Search the Community

Showing results for tags 'group'.

-

In December my carry on bag was lost/stolen whilst queuing to board a flight overseas. It contained just about everything important, laptop, camera, clothes, sunglasses,makeup the lot. As terrible and distressful this was I knew i had travel insurance to cover me for up to £2k of personal possessions. So i thought! I submitted my claim at the beginning of January. When you submit the claim they take 10 days to respond and tell you if they need further info,this has happened twice, meaning that today 20/2/19 still battling with this. "Please note that your insurance policy has a limit of £150.00 in total for unreceipted items. Therefore, as you have only been able to provide a receipt for the trainers of £73.97, our maximum liability for your claim will be £223.97. This will be paid into your nominated bank account within the next 5 days working days. This has been paid as a gesture of goodwill based on the report you provided as it still does not give all of the necessary information. We suggest you contact the airline for further compensation as they are responsible for the loss, we trust this clarifies our position". I called them and said I was very disappointed with this, as there was nothing for the laptop (It says they will cover upto £500 - the laptop was a gift from my late partner and i sent them receipt which was address to me). I also clarfied that the airline were not responsible and provided documentation accordingly. I.e lost and found reports comcluding item not found. I have missed my mortgage payment as have had to replace my laptop (as i cannot work without it) - they are taking so long to come back to me. Also I purchase essential items on arrival and they have not covered them either. They are not covering the majority of items in my bag basically. They have suggested i contact them via the complaints procedure. I am so annoyed, I took out this cover for peace of mind and it was hardly worth it. For the amount of time its taken to get the claim together, I should have just worked more hours doing my job and i would have basically been better off. Does anyone that is familiar with insurance policies know if it is acceptable to time they take to respond to these things, if i complain today (for them not covering the laptop and essential purchases which were receipted) they will probably take another 10 days to respond!

In December my carry on bag was lost/stolen whilst queuing to board a flight overseas. It contained just about everything important, laptop, camera, clothes, sunglasses,makeup the lot. As terrible and distressful this was I knew i had travel insurance to cover me for up to £2k of personal possessions. So i thought! I submitted my claim at the beginning of January. When you submit the claim they take 10 days to respond and tell you if they need further info,this has happened twice, meaning that today 20/2/19 still battling with this. "Please note that your insurance policy has a limit of £150.00 in total for unreceipted items. Therefore, as you have only been able to provide a receipt for the trainers of £73.97, our maximum liability for your claim will be £223.97. This will be paid into your nominated bank account within the next 5 days working days. This has been paid as a gesture of goodwill based on the report you provided as it still does not give all of the necessary information. We suggest you contact the airline for further compensation as they are responsible for the loss, we trust this clarifies our position". I called them and said I was very disappointed with this, as there was nothing for the laptop (It says they will cover upto £500 - the laptop was a gift from my late partner and i sent them receipt which was address to me). I also clarfied that the airline were not responsible and provided documentation accordingly. I.e lost and found reports comcluding item not found. I have missed my mortgage payment as have had to replace my laptop (as i cannot work without it) - they are taking so long to come back to me. Also I purchase essential items on arrival and they have not covered them either. They are not covering the majority of items in my bag basically. They have suggested i contact them via the complaints procedure. I am so annoyed, I took out this cover for peace of mind and it was hardly worth it. For the amount of time its taken to get the claim together, I should have just worked more hours doing my job and i would have basically been better off. Does anyone that is familiar with insurance policies know if it is acceptable to time they take to respond to these things, if i complain today (for them not covering the laptop and essential purchases which were receipted) they will probably take another 10 days to respond! -

Hi There, Been playing games with MBNA for months now on CCA etc and they passed onto PRA Group to chase, they have come back now and said the application was done digitally! Not sure where I stand now or what I can do? Thank you in advance for your help. Regards Steve H

-

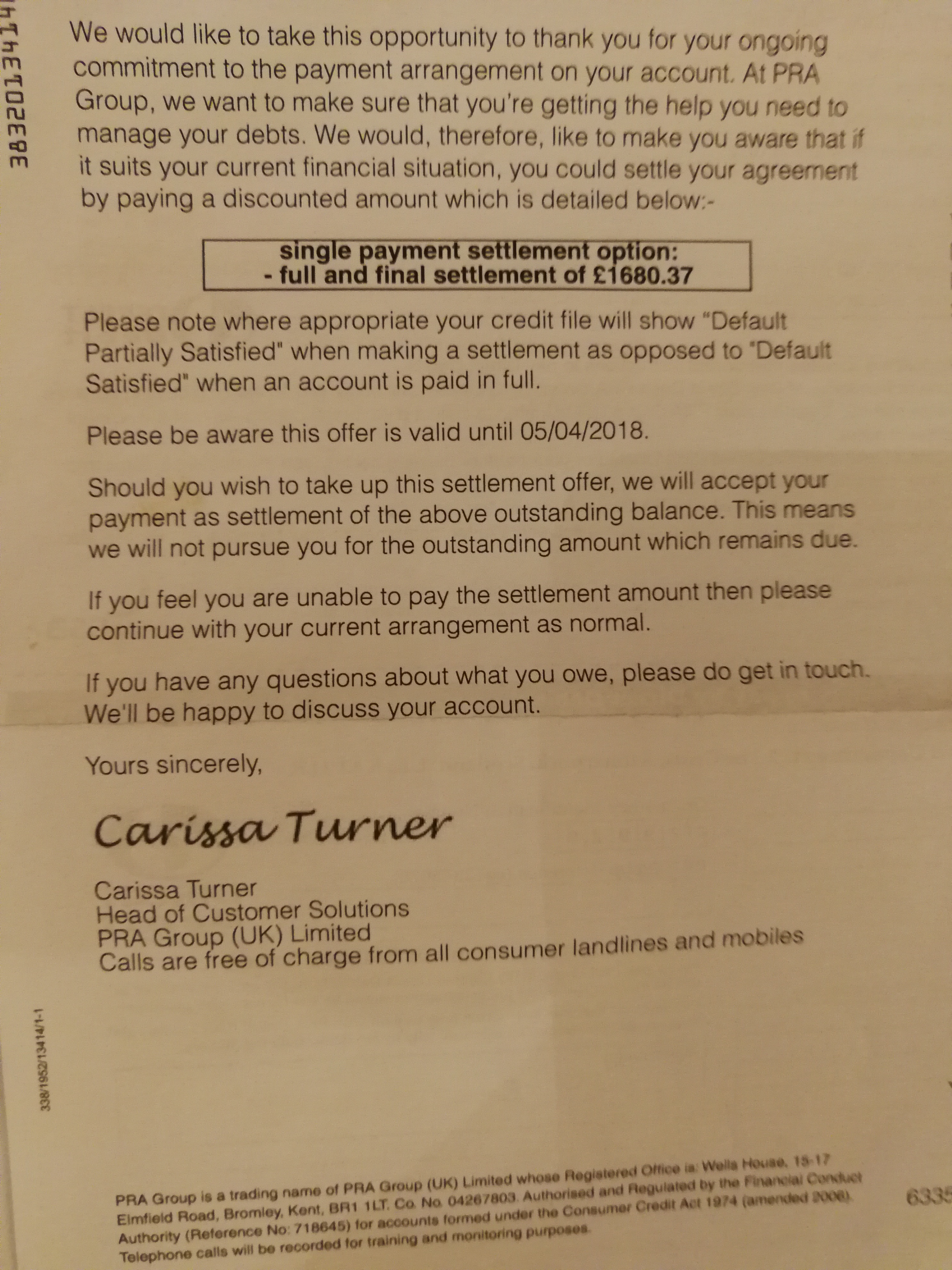

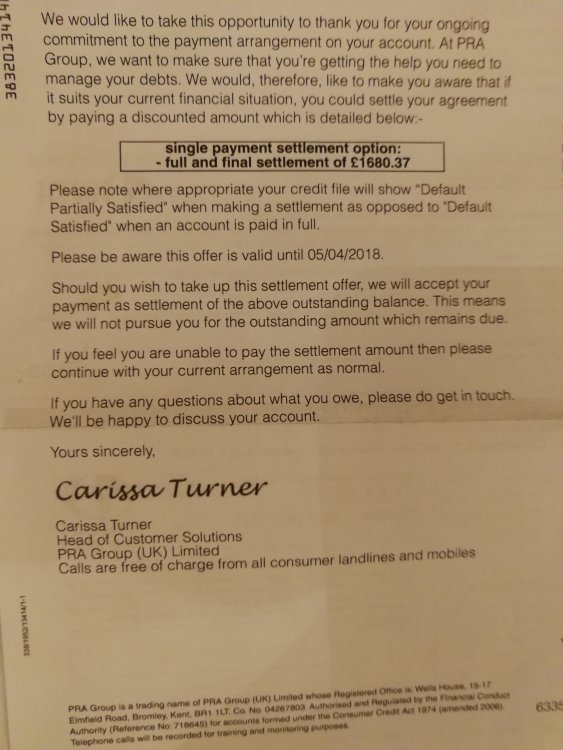

Name of the Claimant ? PRA Group Date of issue 19/12/2018 What is the claim for – 1.The claimant claims the sum of £4793.79 for an outstanding debt owed. 2.On 20.01.2005 the defendant entered into a an agreement with Barclays Bank PLC for a credit card under reference ….. 3.On the 06/05/2011 the defendant defaulted on the agreement with an outstanding balance of £5041.31. 4.On 17/08/2015 the debt of £5041.31 was assigned to PRA Group(UK) Ltd. Notices of assignment were sent to the defendant in accordance with S136 law of property act 1925. Payments of £232.96 were received up to 20/03/20108 and adjustments have been applied in the sum of £14.56. 5.AND THE CLAIMANT CLAIMS 1. The sum of £4793.79 An Egg CC debt £4793.79 + court costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ?Yes What is the total value of the claim? £5058.79 what is the claim for: egg credit card When did you enter into the original agreement before or after April 2007 ? 2005 should I request the CCA I believe they won't have a problem proofing I owe this debt? Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ?No it came off about a year ago Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim.Debt purchaser PRA Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes sure I did ! Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure Why did you cease payments? Had a brain injury What was the date of your last payment?19/12/2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes How shall I defend / respond to this they seem to be using bully tactics and fishing for me to pay up the full amount which I don't have. in March last year they sent me a full and final settlement letter asking for £1680.37 I counter offered £1200 they refused it and said they would only take £1945 which is bizarre. PLEASE SEE ATTACHMENT, I questioned this on another forum and was told the wording is not right and the balance should be zero. If you have not already done so – send a CCA Request to the claimant for a copy of your agreement (except for Overdraft/ Mobile/Telephone accounts) Will Do ! Particulars of Claim An Egg CC debt £4793.79 + court costs I went into arrears in 2010 after a head injury and have been making monthly payments. Egg was bought by Barclaycard since then and then they assigned/sold the debt to the PRA group 17/08/2015. I have been paying without missing a payment but have not done their constant requests for income and expenditure. I got a letter November 13th say my account had been transferred to the investigations and litigation department which I ignored. Thanks for your help I don't have long to respond to this claim

Name of the Claimant ? PRA Group Date of issue 19/12/2018 What is the claim for – 1.The claimant claims the sum of £4793.79 for an outstanding debt owed. 2.On 20.01.2005 the defendant entered into a an agreement with Barclays Bank PLC for a credit card under reference ….. 3.On the 06/05/2011 the defendant defaulted on the agreement with an outstanding balance of £5041.31. 4.On 17/08/2015 the debt of £5041.31 was assigned to PRA Group(UK) Ltd. Notices of assignment were sent to the defendant in accordance with S136 law of property act 1925. Payments of £232.96 were received up to 20/03/20108 and adjustments have been applied in the sum of £14.56. 5.AND THE CLAIMANT CLAIMS 1. The sum of £4793.79 An Egg CC debt £4793.79 + court costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ?Yes What is the total value of the claim? £5058.79 what is the claim for: egg credit card When did you enter into the original agreement before or after April 2007 ? 2005 should I request the CCA I believe they won't have a problem proofing I owe this debt? Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ?No it came off about a year ago Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim.Debt purchaser PRA Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes sure I did ! Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure Why did you cease payments? Had a brain injury What was the date of your last payment?19/12/2018 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes How shall I defend / respond to this they seem to be using bully tactics and fishing for me to pay up the full amount which I don't have. in March last year they sent me a full and final settlement letter asking for £1680.37 I counter offered £1200 they refused it and said they would only take £1945 which is bizarre. PLEASE SEE ATTACHMENT, I questioned this on another forum and was told the wording is not right and the balance should be zero. If you have not already done so – send a CCA Request to the claimant for a copy of your agreement (except for Overdraft/ Mobile/Telephone accounts) Will Do ! Particulars of Claim An Egg CC debt £4793.79 + court costs I went into arrears in 2010 after a head injury and have been making monthly payments. Egg was bought by Barclaycard since then and then they assigned/sold the debt to the PRA group 17/08/2015. I have been paying without missing a payment but have not done their constant requests for income and expenditure. I got a letter November 13th say my account had been transferred to the investigations and litigation department which I ignored. Thanks for your help I don't have long to respond to this claim

-

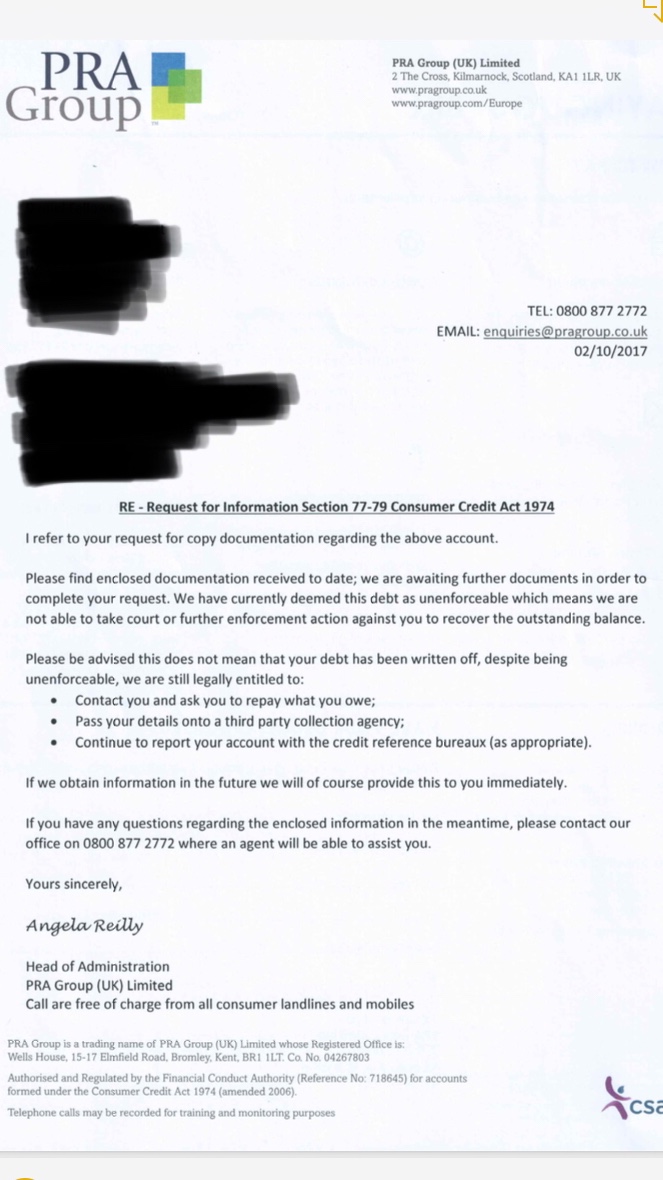

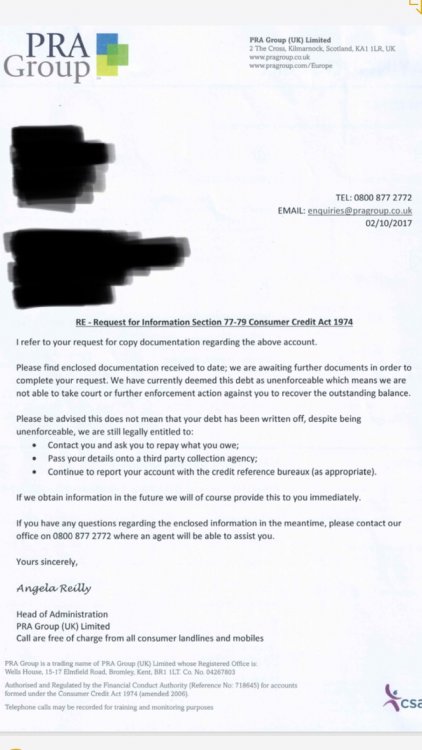

Hi there, Looking to see if someone can give this CCA and accompanying letters a look over, I sent a CCA Request to PRA Group and got the attached back from them is it all there and legit? This is in regard to a recent agreement. Thanks in advance. Barclaycard Letter Redacted.pdf Barclaycard Base CCA Redacted.pdf Barclaycard CCA Redacted.pdf PRA Reply Redacted.pdf

-

I was out of work 4 years ago and agreed a 5 year payment plan with MBNA for a credit card debt (14,000), they stopped the interest , I have been paying this for 4 years +3months never defaulted , I have now received a letter saying they have now sold my debt (1900.00) to The PRA Group … .yesterday I received 3 calls from them which i have not responded to....what happens now? the letter from MBNA says I don't need to do anything and PRA group will carry on the agreement so why are they calling me? any advice appreciated!

-

I have just received my renewal form for ESA. I have been in the support group from the start. Originally claim was based on my depression and severe anxiety. I cannot remember how long since my last assessment but it must be over 5 years+. Since that time my physical health as gone down and I now have emphysema/COPD and severe osteoarthritis. I had one face to face at the beginning and it as all been paper based since then. I have made a "right of access" request for my records. My first question is this the same as a subject access request? Where I get all information about me ie written, digital etc. Secondly will it be useful to know why I was given it last time. Also can their own evidence ie assessments etc be used as nothing as really changed mentally and I have lots of evidence of physical problems.

-

Hi All I have been in an ongoing tennis game with letters going back and fourth with regards to an old debt i had with the bank of scotland (Credit Card) I have sent the usual CCA request to the PRA Group and have received the following A signed credit agreement A notification of assignment - (showing PRA Group as holders of the debt from July 2014) A statement of account up to March 2011 However the statement of account is where I have the issue, they only provided me with a credit card statement up to March 2011, the total they are chasing is lower than the one issued on the statement. I know this should the case as I was using a debt management company (Compass) to handle the account, and they issued payment of £6.49 a month, Compass ironically went under in April 2014, taking my debt savings and no more payments were made to PRA Group. My point is PRA group have only produced a official statement up to 2011, and only provided a spreadsheet on business paper showing payment of £6.49 made a month. There is no official statement showing these payments were made by Compass and especially nothing to indicate compass was acting on my behalf. I am assuming that if PRA group cannot prove the £6.49 payments are made on my behalf, the debt can be classed as Statute Barred as officially my last payment to Bank of scotland would of been in 2011 I have attached the last letter from PRA which includes a sample of the statement they provided (which anyone could knock up on excel). Am I ok to challenge this statement and ask for proof of who paid the £6.49 and confirm documents stating on who's behalf the payments were made? Any help on this is appreciated Thanks

Hi All I have been in an ongoing tennis game with letters going back and fourth with regards to an old debt i had with the bank of scotland (Credit Card) I have sent the usual CCA request to the PRA Group and have received the following A signed credit agreement A notification of assignment - (showing PRA Group as holders of the debt from July 2014) A statement of account up to March 2011 However the statement of account is where I have the issue, they only provided me with a credit card statement up to March 2011, the total they are chasing is lower than the one issued on the statement. I know this should the case as I was using a debt management company (Compass) to handle the account, and they issued payment of £6.49 a month, Compass ironically went under in April 2014, taking my debt savings and no more payments were made to PRA Group. My point is PRA group have only produced a official statement up to 2011, and only provided a spreadsheet on business paper showing payment of £6.49 made a month. There is no official statement showing these payments were made by Compass and especially nothing to indicate compass was acting on my behalf. I am assuming that if PRA group cannot prove the £6.49 payments are made on my behalf, the debt can be classed as Statute Barred as officially my last payment to Bank of scotland would of been in 2011 I have attached the last letter from PRA which includes a sample of the statement they provided (which anyone could knock up on excel). Am I ok to challenge this statement and ask for proof of who paid the £6.49 and confirm documents stating on who's behalf the payments were made? Any help on this is appreciated Thanks -

Hi, Had a letter today from PRA Group for a 16 year old debt had back in 2002 and they're offering a discounted payment i believe the debt would be statute barred? nothing on my credit file is it worth sending a letter under the Limitation Act? Thanks

-

Hi, I appreciate any help on this one. My mum received a letter before claim from bw legal acting on behalf of pra group so we sent a cca request to pra group. This morning she got a response from pra group saying that they were unable to fulfil her request as they have not yet completed the required security checks in order to verify her identity and sent the postal order back. They want her to write or phone to tell them her name, date of birth and previous addresses even though we put her name and adress at the top of the cca request along with the reference no. from bw legals letter. If anyone could give me some advice on how to respond that would be great. I've sent cca request to other dca's in the past but I've never received that response.

-

Good Morning, Today i received a letter from PRA group in relation to a quick quid loan taken out in March 2011, they are offering around a 70% discount, The letter is titled "Could you settle your account?" I did query this loan in 2015 so i have a statement of the account. I was just wondering what my next steps would be to get them to stop hassling me and would this be statue barred as the last payment was made in May 2011. Thanks DC

-

Hi, Just wondering if anyone can help, my claim for income protection has been declined. I have appealed but couldn't see any reason for the insurers to decline the first place I have been diagnosed with depression. Please see the reasons below: 1) They rejected claim without seeking any medical evidence from my doctor 2) They applied a deferred period even though they state it is a linked claim 3) During Rehabilitation Sessions (which turned out to be Claim Assessment Sessions) the specialist was more interested in gathering information to build a predefined conclusion to my absence other than my symptoms I would be grateful if anyone can help with the following: Does my employer have a duty to ensure the claim is assessed fairly Does my employer have a duty to litigate against the insurer Can my employer sack me before I get a decision from the Financial Ombudsman Thanks Ad

Hi, Just wondering if anyone can help, my claim for income protection has been declined. I have appealed but couldn't see any reason for the insurers to decline the first place I have been diagnosed with depression. Please see the reasons below: 1) They rejected claim without seeking any medical evidence from my doctor 2) They applied a deferred period even though they state it is a linked claim 3) During Rehabilitation Sessions (which turned out to be Claim Assessment Sessions) the specialist was more interested in gathering information to build a predefined conclusion to my absence other than my symptoms I would be grateful if anyone can help with the following: Does my employer have a duty to ensure the claim is assessed fairly Does my employer have a duty to litigate against the insurer Can my employer sack me before I get a decision from the Financial Ombudsman Thanks Ad -

Hi, I'm new to this forum and looking to get some advice on a dispute my parents are having. They paid (by cheque) to have new Soffits and Fascia’s fitted by a company called EnviroTherm based in Ilkeston, Derbyshire. https://www.envirothermgroup.com/ My parents received a phone call out of the blue from a salesman who had provided a quote for the work 2/3 years ago saying he had moved company (to EnviroTherm) and asking to visit them to provide a new quote as he felt his new company would be cheaper. His new company (EnviroTherm) were more expensive until he phoned his manager and knocked around £1,000 off the price bringing the total price down to £2,375. I know this is a sales tactic but unfortunately they fell for it. My parents paid a 50% deposit which was £1,187.50. The deposit was only refundable within 14 days but EnviroTherm contacted my parents after 14 days had passed demanding an extra £1,500 for scaffolding. My parents stated that they would not pay the extra money and if the work couldn't be carried out for the agreed price they wanted their money back. EnviroTherm initially argued that their request was after the 14 days but when my parents argued the fact that the agreed price had been changed after the 14 days EnviroTherm agreed to refund their deposit. The process of getting EnviroTherm to agree to refund the deposit took many phone calls to speak to the manager who was always in a meeting or out of the office. One day my mum was even advised in the morning that he was in a meeting and later that day that he wasn't in work that day. Eventually, after many phone calls and many false claims to have posted a cheque EnviroTherm did send a cheque to my parents last Wednesday (25th April) which they received the next day and paid into the bank on Friday. Today my parents have been advised that the cheque has been cancelled by the company. The company have answered my mum's phone call today and claimed they are looking into the situation. They asked for her bank details but she didn't give these as she doesn't trust the company and instead demanded a new cheque. She's currently waiting to hear back. We're not hopeful of getting this resolved as my research into the company has highlighted that it is owned by a Jason David Rowan or Lord Jason David Rowan who was the owner of EnergySave who featured on Rogue Traders for their pressurised selling similar to that used on my parents but also much worse as well as their racism. I'm looking for advice on what legal step to take? I've read about a letter before action, is that the next step to take? I feel that they need to put something in writing the company as most of her communication has been over the phone. Any help or advice would be gratefully received!

Hi, I'm new to this forum and looking to get some advice on a dispute my parents are having. They paid (by cheque) to have new Soffits and Fascia’s fitted by a company called EnviroTherm based in Ilkeston, Derbyshire. https://www.envirothermgroup.com/ My parents received a phone call out of the blue from a salesman who had provided a quote for the work 2/3 years ago saying he had moved company (to EnviroTherm) and asking to visit them to provide a new quote as he felt his new company would be cheaper. His new company (EnviroTherm) were more expensive until he phoned his manager and knocked around £1,000 off the price bringing the total price down to £2,375. I know this is a sales tactic but unfortunately they fell for it. My parents paid a 50% deposit which was £1,187.50. The deposit was only refundable within 14 days but EnviroTherm contacted my parents after 14 days had passed demanding an extra £1,500 for scaffolding. My parents stated that they would not pay the extra money and if the work couldn't be carried out for the agreed price they wanted their money back. EnviroTherm initially argued that their request was after the 14 days but when my parents argued the fact that the agreed price had been changed after the 14 days EnviroTherm agreed to refund their deposit. The process of getting EnviroTherm to agree to refund the deposit took many phone calls to speak to the manager who was always in a meeting or out of the office. One day my mum was even advised in the morning that he was in a meeting and later that day that he wasn't in work that day. Eventually, after many phone calls and many false claims to have posted a cheque EnviroTherm did send a cheque to my parents last Wednesday (25th April) which they received the next day and paid into the bank on Friday. Today my parents have been advised that the cheque has been cancelled by the company. The company have answered my mum's phone call today and claimed they are looking into the situation. They asked for her bank details but she didn't give these as she doesn't trust the company and instead demanded a new cheque. She's currently waiting to hear back. We're not hopeful of getting this resolved as my research into the company has highlighted that it is owned by a Jason David Rowan or Lord Jason David Rowan who was the owner of EnergySave who featured on Rogue Traders for their pressurised selling similar to that used on my parents but also much worse as well as their racism. I'm looking for advice on what legal step to take? I've read about a letter before action, is that the next step to take? I feel that they need to put something in writing the company as most of her communication has been over the phone. Any help or advice would be gratefully received! -

I was on income based ESA in the support group. I just got a letter today, 29 Mar 2018, dated 23 Mar 2018 that my ESA will be cancelled from 27 Mar 2018. Reason: You have not paid or been credited with enough National Insurance Contributions. We have based the tax years ending 5 April 2011 and 5 April 2012 to assess your claim. What confused me is that I was claiming JSA all through those tax years. I thought JSA credited NI payments? Also, in the same letter it says: We will still credit you with National Insurance contributions while claiming Employment and Support Allowance. So, I am confused. How can I run out of NI payments on income based ESA in the support group? There are absolutely no instructions what to do next. They cancelled my ESA 2 days before I received the letter so I have absolutely no income provision. What are my options? Will my housing benefit be cancelled and I am made homeless again?

-

I hope I'm in the right forum for this. I've just made my fortnightly signing on at the job centre and saw someone I have not seen before. When I presented my usual print out of job application emails etc. (trial and error has taught me this is the most idiot proof way to present a job search) she advised me that I didn't have to do that and pretty soon they will be introducing 'group signings' where people attend in groups of about 15 and can just show their job search on their tablet or phone. Apparently they will soon not have enough staff to do anything more personal. 'You can just show them your job search on your phone or tablet' she said I pointed out that I had neither a mobile phone nor a tablet, just a laptop at home, and would prefer to continue bringing in my print outs - didn't mention it was because it's idiot proof but that is why lol - even if I had a phone or tablet I would certainly not be offering up my email or any other personal account to their scrutiny. She then mentioned I could use their computers to go into these account but I found out weeks ago that they use Open Office, cannot open pdf documents, and in any case I was not prepared to do this, I maintained that I preferred to bring in the print outs, and pointed out that it is entirely up to me how I present my job search and this is the method I chose. This was not in any way a nasty conversation and I was actually laughing by now and asked her if she really thought this was going to work, her face said she knew it wouldn't. 'It'll be like a chimps tea party won't it' I suggested, she seemed to agree. ' I bet I'll be the first one out the door after showing someone my print out won't I' she still seemed to agree but now wanted me to leave because I was making too much sense, my first attempt to sign went very wrong because I was laughing so I had to do it again (a first) I've had a bit of a Google and can't find anything about what promises to be an entertaining farce - at least for anyone with a print out of their job search. Anyone heard of or had experience of this 'group signing'?

-

hi guys hoping someone can shed some light on this. applied for universal credits 14/12/16, handing in fit notes ever since etc been waiting since to have WCA and i called to ask what was happening with that on friday UC said my work group had changed to no work related activity and i wouldn't have to attended the appointment they scheduled for me, that for me is a weight off my shoulders since i have agoraphobia being forced to go to the job centre every month always ends up with me in a state crying because i don't want to be outside. anyway, the advisor couldn't work out why now that my group has changed, that there wasn't any payment issued since i've been waiting since Dec 2016. Case manager was meant to call me back friday by 6pm, which never happened. i've had problems with him before, meant to contact me before 6pm the day i called, this was nearly 5 weeks ago and i'm still waiting. anyway, rambling on here. i just want to know really peoples experiences once their work group changed, how long did it take to receive their back payment. My work group changed on the 16th so it seems like its taking longer than it should. im just worried because even though my group has changed, theyve told me that i don't need to go to anymore appointments yet another advisor that i spoke to said i still have to go. if i don't go, i dont get paid and then i dont have any money for myself and my kids to live on. hope someone can put my mind at ease since i'm getting stressed out which isn't helping my current condition. thanks guys

-

Hi there, My wife and I have unfortunately gotten ourselves into around £20,000 of debt. I recently wrote to the agencies sending out letters using the template to ask for the signed credit agreement. We have received this back from PRA GROUP. Could someone possibly give us some advice on what we need to do next Thank you Here

-

Hello ,had a letter today from PRA saying I owed £3,900 I telephoned them and asked what is this about was told it was from a car finance debt from 2011 and not at the address I been living at for 13 years. I asked to see copies of credit agreement which the response was they did not have. after the telephone call ended and asked family I remembered having finance for a car in 2004 and that was the only one I had. Can they still chase me for that debt and why are they saying the debt is from 2011 ?

Hello ,had a letter today from PRA saying I owed £3,900 I telephoned them and asked what is this about was told it was from a car finance debt from 2011 and not at the address I been living at for 13 years. I asked to see copies of credit agreement which the response was they did not have. after the telephone call ended and asked family I remembered having finance for a car in 2004 and that was the only one I had. Can they still chase me for that debt and why are they saying the debt is from 2011 ? -

Hello BWlegal has sent a letter dated 14th August 2017 requesting a final payment from me. I see that the debt they refer to is a closed account on my credit file and the last record on the credit file was from T/A Payday Express, (and recorded by them) showing as 'satisfied ' default assigned in January 2017. I have not paid any monies toward the debt which had a default registered from 2013 until January 2017. There have been no default notices recorded after January 2017. I have letters from Payday Express and Prac dated April 2017 saying the debt was assigned in December 2016 to Prac who use BWlegal. I hope the above is not too confusing, I do want to resolve the issue but is bwlegal entitled to be asking for payments from me? Look forward to your responses

Hello BWlegal has sent a letter dated 14th August 2017 requesting a final payment from me. I see that the debt they refer to is a closed account on my credit file and the last record on the credit file was from T/A Payday Express, (and recorded by them) showing as 'satisfied ' default assigned in January 2017. I have not paid any monies toward the debt which had a default registered from 2013 until January 2017. There have been no default notices recorded after January 2017. I have letters from Payday Express and Prac dated April 2017 saying the debt was assigned in December 2016 to Prac who use BWlegal. I hope the above is not too confusing, I do want to resolve the issue but is bwlegal entitled to be asking for payments from me? Look forward to your responses -

I bought my current Home Contents Insurance a few months ago from Intelligent Insurance and paid annually, upfront. Last month I lost my laptop and iPad after leaving one of my bags behind in a store. I returned to the store and periodically checked to see whether the items had been handed in. I also called the police to report the loss. The following morning I contacted my insurance company to make a claim. I was asked to explain what had happened and to email over receipts proving ownership of the lost items as well as photos of the boxes the items had come in. I did all this straight away. Then I heard nothing at all for 8 days. Finally I was told a Loss Adjustor from Davies Group would be ringing me to "interview" me. The phone interview with the Loss Adjustor lasted for around one hour. The Loss Adjustor requested an increasingly over the top array of documents. He accepted he'd already received ample evidence proving I owned the two lost items. He now asked for receipts and bank statements to document which grocery shops I'd visited to buy groceries in PRIOR to losing my items. Bus and train tickets proving I was in the area. Further receipts proving I was in the shop where I lost my laptop. And various other documents. I sent everything he had requested and answered all of his increasingly bizarre questions. A further three or so days later, the Loss Adjustor emailed me to say he'd sent his report over to the underwriters and they'd sort out settlement of the claim. That was over a week ago. I've now been told, today, all of the following by Davies Group: "We've not received instructions back yet from your underwriter" "Actually we have received instruction from your underwriter but we can't tell you what it says." "We may need to pursue further lines of enquiry." "We may require further communication." "It could take up to 40 or 50 days to give you an answer." "We can't tell you yet whether we will accept your claim." "We've no idea when we will have an update." "The person dealing with your claim is in a meeting." "The person dealing with your claim isn't in the office this week." WHAT ON EARTH?

I bought my current Home Contents Insurance a few months ago from Intelligent Insurance and paid annually, upfront. Last month I lost my laptop and iPad after leaving one of my bags behind in a store. I returned to the store and periodically checked to see whether the items had been handed in. I also called the police to report the loss. The following morning I contacted my insurance company to make a claim. I was asked to explain what had happened and to email over receipts proving ownership of the lost items as well as photos of the boxes the items had come in. I did all this straight away. Then I heard nothing at all for 8 days. Finally I was told a Loss Adjustor from Davies Group would be ringing me to "interview" me. The phone interview with the Loss Adjustor lasted for around one hour. The Loss Adjustor requested an increasingly over the top array of documents. He accepted he'd already received ample evidence proving I owned the two lost items. He now asked for receipts and bank statements to document which grocery shops I'd visited to buy groceries in PRIOR to losing my items. Bus and train tickets proving I was in the area. Further receipts proving I was in the shop where I lost my laptop. And various other documents. I sent everything he had requested and answered all of his increasingly bizarre questions. A further three or so days later, the Loss Adjustor emailed me to say he'd sent his report over to the underwriters and they'd sort out settlement of the claim. That was over a week ago. I've now been told, today, all of the following by Davies Group: "We've not received instructions back yet from your underwriter" "Actually we have received instruction from your underwriter but we can't tell you what it says." "We may need to pursue further lines of enquiry." "We may require further communication." "It could take up to 40 or 50 days to give you an answer." "We can't tell you yet whether we will accept your claim." "We've no idea when we will have an update." "The person dealing with your claim is in a meeting." "The person dealing with your claim isn't in the office this week." WHAT ON EARTH? -

Hi, I am hoping someone here can give me some advice as I am really worried about this I changed my home insurers to John Lewis (from NatWest) in January this year. No specific reason as I was always happy with NatWest but my premium had increased so I shopped around. To my knowledge I gave JL details of all previous claims (i.e. I am not aware that I failed to mention any) and I did not take out no claims protection or did I benefit from a no claims reduction in my new policy. In June last year I claimed with Natwest for a damaged speaker under the accidental section of my policy. Last Thursday my daughter dropped one of my wireless speakers and it was not repairable so, given the cost of it (£499), I contacted JL to make a claim. They offered me a cash settlement which I was happy with but then called to say that "due to the number of undisclosed claims" they would be referring not only my claim for the speaker but also my entire policy to their underwriters. Today I get a call from the Cotswold Group wanting to interview me over the telephone about my claim. I didn't answer because I was in a meeting. I googled them and they are private investigators and insurance fraud specialists I then received an email asking me to make an appointment to discuss my claim and policy naturally I am very confused and scared as to why JL have instructed them to contact me? I decided that given the simplicity of the claim I would call JL to advise them I no longer wanted to proceed as it all seemed rather odd. The chap I spoke to said "I will pass this on to our specialist team" which again caused some alarm. He was very abrupt and then literally minutes later I get another email from The Cotswold Group saying this: "I have received a call from John Lewis to advise of your call mentioned below. They have confirmed they are unable to accept the withdrawal of the claim as we have been appointed to carry out further enquiries in relation to your claim and policy before any decision can be agreed." They are INSISTING I speak to them and I am thinking Why am I being investigated for what JL obviously think is insurance fraud by a team of private investigators specialising in "deep web mining"? Even if i did omit to mention the NatWest Claim last year it was definitely not on purpose! I am quite literally terrified now. Can someone please help or explain why they are doing this and how I should respond to the email from The Cotswold Group. Why are JL refusing to allow me to drop my claim??

Hi, I am hoping someone here can give me some advice as I am really worried about this I changed my home insurers to John Lewis (from NatWest) in January this year. No specific reason as I was always happy with NatWest but my premium had increased so I shopped around. To my knowledge I gave JL details of all previous claims (i.e. I am not aware that I failed to mention any) and I did not take out no claims protection or did I benefit from a no claims reduction in my new policy. In June last year I claimed with Natwest for a damaged speaker under the accidental section of my policy. Last Thursday my daughter dropped one of my wireless speakers and it was not repairable so, given the cost of it (£499), I contacted JL to make a claim. They offered me a cash settlement which I was happy with but then called to say that "due to the number of undisclosed claims" they would be referring not only my claim for the speaker but also my entire policy to their underwriters. Today I get a call from the Cotswold Group wanting to interview me over the telephone about my claim. I didn't answer because I was in a meeting. I googled them and they are private investigators and insurance fraud specialists I then received an email asking me to make an appointment to discuss my claim and policy naturally I am very confused and scared as to why JL have instructed them to contact me? I decided that given the simplicity of the claim I would call JL to advise them I no longer wanted to proceed as it all seemed rather odd. The chap I spoke to said "I will pass this on to our specialist team" which again caused some alarm. He was very abrupt and then literally minutes later I get another email from The Cotswold Group saying this: "I have received a call from John Lewis to advise of your call mentioned below. They have confirmed they are unable to accept the withdrawal of the claim as we have been appointed to carry out further enquiries in relation to your claim and policy before any decision can be agreed." They are INSISTING I speak to them and I am thinking Why am I being investigated for what JL obviously think is insurance fraud by a team of private investigators specialising in "deep web mining"? Even if i did omit to mention the NatWest Claim last year it was definitely not on purpose! I am quite literally terrified now. Can someone please help or explain why they are doing this and how I should respond to the email from The Cotswold Group. Why are JL refusing to allow me to drop my claim?? -

Hello all !, I received a letter from PRA Group a couple of days ago. Letter opens with "in order to comply with our obligations under the Consumer Credit Act 1974, We are providing you with this statement of your account. Opening bal: £545.40 Total payments recieved £0.00 Balance adjustments £0.00" Letter also gives a ref number and says I owed Lloyds TSB Bank PLc, the agreement date was 30 May 2002. And offers a settlement payment amount of £54.54. I have never had an account with Lloyds TSB. I panicked thinking someone may have stolen my details, as I've never had a letter of this nature before. Have checked credit files from the usual three and there's nothing. My name is a common name (G Jones), I work with two others with the same first and sir name so had thought it could be for a different G Jones but that doesn't account for the letter having my address on it. Do I contact PRA Group ? Do I ignore ? I'm not sure what to do, not slept the last two days. Thanks in advance and apologies if I've posted in the wrong place or duplicated a thread. G

-

I need some advice on how to proceed with PRA Group?, over the past years PRA have written to me regarding a debt going back over 7 - 8 years that is owed to Nationwide, just recently they have started writing to me again and their latest letter is not offering their usual hefty discount but instead 'Dear xxxx Could you settle your account?'. Also on their letter they state an agreement date of 13 January 2005, this was not an agreed overdraft but my bank account went overdrawn by a very small amount (just over £10 if I remember rightly) and I was hit with multiple bank charges which caused the account to go even further overdrawn which lead to even more bank charges being added on top, the amount owed according to PRA is £390. After researching the forums I sent the Statute Barred letter to PRA as I was 100% sure that no payments have ever been made by me on this account, today I received a e-mail from PRA stating 'Thank you for your query which we received on 19/05/2017 in which you advised your account has now exceeded the period specified in the “Limitations Act 1980”. Under the “Limitations Act 1980” we have six years to collect the outstanding balance and after this time the debt becomes unenforceable. This means that we are unable to pursue this through the courts. Our records indicate that the last payment made to the account was on 28/02/2017. Please be advised that this payment is deemed as acknowledgement of the debt and as such, would reset the limitations period for a further 6 years from this date. Whilst I appreciate that this may not be the response you were looking for, please be aware that we at PRA Group (UK) remain committed to working with you to come to an appropriate resolution. We have requested documentation from Nationwide. As PRA Group UK Limited do not hold the information internally, we have held your account until our client is able to provide the documentation applied for. During this time you will receive no further letters or calls.' I would like some advice regarding their e-mail as I HAVE NOT MADE ANY PAYMENTS against this debt so I would like to know where they got this date from, I have replied to their e-mail asking for details regarding this payment and I confirmed to them that I have absolutely no knowledge of this payment being made. Are they chancing their luck?

-

I have recently contacted this company regarding a claim. The person who dealt with my call was aggressive and hostile and frequently interrupted me/ talked over me. Aside from this poor communication, the employee continued to insist that a part could be fixed when in fact I had been advised by two separate garages that it could not and would have to be replaced. Then he proceeded to blame the garage. They insist that they will only cover the amount of the part if it had been repaired but of course it cannot be repaired. Has anyone else dealt with this company? Any tips?

-

Hi CAG, Just looking for a quick bit of info. Was placed in ESA Support Group for 2 years from Feb 15 - Feb 17. Obviously we are beyond that date so I'm waiting to hear something any day now. I go away for 10 nights on May 15th (First Holiday in around 10 years) wondering what to do if they throw something in my letter box asking for a re-assessment while I'm set to be away? Am I entitled to go away while I'm in the ESA Support Group and should I inform somebody that I have chosen to do so? Anybody got any idea how long I may be waiting to hear from then as we are now over the 2 recomendded years since I was placed. Thank you in advance for any input, Adam

-

I am starting this thread on behalf of my brother who desperately needs some help. He should've been on Group Income Protection by September however due to his bad health he never chased that up. He was then invited to attend a functional capacity assessment on behalf of insurer in January which itself was around 4 months later than when he should’ve started on income protection. He gave in his 200% in that assessment to a level that he ended up being with swollen legs and pain for next 2 weeks to follow. His illness started around March last year when he was getting bullied at his work place which caused him work-related stress and depression. The bullying continued and that lead him to a stage that he experienced paralysis symptoms in left side and lost strength in left side of body and he ended up being hospitalised. Subsequent tests and check-ups, physiotherapy (neuro physio), neurology consultants after thorough diagnosis ruled out stroke (luckily) and diagnosis were work related stress that caused his functional hemiparesis (losing strength in left side of his body). During this time, the management were still stressing his through different means while he had been off sick as a result his stress and depression got so out of control that it triggered Schizophrenia in him including hearing voices and hallucinations. Things like not being around for the family and being unable to carry out day to day activities worsening his condition and since then he is in care of Mental Health team. After a month, he received a letter of rejection quoting my brother doesn’t fulfil definition of incapacity and his claim was getting rejected. The basis of rejection was they believe there is no evidence of medical condition causing significant impairment in function and his reporting is inconsistent and unreliable (even though he disputes). They cited clinician believed there were number of inconsistencies in my brother’s reporting and his ability of walking and standing during formal testing were inconsistent with his reported left side weakness (even though he pushed himself over pain barrier to carry out these activities). They used around 1-2-day surveillance on him which was done approximately for around 1-2 weeks prior to his assessment and they quoted that surveillance showed him walk and stand unaided whilst grocery shopping and grip items and grocery shopping bags which doesn’t indicate functional loss. Even though they agree there is evidence that he used walking stick and displayed uneven gait throughout surveillance footage. He maintains that the bags referred to were very light. He also says that he doesn’t do these as day to day activity however on that particular day he was severely depressed as this shopping even though caused him physical pain but he did that as it gave him distraction and mental reassurance that he is not a burden on others. Now his mental health condition has further deteriorated due to further stress hence I am helping him with this and he has been given 90 days to appeal against this decision. I wish to get advice on following: 1) What should be his first steps to challenge this? 2) Given that he is physically incapacitated (as per treating doctor, physio and consultant) what weight does assessment from functional assessors carry when they say he is not functionally incapacitated considering they are paid by the insurers? 3) Does just lifting some light grocery bags justify him not being incapacitated? Even though he says it is not one of his regular activities and he did that to fight his depression and it caused him significant pain and distress? Considering that even they mentioned that surveillance shows him using walking stick and maintaining uneven gait throughout the surveillance footage) 4) Even if we ignore him moving with support and with uneven gait for the sake of argument agree with insurers no functional loss argument does high degree of depression and Schizophrenia including voices and hallucination not constitute incapacity considering his job involves high physical activities and care? 5) Considering he was supposed to be on Income Protection in September was it a fair practice from the company to get his evaluation done in January (approximately 4 months later)? 6) Is assessing someone nearly 4 months after they should’ve been on Income Protection good indicator how their condition was 4 months ago? 7) What should happen for the time between when he was due to be on Income Protection and till they assessed him? Any help is highly appreciated