Showing results for tags 'required'.

-

My rent is payable weekly (tenancy agreement states rent is to be paid weekly to landlord's bank account) which I do. I have been told that the landlord should still provide a rent book as it is paid weekly - is that correct? Thank you.

My rent is payable weekly (tenancy agreement states rent is to be paid weekly to landlord's bank account) which I do. I have been told that the landlord should still provide a rent book as it is paid weekly - is that correct? Thank you. -

I took virgin media to CICAS and they lied about the contract. They told CICAS the screen shot of the t&cs I provided was from an old contract from someone else while the screen shot they provided is from my contract (by this time they had changed my online profile and had updated my contract to show new t&cs). I did not have the original contract copy at that moment but later, after CICAS decided in their favour, I found out the email they had sent me which had the contract I signed and could prove my stance was right. The only proof they gave was fake screen shots which I can prove now was fake. CICAS would not listen to me as their decision is final. Can someone help me legally and take them to court. I do not want to spend more money on them unless I have some legal advise. They not only broke their T&Cs with me but also lied to CICAS deliberately as I had pointed out to them in a call that my online profile shows the old t&cs and after three weeks they changed those. I am sure they have done it to 100s of thousands of people and ripping them off. It's a big [problem] I can tell. Please note I am no more looking for the contract I signed as I have it in my email when they originally sent it to me.

I took virgin media to CICAS and they lied about the contract. They told CICAS the screen shot of the t&cs I provided was from an old contract from someone else while the screen shot they provided is from my contract (by this time they had changed my online profile and had updated my contract to show new t&cs). I did not have the original contract copy at that moment but later, after CICAS decided in their favour, I found out the email they had sent me which had the contract I signed and could prove my stance was right. The only proof they gave was fake screen shots which I can prove now was fake. CICAS would not listen to me as their decision is final. Can someone help me legally and take them to court. I do not want to spend more money on them unless I have some legal advise. They not only broke their T&Cs with me but also lied to CICAS deliberately as I had pointed out to them in a call that my online profile shows the old t&cs and after three weeks they changed those. I am sure they have done it to 100s of thousands of people and ripping them off. It's a big [problem] I can tell. Please note I am no more looking for the contract I signed as I have it in my email when they originally sent it to me. -

Would very much appreciate some guidance in putting together an appeal for county court. Mainly in terms of putting paperwork together. All. help would be greatly appreciated. Martin

Would very much appreciate some guidance in putting together an appeal for county court. Mainly in terms of putting paperwork together. All. help would be greatly appreciated. Martin -

Hi all new to the forum. I apologise if this is the wrong sub forum. I have recently decided to get my credit in order. I have for a long time buried my head in the sand and in the process ended up with 2 ccjs and iva i didnt make a payment to after careful 3rd party talks decided it wouldnt be right, numerous defaults. I have made the first steps Got my credit File from Experian and Equifax these show the following ACTIVE 297 - o2 325 - o2 116 - Indigo Michael (Safety net credit) Paid off in full this month account closed. Closed (with a default balance) 400 - O2 765 - Lowell Portfolio ( Provident) 872 - Lowell Portfolio (VODAFONE) 241 - Motormile Finance (Lending Stream) 285 - PRA Group 216 - APS OVERDRAFT (cashplus credit card) 304 - o2 441 - o2 204 - Lowell Portfolio 258 - CFO Lending (now with Motormile finance) 390 - Vanquis 1,361 - CCJ - 20-08-2012 473 - CCJ - 21/2/2013 0 - IVA - 21/12/15 Im am looking for best advise to get this ^ problem in order, paying them all off in full although my preffered option is one I just aint capable of at the present time. CCJ 1 This was taken out by Swansea Council without my knowledge and only after getting my credit file was I aware it even existed. I had moved from Swansea 2 years prior to the judgement and signed the house over to my ex partner at her address. CCJ 2 this was for a advertising debt for a limited company I was running and am unsure as to why or how they gained a judgement in my name when I never signed a directors guarantee etc. IVA I signed up to an IVA but after careful consideration and persistant messing about by the managing company Knightsbridge I decided to pull out of letting them handle my debts and here I am.

-

Name of the Claimant ? Cabot Financial UK Ltd Date of issue – 1 Jun 2017 What is the claim for – 1.By an agreement between IDEM Re Egg Banking Plc & the Defendant on or around 16/8/2005 ('the agreement') IDEM Re Egg Banking Plc agreed to loan the Defendant monies. 2. The Defendant did not pay the installments as they fell due & the Agreement was terminated. The Agreement was assigned to the Claimant. THE CLAIMANT THEREFORE CLAIMS 1397.53 What is the value of the claim? 1547.53 (inc fees of 150) Is the claim for - personal loan When did you enter into the original agreement before or after 2007? before - around 2003-4 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Cabot Were you aware the account had been assigned – did you receive a Notice of Assignment? NO Did you receive a Default Notice from the original creditor? No Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ?No Why did you cease payments? Payments were being taken by direct debit, unaware payments had stopped, no notices received for lack of payment at any time What was the date of your last payment? Exact date unknown at present, sometime prior to 2010 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management planicon? No financial problems, no need to contact creditor, no need for debt management. They stopped taking payments and did not inform us we were behind Hello I received a county court claim form in the post today from Cabot. I will fill out the details I know you need in the next post. I'm doing this for my wife, who is in bits now because of this form. I'm trying to calm her down but he is scared witless. She did take out a loan over 10 years ago with Egg, but that was sold to another company when Egg got out of the personal loan business and I think we only had one more letter from them after that. This is the only one we've received since. Bank accounts and direct debits have not changed in over 20 years and she always pays her debts on time. I don't think she has ever missed a payment for anything. I work at home and as such, very rarely ever leave the house. No-one has come knocking at the door about this - or any other - debt in the 10 years I've lived here. Can someone lease assist me, I have no idea what I'm doing and we cannot afford solicitors. Thank you in advance Ian

Name of the Claimant ? Cabot Financial UK Ltd Date of issue – 1 Jun 2017 What is the claim for – 1.By an agreement between IDEM Re Egg Banking Plc & the Defendant on or around 16/8/2005 ('the agreement') IDEM Re Egg Banking Plc agreed to loan the Defendant monies. 2. The Defendant did not pay the installments as they fell due & the Agreement was terminated. The Agreement was assigned to the Claimant. THE CLAIMANT THEREFORE CLAIMS 1397.53 What is the value of the claim? 1547.53 (inc fees of 150) Is the claim for - personal loan When did you enter into the original agreement before or after 2007? before - around 2003-4 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Cabot Were you aware the account had been assigned – did you receive a Notice of Assignment? NO Did you receive a Default Notice from the original creditor? No Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ?No Why did you cease payments? Payments were being taken by direct debit, unaware payments had stopped, no notices received for lack of payment at any time What was the date of your last payment? Exact date unknown at present, sometime prior to 2010 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management planicon? No financial problems, no need to contact creditor, no need for debt management. They stopped taking payments and did not inform us we were behind Hello I received a county court claim form in the post today from Cabot. I will fill out the details I know you need in the next post. I'm doing this for my wife, who is in bits now because of this form. I'm trying to calm her down but he is scared witless. She did take out a loan over 10 years ago with Egg, but that was sold to another company when Egg got out of the personal loan business and I think we only had one more letter from them after that. This is the only one we've received since. Bank accounts and direct debits have not changed in over 20 years and she always pays her debts on time. I don't think she has ever missed a payment for anything. I work at home and as such, very rarely ever leave the house. No-one has come knocking at the door about this - or any other - debt in the 10 years I've lived here. Can someone lease assist me, I have no idea what I'm doing and we cannot afford solicitors. Thank you in advance Ian -

Hi there I've had an Amex card (Amex BA rewards card) for several years. Back in September 2015 I sent a letter to tell them I had moved house and provided our new address. However I was getting my monthly statements on line by email so did not question whether they had updated my postal address on their records. In September 2016 I set up a standing order to cover £1000 per month payment but unbeknown to me the instruction failed. Even though Amex had my phone number and email contact details they did not let me know payments were not being received. Instead they wrote to me at my previous address. What's important here to understand is that up until this point Amex always contacted me via their online messaging system and my overseas mobile (due to the fact we lived overseas and this was an easy and immediate way to reach us). My expectation was therefore always that if Amex needed me urgently this is how they would contact me. Amex claim they never received my letter requesting they change my address. In January of this year (2017) I received an email from someone claiming to be a debt recovery agent for Amex. I thought it prudent to check with Amex this person was legitimate and also ascertained from Amex direct that they had cancelled my account and referred it to their debt collection agency. I immediately paid the missing payments and have continued to pay £1000 per month whilst I decide how to move forward. So my question is this? Even though Amex have cancelled my account they are continuing to charge interest on the balance each month. Which means that the payment I am making is mostly going to servicing the interest. I want to clear the original amount I owe them but do not think it is fair that I should have to pay interest when my account is cancelled. Should I talk to the debt collection agent and propose this? Or do I need to take a different approach (Ombudsman?). All advise greatly appreciated! Thanks in advance

-

Hello. I have some debts with 1st Credit, Westcot, Frederickson, BLS to name a few whom (and switched hands between companies), from my Student days. 1st Credit is near 1.6k, the others are around £400 each. I currently pay back via the Citizens Advice agreements each month. Pretty much it's going to take 14 years to pay off 1st Credit for example. They all often send me offers/reductions on the debt if I pay today, or pay XX amount, Westcot notably just started doing this today for a £400 debt. Would I be wise in potentially sending requests through for the DCA taking control from the original creditor? Or will I be paying these for 14 years? Just seen a lot of posts of similar actions and wondering if it would be a possibility, and would their be any implications to me?

-

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) The following regulation has been discussed for many months, and was finally laid before Parliament a few days ago (11th April). It comes into effect on 6th May 2017. The Road Vehicles (Registration and Licensing) (Amendment) Regulations 2017 http://www.legislation.gov.uk/uksi/2017/554/made

The following regulation has been discussed for many months, and was finally laid before Parliament a few days ago (11th April). It comes into effect on 6th May 2017. The Road Vehicles (Registration and Licensing) (Amendment) Regulations 2017 http://www.legislation.gov.uk/uksi/2017/554/made -

Good evening a couple of weeks ago I received court forms from Nottingham regarding CABOT. I have had a terrible time with this company, 3 times writing to ask for the creditors original signed credit agreement to no avail. I put a defence in to the money online tool (no idea what Im doing really) and stated that this company had harassed me (calls at work etc) and not supplied me with the credit agreement etc. Ive now received a letter from a company called Restons solicitors telling me my defence wont hold water and that I have 14 days to sort it Letter dated 28th March Ive been very ill since Friday so done nothing yet. Could someone please advise me as Ive no idea who Restons are or if they are real Thanking you in advance

-

Hello, A number of PCNs from Smart Parking were delivered to my address in the last few weeks, for an alleged breach of the terms of parking at Matalan in Sutton, Surrey. This was subsequently followed by a Notice of Intended Court Action letter from Debt Recovery Plus (DRP), stating the reason for the PCN being issued as: "Overstayed Paid Time". Earlier this week, another letter was received from SCS Law who claim to act on behalf of Smart Parking Ltd who have allegedly instructed this law firm to recover the PCN charges. The letter then goes on to state that Smart Parking are entitled to the outstanding sum under contract law, adding: "When your vehicle parked at the above mentioned site(s), the driver of the vehicle agreed to be bound by the terms and conditions of parking which was displayed on signage throughout the site(s). The driver of the vehicle breached the terms and conditions of parking on each of the above stated occasions for the reason stated. For each contravention, a parking charge notice was issued, for which the sums owed remain outstanding. We refer you to the Supreme Court decision in ParkingEye Ltd v Beavis [2015] UKSC 67. In this case, the Supreme Court found that parking charge notices do not contravene the penalty rule or Unfair Terms in Consumer Contract Regulations 1999 provided they protect a legitimate interest. Unless payment is made within the next 14 days, we are instructed to issue court proceedings to recover the same and any of our client's legal costs, without further recourse to you". I visited the Matalan store last weekend and discussed my issue with a member of staff, with the hope Matalan would intervene and request for the PCN to be cancelled, being a regular customer of the store. The member of staff was not very helpful but did advise me to contact Smart Parking directly for any resolution and also pointed out that Smart Parking were no longer the contracted to manage the car park. I would now appreciate the kind assistance of our very valued forum members to advice on how to fight this PCN successfully and have provided some relevant pictures from the car park, if this helps construct a solid defence. Thank you.

Hello, A number of PCNs from Smart Parking were delivered to my address in the last few weeks, for an alleged breach of the terms of parking at Matalan in Sutton, Surrey. This was subsequently followed by a Notice of Intended Court Action letter from Debt Recovery Plus (DRP), stating the reason for the PCN being issued as: "Overstayed Paid Time". Earlier this week, another letter was received from SCS Law who claim to act on behalf of Smart Parking Ltd who have allegedly instructed this law firm to recover the PCN charges. The letter then goes on to state that Smart Parking are entitled to the outstanding sum under contract law, adding: "When your vehicle parked at the above mentioned site(s), the driver of the vehicle agreed to be bound by the terms and conditions of parking which was displayed on signage throughout the site(s). The driver of the vehicle breached the terms and conditions of parking on each of the above stated occasions for the reason stated. For each contravention, a parking charge notice was issued, for which the sums owed remain outstanding. We refer you to the Supreme Court decision in ParkingEye Ltd v Beavis [2015] UKSC 67. In this case, the Supreme Court found that parking charge notices do not contravene the penalty rule or Unfair Terms in Consumer Contract Regulations 1999 provided they protect a legitimate interest. Unless payment is made within the next 14 days, we are instructed to issue court proceedings to recover the same and any of our client's legal costs, without further recourse to you". I visited the Matalan store last weekend and discussed my issue with a member of staff, with the hope Matalan would intervene and request for the PCN to be cancelled, being a regular customer of the store. The member of staff was not very helpful but did advise me to contact Smart Parking directly for any resolution and also pointed out that Smart Parking were no longer the contracted to manage the car park. I would now appreciate the kind assistance of our very valued forum members to advice on how to fight this PCN successfully and have provided some relevant pictures from the car park, if this helps construct a solid defence. Thank you. -

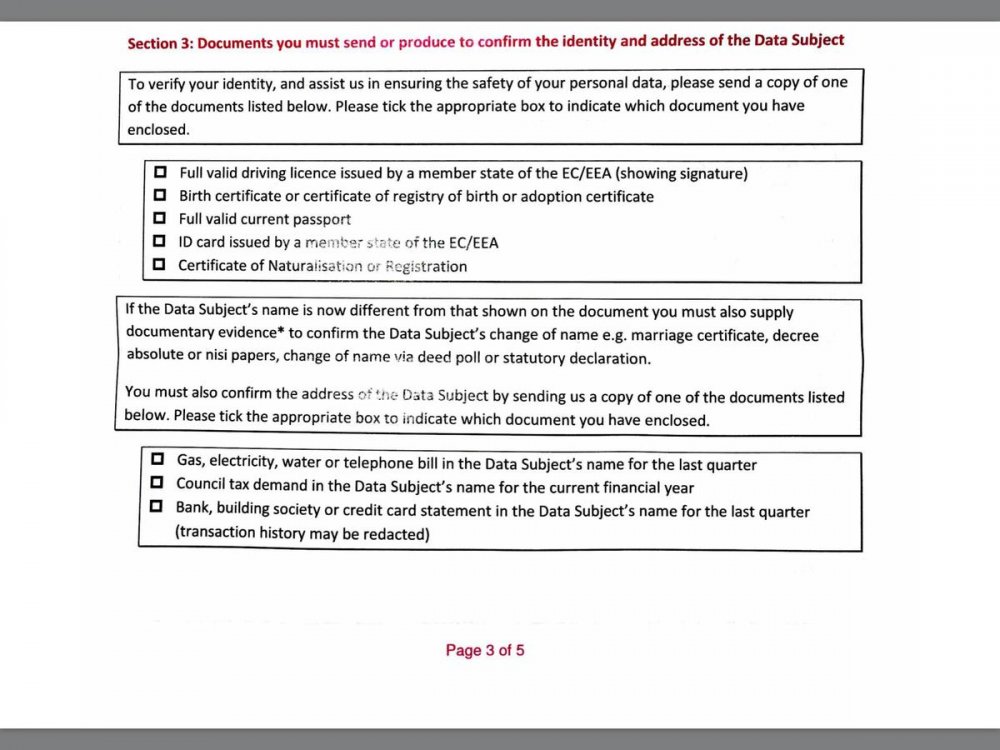

I've just sent off (with the £10 postal order) a Formal DSAR request to 1st Crud. All info required to be supplied, including a signature was provided in my formal and detailed letter. I've just received one of their 'please fill out this 5 page form' before we are obliged to do anything, however I'm not happy with what they are requesting I provide. There is no way I am ever going to provide them a copy of my driving licence, or bank statements and I'm back on here for some advice. I've been completing DSAR requests for approx 10 years, and apart from (almost) starting legal action with BC whilst some have been a struggle to get all info from and in a timely manner most have been compliant and not made me jump through too many hoops. (Oh apart from the DWP completely ignoring me for over 2 months! Still ongoing - but I class them in a different category to the CC companies and DCAs etc). Have the rules changed? I am now legally obliged to provide any of the following on the attached picture? Considering I've lived at the same address for over 10 years, and they've contacted me for 3-4 different companies at this same address, and threatened legal action to me at the same address, and supplied alleged CCA agreements, I would think that they should be fairly confident of my identity? Can I take this route, or will they likely play up and delay provision even though I don't (I think) have to legally provide the documents they have requested I send? Thanks ME_TOO

I've just sent off (with the £10 postal order) a Formal DSAR request to 1st Crud. All info required to be supplied, including a signature was provided in my formal and detailed letter. I've just received one of their 'please fill out this 5 page form' before we are obliged to do anything, however I'm not happy with what they are requesting I provide. There is no way I am ever going to provide them a copy of my driving licence, or bank statements and I'm back on here for some advice. I've been completing DSAR requests for approx 10 years, and apart from (almost) starting legal action with BC whilst some have been a struggle to get all info from and in a timely manner most have been compliant and not made me jump through too many hoops. (Oh apart from the DWP completely ignoring me for over 2 months! Still ongoing - but I class them in a different category to the CC companies and DCAs etc). Have the rules changed? I am now legally obliged to provide any of the following on the attached picture? Considering I've lived at the same address for over 10 years, and they've contacted me for 3-4 different companies at this same address, and threatened legal action to me at the same address, and supplied alleged CCA agreements, I would think that they should be fairly confident of my identity? Can I take this route, or will they likely play up and delay provision even though I don't (I think) have to legally provide the documents they have requested I send? Thanks ME_TOO

-

Hi all Just after some advice really, I traded my car in on Friday for a BMW 118d which to be honest I am happy with apart from the fact that the drivers side window switch (its a master switch which controls passenger window/driver window and electric mirrors) when I enquired about the car I was told it had 6 months MOT on it but they would put through a new MOT. This they have done and they did change 2 rear tyres as these were advisories, the guy I spoke to also said that it needed a new window switch....... picked the car up on Friday and again it was mentioned that the switch was changed so didnt think anything of it. However on way home from garage try windows and it doesnt work, I didnt bother mentioning that day as it was late Friday and thought I would wait til Monday. I emailed the garage yesterday and no response, emailed again today and so far no response. Now its only a window so its not a major big deal I suppose but I paid £7.5k for the car (7k trade-in on mine) and my car was immaculate and everything worked. Am I being a biy picky bearing in mind the car is 6.5 years old or not? The good news is that £250 of the £500 extra I paid was on my credit card so I do think I have some comeback via that if necesssary. ANy advice much appreciated!

-

Hi All, Currently have sent out CCA's to numerous DCA's However there is one i am unsure of how to proceed. Debt in question is loan from around 2000. Defaulted early 2004. CCJ obtained Sept 04 Interim Restriction added on Land Registry Oct 2004 (Debt in my name, house in mine and my wife's). I have checked the Land Registry and the name of the original creditor is still on there - CCJ not on Trust Online. This debt has been sold on - current DCA has had it since 2012. They have never mentioned the CCJ or CO in any correspondence. Can they really chase this debt? Can I send them a CCA as there is already a CCJ for the debt. Can they enforce as there is already an enforced CCJ on the debt - I am sure you cannot get 2 CCJ's for the same debt. Surely this debt is is Res Judicata - already decided upon so the DCA cannot take it to court again. Have trawled posts for this but cannot seem to find the best way forward for this - any advice would be greatly received

Hi All, Currently have sent out CCA's to numerous DCA's However there is one i am unsure of how to proceed. Debt in question is loan from around 2000. Defaulted early 2004. CCJ obtained Sept 04 Interim Restriction added on Land Registry Oct 2004 (Debt in my name, house in mine and my wife's). I have checked the Land Registry and the name of the original creditor is still on there - CCJ not on Trust Online. This debt has been sold on - current DCA has had it since 2012. They have never mentioned the CCJ or CO in any correspondence. Can they really chase this debt? Can I send them a CCA as there is already a CCJ for the debt. Can they enforce as there is already an enforced CCJ on the debt - I am sure you cannot get 2 CCJ's for the same debt. Surely this debt is is Res Judicata - already decided upon so the DCA cannot take it to court again. Have trawled posts for this but cannot seem to find the best way forward for this - any advice would be greatly received -

Heres one for you. Am i able to give more than the required length of notice to inform a company I am leaving them? IE 2 weeks instead of 1?

-

Hi all, first post and looking for advice/plan of attack. Parking Notice relates back to 15 May 2012. I was registered keeper but not using the vehicle at the time (I was in bed after a night shift!) The car park in question is free for 1 hour and no option to pay. The notice relates to an over stay. The original paperwork from June 2012 showed photo evidence of the vehicle, but no image of the driver. I don't have this anymore. binned it 6 months ago thinking this had gone away. BW Legal are now involved and I've sent them one denial letter. I did state I was going to complain to the CSA and SRA but got sidetracked and didn't get round to it. BW have responded with 2 letters. 1 dated 31 Oct. The main point being "We can confirm that our client does not intend to rely upon the Protection of Freedom Act 2012. as such we do not accept your assertions regarding payment. In the absence of driver details we are instructed to recover the suns due from you". The second letter looks to be a bog standard Final Notice letter dated 2 November. They have tried to call me once, but ignored it. Would be grateful for advice on my next actions and pointers to any CSA and SRA templates if needed. In this case, I genuinely wasn't the driver!!!! Thanks in advance

Hi all, first post and looking for advice/plan of attack. Parking Notice relates back to 15 May 2012. I was registered keeper but not using the vehicle at the time (I was in bed after a night shift!) The car park in question is free for 1 hour and no option to pay. The notice relates to an over stay. The original paperwork from June 2012 showed photo evidence of the vehicle, but no image of the driver. I don't have this anymore. binned it 6 months ago thinking this had gone away. BW Legal are now involved and I've sent them one denial letter. I did state I was going to complain to the CSA and SRA but got sidetracked and didn't get round to it. BW have responded with 2 letters. 1 dated 31 Oct. The main point being "We can confirm that our client does not intend to rely upon the Protection of Freedom Act 2012. as such we do not accept your assertions regarding payment. In the absence of driver details we are instructed to recover the suns due from you". The second letter looks to be a bog standard Final Notice letter dated 2 November. They have tried to call me once, but ignored it. Would be grateful for advice on my next actions and pointers to any CSA and SRA templates if needed. In this case, I genuinely wasn't the driver!!!! Thanks in advance -

Hi there, I (like many others) am in the same situation as Ginger - handed a PCN from ES for parking /stopping in the Spinningfields area. Letters of complaint / information requests have been ignored, Gladstones involved and the case referred to County Curt Business Centre. I'm pretty anxious and have never dealt with anything like this before. I am seeking some urgent advice as I returned from holiday to find the county court claim and now only have 2 days to respond... I obviously want to appeal and thinking along the lines of (pls forgive the lack of legal terms etc) : I am disputing this claim for the following reasons : 1) I have written to ES Parking and their legal representatives (Gladstones) several times to ask for more information and complain about their imposed fines. No acknowledgement or response has been received. 2) No evidence of wrongdoing / an offence being committed has been provided. They have sent me a photo of the front of a car - it is not evidence that an offence is being committed as you can only see the front half of a front end of a car in the photo (not the location or that the car is stopped). In the photo you can clearly see the two hands of the driver at the steering wheel, which suggests that the car was being driven at the time of taking the photo (i.e. not parked). 3) The charge they have applied is excessive, disproportionate and not commercially justifiable. Was £100, then £150, now £227. The original £100 is excessive and the subsequent increases and escalation to court whist ignoring my requests for more information and letters of complaint is wholly wrong. I suggested to ES parking that the original £100 charge was excessive and outweighs any cost to the landowner - I have asked for a breakdown of actual costs and subsequent increases. (No acknowledgment or response received). 4) The photo evidence provided is time-stamped with a different time to that of the alleged offence (the photo was taken at a different time to that of the alleged offence). Moreover as per point 2 - the photo is not evidence of any offence being committed. Their letter states that "the 'period of parking' to which the charge relates is the period immediately preceding the incident time" (the photo evidence is taken after the incident time). (the incident time is 12:00, photo is time stamped at 12:03) 5) There was no/insufficient signage on site at the time of the alleged offence. I have asked ES parking to confirm that there was signage on date of alleged offence - no response received. There is now signage onsite (months later) however this signage is inadequate as it's too small (roughly A4 size with lot's of very small text written on it), it is difficult to read from any distance and certainly cannot be read from a car, let alone a moving vehicle. There are no signs or anything to suggest that you are leaving a public road and onto a private one (the site of alleged offence is Manchester City Centre) - this is very confusing, perhaps deliberately so. It is not clear that the signs are referring to the road - it looks like they are referring to the adjacent pedestrian areas in front of some flats / offices, not that they are referring to the road - which you would assume was a public highway. 6) There were no road markings at the time of the offence to suggest that parking was prohibited (can evidence via google maps). 7) I have a 24/7 365 day a year parking space in my office underground car park at the site of alleged offence (so I have no reason to park outside, when I have a space inside). This can be evidenced if required. Does the fact that both drivers hands are at on the wheel in the photo provided suggest that the car was being driven into work car park ? (if indeed the photo was even taken at the site of alleged offence). 8) I have asked ES Parking and their solicitors (Gladstones) for more information to confirm who is the legal landowner and that ES Parking has their authority in this matter and also to confirm that the road where the alleged offence took place is in fact a private road. I have also asked for full details of the alleged offence and how long the car was parked for. No response or acknowledgment received. It is just not credible or fair that ES Parking can send members of the public a picture of half of the front end a car, showing only that the drivers hands are at the wheel and not the location where the photo was taken or that the car is illegally parked (or even parked at all) and demand payment of £100. They have not provided any details or evidence : - Of any offence being committed. - Details of the offence and how long the car was parked for. - That the vehicle was on site at the time of offence. - That they have authority from the landowner to pursue costs. - That actual costs to the landowner have occurred. - That the site of alleged offence is not a public highway. - In addition the time of offence is not the time the photo was taken. With the above points in mind, you write back to ES Parking to ask for more information and to contest their parking charge, they ignore you and ramp the costs up to £125, a further letter from you is ignored and then costs ramped up again to £150, you write again, which they ignore and then escalate the matter to a court. I believe that this demonstrates that ES Parking are operating in an aggressive, predatory and disproportionate manner which is designed to bully and intimidate innocent members of the public in order for them to obtain money. Are points 2 and 4 valid ? I'm (very obviously) a lay person but I'm hoping these are important from a legal perspective. Would really appreciate any help and guidance you can offer - thanks so much Roo

Hi there, I (like many others) am in the same situation as Ginger - handed a PCN from ES for parking /stopping in the Spinningfields area. Letters of complaint / information requests have been ignored, Gladstones involved and the case referred to County Curt Business Centre. I'm pretty anxious and have never dealt with anything like this before. I am seeking some urgent advice as I returned from holiday to find the county court claim and now only have 2 days to respond... I obviously want to appeal and thinking along the lines of (pls forgive the lack of legal terms etc) : I am disputing this claim for the following reasons : 1) I have written to ES Parking and their legal representatives (Gladstones) several times to ask for more information and complain about their imposed fines. No acknowledgement or response has been received. 2) No evidence of wrongdoing / an offence being committed has been provided. They have sent me a photo of the front of a car - it is not evidence that an offence is being committed as you can only see the front half of a front end of a car in the photo (not the location or that the car is stopped). In the photo you can clearly see the two hands of the driver at the steering wheel, which suggests that the car was being driven at the time of taking the photo (i.e. not parked). 3) The charge they have applied is excessive, disproportionate and not commercially justifiable. Was £100, then £150, now £227. The original £100 is excessive and the subsequent increases and escalation to court whist ignoring my requests for more information and letters of complaint is wholly wrong. I suggested to ES parking that the original £100 charge was excessive and outweighs any cost to the landowner - I have asked for a breakdown of actual costs and subsequent increases. (No acknowledgment or response received). 4) The photo evidence provided is time-stamped with a different time to that of the alleged offence (the photo was taken at a different time to that of the alleged offence). Moreover as per point 2 - the photo is not evidence of any offence being committed. Their letter states that "the 'period of parking' to which the charge relates is the period immediately preceding the incident time" (the photo evidence is taken after the incident time). (the incident time is 12:00, photo is time stamped at 12:03) 5) There was no/insufficient signage on site at the time of the alleged offence. I have asked ES parking to confirm that there was signage on date of alleged offence - no response received. There is now signage onsite (months later) however this signage is inadequate as it's too small (roughly A4 size with lot's of very small text written on it), it is difficult to read from any distance and certainly cannot be read from a car, let alone a moving vehicle. There are no signs or anything to suggest that you are leaving a public road and onto a private one (the site of alleged offence is Manchester City Centre) - this is very confusing, perhaps deliberately so. It is not clear that the signs are referring to the road - it looks like they are referring to the adjacent pedestrian areas in front of some flats / offices, not that they are referring to the road - which you would assume was a public highway. 6) There were no road markings at the time of the offence to suggest that parking was prohibited (can evidence via google maps). 7) I have a 24/7 365 day a year parking space in my office underground car park at the site of alleged offence (so I have no reason to park outside, when I have a space inside). This can be evidenced if required. Does the fact that both drivers hands are at on the wheel in the photo provided suggest that the car was being driven into work car park ? (if indeed the photo was even taken at the site of alleged offence). 8) I have asked ES Parking and their solicitors (Gladstones) for more information to confirm who is the legal landowner and that ES Parking has their authority in this matter and also to confirm that the road where the alleged offence took place is in fact a private road. I have also asked for full details of the alleged offence and how long the car was parked for. No response or acknowledgment received. It is just not credible or fair that ES Parking can send members of the public a picture of half of the front end a car, showing only that the drivers hands are at the wheel and not the location where the photo was taken or that the car is illegally parked (or even parked at all) and demand payment of £100. They have not provided any details or evidence : - Of any offence being committed. - Details of the offence and how long the car was parked for. - That the vehicle was on site at the time of offence. - That they have authority from the landowner to pursue costs. - That actual costs to the landowner have occurred. - That the site of alleged offence is not a public highway. - In addition the time of offence is not the time the photo was taken. With the above points in mind, you write back to ES Parking to ask for more information and to contest their parking charge, they ignore you and ramp the costs up to £125, a further letter from you is ignored and then costs ramped up again to £150, you write again, which they ignore and then escalate the matter to a court. I believe that this demonstrates that ES Parking are operating in an aggressive, predatory and disproportionate manner which is designed to bully and intimidate innocent members of the public in order for them to obtain money. Are points 2 and 4 valid ? I'm (very obviously) a lay person but I'm hoping these are important from a legal perspective. Would really appreciate any help and guidance you can offer - thanks so much Roo -

Hope someone with legal knowledge can help with this matter, We have sold our house in scotland and complete in 4 weeks. We have since discovered we have an inhibition order that was renewed for an old CCJ obtained in England that we need to get lifted. The story is this. We had a default judgement registered in england in january 2008 for 19k by a debt collection company. We went to court to get it set aside/defend as we were living in Scotland at that time. We were challenging jurisdiction and the amount plus. The judge issued a revised order in may 2008 amending the original judgement to £8k and requesting claimants to instigate mediation thereafter. No order was made about jurisdiction. We subsequently also found out after the judgement that PPI was included and the agreement has a false signature. This information was not available to us at the time of the second judgement in May 2008. The claimants registered the original CCJ in Scotland so they could pursue which resulted in an inhibition order, however, the inhibition order was issued in 2010 quoting the original CCJ in default issued in January 2008 of £19k and not the revised amount detailed at the hearing in May 2008 . The 5 year period expired and the inhibition was renewed in feb 2015. Is the inhibition valid given it quotes A CCJ amount that was subsequently amended by the court? What can we do to get it lifted quickly? We have subsequently moved back to England. Would appreciate any help available.

Hope someone with legal knowledge can help with this matter, We have sold our house in scotland and complete in 4 weeks. We have since discovered we have an inhibition order that was renewed for an old CCJ obtained in England that we need to get lifted. The story is this. We had a default judgement registered in england in january 2008 for 19k by a debt collection company. We went to court to get it set aside/defend as we were living in Scotland at that time. We were challenging jurisdiction and the amount plus. The judge issued a revised order in may 2008 amending the original judgement to £8k and requesting claimants to instigate mediation thereafter. No order was made about jurisdiction. We subsequently also found out after the judgement that PPI was included and the agreement has a false signature. This information was not available to us at the time of the second judgement in May 2008. The claimants registered the original CCJ in Scotland so they could pursue which resulted in an inhibition order, however, the inhibition order was issued in 2010 quoting the original CCJ in default issued in January 2008 of £19k and not the revised amount detailed at the hearing in May 2008 . The 5 year period expired and the inhibition was renewed in feb 2015. Is the inhibition valid given it quotes A CCJ amount that was subsequently amended by the court? What can we do to get it lifted quickly? We have subsequently moved back to England. Would appreciate any help available. -

I need some advice as to what I should do... here are the details of my situation. I purchased in to a property scheme run by a vendor in Nov 2008 , where you pay the vendor £2000 and for this they find a buy to let property for you where the rent covers the mortgage payment , the vendor takes care of the purchase of the property, they take care of the solicitor, all the management, (renting, any bills) all bills after two years you have the option to sell the property or to continue to use their services. The Solicitor used was in this with the vendor, the valuation from the surveyor showed that the property was worth more than what I was paying After three months after purchasing the property, the rents stopped coming in I started to chase the vendor who told me they were having some cash flow problems and I will get the rents to cover the mortgage, this went on for a two to three months and soon the vendor had disappeared. I visited the property I had purchased and asked the tenant for the rent and to pay me directly, and found out that that the rent came very short of the monthly mortgage payment , I got a local estate to come and value the property and they valued it less than £120K of the purchase price. I went to the police and told them about this, they said there is nothing they can do as this is a civil case I then instructed a solicitor to investigate and their findings showed that the property was bought and sold in a very short period less than a month, where the price sold at was over inflated by 120k, without any work done to the property. I told the mortgage company and told them there is no way I can afford the to pay the mortgage, this was around June 2009, The mortgage company repossessed the property and sold it in 2010, this is where the shortfall of 110K is. The conveyancing solicitor was part of a fraud, the solicitor is now no longer around, they were an LLP and I have tried to take them to court and sue them and claim damages from their indemnity insurance, but the indemnity insurers have said they will not cover this as this was a fraudulent act intentionally done by the solicitor. Now the bank has passed the debt to a number of debt collectors , this is the third one who is contacting me. To make things even worse, at the time, back in 2008 I actually bought three properties via this vendor, so I actually have three mortgage shortfalls that I need to deal with. I have been living with a lot of stress ever since this has happened, it is really getting me down, has affected my whole life, mentally, physically, affecting my family. I feel I have been let down by the whole system, I purchased these properties in good faith, thinking this will be an investment for the future but in reality it has been nothing but a nightmare. I need to find out what I can do to stop the debt or not pay the shortfall the debt collectors are asking for. Can anyone help and point me in the right direction

I need some advice as to what I should do... here are the details of my situation. I purchased in to a property scheme run by a vendor in Nov 2008 , where you pay the vendor £2000 and for this they find a buy to let property for you where the rent covers the mortgage payment , the vendor takes care of the purchase of the property, they take care of the solicitor, all the management, (renting, any bills) all bills after two years you have the option to sell the property or to continue to use their services. The Solicitor used was in this with the vendor, the valuation from the surveyor showed that the property was worth more than what I was paying After three months after purchasing the property, the rents stopped coming in I started to chase the vendor who told me they were having some cash flow problems and I will get the rents to cover the mortgage, this went on for a two to three months and soon the vendor had disappeared. I visited the property I had purchased and asked the tenant for the rent and to pay me directly, and found out that that the rent came very short of the monthly mortgage payment , I got a local estate to come and value the property and they valued it less than £120K of the purchase price. I went to the police and told them about this, they said there is nothing they can do as this is a civil case I then instructed a solicitor to investigate and their findings showed that the property was bought and sold in a very short period less than a month, where the price sold at was over inflated by 120k, without any work done to the property. I told the mortgage company and told them there is no way I can afford the to pay the mortgage, this was around June 2009, The mortgage company repossessed the property and sold it in 2010, this is where the shortfall of 110K is. The conveyancing solicitor was part of a fraud, the solicitor is now no longer around, they were an LLP and I have tried to take them to court and sue them and claim damages from their indemnity insurance, but the indemnity insurers have said they will not cover this as this was a fraudulent act intentionally done by the solicitor. Now the bank has passed the debt to a number of debt collectors , this is the third one who is contacting me. To make things even worse, at the time, back in 2008 I actually bought three properties via this vendor, so I actually have three mortgage shortfalls that I need to deal with. I have been living with a lot of stress ever since this has happened, it is really getting me down, has affected my whole life, mentally, physically, affecting my family. I feel I have been let down by the whole system, I purchased these properties in good faith, thinking this will be an investment for the future but in reality it has been nothing but a nightmare. I need to find out what I can do to stop the debt or not pay the shortfall the debt collectors are asking for. Can anyone help and point me in the right direction -

first of all to say hello to all users. i am new here be gentle . i have read the forum rules etc . feel free to say hello and if i can help i will. right down to the nitty gritty. i have recently discovered i had ppi with mbna on 3 accounts out the 6 they told me i had in total (possibly linked cards) they are investigating the 3 they have told me about. is it worth me sending sar requests for the others. just read some old posts regarding dishonest mbna online. or am i barking up the wrong tree here. grateful for any help or advice all the best

-

Hello, I would like to find a solicitor that would act to defend me in a litigation case - I would hope that mediation or a 'round table' discussion could be held prior to litigation. The case has had a Barristers opinion and that is 65% chance of success the claim value including damages and fees to date is circa £200K. I have previously had a large firm of solicitors dealing with it and felt frustrated with delays and lack of help. I want a small sole practitioner or similar. The claim is backed by DAS and paid for via insurance, the rate agreed previously was £201.00 ph. Please message me if you feel you can help and have the time to deal with this, a note the other party has sufficient funds to pay the damages/fees.

-

Hi, I've been looking at reclaiming PPI from a 2002 loan I got to buy musical equiptment. After being messed around claiming they couldn't find my account details I SAR'd my bank at the time and sifted through 1000+ pages of documentation in order to find my agreement number, 160 days after the initial SAR request I was eventually supplied my account detals. Long story short it was single payment / front loaded PPI payment. I did however run into difficulties paying the account and it was "written off (term as per transaction description) / defaulted at £520 in 31/07/2003. What I've since learned was that this debt was sold off to 1st Credit DCA, who subsequently persued me (and me simply not knowing any better thinking I was simply settling one of many debts I had from my younger years) I made an initial £26 payment on 31/05/2006 as a token of my eventual desire to pay said debt completely. I WAS AT NO POINT AWARE THIS WAS ACTUALLY THE BLACKHORSE ACCOUNT The following day (01/06/2006) while continuing to settle debts I called Black Horse and made what i was to believe was the final £520.85 payment.due on the old loan. After saving for a few months more I then contacted 1st Credit and paid the rest of the £525 debt they asked for. It has now come to light while I've checking old bank statements that Black Horse accepted the final settlment from me while actually not owning the debt having it been sold on to 1st Credit. Where do I stand in Scotland with regards timeframe to claim the full £525 payment from either party? Any advice would be appreciated

-

I moved into a new rental property 5 weeks ago. When I moved in I realised it was a pre-pay meter. I hadn't had one before and immediately called to ask to change to a DD account. I was told I would have to wait a month then have a credit check and then if approved move off. I called today to start that process and whilst I was on the phone the customer service rep performed an Experian credit check and told me I failed and I could not apply again for another 60 days. I logged onto Experian to see my report which is a 989 score out of a possible 999 - an almost perfect excellent rating. It shows a 989 because a couple of months ago I took out a small loan out but I am paying that off as I should and I hope to clear it early in a few months. The only other thing I can think of is it had not updated my electoral register information despite my council telling me on the phone today I am definitely on their list and they have said Experian should update their records this week. So I called British Gas again to enquire further why I had failed their check and they refuse to tell me....well in fact I was told they themselves do not know because she said it was all down to algorithms. Yes computer says no. So, can anyone let me know if British Gas demand a 999 scoring for Experian? And why the do I have to wait 60 days if all it is my electoral registration data had not updated as quickly as it should have? I mean...is that even legal that they force us wait so long? It seems to me just a flimsy excuse to extract more money out of me because of a previous tenant's failure to pay on time. Agh....

I moved into a new rental property 5 weeks ago. When I moved in I realised it was a pre-pay meter. I hadn't had one before and immediately called to ask to change to a DD account. I was told I would have to wait a month then have a credit check and then if approved move off. I called today to start that process and whilst I was on the phone the customer service rep performed an Experian credit check and told me I failed and I could not apply again for another 60 days. I logged onto Experian to see my report which is a 989 score out of a possible 999 - an almost perfect excellent rating. It shows a 989 because a couple of months ago I took out a small loan out but I am paying that off as I should and I hope to clear it early in a few months. The only other thing I can think of is it had not updated my electoral register information despite my council telling me on the phone today I am definitely on their list and they have said Experian should update their records this week. So I called British Gas again to enquire further why I had failed their check and they refuse to tell me....well in fact I was told they themselves do not know because she said it was all down to algorithms. Yes computer says no. So, can anyone let me know if British Gas demand a 999 scoring for Experian? And why the do I have to wait 60 days if all it is my electoral registration data had not updated as quickly as it should have? I mean...is that even legal that they force us wait so long? It seems to me just a flimsy excuse to extract more money out of me because of a previous tenant's failure to pay on time. Agh.... -

Hi I'm hoping I am posting this question in the right forum? My cousin who turned 50 in March passed away from a short cancer related illness. She was an only child and her mother, my aunt, is in her 80's. They had a joint savings account which they both contributed money into for more than 10 years and when she passed away the account had approximately £19,000. The estate has gone to probate and when the building society were informed, they sent a cheque direct to my aunt for the full amount. We assumed that as the account was in joint names the money would automatically be hers. However, the solicitor that is dealing with the probate has advised my aunt that the £19,000 should be included as part of the overall estate, which I understand exceeds £350,000. Question: As my aunt contributed to the savings account and as it was in joint names, should this still be included as part of the estate?

-

I've received a notice stating that my landlord is offering me suitable alternative accommodation and I shall be required to move. That was two weeks ago. 1 Previously the landlord has written to me stating that they cannot require me to move and will not require me to move. 2 No alternative has in fact been offered. I've done the obvious and emailed pointing out the above and also expressing surprise at receiving a notice without warning. I have had a reply stating that they have noted what I have written. Now, what do I do? I am a Housing Association tenant and have lived in my flat for over twenty years. They want me to move so that they can sell the property and move me to a cheaper area. Any advice appreciated, please.

I've received a notice stating that my landlord is offering me suitable alternative accommodation and I shall be required to move. That was two weeks ago. 1 Previously the landlord has written to me stating that they cannot require me to move and will not require me to move. 2 No alternative has in fact been offered. I've done the obvious and emailed pointing out the above and also expressing surprise at receiving a notice without warning. I have had a reply stating that they have noted what I have written. Now, what do I do? I am a Housing Association tenant and have lived in my flat for over twenty years. They want me to move so that they can sell the property and move me to a cheaper area. Any advice appreciated, please. -

Hello 1st post and I hope I'm posting in correct forum. if not could Mods please move post. The wife of a friend of mine has walked out a couple of weeks ago. Shes has walked away and left everything in limbo. Friend phoned the bank and arranged an appointment where they froze the joint account , opened a new account in his name only so he can have his wages paid in, pay bills / dd/so and mortgage etc Wife had a gym membership, He phoned the gym to tell them she had left, bank acc closed and they told him he was liable , so he set up new direct debit from new account and was going to pay. 1st payment from new account already been paid. Is he liable, can he cancel. any letter templates available Ideas or advice appreciated Many Thanks

.thumb.jpg.bf2f59e5260173230834ce3ad8015900.jpg)

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS