Search the Community

Showing results for tags 'ltd'.

-

Hi guys I have received a parking charge of 100 to be paid in 28 days or 60 if paid in 14 days. I received this just after midnight. I believe that this is unfair as I parked there only for a maximum of 15 minutes to drop my wife and 9months old daughter. It was late in the evening and it was dark. The area is known for drug dealings and drug addicts loitering. I didn't wanted to walk there during that late hours with my daughter and wife. I decided to park near by which is a private road just to drop my family and luggage as we were coming back from holiday. This is the only way to get to access to my flat as it is a new development. By the time I come back to move my car I got a ticket. Kindly advice me on the grounds I can appeal. Thanks Sri

Hi guys I have received a parking charge of 100 to be paid in 28 days or 60 if paid in 14 days. I received this just after midnight. I believe that this is unfair as I parked there only for a maximum of 15 minutes to drop my wife and 9months old daughter. It was late in the evening and it was dark. The area is known for drug dealings and drug addicts loitering. I didn't wanted to walk there during that late hours with my daughter and wife. I decided to park near by which is a private road just to drop my family and luggage as we were coming back from holiday. This is the only way to get to access to my flat as it is a new development. By the time I come back to move my car I got a ticket. Kindly advice me on the grounds I can appeal. Thanks Sri -

Name of the Claimant: Civil Enforcement Ltd Date of issue: 13th January 2017 Date to acknowledge = 31.01.2017 DAte to submit defence = 4pm 14.02.2017 What is the claim for: 1.The Claimant claims the sum of 248.05 for Outstanding debts and damages including 12.05 interest pursuant to S.69 of the county courts Act 1984. Total debt and interest due - 248.05. I will provide the defendant with separate detailed particulars within 14 days after service of the claim form. What is the value of the claim? £323.05 including all costs. Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim: Only Civil Enforcement Ltd are mentioned, no mention of creditor or account being assigned Were you aware the account had been assigned – did you receive a Notice of Assignment? No. I didn't even receive a letter before claim. I have attached the claim form and the separate particulars of claim form (dated 24 January 2017). The particulars were sent after I acknowledged the service. (I have attempted to upload redacted version but correct me if its not all correct!) My first question is how long do i have to submit my defence/skeleton defence? A claim was issued against you on 13/01/2017 Your acknowledgment of service was submitted on 22/01/2017 at 14:55:15 Your acknowledgment of service was received on 23/01/2017 at 01:09:20 The website states Before you can file a defence to the claim against you, you must make sure the following apply in your case: you are filing your defence within 14 days of service of the claim on you (a claim is considered served on the fifth day after it is issued) or where separate detailed particulars of claim were served, within 14 days of service of those or if you filed an acknowledgement of service, within 28 days of service of the claim (or separate particulars) Hey knowledgeable ones..... I was hoping you are able to help advise me on the next steps in the scenario below. As they sent a separate particulars of claim dated 24 Jan - am i correct to assume i have 28 days from this date to submit my defence? Secondly i have not recieved a letter before claims. Nor do i recall the NTK - although this may been sent i would like to see if its valid and also i can't see any evidence specifically any images of the vehicle alleged to made the contravention. So how am I supposed to accept their allegations - based on their nothing but their words? Do i send a CPR requesting evidence and if so do i include in the above points. I have seen the template CPR request but can i include the above in it and if so how best to word this please? I suppose the skeleton defence can be addressed later after the CPR but any thoughts welcome! If you have any links you can direct to me that might help that would be most appreciated also Many thanks COURT LETTER.pdf PARTICULARS OF CLAIM.pdf

Name of the Claimant: Civil Enforcement Ltd Date of issue: 13th January 2017 Date to acknowledge = 31.01.2017 DAte to submit defence = 4pm 14.02.2017 What is the claim for: 1.The Claimant claims the sum of 248.05 for Outstanding debts and damages including 12.05 interest pursuant to S.69 of the county courts Act 1984. Total debt and interest due - 248.05. I will provide the defendant with separate detailed particulars within 14 days after service of the claim form. What is the value of the claim? £323.05 including all costs. Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim: Only Civil Enforcement Ltd are mentioned, no mention of creditor or account being assigned Were you aware the account had been assigned – did you receive a Notice of Assignment? No. I didn't even receive a letter before claim. I have attached the claim form and the separate particulars of claim form (dated 24 January 2017). The particulars were sent after I acknowledged the service. (I have attempted to upload redacted version but correct me if its not all correct!) My first question is how long do i have to submit my defence/skeleton defence? A claim was issued against you on 13/01/2017 Your acknowledgment of service was submitted on 22/01/2017 at 14:55:15 Your acknowledgment of service was received on 23/01/2017 at 01:09:20 The website states Before you can file a defence to the claim against you, you must make sure the following apply in your case: you are filing your defence within 14 days of service of the claim on you (a claim is considered served on the fifth day after it is issued) or where separate detailed particulars of claim were served, within 14 days of service of those or if you filed an acknowledgement of service, within 28 days of service of the claim (or separate particulars) Hey knowledgeable ones..... I was hoping you are able to help advise me on the next steps in the scenario below. As they sent a separate particulars of claim dated 24 Jan - am i correct to assume i have 28 days from this date to submit my defence? Secondly i have not recieved a letter before claims. Nor do i recall the NTK - although this may been sent i would like to see if its valid and also i can't see any evidence specifically any images of the vehicle alleged to made the contravention. So how am I supposed to accept their allegations - based on their nothing but their words? Do i send a CPR requesting evidence and if so do i include in the above points. I have seen the template CPR request but can i include the above in it and if so how best to word this please? I suppose the skeleton defence can be addressed later after the CPR but any thoughts welcome! If you have any links you can direct to me that might help that would be most appreciated also Many thanks COURT LETTER.pdf PARTICULARS OF CLAIM.pdf -

Hi I have received a claim form with a stamp and the county court address on there. It says on the back of the letter - Do not ignore this claim form - if you do nothing judgement may be entered against you without further notice. This will make it difficult for you to get credit. Included in the pack are Admission Form N9A Defence and Counterclaim Forrm N9B Acknowledgement of service The top two are options are self explanatory i believe it does state the following under the 'acknowledgement of service' option: If you file an acknowledgement of service but do not file a defence within 2 days of service of the claim form, or particulars of claim if served separately, judgement may be entered against you. If you do not file an application within 14 days of the date of filing this acknowledgement of service, it will be assumed that you accept the court's jurisdiction and judgement may be entered against you. I can recall this relates to when they claim I had stopped in a no stopping zone at one stop shopping centre in Perry Barr Birmingham. I was totally unaware of this till i recieved the letter and it was asking for £100! On recollection i had parked next to where all the taxis park, so my mother could run to the cash point. I was in my car at all times and my engine was on - she was back in my car in two minutes and i was out o there. There was no obstruction caused and i even doubt i crossed the line where the cross hatches begin - probably only to turn around and get out of there! Naturally i have been ignoring their demands and have not sent them anything, but upon receiving this now i am concerned as to what it is? Am i being taken to court? will i get a CCJ? and do i need to respond? what is my best course of action? Hoping somebody can advise me please. Many many thanks

-

Hi i started a DMP with Moorhead Savage in @ 2011 things where fine until 2016 when they stopped managing plans , took on running my plan myself . In August last year i received a letter off Regal Credit ltd informing me they were ceasing trading and the debt was been returned back to BMI . In November i received a letter to contact them , which i did offering to continoue with the same payments . which they refused , i contacted them again saying i cant increase my offer as all my Creditors are paid Pro-Rata and it would be unfair . i then got a statement a month later wanting double . On the 30/12/16 letter from Style Credit dated 28/12/16 wanting contact immediately or legal action , i replied on the 03/01/17 which they received on the 05/01/17 ( recorded ) On the 20/01/17 i received a letter dated 16/01/17 which states since ive failed to contact them they will started legal action , i had till the 23/01/17 now the 21 / 22 was the weekend . i replied the same day and wrote to the address on the top of the page and also the registered offic on the bottom of letter , they received both letters on the 23/01/17 signed for by the same person . On the 26/01/17 i received a letter from HLW Keeble Hawson saying i failed to make a payment despite repeated requests and if they dont receive full payment within seven days they are starting a claim in the County Court , i have wrote to them too with a offer of payment and list of creditors . im not sure if the account has been Defaulted or not as all paper work went to Moorhead Savage , on the staetments BMI added inetrest which had been stopped . No payments have been missed to any Creditor , im dealing with 19 in total this seams like a rail road job any comment or ideas ! Thanks

-

Today I received a Claim Form for an old Bank Of Scotland Credit Card debt that had been passed on to IDEM Securities Limited. I had been sending regular monthly payments to Idem via Standing Order, last payment sent was January 2016. I had sent a signed for CCA Request on 28 December 2015 to IDEM SERVICING. The reply to my CCA request was: IDEM acknowledged they were unable to supply a copy and acknowledged until they could do so the agreement cannot be enforced. in March 2016 they wrote again saying they have now received a copy from LLOYDS BANKING GROUP and enclosed a copy. No signatures whatsoever are shown and just a print off of Repayment and Interest Charging, all looks like a generic print off. I never made any communication whatsoever with IDEM from this point. They tried phoning me daily and leaving messages on my answer machine which i never responded to. They then wrote to me in April 2016 saying they were unable to speak with me. Then they wrote in May 2016 saying they are keen to speak with me. Then on 14th July they wrote saying account transferred to Litigation. Today I received the County Court Claim Form with Issue Date 27 July 2016. I have logged into MCOL and done acknowledgement of service, and defend all. I have also a CPR 31.14 request to send signed for to Claimant in the morning. I also at this moment have a Claim Form going on with PRA-Halifax(LLoyds) which i have a thread on the forum, i have filed defence on that, and awaiting the 28 days to see if gets stayed, so i already was aware with MCOL and defend all being way to go. I thought it would still be worth while posting a new thread with this particular claim that has arrived today, just incase any different cause of action is best, both cases are very similar intruth as both have not provided a true copy of CCA. Any help/advice as always truly appreciated! Thank you

Today I received a Claim Form for an old Bank Of Scotland Credit Card debt that had been passed on to IDEM Securities Limited. I had been sending regular monthly payments to Idem via Standing Order, last payment sent was January 2016. I had sent a signed for CCA Request on 28 December 2015 to IDEM SERVICING. The reply to my CCA request was: IDEM acknowledged they were unable to supply a copy and acknowledged until they could do so the agreement cannot be enforced. in March 2016 they wrote again saying they have now received a copy from LLOYDS BANKING GROUP and enclosed a copy. No signatures whatsoever are shown and just a print off of Repayment and Interest Charging, all looks like a generic print off. I never made any communication whatsoever with IDEM from this point. They tried phoning me daily and leaving messages on my answer machine which i never responded to. They then wrote to me in April 2016 saying they were unable to speak with me. Then they wrote in May 2016 saying they are keen to speak with me. Then on 14th July they wrote saying account transferred to Litigation. Today I received the County Court Claim Form with Issue Date 27 July 2016. I have logged into MCOL and done acknowledgement of service, and defend all. I have also a CPR 31.14 request to send signed for to Claimant in the morning. I also at this moment have a Claim Form going on with PRA-Halifax(LLoyds) which i have a thread on the forum, i have filed defence on that, and awaiting the 28 days to see if gets stayed, so i already was aware with MCOL and defend all being way to go. I thought it would still be worth while posting a new thread with this particular claim that has arrived today, just incase any different cause of action is best, both cases are very similar intruth as both have not provided a true copy of CCA. Any help/advice as always truly appreciated! Thank you -

Greetings, i lost my business a couple of years ago and was left with arrears on my Business rates , the shop premises was leased to my Ltd Company but went into administration . The council served a liability order in jan 2013 in my name They have told me because i did not attend the hearing that i have to pay and the opportunity to dispute the liability has expired .. on top of this they are insisting i make large regular monthly payments which equates to 30% of my monthly take home pay saying they WILL NOT accept lower payments because of the age of the debt this is putting an extreme strain on my family and children Southend council have already sent enforcement agents to our home any advice will be greatly appropriated thank you here is their response to my question below Dear ***** I refer to your email received on * January 2016 advising that******* Limited should have been liable for Non-Domestic Rates at ******for the period **June 2012 - ** November 2013. Liability Orders were granted for this period of time on 9th January 2013 and 14th August 2013 in your name. When a Liability Order has been granted, the opportunity to dispute the liability for rates has expired. The matter will therefore not be investigated and account will not be retrospectively amended. I trust this has clarified matters.

Greetings, i lost my business a couple of years ago and was left with arrears on my Business rates , the shop premises was leased to my Ltd Company but went into administration . The council served a liability order in jan 2013 in my name They have told me because i did not attend the hearing that i have to pay and the opportunity to dispute the liability has expired .. on top of this they are insisting i make large regular monthly payments which equates to 30% of my monthly take home pay saying they WILL NOT accept lower payments because of the age of the debt this is putting an extreme strain on my family and children Southend council have already sent enforcement agents to our home any advice will be greatly appropriated thank you here is their response to my question below Dear ***** I refer to your email received on * January 2016 advising that******* Limited should have been liable for Non-Domestic Rates at ******for the period **June 2012 - ** November 2013. Liability Orders were granted for this period of time on 9th January 2013 and 14th August 2013 in your name. When a Liability Order has been granted, the opportunity to dispute the liability for rates has expired. The matter will therefore not be investigated and account will not be retrospectively amended. I trust this has clarified matters. -

Hi All, Came home from work today to find a letter packed with 6 monthly statements of account going back to 05/03/2010 this was for a welcome debt that I stopped paying sometime in 2007 or possibly earlier. I have been chased by robbers way about this debt I have ignored them because I know the debt is statute barred. I wonder why they have sent this lot (the letter states un CCA 74 they should have been sending these every six months but failed to do so). The other point it that the first statement is from 05/03/2010 showing no transactions on the account which in my eyes means they have just admitted that the debt is statute barred (and indeed all the statements up to september 16 show no transactions). I never got chased by welcome when I stopped paying them (due to extended period in hospital and out of work for 8 months) funnily enough I only started hearing from robbers way about 6 months ago random phone calls and the odd letter. Anyone else had this?

-

Dear all I am seeking advise once again on how to respond to a claim form issued to me by BW Legal on behalf of Lowell for a home shopping agreement through the County Court. Any help is appreciated.

-

Apologies if this has been covered elsewhere but I am trying to get in a Defence on the Webiste before a deadline and can't spend too much time searching for a possibly similar case. In short this is my story; This entire "debt" was manufactured by the original lender*(Halifax) reneging on Payment Protection Insurance for the Credit Card when*I lost my job. I continued trying to pay the minimum monthly payment despite*being unemployed and unaware I could make a payment arrangement*which meant the interest just kept mounting up. I eventually was directed to Citizens Advice Bureau who assisted*me in making payment arrangement. I was subsequently advised by a friend that the debt was likely*not legally enforceable and I should request a copy of the* original agreement which I did and the lender was unable to do so* as such I*stopped paying anything. The Lender then kept sending the debt to a succession of*Collection Agencies (many just "fronts" for departments of the* Lender) who would harass me by letter and phone until I pointed*out the debt was unenforceable they would then "check with the*lender" and eventually leave me alone at which point the Lender*would engage another Agency and the pattern would begin again this*happened so often I began being contacted by some agencies for a*second time! Finally on 11th of May 2012 a letter and cheque for £103.45 (being*10% of the claimed outstanding amount) were sent to the Lender on*the stated condition this was an offer in full and final*settlement of the matter and encashment of the cheque would be*deemed acceptance of those terms. The cheque was cashed by the Lender on 28th May 2012. Since the cheque was cashed I have been telling Agencies the matter is settled and they have eventually left me a lone and then another one appears. However on 28th February 2013 the funds were refunded without any*notification or explanation. The latest agency Lowell have finally upped the ante and actually made good on threats to take me to court and I have received Claim Form from County Court Business Centre. When I pointed out the matter was settled Lowell stated the lender now claims that the money was deducted from the debt*but they didn't accept the terms and the balance is still*outstanding. However no such notification was received by myself. Furthermore the cheque sent was drawn on an account belonging to*my mother, no myself, for the sole purpose of settling the*debt as per the terms set out in the accompanying letter. If the*Lender was not willing to accept the terms then surely they had no entitlement*to the funds and have therefore cashed the cheque fraudulently!* Which potentially explains the covert refund nine months later! Any thoughts or advice would be appreciated as yet my defence on the Govt site is much as listed above.

Apologies if this has been covered elsewhere but I am trying to get in a Defence on the Webiste before a deadline and can't spend too much time searching for a possibly similar case. In short this is my story; This entire "debt" was manufactured by the original lender*(Halifax) reneging on Payment Protection Insurance for the Credit Card when*I lost my job. I continued trying to pay the minimum monthly payment despite*being unemployed and unaware I could make a payment arrangement*which meant the interest just kept mounting up. I eventually was directed to Citizens Advice Bureau who assisted*me in making payment arrangement. I was subsequently advised by a friend that the debt was likely*not legally enforceable and I should request a copy of the* original agreement which I did and the lender was unable to do so* as such I*stopped paying anything. The Lender then kept sending the debt to a succession of*Collection Agencies (many just "fronts" for departments of the* Lender) who would harass me by letter and phone until I pointed*out the debt was unenforceable they would then "check with the*lender" and eventually leave me alone at which point the Lender*would engage another Agency and the pattern would begin again this*happened so often I began being contacted by some agencies for a*second time! Finally on 11th of May 2012 a letter and cheque for £103.45 (being*10% of the claimed outstanding amount) were sent to the Lender on*the stated condition this was an offer in full and final*settlement of the matter and encashment of the cheque would be*deemed acceptance of those terms. The cheque was cashed by the Lender on 28th May 2012. Since the cheque was cashed I have been telling Agencies the matter is settled and they have eventually left me a lone and then another one appears. However on 28th February 2013 the funds were refunded without any*notification or explanation. The latest agency Lowell have finally upped the ante and actually made good on threats to take me to court and I have received Claim Form from County Court Business Centre. When I pointed out the matter was settled Lowell stated the lender now claims that the money was deducted from the debt*but they didn't accept the terms and the balance is still*outstanding. However no such notification was received by myself. Furthermore the cheque sent was drawn on an account belonging to*my mother, no myself, for the sole purpose of settling the*debt as per the terms set out in the accompanying letter. If the*Lender was not willing to accept the terms then surely they had no entitlement*to the funds and have therefore cashed the cheque fraudulently!* Which potentially explains the covert refund nine months later! Any thoughts or advice would be appreciated as yet my defence on the Govt site is much as listed above. -

Hello all, Am after some help with Mortgage Agency Number 4 LTD which I have seen mentioned a few times throughout the years on this forum. I'll try not to go on too much and keep it short, any pointers would be greatly received. In 2006 our mortgage mysterily changed from GMAC to Mortgage Agency Number 4 LTD. At the time we where on a fixed rate with GMAC and nothing had changed so we merely continued as normal. The real illusion came to light when our fixed rate was coming to a end and we called MAS No 4 Ltd to check what new deals there where (fixed rates, trackers etc). We where trapped, mortgage was going to their standard variable rate and with the downturn moving mortgages without a perfect clean file wasn't possible. We therefore changed it to interest only to bring the payment within affordability. In december 2015 I suffered a accident at work (work fault) and required emergency surgery over the Christmas period, further surgery in April 2016 and another November 2016. I wasn't able to weight bare between Xmas 2015 and April 2016. It has been a terrible year. Being given only SSP for 28 weeks, the mortgage company where advised straight away, however there help was none existence. They refused point blank to reduce the interest rate to stop arrears building up, they gave us payment breaks but this acheived nothing but create arrears quickly. Their operators just advised us to sell and move, careless in every manor, every option or idea we put through to them shot down within seconds. They where advised all the way how things where but persited in daily phone calls and letters asking for updates, answered them and few days later back to the same questions as if I have had a immaculate recovery over night. There harrasment is in no way helping my recovery, did I ask for this = no. Have I ever been out of work since I left school = no. We have kept every single letter sent and received by them and have also recorded and stored every single phone call with them. They have been advised in writing that we are recording their calls but this doesn't stop their "sell up" manor To prevent the mortgage getting endless arrears, a parent offered to cover our monthly minimum contractual payment for a few months (Nov, Dec, Jan & Feb) this was to keep them happy and prevent arrears building. As per this was not good enough for MAS, they said they see this as an additional income and therefore this should come off the arrears. As they where fully aware, we didn't have enough funds coming in to cover the mortgage let alone the arrears. Another obsticle put in the way. It seems like all they want possession of the property, they simply dont care one ounce. I asked if they could capitalise the arrears too which within seconds was told that will never happen. I'm at a total loss with them and the last thing I told them is what we have always told them, once I am either back at work or my injury claim is settled we would be in touch to have the matter settled. I have nothing to gain not contacting them when things have improved. I dont want to discuss work within this thread as this is a sore area #I'm just looking for pointers please on how and what we should do to deal with these bullies the best way possible? Thank you

-

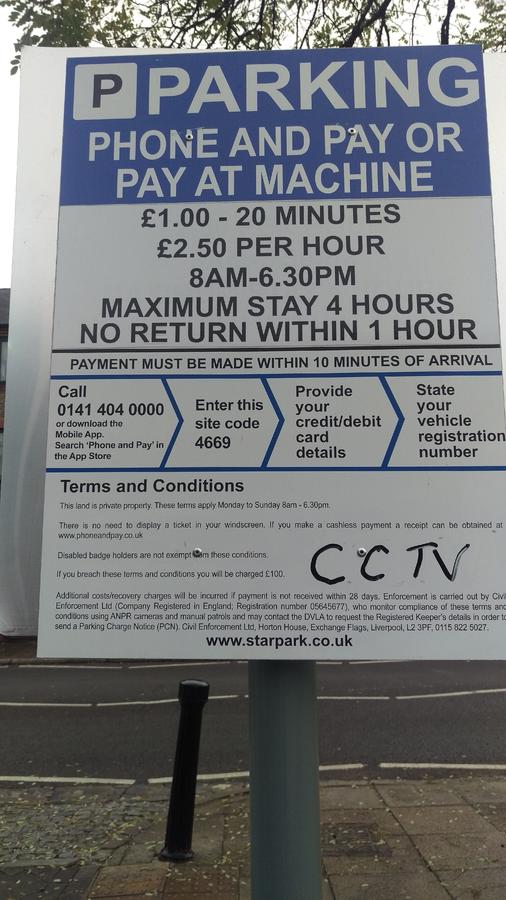

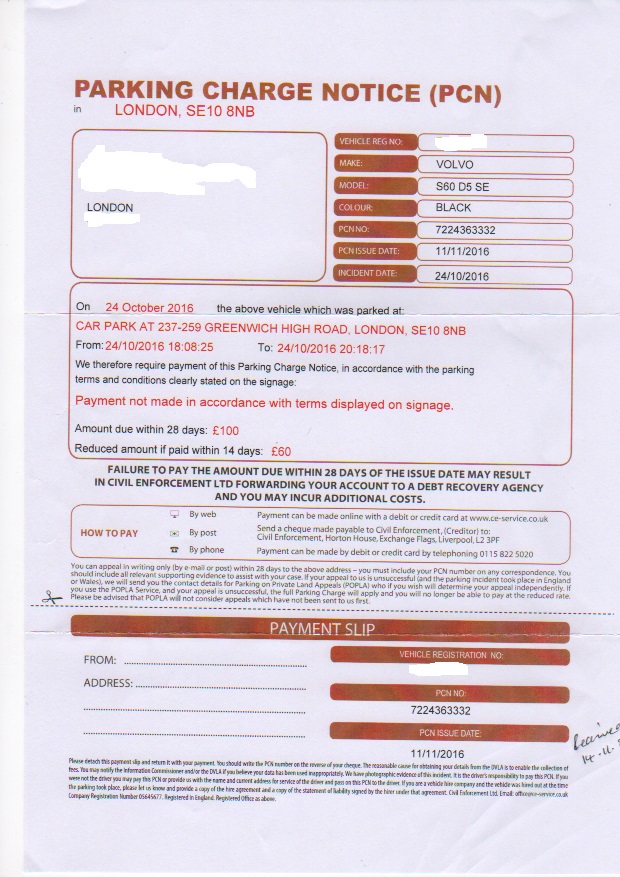

You've helped me once before (post4830039) with a 'parking charge notice'. I don't think I actually need help this time, but wanted to post on this site for general awareness in case there's a pattern in how this firm operates. I parked in a car park where controls are effective 08:00-18:30. The PCN shows I entered the car park at 18:08:25. I purchased a ticket (which I still have) at 18:12, paying £2 for 20 minutes as I didn't have anything smaller. The ticket I purchased shows the expiry time as 18:32 (ie, 2 minutes after parking controls ceased to be effective). Today I received a PCN from CEL citing 'Payment not made in accordance with the terms displayed on the signage'. I've gone back and checked the sign and I can't see any term that I failed to comply with: - I paid the fee - the ticket was purchased within 10 minutes of entering the car park - I didn't exceed the maximum stay Although I said I don't think I need help on this, any offered would be appreciated especially if you spot something I've missed. Otherwise I will email CEL advising the above facts and that if they don't withdraw the charge they must stipulate exactly which term or terms they believe I contravened, with the effective date of the charge being the date they reply. Incidentally, I only received notification of the supposed offence 3 weeks later and it's pure luck that I still have the ticket. What does anyone do in the situation where no parking notice was issued at the time and the ticket has been discarded? It seems pretty outrageous to me that these parking cowboys have the law on their side in cases like this...

You've helped me once before (post4830039) with a 'parking charge notice'. I don't think I actually need help this time, but wanted to post on this site for general awareness in case there's a pattern in how this firm operates. I parked in a car park where controls are effective 08:00-18:30. The PCN shows I entered the car park at 18:08:25. I purchased a ticket (which I still have) at 18:12, paying £2 for 20 minutes as I didn't have anything smaller. The ticket I purchased shows the expiry time as 18:32 (ie, 2 minutes after parking controls ceased to be effective). Today I received a PCN from CEL citing 'Payment not made in accordance with the terms displayed on the signage'. I've gone back and checked the sign and I can't see any term that I failed to comply with: - I paid the fee - the ticket was purchased within 10 minutes of entering the car park - I didn't exceed the maximum stay Although I said I don't think I need help on this, any offered would be appreciated especially if you spot something I've missed. Otherwise I will email CEL advising the above facts and that if they don't withdraw the charge they must stipulate exactly which term or terms they believe I contravened, with the effective date of the charge being the date they reply. Incidentally, I only received notification of the supposed offence 3 weeks later and it's pure luck that I still have the ticket. What does anyone do in the situation where no parking notice was issued at the time and the ticket has been discarded? It seems pretty outrageous to me that these parking cowboys have the law on their side in cases like this...

-

I'm new to this and not experienced with dealing with the courts and the big lawyers, in fact it is quite scary.. Below is an outline of what has happened to date but now I really need some help to guide me best way through this mess. Background: I had a credit card debt with barclays of £9k and this has gone up to £11k with court fees, Legal and with interest charged from 04/2014 making a total of £11k (All figures have been rounded up.) I missed payment in 2014 which shows up in 2014 on my credit file as a default and not made any payments since, I had the card for 35 years during which it was faultless. In May 2016 ,i got a claim form from County Court Business centre and sent in a acknowledgment of service: Claimants are: Hoist Portfilio Holdings 2 Ltd and Howard Cohen are their acting Solicitors. Next:24 June 2106 I emailed the following to hmcts.gsi as a defence statement: Stating the following: This claim is for the sum of £9000 in respect of monies owing under an Agreement with the Account No. XXXXXXXX pursuant to the The Consumer Credit ACT 1974 (CCA). The debt was legally assigned by MKDP LLP (Ex Barclaycard) to the claimant and notice has been served. The Defendant has failed to make contractual payments under the terms of the Agreement. A default notice has been served upon the Defendant pursuant to s.87(1) CCA. The Claimant claims The sum of 9000 Interest pursuant to s69 of the Count Court Act 1984 at a rate of 8.00 percent from 01/04/14 to the date hereof xxx is the sum £1500 Future interest accruing at the daily rate of 1.96 4. Costs Defence: With reference to the defence i would like to mention the following points and request the information to assist in my defence: Information of the original debt with Barclaycard of £9000 and any copies of a default notice served by Barclaycard. It is my understanding that through Lovell Portfolio Ltd in 28/01/2014 that a default notice was served on my account without my consent or my authority or signature to them as a third party. Claimants to supply a copy of the executed deed of assignment from Barclaycard to Lovell Porffolio, MKDPP LLP and to Claimant Hoist Portfolio Holdings Ltd a for the above referenced agreement An issue of confusion has been created in this case and seek clarification in having this matter properly resolved. As this has been done without my knowledge, consent or my authority and that the claimant as a third party may have wrongly taken this matter to County Court Business Centre. I would like to put this matter into mediation to have it resolved and establish how best this cane satisfied without going to court. In my defence it should be noted that i have with assistance cleared a majority of my debts and have had stated Barclaycard for 35 years, during which the account has traded without any problems and without any defaults being issued. it was in fact a surprise to me that a default notice has been served by Lowell Portfolio Ltd who had not informed me of this and not had any correspondence from Barclaycard on this matter. In terms of the cost please note this is refuted and will be discussed or best resolved through Mediation, any documentation regarding this and supporting documentation from claimants on this case should be sent to me for the my attention. To Note: I have had problems going through the website in filing this defence and proof copy is attached of that information, I subsequently rang the County Court Business Centre to seek how I could best file this defence claim. After speaking to XXXX who was very helpful i was informed that it was satisfactory to file it via email and the deadline was Saturday 25th June 2016 and gave me the email address to which it can be sent. Before this I have also sought advice from CAB and XXXXX from Legal firm XXXXXX who are based in XXXXX who kindly assisted me on the phone. It is with regret that this matter has been taken to Court and would urge a resolution that is satisfactory to all parties. Thank you for your attention to the above and request confirmation of this defence as i am experiencing difficulty with the internet whilst away. Please confirm that this has been received and will wait response Yours Faithfully XXXXXXXX .. Next: 31st August 2106 I received a Letter from Howard Cohen And Co on 31st August with details of Draft Directions. 1) Pursuant to CPR 26.7(2) Claim to be allocated to Small Claims Court 2) A stay or proceedings for 1 month to allow both parties to negotiate settlement of claim by way of Small Claims Mediation 3) Both parties to inform the court by 30th September 2106 if a settlement has been agreed or if an extension of stay is required. 4) If a settlement has not been agreed, then the claim be transferred to the Defendants local Court to be allocated to the Small Claims Track and listed for a hearing on a date to be fixed by the court with a time estimated of 1 hour 5) Claimant pay the hearing fee on a date to be fixed by the Court 6) No experts evidence being necessary, no party has permission to call or reply on experts evidence 7) Each party shall deliver to every party and to the Court Office, copies of all documents on which they intend to rely upon no later that 14 days before the hearing along with signed statements of truth ... Next: 01/09/16 to the Courts. I submitted a Directions Questionnaire (Fast Track and Multi Track) Stating that I wished to settle the claim and I wanted a month stay, required assist of mediation, acknowledged request for local court, NO witness and it would be less than a day in court. ... Next:10 September 2106 I received a Order of Stay which now runs out on 24th October and not received any communication or information from the Claimants to try and resolve this matter out of court. I have heard nothing from the claimants to try and get this matter resolved. I need HELP now to try and sort this out the best way, I am getting mixed messages that I should try and speak to their Solicitors 'Howard Cohen And Co' find out whats going on but I am scared of that and also try speak to MKDDP or Barclays ??? Sorry for the late action but it was becoming quite embarrassing to handle this.. Hope someone can help. I can try ask for some money from family and friends but not anywhere near the amount requested I also need to know if it will help resolve all this first and how much, before approaching outsiders to help.. as I have little left over after the bills and food. I am in full time work but do not have that kinda money to settle. Please Help if you can.

-

Name of the Claimant - H Cohen Solicitors, Hoist 2 Ltd. Original creditor MKDP LLp (Ex HSBC). Date of issue: 12th September Acknowledgement submitted. What is the claim for – the reason they have issued the claim? This claim is for the sum of £1089 in respect of monies owed pertinent to an overdraft facility under bank account number x. The debt was legally assigned by MKDP (Ex HSBC) to the claimant and notice has been served. The defendant has failed to repay overdraft sums owing under the terms and conditions of the bank account. The Claimant claim: 1. The sum of £1089 2. Interest charges persunt of the county court act 1964 at a rate of 8% from 24/09/12 to the date hereof 1436 is the sum of £343.06. 3. Future interest at the daily rate of .24 4. costs. Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Overdraft When did you enter into the original agreement before or after 2007? Account set up in early 2000s Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? No Did you receive a Default Notice from the original creditor? Not sure. Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure. Why did you cease payments? I didn't, I was a student conducting fieldwork abroad. The overdraft was within its limit, but not enough money was paid into it. Whilst away, HSBC closed the overdraft facility and demanded full payment. (OD Limit was £1500, amount in account was -£1090) What was the date of your last payment? Early 2012 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? Unsure. Hello and thank you for any help. I am a UK citizen but have been living and working abroad for three years - Estonia and Hungary. This is making it very hard for me to deal with this... I was unaware of being chased for this debt. I recently found out about a court summons as post was forwarded to a family member. I called Cohen and Hoist about this debt asking for documents to prove to me the age and the fact it is mine and they said they did not have these. The debt is from 2012, I tried to get access to my statutory C report but as I am a resident abroad this is very difficult and basically is not possible. I have sent a CCA request and CPR 31.14. These were only sent today. I have very little time to submit my defense. I have a defense written - can I submit this even though the solicitors have not had the time to respond? I basically want to say - I don't know what this is, I would like them to show me documentation. 1. I received the claim xxxxxx from the Northampton County Court on 12th September. 2: Each and every allegation in the Claimants statement of case is denied unless specifically admitted in this Defence. 3: This claim appears to be for an overdraft agreement regulated under the Consumer Credit Act 1974. 4: The Claimants statement of case fails to give adequate information to enable me to properly assess my position with regards the claim. 4.(a). The defendant is unable to reconcile the amount claimed with any account he may have had with the original credit and remains at a disadvantage not having access to relevant record. 5. The defendant is Litigant in and domiciled outside the UK requests for inspection of documents on which the claimant intends to rely have been made via the provisions of CCA 1974 and CPR31.4 and he awaits replies. - I am well out of my comfort zone here, this process has caused considerable stress in the last week, please excuse any ignorance on my side! - I am really struggling with this - is what I have written above logical? Is there something wrong with this, should I be doing something else? What happens next - where does the process go from here? Thank you very much for any help.

Name of the Claimant - H Cohen Solicitors, Hoist 2 Ltd. Original creditor MKDP LLp (Ex HSBC). Date of issue: 12th September Acknowledgement submitted. What is the claim for – the reason they have issued the claim? This claim is for the sum of £1089 in respect of monies owed pertinent to an overdraft facility under bank account number x. The debt was legally assigned by MKDP (Ex HSBC) to the claimant and notice has been served. The defendant has failed to repay overdraft sums owing under the terms and conditions of the bank account. The Claimant claim: 1. The sum of £1089 2. Interest charges persunt of the county court act 1964 at a rate of 8% from 24/09/12 to the date hereof 1436 is the sum of £343.06. 3. Future interest at the daily rate of .24 4. costs. Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Overdraft When did you enter into the original agreement before or after 2007? Account set up in early 2000s Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? No Did you receive a Default Notice from the original creditor? Not sure. Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure. Why did you cease payments? I didn't, I was a student conducting fieldwork abroad. The overdraft was within its limit, but not enough money was paid into it. Whilst away, HSBC closed the overdraft facility and demanded full payment. (OD Limit was £1500, amount in account was -£1090) What was the date of your last payment? Early 2012 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? Unsure. Hello and thank you for any help. I am a UK citizen but have been living and working abroad for three years - Estonia and Hungary. This is making it very hard for me to deal with this... I was unaware of being chased for this debt. I recently found out about a court summons as post was forwarded to a family member. I called Cohen and Hoist about this debt asking for documents to prove to me the age and the fact it is mine and they said they did not have these. The debt is from 2012, I tried to get access to my statutory C report but as I am a resident abroad this is very difficult and basically is not possible. I have sent a CCA request and CPR 31.14. These were only sent today. I have very little time to submit my defense. I have a defense written - can I submit this even though the solicitors have not had the time to respond? I basically want to say - I don't know what this is, I would like them to show me documentation. 1. I received the claim xxxxxx from the Northampton County Court on 12th September. 2: Each and every allegation in the Claimants statement of case is denied unless specifically admitted in this Defence. 3: This claim appears to be for an overdraft agreement regulated under the Consumer Credit Act 1974. 4: The Claimants statement of case fails to give adequate information to enable me to properly assess my position with regards the claim. 4.(a). The defendant is unable to reconcile the amount claimed with any account he may have had with the original credit and remains at a disadvantage not having access to relevant record. 5. The defendant is Litigant in and domiciled outside the UK requests for inspection of documents on which the claimant intends to rely have been made via the provisions of CCA 1974 and CPR31.4 and he awaits replies. - I am well out of my comfort zone here, this process has caused considerable stress in the last week, please excuse any ignorance on my side! - I am really struggling with this - is what I have written above logical? Is there something wrong with this, should I be doing something else? What happens next - where does the process go from here? Thank you very much for any help. -

I have received a letter this morning at my rented address for a notice of application for attachment of earnings order from Cabot Financial (UK) Ltd. I migrated to Australia in 2011 but had to return in Aug 2015 due to visa refusal but although this letter has a case number and application number as well as a judgement creditors reference I actually have no idea what this debt is supposed to be for as this is the first correspondence I have received at this address and I have been here since August 2015. It says unless I pay the judgement creditor within 8 days I must complete the enclosed form of reply including the statement of means and send it to the court office within 8 days after receiving this notice. I'm not sure what this debt is for which is my main concern as there is no reference to it nor what date this judgment was carried out. It says the address for payment is Restons Solicitors Limited Warrington and that's about as much as I know

I have received a letter this morning at my rented address for a notice of application for attachment of earnings order from Cabot Financial (UK) Ltd. I migrated to Australia in 2011 but had to return in Aug 2015 due to visa refusal but although this letter has a case number and application number as well as a judgement creditors reference I actually have no idea what this debt is supposed to be for as this is the first correspondence I have received at this address and I have been here since August 2015. It says unless I pay the judgement creditor within 8 days I must complete the enclosed form of reply including the statement of means and send it to the court office within 8 days after receiving this notice. I'm not sure what this debt is for which is my main concern as there is no reference to it nor what date this judgment was carried out. It says the address for payment is Restons Solicitors Limited Warrington and that's about as much as I know -

Hi All, Brought a car from Yes Car Credit in May 2004, arranged with Yes Car credit to return due to change in circumstances in September 2004. Debt was transferred to Go Debt, apx £6000. Payment plan in place with my DMP and balance currently apx £1600. Been paying this since 2004 to present date. Looking for a way to end this and looking for best way to try? I was missold the PPI on this agreement and was told i could not proceed unless it was taken, PPI was also apx £1600. is there any option to try with this? This was just before the FSA came into effect in January 2005. Also the deposit of £110 was subtracted from the Insurance / PPI section on the agreement not the Vehicle, seen a few comments on here that this can have an impact on the agreement. I have a copy of the agreement but have sent Go-Debt a CCA request. Any Ideas / Best way to proceed? Thanks.

Hi All, Brought a car from Yes Car Credit in May 2004, arranged with Yes Car credit to return due to change in circumstances in September 2004. Debt was transferred to Go Debt, apx £6000. Payment plan in place with my DMP and balance currently apx £1600. Been paying this since 2004 to present date. Looking for a way to end this and looking for best way to try? I was missold the PPI on this agreement and was told i could not proceed unless it was taken, PPI was also apx £1600. is there any option to try with this? This was just before the FSA came into effect in January 2005. Also the deposit of £110 was subtracted from the Insurance / PPI section on the agreement not the Vehicle, seen a few comments on here that this can have an impact on the agreement. I have a copy of the agreement but have sent Go-Debt a CCA request. Any Ideas / Best way to proceed? Thanks. -

Hi all, I am hoping someone can kindly help here. I received a Northampton County Court Claim form today from the above claimants for an old Barclaycard debt that has been passed to MKDP and then these guys. The claim was issued on 01/03 I filed the AOS online today via MCOL, with the intention of defending the claim in full. The POC is as follows: T1.his Claim is for the sum of £9699.45 in respect of monies owing under an Agreement with the account no. XXXXXXXXXXXXXXXX pursuant to The Consumer Credit Act 1974 (CCA). The debt was legally assigned by MKDP LLP (Ex Barclaycard) to the Claimant and notice has been served. The Defendant has failed to make contractual payments under the terms of the Agreement. A default notice has been served upon the Defendant pursuant to s.87(1) CCA. The Claimant claims 1. The sum of £9699.45 2. Interest pursuant to s69 of the County court Act 1984 at a rate of 8.00percent from the 7/02/12 to the date hereof 1480 is the sum of £3146.33 3. Future interest accruing at the daily rate of "2,13 4. Costs In total, they are claiming over £13k.... Long story short, I was made redundant from my job and I was out of work for over a year - as a result I ran out of money to keep up my credit card payments and ultimately could not keep up the payments and stopped paying altogether. I buried my head in the sand somewhat and hoped the problem would go away, stupidly. If someone can guide me through what needs to be done next and what letters/forms need to be sent next, I would really appreciate it. I am so worried that bailiffs will come knocking on my door - I don't even know where to start with defending this.... Any help or guidance you give will be most appreciated.

-

Hi There Thanks for all the help I have had from people in the past just reading these forums - this kind of thing is why the internet was invented. I have now a personal plea for help if you people would be so kind, I think this is the right format: Name of the Claimant ? LOWELL PORTFOLIO I LTD Date of issue – 13 OCT 2016 What is the claim for – 1. the defendant entered into a consumer creditic act 1974 regulated agreement with JD Williams *********( the agreement) 2. the defendant failed to maintain the required payments and a default notice was served and not complied with. 3. the agreement was later assigned to the claimant on the 31/03/2014 and notice given to defendant. 4. despite repeated request for payment the sum of £1430.00 remains due and outstanding And the claimant claims a) the said sum £1430.00 b) interest pursuant to s69 county courts act 1984 at the rate of 8% per annum from the date of assignment to the date of issue, accruing at a daily rate of £0.313, but limited to one year, being £114.40 c) Costs What is the value of the claim?£1544.40 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? CATALOGUE CREDIT ACCOUNT When did you enter into the original agreement before or after 2007? NOT 100% AS ITS DROPPED OFF CREDIT FILE ALSO Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. IT WAS ASSIGNED TO LOWELLS Were you aware the account had been assigned – did you receive a Notice of Assignment? NOT SURE - A BITTER DIVORCE ENSUED Did you receive a Default Notice from the original creditor? NOT SURE - AGAIN I WAS OUT OF THE HOME Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? NOT SURE - SAW A NUMBER OF LETTERS TO MY PARENTS HOME IN THE LAST 6/8 MONTHS AS IT HAS BEEN ABOUT TO DROP OF MY FILE Why did you cease payments? MOVED HOUSE THROUGH A BITTER DIVORCE AND ASSUMED EX WAS TAKING CARE (stupidly) What was the date of your last payment? THE DEFAULT WAS ISSUED JULY 2010 SO BEFORE THIS DATE Was there a dispute with the original creditor that remains unresolved? NO Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? NO Thanks in advance

-

My father is in his 70's and was worried when he received a Parking Fine from Athena Ltd and complained to me that he actually parked in their car park and shopped in the Lidl store. He was there for quite a while and I am unsure if he went anywhere else either way the ticket states he was 1 hour and 13 minutes. In his annoyance my father contacted Athena to complain about the ticket and was given a deadline to appeal but handed it to me to write to them. I was very dismayed that he contacted them and informed him that he should not bother with civil parking fines but as an elderly person he is worried. My concern is that as he had made contact with them, he has admitted to being the driver of the vehicle. Should I write to them or leave it?

My father is in his 70's and was worried when he received a Parking Fine from Athena Ltd and complained to me that he actually parked in their car park and shopped in the Lidl store. He was there for quite a while and I am unsure if he went anywhere else either way the ticket states he was 1 hour and 13 minutes. In his annoyance my father contacted Athena to complain about the ticket and was given a deadline to appeal but handed it to me to write to them. I was very dismayed that he contacted them and informed him that he should not bother with civil parking fines but as an elderly person he is worried. My concern is that as he had made contact with them, he has admitted to being the driver of the vehicle. Should I write to them or leave it? -

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) Given the seriousness of this thread, it really does need to get wide coverage. Accordingly, I would hope that the moderators allow it to remain on this section of the forum. Sadly, this is not the first time that I have taken issue with documentation from DCBL. There is a long thread on here regarding this firm and their letters regarding private parking debts (more later). This firm are also behind the TV series....Can't Pay...We Will Take it Away. Yesterday, I was contacted by a gentleman who had received a letter from DCBL the previous day. The letter was received by post and was on headed notepaper from DCBL and clearly stated at the top of the letter (beside the word DCBL) the words: Certificated Bailiffs and High Court Enforcement Officers. The letter referred to a 'debt' in excess of £10,000. Interest of 8% (since May 2016) had also been added. The letter stated the following: Unless we receive immediate proposals from you regarding the repayment of this debt, the recovery process will commence 7 days from the date of this letter. We may also make arrangements for a representative to call upon you to open up lines of communication. The person receiving the letter knew about the 'debt' and knew that it was heavily disputed. More importantly, he was adamant that court proceedings had not been undertaken against him and that a judgment had not been obtained. He intended writing to DCBL. Before being able to, he had a visit at his home from a High Court Enforcement Agent from DCBL. It is fair and accurate to state that an argument broke out. The 'debtor' called the police. Astonishingly, the police refused to attend stating that they were satisfied that DCBL had authority to attend his premises to enforce the debt. The High Court Enforcement Agent from DCBL refused to leave the premises unless he received payment. Under duress, the debtor borrowed a sum of £2,000. DCBL yesterday confirmed the following: That the debt had not been subject to court action. That a judgment had not been obtained by the creditor. That they were enforcing a 'pre judgment' debt. That the 'High Court Enforcement Officer' was attending as a 'Debt Collector' Members of the public receiving letters such as these will no doubt be hoodwinked into believing that the debt was legally due and that a court order exists. They would be wrong.

Given the seriousness of this thread, it really does need to get wide coverage. Accordingly, I would hope that the moderators allow it to remain on this section of the forum. Sadly, this is not the first time that I have taken issue with documentation from DCBL. There is a long thread on here regarding this firm and their letters regarding private parking debts (more later). This firm are also behind the TV series....Can't Pay...We Will Take it Away. Yesterday, I was contacted by a gentleman who had received a letter from DCBL the previous day. The letter was received by post and was on headed notepaper from DCBL and clearly stated at the top of the letter (beside the word DCBL) the words: Certificated Bailiffs and High Court Enforcement Officers. The letter referred to a 'debt' in excess of £10,000. Interest of 8% (since May 2016) had also been added. The letter stated the following: Unless we receive immediate proposals from you regarding the repayment of this debt, the recovery process will commence 7 days from the date of this letter. We may also make arrangements for a representative to call upon you to open up lines of communication. The person receiving the letter knew about the 'debt' and knew that it was heavily disputed. More importantly, he was adamant that court proceedings had not been undertaken against him and that a judgment had not been obtained. He intended writing to DCBL. Before being able to, he had a visit at his home from a High Court Enforcement Agent from DCBL. It is fair and accurate to state that an argument broke out. The 'debtor' called the police. Astonishingly, the police refused to attend stating that they were satisfied that DCBL had authority to attend his premises to enforce the debt. The High Court Enforcement Agent from DCBL refused to leave the premises unless he received payment. Under duress, the debtor borrowed a sum of £2,000. DCBL yesterday confirmed the following: That the debt had not been subject to court action. That a judgment had not been obtained by the creditor. That they were enforcing a 'pre judgment' debt. That the 'High Court Enforcement Officer' was attending as a 'Debt Collector' Members of the public receiving letters such as these will no doubt be hoodwinked into believing that the debt was legally due and that a court order exists. They would be wrong. -

Hi, yesterday I was issued with a PCN for parking in a disabled space without clearly displaying a disabled badge. I have a disabled badge but it had slid from the dashboard to down the side of the dashboard. I was distracted when parking and had realised it had slid down the side. I have read lots of threads on here and am totally confused. Should I hold my hands up and admit it wsnt displayed clearly or defend the claim. My nissan note has a small side window that would have shown the badge had slipped down the side but I doubt this is clearly displayed. The disabled bat was clearly marked with signage etc. This was at Faraday Retail Park Coatbridge ML5 3SQ. Many thanks for your advise

-

hi I have uploaded 2 letters that I have received from robinson way. the first asking me if I lived at an address in Cyprus. which I did from 2006 until 2010. the 2nd telling me that I had a debt owed to HPH2 (ex Lolyds overseas) for £3037.00. I did have a loan in 2004 but due to loss of job while in Cyprus could not keep up the payments last payment was early 2007. since then had on contact with anyone regarding this debt until 2 weeks ago 1st letter. then the 2nd letter today. note on the 1st letter theres no mention of them being a DCA can you advise me on how to deal with this please Thanks

hi I have uploaded 2 letters that I have received from robinson way. the first asking me if I lived at an address in Cyprus. which I did from 2006 until 2010. the 2nd telling me that I had a debt owed to HPH2 (ex Lolyds overseas) for £3037.00. I did have a loan in 2004 but due to loss of job while in Cyprus could not keep up the payments last payment was early 2007. since then had on contact with anyone regarding this debt until 2 weeks ago 1st letter. then the 2nd letter today. note on the 1st letter theres no mention of them being a DCA can you advise me on how to deal with this please Thanks

-

Hello, I hope someone can advise. I am looking for some assistance. I have just recieved a Small Claims Summons from a large organisation chasing a debt from a Ltd Company I was a Director for the sum of £840.70. The company I was a Director for dissolved in June 2015. I signed a trade account agreement in my name on behalf of the company as I was the Director. The company only had a £750.00 trade limit. It was a trade account but yet the large organisation is chasing me personally now for the debt. I started the business in the hope of success but was not paid by several customers and did not have the monies to chase the debt so closed the company as it was no longer viable and I got a job. Am I liable for this debt and do I have to pay?

-

Good Afternoon Hoping someone can help me please. Myself and my hubby had a car on finance with Finance U a good few years ago, long story short, run into financial difficulty, car was taken back, ccj put against us and a charging order. This year in February we finally finished paying them. May of this year we received a letter saying we still owed about £900 which was interest. Each month I sent a cheque along with a complete monthly letter with date, amount paid, cheque number and balance. They cashed each cheque but not once did they mention that OUR balance was incorrect by them. No mention off them either whilst we were paying every month that interest was going to be added. ..Any help would be very much appreciate please

Good Afternoon Hoping someone can help me please. Myself and my hubby had a car on finance with Finance U a good few years ago, long story short, run into financial difficulty, car was taken back, ccj put against us and a charging order. This year in February we finally finished paying them. May of this year we received a letter saying we still owed about £900 which was interest. Each month I sent a cheque along with a complete monthly letter with date, amount paid, cheque number and balance. They cashed each cheque but not once did they mention that OUR balance was incorrect by them. No mention off them either whilst we were paying every month that interest was going to be added. ..Any help would be very much appreciate please -

Hello. I am new to this and sure not what i am doing. I have never used a forum. I have recently recieved a letter from the above which has now followed by a statement of means for £8, 506.74. This i believe has something to do with Abbey National which is now Santander. I originally had an overdraft for £250,only. How this has got to this is through i guess bank charges. I have no records of the original overdraft or any paper work as i no longer bank with them. I have ignored them as i was told that the letters are just threats. I could never pay this back as i work parttime and feel that they have taken advantage of the situation. The court letter seems weird as it comes from local court in my area and then has big red stamp saying return to basildon. Really worried and stressed as i have only a day to send it off. please could someone advise as i dont even know if i am doing this right and where to find the reply should someone advise me. Very new to this Regards and thankyou.

-

Hi All Short version is I owe HPH2 (ex Capital One) £935 since 2011. Hasn't been paid due to dispute between ex wife and I as to who should pay debt. Stubbornly I have until this point refused despite debt being in my name. Today I received a letter from Howard Cohen and Co - Notice of Pending Legal Action. It says I have 10 days from date of letter to respond by either making payment or payment plan with Robinson Way or I will be taken to court for CCJ. I am up against the clock as letter is dated 24th August but only arrived today (1st September). At this point what should I do? 1. Ignore letter (is it just a bluff?) 2. Call Robinson Way and agree a payment plan (can I just offer them a monthly figure or will I have to go through a whole income expenditure exercise? Thought I would offer £35 a month. Will they agree to a plan or insist on total payment which I cant afford? 3. Other - should I be doing something else? Any help greatly appreciated. kind regards Steve