Search the Community

Showing results for tags 'fees'.

-

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) The Local Government Ombudsman's office has just released the following decision. Re: London Borough of Haringey. The complaint 1. The complainant, who I shall call Ms A, complains the Council allowed her to make payment towards an outstanding Penalty Charge Notice (PCN) although it had passed the matter to its enforcement agents (bailiffs), incurring additional costs. What I found 4 The Council issued Ms A a PCN for a parking contravention on 29 September 2015. Ms A did not pay or make formal representations against the PCN so the Council pursued the debt against her. It issued a warrant of execution and passed the debt to its bailiffs to enforce on 16 June 2016. 5. Ms A made a payment of £97 for the PCN using the Council’s online system on 23 June 2016. However by this point the Council had already passed the case to its bailiffs, incurring further costs. Ms A says she paid the fine so bailiff action should cease. However, the Council says she is still liable for the bailiff fees. Ms A says the Council should not have allowed her to make a payment online when the case was with its bailiffs. The Council confirmed it passed the debt onto the enforcement agency on 13 June because it had not received payment and sent a Notice of Enforcement on 16 June. 6. Ms A complained to the Council that she had not received the statutory notices the Council says it sent. The Council confirmed it sent the notices to the registered keepers address. These included the Notice to Owner, the Charge Certificate and the Order of Recovery. Each notice summarised the amount due at each stage. The Council said Royal Mail did not return the letters as undelivered so considered them served. The Council included copies of the notices it sent to Ms A in its response to her complaint. 7. A motorist may make part-payment towards a PCN debt and there was no reason for the Council to refuse Ms A’s payment made on 23 June 2016. Ms A sought to challenge the Council’s action but was unsuccessful, and the Council is therefore entitled to pursue the debt against her, including by passing the case to its bailiffs. Ms A made payment only after the case had been referred to bailiffs and the Ombudsman cannot therefore say she is not liable for the bailiff’s fees. The Council’s acceptance of Ms A’s payment has also not caused Ms A an injustice as it has been put towards the cost of the PCN and bailiff’s fees incurred to pursue it. http://www.lgo.org.uk/decisions/transport-and-highways/parking-and-other-penalties/16-008-073

The Local Government Ombudsman's office has just released the following decision. Re: London Borough of Haringey. The complaint 1. The complainant, who I shall call Ms A, complains the Council allowed her to make payment towards an outstanding Penalty Charge Notice (PCN) although it had passed the matter to its enforcement agents (bailiffs), incurring additional costs. What I found 4 The Council issued Ms A a PCN for a parking contravention on 29 September 2015. Ms A did not pay or make formal representations against the PCN so the Council pursued the debt against her. It issued a warrant of execution and passed the debt to its bailiffs to enforce on 16 June 2016. 5. Ms A made a payment of £97 for the PCN using the Council’s online system on 23 June 2016. However by this point the Council had already passed the case to its bailiffs, incurring further costs. Ms A says she paid the fine so bailiff action should cease. However, the Council says she is still liable for the bailiff fees. Ms A says the Council should not have allowed her to make a payment online when the case was with its bailiffs. The Council confirmed it passed the debt onto the enforcement agency on 13 June because it had not received payment and sent a Notice of Enforcement on 16 June. 6. Ms A complained to the Council that she had not received the statutory notices the Council says it sent. The Council confirmed it sent the notices to the registered keepers address. These included the Notice to Owner, the Charge Certificate and the Order of Recovery. Each notice summarised the amount due at each stage. The Council said Royal Mail did not return the letters as undelivered so considered them served. The Council included copies of the notices it sent to Ms A in its response to her complaint. 7. A motorist may make part-payment towards a PCN debt and there was no reason for the Council to refuse Ms A’s payment made on 23 June 2016. Ms A sought to challenge the Council’s action but was unsuccessful, and the Council is therefore entitled to pursue the debt against her, including by passing the case to its bailiffs. Ms A made payment only after the case had been referred to bailiffs and the Ombudsman cannot therefore say she is not liable for the bailiff’s fees. The Council’s acceptance of Ms A’s payment has also not caused Ms A an injustice as it has been put towards the cost of the PCN and bailiff’s fees incurred to pursue it. http://www.lgo.org.uk/decisions/transport-and-highways/parking-and-other-penalties/16-008-073 -

Morning Continuing to go through all my credit card/bank account files and checking the grand total of Late Payment Fees and other such charges. Finally got to Barclaycard today. I have had a Barclaycard credit card since 03. I have just collated all the Late Payment Fees B'Card added from 05 to date. Interestingly - from mid 2011 until start 2014 only - B'Card also added a charge titled "Interest on default Sum". Before and after these dates B'card never isolated and advised this charge. The total of charges from 05 = apx £650. The total of compound Interest @ 29.9% = apx £2100 The sum total = apx £2750 My current B'card balance is £5k. So should I now write a nice letter asking for them to reimburse these charges? And also asking them to stop adding them on to future statements ? Thanks for any response....

Morning Continuing to go through all my credit card/bank account files and checking the grand total of Late Payment Fees and other such charges. Finally got to Barclaycard today. I have had a Barclaycard credit card since 03. I have just collated all the Late Payment Fees B'Card added from 05 to date. Interestingly - from mid 2011 until start 2014 only - B'Card also added a charge titled "Interest on default Sum". Before and after these dates B'card never isolated and advised this charge. The total of charges from 05 = apx £650. The total of compound Interest @ 29.9% = apx £2100 The sum total = apx £2750 My current B'card balance is £5k. So should I now write a nice letter asking for them to reimburse these charges? And also asking them to stop adding them on to future statements ? Thanks for any response.... -

Propsed fees for failure to notify a change of circumstances to a Local Authorities (LA) in regards to Council tax and possibly Housing benefit too! My local LA (Southend on sea Borough Council) SBC)) has recently had a full Council meeting and are propsing charging people for failing to notify a change of circumstances. This could be between £70-£280! (please see my attacments (1) (2). 2 for the quick version and 1 for the full document. Or see section 6 page 67 all... This was previously just £50 now the new rates could cause more financial issues for many people. 2 RECOMMENDATIONS 2.1 That the Executive agree that consultation takes place on the implementation of a fixed penalty of £70 to Council tax charge payers, permitted under the provisions of the Local Government Finance Act 1992, who intentionally or knowingly fail to notify the Council of any change affecting Council Tax Liability or Local Council Tax Benefit Scheme (LCTBS) without reasonable excuse. 3 REASONS FOR RECOMMENDATIONS 3.1 The Council has powers under the Local Government Finance Act 1992 (Schedule 3) to impose civil penalties to those charge payers who wilfully neglect to inform the Council of changes which affect their Council Tax liability. There are at least 6 areas that could affect the claimant/bill payer this could be on top of what DWP already charge. It could pay to ask your LA if they also intend on doing the same as mine. Given that most LAs now have to find new inovative ways to get more money in their coffers then this one surely is a way to make money from failure to notiy a change of circumstances in a reasonable time frame (normally 28 days) sometimes less.... Info here and other places >> https://www.gov.uk/civil-penalty-changes-affect-benefits Your thoughts.... Benefit failure fees.pdf Public reports pack 14th-Feb-2017 14.00 Cabinet[556].pdf

-

Hello all, I can't quite believe this forum and site exists with such great advice and information!! well done to all involved. Now on to my problem (amounts slightly varied to keep anonymity) I was lent £20,000 from an ex employer who also happened to be my boyfriend at the times family business (big mistake) It was lent on the basis I would repay it when I could. Interest would not be charged. some unfortunate events happened and I had to stop working for them. I offered 3 dates when I would return the money in instalment. The first date I kept and paid them the £10,000 as promised. Unfortunately relations with them went down hill and I had stored around £10,000 worth of goods at their home. They were not being forth coming with returning my items or even allowing me to pick them up. I wasn't sure and still am not if my items still exist. And so I decided i would offer the second installment in person at their home so I could pick up my belongings. I sent over 20 emails offering dates saying I would happily give them the cheque. I heard nothing back. Sadly a few months later I became ill and have been signed off work for 6 months and been away from my home recovering. Unbeknown to me during this time they had sent one email to my sister asking for my address in which my sister responded saying she couldn't give out my location as I was very ill and she didn't feel it was ok to raise this subject with me. Forward 5 months when I return to my home in England and I have a ccj issued against me and I have x amount of days to pay. I sent a letter straight away to their lawyer stating I had been ill and I would have responded if I had received the letters. They responded saying I had 15 days to reply. 3 days later I sent an offer letter to their lawyers along with doctors notes to prove I was sick. I am currently waiting for their response. But I am very very worried because A. I have a ccj against my name and I would really be grateful of any advice setting this aside? Can I do it on the basis I never received it because of my illness? B. I am on the understanding I only had 28 days after the ccj was issued to come to an agreement or they could go to court to issue baliffs etc? It is day 25 today! ANY HELP so much appreciated. Very stressed and trying to remain calm so I don't get sick again! Kind Regards x

Hello all, I can't quite believe this forum and site exists with such great advice and information!! well done to all involved. Now on to my problem (amounts slightly varied to keep anonymity) I was lent £20,000 from an ex employer who also happened to be my boyfriend at the times family business (big mistake) It was lent on the basis I would repay it when I could. Interest would not be charged. some unfortunate events happened and I had to stop working for them. I offered 3 dates when I would return the money in instalment. The first date I kept and paid them the £10,000 as promised. Unfortunately relations with them went down hill and I had stored around £10,000 worth of goods at their home. They were not being forth coming with returning my items or even allowing me to pick them up. I wasn't sure and still am not if my items still exist. And so I decided i would offer the second installment in person at their home so I could pick up my belongings. I sent over 20 emails offering dates saying I would happily give them the cheque. I heard nothing back. Sadly a few months later I became ill and have been signed off work for 6 months and been away from my home recovering. Unbeknown to me during this time they had sent one email to my sister asking for my address in which my sister responded saying she couldn't give out my location as I was very ill and she didn't feel it was ok to raise this subject with me. Forward 5 months when I return to my home in England and I have a ccj issued against me and I have x amount of days to pay. I sent a letter straight away to their lawyer stating I had been ill and I would have responded if I had received the letters. They responded saying I had 15 days to reply. 3 days later I sent an offer letter to their lawyers along with doctors notes to prove I was sick. I am currently waiting for their response. But I am very very worried because A. I have a ccj against my name and I would really be grateful of any advice setting this aside? Can I do it on the basis I never received it because of my illness? B. I am on the understanding I only had 28 days after the ccj was issued to come to an agreement or they could go to court to issue baliffs etc? It is day 25 today! ANY HELP so much appreciated. Very stressed and trying to remain calm so I don't get sick again! Kind Regards x -

Hi everyone, I'm looking for some advice on some fees I was charged in relation to a cosmetic surgery consultation I had back in 2016. At the time I was considering having some cosmetic surgery, so was looking to arrange a few consultations with different surgeons to make sure I was making the correct choices on procedure and when choosing the actual surgeon. I tried to get in touch with one of the practices in question to enquire about a consultation - firstly on the number listed on the surgeons website and then as I couldn't get through on this line, I contacted the private hospital in London where the said surgeon runs his practice - I got through on this number. When speaking to the person at the private hospital I enquired about waiting times and how much this doctor actually charges for a consultation (I had a limited budget for consultations). I was informed of the available dates and I was explicitly told that there would be no charge for the initial consultation - this is nothing out of the ordinary as many cosmetic surgeons offer a free initial consultation. I went ahead and booked a consultation. I then received the booking confirmation through email, again with no mention of any fees. I attended the consultation with the doctor where everything was OK, a very brief consultation compared with some others but I wasn't too concerned as I thought this was a no charge consultation. Again no mention of any cost or taking any payment before, during or immediately after the consultation (the surgeon just said if I was to go with him, we would need to have a second more in depth consultation before surgery) - It's worth noting that I did attend 2 other consultations which we're chargeable, however this was made explicitly clear at the time of booking, and payment was also taken at the point of booking - otherwise the booking would not be made. To my surprise a couple of days later an invoice drops through the post for £215. I contacted the surgeons practice to discuss this and explain the situation, however his practice manager just said I'd been informed wrongly by the private hospital employee, and even though I'd had confirmation and they acknowledged that I was mis-informed, that it wasn't their issue. Which I obviously didn't agree with. I then had a couple of invoice reminders come through the door I got back in touch again to try and resolve the matter. I was then given the contact details of one of the managers of the private hospital and told to try and sort it out with them. Before I'd had chance to resolve this (this was over Christmas so I wasn't able to get hold of said person) I've had a letter through the door from a debt collection services company requesting the money. Now I know these have no legal power as such, but I'd rather nip this in the bud before it goes any further. Am I correct to believe that any charges need to be made clear before a service is provided? Particularly as I explicitly asked before I made the booking if there was any charge (there is also no mention of fees on the surgeons website). If I'd known this consultation was chargeable I wouldn't have gone ahead as the surgeon in question was not my top or second choice. I don't feel like I should have to pay as a result of being provided the wrong information by the hospital. Any thoughts on this? Thanks for the help.

Hi everyone, I'm looking for some advice on some fees I was charged in relation to a cosmetic surgery consultation I had back in 2016. At the time I was considering having some cosmetic surgery, so was looking to arrange a few consultations with different surgeons to make sure I was making the correct choices on procedure and when choosing the actual surgeon. I tried to get in touch with one of the practices in question to enquire about a consultation - firstly on the number listed on the surgeons website and then as I couldn't get through on this line, I contacted the private hospital in London where the said surgeon runs his practice - I got through on this number. When speaking to the person at the private hospital I enquired about waiting times and how much this doctor actually charges for a consultation (I had a limited budget for consultations). I was informed of the available dates and I was explicitly told that there would be no charge for the initial consultation - this is nothing out of the ordinary as many cosmetic surgeons offer a free initial consultation. I went ahead and booked a consultation. I then received the booking confirmation through email, again with no mention of any fees. I attended the consultation with the doctor where everything was OK, a very brief consultation compared with some others but I wasn't too concerned as I thought this was a no charge consultation. Again no mention of any cost or taking any payment before, during or immediately after the consultation (the surgeon just said if I was to go with him, we would need to have a second more in depth consultation before surgery) - It's worth noting that I did attend 2 other consultations which we're chargeable, however this was made explicitly clear at the time of booking, and payment was also taken at the point of booking - otherwise the booking would not be made. To my surprise a couple of days later an invoice drops through the post for £215. I contacted the surgeons practice to discuss this and explain the situation, however his practice manager just said I'd been informed wrongly by the private hospital employee, and even though I'd had confirmation and they acknowledged that I was mis-informed, that it wasn't their issue. Which I obviously didn't agree with. I then had a couple of invoice reminders come through the door I got back in touch again to try and resolve the matter. I was then given the contact details of one of the managers of the private hospital and told to try and sort it out with them. Before I'd had chance to resolve this (this was over Christmas so I wasn't able to get hold of said person) I've had a letter through the door from a debt collection services company requesting the money. Now I know these have no legal power as such, but I'd rather nip this in the bud before it goes any further. Am I correct to believe that any charges need to be made clear before a service is provided? Particularly as I explicitly asked before I made the booking if there was any charge (there is also no mention of fees on the surgeons website). If I'd known this consultation was chargeable I wouldn't have gone ahead as the surgeon in question was not my top or second choice. I don't feel like I should have to pay as a result of being provided the wrong information by the hospital. Any thoughts on this? Thanks for the help. -

Good morning, My 18 yr old daughter took out a policy with 'MyPolicy' car insurance 8 months ago when she passed her test. They seemed the best price at the time but have cost dearly over the 8months, mainly in charges for extra miles. a few weeks ago she was involved in an accident which wasn't her fault, the other driver admitted blame immediately. The claim has been settled and they have sent the cheque. Now, the problem is the charges they want to slap on her. Her car was a write off so she is going to buy her brother's car. They want to charge her £150 for a new black box and £100 to change the details on the policy to the new car. This sounds totally unreasonable to me and is a loss on her part seeing as the accident wasn't her fault. Baring in mind the black box only cost £50 to fit when she first took out the policy. She's young and inexperienced and doesn't know what to say on the phone. Last time I tried, they wouldn't speak to me, but surely if she gives her permission that should be fine? I need to fight her corner for her as I can be stronger on the phone. I need some advice as this charging can't be right. It's a total rip off to me. Any advice would be greatly appreciated.

Good morning, My 18 yr old daughter took out a policy with 'MyPolicy' car insurance 8 months ago when she passed her test. They seemed the best price at the time but have cost dearly over the 8months, mainly in charges for extra miles. a few weeks ago she was involved in an accident which wasn't her fault, the other driver admitted blame immediately. The claim has been settled and they have sent the cheque. Now, the problem is the charges they want to slap on her. Her car was a write off so she is going to buy her brother's car. They want to charge her £150 for a new black box and £100 to change the details on the policy to the new car. This sounds totally unreasonable to me and is a loss on her part seeing as the accident wasn't her fault. Baring in mind the black box only cost £50 to fit when she first took out the policy. She's young and inexperienced and doesn't know what to say on the phone. Last time I tried, they wouldn't speak to me, but surely if she gives her permission that should be fine? I need to fight her corner for her as I can be stronger on the phone. I need some advice as this charging can't be right. It's a total rip off to me. Any advice would be greatly appreciated. -

Millions of people who have basic bank accounts may be paying higher fees than necessary.. Basic bank accounts are designed for people who do not already have a bank account and are ineligible for a standard current account .While eight million people have basic accounts, around half of them are still liable to pay fees for failed payments. Completely fee-free basic accounts have been available since January 2016, following an industry agreement. Vulnerable customers who have such accounts are not charged for failed payments, or for going overdrawn. The Treasury figures show that 3.7 million people have accounts that do not conform to the agreement, struck between the government and the banking industry, in 2014. Of those, 3.6 million bank with Lloyds, the rest being RBS customers All the other seven big High Street banks do not charge fees for basic account customers http://www.bbc.co.uk/news/business-38289654

-

My husband recently engaged The Claims Guys to do a free PPI check for him (much to my horror) and surprise, surprise, they are now demanding payment of over £2000 for the first compensation pay-out (30% plus VAT). I object strongly to paying these jokers anything at all, but despite interrogating my husband, I can't seem to work out how they got from free check to binding contract. I believe he only signed letters of authority for 2 companies (he can't remember which ones) but we have already been contacted by 3 companies so I really don't know what is going on. Is there any way we can get the contract cancelled? Is it worth me trying to fight it? (On the grounds that they did not make it clear to my husband that he could do it himself or that he signed it under duress) Is there anything at all I can do, or do we just have to pay up and find some way of keeping my husband away from all paperwork in future? (For what it's worth, my husband is quite a successful professional - he is just hopeless at admin and anything financial...)

My husband recently engaged The Claims Guys to do a free PPI check for him (much to my horror) and surprise, surprise, they are now demanding payment of over £2000 for the first compensation pay-out (30% plus VAT). I object strongly to paying these jokers anything at all, but despite interrogating my husband, I can't seem to work out how they got from free check to binding contract. I believe he only signed letters of authority for 2 companies (he can't remember which ones) but we have already been contacted by 3 companies so I really don't know what is going on. Is there any way we can get the contract cancelled? Is it worth me trying to fight it? (On the grounds that they did not make it clear to my husband that he could do it himself or that he signed it under duress) Is there anything at all I can do, or do we just have to pay up and find some way of keeping my husband away from all paperwork in future? (For what it's worth, my husband is quite a successful professional - he is just hopeless at admin and anything financial...) -

Hi guys. Simply put. Parking fine - £82 Forgot to pay it. Went to a Debt Collector, who added their £75 on top. As soon as I got the letter and remembered the debt, I paid Stockport Council via their website The £82. I have an email proving so. This was October 3rd Just had a letter placed through the door tonight for.... The original debt £82 Compliance fee £75 1st visit £235 Total: £392. Am I missing something here? Clearly a lack of comms between the council and the bailiff. According to the law, do I have to pay the bailiffs' fees for a debt I paid 2 months ago? Thank you so much in advance

Hi guys. Simply put. Parking fine - £82 Forgot to pay it. Went to a Debt Collector, who added their £75 on top. As soon as I got the letter and remembered the debt, I paid Stockport Council via their website The £82. I have an email proving so. This was October 3rd Just had a letter placed through the door tonight for.... The original debt £82 Compliance fee £75 1st visit £235 Total: £392. Am I missing something here? Clearly a lack of comms between the council and the bailiff. According to the law, do I have to pay the bailiffs' fees for a debt I paid 2 months ago? Thank you so much in advance -

Lettings agents in England will be banned from charging fees to tenants "as soon as possible" under plans announced in the Autumn Statement. Tenants can be charged fees for a range of administration, including reference, credit and immigration checks. Chancellor Philip Hammond said shifting the cost to landlords will save 4.3 million households hundreds of pounds. The move could spur competition as landlords, unlike tenants, can shop around for the cheapest agent. In Scotland, lettings agency fees to tenants have already been banned. In England and Wales since last year, lettings and managing agents have been legally obliged to clearly publicise their fees. Fees vary widely, with costs in some big cities much higher than elsewhere. Tenants face charges when agents draw up tenancy agreements along with the possibility of a non-refundable holding deposit paid before signing up to the deal. http://www.bbc.co.uk/news/business-38065249

Lettings agents in England will be banned from charging fees to tenants "as soon as possible" under plans announced in the Autumn Statement. Tenants can be charged fees for a range of administration, including reference, credit and immigration checks. Chancellor Philip Hammond said shifting the cost to landlords will save 4.3 million households hundreds of pounds. The move could spur competition as landlords, unlike tenants, can shop around for the cheapest agent. In Scotland, lettings agency fees to tenants have already been banned. In England and Wales since last year, lettings and managing agents have been legally obliged to clearly publicise their fees. Fees vary widely, with costs in some big cities much higher than elsewhere. Tenants face charges when agents draw up tenancy agreements along with the possibility of a non-refundable holding deposit paid before signing up to the deal. http://www.bbc.co.uk/news/business-38065249 -

Hi being threatened with court action from holiday company, the holiday was booked with a deposit and then 2 payments were due to be taken from card, The 1st payment that was due I asked for a extension of 10 days as my mother was ill in hospital, ( I am a self employed taxi driver) they agreed so all was fine, then sadly my mother passed away and the holiday was just forgotten about. Started getting emails saying payment had failed and they would have to cancel the holiday, I really did not care at that time, received an email saying Cancellation charges, and they were the same as the holiday, Now I expected easy jets flight costs were probably due but they have asked for payment for the hotel and transfers etc ATOL protection and transaction fees. I returned the email and asked them to provide receipts for the so called payments for the transfers, hotel etc and they just ignored me, today I have received a letter threatening court action and I dont really know where I stand and what to do Any help would be gratefully appreciated

-

hi all, i need some help with solicitors fees. i took my civil claim for a used car i purchased to a solicitor as i was not getting anywhere with the car dealer i purchased from. long story short, the solicitor had my file for 3 years, ran the case into the ground, i paid £17k in costs, the solicitor then came off file when i refused to pay any further money. now the solicitors firm want another £8000. in the end the solicitor did absolutely nothing for me, i didn't win the case nor did i lose it. the dealer in the end repaired the car and gave it back to me, for the privilege i paid a solicitor £17k. what i don't understand is, if my case had no prospect of winning why did they pursue it down the fast track route, instead of offering me legal advice, i was always asked, what i want to do, it was extremely reactive in nature. there would have been a better chance to pursue the defendant for costs in relation to make the car road worthy, the repair would have cost between £2000-£3000 maximum and we could have pursued it smalls claims. they are threatening court action if i don't pay and i really need to know what i can do?? i have been bled dry and dont have any more money to pay another solicitor. really hope someone can help me

-

Hi, I was hoping to possibly get some advice. My kids where at a private school (fees paid till the end of the school year). Then this happens.. . http://www.shernoldschool.co.uk/118972__1.pdf and http://www.kentonline.co.uk/maidstone/news/shernold-school-inadequate-staff-checks-97172/ at which point we withdrew the kids from the school and moved them elsewhere. We have told the school that we where not happy (so have others) and we would not be paying the notice period (although the bill they have sent us appears to only be for half of the term Fast forward a few months of email exchanges to yesterday, we receive a letter from Redwood Collections looking to collect the outstanding amount. Its there typical "We are instructed to take all necessary steps to recover the sum shown, including legal action if required". Some (hopefully) useful points: 1. The school fees where paid in full till the end of the school year 2. My eldest son has moderate aspergers syndrome and ADHD (we have letters proving it and the school where aware of this) he also had major heart surgery in March of this year 3. My sons care team had tried to work with the school with regards to what is the best outcome for my eldest sons education. They weren't interested (can prove this as well). 4. All things said done we where going to move them regardless due to having (documented) concerns for a while. Whats the best way forward with this? Thanks in advance! P.S. Sorry to work around the "To be able to post links or images your post count must be 10 or greater. You currently have 0 posts." message, but I think the links are important to what is going on here.

Hi, I was hoping to possibly get some advice. My kids where at a private school (fees paid till the end of the school year). Then this happens.. . http://www.shernoldschool.co.uk/118972__1.pdf and http://www.kentonline.co.uk/maidstone/news/shernold-school-inadequate-staff-checks-97172/ at which point we withdrew the kids from the school and moved them elsewhere. We have told the school that we where not happy (so have others) and we would not be paying the notice period (although the bill they have sent us appears to only be for half of the term Fast forward a few months of email exchanges to yesterday, we receive a letter from Redwood Collections looking to collect the outstanding amount. Its there typical "We are instructed to take all necessary steps to recover the sum shown, including legal action if required". Some (hopefully) useful points: 1. The school fees where paid in full till the end of the school year 2. My eldest son has moderate aspergers syndrome and ADHD (we have letters proving it and the school where aware of this) he also had major heart surgery in March of this year 3. My sons care team had tried to work with the school with regards to what is the best outcome for my eldest sons education. They weren't interested (can prove this as well). 4. All things said done we where going to move them regardless due to having (documented) concerns for a while. Whats the best way forward with this? Thanks in advance! P.S. Sorry to work around the "To be able to post links or images your post count must be 10 or greater. You currently have 0 posts." message, but I think the links are important to what is going on here. -

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance -

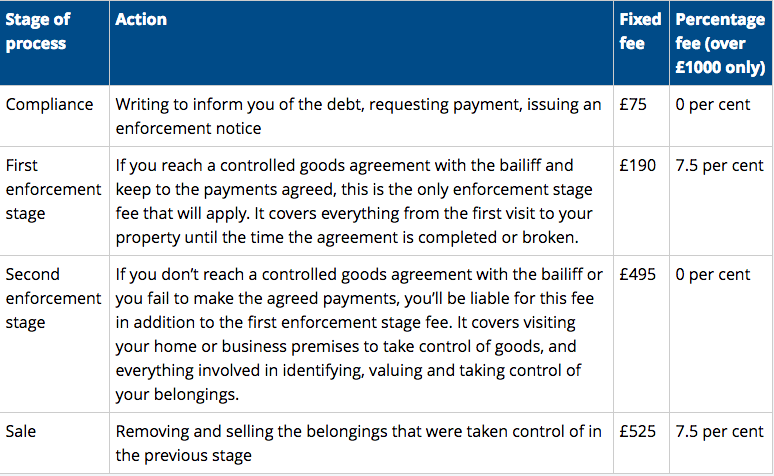

Hi all, I would really appreciate some advice. My business partner and I run a small business, and cashflow is very delicate. Some time ago we got in some money trouble and an invoice was sold to a debt recovery company. We managed to pay it off (or so we thought), but unfortunately my business partner is a bit scatternbrained with numbers, and paid the incorrect amount. The total outstanding debt was £5,723.96. My business partner sent them a transfer of £5,700, accidentally leaving off the £23.96. My business partner had some fees he wanted to dispute - The debt recovery company then sent a follow up email saying all prior fees are legitimate, and that "I have checked your account and can see we are still awaiting a payment of £23.96. I am assured this will be paid in due course, and this case can then be closed.". My business partner forgot to respond to the email (stupid, I know), and three weeks later (yesterday) they send a hired thug to our place of business, while customers were there, demanding the £23.96 plus a £1111.87 enforcement charge. He said that unless we paid that to him on the spot, he would confiscate goods that he valued to the sum of £8000. The £5,723.96 sum had a high court writ, which comes with a cap on fees of this nature that can be charged, as illustrated by the table below: The bailiff claimed to be able to charge for both stage two and three whether or not he actually had to carry out stage three. I pointed out that I was perfectly willing to pay the debt and the enforcement fee on the spot, which meant that he did not have the right to charge a "sale" enforcement fee, but he refused to drop it, saying I either pay exactly what he is demanding, or he starts ripping equipment out of the walls there and then. I had no choice but to pay the entire sum, and did so. There is no doubt in my mind that this is illegal and extortion, and in fact the bailiff himself used the very word "extortionate" when explaining the situation he was putting us in. My question to you is which regulatory body can I bring this to the attention of, are there any court cases setting a precedent in these situations, and are there guidelines that prevent bailiffs from charging huge bills for debts as low as £23? Even the £495 bill is entirely unfair, and clearly taking advantage of an admin error made by a small business. The law was not written to allow them to do this, and it puts our business at risk. Any advice on putting this right would be massively appreciated. Thanks a lot.

Hi all, I would really appreciate some advice. My business partner and I run a small business, and cashflow is very delicate. Some time ago we got in some money trouble and an invoice was sold to a debt recovery company. We managed to pay it off (or so we thought), but unfortunately my business partner is a bit scatternbrained with numbers, and paid the incorrect amount. The total outstanding debt was £5,723.96. My business partner sent them a transfer of £5,700, accidentally leaving off the £23.96. My business partner had some fees he wanted to dispute - The debt recovery company then sent a follow up email saying all prior fees are legitimate, and that "I have checked your account and can see we are still awaiting a payment of £23.96. I am assured this will be paid in due course, and this case can then be closed.". My business partner forgot to respond to the email (stupid, I know), and three weeks later (yesterday) they send a hired thug to our place of business, while customers were there, demanding the £23.96 plus a £1111.87 enforcement charge. He said that unless we paid that to him on the spot, he would confiscate goods that he valued to the sum of £8000. The £5,723.96 sum had a high court writ, which comes with a cap on fees of this nature that can be charged, as illustrated by the table below: The bailiff claimed to be able to charge for both stage two and three whether or not he actually had to carry out stage three. I pointed out that I was perfectly willing to pay the debt and the enforcement fee on the spot, which meant that he did not have the right to charge a "sale" enforcement fee, but he refused to drop it, saying I either pay exactly what he is demanding, or he starts ripping equipment out of the walls there and then. I had no choice but to pay the entire sum, and did so. There is no doubt in my mind that this is illegal and extortion, and in fact the bailiff himself used the very word "extortionate" when explaining the situation he was putting us in. My question to you is which regulatory body can I bring this to the attention of, are there any court cases setting a precedent in these situations, and are there guidelines that prevent bailiffs from charging huge bills for debts as low as £23? Even the £495 bill is entirely unfair, and clearly taking advantage of an admin error made by a small business. The law was not written to allow them to do this, and it puts our business at risk. Any advice on putting this right would be massively appreciated. Thanks a lot.

-

I normally manage to avoid the store exit reps, those who are selling double glazing, conservatories etc, However, yesterday whilst I was at the Range, I got caught by a lady working for a law firm offering an hour's free advice on how to avoid assets being gobbled up by Care Home Fees and Inheritance Tax. I have already written a will, as has hubby, with the help of our own solicitor - we are tenants in common on a mortgage free property and have both nominated our son to inherit our share of the property and assets in the event one of us dies before the other. The chances of our having property value and assets that would create a need to pay inheritance tax is in the realms of fantasy (unless we come up on the premium bonds or win the lottery). The lady who was making appointments for her firm seemed to bat back my responses to her questions making like despite the plans already in place, that the authorities would still be able to place a charge on the home in the event one of us requires admission to a care home - despite the other still living in the home ? I have had a read of the following article in the Guardian and used their calculator using a hypothetical situation. According to the result of the Q/A - then if only one of us required admission to a care home and the other left still living in the property then the person who was admitted would not have their share of the property included in any calculation for fees.. this was not what we were told at the Range ? https://www.theguardian.com/money/2014/aug/28/tenancy-common-care-home-fee-solution I have also looked at Age UK's website http://www.ageuk.org.uk/ I believe that I might have been misled by the above person in order to secure an appointment. The flyer I have been given indicates that there will one hour's free legal advice worth £200.00 VAT. I am assuming that if we were to go ahead with the appointment then any time outside of that hour will be charged at that rate. I will not be taking the Firm up on their offer, instead, I will contact my own solicitor on Monday to ensure that we have covered all bases, but would still be interested in hearing if anyone else has been caught out like this ?

I normally manage to avoid the store exit reps, those who are selling double glazing, conservatories etc, However, yesterday whilst I was at the Range, I got caught by a lady working for a law firm offering an hour's free advice on how to avoid assets being gobbled up by Care Home Fees and Inheritance Tax. I have already written a will, as has hubby, with the help of our own solicitor - we are tenants in common on a mortgage free property and have both nominated our son to inherit our share of the property and assets in the event one of us dies before the other. The chances of our having property value and assets that would create a need to pay inheritance tax is in the realms of fantasy (unless we come up on the premium bonds or win the lottery). The lady who was making appointments for her firm seemed to bat back my responses to her questions making like despite the plans already in place, that the authorities would still be able to place a charge on the home in the event one of us requires admission to a care home - despite the other still living in the home ? I have had a read of the following article in the Guardian and used their calculator using a hypothetical situation. According to the result of the Q/A - then if only one of us required admission to a care home and the other left still living in the property then the person who was admitted would not have their share of the property included in any calculation for fees.. this was not what we were told at the Range ? https://www.theguardian.com/money/2014/aug/28/tenancy-common-care-home-fee-solution I have also looked at Age UK's website http://www.ageuk.org.uk/ I believe that I might have been misled by the above person in order to secure an appointment. The flyer I have been given indicates that there will one hour's free legal advice worth £200.00 VAT. I am assuming that if we were to go ahead with the appointment then any time outside of that hour will be charged at that rate. I will not be taking the Firm up on their offer, instead, I will contact my own solicitor on Monday to ensure that we have covered all bases, but would still be interested in hearing if anyone else has been caught out like this ? -

The Taking Control of Goods Regulations 2013 came into effect in April 2014. A significant change to the regulations was how bailiff fees are to be deducted from any payment made. This is explained in detail on the following STICKY: http://www.consumeractiongroup.co.uk/forum/showthread.php?453047-Bailiff-enforcement-Setting-up-a-payment-arrangement-and-whether-you-can-pay-the-court-or-the-council-direct Almost as soon as the regulations were introduced, local authorities around the country were inundated with Freedom of Information requests to ascertain whether or not the council would properly deduct the bailiffs fees in accordance with legislation in cases where the debtor defied the instruction on the Notice of Enforcement, and instead, paid the council the amount of the liability order only (minus bailiff fees). If nothing else, these FOI requests have highlighted to the councils the way in which the regulations had changed. With the regulations having now been in place for 20 months it is now the case that paying the council direct (minus bailiff fees) rarely ever succeeds and instead, is leading to debtors being in a much worse financial position than ever before given that by the time the payment has been processed by the local authority, the 'compliance stage' outlined in the Notice of Enforcement would have ended and with it, the opportunity to enter into a payment arrangement without the need for a personal visit from the enforcement agent and a charge of £235 being applied. Given that this is a discussion thread, it may be useful to debate this subject but please.....no arguments or squabbles.

-

Consumers who are forced to have prepayment energy meters put in should face a maximum installation fee of £150, the regulator has proposed. Currently such energy users - already the most vulnerable to debt - face a charge of up to £900, said Ofgem. As many as 4.5 million people use prepayment meters for electricity, while 3.5 million use them for gas. Ofgem is suggesting that the maximum fee should be between £100 and £150. For particularly vulnerable consumers, such as those in financial hardship or those with health issues, it says there should be no charge at all. http://www.bbc.co.uk/news/business-37349013 Ofgem is now inviting comments and responses to its plans before it finalises them in Novembe and. has published a series of proposals

-

Hi everyone, I live in a flat which i have to pay ground rent every 6 months. I've always paid on time over the space of 6 years. The account was setup to have payment requests sent via email, a work email. Since October last year that email address no longer existed, better put i had no access to it anymore. I then received a Payment request through the post demanding what is rightfully owed to them but they have added "Ground Rent Arrears Fee" x4 of them totaling to: £330.00, i disputed this amount and sent a cheque of the original amount due of £200.00 saying there was no access to emails since this had become due. They sent the cheque back and demanded the full payment and still are with arrears fees still being added. In answer to my first letter to them explaining about the email, they said i was bound to the terms when registering for an online billing account that all bills would be sent to that email address only. Do i have any space for argue here? Seeing as the fees are so high every time, i have no means to pay it at the moment due to my working hours have been heavily decreased. Can i argue to the fact of the email account or the extremely high charges? Your help would be appreciated. Thank you.

Hi everyone, I live in a flat which i have to pay ground rent every 6 months. I've always paid on time over the space of 6 years. The account was setup to have payment requests sent via email, a work email. Since October last year that email address no longer existed, better put i had no access to it anymore. I then received a Payment request through the post demanding what is rightfully owed to them but they have added "Ground Rent Arrears Fee" x4 of them totaling to: £330.00, i disputed this amount and sent a cheque of the original amount due of £200.00 saying there was no access to emails since this had become due. They sent the cheque back and demanded the full payment and still are with arrears fees still being added. In answer to my first letter to them explaining about the email, they said i was bound to the terms when registering for an online billing account that all bills would be sent to that email address only. Do i have any space for argue here? Seeing as the fees are so high every time, i have no means to pay it at the moment due to my working hours have been heavily decreased. Can i argue to the fact of the email account or the extremely high charges? Your help would be appreciated. Thank you. -

Hi all. Is there a time limit on attempting to reclaim packaged account fees? I was charged for a packaged account with HSBC between November 2008 and December 2010. They continued to charge the fee even when the account went into an unauthorised overdraft and closed due to default in December 2010. I believe I took the account having been told it would mean I could have an overdraft - which I never actually got. It also provided breakdown cover but I do not drive. I do not know what the other benefits were - I was suffering from mental illness at the time. The delay on me looking into this is due to my illness - I only obtained statements at the end of April this year. Over £350 of packaged fees, but most of them are over 6 years old. Does a time bar apply?

-

Hi, Before I start, a big thanks to CAG for past help with different matters. If you read any of my other posts you will see I had debt problems in 2007, with a failed company and business / personal debts to near £150k, its taken 9 years to clear everything, finally debt free I'm looking back over accounts to see where I can claim back some of the huge interest amounts and fees whilst paying off credit cards overdrafts etc.. my wife has a Barclays account, it's still her current account and its been active for over 30 years, due to our extreme financial hardship in 2007, we had big monthly charges, as I mentioned we had cci's and £150k of debt to repay, we had to sell the house, remortgaging with a sub prime lender, DB, Yep DB! it was a real nightmare, looking at her account you can see our mortgage, gas, electric and all necessity bills bouncing every month for years, I have statements, letters etc to prove hardship... To be honest we are not in financial trouble anymore, after 8 years working 24 hours a day, we have cleared every debt, and have brought a house and live mortgage free, I know its been said in a few posts that you have to still be in hardship and that its maybe to late to claim now. I had a thought about this though today, the figures are: Barclays current account, charges including reserve charges up to £200 a month max, we had charges every month from April 2008 to September 2015 total charges nearly £5,000 If hardship and the 2009 time scale is out of the question how about the fact we have just had three PPI claims upheld against Barclays one on this account dating back nearly 25 years, we had a payout of just over £9,000 (which is great) could I not use this as a argument that if she had not been paying these monthly amount (which they agree was mis sold and have paid) she would not been overdrawn and therefore would not have received these charges. Thinking about it there is a note on the PPI payout letter which asks if you incurred any other financial costs... Should she be going down that route or treating it separately this way? I have gone through every statement and noted the date and cost for each charge, put them on an excel sheet and used the template for hardship, I wanted to get feedback first before sending, and only thought of the note on the PPI payout letter whilst typing As always thanks for your comments in advance! Dave

-

Hope this is the right place, my issue is in relation to Scottish Law. In March 2016 I signed up for a home study course, I had two options. Either sign up for each module individually or 4 of them which gave a greater discount. I signed for all 4 and paid about £1k on my personal credit card. It was suggested a higher discount was available and that seemed appropriate. The plan was to recover the cost from my employer now that did not work out as I planned and ultimately they paid nothing. Although some months have passed since my initial sign up I asked for a refund of the fee’s for the modules not started so that I could pay that back to my card, from there I could then pay for each module as I pass the previous. They have refused to do this stating that I agreed to terms that refunds were only due within 14 days. I did not understand that I had agreed to such terms. Each module is available from the provider as a standalone course, although I have paid for them all I have only received material for the first module. They will not issue any material for the subsequent modules until I complete the previous one. they are in no way out of pocket for anything but the first module. Part of the fees paid are for exams for those modules which would only be payable to the exam provider in the future. At first they said they would consider a refund, then they accused me of dishonesty suggesting my employer had paid the fees and I was trying to get them back from them. I offered to get a letter from my employer confirming they have not paid fees however they then ignored that and have insisted they can speak to my employer and explain the value in the course which is none of their concern quite frankly. As far as I am aware the contract is ultimately between them and myself, nothing to do with my employer as they had not agreed to pay them anyway. At this point the relationship has broken down completely, especially after their suggestion that I was being dishonest in requesting a refund. I have no desire to continue studying with them and want to move to another provider. My question therefore is whether I have a case to raise a small claims summons to recover the remaining fees or even a charge back on my credit card? T hey are just stalling now. I have even offered a compromise in that I will accept £100 less to cover their administration for processing the refund. I have not had to sign anything throughout the process. This is what they say covers their position; Fees are not refundable after two weeks have elapsed, but a transfer to another course of comparable value may be considered. Such a transfer may be subject to an administration fee,depending on how far you have progressed on the first course. (Where software has been supplied as part of the course, and the seal on this has been broken, no refunds will be considered for this particular item.) Would welcome some thoughts on the best way to approach this in order to get a refund if you are of the opinion I am entitled to one.

Hope this is the right place, my issue is in relation to Scottish Law. In March 2016 I signed up for a home study course, I had two options. Either sign up for each module individually or 4 of them which gave a greater discount. I signed for all 4 and paid about £1k on my personal credit card. It was suggested a higher discount was available and that seemed appropriate. The plan was to recover the cost from my employer now that did not work out as I planned and ultimately they paid nothing. Although some months have passed since my initial sign up I asked for a refund of the fee’s for the modules not started so that I could pay that back to my card, from there I could then pay for each module as I pass the previous. They have refused to do this stating that I agreed to terms that refunds were only due within 14 days. I did not understand that I had agreed to such terms. Each module is available from the provider as a standalone course, although I have paid for them all I have only received material for the first module. They will not issue any material for the subsequent modules until I complete the previous one. they are in no way out of pocket for anything but the first module. Part of the fees paid are for exams for those modules which would only be payable to the exam provider in the future. At first they said they would consider a refund, then they accused me of dishonesty suggesting my employer had paid the fees and I was trying to get them back from them. I offered to get a letter from my employer confirming they have not paid fees however they then ignored that and have insisted they can speak to my employer and explain the value in the course which is none of their concern quite frankly. As far as I am aware the contract is ultimately between them and myself, nothing to do with my employer as they had not agreed to pay them anyway. At this point the relationship has broken down completely, especially after their suggestion that I was being dishonest in requesting a refund. I have no desire to continue studying with them and want to move to another provider. My question therefore is whether I have a case to raise a small claims summons to recover the remaining fees or even a charge back on my credit card? T hey are just stalling now. I have even offered a compromise in that I will accept £100 less to cover their administration for processing the refund. I have not had to sign anything throughout the process. This is what they say covers their position; Fees are not refundable after two weeks have elapsed, but a transfer to another course of comparable value may be considered. Such a transfer may be subject to an administration fee,depending on how far you have progressed on the first course. (Where software has been supplied as part of the course, and the seal on this has been broken, no refunds will be considered for this particular item.) Would welcome some thoughts on the best way to approach this in order to get a refund if you are of the opinion I am entitled to one. -

I recently ordered an unvented water cylinder in error from an internet company. Their T&C clearly stated that they charged a 25% of the item's price for returns. They did not say whether this was on the vat as well, but I believe that it should not be. However, it appears to me that this fee could well be an unlawful penalty, (Dunlop v New Garage 1915) . . Surely it must cost very little more to restock a £1,000 thermal store than it does a £150 immersion heater of the same size I realise that this is to deter time wasters, but it my case I am returning a £350 unvented cylinder, and buying a £1,000 thermal store from them in its place. Does anyone have any thoughts on this?

-

Hi, the OH has a new look account and has been "late" a few times and has had £12 fees added to her account, this totals £72, at first her payment schedule was for the 1st of the month but this was changed to the 5th, she can't remember if she was notified of this. If she missed a payment by a day they would ring up multiple times each day until the payment was made. First question, are these able to be returned. Second, where do we start with? SAR? Regards, DreamEater.

-

Hi there, Thanks for reading. I'm new to the forum, and hoping I may be able to find a little help with my current situation. I'm in a bit of a tangle!. Essentially I received an N1SDT CCJ claim form in the mail, too late to reply, and subsequently received a CCJ. I believe the debt to be statute barred, and intent to have it set aside if possible. I'm currently trying to claw my way out of long term unemployment by starting a small business (via the JSA/NEA scheme. I'm in the very early stages), so this is pretty awful timing. On the 18th of August I received a claim form dated 25th July. Obviously at that point it was too late to submit a seemingly simple defense, and the court ruled in favour of the claimant. I have received a 'Judgment for Claimant' notification, and correspondence from the claimant. The debt is from a capital one credit card dating back to August 2007, and was apparently 'assigned to the claimant' in Oct 2009 (this information is taken from the 'particulars of claim' section of the claim form that I received). I have no records of the debt, but have had no contact with anyone regarding the debt/account since the point were I stopped making payments (which I assume is 2007). I'm hoping that I can have this CCJ set aside, owing to the debt being statute barred. I'm currently claiming JSA, have no savings/additional income, live in my father's home, and I believe that I meet the requirements for a full remission of court fees, should I be able to go down that route. Though I'm not really sure how I go about doing that. Also I'm not entirely sure what kind of evidence I would have to supply. I have no records from the time, and assume I'll be needing them. Any advice with regards to my options at this point would be greatly appreciate. My understanding's pretty limited, and time is of the essence it seems. Thanks for any help.

Hi there, Thanks for reading. I'm new to the forum, and hoping I may be able to find a little help with my current situation. I'm in a bit of a tangle!. Essentially I received an N1SDT CCJ claim form in the mail, too late to reply, and subsequently received a CCJ. I believe the debt to be statute barred, and intent to have it set aside if possible. I'm currently trying to claw my way out of long term unemployment by starting a small business (via the JSA/NEA scheme. I'm in the very early stages), so this is pretty awful timing. On the 18th of August I received a claim form dated 25th July. Obviously at that point it was too late to submit a seemingly simple defense, and the court ruled in favour of the claimant. I have received a 'Judgment for Claimant' notification, and correspondence from the claimant. The debt is from a capital one credit card dating back to August 2007, and was apparently 'assigned to the claimant' in Oct 2009 (this information is taken from the 'particulars of claim' section of the claim form that I received). I have no records of the debt, but have had no contact with anyone regarding the debt/account since the point were I stopped making payments (which I assume is 2007). I'm hoping that I can have this CCJ set aside, owing to the debt being statute barred. I'm currently claiming JSA, have no savings/additional income, live in my father's home, and I believe that I meet the requirements for a full remission of court fees, should I be able to go down that route. Though I'm not really sure how I go about doing that. Also I'm not entirely sure what kind of evidence I would have to supply. I have no records from the time, and assume I'll be needing them. Any advice with regards to my options at this point would be greatly appreciate. My understanding's pretty limited, and time is of the essence it seems. Thanks for any help.