Showing results for tags 'request'.

-

For tickets received through the post (Notice to Keeper) please answer the following questions. 1) Date of the infringement: 20/05/2016 2) Date on the NTK: 27/05/2016 3) Date received: 30/06/2016 4) Does the NTK mention schedule 4 of The Protections of Freedoms Act 2012? Yes “On the 20 May 2016 vehicle ‘reg correct’ entered the Marriott Huntington car park at 11:18:00 and departed at 13:36:24 on the 20 May 2016 May 2016. The signage, which is clearly displayed at the entrance to and throughout the car park, states that this is private land, the car park is managed by Parking Eye Ltd, as a permit only / paid parking car park, what parking tariffs apply and the parking charge applicable without the appropriate permit or payment of the appropriate tariff when parking, along with other terms and conditions of the car park by which those who park in the car park agree to be bound. By either not purchasing the appropriate parking time or parking without a valid permit, in accordance with the terms and conditions set out in the signage, the Parking Charge is now payable to Parking Eye Ltd (as the Creditor). You are notified under paragraph 9(2) (b) of schedule 4 of the Protection of Freedoms Act 2012 that the driver of the motor vehicle is required to pay this parking charge in full. As we do not know the driver's name or current postal address, if you were not the driver at the time, you should tell us the name and current postal address of the driver and pass this notice to them. You are warned that if, after 29 days from the date given (which is presumed to be the second working day after the Date Issued) the parking charge has not been paid in full and we do not know both the name and current address of the driver, we have the right to recover any unpaid part of the parking charge from you. This warning is given to you under paragraph 9 (2) (f) of Schedule 4 of the Protection of Freedoms Act 2012 and subject to our complying with the applicable conditions under Schedule 4 of that Act. Should you provide an incorrect address for service, we will pursue you for any Parking Charge amount that remains unpaid. Should you identify someone who denies they were the driver, we will pursue you for any Parking Charge amount that remains unpaid” 5) Is there any photographic evidence of the event? Yes 6) Have you appealed? Not directly to Parking Eye. I contacted the owner of the land Marriott Hotels on the 08/06/2016 and they contacted Parking Eye confirming I was a guest at a meeting and requested the charge be cancelled. Have you had a response? No 7 Who is the parking company? Parking Eye For either option, does it say which appeals body they operate under: Independent Appeals Service (POPLA) If you have received any other correspondence, please mention it here I received a further notice from Parking Eye on the 30th June stating the charge had now gone from £65 up to £100. And I had/have 14 days to pay it from the 30th June I assume. The Marriott Hotel advised me I didn’t need to contact Parking Eye as they would deal with it. After the second letter I contacted the Marriott again and they again emailed Parking Eye asking them to cancel the parking ticket. I am seeking advice on whether I should contact Parking Eye directly, what have other people experienced when the landowner attempts to cancel the parking charge? I am in the wrong in terms of the parking ticket I missed the multiple signs (new arrangement with Parking Eye and I just didn’t realise) Thank you for your assistance. Audrey

For tickets received through the post (Notice to Keeper) please answer the following questions. 1) Date of the infringement: 20/05/2016 2) Date on the NTK: 27/05/2016 3) Date received: 30/06/2016 4) Does the NTK mention schedule 4 of The Protections of Freedoms Act 2012? Yes “On the 20 May 2016 vehicle ‘reg correct’ entered the Marriott Huntington car park at 11:18:00 and departed at 13:36:24 on the 20 May 2016 May 2016. The signage, which is clearly displayed at the entrance to and throughout the car park, states that this is private land, the car park is managed by Parking Eye Ltd, as a permit only / paid parking car park, what parking tariffs apply and the parking charge applicable without the appropriate permit or payment of the appropriate tariff when parking, along with other terms and conditions of the car park by which those who park in the car park agree to be bound. By either not purchasing the appropriate parking time or parking without a valid permit, in accordance with the terms and conditions set out in the signage, the Parking Charge is now payable to Parking Eye Ltd (as the Creditor). You are notified under paragraph 9(2) (b) of schedule 4 of the Protection of Freedoms Act 2012 that the driver of the motor vehicle is required to pay this parking charge in full. As we do not know the driver's name or current postal address, if you were not the driver at the time, you should tell us the name and current postal address of the driver and pass this notice to them. You are warned that if, after 29 days from the date given (which is presumed to be the second working day after the Date Issued) the parking charge has not been paid in full and we do not know both the name and current address of the driver, we have the right to recover any unpaid part of the parking charge from you. This warning is given to you under paragraph 9 (2) (f) of Schedule 4 of the Protection of Freedoms Act 2012 and subject to our complying with the applicable conditions under Schedule 4 of that Act. Should you provide an incorrect address for service, we will pursue you for any Parking Charge amount that remains unpaid. Should you identify someone who denies they were the driver, we will pursue you for any Parking Charge amount that remains unpaid” 5) Is there any photographic evidence of the event? Yes 6) Have you appealed? Not directly to Parking Eye. I contacted the owner of the land Marriott Hotels on the 08/06/2016 and they contacted Parking Eye confirming I was a guest at a meeting and requested the charge be cancelled. Have you had a response? No 7 Who is the parking company? Parking Eye For either option, does it say which appeals body they operate under: Independent Appeals Service (POPLA) If you have received any other correspondence, please mention it here I received a further notice from Parking Eye on the 30th June stating the charge had now gone from £65 up to £100. And I had/have 14 days to pay it from the 30th June I assume. The Marriott Hotel advised me I didn’t need to contact Parking Eye as they would deal with it. After the second letter I contacted the Marriott again and they again emailed Parking Eye asking them to cancel the parking ticket. I am seeking advice on whether I should contact Parking Eye directly, what have other people experienced when the landowner attempts to cancel the parking charge? I am in the wrong in terms of the parking ticket I missed the multiple signs (new arrangement with Parking Eye and I just didn’t realise) Thank you for your assistance. Audrey -

I asked for a copy of a CCA agreement from Drysdens / Max Recovery recently. A letter dated March 2016 stated that they were unable to fulfill my request. A letter today from Drysden attached a "copy of the credit agreement conditions". It has none of my details on, nor my signature. The letter says " our client considers the debt due and owing" What do I do now?

I asked for a copy of a CCA agreement from Drysdens / Max Recovery recently. A letter dated March 2016 stated that they were unable to fulfill my request. A letter today from Drysden attached a "copy of the credit agreement conditions". It has none of my details on, nor my signature. The letter says " our client considers the debt due and owing" What do I do now? -

Sent a CCA request and this was the response, what do you recommend i do next? They have said they didn't send me the notification letters as they didn't have a confirmed address? the address is the same as the one on the CCA that they have sent these letters to? HFC, CCA request response.pdf

-

Hi, I have asked Robinson Way for a CCA request. But can I just clarify something please. The card was a Barclaycard which defaulted, sold to MKDPP who sold to Hoist/Robinson Way. The card was taken out in August 1993. As part of the CCA should I be sent a copy of a "true signed agreement" or can they send me a reconstituted one. I am not sure which one applies to my card or if in fact they could send either. Any help would be greatly appreciated. Also, is there legislation to say which one I should receive, if so what is that legislation. Many thanks

-

Hello, This is something I'm losing my sleep over. I've struggling for the last six months with the HMRC to obtain a full and detailed employment history going back to 16 years ago. I need this, because I need to send a request for permanent residency and I've lost some documentation. I first wrote to the HMRC last November and they replied almost immediately but only sending my national insurance contributions record. Then I wrote again in December, pointing out that I needed a breakdown of my employers instead. They replied in February, again sending the same ni record. So I called the hmrc helpline and the operator suggested that I wrote a request under the Data Protection Act, which I did immediately. I called the HMRC again in April and they told me that, due to the length of the period, it might take up to 375 days. However on their website they state: Now it's more than 3 months and yet no answer has come. Incidentally, re-reading the letter I sent, I have realised I had omitted my national insurance number. Terrible mistake, however I had included so much data that they could identify me without delays. What do do now? I'll call the HMRC tomorrow and if it goes nowhere, I'll write a second letter. Is there anything else I can do? This thing has been eating me for the last six months. Thank you

-

Hi I would like to were I stand about requesting my landlords details? The reason for this is about two months ago they tried to fit prepayment meters in the property, which I refused to let the engineer to do. I live in a shared house, we pay one sum for rent and all bills expect TV license. We have a sheared kitchen, utility room and bath room. I rang my local council for information regarding this and was told we should be a HMO (house of multiple occupancy) and the house is not registered as one. The council are now requesting me to let them do an inspection? so I called them about it and got fobbed off, so I requested my landlords details as no one has it in the house. I have sent numerous emails, calls and texts and had not received any reply. So I sent this to them on the 13.04.2016 and no reply. Any help would be very appropriated. Strongdumplin I am the tenant of the above property. Under section 1 of the Landlord and Tenant Act 1985, I hereby request you to provide me with a written statement of the landlord’s name and address within the period of 21 days beginning with the day on which you receive this request. You should be aware that a person who, without reasonable excuse, fails to comply with this request commits a summary offence and is liable on conviction to a fine not exceeding level 4 on the standard scale, which currently stands at £2,500. I look forward to receiving your prompt reply. Yours sincerely.

Hi I would like to were I stand about requesting my landlords details? The reason for this is about two months ago they tried to fit prepayment meters in the property, which I refused to let the engineer to do. I live in a shared house, we pay one sum for rent and all bills expect TV license. We have a sheared kitchen, utility room and bath room. I rang my local council for information regarding this and was told we should be a HMO (house of multiple occupancy) and the house is not registered as one. The council are now requesting me to let them do an inspection? so I called them about it and got fobbed off, so I requested my landlords details as no one has it in the house. I have sent numerous emails, calls and texts and had not received any reply. So I sent this to them on the 13.04.2016 and no reply. Any help would be very appropriated. Strongdumplin I am the tenant of the above property. Under section 1 of the Landlord and Tenant Act 1985, I hereby request you to provide me with a written statement of the landlord’s name and address within the period of 21 days beginning with the day on which you receive this request. You should be aware that a person who, without reasonable excuse, fails to comply with this request commits a summary offence and is liable on conviction to a fine not exceeding level 4 on the standard scale, which currently stands at £2,500. I look forward to receiving your prompt reply. Yours sincerely. -

Hello, I wonder if anyone can help me. I bought 2 items from an ebay seller listed as a business seller. Firstly there was a problem with postage, 2nd item was supposed to be £1.00 postage and was charged full. Wrote a friendly email, no reply, left a friendly phone message and asked if I should go through paypal or if they could sort it. It was sorted the next day. OK, the items are not suitable, I collected from the post office last saturday, seller has a 14 day return policy and insists on a form being filled out via access to an ebay account. No ebay account. Have written 3 polite emails requesting the return, left 2 polite phone messages indicitating said emails are awaiting response. Meanwhile checked the new rules for distance selling, Consumer Contract Regulations. This says that the form requested is to make cancelling easier but does not affect the return of goods. As I used ebay as a guest I can't access the form the seller insists on and have made a request by email 3 times now and twice by phone. So as I understand it I have fulfilled my obligation to alert the seller within the 14 days (day 1 actually) that I want to return the items for a refund. No word from the seller. Any idea how I might proceed with this now to ensure the seller gives me a refund. I am trying to keep things cordial but I am anxious to get the items back and have the money returned to my account. Help much appreciated.

-

Good Afternoon CAG Firstly i would like to thank the people that helped me in my first two issues that are now resolved you know who you are much appreciated. I have another issue that involves opos limited in 2012 i was being contacted constantly bu this company they were even harassing my employers switchboard trying to contact me. in July 2012 I was asked to attend a HR meeting with my employer to discuss informally the nuisance calls that there switchboard was receiving from Opos Limited asking for me and being very aggressive with staff, I was asked for this to stop as company switchboard was not my personal secretaries and if it continued we would be coming back for a more formal discussion. Immediately i contacted the ICO who advised me to send them a section 10 notice for them to remove my details and i did state they should correspond with me in writing, I also sent an email as well stating the same thing Everything stopped for 3yrs 5mths, Then December 2015 i received an email at work from Opos followed by harassing calls to my mobile, I once again asked them to remove my details and they were in breach of the section 10 notice sent to them in July 2012, They once again removed by details and said they would only correspond via Letter as requested. You would think this was the end sadly not Roll on March 2016 once again start ringing me sending emails to my work wouldn't stop, I contacted Opos which i am very lucky to have a call recorded on my phone which records all out and inbound calls and has been very handy in the past, I wanted to make a complaint which i was told i couldn't and they wouldn't take one , Spoke to a manager who also refused to take the complaint same time also refusing to remove my details stating they sent me a letter to an old address saying that if i do not reply to them via letter they would re-instate my details and start contacting all over again, I sent an email to Opos expressing my dissatisfaction on what was happening they responded via letter to say they would investigate my complaint and would supply me with a final response, Many weeks had past and approaching the 8 week deadline, I called them to be told it was sent out on the 27th March and still in the post, I asked if they could sent a copy to my email. Next day they started harassing me once again two calls 8.00am & 8.01am Yesterday morning i answered second time the agent from Opos was so aggressive and rude i asked to make a complaint and be put through to her manager, I explained to her manager very clearly i wished to make a second complaint in relation to the agent i had just spoken to, They once again like the first time refused to take the complaint stating they had already sent a final response and i should take it up with financial ombudsman, I explained that this second complaint is nothing do do with the first complaint and is in relation to whats happened on the call today, Once again manager refused to take complaint and hung up on me, I email Opos complaints team after this, They responded saying the manager may have be confused by what i want to do and want me to send them the complaint again, I will be refusing i have made it very clear twice on that call in great detail of my complaint so should have to do it all over again they have already sacked somebody over this the first time as you will see from final response. Now there repeating the same thing all over again Here is Opos Limited's Final Response --- I have removed identifiable contact numbers and email addresses Further to your recent communications with our office, I am concerned to hear that you have been dissatisfied with the service that has been provided. At Opos Limited we always welcome customer comments as it helps us to review our processes and where necessary put things right for you. Please note that this debt was purchased in December 2014 by Kapama Limited and as a result is now being managed by Opos Limited. My understanding of your complaint is that: 1. You were contacted by email to an employee email address which you had previously requested was removed from our systems 2. You were unhappy that a complaint had not been logged on the first occassion that you expressed you were dissatisfied In reference to the contact information we held for you, the email address of @bri was supplied during the application process for this loan, along with a second email of @live.co.uk. On the 10th July 2012 we sent an email to both of these email addresses requesting that you contact us to resolve the above balance. At this point we were acting on behalf of Mini Credit and both of these emails were supplied as a contact method for yourself. Following this, we received an email from you requesting that the contact emails were removed and that we contact you only by post. At this point we did remove all other forms of contact, which included both email and telephone numbers. We did send information to you by post as requested on three separate occasions; 19th July 2012, 24th July 2012 and 9th September 2012. This account was then passed back to Mini Credit in 2012 as we were unable to contact you. In December 2014 this debt was purchased by Kapama Limited, and the account was then reopened with Opos Limited on 16th October 2015. We again attempted to contact you by post, however had no response. As a result of this we reinstated the contact telephone number of 07 and the email addresses we had on the system, as we had no other way to contact you to discuss your outstanding balance. We spoke with you on 7th December 2015 and again you stated only to contact you by post. Our agent advised you at this time that if we had no response via post then we would reinstate other contact methods, as we had an outstanding balance to resolve with you. Again, we had no response from you by post and no payments were made towards your outstanding balance. As advised, the contact information we held for you was reinstated as we had an outstanding balance to discuss and had been unsuccessful using the contact method you had stated you would respond to. In terms of the annual account statement, this is a document we send out in line with the regulatory oblilgations set out by the Financial Conduct Authority. These were all set out by email and it was appropriate to send this to you as we had no contact from you to resolve this balance. I understand that you called in on 15th March 2016 as you were unhappy you had recieved this. Our agent did advise why this was the case and explained why the contact information had been reinstated, but at that point you advised her that you wanted to make a formal complaint. Although you did end the call, this complaint should still have been logged and I can only apologise that this was not done at that time. This was down to the human error of the particular agent who dealt with you. It is unfortunate that in this instance we have not achieved the high standards we set ourselves and can confirm that the right level of feedback has been given to the individual concerned. In addition, further steps have been taken to ensure that this cannot happen again and the individual concerned is no longer employed by Opos Limited. Feedback has also been given to the collections team using your case as an example of how human error can negatively impact our customers’ journey. For the record i did not hang up i was transferred to a manager who also started stating i could not raise a complaint backing up here colleague, So looks like they sacked the agent and not the manager even though both equally responsible, Here are some other points they make not relating to my complaint do not know why they included it since i have never acknowledged this debt and never will, The credit agreement sets out the borrower: your name and correct address, the duration of the credit facility, the amount of interest charged per day and the APR, the charges applied should you not pay back the amount in time, as well as all terms and conditions associated with this information. According to the information provided by Mini Credit at the point of sale, the default date of this accountis 5th July 2012. Unfortunately, a copy of the default notice issued to you was not included in the documentation provided but it should be noted that whilst it is good practice and should ideally be done, lenders are not required to issue default notices before recording defaults on a credit file. Because of this, I have to tell you that I am only able to partially uphold your complaint. I appreciate that this is likely to come as a disappointment to you but I hope that my explanation has been helpful in setting out clearly why I have taken this view. That said however, in an effort to put things right for you and by way of apology for any inconvenience caused, I propose to remove the debt collection fee from your outstanding balance, which will reduce Opos Limited Registered Office: 2nd Floor, 15 Meadowbank Street, Dumbarton, Dunbartonshire, G82 1JR Registered in Scotland: SC338837 Telephone: 0141 428 3990 Email: general@oposlimited.com Secure Website: www.oposlimited.com Authorised and Regulated by the Financial Conduct Authority: IP616281 Calls may be recorded for training and quality purposes your balance by £100 and leave an outstanding balance of £1,089.00. Upon repayment of this balance, this will also be reflected on your credit file. If you wish to accept my proposal as final resolution of your complaint, please complete the section on the bottom of both copies of this letter, retain a one copy for yourself and return the other to me within 30 days of the date of this letter. If you fail to respond to this offer within the given timeline my offer of resolution will not be binding and the full outstanding balance will be due. To date i am in the middle of taking my complaint to ICO as a Section 10 has no time limit and feel my data is not been processed correctly. I need somebody help me put a case together to send to the financial ombudsman, Also is what they say correct lenders are not required to issue default notices before recording defaults on a credit file Thank you for taking the time to stop by and thank you in advance for any advice you can give me as the harassment is non stop, Regards PCR

Good Afternoon CAG Firstly i would like to thank the people that helped me in my first two issues that are now resolved you know who you are much appreciated. I have another issue that involves opos limited in 2012 i was being contacted constantly bu this company they were even harassing my employers switchboard trying to contact me. in July 2012 I was asked to attend a HR meeting with my employer to discuss informally the nuisance calls that there switchboard was receiving from Opos Limited asking for me and being very aggressive with staff, I was asked for this to stop as company switchboard was not my personal secretaries and if it continued we would be coming back for a more formal discussion. Immediately i contacted the ICO who advised me to send them a section 10 notice for them to remove my details and i did state they should correspond with me in writing, I also sent an email as well stating the same thing Everything stopped for 3yrs 5mths, Then December 2015 i received an email at work from Opos followed by harassing calls to my mobile, I once again asked them to remove my details and they were in breach of the section 10 notice sent to them in July 2012, They once again removed by details and said they would only correspond via Letter as requested. You would think this was the end sadly not Roll on March 2016 once again start ringing me sending emails to my work wouldn't stop, I contacted Opos which i am very lucky to have a call recorded on my phone which records all out and inbound calls and has been very handy in the past, I wanted to make a complaint which i was told i couldn't and they wouldn't take one , Spoke to a manager who also refused to take the complaint same time also refusing to remove my details stating they sent me a letter to an old address saying that if i do not reply to them via letter they would re-instate my details and start contacting all over again, I sent an email to Opos expressing my dissatisfaction on what was happening they responded via letter to say they would investigate my complaint and would supply me with a final response, Many weeks had past and approaching the 8 week deadline, I called them to be told it was sent out on the 27th March and still in the post, I asked if they could sent a copy to my email. Next day they started harassing me once again two calls 8.00am & 8.01am Yesterday morning i answered second time the agent from Opos was so aggressive and rude i asked to make a complaint and be put through to her manager, I explained to her manager very clearly i wished to make a second complaint in relation to the agent i had just spoken to, They once again like the first time refused to take the complaint stating they had already sent a final response and i should take it up with financial ombudsman, I explained that this second complaint is nothing do do with the first complaint and is in relation to whats happened on the call today, Once again manager refused to take complaint and hung up on me, I email Opos complaints team after this, They responded saying the manager may have be confused by what i want to do and want me to send them the complaint again, I will be refusing i have made it very clear twice on that call in great detail of my complaint so should have to do it all over again they have already sacked somebody over this the first time as you will see from final response. Now there repeating the same thing all over again Here is Opos Limited's Final Response --- I have removed identifiable contact numbers and email addresses Further to your recent communications with our office, I am concerned to hear that you have been dissatisfied with the service that has been provided. At Opos Limited we always welcome customer comments as it helps us to review our processes and where necessary put things right for you. Please note that this debt was purchased in December 2014 by Kapama Limited and as a result is now being managed by Opos Limited. My understanding of your complaint is that: 1. You were contacted by email to an employee email address which you had previously requested was removed from our systems 2. You were unhappy that a complaint had not been logged on the first occassion that you expressed you were dissatisfied In reference to the contact information we held for you, the email address of @bri was supplied during the application process for this loan, along with a second email of @live.co.uk. On the 10th July 2012 we sent an email to both of these email addresses requesting that you contact us to resolve the above balance. At this point we were acting on behalf of Mini Credit and both of these emails were supplied as a contact method for yourself. Following this, we received an email from you requesting that the contact emails were removed and that we contact you only by post. At this point we did remove all other forms of contact, which included both email and telephone numbers. We did send information to you by post as requested on three separate occasions; 19th July 2012, 24th July 2012 and 9th September 2012. This account was then passed back to Mini Credit in 2012 as we were unable to contact you. In December 2014 this debt was purchased by Kapama Limited, and the account was then reopened with Opos Limited on 16th October 2015. We again attempted to contact you by post, however had no response. As a result of this we reinstated the contact telephone number of 07 and the email addresses we had on the system, as we had no other way to contact you to discuss your outstanding balance. We spoke with you on 7th December 2015 and again you stated only to contact you by post. Our agent advised you at this time that if we had no response via post then we would reinstate other contact methods, as we had an outstanding balance to resolve with you. Again, we had no response from you by post and no payments were made towards your outstanding balance. As advised, the contact information we held for you was reinstated as we had an outstanding balance to discuss and had been unsuccessful using the contact method you had stated you would respond to. In terms of the annual account statement, this is a document we send out in line with the regulatory oblilgations set out by the Financial Conduct Authority. These were all set out by email and it was appropriate to send this to you as we had no contact from you to resolve this balance. I understand that you called in on 15th March 2016 as you were unhappy you had recieved this. Our agent did advise why this was the case and explained why the contact information had been reinstated, but at that point you advised her that you wanted to make a formal complaint. Although you did end the call, this complaint should still have been logged and I can only apologise that this was not done at that time. This was down to the human error of the particular agent who dealt with you. It is unfortunate that in this instance we have not achieved the high standards we set ourselves and can confirm that the right level of feedback has been given to the individual concerned. In addition, further steps have been taken to ensure that this cannot happen again and the individual concerned is no longer employed by Opos Limited. Feedback has also been given to the collections team using your case as an example of how human error can negatively impact our customers’ journey. For the record i did not hang up i was transferred to a manager who also started stating i could not raise a complaint backing up here colleague, So looks like they sacked the agent and not the manager even though both equally responsible, Here are some other points they make not relating to my complaint do not know why they included it since i have never acknowledged this debt and never will, The credit agreement sets out the borrower: your name and correct address, the duration of the credit facility, the amount of interest charged per day and the APR, the charges applied should you not pay back the amount in time, as well as all terms and conditions associated with this information. According to the information provided by Mini Credit at the point of sale, the default date of this accountis 5th July 2012. Unfortunately, a copy of the default notice issued to you was not included in the documentation provided but it should be noted that whilst it is good practice and should ideally be done, lenders are not required to issue default notices before recording defaults on a credit file. Because of this, I have to tell you that I am only able to partially uphold your complaint. I appreciate that this is likely to come as a disappointment to you but I hope that my explanation has been helpful in setting out clearly why I have taken this view. That said however, in an effort to put things right for you and by way of apology for any inconvenience caused, I propose to remove the debt collection fee from your outstanding balance, which will reduce Opos Limited Registered Office: 2nd Floor, 15 Meadowbank Street, Dumbarton, Dunbartonshire, G82 1JR Registered in Scotland: SC338837 Telephone: 0141 428 3990 Email: general@oposlimited.com Secure Website: www.oposlimited.com Authorised and Regulated by the Financial Conduct Authority: IP616281 Calls may be recorded for training and quality purposes your balance by £100 and leave an outstanding balance of £1,089.00. Upon repayment of this balance, this will also be reflected on your credit file. If you wish to accept my proposal as final resolution of your complaint, please complete the section on the bottom of both copies of this letter, retain a one copy for yourself and return the other to me within 30 days of the date of this letter. If you fail to respond to this offer within the given timeline my offer of resolution will not be binding and the full outstanding balance will be due. To date i am in the middle of taking my complaint to ICO as a Section 10 has no time limit and feel my data is not been processed correctly. I need somebody help me put a case together to send to the financial ombudsman, Also is what they say correct lenders are not required to issue default notices before recording defaults on a credit file Thank you for taking the time to stop by and thank you in advance for any advice you can give me as the harassment is non stop, Regards PCR -

Nat West Directors Personal Guarantee - request for advice

bubblesmum posted a topic in NatWest Bank

Dear All, In June 2014, my partner and I arranged an overdraft with our business bank (Nat West) as match funding for a government loan scheme. We were asked to sign a personal directors guarantee and, at the same moment in time, signed the waiver to legal advice form in the bank's office. Sadly, our business has now been declared insolvent and the bank are now calling in the personal guarantee for £20k. Originally, we did not believe we had signed a guranatee but the bank have now come up with the evidence (although that was never originally forwarded to us so we had no copy until now). We have also never received a copy of the overdraft agreement signed in June 14 although we have one signed September 14 with a pp signature from the bank. We were also asked to sign a debenture (again, we have no signed copy) and also a postponement of directors loan account which we definitely didn't sign as they were still chasing us for that in February last year and I know we never signed this. I recently wrote to the bank asking for copies of ALL signed security documents and they only sent me the PG and waiver. I have written to them again today asking for the other security documents. Nether my partner nor I are ones to shirk our responsibilities but I would like to come to an arrangement/agreement with the bank to either pay a lesser amount or a small monthly payment. I have already lost 200k personally from the business failure and hoped that was the end of it. I have phoned several companies who state they deal with these types of issues but not one has come back to me. My question is How is it best to start the process of negotiation with Nat West and what should I say initially? And is it feasible that the guarantee could somehow be unenforceable? I should say that I had another company (Credit4 - beware!) took me to court re another directors personal guarantee for the same failed company and got a ccj and a charging order against a property I owned. i have had to sell that property (my main income) to satisfy their debt and have a small sum left over which I really want to keep to buy somewhere else to live now. Another £20k will add to my losses even more and will dent that small sum. I can't get a mortgage now due to this ccj, even though it is settled, hence why I need to keep as much as I can to buy somewhere to live without a mortgage. My partner now has a new job but has to live away as its not local. We cant afford to buy anything where he is working. Feeling really fed up and just wondered if anyone had some sensible advice on how to get a settlement agreed. Or to know someone who can help at a reasonable cost. A little light at the end of this dark tunnel would be so nice. Thank you in advance to anyone who responds to my request -

Having received court paperwork from hoist portfolio holding for a old HSBC overdraft And loan all merged into one account. Sent hoist solicitors a CPR request After hearing nothing submitted a holding defence I now have notice of proposed allocation to small claims track Do I need to tick no to small claims track being appropriate as they have failed with CPR request Can only find conflicting information looking online about what to put:boxing:

Having received court paperwork from hoist portfolio holding for a old HSBC overdraft And loan all merged into one account. Sent hoist solicitors a CPR request After hearing nothing submitted a holding defence I now have notice of proposed allocation to small claims track Do I need to tick no to small claims track being appropriate as they have failed with CPR request Can only find conflicting information looking online about what to put:boxing: -

Early last year my husband received a county court summons for £11,500 for a credit card debt sold on to a DCA. He replied and defended the action on the basis of the limited information on the summons and that he was awaiting a reply to the CCA letter sent to them on the day the summons was received. He never received a copy of the CCA, just a letter from them saying the debt was no longer enforceable and they could not proceed any further through the courts, but would he please call them to discuss a repayment plan. They also promised to forward the copy of the CCA. That was over a year ago and we are still haven’t received the CCA, but what he did not advise them was the debt would not really be statute barred until last October , three months after their letter. Move forward to now, and I have received a letter from the same DCA and they are chasing a debt for £8.250 for a card of mine. This will become statute barred in the middle of August when it will be 6 years since the last payment. I received a letter from them dated 6 April but not received until 12 April, saying if I did not contact them within 14 days they would commence legal action. My understanding of statute barred debts is they expire six years after the last payment or admission of the debt and the creditor has until this time to obtain judgement. Is this correct and can the DCA request to the courts an extension this period for the time it takes to transfer to a local court and to a hearing? The default for this will expire soon and I am l keen to keep as clean a record as possible after eight years of financial misery. I appreciate I am morally wrong but this DCA will have purchased the debt for peanuts,

Early last year my husband received a county court summons for £11,500 for a credit card debt sold on to a DCA. He replied and defended the action on the basis of the limited information on the summons and that he was awaiting a reply to the CCA letter sent to them on the day the summons was received. He never received a copy of the CCA, just a letter from them saying the debt was no longer enforceable and they could not proceed any further through the courts, but would he please call them to discuss a repayment plan. They also promised to forward the copy of the CCA. That was over a year ago and we are still haven’t received the CCA, but what he did not advise them was the debt would not really be statute barred until last October , three months after their letter. Move forward to now, and I have received a letter from the same DCA and they are chasing a debt for £8.250 for a card of mine. This will become statute barred in the middle of August when it will be 6 years since the last payment. I received a letter from them dated 6 April but not received until 12 April, saying if I did not contact them within 14 days they would commence legal action. My understanding of statute barred debts is they expire six years after the last payment or admission of the debt and the creditor has until this time to obtain judgement. Is this correct and can the DCA request to the courts an extension this period for the time it takes to transfer to a local court and to a hearing? The default for this will expire soon and I am l keen to keep as clean a record as possible after eight years of financial misery. I appreciate I am morally wrong but this DCA will have purchased the debt for peanuts, -

Hi Guys Long winded but will cut it down best I can, will start with the numbers loan 1 July 98 for £3000 PPI single policy of £443 added to loan (paid 46/60 payments) £144 of ppi refinanced by loan 3 loan 2 Dec 98 for £1400 PPI single policy of £198 added to loan (paid 39/48 payments) £50 of ppi refinanced by loan 3 loan 3 April 02 for £5000 PPI single policy of £1174 added to loan (paid 13/60 payments) £980 of ppi refinanced by loan 4 loan 4 may 03 for £7500 PPI single policy of £1762 added to loan (paid 11/60 payments) £1500 of ppi refinanced by loan 5 loan 5 may 03 for £11000 PPI single policy of £2383 added to loan (paid 12/60 payments) £2032 of ppi refinanced by loan 6 loan 6 may 08 for £10000 PPI NO PPI added to loan still paying Now we had a decision letter from Lloyd's stating they upheld all of the complaints offering refund of the ppi part of the loan that was paid in installments plus interest, which worked out about £7,700 according to their workings out, I had it in my head from working it out that it should have been nearer 10k but at first glance of their workings it looked OK but I still couldn't get it out of my head that something was wrong. It then clicked that they had calculated all their figures ONLY on the installments made and had completely ignored the bits that were left on refinancing which by itself without adding interest is about £4700, this amount is still being paid off on loan 6. I phoned them as the offer letter tells me to do and explained why I felt it was wrong, the guy said that I am not entitled to that bit back as the loan was refinanced, I argued and tried to speak to a manager but was brickwalled, he insisted I was wrong and that the payment of £7700 was going to be sent, I told him at this point that I DO NOT ACCEPT the offer, and under no circumstances are they to consider the matter closed, I even got him to repeat it back to me several time, as they supposedly record the calls. what I would like to know is am I wrong, am I not able to reclaim the bits that were refinanced by the new loans, or are Lloyd's trying it on Many Thanks

Hi Guys Long winded but will cut it down best I can, will start with the numbers loan 1 July 98 for £3000 PPI single policy of £443 added to loan (paid 46/60 payments) £144 of ppi refinanced by loan 3 loan 2 Dec 98 for £1400 PPI single policy of £198 added to loan (paid 39/48 payments) £50 of ppi refinanced by loan 3 loan 3 April 02 for £5000 PPI single policy of £1174 added to loan (paid 13/60 payments) £980 of ppi refinanced by loan 4 loan 4 may 03 for £7500 PPI single policy of £1762 added to loan (paid 11/60 payments) £1500 of ppi refinanced by loan 5 loan 5 may 03 for £11000 PPI single policy of £2383 added to loan (paid 12/60 payments) £2032 of ppi refinanced by loan 6 loan 6 may 08 for £10000 PPI NO PPI added to loan still paying Now we had a decision letter from Lloyd's stating they upheld all of the complaints offering refund of the ppi part of the loan that was paid in installments plus interest, which worked out about £7,700 according to their workings out, I had it in my head from working it out that it should have been nearer 10k but at first glance of their workings it looked OK but I still couldn't get it out of my head that something was wrong. It then clicked that they had calculated all their figures ONLY on the installments made and had completely ignored the bits that were left on refinancing which by itself without adding interest is about £4700, this amount is still being paid off on loan 6. I phoned them as the offer letter tells me to do and explained why I felt it was wrong, the guy said that I am not entitled to that bit back as the loan was refinanced, I argued and tried to speak to a manager but was brickwalled, he insisted I was wrong and that the payment of £7700 was going to be sent, I told him at this point that I DO NOT ACCEPT the offer, and under no circumstances are they to consider the matter closed, I even got him to repeat it back to me several time, as they supposedly record the calls. what I would like to know is am I wrong, am I not able to reclaim the bits that were refinanced by the new loans, or are Lloyd's trying it on Many Thanks -

