Showing results for tags 'fees'.

-

Hi I have been reading the following thread forum thread 353395 - Letter-to-send-if-you-are-being-charged-bank-fees-whilst-on-benefits (Will not allow link) and have been trying to locate the initial letter sent to the bank, before action However there is a link at the first comment at the top of the page yet it simply goes to the forums titles and no letter I wonder if anyone can help at all as i wanted to send to my bank to see if i could stop monthly overdraft fees occurring which because i seem to be in overdraft most of the time, i always receive at least £33 in fees every month from their £1 per day overdraft fee and is quite a chunk from my ESA payments i receive Any general advice will also be greatly appreciated Many thanks for your time Regards

Hi I have been reading the following thread forum thread 353395 - Letter-to-send-if-you-are-being-charged-bank-fees-whilst-on-benefits (Will not allow link) and have been trying to locate the initial letter sent to the bank, before action However there is a link at the first comment at the top of the page yet it simply goes to the forums titles and no letter I wonder if anyone can help at all as i wanted to send to my bank to see if i could stop monthly overdraft fees occurring which because i seem to be in overdraft most of the time, i always receive at least £33 in fees every month from their £1 per day overdraft fee and is quite a chunk from my ESA payments i receive Any general advice will also be greatly appreciated Many thanks for your time Regards -

Can pre-paid debit cards get you into debt for inactivity/dormancy fees? How much can they charge you?

-

Hi, Hope someone can help. For Ctax 2016/17. I have been charged two fees the £75 and the £235. I'm not sure the £235 is correct as it was added three days after I started making payments, and without any entry into my home for control of goods etc. In fact when it was applied there was no mention of control of goods. Could someone please clear up what the £235 charge should be for? - As it seems to have been added on incorrectly. I haven't spoken to the bailiff concerned yet as I wanted to check my facts before doing so.

Hi, Hope someone can help. For Ctax 2016/17. I have been charged two fees the £75 and the £235. I'm not sure the £235 is correct as it was added three days after I started making payments, and without any entry into my home for control of goods etc. In fact when it was applied there was no mention of control of goods. Could someone please clear up what the £235 charge should be for? - As it seems to have been added on incorrectly. I haven't spoken to the bailiff concerned yet as I wanted to check my facts before doing so. -

Hello, I posted on Saturday a letter to Santander reclaiming over 2 k of bank fees (template from this site) . It contained a paragraph in which you say what has happened - lot of death in my family and lost biz too. It was a very painful letter to write. (I kept it just a paragraph). Today they texted me they had been trying to call me and to call back. I hadn't answered since I am avoiding calls from anyone (not in a good place). I feel sick. Do I have to talk to them? I don't think I am strong enough to hold it together on a call (now my keyboard is wet). Kicking myself.

Hello, I posted on Saturday a letter to Santander reclaiming over 2 k of bank fees (template from this site) . It contained a paragraph in which you say what has happened - lot of death in my family and lost biz too. It was a very painful letter to write. (I kept it just a paragraph). Today they texted me they had been trying to call me and to call back. I hadn't answered since I am avoiding calls from anyone (not in a good place). I feel sick. Do I have to talk to them? I don't think I am strong enough to hold it together on a call (now my keyboard is wet). Kicking myself. -

Broadband providers drop cancellation fees for Armed Forces personnel READ MORE HERE: https://www.gov.uk/government/news/broadband-providers-drop-cancellation-fees-for-armed-forces-personnel

Broadband providers drop cancellation fees for Armed Forces personnel READ MORE HERE: https://www.gov.uk/government/news/broadband-providers-drop-cancellation-fees-for-armed-forces-personnel -

Just a brief overview.. I received a PCN from ES Parking Enforcement about 10 days ago. I attempted to make the payment a couple of days ago now, both by calling the number provided and on their website. It is saying that the number I have entered isn't recognised. They don't seem to make it easy to contact them, as they provide no email address (just an online form, which stated for business correspondence only. . and directs you elsewhere if you want to dispute the ticket - IAS? - but I don't want to appeal it I want the correct reference number!) I don't know how to go forward with this. I have no 'proof' I have attempted payment, so if it did go further it would be my word against theirs. I was thinking of writing a letter requesting the correct PCN reference number from them, but how much information should I include on this letter? Should I put my car registration number and date and time of issue, or just the original number they've issued me and let them deal with it. I know that sounds awkward, but they don't seem to make it easy for you, and the more I have read about them the more anxious I am getting about their response, as I don't imagine they'll still 'honour' the £60 'discounted' charge as by the time I've written to them and received a response it'll be outside the 14 days. Do I have a right to refuse to pay the 'full' amount of £100 based on the fact they have (presumably) written the wrong number on the ticket? Any advice would be greatly appreciated. Thanks

Just a brief overview.. I received a PCN from ES Parking Enforcement about 10 days ago. I attempted to make the payment a couple of days ago now, both by calling the number provided and on their website. It is saying that the number I have entered isn't recognised. They don't seem to make it easy to contact them, as they provide no email address (just an online form, which stated for business correspondence only. . and directs you elsewhere if you want to dispute the ticket - IAS? - but I don't want to appeal it I want the correct reference number!) I don't know how to go forward with this. I have no 'proof' I have attempted payment, so if it did go further it would be my word against theirs. I was thinking of writing a letter requesting the correct PCN reference number from them, but how much information should I include on this letter? Should I put my car registration number and date and time of issue, or just the original number they've issued me and let them deal with it. I know that sounds awkward, but they don't seem to make it easy for you, and the more I have read about them the more anxious I am getting about their response, as I don't imagine they'll still 'honour' the £60 'discounted' charge as by the time I've written to them and received a response it'll be outside the 14 days. Do I have a right to refuse to pay the 'full' amount of £100 based on the fact they have (presumably) written the wrong number on the ticket? Any advice would be greatly appreciated. Thanks -

Hi, I was repossessed by Kensington Mortgages in 2008, and the fee's and charges before and during this time were awful. Would it be too late for me to now try and reclaim these fee's as I now have very limited paperwork left? Thanks in advance for any advice.

-

Hoping someone can help. I was in a payment plan for paying council tax - missed one payment so the whole amount was due - I managed to pay it all off directly to the council. However, shortly after paying it off in full. I received a letter from the bailiffs warning about an enforcement visit and adding £75 to my outstanding amount (the total amount included £300 (the final payment of council tax). I logged into my council account and balance was £0 I assumed that there was a cross-over - I left a phone message with the bailiff explaining it had all been paid and also sent an email to the council and the enforcement company. Heard nothing more, until I returned home to find a letter from the bailiff demanding £75 + £235 for a visit = £310 in total. Can they do this? Are they allowed to add charges to their fees. At a push I would pay the £75, but the £235 seems silly as they were trying to collect a debt under an order that was already paid. The council have confirmed I owe them nothing and say the fees are a matter between me and the bailiff. What do I do??

Hoping someone can help. I was in a payment plan for paying council tax - missed one payment so the whole amount was due - I managed to pay it all off directly to the council. However, shortly after paying it off in full. I received a letter from the bailiffs warning about an enforcement visit and adding £75 to my outstanding amount (the total amount included £300 (the final payment of council tax). I logged into my council account and balance was £0 I assumed that there was a cross-over - I left a phone message with the bailiff explaining it had all been paid and also sent an email to the council and the enforcement company. Heard nothing more, until I returned home to find a letter from the bailiff demanding £75 + £235 for a visit = £310 in total. Can they do this? Are they allowed to add charges to their fees. At a push I would pay the £75, but the £235 seems silly as they were trying to collect a debt under an order that was already paid. The council have confirmed I owe them nothing and say the fees are a matter between me and the bailiff. What do I do?? -

Hello I am looking for some advice but couldn't work out how to create a new post? I joined a gymtec gym in May 2013 on a 12 month contract but became unwell late 2013, early 2014 I was diagnosed with Fibromyalgia I wrote to my gym cancelling my membership due to developing a disability and being unable to use the gym due to severe muscle pain, limited mobility and fatigue. I included a copy of my consultants letter confirming diagnosis and also informed the gym I was struggling financially due to divorce proceedings and now supporting myself and my step daughter on only my income. I heard nothing but cancelled my direct debit the following month in April 2014. I the recieved a letter in Jan from CRS on behalf of Harlands to say I owed £186 for unpaid membership fees and associated charges. I wrote to the gym stating I wanted to deal with them and explain I cancelled and why I did and included a copy of my original letter and the consultants letter. I've heard nothing and had another CRS letter threatening CCJ. I've emailed the gym again and stated clearly I had a material change in circumstances that prevented me from using the gym. What should I do next? Have CRS ever obtained a successful CCJ for gym membership? I can prove I am disabled and this condition developed and was diagnosed during the contract corresponding with my cancellation I can also prove I was struggling finacially at that point too due to the divorce. I was hoping to get some advice from Slick as he seems to be the guru on all things Harlands/gym related The threat of legal action feels very intimidating but can they really do anything? Thanks

Hello I am looking for some advice but couldn't work out how to create a new post? I joined a gymtec gym in May 2013 on a 12 month contract but became unwell late 2013, early 2014 I was diagnosed with Fibromyalgia I wrote to my gym cancelling my membership due to developing a disability and being unable to use the gym due to severe muscle pain, limited mobility and fatigue. I included a copy of my consultants letter confirming diagnosis and also informed the gym I was struggling financially due to divorce proceedings and now supporting myself and my step daughter on only my income. I heard nothing but cancelled my direct debit the following month in April 2014. I the recieved a letter in Jan from CRS on behalf of Harlands to say I owed £186 for unpaid membership fees and associated charges. I wrote to the gym stating I wanted to deal with them and explain I cancelled and why I did and included a copy of my original letter and the consultants letter. I've heard nothing and had another CRS letter threatening CCJ. I've emailed the gym again and stated clearly I had a material change in circumstances that prevented me from using the gym. What should I do next? Have CRS ever obtained a successful CCJ for gym membership? I can prove I am disabled and this condition developed and was diagnosed during the contract corresponding with my cancellation I can also prove I was struggling finacially at that point too due to the divorce. I was hoping to get some advice from Slick as he seems to be the guru on all things Harlands/gym related The threat of legal action feels very intimidating but can they really do anything? Thanks -

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) The Local Government Ombudsman's office has just released the following decision. Re: London Borough of Haringey. The complaint 1. The complainant, who I shall call Ms A, complains the Council allowed her to make payment towards an outstanding Penalty Charge Notice (PCN) although it had passed the matter to its enforcement agents (bailiffs), incurring additional costs. What I found 4 The Council issued Ms A a PCN for a parking contravention on 29 September 2015. Ms A did not pay or make formal representations against the PCN so the Council pursued the debt against her. It issued a warrant of execution and passed the debt to its bailiffs to enforce on 16 June 2016. 5. Ms A made a payment of £97 for the PCN using the Council’s online system on 23 June 2016. However by this point the Council had already passed the case to its bailiffs, incurring further costs. Ms A says she paid the fine so bailiff action should cease. However, the Council says she is still liable for the bailiff fees. Ms A says the Council should not have allowed her to make a payment online when the case was with its bailiffs. The Council confirmed it passed the debt onto the enforcement agency on 13 June because it had not received payment and sent a Notice of Enforcement on 16 June. 6. Ms A complained to the Council that she had not received the statutory notices the Council says it sent. The Council confirmed it sent the notices to the registered keepers address. These included the Notice to Owner, the Charge Certificate and the Order of Recovery. Each notice summarised the amount due at each stage. The Council said Royal Mail did not return the letters as undelivered so considered them served. The Council included copies of the notices it sent to Ms A in its response to her complaint. 7. A motorist may make part-payment towards a PCN debt and there was no reason for the Council to refuse Ms A’s payment made on 23 June 2016. Ms A sought to challenge the Council’s action but was unsuccessful, and the Council is therefore entitled to pursue the debt against her, including by passing the case to its bailiffs. Ms A made payment only after the case had been referred to bailiffs and the Ombudsman cannot therefore say she is not liable for the bailiff’s fees. The Council’s acceptance of Ms A’s payment has also not caused Ms A an injustice as it has been put towards the cost of the PCN and bailiff’s fees incurred to pursue it. http://www.lgo.org.uk/decisions/transport-and-highways/parking-and-other-penalties/16-008-073

The Local Government Ombudsman's office has just released the following decision. Re: London Borough of Haringey. The complaint 1. The complainant, who I shall call Ms A, complains the Council allowed her to make payment towards an outstanding Penalty Charge Notice (PCN) although it had passed the matter to its enforcement agents (bailiffs), incurring additional costs. What I found 4 The Council issued Ms A a PCN for a parking contravention on 29 September 2015. Ms A did not pay or make formal representations against the PCN so the Council pursued the debt against her. It issued a warrant of execution and passed the debt to its bailiffs to enforce on 16 June 2016. 5. Ms A made a payment of £97 for the PCN using the Council’s online system on 23 June 2016. However by this point the Council had already passed the case to its bailiffs, incurring further costs. Ms A says she paid the fine so bailiff action should cease. However, the Council says she is still liable for the bailiff fees. Ms A says the Council should not have allowed her to make a payment online when the case was with its bailiffs. The Council confirmed it passed the debt onto the enforcement agency on 13 June because it had not received payment and sent a Notice of Enforcement on 16 June. 6. Ms A complained to the Council that she had not received the statutory notices the Council says it sent. The Council confirmed it sent the notices to the registered keepers address. These included the Notice to Owner, the Charge Certificate and the Order of Recovery. Each notice summarised the amount due at each stage. The Council said Royal Mail did not return the letters as undelivered so considered them served. The Council included copies of the notices it sent to Ms A in its response to her complaint. 7. A motorist may make part-payment towards a PCN debt and there was no reason for the Council to refuse Ms A’s payment made on 23 June 2016. Ms A sought to challenge the Council’s action but was unsuccessful, and the Council is therefore entitled to pursue the debt against her, including by passing the case to its bailiffs. Ms A made payment only after the case had been referred to bailiffs and the Ombudsman cannot therefore say she is not liable for the bailiff’s fees. The Council’s acceptance of Ms A’s payment has also not caused Ms A an injustice as it has been put towards the cost of the PCN and bailiff’s fees incurred to pursue it. http://www.lgo.org.uk/decisions/transport-and-highways/parking-and-other-penalties/16-008-073 -

very long story which I will add later today, if possible, but your question of {did you make offers to the creditor before ccj } made me think because I made the offer which they refused,and yet when we went to court they accepted the exact amount! http://www.consumeractiongroup.co.uk/forum/showthread.php?398804-Help-with-a-judgement-and-visit-from-HCEO-**Partial-Refund-Obtained** but I am not a business, just a pensioner who has now fees which like yours, didn't apply , I have now paid all but 200 which they say I still owe, did it cost you much and how did you go about taking them to court, As I am new on here I dont know how far I can go asking personal questions , but I know ,{ I am not being arrogant} that the original debt was just so flawed , and I cant seem to find out how to go about proving it, I am not disputing the money owed on the debt , but the lies which were behind it, and it need not have gone this far paying all the HCEO fees, As I said I dont know how far to go on here, with company names etc, I would like to copy and paste the costs etc , but is this allowed, because then I can explain a bit more in detail what happened? Long story , had delivery of oil which I HAD NOT ordered which was £739 , it was signed for by my partner who just thought I had ordered it, I asked them to come take back on same day, they refused and said I had signed up to their top up service, which I had not, as always paid for my oil when I had saved enough money, I couldnt afford to pay all that at once and save weekly for my oil as well, I made them 2 offers, which they refused, next thing I knew was an HCEO was at my door, with a writ I explained I didnt know anything about the court proceedings, and was just waiting for the claimant to get back to me again to see if we could come to an agreement, they had gone to the High Court which was around 200 miles form me, I had to ask him for it to be set aside, he did an inventory and went away. The original court case was 27 1 2011 and I wasn't aware until 7th june 2011 . , The reason for me posting is the fees are very high, having read some of the comments on here, are not right, and they are still chasing me for more, and keep stating about 2004 regulations . I have got an email with court papers and fees, and also a breakdown of fees, which are a joke, even more of a joke is the fact that my monthly payment which I have paid to the court is the exact amount I offered the claimant and was refused out of court on a debt and judgement of 795 with the court costs, I have now paid 65 payments of 35 .00 and DARE NOT cancel it as they told me in an email they will enforce again, For the last 3 weeks I have nearly drove myself crazy trying to find out what I can do to claim these fees back, I dont have a problem about paying the oil debt, but I do have a problem with their under hand way they have gone about it and now I am owing money to my friends who have been helping me pay this, I would be really grateful for any advice, thank you x

very long story which I will add later today, if possible, but your question of {did you make offers to the creditor before ccj } made me think because I made the offer which they refused,and yet when we went to court they accepted the exact amount! http://www.consumeractiongroup.co.uk/forum/showthread.php?398804-Help-with-a-judgement-and-visit-from-HCEO-**Partial-Refund-Obtained** but I am not a business, just a pensioner who has now fees which like yours, didn't apply , I have now paid all but 200 which they say I still owe, did it cost you much and how did you go about taking them to court, As I am new on here I dont know how far I can go asking personal questions , but I know ,{ I am not being arrogant} that the original debt was just so flawed , and I cant seem to find out how to go about proving it, I am not disputing the money owed on the debt , but the lies which were behind it, and it need not have gone this far paying all the HCEO fees, As I said I dont know how far to go on here, with company names etc, I would like to copy and paste the costs etc , but is this allowed, because then I can explain a bit more in detail what happened? Long story , had delivery of oil which I HAD NOT ordered which was £739 , it was signed for by my partner who just thought I had ordered it, I asked them to come take back on same day, they refused and said I had signed up to their top up service, which I had not, as always paid for my oil when I had saved enough money, I couldnt afford to pay all that at once and save weekly for my oil as well, I made them 2 offers, which they refused, next thing I knew was an HCEO was at my door, with a writ I explained I didnt know anything about the court proceedings, and was just waiting for the claimant to get back to me again to see if we could come to an agreement, they had gone to the High Court which was around 200 miles form me, I had to ask him for it to be set aside, he did an inventory and went away. The original court case was 27 1 2011 and I wasn't aware until 7th june 2011 . , The reason for me posting is the fees are very high, having read some of the comments on here, are not right, and they are still chasing me for more, and keep stating about 2004 regulations . I have got an email with court papers and fees, and also a breakdown of fees, which are a joke, even more of a joke is the fact that my monthly payment which I have paid to the court is the exact amount I offered the claimant and was refused out of court on a debt and judgement of 795 with the court costs, I have now paid 65 payments of 35 .00 and DARE NOT cancel it as they told me in an email they will enforce again, For the last 3 weeks I have nearly drove myself crazy trying to find out what I can do to claim these fees back, I dont have a problem about paying the oil debt, but I do have a problem with their under hand way they have gone about it and now I am owing money to my friends who have been helping me pay this, I would be really grateful for any advice, thank you x -

Propsed fees for failure to notify a change of circumstances to a Local Authorities (LA) in regards to Council tax and possibly Housing benefit too! My local LA (Southend on sea Borough Council) SBC)) has recently had a full Council meeting and are propsing charging people for failing to notify a change of circumstances. This could be between £70-£280! (please see my attacments (1) (2). 2 for the quick version and 1 for the full document. Or see section 6 page 67 all... This was previously just £50 now the new rates could cause more financial issues for many people. 2 RECOMMENDATIONS 2.1 That the Executive agree that consultation takes place on the implementation of a fixed penalty of £70 to Council tax charge payers, permitted under the provisions of the Local Government Finance Act 1992, who intentionally or knowingly fail to notify the Council of any change affecting Council Tax Liability or Local Council Tax Benefit Scheme (LCTBS) without reasonable excuse. 3 REASONS FOR RECOMMENDATIONS 3.1 The Council has powers under the Local Government Finance Act 1992 (Schedule 3) to impose civil penalties to those charge payers who wilfully neglect to inform the Council of changes which affect their Council Tax liability. There are at least 6 areas that could affect the claimant/bill payer this could be on top of what DWP already charge. It could pay to ask your LA if they also intend on doing the same as mine. Given that most LAs now have to find new inovative ways to get more money in their coffers then this one surely is a way to make money from failure to notiy a change of circumstances in a reasonable time frame (normally 28 days) sometimes less.... Info here and other places >> https://www.gov.uk/civil-penalty-changes-affect-benefits Your thoughts.... Benefit failure fees.pdf Public reports pack 14th-Feb-2017 14.00 Cabinet[556].pdf

-

Hi All I have opened a claim for refund of Additions account fee's and have received a questionnaire to complete; which I would like some advice on how best to proceed. Here are some background details first: I first became aware of Package Bank Accounts last year when a colleague at work told me that he had reclaimed some money. I was shocked; having only ever banked with barclays for the last 24years I genuinely thought that I had to pay for my bank account and that the insurances etc. were free perks. I decided to pursue a claim myself; I only have statements from 2011 I did an SAR request on the internet in around May last year. After 45 days I had not heard or received anything I rang the number given on Barclays site; the telephone banking agent gave me a number to ring for the SAR team. I rang the number several times but it was a dud number. Made an appointment at the Bank, spoke to an advisor who gave me an SAR request form to fill in; I filled this in and sent it recorded delivery with my cheque for £10. They received the form but again after 45 Days nothing. At this point I gave up. In December I recieved the letter from Barclays saying Additions was being removed and offering the Fee Free Account; In January I went to the bank and cancelled the Tech and Travel pack. This spurred me to look at claiming again. I read on the internet that even with an SAR they only go back 6 Years; so I thought well I won't gain much from it anyway. Is this true that they only go back 6 years? this is what I know: I opened my current account with Barclays in March 1993 at the age of 21; this was my first current account and to this day is the only current account I have ever held. Through research I found that the Additions account wasn't introduced until 1996 I must initially have had a fee free account? I do not recall ever agreeing to the Additions account; I do not recall agreeing to iot being upgraded to Additions Plus. I do not recall agreeing to the cost of the account being hiked up over the years. As long as I can remember I have paid a fee; I definitely remember it being £6.50 a long long time ago it may have even been £5.00 but not sure of this. I remember it being Additions then Additions Plus; before I opted for the Fee Free account without the Tech or Travel pack in Jan this year the fee was £16.00. Over the years the fee increased; I rember it being £13.50 at one point. I think I may have had it from the beginning before Breakdown cover was included; I know I had CPP card protection and I have a vague recollection of having a tag to go on your keys incase you lost them? I suspect that my account was upgraded to Additions from my original fee free account without my knowledge. Initially I did not have an overdraft with the account; I asked for one at some point many years after I had opened the account somewhere between 2000-2005. I only asked for a small overdraft for emergencies only and it was only a small one I would have only wanted £100 and probably wouldn't have used it in the beginning. Maybe I was conned into having additions at this point; but I am sure I already had it. Regarding the insurances; I have only ever used the Breakdown cover and only once bcause I thought it was a free benefit to an account I had to pay for anyway. I have never had any expensive gadgets or a mobile worth insuring I have never used gadget insurance. I only holiday in the UK and would never use travel insurance. Over the latter years I have used my overdraft but again only because I thought it was a free perk to an account I had to pay for. If I had had a fee free account I would have managed my money differently and could have done without the overdraft. On January the 24th I this to file a claim: Packaged Bank Account Claim: Barclays Sort code or branch name: xx-xx-xx Existing complaint reference: N/A xxxxxxxxxxx I am writing to you as I believe the packaged bank account which I have had since some time after March 25th, 1993 was mis-sold/inappropriate for me. This is because... - I don’t remember ever agreeing to having this account. - I was upgraded without my knowledge Additional information: - The addressess that I have lived at whilst holding the packaged bank account are: xxxxxxxxxxxx I have no recollection of ever having opened a package bank account. I started banking with Barclays on 25/03/1993 when I opened a current account; I think that the reason for opening the account was that I needed an account to have my wages paid into. You are the only bank that I have ever banked with and this is the only current account that I ever held. At some point it seems, my current account became a packaged bank account but I do not remember ever agreeing to this; I remember along time ago on my statements paying a £6.50 account fee which has been risen over the years to £16.00 without my consent! I thought that this account fee on my statements was exactly what it stated; a fee for my account that I had to pay to have a current account; I did not know that the fee was for the additional benefits such as travel insurance, breakdown cover etc.. I thought that these came FREE with the account and that the account fee was for the account itself and NOT to pay for these benefits; which I never requested anyway. Upon receipt of your recent letter informing me that Additions is being removed and giving me the option of removing the benefits; I have cancelled the tech and travel packs and now have a fee free account whilst retaining my overdaft facility which is all I have ever required from my bank account. [removed template details - dx] Today I recieved a reply and a questionnaire to fill in. After researching on this site; I think that my strongest complaint is that Additions was applied to my account without my knowledge or approval rather than it being mis-sold. I think that this is reflected in my Complaint letter above. Reading the questionnaire: Section A asks for details of my Package Account. Section B asks - Am I complaining about the sale of the account. - If NO go straight to Section F Selecting NO here skips all of the questions in the questionnaire and takes me to Section F - any additional information Section G - Your declaration. End of Questionnaire. Should I select 'NO' in Section B and skip all the questions. Can anyone advise what additional Information I can give? Also If the question is asked of when I became aware that I could have a fee free account and could make a complaint; should I say December 2016 when I received the letter which is simpler ( But will they be suspiciouse of my earlier SAR requests and visit to the bank regarding them). Or should I be honest and say that I heard through a colleague early in 2016 ( They may ask why it took me so long to switch to a fee free account and to make a complaint - which was because I was waiting for my two SAR requests). Any advice on how to proceed with my claim will be gratefully accepted; I will keep an eye on my thread, respond to any replies and update my progress. If I am succesfull I will make a donation to the the forum in thanks. Thankyou in advance. Alice

-

Hi All Just got my SAR back from MBNA. CC taken out 1998. Defaulted 2003. Informed no CCA which is good to know as DCA chasing and have been cca,d. My question is the statments show payment protection insurance as well as penalty fees for late payments and over limit. Is it too late to claim these back? Many thanks

-

Hi everyone, I'm looking for some advice on some fees I was charged in relation to a cosmetic surgery consultation I had back in 2016. At the time I was considering having some cosmetic surgery, so was looking to arrange a few consultations with different surgeons to make sure I was making the correct choices on procedure and when choosing the actual surgeon. I tried to get in touch with one of the practices in question to enquire about a consultation - firstly on the number listed on the surgeons website and then as I couldn't get through on this line, I contacted the private hospital in London where the said surgeon runs his practice - I got through on this number. When speaking to the person at the private hospital I enquired about waiting times and how much this doctor actually charges for a consultation (I had a limited budget for consultations). I was informed of the available dates and I was explicitly told that there would be no charge for the initial consultation - this is nothing out of the ordinary as many cosmetic surgeons offer a free initial consultation. I went ahead and booked a consultation. I then received the booking confirmation through email, again with no mention of any fees. I attended the consultation with the doctor where everything was OK, a very brief consultation compared with some others but I wasn't too concerned as I thought this was a no charge consultation. Again no mention of any cost or taking any payment before, during or immediately after the consultation (the surgeon just said if I was to go with him, we would need to have a second more in depth consultation before surgery) - It's worth noting that I did attend 2 other consultations which we're chargeable, however this was made explicitly clear at the time of booking, and payment was also taken at the point of booking - otherwise the booking would not be made. To my surprise a couple of days later an invoice drops through the post for £215. I contacted the surgeons practice to discuss this and explain the situation, however his practice manager just said I'd been informed wrongly by the private hospital employee, and even though I'd had confirmation and they acknowledged that I was mis-informed, that it wasn't their issue. Which I obviously didn't agree with. I then had a couple of invoice reminders come through the door I got back in touch again to try and resolve the matter. I was then given the contact details of one of the managers of the private hospital and told to try and sort it out with them. Before I'd had chance to resolve this (this was over Christmas so I wasn't able to get hold of said person) I've had a letter through the door from a debt collection services company requesting the money. Now I know these have no legal power as such, but I'd rather nip this in the bud before it goes any further. Am I correct to believe that any charges need to be made clear before a service is provided? Particularly as I explicitly asked before I made the booking if there was any charge (there is also no mention of fees on the surgeons website). If I'd known this consultation was chargeable I wouldn't have gone ahead as the surgeon in question was not my top or second choice. I don't feel like I should have to pay as a result of being provided the wrong information by the hospital. Any thoughts on this? Thanks for the help.

Hi everyone, I'm looking for some advice on some fees I was charged in relation to a cosmetic surgery consultation I had back in 2016. At the time I was considering having some cosmetic surgery, so was looking to arrange a few consultations with different surgeons to make sure I was making the correct choices on procedure and when choosing the actual surgeon. I tried to get in touch with one of the practices in question to enquire about a consultation - firstly on the number listed on the surgeons website and then as I couldn't get through on this line, I contacted the private hospital in London where the said surgeon runs his practice - I got through on this number. When speaking to the person at the private hospital I enquired about waiting times and how much this doctor actually charges for a consultation (I had a limited budget for consultations). I was informed of the available dates and I was explicitly told that there would be no charge for the initial consultation - this is nothing out of the ordinary as many cosmetic surgeons offer a free initial consultation. I went ahead and booked a consultation. I then received the booking confirmation through email, again with no mention of any fees. I attended the consultation with the doctor where everything was OK, a very brief consultation compared with some others but I wasn't too concerned as I thought this was a no charge consultation. Again no mention of any cost or taking any payment before, during or immediately after the consultation (the surgeon just said if I was to go with him, we would need to have a second more in depth consultation before surgery) - It's worth noting that I did attend 2 other consultations which we're chargeable, however this was made explicitly clear at the time of booking, and payment was also taken at the point of booking - otherwise the booking would not be made. To my surprise a couple of days later an invoice drops through the post for £215. I contacted the surgeons practice to discuss this and explain the situation, however his practice manager just said I'd been informed wrongly by the private hospital employee, and even though I'd had confirmation and they acknowledged that I was mis-informed, that it wasn't their issue. Which I obviously didn't agree with. I then had a couple of invoice reminders come through the door I got back in touch again to try and resolve the matter. I was then given the contact details of one of the managers of the private hospital and told to try and sort it out with them. Before I'd had chance to resolve this (this was over Christmas so I wasn't able to get hold of said person) I've had a letter through the door from a debt collection services company requesting the money. Now I know these have no legal power as such, but I'd rather nip this in the bud before it goes any further. Am I correct to believe that any charges need to be made clear before a service is provided? Particularly as I explicitly asked before I made the booking if there was any charge (there is also no mention of fees on the surgeons website). If I'd known this consultation was chargeable I wouldn't have gone ahead as the surgeon in question was not my top or second choice. I don't feel like I should have to pay as a result of being provided the wrong information by the hospital. Any thoughts on this? Thanks for the help. -

Good morning, My 18 yr old daughter took out a policy with 'MyPolicy' car insurance 8 months ago when she passed her test. They seemed the best price at the time but have cost dearly over the 8months, mainly in charges for extra miles. a few weeks ago she was involved in an accident which wasn't her fault, the other driver admitted blame immediately. The claim has been settled and they have sent the cheque. Now, the problem is the charges they want to slap on her. Her car was a write off so she is going to buy her brother's car. They want to charge her £150 for a new black box and £100 to change the details on the policy to the new car. This sounds totally unreasonable to me and is a loss on her part seeing as the accident wasn't her fault. Baring in mind the black box only cost £50 to fit when she first took out the policy. She's young and inexperienced and doesn't know what to say on the phone. Last time I tried, they wouldn't speak to me, but surely if she gives her permission that should be fine? I need to fight her corner for her as I can be stronger on the phone. I need some advice as this charging can't be right. It's a total rip off to me. Any advice would be greatly appreciated.

Good morning, My 18 yr old daughter took out a policy with 'MyPolicy' car insurance 8 months ago when she passed her test. They seemed the best price at the time but have cost dearly over the 8months, mainly in charges for extra miles. a few weeks ago she was involved in an accident which wasn't her fault, the other driver admitted blame immediately. The claim has been settled and they have sent the cheque. Now, the problem is the charges they want to slap on her. Her car was a write off so she is going to buy her brother's car. They want to charge her £150 for a new black box and £100 to change the details on the policy to the new car. This sounds totally unreasonable to me and is a loss on her part seeing as the accident wasn't her fault. Baring in mind the black box only cost £50 to fit when she first took out the policy. She's young and inexperienced and doesn't know what to say on the phone. Last time I tried, they wouldn't speak to me, but surely if she gives her permission that should be fine? I need to fight her corner for her as I can be stronger on the phone. I need some advice as this charging can't be right. It's a total rip off to me. Any advice would be greatly appreciated. -

Millions of people who have basic bank accounts may be paying higher fees than necessary.. Basic bank accounts are designed for people who do not already have a bank account and are ineligible for a standard current account .While eight million people have basic accounts, around half of them are still liable to pay fees for failed payments. Completely fee-free basic accounts have been available since January 2016, following an industry agreement. Vulnerable customers who have such accounts are not charged for failed payments, or for going overdrawn. The Treasury figures show that 3.7 million people have accounts that do not conform to the agreement, struck between the government and the banking industry, in 2014. Of those, 3.6 million bank with Lloyds, the rest being RBS customers All the other seven big High Street banks do not charge fees for basic account customers http://www.bbc.co.uk/news/business-38289654

-

My daughter's nursery has asked for payment of arrears which is considerably large, i.e. greater than £1000. However, they have sent a hand written letter without a date setting out a payment plan (without consulting with me or my soon to be ex). They further state that if the payments are not made on the dates stated, they will apply am additional charge. I've read through similar threads and understand that the additional charges cannot be applied unless I have signed an agreement that mentions additional charges. Strangely, they have also given me a blank agreement and registration form for the nursery requesting that I fill it in so that they can "update their records". This was given to me along with the letter regarding fees. I am willing to pay the outstanding amount in reasonable installments based upon my total monthly outgoings, but I am planning to write to them regarding the additional charges. I also plan to write to them asking for a copy of the original agreement and T&C's that I may have signed at the start. WIll they be able to take me to court for this if there is no agreement signed? Thank you for any replies!

-

Hi guys. Simply put. Parking fine - £82 Forgot to pay it. Went to a Debt Collector, who added their £75 on top. As soon as I got the letter and remembered the debt, I paid Stockport Council via their website The £82. I have an email proving so. This was October 3rd Just had a letter placed through the door tonight for.... The original debt £82 Compliance fee £75 1st visit £235 Total: £392. Am I missing something here? Clearly a lack of comms between the council and the bailiff. According to the law, do I have to pay the bailiffs' fees for a debt I paid 2 months ago? Thank you so much in advance

Hi guys. Simply put. Parking fine - £82 Forgot to pay it. Went to a Debt Collector, who added their £75 on top. As soon as I got the letter and remembered the debt, I paid Stockport Council via their website The £82. I have an email proving so. This was October 3rd Just had a letter placed through the door tonight for.... The original debt £82 Compliance fee £75 1st visit £235 Total: £392. Am I missing something here? Clearly a lack of comms between the council and the bailiff. According to the law, do I have to pay the bailiffs' fees for a debt I paid 2 months ago? Thank you so much in advance -

Lettings agents in England will be banned from charging fees to tenants "as soon as possible" under plans announced in the Autumn Statement. Tenants can be charged fees for a range of administration, including reference, credit and immigration checks. Chancellor Philip Hammond said shifting the cost to landlords will save 4.3 million households hundreds of pounds. The move could spur competition as landlords, unlike tenants, can shop around for the cheapest agent. In Scotland, lettings agency fees to tenants have already been banned. In England and Wales since last year, lettings and managing agents have been legally obliged to clearly publicise their fees. Fees vary widely, with costs in some big cities much higher than elsewhere. Tenants face charges when agents draw up tenancy agreements along with the possibility of a non-refundable holding deposit paid before signing up to the deal. http://www.bbc.co.uk/news/business-38065249

Lettings agents in England will be banned from charging fees to tenants "as soon as possible" under plans announced in the Autumn Statement. Tenants can be charged fees for a range of administration, including reference, credit and immigration checks. Chancellor Philip Hammond said shifting the cost to landlords will save 4.3 million households hundreds of pounds. The move could spur competition as landlords, unlike tenants, can shop around for the cheapest agent. In Scotland, lettings agency fees to tenants have already been banned. In England and Wales since last year, lettings and managing agents have been legally obliged to clearly publicise their fees. Fees vary widely, with costs in some big cities much higher than elsewhere. Tenants face charges when agents draw up tenancy agreements along with the possibility of a non-refundable holding deposit paid before signing up to the deal. http://www.bbc.co.uk/news/business-38065249 -

Hi being threatened with court action from holiday company, the holiday was booked with a deposit and then 2 payments were due to be taken from card, The 1st payment that was due I asked for a extension of 10 days as my mother was ill in hospital, ( I am a self employed taxi driver) they agreed so all was fine, then sadly my mother passed away and the holiday was just forgotten about. Started getting emails saying payment had failed and they would have to cancel the holiday, I really did not care at that time, received an email saying Cancellation charges, and they were the same as the holiday, Now I expected easy jets flight costs were probably due but they have asked for payment for the hotel and transfers etc ATOL protection and transaction fees. I returned the email and asked them to provide receipts for the so called payments for the transfers, hotel etc and they just ignored me, today I have received a letter threatening court action and I dont really know where I stand and what to do Any help would be gratefully appreciated

-

My husband recently engaged The Claims Guys to do a free PPI check for him (much to my horror) and surprise, surprise, they are now demanding payment of over £2000 for the first compensation pay-out (30% plus VAT). I object strongly to paying these jokers anything at all, but despite interrogating my husband, I can't seem to work out how they got from free check to binding contract. I believe he only signed letters of authority for 2 companies (he can't remember which ones) but we have already been contacted by 3 companies so I really don't know what is going on. Is there any way we can get the contract cancelled? Is it worth me trying to fight it? (On the grounds that they did not make it clear to my husband that he could do it himself or that he signed it under duress) Is there anything at all I can do, or do we just have to pay up and find some way of keeping my husband away from all paperwork in future? (For what it's worth, my husband is quite a successful professional - he is just hopeless at admin and anything financial...)

My husband recently engaged The Claims Guys to do a free PPI check for him (much to my horror) and surprise, surprise, they are now demanding payment of over £2000 for the first compensation pay-out (30% plus VAT). I object strongly to paying these jokers anything at all, but despite interrogating my husband, I can't seem to work out how they got from free check to binding contract. I believe he only signed letters of authority for 2 companies (he can't remember which ones) but we have already been contacted by 3 companies so I really don't know what is going on. Is there any way we can get the contract cancelled? Is it worth me trying to fight it? (On the grounds that they did not make it clear to my husband that he could do it himself or that he signed it under duress) Is there anything at all I can do, or do we just have to pay up and find some way of keeping my husband away from all paperwork in future? (For what it's worth, my husband is quite a successful professional - he is just hopeless at admin and anything financial...) -

Hi, I was hoping to possibly get some advice. My kids where at a private school (fees paid till the end of the school year). Then this happens.. . http://www.shernoldschool.co.uk/118972__1.pdf and http://www.kentonline.co.uk/maidstone/news/shernold-school-inadequate-staff-checks-97172/ at which point we withdrew the kids from the school and moved them elsewhere. We have told the school that we where not happy (so have others) and we would not be paying the notice period (although the bill they have sent us appears to only be for half of the term Fast forward a few months of email exchanges to yesterday, we receive a letter from Redwood Collections looking to collect the outstanding amount. Its there typical "We are instructed to take all necessary steps to recover the sum shown, including legal action if required". Some (hopefully) useful points: 1. The school fees where paid in full till the end of the school year 2. My eldest son has moderate aspergers syndrome and ADHD (we have letters proving it and the school where aware of this) he also had major heart surgery in March of this year 3. My sons care team had tried to work with the school with regards to what is the best outcome for my eldest sons education. They weren't interested (can prove this as well). 4. All things said done we where going to move them regardless due to having (documented) concerns for a while. Whats the best way forward with this? Thanks in advance! P.S. Sorry to work around the "To be able to post links or images your post count must be 10 or greater. You currently have 0 posts." message, but I think the links are important to what is going on here.

Hi, I was hoping to possibly get some advice. My kids where at a private school (fees paid till the end of the school year). Then this happens.. . http://www.shernoldschool.co.uk/118972__1.pdf and http://www.kentonline.co.uk/maidstone/news/shernold-school-inadequate-staff-checks-97172/ at which point we withdrew the kids from the school and moved them elsewhere. We have told the school that we where not happy (so have others) and we would not be paying the notice period (although the bill they have sent us appears to only be for half of the term Fast forward a few months of email exchanges to yesterday, we receive a letter from Redwood Collections looking to collect the outstanding amount. Its there typical "We are instructed to take all necessary steps to recover the sum shown, including legal action if required". Some (hopefully) useful points: 1. The school fees where paid in full till the end of the school year 2. My eldest son has moderate aspergers syndrome and ADHD (we have letters proving it and the school where aware of this) he also had major heart surgery in March of this year 3. My sons care team had tried to work with the school with regards to what is the best outcome for my eldest sons education. They weren't interested (can prove this as well). 4. All things said done we where going to move them regardless due to having (documented) concerns for a while. Whats the best way forward with this? Thanks in advance! P.S. Sorry to work around the "To be able to post links or images your post count must be 10 or greater. You currently have 0 posts." message, but I think the links are important to what is going on here. -

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance -

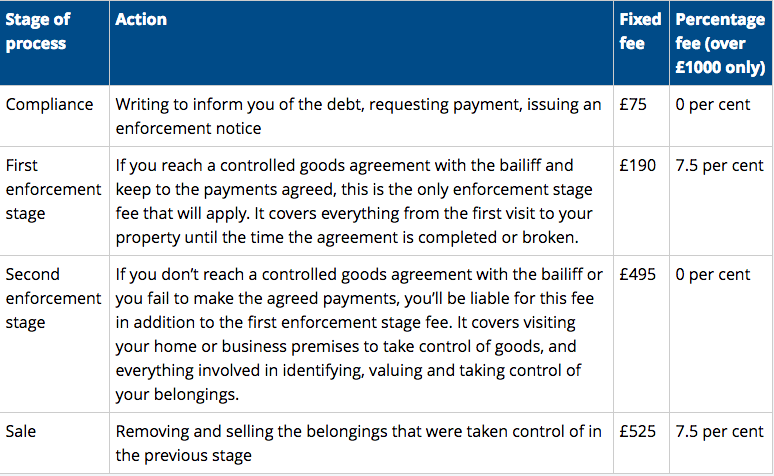

Hi all, I would really appreciate some advice. My business partner and I run a small business, and cashflow is very delicate. Some time ago we got in some money trouble and an invoice was sold to a debt recovery company. We managed to pay it off (or so we thought), but unfortunately my business partner is a bit scatternbrained with numbers, and paid the incorrect amount. The total outstanding debt was £5,723.96. My business partner sent them a transfer of £5,700, accidentally leaving off the £23.96. My business partner had some fees he wanted to dispute - The debt recovery company then sent a follow up email saying all prior fees are legitimate, and that "I have checked your account and can see we are still awaiting a payment of £23.96. I am assured this will be paid in due course, and this case can then be closed.". My business partner forgot to respond to the email (stupid, I know), and three weeks later (yesterday) they send a hired thug to our place of business, while customers were there, demanding the £23.96 plus a £1111.87 enforcement charge. He said that unless we paid that to him on the spot, he would confiscate goods that he valued to the sum of £8000. The £5,723.96 sum had a high court writ, which comes with a cap on fees of this nature that can be charged, as illustrated by the table below: The bailiff claimed to be able to charge for both stage two and three whether or not he actually had to carry out stage three. I pointed out that I was perfectly willing to pay the debt and the enforcement fee on the spot, which meant that he did not have the right to charge a "sale" enforcement fee, but he refused to drop it, saying I either pay exactly what he is demanding, or he starts ripping equipment out of the walls there and then. I had no choice but to pay the entire sum, and did so. There is no doubt in my mind that this is illegal and extortion, and in fact the bailiff himself used the very word "extortionate" when explaining the situation he was putting us in. My question to you is which regulatory body can I bring this to the attention of, are there any court cases setting a precedent in these situations, and are there guidelines that prevent bailiffs from charging huge bills for debts as low as £23? Even the £495 bill is entirely unfair, and clearly taking advantage of an admin error made by a small business. The law was not written to allow them to do this, and it puts our business at risk. Any advice on putting this right would be massively appreciated. Thanks a lot.

Hi all, I would really appreciate some advice. My business partner and I run a small business, and cashflow is very delicate. Some time ago we got in some money trouble and an invoice was sold to a debt recovery company. We managed to pay it off (or so we thought), but unfortunately my business partner is a bit scatternbrained with numbers, and paid the incorrect amount. The total outstanding debt was £5,723.96. My business partner sent them a transfer of £5,700, accidentally leaving off the £23.96. My business partner had some fees he wanted to dispute - The debt recovery company then sent a follow up email saying all prior fees are legitimate, and that "I have checked your account and can see we are still awaiting a payment of £23.96. I am assured this will be paid in due course, and this case can then be closed.". My business partner forgot to respond to the email (stupid, I know), and three weeks later (yesterday) they send a hired thug to our place of business, while customers were there, demanding the £23.96 plus a £1111.87 enforcement charge. He said that unless we paid that to him on the spot, he would confiscate goods that he valued to the sum of £8000. The £5,723.96 sum had a high court writ, which comes with a cap on fees of this nature that can be charged, as illustrated by the table below: The bailiff claimed to be able to charge for both stage two and three whether or not he actually had to carry out stage three. I pointed out that I was perfectly willing to pay the debt and the enforcement fee on the spot, which meant that he did not have the right to charge a "sale" enforcement fee, but he refused to drop it, saying I either pay exactly what he is demanding, or he starts ripping equipment out of the walls there and then. I had no choice but to pay the entire sum, and did so. There is no doubt in my mind that this is illegal and extortion, and in fact the bailiff himself used the very word "extortionate" when explaining the situation he was putting us in. My question to you is which regulatory body can I bring this to the attention of, are there any court cases setting a precedent in these situations, and are there guidelines that prevent bailiffs from charging huge bills for debts as low as £23? Even the £495 bill is entirely unfair, and clearly taking advantage of an admin error made by a small business. The law was not written to allow them to do this, and it puts our business at risk. Any advice on putting this right would be massively appreciated. Thanks a lot.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS