Showing results for tags 'application'.

-

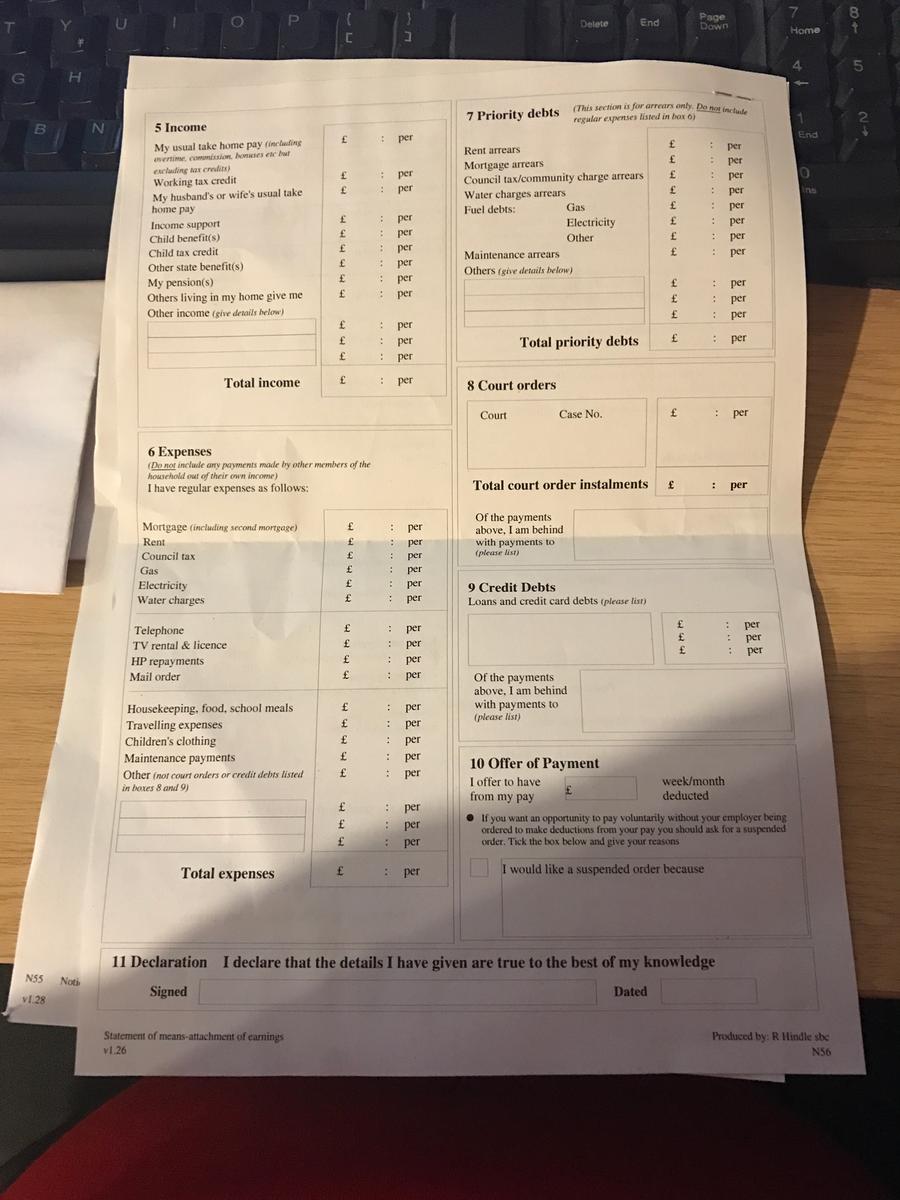

I have just gotten a Nottice of Application for Attachment of Earnings Order for a sum of just over £900 for CCJ issued in the CC busines Court Centre on behalf of Cabot Looking on my CC file i see a CCJ was obtained in summer 2015 for Cabot which after some research appears to be Welcome finance related. (i will contact Mortimer Clarke to confirm who the claimed creditor is but am pretty sure it isnt anyone else) It is the first time i have heard about this CCJ/debt. I returned my car to welcome finance in 2011 and changed address three times since then. I dont think ?I owed/owe them anything and I am not going to be paying £900 in any form if i can help it. I understood i had no debt to them but prior to returning the car under the agreement, I had had some arrears which i had cleared. My income is borderline for getting court fees paid An AOE could affect my job as i work for the government in a finance related role. I understand I can apply to have the CCJ put aside. I understand I could apply for a stay of the warrant I understand I can contact Welcome Finance for a Subject Access Request I have to reply to the application in eight days I don't think I had any PPI with Welcome Finance If I complete the N55 notice of AOE order Form do i make offer payment of an amount and then make the other application (vary warrant or overturn CCJ) or should i simply make an application to suspend and tick the box on the N55 saying I want to the order suspended because I have made that application. Or something else ? My income and expenditures are low and in the past i have made requests to vary judgements on grounds of low income that were accepted by courts after applying to stay warrant. but those were for debts i knew I owed and had had a chance to defend. Thank you in advance.

I have just gotten a Nottice of Application for Attachment of Earnings Order for a sum of just over £900 for CCJ issued in the CC busines Court Centre on behalf of Cabot Looking on my CC file i see a CCJ was obtained in summer 2015 for Cabot which after some research appears to be Welcome finance related. (i will contact Mortimer Clarke to confirm who the claimed creditor is but am pretty sure it isnt anyone else) It is the first time i have heard about this CCJ/debt. I returned my car to welcome finance in 2011 and changed address three times since then. I dont think ?I owed/owe them anything and I am not going to be paying £900 in any form if i can help it. I understood i had no debt to them but prior to returning the car under the agreement, I had had some arrears which i had cleared. My income is borderline for getting court fees paid An AOE could affect my job as i work for the government in a finance related role. I understand I can apply to have the CCJ put aside. I understand I could apply for a stay of the warrant I understand I can contact Welcome Finance for a Subject Access Request I have to reply to the application in eight days I don't think I had any PPI with Welcome Finance If I complete the N55 notice of AOE order Form do i make offer payment of an amount and then make the other application (vary warrant or overturn CCJ) or should i simply make an application to suspend and tick the box on the N55 saying I want to the order suspended because I have made that application. Or something else ? My income and expenditures are low and in the past i have made requests to vary judgements on grounds of low income that were accepted by courts after applying to stay warrant. but those were for debts i knew I owed and had had a chance to defend. Thank you in advance. -

Hi, first post on something I need a little help on please. I receieved a court claim about a credit card I took out 14 years ago but I had kept no records of it. I did a CPR and CCA request to get some documentation. What they sent through was a copy of the application form. All my details were legible within the white boxes of the form, strangely legible when compared to the rest of the form, but the surrounding areas with their information is illegible and very grey and pixalated. You can make out my signature, but not the date. They also sent me some terms and conditions as a separate photocopy. Am I right in thinking that pre 2007 it has to contain proof that the t's & c's were signed by me for it to be enforceable? I came across an old post in the forum about a similar issue and I'll quote it below, but does this apply too:

-

Thought it time I paid off and ditched my Vanquis card. Do not get me wrong it has been great with my credit profile. Had it for about three years, never missed a payment and have a Three Grand credit limit. So much for customer loyalty though, they point blank would not negotiate the APR, 59.9% So yesterday applied for a BarclayCard, eligibility checker stated 95% chance of being accepted. Went through the application, Digitally signed for it to come back as referred. Strange as 12 months ago did the same with Capital One and was instantly accepted with a two grand credit limit. Never missed any payment with any of my credit obligations for the last three years. Credit scores from the credit agencies mean SFA as each credit company have their own lending criteria. Now i know this is simply the automatic computer process wanting manual intervention from a human being. This was not an outright No and will be probably be accepted, But: What causes these referrals as a matter of interest??

-

READ MORE HERE: https://www.gov.uk/government/publications/armed-forces-veterans-badge-application-form

READ MORE HERE: https://www.gov.uk/government/publications/armed-forces-veterans-badge-application-form -

I purchase a car on 29th Sept 2016 from a garage in Surrey. The car is a "lemon" when I went on the companies house to see where to send my letter of complaint under the Consumer Credit Act 1985 I found that it was dissolved in Nov 2016. I downloaded the DS01 form and found that it had been signed and dated 22 August 2016. It means that the garage sold me a car when it should not have been trading under that name. Am I right ? They may have got away with me claiming my money back from their Limited Company but has the director been acting according to the Law ? If not , who should I notify so that he gets prosecuted ? Companies House ? The Inland Revenue ? Your valuable expert advice is appreciated . Many thanks !!

-

I am currently living apart from my wife. We are planning to get divorced,but have not begun proceedings, yet. Neither are we legally separated. However, all expenses are currently separate. For the purpose of completing the tax credit application form, would I be considered single or married?

-

Hi, Can anyone offer me any advice on an issue I have with the FOS. I took out life and critical illness cover through a tied broker in 2012. In 2016 I claimed and my claim was turned down by the insurer as they did not know about surgery I'd had prior to applying for insurance. Trouble is both me and the wife know we told the brokers agent all about the surgery on the night he came to get our signatures after checking the application. I made my initial call on the 14/4/12, their agent visited my home on 17/4/12. The FOS got involved after my complaint to the company was turned down. The original sales phone call in which I tell the salesman about my surgery is 'missing'. The FOS adjudicator requested the application and signed declaration from the brokers. What she received (and accepted!) was amazing. Pages 1 to 5 were missing and the last 4 pages (the declaration) were scanned in such a way as to obscure the date in the top left hand corner. There were no other dates on any of the remaining pages. It took me 4 subject access requests to finally receive the complete form including dates. Their excuse for their inability to supply what I'd asked for previously was that their scanner could not scan complete pages the right way up!? On each of the replies to my requests the broker states the completion date of the form as 16/4/12 The FOS is not upholding my complaint. I've always maintained that I (and my wife who took out cover at the same time) told the broker and agent all about the surgery and that therefore, knowing that it was unlikely the insurer would offer me cover, the broker and/or agent altered the application without our knowledge. I even had a photo dated 2 days prior of the 4" scar on my part shaven head clearly visible on the night of 17/4/12! Turns out the date on the missing 5 pages was the 19/4/12 - a whole 2 days after my signature was obtained on the declaration. The date on the declaration was 16/4/12. This appears to be the date the declaration pages were sent to the agent and therefore the declaration was produced on or before 16/4/12. This is where I'd really appreciate some advice - the FOS Adjudicator and Ombudsman actually used the application/declaration in their decision. Can they do this?, should they do this? and where do I go from here? Thanks

Hi, Can anyone offer me any advice on an issue I have with the FOS. I took out life and critical illness cover through a tied broker in 2012. In 2016 I claimed and my claim was turned down by the insurer as they did not know about surgery I'd had prior to applying for insurance. Trouble is both me and the wife know we told the brokers agent all about the surgery on the night he came to get our signatures after checking the application. I made my initial call on the 14/4/12, their agent visited my home on 17/4/12. The FOS got involved after my complaint to the company was turned down. The original sales phone call in which I tell the salesman about my surgery is 'missing'. The FOS adjudicator requested the application and signed declaration from the brokers. What she received (and accepted!) was amazing. Pages 1 to 5 were missing and the last 4 pages (the declaration) were scanned in such a way as to obscure the date in the top left hand corner. There were no other dates on any of the remaining pages. It took me 4 subject access requests to finally receive the complete form including dates. Their excuse for their inability to supply what I'd asked for previously was that their scanner could not scan complete pages the right way up!? On each of the replies to my requests the broker states the completion date of the form as 16/4/12 The FOS is not upholding my complaint. I've always maintained that I (and my wife who took out cover at the same time) told the broker and agent all about the surgery and that therefore, knowing that it was unlikely the insurer would offer me cover, the broker and/or agent altered the application without our knowledge. I even had a photo dated 2 days prior of the 4" scar on my part shaven head clearly visible on the night of 17/4/12! Turns out the date on the missing 5 pages was the 19/4/12 - a whole 2 days after my signature was obtained on the declaration. The date on the declaration was 16/4/12. This appears to be the date the declaration pages were sent to the agent and therefore the declaration was produced on or before 16/4/12. This is where I'd really appreciate some advice - the FOS Adjudicator and Ombudsman actually used the application/declaration in their decision. Can they do this?, should they do this? and where do I go from here? Thanks -

Hi folks, i need somebody to inform me what the empty spaces are needing as ive re read this block several times and its not clear to me.

Hi folks, i need somebody to inform me what the empty spaces are needing as ive re read this block several times and its not clear to me.

-

Hi All, I am in a bit of a pickle at the moment, I felt I was finally able to afford my council flat that I have lived in for over 15 years, I put in my first RTB application March 2015, and a valuation was done for the property, after the valuation came out, I found that I was not able to afford it even after the London discounts so I didn’t take up the offer, fast track November 2016, the same year I made another application and this time around the price of the flat had reduced by £100k as per the new valuation done in November 2016, so I took up the offer, applied for a mortgage and got it approved etc, to my horror council wrote to me last week saying that they have now revised the offer from the council where they have changed all the figures and have now decided to use the first valuation which is 100k more than the second one. I am a little lost now and do now know what to do. I am already out of pocket after spending on solicitors and mortgage brokers. Thanks in advance.

Hi All, I am in a bit of a pickle at the moment, I felt I was finally able to afford my council flat that I have lived in for over 15 years, I put in my first RTB application March 2015, and a valuation was done for the property, after the valuation came out, I found that I was not able to afford it even after the London discounts so I didn’t take up the offer, fast track November 2016, the same year I made another application and this time around the price of the flat had reduced by £100k as per the new valuation done in November 2016, so I took up the offer, applied for a mortgage and got it approved etc, to my horror council wrote to me last week saying that they have now revised the offer from the council where they have changed all the figures and have now decided to use the first valuation which is 100k more than the second one. I am a little lost now and do now know what to do. I am already out of pocket after spending on solicitors and mortgage brokers. Thanks in advance. -

My Daughter has be hassled by Shoosmiths/ARC over an alleged debt with Egg, this started in March 2011 several DCA's have written and to each we have sent a S78 request, and had nothing returned other than a blank 'example' agreement. A couple of years ago Shoosmiths issued court papers to which I filed a defence on her behalf, pointing out that S78 had not been complied with and that a multitude of DCA's and solicitors had written a range of letters alleging debts but for a number of varying amounts. Shoosmiths responded by withdrawing the court application, out off the blue today we get a letter threatening an application for Summary Judgment, and wanting us to set up an agreement for repayment with them. My Daughter had a nervous breakdown several years ago 2007/8 and genuinely has no recollection of these debts and I have been managing them on her behalf, in may cases PPI has more than covered the debt but Shoosmiths have been particularly difficult to deal with and if this is a genuine debt then it will almost certainly have PPI attached to it, but apart from a bare minimum of information they have given me nothing to work with. I feel like calling their bluff, but the amount they are claiming is around £2k0 and if genuine is not a single debt but a number rolled into one, or has a significant amount of charges added. What would be my best course of action? Thanks in advance.

My Daughter has be hassled by Shoosmiths/ARC over an alleged debt with Egg, this started in March 2011 several DCA's have written and to each we have sent a S78 request, and had nothing returned other than a blank 'example' agreement. A couple of years ago Shoosmiths issued court papers to which I filed a defence on her behalf, pointing out that S78 had not been complied with and that a multitude of DCA's and solicitors had written a range of letters alleging debts but for a number of varying amounts. Shoosmiths responded by withdrawing the court application, out off the blue today we get a letter threatening an application for Summary Judgment, and wanting us to set up an agreement for repayment with them. My Daughter had a nervous breakdown several years ago 2007/8 and genuinely has no recollection of these debts and I have been managing them on her behalf, in may cases PPI has more than covered the debt but Shoosmiths have been particularly difficult to deal with and if this is a genuine debt then it will almost certainly have PPI attached to it, but apart from a bare minimum of information they have given me nothing to work with. I feel like calling their bluff, but the amount they are claiming is around £2k0 and if genuine is not a single debt but a number rolled into one, or has a significant amount of charges added. What would be my best course of action? Thanks in advance.

-

Will not name the company (for now) it's the procedure I am trying to understand. No outstanding amount on account (may be a variation on the amount used due to estimated readings but it wouldn't be a lot but essentially all bills have been paid, nothing was outstanding until now. Utility company write stating that they need to check the meter for safety reasons and quote 'Must Inspect' G4S are those wanting to read the meter, however some years before a member of g4s threatened the householder at the time that if they didn't let them in they'd get a warrant and break in....this from a meter reader and before any ''must inspect' notices had been issued, meter reader dispensed, complaint made with the householder stating any further visits for meter read would need to be anyone other than G4S... Fast Forward a couple of years to end of 2016, Must Inspect letters sent, but these were from G4S and were ignored (see above) Utility company write stating they must be contacted within 7 days to make an appt to check the meter or action will be taken, they were contacted about 14 days later and put on notice that both the utility company and the service distribution company had been in the property just 2 months earlier due to a power outage and where the meter had been checked/ main fuse taken out, tested, put back in, sealed and the road dug up for a week (generators etc) both the distribution company and the utility company had been in and checked the meter safety etc.... At around the same time a letter from G4S arrives stating the householder needs to get in touch as they needed to visually check the meter, the utility company were called again (not G4S) and the same conversation again (paragraph above) and they said not to worry, they'd get it dropped etc. Fast forward to this year, utility company process a bill, usual bill, standing charge and usage..10 days later the householder goes to pay the bill, but when going to notices a further charge of in excess of £50 ....there is nothing on the bill or the account to show as to why the additional price so a call was placed to the Utility company and where they stated 'oh, thats for the warrant application fee' Discussion ensues, they stated they could see contact had been made (as per their and G4's requests) but that the meter still needed to be checked???? The time difference between the letter requesting contact to the time the warrant application fee was applied to the account was 75 days ... G4S requested to remove the application, they state it can only come from the utility company and that as they had heard nothing the warrant application was still to go ahead. Utility company contacted again, complaint raised to a different department and where they appeared to be less than helpful, householder felt somewhat threatened/intimidated (they're registered disabled both physically and mental health) utility company are aware of the status re disabled (householder is registered for priority assistance should there be a outage) They refused to remove the fee, said it still applied, they could see that contact had been made when requested but that G4S needed to check the meter, they acknowledged that the property had been visited by them and the distribution company but still the meter needed to be checked as they'd tried for some time now (yes but it had been checked) Utility company seemed altogether oblivious to any of the points raised re: 1:/Why the fee had been added when no notification as to a court date for the application had been made and that had not the householder queried the additional fee on their newest bill they would have been oblivious to the date at court to see a warrant (only 3 weeks from the time of the fee being added (so not long to go now for the householder) 2:/ Why the utility company acknowledged that when requested they be contacted that they were contacted which in essence nullifies their 'if you dont contact us we'll do......) and where situation explained and they appeared to have accepted it that they then reverse that acceptance. 3:/ Why the extra fee levied does not correspond to their online 'charges' for the same 'application' 4:/ Why they or agents acting on their behalf (G4S) took (a) 75 days to apply the fee and presumably make an application to the court and why they did not inform the householder when the court date was or indeed what court it was to be at? 5:/ Why when they can see both themselves and the distribution company have been in the property and at the meter (checked/resaled/) previous to their warrant threats that this appears not to register with them --- The final contact from the elongated and somewhat intimidating/threatening Utility company wasa followed up by an email to the householder stating 'thanks but we're not withdrawing the warrant and that g4s would still need to attend. ... Further to that, there are a couple of other points to ponder and as yet the householder has not put this to the utility company and any advice confirmation (if applicable) be given. 1:/ G4S as a meter reading company no longer exist, they were sold with the sale complete in January 17, so any court application and when G4S were called a few days ago and where they answered the call as G4S and spoke regarding a reference number on their letter from last year? would need to be from the American company that purchased G4S? 2:/ The legal requirement to inspect a meter was repealed in 2016, becoming defunct from April 1st 2016 , yet 9 months later the Utility company in their letters stated they are 'required by law to check 'your' meter every two years and where you are required to allow them access. I have read the repeal on Ofgem's site, it's quite clear. (they also state somewhere that any utility company using the 2year argument post April 2016 would be pursued Calls to the Utility Company were recorded and they were informed as much, I've listened to some of them, they're dreadful listening and I as an individual could clearly hear the distress in the householders voice and also detect the undeniable intimidatory tone from the Utility company employees The Householder going to court would be detrimental to their health, physically difficult, mentally pretty much impossible but court they will go, better to be avoided but when the above is the situation any homeonwer/tenant would want to protect their home from what is pretty much unlawful entry. Deb Any thoughts ? views? re the Must Inspect repeal?

-

I moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out. I don't live in Scotland anymore. Is it possible to submit a summary application by post or electronically? moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out can someone please suggest a solicitor that can submit the summary application on my behalf and elp handle the process?

I moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out. I don't live in Scotland anymore. Is it possible to submit a summary application by post or electronically? moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out can someone please suggest a solicitor that can submit the summary application on my behalf and elp handle the process? -

After one applies for jobseekers allowance, they are invited to their first appointment to sign their application. If there are topics that need to be expanded, or for example special circumstances that cannot be answered with a simple yes/no, can one attach a written statement to be sent to the decision makers? Thanks

-

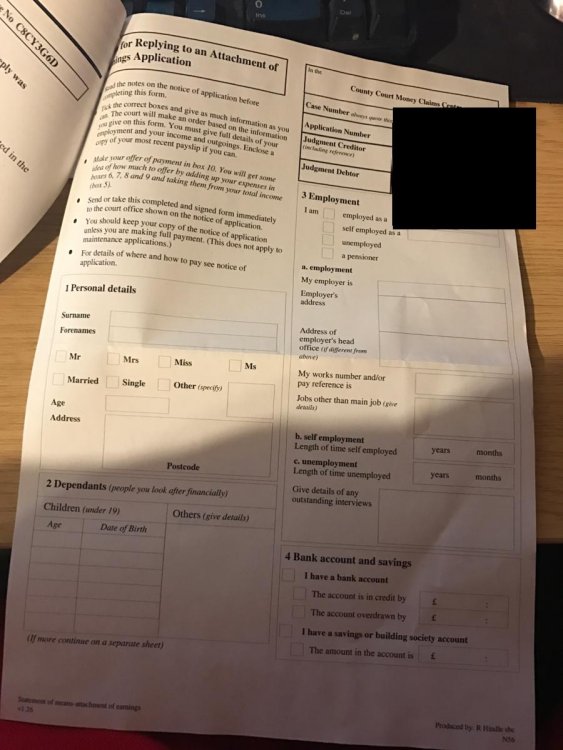

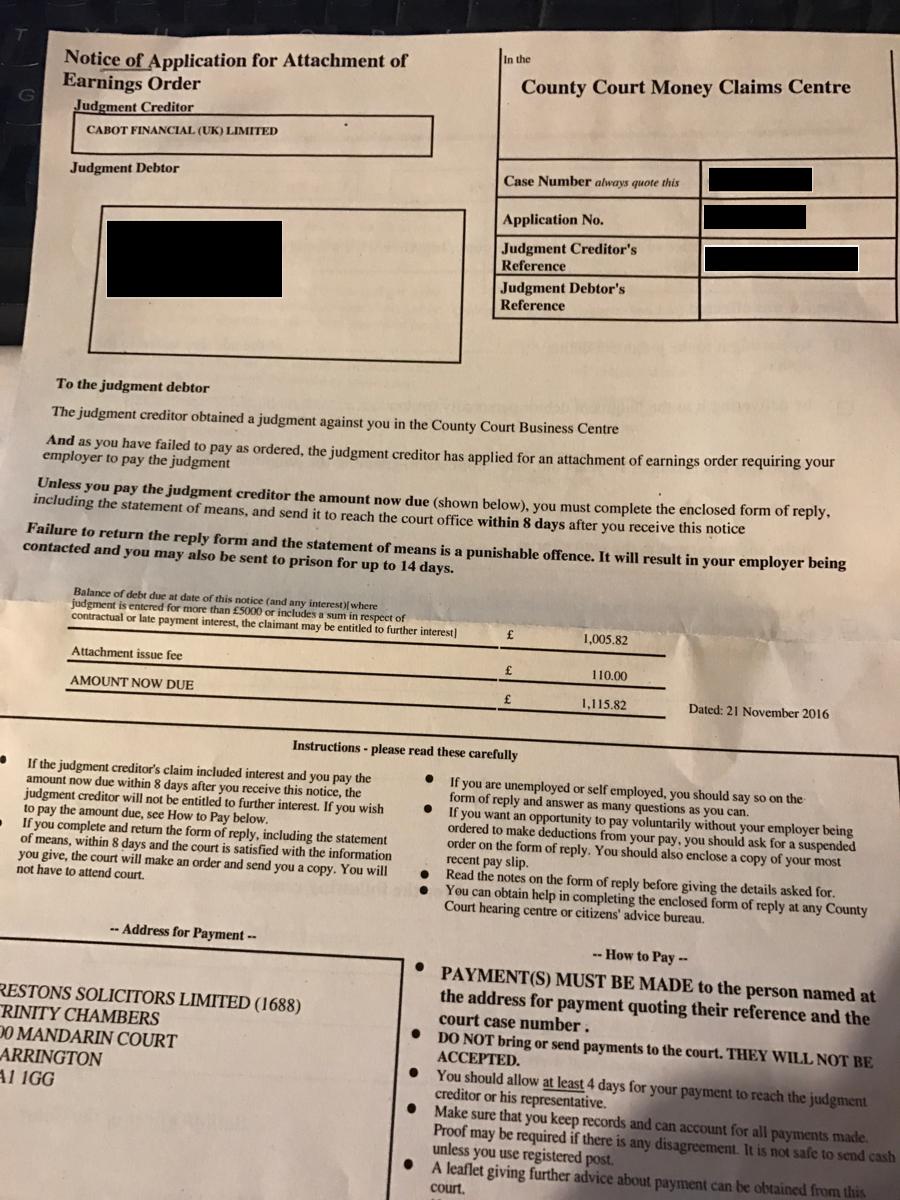

First I've heard of this, I haven't received anything else regarding this matter, isn't this something that I have to attend court for? if so why wasn't nothing stated nor issued to me? I have to pay £1005.82+£110 fee within 8 days to a company I don't even know about? or even know what money they are trying to get from me? Over the past few years I've been working hard to pay back things i genuinely do owe, and for this to pop up is just annoying.. I work a part time 30 hour a week job, any ideas? Obviously if the debt is true I'll pay, but from how long ago could it go back to?

First I've heard of this, I haven't received anything else regarding this matter, isn't this something that I have to attend court for? if so why wasn't nothing stated nor issued to me? I have to pay £1005.82+£110 fee within 8 days to a company I don't even know about? or even know what money they are trying to get from me? Over the past few years I've been working hard to pay back things i genuinely do owe, and for this to pop up is just annoying.. I work a part time 30 hour a week job, any ideas? Obviously if the debt is true I'll pay, but from how long ago could it go back to?

-

I have received a letter this morning at my rented address for a notice of application for attachment of earnings order from Cabot Financial (UK) Ltd. I migrated to Australia in 2011 but had to return in Aug 2015 due to visa refusal but although this letter has a case number and application number as well as a judgement creditors reference I actually have no idea what this debt is supposed to be for as this is the first correspondence I have received at this address and I have been here since August 2015. It says unless I pay the judgement creditor within 8 days I must complete the enclosed form of reply including the statement of means and send it to the court office within 8 days after receiving this notice. I'm not sure what this debt is for which is my main concern as there is no reference to it nor what date this judgment was carried out. It says the address for payment is Restons Solicitors Limited Warrington and that's about as much as I know

I have received a letter this morning at my rented address for a notice of application for attachment of earnings order from Cabot Financial (UK) Ltd. I migrated to Australia in 2011 but had to return in Aug 2015 due to visa refusal but although this letter has a case number and application number as well as a judgement creditors reference I actually have no idea what this debt is supposed to be for as this is the first correspondence I have received at this address and I have been here since August 2015. It says unless I pay the judgement creditor within 8 days I must complete the enclosed form of reply including the statement of means and send it to the court office within 8 days after receiving this notice. I'm not sure what this debt is for which is my main concern as there is no reference to it nor what date this judgment was carried out. It says the address for payment is Restons Solicitors Limited Warrington and that's about as much as I know -

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance -

I failed the PIP medical (by a mere few points). I'd gone through the Mandatory Reconsideration and had posted the paperwork to lodge an appeal before the imposed deadline. On chasing this up, I found that the appeal paperwork had not been received by the tribunal. Thankfully, I had help from a welfare rights worker at my local housing association, who contacted the tribunal and managed to fax them a copy of said paperwork. It's really lucky that I chased this up. They will now process my application and get back to me with a date (hopefully not too far into the future). Please, please, please keep on top of your paperwork. I'm sure it's very rare for important letters to disappear in the post, but it does happen. If you have someone to help you, ask them to confirm that everything is proceeding as expected. If I hadn't asked my welfare rights worker if they'd received any news, I'd be none the wiser and my appeal would be going nowhere.

- 4 replies

-

- 1

-

-

- apparently

- appeal

- (and 2 more)

-

ello theoldgit : I have come across one of your replies in regards to Visa Application UK I was in UK under Tier 1 PSW permit until February 2014 , and had personal loans of GBP 2000 and un paid credit cards and phone contracts not more than 6000 GBP in total, I could not repay them since i left the country due to expired leave to remain . and I have checked on the trustonline.org.uk - i do not have any CCJ against me I am concerned this debt which I owe to the Creditors will hinder my new tier 2 (general) visa application Kindly advise me, will this debt will come under General Grounds of refusal - under Deliberate Debting your reply and advise will be really helpful and appreciated

-

Hi please can you help me, I have received a court claim from Arrow from Northampton Court, for the claim of £4900, issued 8 days ago was a bank loan issued opened up in 1998, , last know payment was 2008/9. I have not acknowledged this debt, or any comms from me to Arrow I have filed online that I will contest this claim, hopefully on Limitation Act 1980 can I now send off a CPR18 request to their solicitor ? what is should I be asking for in the CPR 18 ? All of the below 5 details ? 1.The agreement/contract, including the specific Terms at the point the alleged Agreement was made and any subsequent changes. 2.The deed of assignment 3.The notice of assignment 4.The default warning letter 5.The default notice (CPR 31.14 Request only worth doing if debt is over 10k. I may have this totally wrong..) I have read that some people think that a CC Agreement request letter is not really useful (sorry, I cannot remember their reasons for stating this) Is it worth it your opinion to request CCA from the DCA? shall I ring up my old bank and ask them for the last payment date ? thanks for all help in advance

-

I'm looking for some advice please . I recently applied for a mortgage, and was asked initially over the phone "have you ever had any CCJS or IVAS". The answer was and is no. I was given an agreement in principle. This has now progressed to full application stage , after passing a full credit check. I have received a check list to sign and return to the lender. One of the first questions asks "Have you ever been subject to county court judgements (CCJs) , defaults or a repossession"? Is this asking if I have had a CCJ, county court default judgement or county court repossession order?, or is it asking if I have ever had credit defaults? The answer to that is yes, all unsecured, all now off my file and statute barred. After an initial panic I believe it is all County Court order related but I would like your opinions please.

-

Hi. I have just registered, although I have been on this forum many times over the years as a guest. I am in a bad place, i feel embarrassed. After my marriage broke down this year my ridiculous reaction to the stress and sorrow was to start gambling online and I am now in a position where I owe £30k. I have taken, all in the space of 5 months, 4 x £7.5k loans and have lost it all on a crazy impulsive online gambling spree. I am absolutely disgusted at myself about this behaviour so please do not act on your urge to tell me how wrong this was. I know more than you can imagine. I have never, i repeat EVER gambled in the past and I am a 52 year old man. I am not and have never been a gambler which is why this is even more difficult to make sense of. I had zero debt just 12 months ago. My question in this instance is this: Given the way this debt was taken out, ie in a very short period, spent on gambling (with the ridiculous hope of making losses back each time) and the fact that I exaggerated my income by about 25% in my loan applications, can this lead to a Fraud or criminal prosecution? I didnt lie about anything else, and I stated my other loans at each new application. Can the banks or the official receiver (i will be going BR ) find this behaviour so wrong that I could be charged? I understand that I will most definitely be having a BRU. The use of the funds is clearly documented in bank statements. ie I didnt take loans out and cash them out or purchase things, or give to friends or go on holiday. It was all used on gambling over a very short period. Please only reply if you are aware of English Law regarding fraud (if this is in fact fraud) and under which section of the Fraud Act? I really need some solid knowledgeable advice as I am extremely stressed. I have been reading about S1, S2 of the Fraud Act and searching online but can not really find something clear to suggest whether this is something that, a) can be prosecuted, and b) is in fact prosecuted. Some posts in other forums state that they have never heard of anybody being prosecuted for lying or exxageratin on a consumer loan application but I find that hard to believe? Why would the CPS have a Fraud Act and why would they not pursue it if a bank requested them to? If anybody has been prosecuted please share your experience or some points, or PM me if you are not comfortable to post online. If this is in the wrong forum please move to the appropriate one. Thank you

Hi. I have just registered, although I have been on this forum many times over the years as a guest. I am in a bad place, i feel embarrassed. After my marriage broke down this year my ridiculous reaction to the stress and sorrow was to start gambling online and I am now in a position where I owe £30k. I have taken, all in the space of 5 months, 4 x £7.5k loans and have lost it all on a crazy impulsive online gambling spree. I am absolutely disgusted at myself about this behaviour so please do not act on your urge to tell me how wrong this was. I know more than you can imagine. I have never, i repeat EVER gambled in the past and I am a 52 year old man. I am not and have never been a gambler which is why this is even more difficult to make sense of. I had zero debt just 12 months ago. My question in this instance is this: Given the way this debt was taken out, ie in a very short period, spent on gambling (with the ridiculous hope of making losses back each time) and the fact that I exaggerated my income by about 25% in my loan applications, can this lead to a Fraud or criminal prosecution? I didnt lie about anything else, and I stated my other loans at each new application. Can the banks or the official receiver (i will be going BR ) find this behaviour so wrong that I could be charged? I understand that I will most definitely be having a BRU. The use of the funds is clearly documented in bank statements. ie I didnt take loans out and cash them out or purchase things, or give to friends or go on holiday. It was all used on gambling over a very short period. Please only reply if you are aware of English Law regarding fraud (if this is in fact fraud) and under which section of the Fraud Act? I really need some solid knowledgeable advice as I am extremely stressed. I have been reading about S1, S2 of the Fraud Act and searching online but can not really find something clear to suggest whether this is something that, a) can be prosecuted, and b) is in fact prosecuted. Some posts in other forums state that they have never heard of anybody being prosecuted for lying or exxageratin on a consumer loan application but I find that hard to believe? Why would the CPS have a Fraud Act and why would they not pursue it if a bank requested them to? If anybody has been prosecuted please share your experience or some points, or PM me if you are not comfortable to post online. If this is in the wrong forum please move to the appropriate one. Thank you -

I hope I am posting in the right place. Wayne has been the sole tenant of this little flat for 18 years. We are not married, but do live together. I have never been on the tenancy. I am on the electoral roll (the bit that is private) and the Council Tax know I am here because Wayne had to write to them back along to give up his single person occupancy discount. Wayne applied to buy his flat back in February, and an energy surveyor has already been. He had a letter to tell him that the District Valuer will contact him to make an appointment. RTB2 admitting his Right to Buy has not yet been received. He has been to a broker and he will arrange a mortgage for Wayne, even though Wayne has two small debts that have been registered. These are $501 to Halifax Building Society (now through a debt collection agency). He closed his account in 2007 and unbeknown to him they added bank charges. Over the years they have added up to this amount. Wayne refuses to pay this. They entered a note on his credit file in 2012! And about 9 years ago he had a load from Provident. He handed over the payments regularly, but rarely saw his book. It was always "being updated by Head Office". Then the agent left and Provident came knocking after the money that she had pocketed! Wayne went mad and actually went and had a go at the thief at her other job in a shop, in front of her manager. He never heard from them again, but then when he had his credit check done by the broker, both came up,. Last Monday Wayne was at work, there was a hammering at the door. I opened the door to a burly great bloke and an official looking lady. They asked where Wayne was and I told them he was at work. The man said they were from the Council´s investigation team and they were investigating fraud? I told them they needed to speak to Wayne as it was nothing to do with me. Wayne duly spoke to them, and the lady told him that every time an RTB application was received, they had to investigate the applicant to help prevent fraud. She arranged to call back on Friday, today. She turned up with the same gentleman as before. The first thing the man said was "we have credit checked you and found two debts, and this may prevent your application to buy from being approved!", Wayne looked at me in surprise, so I simply said the mortgage broker said this wasn´t a problem, and I cannot see how this can affect his Right to Buy and in any case Wayne has argued these two debts and he will Tell you about them. The man accused me of being aggressive! Anyway we got past that bit and he denied that he said this! He was asked a series of questions, showed his passport as ID, had his photo taken. The last question before they left, was "have you ever benefitted from the RTB discount before?" Wayne answered honestly "no". The man said "if you are absolutely sure that you have answered honestly ... pause... then please sign this form". Wayne signed. Now, in 1984 I bought my Council flat from this Council under the RTB scheme. Years down the line I sold it and bought another property with my then partner. We split up and the property was sold. Shortly after that in 2006 I met Wayne and we´ve been an item ever since. (I can´t say "girlfriend and "boyfriend" I am 54 and it just doesn´´t sound right!). I am not anything to do with this application, it´s Wayne´s. We are not married and like anyone else we could split up in the future. Without wanting to sound mercenary, I have an elderly aunt/godmother with a house in the New Forest who has not long to go and I am a beneficiary of her will, and I want to buy my own place when the time comes. Therefore I will not benefit from this, Wayne has a much younger brother with learning difficulties and he wants to leave it to him. I am very worried that they are going to stop his RTB because I have already had an RTB before. I´m pretty certain they can´t because we are not married. The other thing was they asked NOK - well, his mother is bonkers, as is his younger brother and his older brother Albert, he rarely sees. So he said me. I´ve told him to ring them and get that changed to Albert. Sorry for long post, but lots went on today! Can anyone see any pit falls here? This is just a case of a long term tenant wanting to exercise his RTB. Can they really stop this because his "girlfriend" had RTB before?

I hope I am posting in the right place. Wayne has been the sole tenant of this little flat for 18 years. We are not married, but do live together. I have never been on the tenancy. I am on the electoral roll (the bit that is private) and the Council Tax know I am here because Wayne had to write to them back along to give up his single person occupancy discount. Wayne applied to buy his flat back in February, and an energy surveyor has already been. He had a letter to tell him that the District Valuer will contact him to make an appointment. RTB2 admitting his Right to Buy has not yet been received. He has been to a broker and he will arrange a mortgage for Wayne, even though Wayne has two small debts that have been registered. These are $501 to Halifax Building Society (now through a debt collection agency). He closed his account in 2007 and unbeknown to him they added bank charges. Over the years they have added up to this amount. Wayne refuses to pay this. They entered a note on his credit file in 2012! And about 9 years ago he had a load from Provident. He handed over the payments regularly, but rarely saw his book. It was always "being updated by Head Office". Then the agent left and Provident came knocking after the money that she had pocketed! Wayne went mad and actually went and had a go at the thief at her other job in a shop, in front of her manager. He never heard from them again, but then when he had his credit check done by the broker, both came up,. Last Monday Wayne was at work, there was a hammering at the door. I opened the door to a burly great bloke and an official looking lady. They asked where Wayne was and I told them he was at work. The man said they were from the Council´s investigation team and they were investigating fraud? I told them they needed to speak to Wayne as it was nothing to do with me. Wayne duly spoke to them, and the lady told him that every time an RTB application was received, they had to investigate the applicant to help prevent fraud. She arranged to call back on Friday, today. She turned up with the same gentleman as before. The first thing the man said was "we have credit checked you and found two debts, and this may prevent your application to buy from being approved!", Wayne looked at me in surprise, so I simply said the mortgage broker said this wasn´t a problem, and I cannot see how this can affect his Right to Buy and in any case Wayne has argued these two debts and he will Tell you about them. The man accused me of being aggressive! Anyway we got past that bit and he denied that he said this! He was asked a series of questions, showed his passport as ID, had his photo taken. The last question before they left, was "have you ever benefitted from the RTB discount before?" Wayne answered honestly "no". The man said "if you are absolutely sure that you have answered honestly ... pause... then please sign this form". Wayne signed. Now, in 1984 I bought my Council flat from this Council under the RTB scheme. Years down the line I sold it and bought another property with my then partner. We split up and the property was sold. Shortly after that in 2006 I met Wayne and we´ve been an item ever since. (I can´t say "girlfriend and "boyfriend" I am 54 and it just doesn´´t sound right!). I am not anything to do with this application, it´s Wayne´s. We are not married and like anyone else we could split up in the future. Without wanting to sound mercenary, I have an elderly aunt/godmother with a house in the New Forest who has not long to go and I am a beneficiary of her will, and I want to buy my own place when the time comes. Therefore I will not benefit from this, Wayne has a much younger brother with learning difficulties and he wants to leave it to him. I am very worried that they are going to stop his RTB because I have already had an RTB before. I´m pretty certain they can´t because we are not married. The other thing was they asked NOK - well, his mother is bonkers, as is his younger brother and his older brother Albert, he rarely sees. So he said me. I´ve told him to ring them and get that changed to Albert. Sorry for long post, but lots went on today! Can anyone see any pit falls here? This is just a case of a long term tenant wanting to exercise his RTB. Can they really stop this because his "girlfriend" had RTB before? -

This was my first application for PIP, and received a text to say I have been awarded it and a I don't have to do anything, they will pay my money into my bank. I had decided if they called me for a face to face I was just going to drop it......as could not face going and too ashamed to take anyone with me as I don't like people knowing how I feel. Is there any way I can find out how I got the points? Is there a form I can ask for? This will be useful when a review comes through as I'll know exactly how I was awarded it, if you get my drift? Thank in advance for any help offered. Miss (less) Anxious

-

Hi, hope this is the most relevant forum, if not please move. Try as might, attempted to find out answer to my query but my LA does not give any details on this subject. Nor does there appear to be any legal website giving law surrounding! However,as the title says, due to parking problems some years ago, our road/close/avenue, is a residential parking permit area. In addition, each resident is allowed to apply for upto 2 visitor passes. Parking, even with permits, now seems to becoming a problem again. My question is quite simply, is it possible to apply for residential disabled parking bay within a residential permit parking area? Different LA seem to have different approaches to this, but as previously mentioned nothing on my LA website, merely blue badge information. I am in possession of blue badge, as are a couple of other residents, but the added difficulty is our next door neighbour who, if the opportunity arises, parks his vehicle over 2 spaces (there are no marked parking spaces), causing us to seek at times a parking space 2 or 3 times distance from where we are normally able to park as close to our flat, although still within residential parking area. Wondering if any readers had/have similiar problems ways or resolving. Grateful for any responses and advice.

Hi, hope this is the most relevant forum, if not please move. Try as might, attempted to find out answer to my query but my LA does not give any details on this subject. Nor does there appear to be any legal website giving law surrounding! However,as the title says, due to parking problems some years ago, our road/close/avenue, is a residential parking permit area. In addition, each resident is allowed to apply for upto 2 visitor passes. Parking, even with permits, now seems to becoming a problem again. My question is quite simply, is it possible to apply for residential disabled parking bay within a residential permit parking area? Different LA seem to have different approaches to this, but as previously mentioned nothing on my LA website, merely blue badge information. I am in possession of blue badge, as are a couple of other residents, but the added difficulty is our next door neighbour who, if the opportunity arises, parks his vehicle over 2 spaces (there are no marked parking spaces), causing us to seek at times a parking space 2 or 3 times distance from where we are normally able to park as close to our flat, although still within residential parking area. Wondering if any readers had/have similiar problems ways or resolving. Grateful for any responses and advice. -

Hello Friends, Can you tell me whether the UKBA service of assessing visa application is subject to general consumer laws or not ? And if so , can I raise a claim in court, six years after I was wronged by them. they had made and admitted their mistake in assessing my application but refused to refund my air travel ticket saying that they advise applicants not to book ticket in advance. However I don't think I am bound by their advise and that I want to claim this in court, five years after the incident.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS