Showing results for tags 'mkdp'.

-

Hi, I'm hoping someone can give me some advice. I have an old MBNA debt which I defaulted on in 2010. Since then I have religiously been making pro-rata payments up to and including this month. MBNA sold the debt to Aktiv Kapital who in turn sold it to PRA in 2014. I know that PRA have been receiving my payments because they sent me a letter towards the end of last year saying "...thank you for your ongoing commitment to the payment arrangement on your account". It goes on to say "....We would therefore like to make you aware that if it suits your current financial situation, you could settle your agreement by paying a discounted amount which is detailed below" The letter ends with " If you feel you are unable to pay the settlement amount then please continue with your arrangement as normal." Which I have done! However, on the claim form they state "..Payments of £307 received up to 16/6/16" and are now claiming sum owed plus 8% interest + court fee + legal costs. I know I have not missed any payments because my bank statements tell me so I know they have been receiving them because they wrote and thanked me for my continued commitment 4 months after the date that they claim they received last payment. To say I was shocked and confused to receive the claim form from the court is an understatement. What's going on? and how to tackle this? Any help would be appreciated.

-

Name of the Claimant ? Hoist Portfolio Holding 2 LTD Date of issue 02/11/2016 Date to acknowledge =20/11/2016 Date to submit defence = 4pm Friday 02/12/2016 POC 1.This claim is for the sum of £4900 in respect of monies owing under an Agreement with the account number xxxxx pursuant to The Consumer Credit Act 1974 (CCA) The debt was legally assigned by MKDP LLP (Ex HSBC) to the Claimant and notice has been served 2.The Defendant has failed to make contractual payments under the terms of the Agreement. A default notice has been served upon the defendant pursuant to s.87(1) CCA. 3.The Claimant claims 1.The sum of £4900 2.Interests pursuant to s69 of the County Court Act 1984 at a rate of 8.00percent from the 2/11/10 to the date hereof 2188 days is the sum of £2300 3.Future interest of accruing at the daily rate of £1 4.costs What is the value of the claim?£7800 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Credit Card When did you enter into the original agreement before or after 2007? Pre 2007 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? could no longer afford to maintain What was the date of your last payment? 2012 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes In 2012 I requested my CCA, they returned to me only generic docs, with no signed application or agreement form. I will send off tomorrow for CCA and CPA? Thanks

Name of the Claimant ? Hoist Portfolio Holding 2 LTD Date of issue 02/11/2016 Date to acknowledge =20/11/2016 Date to submit defence = 4pm Friday 02/12/2016 POC 1.This claim is for the sum of £4900 in respect of monies owing under an Agreement with the account number xxxxx pursuant to The Consumer Credit Act 1974 (CCA) The debt was legally assigned by MKDP LLP (Ex HSBC) to the Claimant and notice has been served 2.The Defendant has failed to make contractual payments under the terms of the Agreement. A default notice has been served upon the defendant pursuant to s.87(1) CCA. 3.The Claimant claims 1.The sum of £4900 2.Interests pursuant to s69 of the County Court Act 1984 at a rate of 8.00percent from the 2/11/10 to the date hereof 2188 days is the sum of £2300 3.Future interest of accruing at the daily rate of £1 4.costs What is the value of the claim?£7800 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Credit Card When did you enter into the original agreement before or after 2007? Pre 2007 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? could no longer afford to maintain What was the date of your last payment? 2012 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes In 2012 I requested my CCA, they returned to me only generic docs, with no signed application or agreement form. I will send off tomorrow for CCA and CPA? Thanks -

Hi, Could you help me with a Northampton county court claim dated 13 sep 2016 which is for £935.50 + interest. I have acknowledged it online and the issue date is 13 Sep 2016. Claim History A claim was issued against you on 13/09/2016 Your acknowledgment of service was submitted on 22/09/2016 at 20:20:43 Your acknowledgment of service was received on 23/09/2016 at 08:01:36 I want to dispute the whole claim which I have told the court online as im not sure about this credit card or when it was taken out as at that time I had so many debt but im not sure which one this is. Which forms do I need to send off to the claimant and the solicitors. CCA and 31:14? Any help will be appreciated.

Hi, Could you help me with a Northampton county court claim dated 13 sep 2016 which is for £935.50 + interest. I have acknowledged it online and the issue date is 13 Sep 2016. Claim History A claim was issued against you on 13/09/2016 Your acknowledgment of service was submitted on 22/09/2016 at 20:20:43 Your acknowledgment of service was received on 23/09/2016 at 08:01:36 I want to dispute the whole claim which I have told the court online as im not sure about this credit card or when it was taken out as at that time I had so many debt but im not sure which one this is. Which forms do I need to send off to the claimant and the solicitors. CCA and 31:14? Any help will be appreciated. -

Hi my wife had an account with Nationwide due to money issues she went overdrawn and with charges the amount went up to over £500. in 2014 unknown to us a company bought the debt from nationwide and then promptly took it to court, last month the MKDP sold this debt on to Hoist Portfolio Holding Ltd who as soon as they got the name changed on the ccj promptly sent it to the bailiffs. We are not sure if at the time of the ccj it was statute bared, I am currently applying to nationwide for all the paper work but I need to apply to set the judgment aside to stop the bailiffs can anyone help and how would fight the original charges because I read that someone had recently removed bank charges through the courts.

Hi my wife had an account with Nationwide due to money issues she went overdrawn and with charges the amount went up to over £500. in 2014 unknown to us a company bought the debt from nationwide and then promptly took it to court, last month the MKDP sold this debt on to Hoist Portfolio Holding Ltd who as soon as they got the name changed on the ccj promptly sent it to the bailiffs. We are not sure if at the time of the ccj it was statute bared, I am currently applying to nationwide for all the paper work but I need to apply to set the judgment aside to stop the bailiffs can anyone help and how would fight the original charges because I read that someone had recently removed bank charges through the courts. -

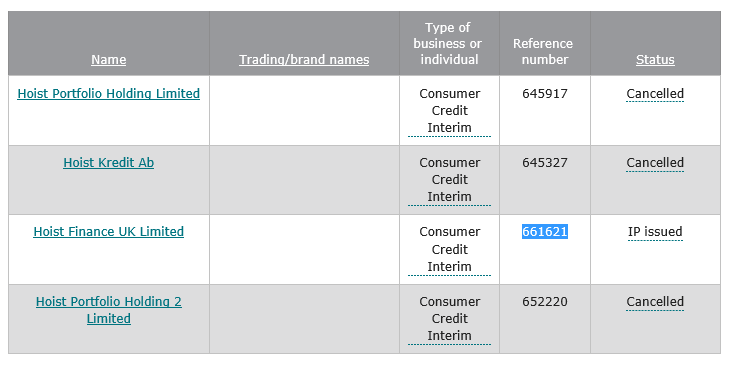

Upon checking the new FCA Public Register which is listing "Interim Permissions" in its transitional role from the OFT, I find that Hoist wildcard returns 4 results : Hoist Portfolio Holding Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Portfolio Holding 2 Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Kredit Ab (Presumably Swedish Parent Company) - IP CANCELLED Hoist Finance UK Limited - Reference Number 661621 - IP ISSUED Having received a letter from Robinson Way (As we know now owned by Hoist Finance UK Limited) they state that they have purchased an account from MKDP LLP (Compello - Hoist Director is director of Compello also). They state quite clearly and unambiguously that the alleged new beneficial owner of the account is Hoist Portfolio 2 Limited, who clearly are not registered nor authorised to engage in CC activity, and as such cannot legally instruct their associate company Robinson Way to attempt any form of recovery on their behalf. This latest threat to the consumer has all the hallmarks and modus operandi of the last bunch of cowboys who fought their corner for so long and then voluntarily surrendered their licences. I'm not mentioning names, but everyone knows whom I'm referring to. This is now the same old story, one director pulling the strings with an absolute labyrinth of companies who are nothing more than a file on a shelf and a brass plate on an accountants door, representing the fiddles of the strings. I'm making it my business to enquire with the FCA as to the status of Hoist Portfolio 2 Holding Limited just to see and hear from them directly their legal status. They would probably just BS consumers and say "oh well we're all part of the same group" blah blah blah - now where have I heard that before - sounds familiar. Would appreciate all your comments on this matter. Ive been in Court before with people as a MacKenzie Friend against the last mob who tried to collect accounts whilst unauthorised and tried to wriggle with intertwined companies. The Judge generally sees right through it.

Upon checking the new FCA Public Register which is listing "Interim Permissions" in its transitional role from the OFT, I find that Hoist wildcard returns 4 results : Hoist Portfolio Holding Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Portfolio Holding 2 Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Kredit Ab (Presumably Swedish Parent Company) - IP CANCELLED Hoist Finance UK Limited - Reference Number 661621 - IP ISSUED Having received a letter from Robinson Way (As we know now owned by Hoist Finance UK Limited) they state that they have purchased an account from MKDP LLP (Compello - Hoist Director is director of Compello also). They state quite clearly and unambiguously that the alleged new beneficial owner of the account is Hoist Portfolio 2 Limited, who clearly are not registered nor authorised to engage in CC activity, and as such cannot legally instruct their associate company Robinson Way to attempt any form of recovery on their behalf. This latest threat to the consumer has all the hallmarks and modus operandi of the last bunch of cowboys who fought their corner for so long and then voluntarily surrendered their licences. I'm not mentioning names, but everyone knows whom I'm referring to. This is now the same old story, one director pulling the strings with an absolute labyrinth of companies who are nothing more than a file on a shelf and a brass plate on an accountants door, representing the fiddles of the strings. I'm making it my business to enquire with the FCA as to the status of Hoist Portfolio 2 Holding Limited just to see and hear from them directly their legal status. They would probably just BS consumers and say "oh well we're all part of the same group" blah blah blah - now where have I heard that before - sounds familiar. Would appreciate all your comments on this matter. Ive been in Court before with people as a MacKenzie Friend against the last mob who tried to collect accounts whilst unauthorised and tried to wriggle with intertwined companies. The Judge generally sees right through it.

-

Hi, I took out a Goldfish credit card in 2003. The account had a balance of around £1000 which I was making minimum monthly payments towards. Goldfish then sold the account to Barclaycard when they merged. At this point I stopped receiving paper statements. I therefore called them on numerous occasions to try and rectify this and continued to make monthly payments of random amounts as I had no statement to refer too. I then received threatening letters from Barclaycard stating my balance was over £4000. I had not used the card and I had not received statements so I disputed this and told them I would not pay any further balances until this was resolved and they could tell me where these additional charges came from. No statements were ever received and then I received communication from a debt chasing company stating they had been appointed to retrieve the debt in full. I explained the circumstances to them and again tried to call Barclaycard. Barclaycard could now not even discuss the account as it had been closed on their systems as the debt was sold. Around 6-8 debt companies have since tried to retrieve the debt but each time I call them to ask for evidence they go silent. MKDR is the latest company to 'own' the debt and they issued a small claims court case against me in 2015. I submitted by defence and nothing happened. I called the court and they informed me MKDR had not proceeded any further with the case. The issue I have is that this seriously affects my credit rating and will do for another year. My credit report states that the account has been overdue since 27/04/2011 and if I am to wait 6yrs this will not expire until 2017. Is there anything I can do to challenge this in the meantime? I am certain no one has the statements I have been asking for for the past 5yrs. How can I get MKDR to either proceed or close the debt off? Thanks in advance Katie

-

I'm sure I saw it on here but can't find it. My partner had a letter from Welcome Finance (MKDP) saying she owed over £4,0000. It was statute barred which, with the help of the Ombudsman, they eventually agreed. However, we just saw that the 'debt' appears on her Experian credit score! Is this legal? We've just emailed the Ombudsman again to ask advice on how to get this b/s off of her credit score.

I'm sure I saw it on here but can't find it. My partner had a letter from Welcome Finance (MKDP) saying she owed over £4,0000. It was statute barred which, with the help of the Ombudsman, they eventually agreed. However, we just saw that the 'debt' appears on her Experian credit score! Is this legal? We've just emailed the Ombudsman again to ask advice on how to get this b/s off of her credit score. -

Hi all, Sorry this may be a tad long-winded!! Car purchased from Welcome Finance in mid-2008, stopped paying the instalments in mid-2009 as I was unhappy with the car, how they operated and how they had treated me. I have no records from that time as to when the last payment was made but I know that the car was returned to them around October 2009. They agreed on the phone to collect the car and because I had rectified some existing faults at my expense etc etc I was told the final balance owed was up to £300 once the car had been handed back depending on a few factors. I asked for written confirmation of this as a full & final settlement offer and would make payment immediately. I never received this and then didn't hear anything else for quite some time. In the mean time I had been in and out of the country, moved house etc eventually a couple of years ago I received some letters via my mum's address from MKDP saying I owed £4000. Significantly more than £300!! I confirmed this detail by applying for a credit report with experian and note that they hold an account on my record for £4000 which is defaulted as of 28/10/2009. Then today I was passed a letter from MKDP, which was again sent to my mum's address, stating that the debt of £4000 had been sold to Robinson's and also enclosed was an offer letter from Robinson's saying I can pay £10 per week for several years, £15 per week for less years or call them to discuss options. I've always ignored all letters and never replied to them or spoken to them on the phone. As I was;t even in the country for some of the past few years I never even needed credit so it didn't affect me, however I'm now back permanently so want to make sure this doesn't go to CCJ. Now, I'm aware that this debt is either Statute Barred already or is about to be. If, for instance, the SB start date is indeed 28/10/09 then this is just 2 months away from now, however I'm not exactly certain when the car was returned or when exactly the last payment was made to Welcome Finance. I've never received a default notice, never received a notice of assignment to MKDP and generally didn't receive anything after the car had been handed back so I assumed there was no outstanding amount and that was the end of it. I moved house a couple months after the car went back so I can only guess that some paperwork may have been sent to my old address, but seeing as I hadn't heard anything from Welcome Finance in that time I assumed, rightly or wrongly, that there was no need to update my address with them. Now my questions, if I may.... 1. Should I just sit it out and hope a claim form doesn't arrive in the post? 2. If no to Q1, then I'm looking to clarify exactly when the debt was/will be SB. What''s the best way to do this and how long does that add to the process? 3. If yes to Q1, then I guess if a claim form does arrive I'll need to formulate a defence and cross that bridge when it comes? Any advice is greatly appreciated!

Hi all, Sorry this may be a tad long-winded!! Car purchased from Welcome Finance in mid-2008, stopped paying the instalments in mid-2009 as I was unhappy with the car, how they operated and how they had treated me. I have no records from that time as to when the last payment was made but I know that the car was returned to them around October 2009. They agreed on the phone to collect the car and because I had rectified some existing faults at my expense etc etc I was told the final balance owed was up to £300 once the car had been handed back depending on a few factors. I asked for written confirmation of this as a full & final settlement offer and would make payment immediately. I never received this and then didn't hear anything else for quite some time. In the mean time I had been in and out of the country, moved house etc eventually a couple of years ago I received some letters via my mum's address from MKDP saying I owed £4000. Significantly more than £300!! I confirmed this detail by applying for a credit report with experian and note that they hold an account on my record for £4000 which is defaulted as of 28/10/2009. Then today I was passed a letter from MKDP, which was again sent to my mum's address, stating that the debt of £4000 had been sold to Robinson's and also enclosed was an offer letter from Robinson's saying I can pay £10 per week for several years, £15 per week for less years or call them to discuss options. I've always ignored all letters and never replied to them or spoken to them on the phone. As I was;t even in the country for some of the past few years I never even needed credit so it didn't affect me, however I'm now back permanently so want to make sure this doesn't go to CCJ. Now, I'm aware that this debt is either Statute Barred already or is about to be. If, for instance, the SB start date is indeed 28/10/09 then this is just 2 months away from now, however I'm not exactly certain when the car was returned or when exactly the last payment was made to Welcome Finance. I've never received a default notice, never received a notice of assignment to MKDP and generally didn't receive anything after the car had been handed back so I assumed there was no outstanding amount and that was the end of it. I moved house a couple months after the car went back so I can only guess that some paperwork may have been sent to my old address, but seeing as I hadn't heard anything from Welcome Finance in that time I assumed, rightly or wrongly, that there was no need to update my address with them. Now my questions, if I may.... 1. Should I just sit it out and hope a claim form doesn't arrive in the post? 2. If no to Q1, then I'm looking to clarify exactly when the debt was/will be SB. What''s the best way to do this and how long does that add to the process? 3. If yes to Q1, then I guess if a claim form does arrive I'll need to formulate a defence and cross that bridge when it comes? Any advice is greatly appreciated! -

Hi All I am looking for some advice, I have recently received a letter from MKDP stating my outstanding balance is 3,356.39 and they are informing me they are instructing their pre-legal department to review my account . I haven't communicated with them as i am financially in a mess. I believe this is from when I banked with the Nationwide and I had a loan and overdraft with them, they recalled both, gave me 28 days notice that they would be taking the money from my bank account this was September 2010 , I had to move my bank account or I would of gone into mortgage arrears and utility bill arrears and unable to support at that time my dependant, I have buried my head in the sand! I am aware after six years I can still be chased but under no obligation to pay this, I really am stuck about what I do. I have since learnt about the Conduct of Business Regulations (BCOB), BCOB makes it unlawful for your bank to treat you unfairly. which giving me 28 days notice for such a large debt feels unfair. MKDP have registered a debt in their name against me on my credit referance Any advice?

-

I have a £12.5k debt to Nationwide that was sold to MKDP. On 30th September 2015 the debt will be statute barred however on 27th November 2013 MKDP issued a claim in court to which I put in a defence - to do with exorbitant charges I think but I can't remember now. I have not heard anything since does this mean that the debt is fixed for them to come back anytime or will it be barred on 30th September 2015 if I hear nothing from them. Now that Hoist have hold it of it I doubt it will get that far would it be better to contact them and offer some form of repayment?

I have a £12.5k debt to Nationwide that was sold to MKDP. On 30th September 2015 the debt will be statute barred however on 27th November 2013 MKDP issued a claim in court to which I put in a defence - to do with exorbitant charges I think but I can't remember now. I have not heard anything since does this mean that the debt is fixed for them to come back anytime or will it be barred on 30th September 2015 if I hear nothing from them. Now that Hoist have hold it of it I doubt it will get that far would it be better to contact them and offer some form of repayment? -

Hi all have been attempting to help my daughter sort out her debt problems . Recent success Bryan carter discontinued court claim due to information from this site . We now however have MKDP claiming for old hsbc debt . details below . Current account overdraft shows on CRA as defaulted November 2007 as does flexiloan . Name of the Claimant MKDP LLP Date of issue 08 June 2015 What is the claim for The claimant claims sum of xxxx being monies due from the defendant(s) to HSBC bank plc under a bank account facility regulated by the consumer credit act 1974 and assigned to the claimant on 08/12/011. The defendant(s) s account number was xxxxxxxxx. It was a term of the bank account that any debit balance would be repayable in full on demand . The defendant(s) has failed to make payment as required by the demand for payment sent by HSBC bank plc. The claimant claims the sum of xxxxxxx and costs . The claimant has complied , as far as is necessary , with the pre-action connduct practice direction. What is the value of the claim? 1,761.70 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Overdraft /combined with loan. Account number claim under is current account no mention of loan account number . When did you enter into the original agreement before or after 2007? bank account 2004 / loan 2007 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. debt purchaser MKDP LLP Were you aware the account had been assigned – did you receive a Notice of Assignment? unsure Did you receive a Default Notice from the original creditor? unsure Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? Debts were building up not enough money to go round so prioritised to rent and neccesities . What was the date of your last payment? poss 2013 to MKDP under current account number no mention of loan Was there a dispute with the original creditor that remains unresolved? unsure Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? Yes they offered consolidating loan at payments i could not afford , so i refused . Actions so far are as follows AOS done 13/06/15 , CPR 31.14 to MKDP done 15/06/15 , SAR to HSBC done 15/06/15 . MKDP responded to CPR with copy of terms an conditions effective 1st november 2007 , also copy (looks like computer printout as opposed to original ) of a default notice not signed or dated however the account number on this notice is for the flexiloan account and not the bank current account number of which the claim in the POC is for . It would seem that the two debts have been combined and i would say that MKDP are unaware of this , as they make no mention to the flexiloan in their claim . To sum up looking for some advice as to how to proceed as the bulk of the debt is the flexiloan , and the overdraft is mainly charges . I do not want to accidentlly alert MKDP of their error with the default notice and the fact that the loan has been bundled in with a current account as they make no mention of the loan in their claim . Where do MKDP stand if they continue to court ,and what would be the best way forward IE ask MKDP for cca and informing them about the two accounts being combined (as im pretty sure that the flexiloan was statute barred as of 2013 , however as said earlier 10 pound payment was made to MKDP under this debt after constant phonecalls and hounding but with only the current account details . Would appreciate some advice if anyone is able to offer some as defence is due Friday 10th if i worked it out correctly .

Hi all have been attempting to help my daughter sort out her debt problems . Recent success Bryan carter discontinued court claim due to information from this site . We now however have MKDP claiming for old hsbc debt . details below . Current account overdraft shows on CRA as defaulted November 2007 as does flexiloan . Name of the Claimant MKDP LLP Date of issue 08 June 2015 What is the claim for The claimant claims sum of xxxx being monies due from the defendant(s) to HSBC bank plc under a bank account facility regulated by the consumer credit act 1974 and assigned to the claimant on 08/12/011. The defendant(s) s account number was xxxxxxxxx. It was a term of the bank account that any debit balance would be repayable in full on demand . The defendant(s) has failed to make payment as required by the demand for payment sent by HSBC bank plc. The claimant claims the sum of xxxxxxx and costs . The claimant has complied , as far as is necessary , with the pre-action connduct practice direction. What is the value of the claim? 1,761.70 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Overdraft /combined with loan. Account number claim under is current account no mention of loan account number . When did you enter into the original agreement before or after 2007? bank account 2004 / loan 2007 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. debt purchaser MKDP LLP Were you aware the account had been assigned – did you receive a Notice of Assignment? unsure Did you receive a Default Notice from the original creditor? unsure Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? Debts were building up not enough money to go round so prioritised to rent and neccesities . What was the date of your last payment? poss 2013 to MKDP under current account number no mention of loan Was there a dispute with the original creditor that remains unresolved? unsure Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? Yes they offered consolidating loan at payments i could not afford , so i refused . Actions so far are as follows AOS done 13/06/15 , CPR 31.14 to MKDP done 15/06/15 , SAR to HSBC done 15/06/15 . MKDP responded to CPR with copy of terms an conditions effective 1st november 2007 , also copy (looks like computer printout as opposed to original ) of a default notice not signed or dated however the account number on this notice is for the flexiloan account and not the bank current account number of which the claim in the POC is for . It would seem that the two debts have been combined and i would say that MKDP are unaware of this , as they make no mention to the flexiloan in their claim . To sum up looking for some advice as to how to proceed as the bulk of the debt is the flexiloan , and the overdraft is mainly charges . I do not want to accidentlly alert MKDP of their error with the default notice and the fact that the loan has been bundled in with a current account as they make no mention of the loan in their claim . Where do MKDP stand if they continue to court ,and what would be the best way forward IE ask MKDP for cca and informing them about the two accounts being combined (as im pretty sure that the flexiloan was statute barred as of 2013 , however as said earlier 10 pound payment was made to MKDP under this debt after constant phonecalls and hounding but with only the current account details . Would appreciate some advice if anyone is able to offer some as defence is due Friday 10th if i worked it out correctly . -

Another One Bites the dust again! Hoist has bought Robinson Way in the past but now it has made advances towards Compello Group HERE Compello Owns; MKDP LLP MK Rapid Recoveries Keynes Collections

-

I have received two letters today for "formal demand for payment made in accordance with the Practice Direction - Pre-Action Conduct of the Civil Procedure Rules". These are for an HSBC overdraft and Credit Card that I know are statute barred. Should I reply now with the SB letter or wait for the claim forms?

-

Hi Received a statement from MKDP today for a statute Barred Debt. In June last year before the statue I sent a S77/78 request along with the £1.00 Postal Order clearly stating it was for the Fee incurred and not to be used for anything else. I didnt receive anything from my request. On their statement its gone down as payment received!!! The Debt was statute from Feb 2015 I thought this wasnt allowed??? Hadituptohere

Hi Received a statement from MKDP today for a statute Barred Debt. In June last year before the statue I sent a S77/78 request along with the £1.00 Postal Order clearly stating it was for the Fee incurred and not to be used for anything else. I didnt receive anything from my request. On their statement its gone down as payment received!!! The Debt was statute from Feb 2015 I thought this wasnt allowed??? Hadituptohere -

Please can someone advise please as we thought this had all been resolved: Back on the 31/1/04 we got a car from welcome finance since then actually taking the car we had nothing but problems car was unfit was in garage more than on the road etc etc But we kept paying original debt was £11337 we got this down to £6,247 until we had enough and refused to pay till car was swapped or sorted well to cut a long story short it tooks many more years until 5.3.10 when WF told us to sell car as full and final settlement So we did and thought that would be the end of it then earlier this week (todays date 20.4.2015) we got a letter from a company called MKDP telling us we still owed £6247 as they had now bought our debt from WF i disputedd this and explain the situation over the phone and they said they would put on hold and check They sent me a statement of my finacial account with welcome finance on which it states 5/3/10 account type credit amount : £6247.48 balance £0.00 description: Debt written off ..... if this is on my statement which is supposed to be from welcome car finance how can mkdp be chasing us for that ammount and why have we not heard anything from 2010 until just over 2 weeks ago. The welcome car finance default was even removed from our credit score over a year ago and we thought we were rebuilding again can someone advvice whats the best course of action to take please..

-

Hello everyone sorry to bother you all I've been searching online and have come across this amazing site and fingers crossed I'm hoping someone will be able to help and advise me on how to proceed with a CCJ that I've just had put onto my credit file. The debt is for £3300 and states the judgement date was 26th January 2015 but was only added to my credit file yesterday. This debt is for a very old HSBC bank account debt that went into default on the 5th November 2009 for £3145 and now looks like MKDP LLP have purchased the debt I've heard nothing from them at all and moved into my new house in july 2014. so would not have received any court papers. I'm just looking for some legal advice on what id need to do to get this sorted it was due to come off in November this year so they got in before the 6 years and i can't afford to have this on my file as I've been trying so hard to sort my life out and it seems everything is now coming back to bite me I have also noticed a new company have applied a default to my credit file called MYJAR for £692 it looks like its for a old payday loan from txt loan from 2012-2013 again in my old address but i defaulted 2-3 years ago and its only just been put on my credit file and the default date is missing is this allowed as its showing on my file as if I've only just started missing payments ? Any help would be amazing and id be very grateful

Hello everyone sorry to bother you all I've been searching online and have come across this amazing site and fingers crossed I'm hoping someone will be able to help and advise me on how to proceed with a CCJ that I've just had put onto my credit file. The debt is for £3300 and states the judgement date was 26th January 2015 but was only added to my credit file yesterday. This debt is for a very old HSBC bank account debt that went into default on the 5th November 2009 for £3145 and now looks like MKDP LLP have purchased the debt I've heard nothing from them at all and moved into my new house in july 2014. so would not have received any court papers. I'm just looking for some legal advice on what id need to do to get this sorted it was due to come off in November this year so they got in before the 6 years and i can't afford to have this on my file as I've been trying so hard to sort my life out and it seems everything is now coming back to bite me I have also noticed a new company have applied a default to my credit file called MYJAR for £692 it looks like its for a old payday loan from txt loan from 2012-2013 again in my old address but i defaulted 2-3 years ago and its only just been put on my credit file and the default date is missing is this allowed as its showing on my file as if I've only just started missing payments ? Any help would be amazing and id be very grateful -

Some help and advice would be greatly appreciated I've received a N1 claim form this morning for a Aqua (New Day Cards ltd) credit card sold to MKDP The claim is for just under £1300 + £70 court fee. I'm not disputing the debt as I do genuinely owe it and from looking at the balance, minimal late fees/penalty fees were ever applied to the account I'm wondering what options are open to me as I contacted MKDP this morning with an offer to make a pay plan. I explained that I couldn't afford much as I'm on low income and in receipt of benefits such as housing benefit/tax credits/war disablement pension etc. They replied that yes, I can fill out the Admission part of the N1 with an offer of a monthly pay plan, but they'd still 'file the CCJ' with the court and warned me that it would appear on my credit file... ..For me personally, a CCJ would be a disaster as my partner and I rent a house and will probably have to move this year (can't afford the rent' and from what I understand, we'll find it very difficult finding an affordable rental property with a new CCJ on my file).... ..Are they allowed to accept a payment plan but still CCJ me?? MKDP bought the debt on 30/9/2014, they have sent me some letters asking for repayment, but to be totally honest, I've buried my head in the sand as I'm feeling buried with the amount of other debt we have and are unable to pay those as well

Some help and advice would be greatly appreciated I've received a N1 claim form this morning for a Aqua (New Day Cards ltd) credit card sold to MKDP The claim is for just under £1300 + £70 court fee. I'm not disputing the debt as I do genuinely owe it and from looking at the balance, minimal late fees/penalty fees were ever applied to the account I'm wondering what options are open to me as I contacted MKDP this morning with an offer to make a pay plan. I explained that I couldn't afford much as I'm on low income and in receipt of benefits such as housing benefit/tax credits/war disablement pension etc. They replied that yes, I can fill out the Admission part of the N1 with an offer of a monthly pay plan, but they'd still 'file the CCJ' with the court and warned me that it would appear on my credit file... ..For me personally, a CCJ would be a disaster as my partner and I rent a house and will probably have to move this year (can't afford the rent' and from what I understand, we'll find it very difficult finding an affordable rental property with a new CCJ on my file).... ..Are they allowed to accept a payment plan but still CCJ me?? MKDP bought the debt on 30/9/2014, they have sent me some letters asking for repayment, but to be totally honest, I've buried my head in the sand as I'm feeling buried with the amount of other debt we have and are unable to pay those as well -

Hi! I wonder if I could get a little help with a claim received for a Lloyds bank Small Business overdraft sold to MKDP, I'm submitting it on behalf of my wife, I have read several very similar threads so I believe I have a handle on how to deal with most of the process but I just want to be 100% Regards Lee PS I think this site is fantastic

-

I have received a claim form from Northampton CCBC as per below on Friday. I'm unsure what to do with this, the form states If you agree and are asking for time to pay then send this direct to the claimant and not the court as this may result in a judgement against you, does this mean if I make a deal with MKDP LLP then I will not get a CCJ? It's a long story of how I ended up with this debt but the short version is that in Jan 2008 I was out of work for 3 months, my overdraft facility was £1000 which was maxed. .. I had secured a new job but needed another £500 to see me through until the first payday, they refused of course.. . I moved bank accounts and didn't pay off the £1000 owing due to servicing other priority debts. I'm almost there out of my debt mountain, I have paid off everything other than the car which finishes in June and was hoping to buy a house in 12-18 months time but getting a CCJ now will end up with me getting a high rate if anything at all making it unaffordable. I think this may be more than 6 years old but have no way of proving this.. . the bank may have kept the account running for a good while as the £700 of charges must have taken a while to accrue. Do I contact them and try to make a deal? In all honesty it galls me that they have probably bought the debt for buttons and I'd like very much for them not to get a sausage, call me niave but if it was Lloyds themselves I'd offer to pay them back the grand (in bits) that I do indeed owe them but not this lot. I have seen a number of wins against them on various threads but don't know where to begin? Can anyone please help? Claimant MKDP LLP FLEMING HOUSE SEEBECK PLACE KNOWLHILL MILTON KEYNES MK5 8FR Defendant my name spelt incorrectly (does that matter?) Correct Address Particulars of claim The claimant claims the sum of 1,722.94 being monies due from the Defendant(s) to Lloyds Bank PLC under a bank account facility regulated by the Consumer Credit Act 1974 and assigned to the Claimant on 20/06/2014. The defendant(s) account number was (14 digit number... seems too long to be correct?). It was a term of the bank account that any debit balance would be repayable in full on demand. The Defendant(s) has failed to make payment as required by the demand for payment sent by Lloyds Bank PLC. The Claimant claims the sum of 1722.94 and costs. The Claimant has complied, and as far as is necessary, with the Pre-Action Conduct Practice Direction. Sorry I forgot to add that I opened the account in 1998.

-

My apologies for leaving this so late, but it had appeared that the claim wasn't moving forward. I have now found I'm in Court! Claimant: MKDP LLP (claim value £9999 - !) acknowledged and the attached defence submitted October 2014 Heard nothing further until Wednesday (25/02/2015) when claimant served witness statements and included various reconstituted documents. This was an electronic application from my Barclays current account for a Barclaycard made in 1992, I did not sign anything. I intended if this ever made it to Court to rely on unenforceable and the ‘four corners of the page’ for a properly executed agreement. None of this matters now as I am in Court. The claimant hasn’t filed or served in accordance with the Court Order (to be filed and served 16/02/2015) and I am wondering if I should object to their witness statements (for late filing) and apply to have their claim struck out and their claim dismissed with prejudice as they have no prospect of success. Alternatively as their witness statement may prove they have no case, should I leave it in and proceed to defend on the basis that no document was ever signed? The Claimant was served in September 2014 with S78 and cpr 31.14 requests. They said 31.14 didn’t apply as it was small claims. They said they would request info from Barclaycard and that it could take 8 weeks but would forward it on - this arrived in their witness statement on Wednesday. I’m beginning to flap now. Thanks for looking at this and please, if you can help, I’d really appreciate it. C

-

Hi. I received a letter from MKDP a couple of weeks back about my lloyds overdraft. I am sure that this account has not been acknowledged for possibly 8 years so I sent the statute barred letter. They responded today and apparently £3 was paid to the account in March 2010, which is nonsense. They have provided no proof they just say 'This has been confirmed with lloyds'. Can I ask them to provide proof or do I need to send a sar? Thanks, Paul.

-

Hi, I'm about to make a claim for missold PPI on a Welcome Finance loan sold that was sold to MKDP in 2010, it is definitely statute barred ( sure of that). I wanted to know if FSCS rules are different that with normal lenders, if I put the claim in will they be able to offset the refund against the debt? As far as I'm aware, a company can't offset a PPI refund against a debt that has been sold to an external DCA (in this case MKDP). I would be grateful for any help with this. Thanks in advance.

-

Hiya, Bit of a complex one, Got an account with Halifax that went into many problems - mainly system problems that caused the account to disappear, lose address records etc but it also lost my overdraft and was therefore moved to debt collection while I was in complaints process with them! Due to illness and a death in the family a few months passed and I did not hear back from Halifax. I then recieved out the blue a letter from MKDP saying I owe the account balance I gave them my complaint reference and re-wrote to Halifax who said they will get back to me in 4 weeks - I asked MKDP to put it on hold while this happened. Now today I have come in to see a court claim form from MKDP for the account balance + costs. Obviously I am going to defend myself against this especially as this is still in complaints but just want to know the best way to do it before I do Is it relevant as well that the claim has only been made in my name when it is joint account? Any help appreciated

Hiya, Bit of a complex one, Got an account with Halifax that went into many problems - mainly system problems that caused the account to disappear, lose address records etc but it also lost my overdraft and was therefore moved to debt collection while I was in complaints process with them! Due to illness and a death in the family a few months passed and I did not hear back from Halifax. I then recieved out the blue a letter from MKDP saying I owe the account balance I gave them my complaint reference and re-wrote to Halifax who said they will get back to me in 4 weeks - I asked MKDP to put it on hold while this happened. Now today I have come in to see a court claim form from MKDP for the account balance + costs. Obviously I am going to defend myself against this especially as this is still in complaints but just want to know the best way to do it before I do Is it relevant as well that the claim has only been made in my name when it is joint account? Any help appreciated -

Hi all Firstly apologies this is my first time posting, have had a good look around the site and am very impressed. I've been able to kind of answer my question by studying other posts here but would appreciate peoples opinions if they have time. I defaulted on a HSBC current account that was overdrawn in September 2009. The amount was approx. £4000 and was mostly unfair charges from the bank. I did attempt reclaiming charges prior to default but in the end just gave up, cowardly I know. Since 2009 I've moved addresses a few times and had letters from Compello Group chasing this matter up. Until now I've just ignored everything (possibly a stupid idea) Lately the letters have been coming from MKDP arm of Compello and the latest one looks a little more serious. Its a fishing letter no mistake "We have undertaken further investigation using Credit Reference Agencies in addition to other reliable databases and understand you reside at this address" goes on to say about an instruction to pre-legal department and if the matter proceeds possible CCJ, Balliffs or Attachment of Earnings. The matter would be Statute Barred by my calculation later this year (September 2015), but have read on here firms like MKDP go for a CCJ to prevent it becoming SB ? Should I go for it with the SAR, CCA letters do you think ? Or am I just entering a big next of vipers ?! Thanks folks

-

MKDP Barclaycard debt - used CCA £1 for payment?Pulling a Fast One......

Guest posted a topic in Barclaycard

Hello.... I think I''m being duped and am hoping you can advise on the following please....... Back on March 26th last year I CCAd MKDP regarding an outstanding debt on my credit file... Since then they have regularly written to say that they don't have the information and are liaising with the original creditor... Today I received a letter headed "Statement in relation to the below agreement governed by the consumer credit act 1974". It lays out details of the debt under query with the addition of a transaction made on the 28/2/2014 of £1 - plus another transaction on 2/4/2014 entitled "miscellaneous charge" of £1. That £1 can only be the fee related to the CCA letter. Are they effectively trying to prove a tacit agreement and re-activate the account - if so what steps should I take next? My initial reaction was to send a letter pointing out their "mistake" but then decided to council your opinion first. I've attached their letter and my CCA letter to make things a bit clearer... - which appear to have dropped off so added in later post... Kind regards and thanks - Andy

.thumb.jpg.bf2f59e5260173230834ce3ad8015900.jpg)

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS