Showing results for tags 'dlc'.

-

i need some advice, first a bit of background this may be long I had a loan with black horse june 2006, i kept up repayments for awhile but started to struggle after i was made redundant and in august 2007 they got a ccj against me. i agreed to pay £30 a month and did so for 15 months. Then my partner was made redundant who was the main wage earner and i could no longer afford the £30, i had the order changed to £1 a month and i paid that until sept 2011 when i recieved a letter from a company called hillesden securities saying they were the new owners of the debt and i should start paying them. i wrote to both hillesden and black horse. i didnt hear anything from black horse directly but i recieved a reply from hillesden with a black horse letter attatched to theirs saying hillesden had purchased the account. i wrote to hillesden to tell them i wouldnt be making payments until i was notified by the court or black horse direct. i didnt hear anymore and forgot all about it to be honest. oct 2012 we recieved a annual statement of account from dlc (direct legal & collections) i wrote to them asking who they were and recieved a reply saying they were acting on behalf of hillesden securities to which i replied with a letter saying i didnt have an account with hillesden and asked for further details. today i recieved a letter again from dlc with their further details, black horse agreement number, agreement date, date hillesden purchased the account from black horse, ccj number and date of ccj. plus they have told me dlc are a trading name of hillesden securities. Agreement number & ccj info are correct but their dates are wrong. the loan was taken out jun 2006 cant remember exact date but was last week of june and ccj 15th august 2007, dlc says original date of agreement is 26th aug 2007 and ccj was registered on 15th august 2007. yes that means the ccj came before the agreement, these dates have been quoted several times. is the ccj still valid or do hillesden need to transfer it to their name? i have checked my files with equifax, experian & call credit and also done a check on trust online but neither the account or ccj show on any. this is the first time i have check so do not know if there was anything showing before. can ccjs be removed from credit files even though its only been 5 years since ccj was registered? i know i definately have/had a ccj for black horse. confused as i have another ccj which shows on all. they havent made any demands for payments so not sure if i should just ignore them again or if i should reply or even sar them

-

Hi Folks, Looking for some advice please on some letters my mum has been sent from a Company called DLC, working on behalf of Hillesden Securities who now claim they own a debt which was previously to Morses Club. My mum had a loan out with Morses some years ago before they went bust, afterwards no-one came round to collect any re-payments and no letters were sent to instruct her on how to make any payments. Now she has started receiving letters from this DLC company asking for her to make payments. I have sent the letter i got from here asking for a true copy of the CCA, this was in May of this year and all she had received back was a letter confirming receipt of the request and that they would request the info required. Every couple of months she got a letter to say that they were still 'chasing up' the required paperwork but that it didn't consitute enforcement if they still asked for her to make payments. She then received another letter about 2 weeks ago from the DLC parent company 'MDB' saying that the debt had now been passed to them as she wasn't making any payments. I sent the the letter from here saying that they had failed to comply with my request for a true copy of the CCA within the statutory time limit and as such the matter was now a formal complaint. We received a letter back very quickly from DLC stating 'The logistical aspects of recovering the original documents in time was virtually impossible' and that at the time the complaint letter was received they were 'technically' in breach of the 1974 act. They go on to say that while they disagree with my claims that they have failed to respond my complaint has been upheld. They say in their letter that as payments have been towards the debt the question of liability for the debt is not in question. I have asked them several times to supply a statement of any payments made but they have failed to do this, also with a copy of the CCA we have no idea exactly how old this agreement is. They have asked that i respond within 14 days to confirm what they have written but i was hoping to get some advice on here first before going back with another letter. Any help would be much appreciated, Thanks and Best Regards, Liam

-

Hi me and my partner have an account with brighthouse but i have been looking on here about the osc and dlc i now understand we dont need the osc but do we really need the dlc and if not how can i stop it ?

-

Hello this my first post on here, after reading many posts on here and gaining alot of insight to the unscrupulous world of the debt collection lot, however I received a odd letter today from DLC, an old Black Horse loan from 2005 which im disputing as its mostly PPI , the letter isnt a demand for payment just says creditor name Hillesdan Securities formerly Black Horse, its gives a balance and says information only, you do not need to respond!. theres no phone number on it anyway (not that i`d ring them if there was). Any ideas what i do with it-im tempted to file it in my favorite place-the toilet!

-

Wondered if someone could advise on what to do next. Had a credit card with mbna now Hillesden Securities Ltd. Had a lot of harrasement with them, agreed a monthly payment of £ 10.00 a month. Have been paying every month. I have asked them for a copy of my original agreement but nothing has appeared. Just recently they are wanting increased monthly payments of £ 85,00. There is no way I can afford this. Said I could only afford £ 10.00 and will continue to pay this, and am still requesting my agreement. They have recently said they would start court proceedings, if I did not increase payments, This would put a charge on my property, They have even said they have heard I am putting my property on the market, which is not true, cannont afford to move. Asked them where they had heard this, they would not say. I wrote to them about their harrasement and sent copies of other lettersI I had sent them. explaining my situation. They did offer a settlement figure but I cannot afford it. Yesterday received a short letter saying "We confirm the agreed settlement on your account has been paid in full. No further payments are required. All reference numbers are correct. Wondered what I should do. Can anyome advise.

-

Hi I am new to these forums - I have an outstanding debt of about £7000 with the HRMC which has been referred to DLC . I cannot afford to pay in one lump sum. What is my next course of action ? Can I offer to make monthly payments ? Should I pay HMRC or DLC ? What is the least they will generally accept ? I have received one letter one text and one phone call so far none of which I have answered. I have read in the forums about solutions but these generally refer to loans and credit cards and not income tax. Any help gratefully received.

-

Firstly - I'm a newbie here - so apologies if I ask the same as others have !!! I had a credit card with MBNA for around 15 years before I used the card to purchase a car (cost approx £9k) in March 2011. The transaction was made by myself with the car dealer that advertised it, I called the dealer and read out my card details over the telephone for the car that I had seen a description of on the internet. The car dealer delivered the car and upon arrival it was clearly not as described in a number of ways (some damage and no full MoT to mention a couple) and this is clearly provable against the internet description where it stated full MoT and no mention of any damage. The supplying car dealer was clearly in the business of selling cars as he had about 6 other cars advertised for sale at the time and I've kept copies of all these descriptions in case they are required later. So under distance selling regulations, I complained to the supplying car dealer and asked for a refund, made the car available for them to collect but they refused to accept the car back and refused to collect the car. I immediately made a section 75 claim to MBNA. MBNA stated the disputed amount would be put on hold until the matter was resolved. Sensing there was going to be a fight I cancelled the direct debit so that the disputed amount would be "on hold" with MBNA and not with myself and wrote to MBNA telling them that was my course of action and supplied copies of all information receipts/descriptions/correspondence with the car dealer. Eventually MBNA refused the section 75 claim, for a couple of spurious reasons. One was broken debtor-creditor relationship - MBNA claimed the car dealer was selling the car on behalf of the previous owner !! clearly MBNA don't seem to understand how car dealers sell cars and this one was an obviously blatant attempt by the car dealer to attempt to avoid responsibility. The other was that MBNA claimed that I knew about the damage prior to delivery and that I should have checked the car before purchasing. I demonstrated to them that I relied upon the description and could not have been expected to travel from Oxford to Scotland to check the car over before deciding to purchase. It was clear to me that I had provided sufficient information and evidence to support my section 75 claim, and I repeatedly insisted that MBNA honour their obligations under section 75. However, they refused and set on a course of pursuing me for what they claimed was an outstanding balance and what I repeatedly claimed was the disputed "on hold" amount. I wrote to them on several occasions suggesting that we should put the matter in front of a judge to decide. Eventually they went through the process sent me lots of demanding letters and default notices which I always replied to and politely reminded them that the outstanding balance is subject to a Section 75 claim and that if they felt strongly about it then I would be happy to talk it all over in front of a judge. MBNA's last letter they stated that they would be selling the debt. I immediately wrote back to MBNA and informed them that they do not have my permission to give or sell any of my personal data to anyone. At this point I made a claim through the financial ombudsman, which is currently in progress. In the meantime, MBNA have sold the debt to DLC who appear oblivious to the section 75 claim and are now harrassing me with letters and phone calls. I have written to DLC telling them to stop harrassing me and referred them back to MBNA, stating that it appears that they have obtained my personal data in contravention of the data protection act. Clearly there are several strands to this situation, I feel strongly that this is a valid section 75 claim, but it seems that MBNA have simply avoided justice and I have been left with a blemished credit history. My first concern is that the claim via the financial ombudsman may be too late. My second concern is that having not paid the balance when I left the "on hold" balance with MBNA may have undermined the claim to some extent. Comments, the experience of others in similar situations and all advice is appreciated. (I will add/update as and when I get updates) thanks !

-

Hi all, Wonder if anyone could shed a bit of light on this situation My in laws, who are in their 60's, have a washing machine from Brighthouse, which they have had for about 3 years. They have never had an annual statement in the 3 years and when they asked their local store they were fobbed off with excuses. Does anyone know how they would go about getting one of these that would cover from the period they got the washing machine til now as they have been told that the machine wont be paid off until a week before christmas which we think it longer than what it should be. They have also had a tv and a touchscreen pc in previous years, the tv went back because they missed a payment and the pc was a joke, it broke, was returned three times each time with another pc that was clearly broken and during this time they were advised not to pay as they didnt have the pc. They were told that they would only be entitled to a new working pc if they signed a new agreement with them which they didn't. With all of these items they had OSC and DLC, where do they stand with these as the have occasionally fell behind with payments and have continued to pay they're weekly payment which included these covers? Thank You

Hi all, Wonder if anyone could shed a bit of light on this situation My in laws, who are in their 60's, have a washing machine from Brighthouse, which they have had for about 3 years. They have never had an annual statement in the 3 years and when they asked their local store they were fobbed off with excuses. Does anyone know how they would go about getting one of these that would cover from the period they got the washing machine til now as they have been told that the machine wont be paid off until a week before christmas which we think it longer than what it should be. They have also had a tv and a touchscreen pc in previous years, the tv went back because they missed a payment and the pc was a joke, it broke, was returned three times each time with another pc that was clearly broken and during this time they were advised not to pay as they didnt have the pc. They were told that they would only be entitled to a new working pc if they signed a new agreement with them which they didn't. With all of these items they had OSC and DLC, where do they stand with these as the have occasionally fell behind with payments and have continued to pay they're weekly payment which included these covers? Thank You -

Hi, first post so please bear with me. My husband submitted his NDL Cashflow to the HSBC in April this year when he realised he could not meet his commitments, mostly in return he has had letters advising him to get help from a DC and of course the phone calls. The HSBC also denied that he had written to them so he sent them copies of the recorded delivery receipts and complained about the way he had been treated, he did receive a better response to this and an apology and a refund of charges for that month, he also pointed out that he would not deal with this matter on the telephone and would they please deal with it by letter, he also received a letter offering him a reduced full and final settlement which he replied to saying if he had any money he would be making his monthly payments, no reply yet. Frankly this is one of the more baffling elements of being in debt, you do what you think is the right thing and offer what you can and it gets ignored? I cannot see any merit in totally ignoring an offer,they can always say no (in writing of course). I think it is back to the drawing board Rohannah

-

Hi all Firstly I have just joined this site owing to a letter i recieved today from DLC/Hillesden Securities Ltd I am desperately in need some advice. Apologies if i have posted this in the wrong place or have duplicated an ongoing thread like i say im new to this site and just hopeful of some advice on what to do. I have been on a dmp for approx three years, I now owe circa £28 k from an initial debt of £35k. I work full time and have a house (mortgaged with little equity). A couple of times I hve had to reduce the amount i pay on the dmp im on (with cccs) owing to different circumstances. After a reduction earlier in the year i started getting threatening letters from DLC (direct legal collections) as in april/may i had to reduce my dmp payment to £5 per creditor temporarily which is where the problems started. I have since done a review with CCCS and for the past two month am paying £136 per month towards my dmp, the share to DLC/Hillesden Securities is £38 per month (I owe DLC/Hillesden £8k). They said this isnt enough and want circa £90 which i clearly cant afford. They said they would proceed with litigation with a view to geting a charging order against my house. This morning i recieved a default notice and a county court claim form. My question is does anyone know how i should proceed i.e accept the debt or contest it. If i contest it apart from buying me a further 28 days will it get me any further or in reality am i resinged to getting a CCJ against me. I work for a professional prctice and my concern is if they get wind of this i.e a attachment of earnings I will lose my job. Also given my house has little or no equity i cant see how a charging order will benefit them. This also seems unfair on my other creditors as part of the dmp ethos is meant to be fairness/equlaity to all of my creditors. Can any oof this be used as a defence? Sorry if im rambling but im very worried about this, really mkes me feel like giving up, any suggestions on how to proceed would be very gratefully received as the clock is now ticking. Thanks

-

Like many here in the sub-forums, I have debt problems and I'm paying my debts off in the best way I can afford with good advice learned from the internet (especially The Consumer Action Group) in how to tackle my problems. Having said that, DLC are the only debt collecting company that have caused me more grief than I think I deserve I sometimes feel like throwing in the towel. DLC acquired my MBNA credit card debt late 2009. At first, they phoned me regularly, sent me letters etc but advice from CAG helped me stave them off. We correspond by email only now. I am currently paying £5 per month towards my old MBNA credit card debt and this is the absolute max I can afford. They accepted this payment about 6 months ago (even sent me paying in slips) with the condition that they can review at anytime. I recently started receiving emails from them asking me to forward my income/expenditure details. I just secured a new job (7 weeks ago) which is only a temporary, ongoing, full time job (minimum wage). My net pay pays all my bills and I have roughly £2.50 disposable income left per week so living on the edge all the time. Obviously I'm looking for new work but that's difficult round here in Doncaster given the current employment problems we have. Their latest email worries me the most: Thank you for your e-mail of 28 May 2012, your comments have been noted. Whilst you are not obliged to provide us with income & expenditure details if you do not wish to do so, we are entitled to request these in order to consider if we are willing to accept a payment arrangement towards your balance. The reason that we have requested income and expenditure details from you is because you have advised us that you are unable to pay this balance in full. In order to determine whether we are able to offer you a monthly payment arrangement, we need information regarding your financial situation to ensure that any arrangement agreed is appropriate to both your circumstances and our requirements. I f we are able to come to a mutually agreeable arrangement with you, for repayments towards this balance, then this will prevent any possibility of the account being passed to our Litigation Department for further action to commence. If repayment negotiations fail I can confirm it is our intention to transfer your account to our litigation department for assessment. If approved by our litigation department a claim will be issued in the County Court with a view to submitting an application for a County Court Judgment, upon completion we will issue proceedings to obtain a Charging Order against your property. We can assure you that the Charging Order is required as security only and, if granted, will not be enforced by seeking an order for sale of the property or a lever to force you to make payments you can not realistically afford. Should you fail to provide an income and expenditure form and evidence your current financial situation, I can confirm we intend to proceed as above. Please either complete the attached income and expenditure and return it to us by 13 July 2012 or contact Sandy Lloyd on 0844 335 6497, quoting extension 7528, to discuss your account. Yours sincerely Duncan Pierce Team Leader They already accepted a payment arrangement 6 months ago, I cannot afford to pay more at present. What's my next step? Hope someone can help

-

I've had a debt with DLC for a while now. Coming up to SB and had a few discount offers from them. Obviously they now realise that no-ones going to get a yearly bonus from me and they' ve passed it on to another DCA. Is this sort of thing normal?

I've had a debt with DLC for a while now. Coming up to SB and had a few discount offers from them. Obviously they now realise that no-ones going to get a yearly bonus from me and they' ve passed it on to another DCA. Is this sort of thing normal? -

MBNA/DLC/Hillesden Securities have issued a claim for a debt of £17,000 including court/solicitor fees. I did a CCA request a long time ago but did nothing with it, I think they failed to supply an original agreement but took it no further. I cannot find the response at the moment. If i can find it, is there anything I can do to fight the claim and in the meantime can someone recommend a delaying tactic to buy myself some time. Can I say the debt is in dispute even though I have not pursued it with MBNA? Thankyou in anticipation of some help.

MBNA/DLC/Hillesden Securities have issued a claim for a debt of £17,000 including court/solicitor fees. I did a CCA request a long time ago but did nothing with it, I think they failed to supply an original agreement but took it no further. I cannot find the response at the moment. If i can find it, is there anything I can do to fight the claim and in the meantime can someone recommend a delaying tactic to buy myself some time. Can I say the debt is in dispute even though I have not pursued it with MBNA? Thankyou in anticipation of some help. -

Hi Guys! I am new to this forum, but unfortunately not new to my HPI debt, which is now contorlled by DLC AKA Hillesden Securites! I bought a car on Hire Purchase in 2008 The car broke, and as a result had a new gearbox fitted under warranty, which itself broke 2 months later Peugeot refused to fix under warranty, saying it was drivers error, black horse did not want to help, and I could not keep up the finance!! The debt now stands at £12000+. I am currently bankrupt, the insolvency service are aware of this debt with the car, but cannot take it on fully until the car is reposessed!! Currently DLC own the car, but are refusing to reposess! they contatntly ring me, which is NOT allowed under section 285 of the insolvency act!!! Peugeot are charging me storage which is currently at £1572.00, they will not release the car until payment is made (I am liable as i well know and am fine with) but they will not release the car to me as DLC own the car, but DLC will not reposess and will not give a reason as to why! Until they do, the insolvency service will not take this debt on fully!!! Please help I need to know what to do, DLC are very threatening, but this does not bother me, but what does bother me is the smarmy comments i get when they think they have won because they will not reposess the car! BUT even after I am discharged from bankruptcy, They debt will still be included in my bankruptcy estate as the debt was incurred before I was made officially bankrupt!! Sorry to go on, but this debt is going on as is the problems with DLC!! Thankyou in advance for any advice Tom

-

Hi Guys, I have received a few letters from Clarity which started with the usual we are trying to contact someone, which I ignored (why help them?) then came the "you owe us loads of money" letter, which I also ignored because I see why I should ring them or do anything initially. Then came the "we will send round the FieldCall people to discuss the fact that you owe us loads of money" letter. I was not too purturbed because a) I had been chased almost a year ago for almost the exact same amount by Lowell, who finally admitted they were wrong and appologised for writing to me (I had written a very polite "prove it" letter), and b) I recently came across these forums which are a revelation. I wrote a letter back basically saying, very nicely (I think) - prove it, and I don't want you sending anyone round to talk to me about it. Today I received the attached letter (suitably redacted), to which I want to reply in this way: Dear Clarity, If you don't know who I am, then stop accusing me of owing you money. Yours faithfully, etc. What do people think? I don't wish to fire flaming letters at them, because I feel that that sort of thing can later predudice things, if, for some reason it all turns sour. I am not worrying particularly, but would like to ensure that my response is measured and reasonable. Any advice?

-

Has anybody had any dealings with Wescot Credit Services I would be interested to about experiences you may have had and how best to deal with them. They seem to follow the same general way of most debt collectors " threaten first and the back off when you fight back". Regards Mike

-

I was recently sent a letter by Mercantile Data Bureau Limited (the reasons are unimportant at this time) and as always decided to do a little research on them. It seems they have a less than stellar reputation, even for a debt collector, and I discover that their limited company is actually dormant and has been for a number of years. It is an offense to trade as a dormant company according to Companies House. If Mercantile Data Bureau Limited have recieved monies from people or sent invoices for the same then this is classed as trading. My suggestion to you dear readers is to alert Companies House if you have paid any money to them and have proof of the same. They will be very happy to hear from you. Their reply to my email: Thank you for your email. With regard to the dormant accounts filed for ‘Mercantile Data Bureau Limited’ I appreciate your concerns, however we would only be able to consider this matter further if you could supply evidence that the company is trading or has traded during a particular period, such evidence would be receipts, invoices, cheques or bank statements in the name of the limited company. We need to be satisfied that significant financial transactions were made by the limited company during the period concerned. The registration of the name as a limited company may have been done to protect the name or the company may have recently started trading. Please could you forward such evidence via email as an attachment, or you may wish to write to us at the following address: Technical Offences Team Companies House Crown Way Cardiff CF14 3UZ enquiries@companies-house.gov.uk

-

Hi I received a letter from dcl In June in respect of a Welcome Finance Loan, I sent off a CCA request non recorded on the 23rd of June. Up until yesterday 18th July I had not heard from this company, so I prepared a letter advising that I was placing the account in dispute. Today 19th July I received the following letter. "Hillesden Securities Hillesden Securities Ltd. BUCKINGHAM ROAD BRACKLEY NORTHANTS NN13 7DN Mr X Xxxxxx 18 July 2011 Dear Mr Xxxxxx Account Number 1xxxxxxxxx0 Formerly Welcome Financial Services Ltd xxxxxxx Thank you for your letter dated 23 June 2011 regarding the above account. I can confirm and advise the following:- We have removed your contact telephone number from our records and will continue to pursue you through written communication only. Please note that if you do not keep a regular dialogue with us regarding this account and update us accordingly, our guidance from the Information Commissioner states that we are entitled to re-instate your contact telephone number to continue collection activity on the account when required. Hillesden Securities T/A direct legal & collections are an agency collecting on behalf of our client, Welcome Financial Services Ltd who remains the legal owner of your account. Your request for information under the Consumer Credit Act 1974 is required to be made directly to Welcome Financial Services Ltd. Your letter states that a postal order for £1.00 is included, however there was no postal order enclosed. Upon receipt of your letter and statutory fee Welcome Financial Services Ltd will comply with your request. Yours sincerely Data Controller Compliance Team Telephone: 01280 845616 Registered Office: Willow Road, Bracklcy, Northants. Registered No. 1418063 in England. A Member of the FACCENDA Group of Companies" My query is do I contact Welcome or as dlc are their agent continue to deal with them. I have sent off the dispute letter and a copy of the original request again this time registered post.

-

I tried to do a search and see if there was a thread about this but there wasn't. Went into my spam folder and found this email.... Looks like they are trying whatever they can and hiding behind words to get people to contact them.:mad2 I have never given a DCA this email address but I must asume that they must of received it by other means, for example my bank. I didn't click on the link and I sent this to trash after I uploaded it. Just a heads up to let people know. Aunt Rene. EDIT* I don't have enough posts to upload the screen print. Sorry....

-

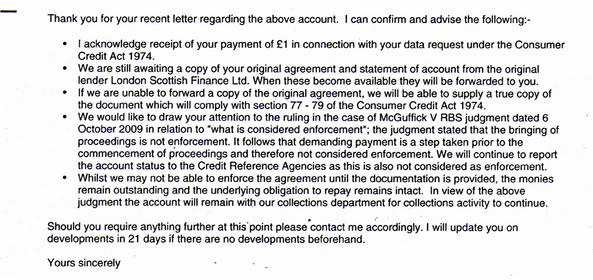

Hi Everyone, [goto post 73, details until them are wrong] I’ve found out recently that my mother and her partner took out a 900 pound loan out with Scottish Finance in 2002. Originally paying back 30 pounds a week for 2 – 2 ½ years until her partner died. She then paid either 15, 20, 22 pounds a month ever since. It was passed onto DLC in 2008 and they keep calling her to increase the repayment amount, even though they know, she’s on the basic state pension. I’ve been to the CAB and they gave me a CCA request to send off, and then return to them with the reply. Unfortunately, the local CAB is now in crises and not answering their phones, or taking on any new cases. And I’ve been told it’s going take at least a month to get a return appointment. So I was wondering what to do next, basically. it appears my mother has repaid over 4000 pounds so far in ‘interest’ and the balance is still higher than the original loan. It’s around 1200 pounds. I sent the CCA request to DLC, and received a reply from Hillesden. Inside an envelope with a ‘return to DLC if undelivered’.! Their reply to the CCA says that they are ‘awaiting a copy of your original agreement and statement of account from your original lender…..’. I visited, what was the local office, of London Scottish and found out that they went into liquidation in 2008. And that they had left all their files behind, which the new occupiers (who I spoke to) had to shred and take to the tip. So basically, I think I need to know whether to wait the 21 days that Hillesden would like, which means the letter should hopefully wound arrive just before my new CAB appointment, and taken both letters there. Or should I send them a ‘failure to provide a copy…’ type letter and take all three letters along to CAB. She's not paying any money at the moment so should I send a in dispute letter? Or have they admitted that in the '...not able to enforce..." section. Any info, suggestions, or advice would be really helpful. Thanks, bob

Hi Everyone, [goto post 73, details until them are wrong] I’ve found out recently that my mother and her partner took out a 900 pound loan out with Scottish Finance in 2002. Originally paying back 30 pounds a week for 2 – 2 ½ years until her partner died. She then paid either 15, 20, 22 pounds a month ever since. It was passed onto DLC in 2008 and they keep calling her to increase the repayment amount, even though they know, she’s on the basic state pension. I’ve been to the CAB and they gave me a CCA request to send off, and then return to them with the reply. Unfortunately, the local CAB is now in crises and not answering their phones, or taking on any new cases. And I’ve been told it’s going take at least a month to get a return appointment. So I was wondering what to do next, basically. it appears my mother has repaid over 4000 pounds so far in ‘interest’ and the balance is still higher than the original loan. It’s around 1200 pounds. I sent the CCA request to DLC, and received a reply from Hillesden. Inside an envelope with a ‘return to DLC if undelivered’.! Their reply to the CCA says that they are ‘awaiting a copy of your original agreement and statement of account from your original lender…..’. I visited, what was the local office, of London Scottish and found out that they went into liquidation in 2008. And that they had left all their files behind, which the new occupiers (who I spoke to) had to shred and take to the tip. So basically, I think I need to know whether to wait the 21 days that Hillesden would like, which means the letter should hopefully wound arrive just before my new CAB appointment, and taken both letters there. Or should I send them a ‘failure to provide a copy…’ type letter and take all three letters along to CAB. She's not paying any money at the moment so should I send a in dispute letter? Or have they admitted that in the '...not able to enforce..." section. Any info, suggestions, or advice would be really helpful. Thanks, bob

-

I purchased a phone on an 18 month contract from Orange in April 2008. In September 2009 I decided I wanted to cancel the contract after the 18 month period was up and sent an e-mail and covering letter by post to this effect. I also cancelled the direct debit after the final payment was taken from my bank account. The phone was not used after the date I sent the cancellation e-mail and letter. I heard nothing from Orange and considered the contract closed and all was ok. Then in early January 2010 I received a letter from Orange stating that my account was in default and that I owed £60.74 in airtime. I immediately phoned Orange who said they had received my e-mail but an operator had tried to contact me but I was unavailable and a message was left to phone their help desk. There was no message left on my land line, and as I was not using the mobile phone no message was seen. No letter was received either. The operator asked for a payment of the £60.74 which I refused. Since then I have received many letters and phone calls from debt agencies, firstly from Moorcroft then DLC and now the latest is Scotcall. All have asked for the payment and which I have refused. Threats of court action, doorstep collectors etc have followed. I have told Moorcroft and Scotcall that I want them to take me to court as I dispute the debt, but nothing has happened yet. Now the final straw. I tried to purchase a computer yesterday on a buy now pay later finance option but was refused finance for the first time ever in my 64 year life. I went to creditexpert and got a credit report and lo and behold there is one default among the 17 listed and it's Orange. This was added in June of this year. So although I am disputing the debt, Orange are allowed to trash my otherwise perfect credit rating. What can I do now? Any help would be great.

-

Defaulted on an £8k secured loan 3 years ago which has now is now £13k when I lost my job. Since then I have been working but the jobs have been much lower paid I would not have been able to pay my contractual payment of near £300 per month. I've been on reduced payments for 3 years now. Every 3 months I have to send my bank statements and they question every entry they believe is not essential and I have to justify why I spent money on that item. Well I'm really fed up with the patronising collections and I want to tell them I'm working but I don't earn that much and I'm really struggling financially. They have told me that I can't stay on a reduced payment plan indefinitely and this time he was really threatening. Ok, I hold my hands up I've not been entirely honest with them about working but I need to manage this situation before they find out something and decided to take my house away. What advice can you give me to try to manage this situation. I will cancel the payment protection which will reduce the outstanding balance but there is still the question of the rest. Secondly, does anyone now how I could possibly get rid of these people without losing my house? How can I get these people of my back.

Defaulted on an £8k secured loan 3 years ago which has now is now £13k when I lost my job. Since then I have been working but the jobs have been much lower paid I would not have been able to pay my contractual payment of near £300 per month. I've been on reduced payments for 3 years now. Every 3 months I have to send my bank statements and they question every entry they believe is not essential and I have to justify why I spent money on that item. Well I'm really fed up with the patronising collections and I want to tell them I'm working but I don't earn that much and I'm really struggling financially. They have told me that I can't stay on a reduced payment plan indefinitely and this time he was really threatening. Ok, I hold my hands up I've not been entirely honest with them about working but I need to manage this situation before they find out something and decided to take my house away. What advice can you give me to try to manage this situation. I will cancel the payment protection which will reduce the outstanding balance but there is still the question of the rest. Secondly, does anyone now how I could possibly get rid of these people without losing my house? How can I get these people of my back. -

MBNA have confirmed to me that they only have page 1 of my application form from 1993. They have nothing else relating to my application. They quote the Carey case and say that not having all the paperwork is not an issue and that I must continue to pay. I do not want a bad mark on my file but surely I can reclaim all the charges and interest and ask them to stop all interest and charges from this point on? What is my best course of action? thank you.

-

We've lived in this cottage about 18 months now. When we first moved in we had letters from DLC for various people (some were the previous tenants) and they stopped. Just had a letter arrive from them for someone completely different and the amount owed is very large. Is there any way we can get them to stop sending us letters for all these people? If anything it's just plain annoying and not wanting things to go missing for someone else's debt. The other thing I'm wondering about is this debt dates back to 2001 - isn't there a cut-off point when debts can no longer be chased?

-

Today received MBNA's response to my CCA request - a mail-in application from 2000. The two 'halves' don't appear to match. The application refers to data protection info. in condition 12 but condition 12 on the other half is about payment holidays. Possibly it could refer to a different condition 12 on a tear-off list but who knows? I'd be grateful for any comments and suggestions of what my next move should be. I haven't paid anything for a few months although CAB is supposedly negotiating a six-month freeze but I'm still receiving statements with about £500 extra interest each month. (I'm awaiting their response to a SAR as well.)

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS