company, asking for evidence, print outs, and offence. 2. Recorded delivery letter to BW asking for data restriction. ( they replied saying not applicable ) 3. Letter to my MP 4. Letter to the cinema asking for them to make their signs to the car park clearly state you have to pay - and to step in and make contact. I enclose the two letters. I have sent a follow up email to the cinema stating I will write to the board and the local press - and that my complaint is under unfair contracts. Shall I post the letters here, obviously edited?

Noting the branding on a cinemas car park, I parked to watch a film. Not noticing any clear notifications to pay, they clearly are there. Naturally this is a Br2ttaN3a managed carpark. I now have two letters. 1. Letter before action from the dubious BW 2. A final 16 day demand before court. I have done the following but have had no response. 1. Recorded delivery letter to parking management company, asking for evidence, print outs, and offence. 2. Recorded delivery letter to BW asking for data restriction. ( they replied saying not applicable ) 3. Letter to my MP 4. Letter to the cinema asking for them to make their signs to the car park clearly state you have to pay - and to step in and make contact. I enclose the two letters. I have sent a follow up email to the cinema stating I will write to the board and the local press - and that my complaint is under unfair contracts. Shall I post the letters here, obviously edited? -

CIFAS handled ny complaint against an application fraud warning in a reckless manner. I decided to take CIFAS to Court. I would like some insights as whether or not CIFAS is subject to Consumer Rights Act 2015 for service provisions? My second question is: are there precedents of consumers taking CIFAS to Court?

-

Hi I've received a 'letter before county court claim' from ParkingEye regarding an unpaid ticket and I would like your opinion and advice please. I like to think it's just scare tactics but I want to be sure. I parked on a Tesco car park, supposedly overstayed (3 hours on a 2 hour max stay. I disputed the ticket with a POPLA template I found here that at CAG that said I don't acknowledge the debt, don't have to name the driver, and that I will defend myself at POPLA if need be. This has worked the other times I've had tickets but this time I've received a new and different response. In bold, capital letters it states 'letter before county court claim' and straight away this just screams 'we're trying to scare you'. The letter notes when and where I was caught by their cameras and that the charge was for breach of contract and that when they rejected my appeal I had 28 days to lodge an appeal with POPLA and that as I didn't appeal, the ticket must be paid. To be fair, I thought I only had to appeal to POPLA when PE took me to POPLA (and I was there to defend myself - not preempt my defence by writing to POPLA myself). Next it details how to contact PE to make payment within 30 days and that if further action is required and court proceedings are issued then costs will be incurred - including £50 solicitor's costs and £25 court claim issue fee - and that no costs have been added at this stage. I think this is scare mongering because AFAIK extra costs cannot be added and that £50 wouldn't even cost solicitor costs anyway. The final paragraph is to draw my attention to the Supreme Court's decision 'concerning the value of PE's Parking Charges and the judgement granted in PE's favour, delivers a binding precedent in respect of the sum sought as the Supreme Court found that the Parking Charge was set at a reasonable amount'. On the flip side was further details about a judgement on 4th Nov 2015 in PE vs Barry Beavis, dismissing his appeal on both grounds, and that the Supreme Cour found that the Parking Charge issued was neither unfair nor penal; that the Court agreed with the analysis proffered by HHJ Moloney and the Court of Appeal that £85 was neither extravagant or unconscionable; and that this judgement is binding upon all lower courts and independent appeals services. The remaining pages of the letter includes a 7 point 'further information (see screenshot), info on where to get debt advice and how to flll in the reply form, the reply form itelf which inludes options such as 'I owe the debt', ' I owe some but all of it', 'I dispute the debt', 'I will pay now'. 'I need more documents/information', and a financial statement form. Your advice is much appreciated.

Hi I've received a 'letter before county court claim' from ParkingEye regarding an unpaid ticket and I would like your opinion and advice please. I like to think it's just scare tactics but I want to be sure. I parked on a Tesco car park, supposedly overstayed (3 hours on a 2 hour max stay. I disputed the ticket with a POPLA template I found here that at CAG that said I don't acknowledge the debt, don't have to name the driver, and that I will defend myself at POPLA if need be. This has worked the other times I've had tickets but this time I've received a new and different response. In bold, capital letters it states 'letter before county court claim' and straight away this just screams 'we're trying to scare you'. The letter notes when and where I was caught by their cameras and that the charge was for breach of contract and that when they rejected my appeal I had 28 days to lodge an appeal with POPLA and that as I didn't appeal, the ticket must be paid. To be fair, I thought I only had to appeal to POPLA when PE took me to POPLA (and I was there to defend myself - not preempt my defence by writing to POPLA myself). Next it details how to contact PE to make payment within 30 days and that if further action is required and court proceedings are issued then costs will be incurred - including £50 solicitor's costs and £25 court claim issue fee - and that no costs have been added at this stage. I think this is scare mongering because AFAIK extra costs cannot be added and that £50 wouldn't even cost solicitor costs anyway. The final paragraph is to draw my attention to the Supreme Court's decision 'concerning the value of PE's Parking Charges and the judgement granted in PE's favour, delivers a binding precedent in respect of the sum sought as the Supreme Court found that the Parking Charge was set at a reasonable amount'. On the flip side was further details about a judgement on 4th Nov 2015 in PE vs Barry Beavis, dismissing his appeal on both grounds, and that the Supreme Cour found that the Parking Charge issued was neither unfair nor penal; that the Court agreed with the analysis proffered by HHJ Moloney and the Court of Appeal that £85 was neither extravagant or unconscionable; and that this judgement is binding upon all lower courts and independent appeals services. The remaining pages of the letter includes a 7 point 'further information (see screenshot), info on where to get debt advice and how to flll in the reply form, the reply form itelf which inludes options such as 'I owe the debt', ' I owe some but all of it', 'I dispute the debt', 'I will pay now'. 'I need more documents/information', and a financial statement form. Your advice is much appreciated.