Hi I have several debts that have been passed to Lowell's. I've had the usual letters from them requesting payment etc. Some of the balances though, seem a lot higher than i remember so have written to Lowell's the standard letter requesting CCA. The letter was dated 15th January 2016. I have had a couple of replies which read as follows: "you have requested documentation under sections 77/78 of the Consumer Credit Act 1974 for this former/B]XXXX account. We have asked XXXX to provide us with the requested documentation and will send this to you as soon as possible. We aim to provide this to you within 12 working days. In the meantime this account is on hold and we will not contact you to request payment. If we have not heard anything from XXXX after 40 days we will send you an update." I received the following letter as a follow up to the above one: "We refer to your recent request under sections 77/78 of the consumer Credit Act 1974 for a copy of the documentation for this former XXXX account. We have requested a copy of the documentation but have not received this yet. Your account will remain on hold while we await the requested information from XXXX." My questions are: 1. In both letters they refer to the account as a "former" account. Does this mean the debt now belongs to Lowell completely or are they simply acting as an Agent? 2. I want to do a follow up letter to Lowell's about all the accounts but am unsure of the time scales within which they have to supply the requested information. I've tried looking this up but keep getting conflicting information. Am I correct in thinking that the first deadline is 12 days plus 2 (is this working days or just continuous days?)? They also mention a further 40 days time limit. From the research I've done I've only come across 30 days but again don't know if this is working days or not. Could someone please clarify the time limits and from which date each time limit should commence? 3. Finally could someone advise on a follow up letter or a template letter that i can use? The original letter I sent made no acknowledgement to the debts. Hope someone can help.

-

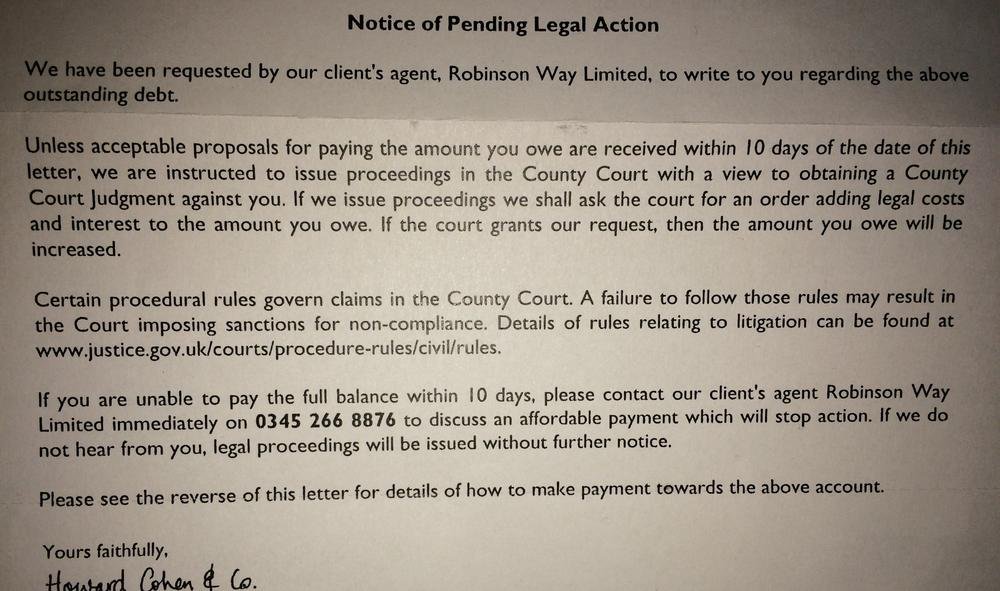

I'm usually happy to ignore letters from debt collectors but this one seems to be more definitive in its terminology. Do you think I should I make the CCA request to Robinson Way? I've never contacted them before. TIA!

-

In October 2015 we ordered a new Buccaneer Cruiser caravan and paid a deposit of £1000. The caravan is due to delivery within the next few days. We chose this caravan as it is wider and has self levelling making it easier for me as I have rheumatoid arthritis and therefore mobility problems. Between the time we paid the deposit and now we raise a few issues about the rear panels on these caravans as there was an issue with some developing cracks. The caravan is advertised with a 10 year water ingress warranty and one would assume that this covers the outside panels however on reading the owner's manual which cna be obtained online I found out that the panels only had a 1 year warranty. I emailed the dealer on a few occasions with our concerns about the rear panel and they replied and gave us re-assurance and I left it at that however on Saturday someone went to take delivery of their 2016 Cruiser and foudn crazing on the rear panel. I raised this with the dealer as we were have 2 units fitted onto the caravan and requested if we coudl view the caravan when it was delivered and before they did any fitments to the caravan. This was their response; Martyn is on holiday at the moment and won’t be back for a few weeks .I have just been looking through your email with the concerns you have with the buccaneer cruiser 2016. I then started to look though the rest of the emails you have sent us over the past few months. You have great concerns with the caravan . On a personal level ,this occasion we feel this would cause you a great deal of stress to yourself and the company if a problem was to happen in the future with the buccaneer cruiser. with this in mind on this occasion I obliged to return your deposit and cancel your order. we feel this is the best course of action for you .can you please call us to return your deposit asap . Can they cancel the order and issue a refund bearing in mind that they have had our deposit for 5 months plus I have had to paid £425 for the air con on our current caravan to be transferred and another £99 deposit for a Paintseal treatment? The wife is absolutely livid as she has been looking forward to us taking delivery of the caravan.

In October 2015 we ordered a new Buccaneer Cruiser caravan and paid a deposit of £1000. The caravan is due to delivery within the next few days. We chose this caravan as it is wider and has self levelling making it easier for me as I have rheumatoid arthritis and therefore mobility problems. Between the time we paid the deposit and now we raise a few issues about the rear panels on these caravans as there was an issue with some developing cracks. The caravan is advertised with a 10 year water ingress warranty and one would assume that this covers the outside panels however on reading the owner's manual which cna be obtained online I found out that the panels only had a 1 year warranty. I emailed the dealer on a few occasions with our concerns about the rear panel and they replied and gave us re-assurance and I left it at that however on Saturday someone went to take delivery of their 2016 Cruiser and foudn crazing on the rear panel. I raised this with the dealer as we were have 2 units fitted onto the caravan and requested if we coudl view the caravan when it was delivered and before they did any fitments to the caravan. This was their response; Martyn is on holiday at the moment and won’t be back for a few weeks .I have just been looking through your email with the concerns you have with the buccaneer cruiser 2016. I then started to look though the rest of the emails you have sent us over the past few months. You have great concerns with the caravan . On a personal level ,this occasion we feel this would cause you a great deal of stress to yourself and the company if a problem was to happen in the future with the buccaneer cruiser. with this in mind on this occasion I obliged to return your deposit and cancel your order. we feel this is the best course of action for you .can you please call us to return your deposit asap . Can they cancel the order and issue a refund bearing in mind that they have had our deposit for 5 months plus I have had to paid £425 for the air con on our current caravan to be transferred and another £99 deposit for a Paintseal treatment? The wife is absolutely livid as she has been looking forward to us taking delivery of the caravan. -

HI there i am appealing a mandatory review from the ESA. Is there a form that i can use to ask for all info they have held on record about me? If there is could you post a link as i can't find one. Is there also a charge for this? \thanx in advance

-

Hi Guys Im trying to be proactive regarding some letters im receiving from Cabot but i cannot find a recent SAR address for MBNA? Does this one look current? I found it on thread dated from 2007, thats my only concern. MBNA Europe Bank Ltd PO Box 1004 Chester Business Park Wrexham Road Chester CH4 9WW

-

Hello, im after some advice if possible. CAG has been helpful to read but im now stuck. Following redundancy I got into a bit of credit card debt, im now in a position to try and resolve the debt but don't know where I stand. One of the credit card debts is now with Idem servicing. I sent the a CCA request and they replied stating they had no agreement, should one be found they would send it. Foolishly maybe, I offered a full and final settlement offer just to move on. They rejected the offer and sent a credit card agreement (13 days after they said they didn't have one). They say the agreement was signed in 2001, however the address on the agreement is the address I moved to in 2008, so a different address I was at in 2001, secondly the credit limit states 1500£, with an APR of 27.9%, I cant prove it but the original credit limit was 950£ and the APR 15.9%, it only went up to 27.9% when I closed my current account at the Halifax and moved to Barclays around 2005/6, I remember that because at the time as I was annoyed to put it mildly - Just to add the credit card was with the Halifax. Idems letter keeps referring to LLoyds Banking Group are they linked to Halifax? The agreement also says bank charges were 12£, again I remember paying 35£ when one of my first payments was a few days late. Some pages of the agreement are blue, some white and all different fonts. Idem claim they own the debt, but terms in the agreement only state they can transfer the debt, but another clause in the terms says only We or You (meaning Halifax or me I assume) can enforce any part of the agreement. The agreement also state that interest will not be charged on defaulted accounts, however Halifax continued to apply interest when in the debt management plan and the account had been defaulted. Where the signature is supposed to be for me is blank, and the agreement contains no dates. Can anyone advise where I stand with this agreement. I can scan in later if it helps? It all just seems dodgy to me, and incorrect for the terms I remember. The debt is also 5481£ which is significantly higher than I recall ( I did bury my head in the sand for a few years, I had no money and no way of dealing with the debts, contributions were made through a dmp, it has been defaulted but the 6 years has now passed) The agreement just isn't correct from what I can see, but if anyone could advise further, it would be greatly appreciated? Chris

Hello, im after some advice if possible. CAG has been helpful to read but im now stuck. Following redundancy I got into a bit of credit card debt, im now in a position to try and resolve the debt but don't know where I stand. One of the credit card debts is now with Idem servicing. I sent the a CCA request and they replied stating they had no agreement, should one be found they would send it. Foolishly maybe, I offered a full and final settlement offer just to move on. They rejected the offer and sent a credit card agreement (13 days after they said they didn't have one). They say the agreement was signed in 2001, however the address on the agreement is the address I moved to in 2008, so a different address I was at in 2001, secondly the credit limit states 1500£, with an APR of 27.9%, I cant prove it but the original credit limit was 950£ and the APR 15.9%, it only went up to 27.9% when I closed my current account at the Halifax and moved to Barclays around 2005/6, I remember that because at the time as I was annoyed to put it mildly - Just to add the credit card was with the Halifax. Idems letter keeps referring to LLoyds Banking Group are they linked to Halifax? The agreement also says bank charges were 12£, again I remember paying 35£ when one of my first payments was a few days late. Some pages of the agreement are blue, some white and all different fonts. Idem claim they own the debt, but terms in the agreement only state they can transfer the debt, but another clause in the terms says only We or You (meaning Halifax or me I assume) can enforce any part of the agreement. The agreement also state that interest will not be charged on defaulted accounts, however Halifax continued to apply interest when in the debt management plan and the account had been defaulted. Where the signature is supposed to be for me is blank, and the agreement contains no dates. Can anyone advise where I stand with this agreement. I can scan in later if it helps? It all just seems dodgy to me, and incorrect for the terms I remember. The debt is also 5481£ which is significantly higher than I recall ( I did bury my head in the sand for a few years, I had no money and no way of dealing with the debts, contributions were made through a dmp, it has been defaulted but the 6 years has now passed) The agreement just isn't correct from what I can see, but if anyone could advise further, it would be greatly appreciated? Chris -

hi guys i had an issue with a dca about four years ago which was halted by a cca requested helpfully obtained from this site the debt has been sold on to several other dca,s, who although i can head them off with further cca requests, they keep registering the debt on my credit file is there anything i can do to prevent this happening in future? cheers Mark

-

Hi, I sent out a CCA request to DLC, who were collecting for an old Egg debt; I have been paying £1 token payments to them every since the account defaulted over 6 years ago, and due to having moved house a couple of times since, have completely lost track of what has happened with this as the standing orders were set up to come out automatically. Last week I received a response to my request from DLC stating "we returned the account to Egg in July 2010, who have since ceased to trade. We assume that your account has been acquired by a third party company and we suggest you contact them". I have no idea who to contact about this now! Any advise as to what I should do next? If Egg have ceased to trade, then where has my £1 a month been going?!! Many thanks AM

Hi, I sent out a CCA request to DLC, who were collecting for an old Egg debt; I have been paying £1 token payments to them every since the account defaulted over 6 years ago, and due to having moved house a couple of times since, have completely lost track of what has happened with this as the standing orders were set up to come out automatically. Last week I received a response to my request from DLC stating "we returned the account to Egg in July 2010, who have since ceased to trade. We assume that your account has been acquired by a third party company and we suggest you contact them". I have no idea who to contact about this now! Any advise as to what I should do next? If Egg have ceased to trade, then where has my £1 a month been going?!! Many thanks AM -

Hi all, I recently CCAed all my creditors in order to try and sort out my finances finally. I have been paying £1 token payments to each, having defaulted on all over 6 years ago. I have moved house a few times since and have lost track of what has happened to them all. having sent a CCA request to Robinson Way, who I originally dealt with for a Halifax debt, I received a strange reply, returning my £1 PO, and saying that "the account is closed on our files, please contact our principal". This was written on a very unprofessional piece of paper that looked more like a memo than a letter! Has anyone got any advise as to how I should proceed with this? The 12+2 days are definitely over. As Robinson Way were dealing with this, is it still their responsibility to respond to my CCA request? Thanks AM

-

I paid them for a couple months via Monthly Standing Orders which i set up, this was after the Debt Management Company I used folded, I then stopped paying all of them recently ... I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them They are the only 1 from 5 to provide thus far, so tbh i still had a great result This is very true, i assumed info from a company like StepChange would be best i would get, not a mention or suggestion of doing CCA's came from them Sometimes their hands are tied to give certain aspects of advice and as I say CAG was a blessing in disguise when i read what people were saying about making CCA requests I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them, they are the only 1 from 5 to provide thus far, so tbh i have still had a great result ! Better late than never, very true

I paid them for a couple months via Monthly Standing Orders which i set up, this was after the Debt Management Company I used folded, I then stopped paying all of them recently ... I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them They are the only 1 from 5 to provide thus far, so tbh i still had a great result This is very true, i assumed info from a company like StepChange would be best i would get, not a mention or suggestion of doing CCA's came from them Sometimes their hands are tied to give certain aspects of advice and as I say CAG was a blessing in disguise when i read what people were saying about making CCA requests I have just received a true copy of my original CCA from Halifax, back dating to 2001, so will now need to sort a repayment offer with them, they are the only 1 from 5 to provide thus far, so tbh i have still had a great result ! Better late than never, very true -

Hi all, I started a previous thread to share my general issues, but am posting in this section for specific advise relating to First Direct. Previous forum address here if anyone is interested: http://www.consumeractiongroup.co.uk/forum/showthread.php?458839-Low-income-6-year-old-debts-and-worrying-about-the-possibility-of-future-court-action I had an account with an overdraft, credit card and loan with First Direct (all pre Apr 2007). I defaulted on payments for the credit card and loan back in 2009, at which point, they closed my account, merging the credit card and overdraft together as one debt, and the remaining loan as another. Since the default in 2009, I have been making token £1 monthly payments to Metropolitan Collection Services; I have since moved house a few times and hence had no contact with them. Aiming to sort things out once and for all, I joined this site, and under some much appreciated advice, sent out a CCA request to Metropolitan last week. First Direct have responded, sending back my CCA letter (but keeping the postal order???), saying: The letter is not signed (didn't think I needed to) - they want me to provide a specimen signature My current address does not match their records (it wouldn't as I have moved, but my credit file address is up-to-date) - they want me to provide the old address to match their records. From this, I gather that FD still own the debt as Metropolitan did not write to me. As mentioned, my credit file is up to date with all addresses. Does anyone have any advice on how I should proceed? Are they trying to delay and does the time limit of 12+2 days still apply? Or, are they valid in their requests? Any help much appreciated Thanks AM

-

Hi I would like to put a SAR in finding out what information my employers hold about me (I work for my local council). In particular interest are some emails which a colleague who left under a compromise agreement sent about me. My employer has email archives dating back ten years so I know they are still available but wasn't sure how to word the request to make sure that these are included. Any ideas Thanks

Hi I would like to put a SAR in finding out what information my employers hold about me (I work for my local council). In particular interest are some emails which a colleague who left under a compromise agreement sent about me. My employer has email archives dating back ten years so I know they are still available but wasn't sure how to word the request to make sure that these are included. Any ideas Thanks -

I am trying to get my finances in order and have been reading up on forums about those who have had successes dealing with DCAs, but unfortunately my accounts don’t seem to make sense. I have four default accounts on my credit file, showing a D sign every single month on my account, but I have three payments from DCA going out of my account two I know why I am paying but PRA I don’t know what its for, and the two bank account overdrafts I have defaults for I don’t know what is happening with them and what to do. Should i send out CCA letters to all creditors including barclays and natwest? On my credit file are these four defaulted accounts Lender Idem Capital Securities Current Balance £1,868 I am paying this via direct debit reduced monthly installment at the moment, this has been passed from Agilent to Moorgate and now to Idem and I it was so long ago now I cant even remember who the original company was who I took a loan out with. Lender NWB Current Accounts Current Balance £1,691 It says I am paying £5 per month but I cannot see any standing order or direct debit going out of my account for £5 per month, so I have no idea what is going on with this account. Both Barclays & Natwest overdrafts have been passed over to DCA I am sure of it, but I am unclear on who they are or what is going on with these accounts. What shall I do? Do I chase up with the actual banks to see what information they can pull up (send SARS) Lender Barclays Bank plc Current Balance £1,590 Similar to my Natwest account, I do not have anything on my bank account showing I am paying them, yet it shows I am paying £18 per month, once again I do not know how to handle this and whether I have a DCA I am paying, I haven’t received any letters for a while and I don’t have a clue what I should do. Lender MKDP LLP Account Type Credit Card Current Balance £264 Finally I have a PRA Group direct debit set up for £8.86 per month but yet again I don’t know what debt this is for now, as it seems to have been set up some time back, with moving and getting married last year I lost a lot of paper work and I cant remember what DCA is for what account and why now. DCA payments: Idem Robinsons Way this is on my credit file under MKDP (are they the same company?)But there is nothing on my credit file saying I am dealing with Robinsons Way PRA Group £8.86 No clue whatsoever why I am paying this and for what account.

I am trying to get my finances in order and have been reading up on forums about those who have had successes dealing with DCAs, but unfortunately my accounts don’t seem to make sense. I have four default accounts on my credit file, showing a D sign every single month on my account, but I have three payments from DCA going out of my account two I know why I am paying but PRA I don’t know what its for, and the two bank account overdrafts I have defaults for I don’t know what is happening with them and what to do. Should i send out CCA letters to all creditors including barclays and natwest? On my credit file are these four defaulted accounts Lender Idem Capital Securities Current Balance £1,868 I am paying this via direct debit reduced monthly installment at the moment, this has been passed from Agilent to Moorgate and now to Idem and I it was so long ago now I cant even remember who the original company was who I took a loan out with. Lender NWB Current Accounts Current Balance £1,691 It says I am paying £5 per month but I cannot see any standing order or direct debit going out of my account for £5 per month, so I have no idea what is going on with this account. Both Barclays & Natwest overdrafts have been passed over to DCA I am sure of it, but I am unclear on who they are or what is going on with these accounts. What shall I do? Do I chase up with the actual banks to see what information they can pull up (send SARS) Lender Barclays Bank plc Current Balance £1,590 Similar to my Natwest account, I do not have anything on my bank account showing I am paying them, yet it shows I am paying £18 per month, once again I do not know how to handle this and whether I have a DCA I am paying, I haven’t received any letters for a while and I don’t have a clue what I should do. Lender MKDP LLP Account Type Credit Card Current Balance £264 Finally I have a PRA Group direct debit set up for £8.86 per month but yet again I don’t know what debt this is for now, as it seems to have been set up some time back, with moving and getting married last year I lost a lot of paper work and I cant remember what DCA is for what account and why now. DCA payments: Idem Robinsons Way this is on my credit file under MKDP (are they the same company?)But there is nothing on my credit file saying I am dealing with Robinsons Way PRA Group £8.86 No clue whatsoever why I am paying this and for what account.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS