Search the Community

Showing results for tags 'cca'.

-

Hi, after CCA'ing my creditors as per advice here in an earlier thread back in October one of my main DCA's (Wescot has responded - took them a while!) They are saying they have sent me my original agreement as requested and have now passed the debt back to Lowell who they were collecting on behalf of? is the CCA a valid copy? The original creditor was HSPF (home shopping personal finance) Not sure if i should get back in touch with Lowell and start arranging payments again or not Any help appreciated as always, i have uploaded copy of what Wescot have sent me.. next steps for me? file_1_pdf.pdf

Hi, after CCA'ing my creditors as per advice here in an earlier thread back in October one of my main DCA's (Wescot has responded - took them a while!) They are saying they have sent me my original agreement as requested and have now passed the debt back to Lowell who they were collecting on behalf of? is the CCA a valid copy? The original creditor was HSPF (home shopping personal finance) Not sure if i should get back in touch with Lowell and start arranging payments again or not Any help appreciated as always, i have uploaded copy of what Wescot have sent me.. next steps for me? file_1_pdf.pdf -

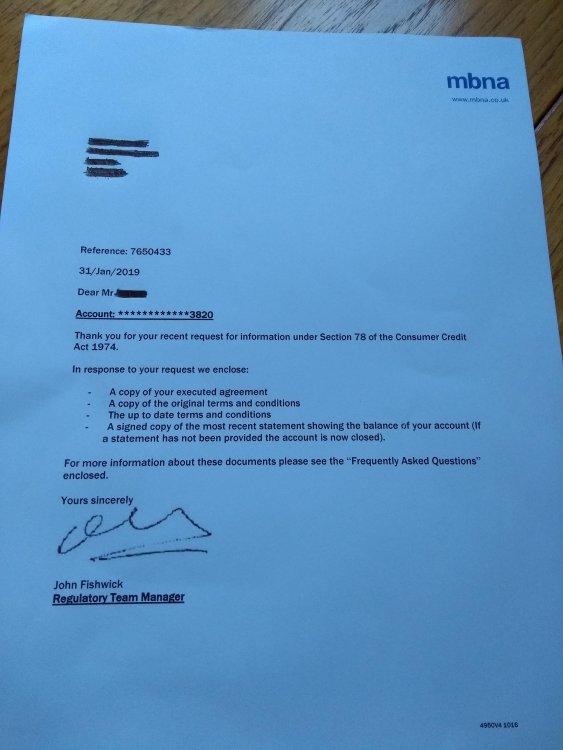

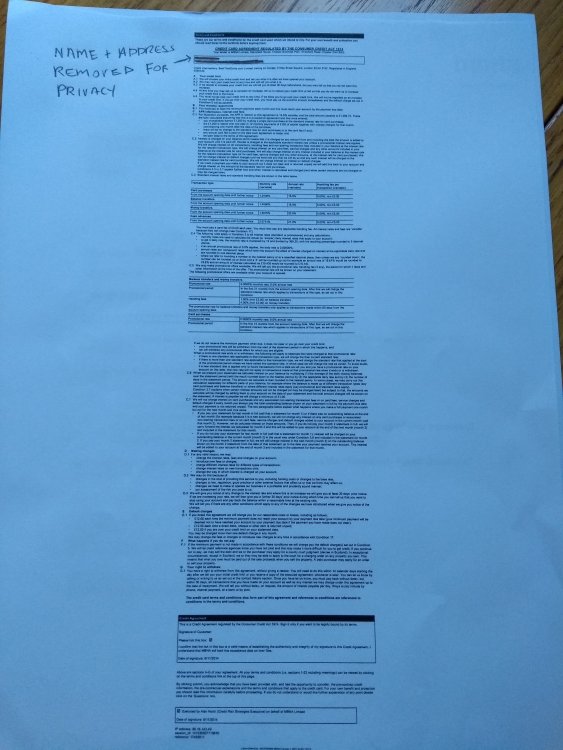

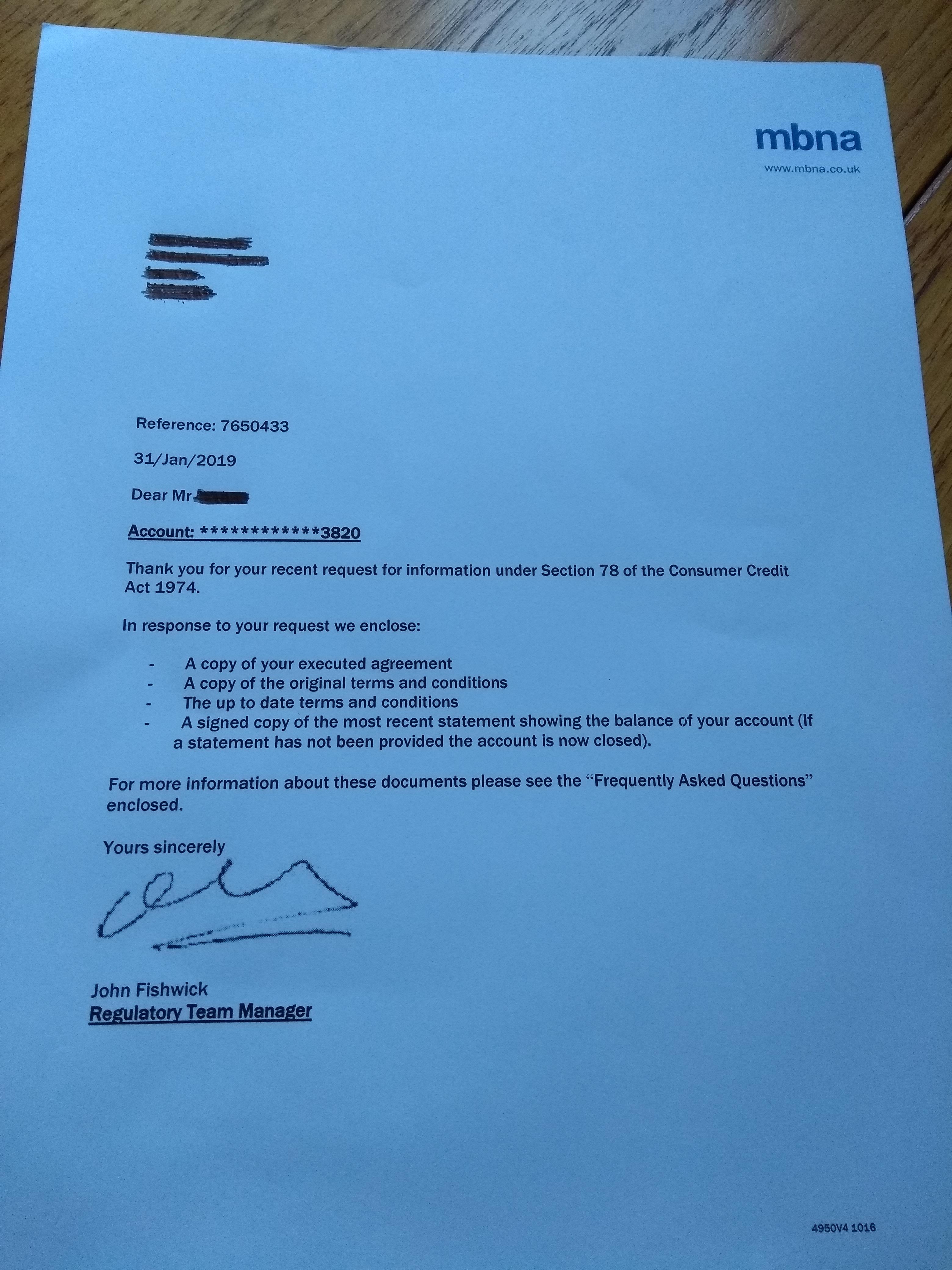

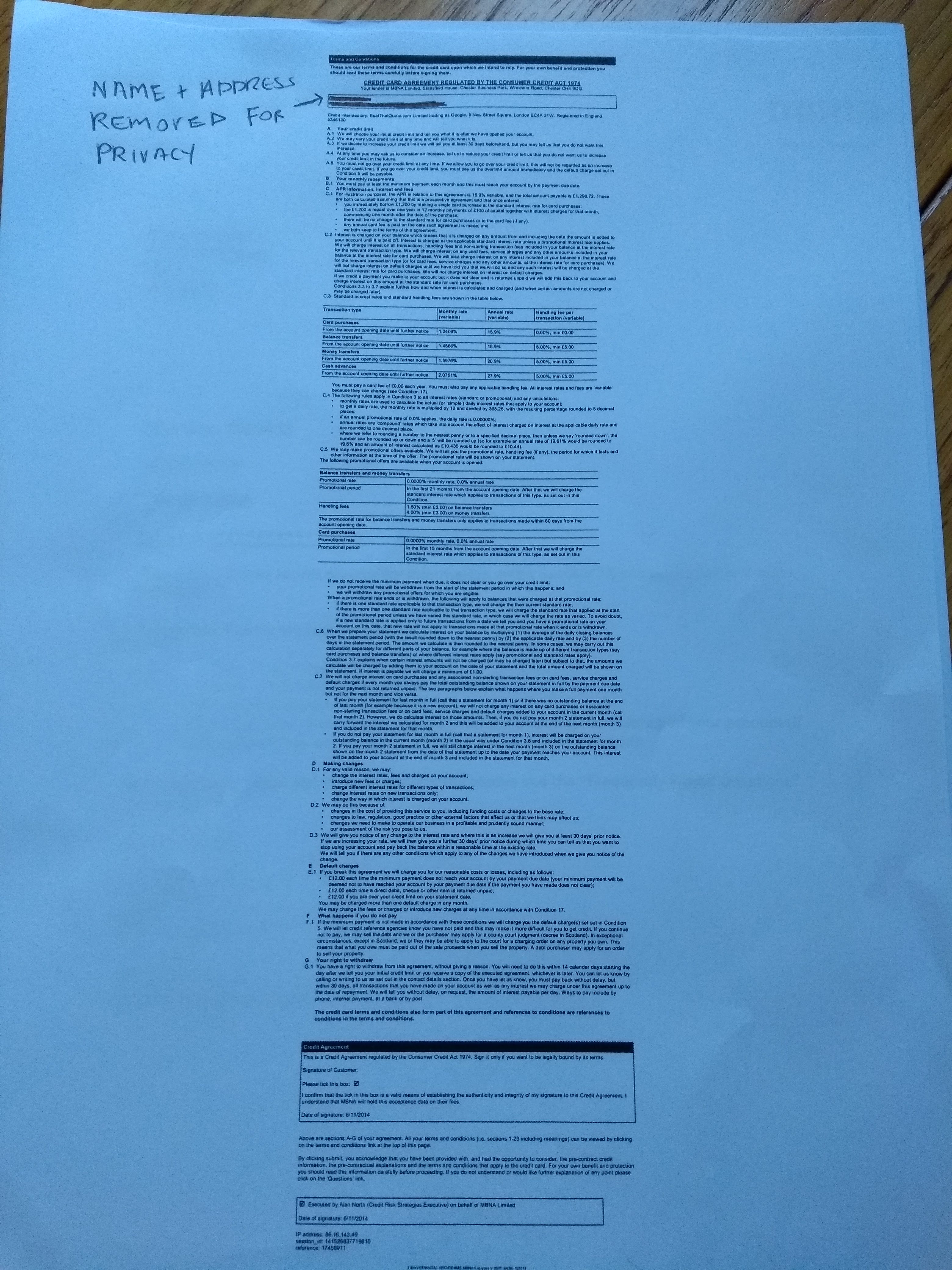

Had the following back from MBNA in response to a CCA request. 2 sets of T&C's, one current, and one supposedly from the time they card was taken out (not sure how I'd actually verify that) A summary statement showing current balance And a "copy executed agreement" Have uploaded the covering letter and the redacted "copy executed agreement". Basically, is this valid? This card was taken out in late 2014, and from what I've read it seems like it probably is a valid an enforceable response to my request, but would like to be sure before taking next step (MBNA bluntly rejected a recent full and final offer of around 60% of balance, claiming they never accept such offers. I should also mention that the debt is still with MBNA and no payments have been made for 3 months now. Current balance is a around £10.5k. Borrowing from family and selling a few things I reckon I could raise £8k tops. It doesn't seem like MBNA would accept this as a full and final, and all the while the interest mounts up.

-

CCA Enforceability Thread I'm sure I've seen it stickied somewhere and cant find it for the life of me.

-

Good morning all Have been an avid reader of CAG for some time. I currently have an alleged debt with shop direct which is being dealt with by Lowells. The debt is for £2k+ I have read the guides and templates available and sent a CCA request to Lowell's in November. I finally received 2 signed documents. You can see on one document the key financial info is set at £36. The other document Is signed and the account number is the same as the first document. Note that the dates are different so the documents were not signed together. Any help or pointers would be greatly appreciated. Many Thanks

.thumb.jpg.157c55a57c1d03e42624bbf0c552576e.jpg)

.thumb.jpg.0a920372943b1ddd34b7a9e31a174b4f.jpg)

-

Hi, I am wondering if anyone can confirm whether the attached CCA request from Barclays is enforceable. I took the card out in 2011 and along with an MBNA card i stopped payments in Feb 2018 with a balance of £9104 on the BC. I contacted Step change and entered into a DMP paying £344pm to cover both cards. In Aug i sent the CCA request to Barclays and they returned the document, i thought it was legit because it had my name and address on so filed it away and did not send one to MBNA. A month after the CCA request i was informed that my debt had been sold on to PRA which i thought odd because i was almost paying the minimum amount. I have been reducing the amount i pay through budget reviews and am down to £170pm between both cards. new year and decided to get a grip, i have requested a CCA from PRA and MBNA, PRA have replied saying that they are trying to retrieve the documents, i am presuming that they will be the same as the ones that BC sent me and have put my account on hold. So, if they supply the same docs is it enforceable and what info is missing from the document. I have searched for what info should be provided but have drawn a blank. Apologies for the first couple of pages not being in order. Any help greatly appreciated. S25C-919012107300.pdf

-

Hi I am new to the site and just learning how to navigate the forums. Hoping I am now in the correct place to get some helpful advice. I have 4 very historic debts being managed for the past 6-7 years by CABOT and 1 with PRA. In the past few weeks, I requested a CAA and SARs from both which was a very revealing exercise. Low and behold:!: CABOT replied saying they could not find CAA for 3 historic debts so these are unenforceable but that I should continue with my monthly payments to my DMC. PRA replied very differently saying "current accounts do not require credit agreements and therefore no credit agreements have been set up when opening the account". How can these 2 Debt Companies behave and respond differently:?: I now plan to stop monthly payments to CABOT and would like your advice if there will be consequences! I am currently 70+ in poor health and want to be debt free in 2019:!: I have also sent GP medical and Cardio reports to both companies but did not receive any compassionate response:sad: Many Thanks for any advice and direction given. nacro:help:

Hi I am new to the site and just learning how to navigate the forums. Hoping I am now in the correct place to get some helpful advice. I have 4 very historic debts being managed for the past 6-7 years by CABOT and 1 with PRA. In the past few weeks, I requested a CAA and SARs from both which was a very revealing exercise. Low and behold:!: CABOT replied saying they could not find CAA for 3 historic debts so these are unenforceable but that I should continue with my monthly payments to my DMC. PRA replied very differently saying "current accounts do not require credit agreements and therefore no credit agreements have been set up when opening the account". How can these 2 Debt Companies behave and respond differently:?: I now plan to stop monthly payments to CABOT and would like your advice if there will be consequences! I am currently 70+ in poor health and want to be debt free in 2019:!: I have also sent GP medical and Cardio reports to both companies but did not receive any compassionate response:sad: Many Thanks for any advice and direction given. nacro:help: -

Good evening...... I had the pleasure of a member of Resolve Calls team visit my home this evening with regard to an old debt of an unsecured loan taken out with Northern Rock in 2004 - last paid via debt management in 2014. Cabot took up this debt in 2015, I sent them a CCA request in Jan 16 but from memory only received a standard response. I have two questions i could really do with some advice on 1) Should I write to Cabot reminding them of the outstanding CCA request or resend the request? From memory i think they sent a generic response effectively saying they were 'looking for it' . I know i should have kept this info, however the original signed agreement was definitely never provided. 2) Is there a letter or anything I can communicate to prevent these people just turning up at my door? They wrote to me months ago informing me of Resolve Calls involvement but i assumed it was fairly generic. The guy was very polite and non-threatening, I gave him no more info than he could find from the electoral roll, his objective seemed to be to get me to call his office on my doorstep at 7.30pm in the dark. At this point i politely told him that wouldn't be happening so he gave me a card with details on to call. I work away fairly often and do not want these people turning up when my partner and young son are at home alone. Thanks in advance for any advice

Good evening...... I had the pleasure of a member of Resolve Calls team visit my home this evening with regard to an old debt of an unsecured loan taken out with Northern Rock in 2004 - last paid via debt management in 2014. Cabot took up this debt in 2015, I sent them a CCA request in Jan 16 but from memory only received a standard response. I have two questions i could really do with some advice on 1) Should I write to Cabot reminding them of the outstanding CCA request or resend the request? From memory i think they sent a generic response effectively saying they were 'looking for it' . I know i should have kept this info, however the original signed agreement was definitely never provided. 2) Is there a letter or anything I can communicate to prevent these people just turning up at my door? They wrote to me months ago informing me of Resolve Calls involvement but i assumed it was fairly generic. The guy was very polite and non-threatening, I gave him no more info than he could find from the electoral roll, his objective seemed to be to get me to call his office on my doorstep at 7.30pm in the dark. At this point i politely told him that wouldn't be happening so he gave me a card with details on to call. I work away fairly often and do not want these people turning up when my partner and young son are at home alone. Thanks in advance for any advice -

Hi all, I received a letter today from BWLegal in relation to a debt of £704.80 original debt was with The Money Shop, payday loan of just over £100.00. The debt is due to be made SB in March. The letter is threatening to take me to court and place a CCJ on my credit file. I have typed the below letter and would appreciate any feedback you could give. This will be the first letter they have received from me, I have not made any contact with them previously. I have also typed out the content of the letter I received from them today. 16th January 2019 CCA Request removed please do not post our template requests. The Below is a rough outline of the letter received today Dear MR XXXXXX We have been instructed by PRAC Financial Ltd to commence legal action in the form of issuing a claim against you in the county court, without further notice, in respect of the above debt. If payment or response is not received before the 14th February 2019. If you dispute this debt please tell us why so we can help resolve this matter. Estimated Claim Such legal action may result in you being liable for court fees, solicitors costs and statutory interest which are listed below: Principal Debt: £708.74 Estimated Interest: £118.37 Estimated Court Fees: £60.00 Estimated Solicitors cost: £70.00 Enclosures Enclosed with this letter are: Information Sheet Reply Form Income & Expenditure form Particulars of the debt On 20 February 2013 you entered into an agreement with Instant Csh Loans Ltd t/a The Money Shop to provide you with a fixed sum Loan agreement account. You failed to make payment in accordance with the terms of the agreement and it was later terminated and has since been assigned to our client on the 9th December 2016. Notice of this assignment has previously been given to you. Our client is not currently applying any interest, fees or charges to your account. Any help with my CCA Request letter is greatly appreciated, I want to make sure I have the correct sections quoted etc. Thanks in advance regards Veteran6224

Hi all, I received a letter today from BWLegal in relation to a debt of £704.80 original debt was with The Money Shop, payday loan of just over £100.00. The debt is due to be made SB in March. The letter is threatening to take me to court and place a CCJ on my credit file. I have typed the below letter and would appreciate any feedback you could give. This will be the first letter they have received from me, I have not made any contact with them previously. I have also typed out the content of the letter I received from them today. 16th January 2019 CCA Request removed please do not post our template requests. The Below is a rough outline of the letter received today Dear MR XXXXXX We have been instructed by PRAC Financial Ltd to commence legal action in the form of issuing a claim against you in the county court, without further notice, in respect of the above debt. If payment or response is not received before the 14th February 2019. If you dispute this debt please tell us why so we can help resolve this matter. Estimated Claim Such legal action may result in you being liable for court fees, solicitors costs and statutory interest which are listed below: Principal Debt: £708.74 Estimated Interest: £118.37 Estimated Court Fees: £60.00 Estimated Solicitors cost: £70.00 Enclosures Enclosed with this letter are: Information Sheet Reply Form Income & Expenditure form Particulars of the debt On 20 February 2013 you entered into an agreement with Instant Csh Loans Ltd t/a The Money Shop to provide you with a fixed sum Loan agreement account. You failed to make payment in accordance with the terms of the agreement and it was later terminated and has since been assigned to our client on the 9th December 2016. Notice of this assignment has previously been given to you. Our client is not currently applying any interest, fees or charges to your account. Any help with my CCA Request letter is greatly appreciated, I want to make sure I have the correct sections quoted etc. Thanks in advance regards Veteran6224 -

Hi, I had a letter off RW last November chasing me for a B/Card CC for £1300 (opened in 2002) last payment to BC in Summer 2017. I requested CCA off RW and they responded 2/1/19 with "couldn't find it and debt now unenforceable, but they would be in touch with regards to setting up a payment plan". Today have received a letter off them with a copy of BC CCA, but not signed by me, looks very much a generic T&C? and wanting details of my Inc & Exp. Can you tell me how I should proceed please.

Hi, I had a letter off RW last November chasing me for a B/Card CC for £1300 (opened in 2002) last payment to BC in Summer 2017. I requested CCA off RW and they responded 2/1/19 with "couldn't find it and debt now unenforceable, but they would be in touch with regards to setting up a payment plan". Today have received a letter off them with a copy of BC CCA, but not signed by me, looks very much a generic T&C? and wanting details of my Inc & Exp. Can you tell me how I should proceed please. -

Hi I was wondering if anyone can offer some advice. My partner took out a Northern Rock loan at the end of 2005 for £25,000, with agreed payment of around £37400 over 120 months. As an aside it just shows how badly NR were engaged in unethical lending as she was only on £11k a year at the time. She made 39 of those payments totalling just under £12200, and additionally she made around £470 in over payments to a grand total of £12670. After being diagnosed with a long term illness, she lost her job and then found it difficult to repay the loan. She organised token payments beginning April 2009, and paid an additional £50 before the debt was written off at just under £24700 at the end of November the same year. She continued to make token payments until the end of July 2013 at which point she could no longer afford to do so, so she stopped. The debt appears to have been sold on to Cabot in October of the same year (2013) for just under £1400 according to the full transaction statement they have returned, but there is no Notice Of Assignment documentation. She started receiving letters from Cabot in June 2018, and she wrote asking for a copy of her CCA. They have complied within the time limit with a full copy (doesn't appear to be reconstituted), including full transaction statements, and they are threatening CCJ action unless payment for the outstanding balance of the loan is made under agreed terms. Like mentioned however, there was no Notice Of Assignment documentation to say how the debt was transferred to them. My partner is very stressed by all this (especially due to the nature of her illness) as she has a very limited income from part time work (being unable to work full time), and I pay the rent and all bills so my money is stretched also. By the way, no debts appear on her credit file, so we are worried that Cabot can also mess with that now. Anyway, does anyone have advice on next steps to take? My partner is looking into a (Debt Relief Order) DRO as a possible solution. Does anyone have experience with these? Any advice would be greatly appreciated. Thank you.

-

Hi there, Looking to see if someone can give this CCA and accompanying letters a look over, I sent a CCA Request to PRA Group and got the attached back from them is it all there and legit? This is in regard to a recent agreement. Thanks in advance. Barclaycard Letter Redacted.pdf Barclaycard Base CCA Redacted.pdf Barclaycard CCA Redacted.pdf PRA Reply Redacted.pdf

-

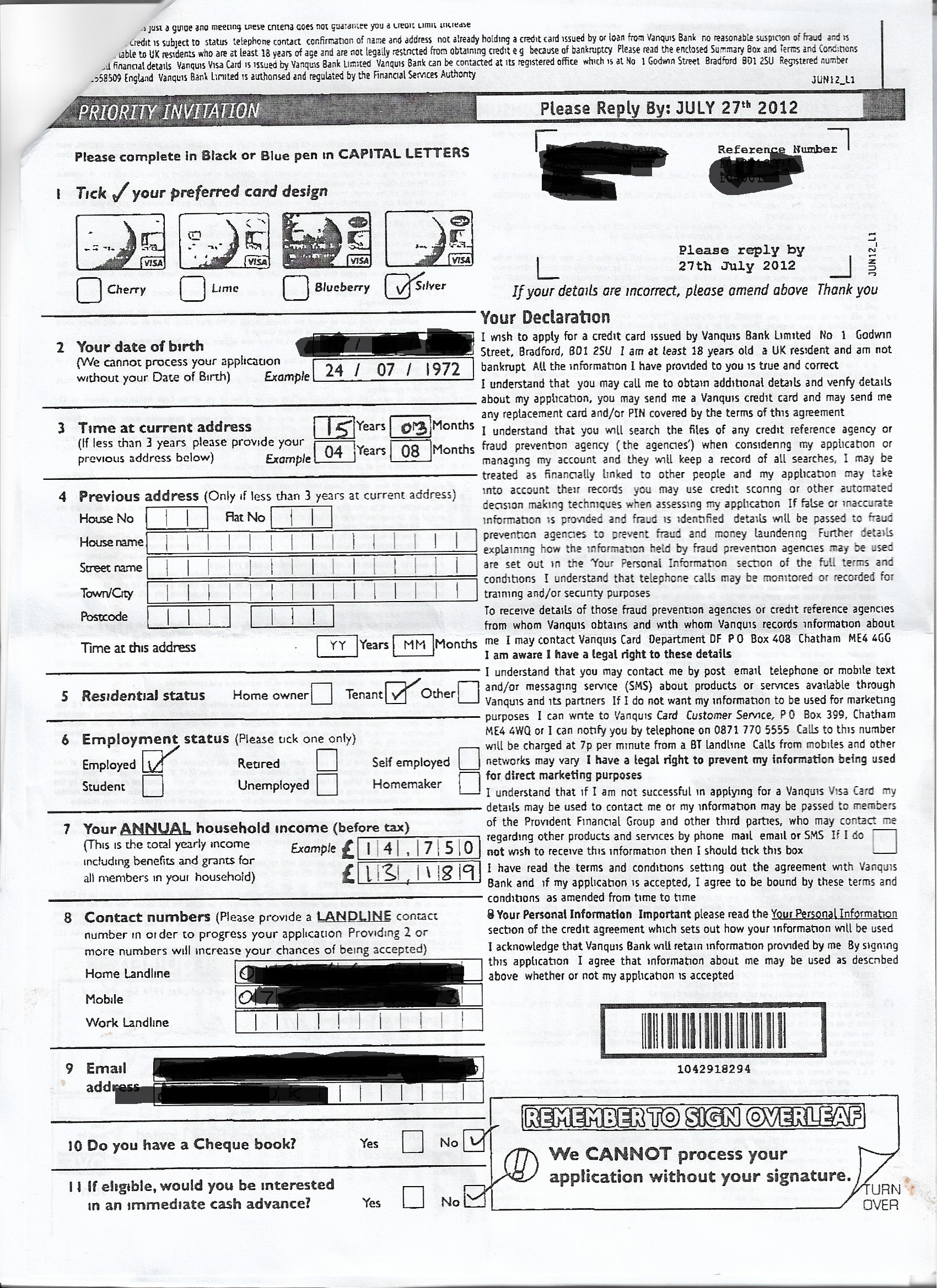

Good morning all, Please could anyone advise if this is an enforceable CCA - received from Lowells for a Vanquis credit card. They've added a sticker with a company reps signature over the date with my signature, which is oddly located - I always sign squarely in the centre of any box. Plus are the elements all correct as I have looked but just not sure. Many thanks in advance.

-

Hi thanks to a member on here telling me to CCA Barclaycard I am looking for help. What makes it unenforceable I keep looking and some people say they have to produce original paperwork, others say they can send a revised one, being taken out in 1999 does it need to show my signature? Any help would be more than appreciated. X

-

Please help , Ive had a Halifax card since late 2004. In early 2007 the account number was changed ( I imagine I may have lost my card and been sent a new one ) or am I being naïve ? Over the next several years my credit limit kept on increasing without me requesting it. It was raised 11 times from the original £2750 till in spring 2014 it stood at £13950 Towards the end of that year Halifax told me that my interest rate was to be hiked up but explained that if I didn't agree to this I was entitled to close the account and pay it off as was previously the case. At this time I was struggling financially and the card was maxed out, so, as the minimum payment was already proving to be a burden I chose to close the account. Since then and up to today Ive never missed a payment and have paid a total of £8000 but have accrued £5450 in interest. So Im still £11400 in debt to them. Last month they kindly reminded me that "just paying minimum payments " is likely to be expensive for me but worryingly they quoted a new FCA DIRECTIVE which says I am in "Persistent debt". I came across your wonderful site and read up and decided to request a copy of my agreement. my request was made using the most recent account number ie from 2007 and what was sent doesn't seem to be an agreement..please help rather worryingly ten minutes after posting my question I got a call on my mobile from 07889902214 and a taped message telling me about a govt scheme to write off debt! Ive NEVER EVER had such a call in the past EVER so something fishys going on!

-

Hi, *deep breath* I am new to the forum so hello everyone, can i say what a great resource of information this place is i have been lurking and reading up the past few weeks and it has helped me massively and made me realise a few things too:) I have been on a DMP for just over 10 years trying to payback a whole load of debt i ran up years ago (i wont go into detail, long story short i was young, naive and the crash in 2008 crippled me when all the discounted mortgage deals got pulled the day before my discounted rate with NR ended), anyway... i have only recently found out about CCA requests and as most of my debts are old and with DCA's i have decided to do some digging... I have sent off a whole bunch ofthe CCA requests today recorded delivery with postal orders for £1 in each. I am wondering what the likely reaction of the companies will be? I am still paying into my DMP and intend to continue doing so for now, are they likely to get uppity at my request and start adding interest and charges again or worse? I am a bit worried about that to be honest. Below is a list of the DCA's and the approx amounts they say i owe, any info about how they are likely to respond or what i should do next would be great guys. Cabot Financial (Europe) Ltd - 4k Cabot Financial (Europe) Ltd - 2.5k Cabot Financial (Europe) Ltd - £700 Clarity Credit Management Solutions Ltd - 1.3k Link Financial Ltd 1.1k Link Financial Ltd - 2.9k Moorcroft - 1.1k Paragon - 1k Paragon - 1.3k Wescot Credit Services - 8k I have looked back and know i have more than paid back what i originally borrowed, this has been going on for nearly 10 years now and i need it to be over i think the bulk of the alleged outstanding amounts will be due to interest charges ect... but i just let the DMP deal with it for years and didnt take much notice..i also moved from CCCS to Payplan a year ago when i was toying with the idea of IVA which i didn't end up doing as wouldn't have been right for my circumstances Any help/advice appreciated. Thanks again for being a great resource for information.

-

Hi all Hope everyone is well. Had this back recently - after months on inactivity on all accounts. For a Lloyd’s credit card This is the one and only sheet sent back from Idem. Looks like an application form to me ? Any help much appreciated. Thanks for looking and Bon weekend ! Here is correct picture Lloyd’s scan 2.pdf

Hi all Hope everyone is well. Had this back recently - after months on inactivity on all accounts. For a Lloyd’s credit card This is the one and only sheet sent back from Idem. Looks like an application form to me ? Any help much appreciated. Thanks for looking and Bon weekend ! Here is correct picture Lloyd’s scan 2.pdf -

I recently made a section 78 CCA request to Cabot who I have been paying a debt off to for 2 years. There was another 12 months left until I realised I could make a CCA request to them. I received a reply today saying that they could not get the info from the original lender, and the account is unenforceable. What data position does this place them in? Can they still request from me or use my data in any way? What about the default under their name on my credit file?

-

Hi, If I have 4 accounts with one DCA, do I need to submit a separate CCA letter per account and a £1 postal order per account or can I just do one CCA requests to them listing all accounts and one postal order? I assume it's the former but wanted to check. Thanks

-

A family member had a loan with Northern Rock. She requested a CCA from them but never heard anything from them. Northern Rock was taken over by NRAM and that was 11 years ago. They have now been contacted by NRAM saying about the Northern Rock loan was being passed to Cabot and for them to contact Cabot regarding the loan. Is it best just to ignore the letter and if they do take it to court go for the Statue Barred letter? Thank you for your help.

-

Good afternoon everyone, I sent off a CCA Request to Santander regarding a Debenhams store card, and got the following back. Does this mean they do not have an original copy on file. The card was originally run by GE Money and sold on to Max Recovery after I took out an IVA in 2012, or should I have written to GE Money or Max Recovery. Any help appreciated. img004.pdf img002.pdf img003.pdf

-

Good evening all, I've done a bit of research trying to close accounts which led me to requesting CCA's to Cabot. I sent two for two different accounts which they took off Halifax (1 x CC & 1 x Current Acc Overdraft). I posted the following to them: Dear Sir/Madam Account No: With reference to the above agreement, I require you to supply the following documentation before I will correspond with you further on this matter. 1. You must supply me with a true copy of the alleged agreement you refer to. This is my right under your obligation to supply a copy of the agreement, under the legislation contained within s.78 (1) Consumer Credit Act 1974. 2. A full statement of account. 3. A signed true copy of the deed of assignment of the above referenced agreement that you allege exists. 4. A copy of any other documents referred to in the agreement. I understand that under the Consumer Credit Act 1974 (sections 77-79) , I am entitled to receive a copy of any credit agreement and a statement of account when I request it. I enclose a payment of £1 which is the fee payable under the Consumer Credit Act 1974. I understand a copy of any credit agreement along with a statement of account should be supplied within 12 working days. I understand that, under the Consumer Credit Act 1974, creditors are unable to enforce an agreement if they fail to comply with the request for a copy of the agreement and statement of account. A speedy response would be appreciated to resolve the matter amicably. I look forward to hearing from you soon. Yours faithfully THE LETTERS WERE RECEIVED ON 17TH/18TH JULY AND TODAY I RECEIVED THE FOLLOWING LETTERS: Thank you for your CCA request etc etc... We currently do not have this information on file. However I have requested the relevant details, which include a copy of the credit agreement, statement of account and relevant terms and conditions from the original lender. You have requested a copy of the Deed of Assignment. Please be advised that the DOA is a confidential document between Cabot and the original lender. It does not contain any personal details relating to you or your account and is not available for disclosure. We sent you a Notice of Assignment for your account to your address, which is sufficient to confirm our ownership of this account. Only the courts can request this... Blah blah blah. A couple of things here... I asked for a true copy, they are referring to simply a copy. If they do obtain a copy, is this enforceable? Also is it acceptable what they are saying about disclosing the DOA to me? I don't ever recall being sent a Notice of Assignment, if I did, is this sufficient to confirm ownership and enforceable? I have been currently paying towards what they are claiming, on a monthly basis via DMP. The next payment is due in a couple of days. Should I continue paying or is it advisable to stop until they wholly action my request? Thanks in advance and any help/advice/feedback is much appreciated! I'm looking to get a mortgage by the end of the year so I can get my son into the school I/he wants. Many thanks.

Good evening all, I've done a bit of research trying to close accounts which led me to requesting CCA's to Cabot. I sent two for two different accounts which they took off Halifax (1 x CC & 1 x Current Acc Overdraft). I posted the following to them: Dear Sir/Madam Account No: With reference to the above agreement, I require you to supply the following documentation before I will correspond with you further on this matter. 1. You must supply me with a true copy of the alleged agreement you refer to. This is my right under your obligation to supply a copy of the agreement, under the legislation contained within s.78 (1) Consumer Credit Act 1974. 2. A full statement of account. 3. A signed true copy of the deed of assignment of the above referenced agreement that you allege exists. 4. A copy of any other documents referred to in the agreement. I understand that under the Consumer Credit Act 1974 (sections 77-79) , I am entitled to receive a copy of any credit agreement and a statement of account when I request it. I enclose a payment of £1 which is the fee payable under the Consumer Credit Act 1974. I understand a copy of any credit agreement along with a statement of account should be supplied within 12 working days. I understand that, under the Consumer Credit Act 1974, creditors are unable to enforce an agreement if they fail to comply with the request for a copy of the agreement and statement of account. A speedy response would be appreciated to resolve the matter amicably. I look forward to hearing from you soon. Yours faithfully THE LETTERS WERE RECEIVED ON 17TH/18TH JULY AND TODAY I RECEIVED THE FOLLOWING LETTERS: Thank you for your CCA request etc etc... We currently do not have this information on file. However I have requested the relevant details, which include a copy of the credit agreement, statement of account and relevant terms and conditions from the original lender. You have requested a copy of the Deed of Assignment. Please be advised that the DOA is a confidential document between Cabot and the original lender. It does not contain any personal details relating to you or your account and is not available for disclosure. We sent you a Notice of Assignment for your account to your address, which is sufficient to confirm our ownership of this account. Only the courts can request this... Blah blah blah. A couple of things here... I asked for a true copy, they are referring to simply a copy. If they do obtain a copy, is this enforceable? Also is it acceptable what they are saying about disclosing the DOA to me? I don't ever recall being sent a Notice of Assignment, if I did, is this sufficient to confirm ownership and enforceable? I have been currently paying towards what they are claiming, on a monthly basis via DMP. The next payment is due in a couple of days. Should I continue paying or is it advisable to stop until they wholly action my request? Thanks in advance and any help/advice/feedback is much appreciated! I'm looking to get a mortgage by the end of the year so I can get my son into the school I/he wants. Many thanks. -

Hi I need some advice about requesting a CCA ive got a ccj more than 4 yrs old I'm being threatened with a warrant of control from restons unless I fill in a expenditure form is there any point in requesting a CCA the original debt is from around 8yrs ago and I've never responded to any letters or paid anything Would like to get some info on this Thanks in advance

Hi I need some advice about requesting a CCA ive got a ccj more than 4 yrs old I'm being threatened with a warrant of control from restons unless I fill in a expenditure form is there any point in requesting a CCA the original debt is from around 8yrs ago and I've never responded to any letters or paid anything Would like to get some info on this Thanks in advance -

Hi all, I have no idea if the reconstituted agreement I have received from Link Financial is enforceable. It is a £6k debt with Barclaycard. Please can somebody advise me how to upload this for somebody to check if it is enforceable? Thanks,

Hi all, I have no idea if the reconstituted agreement I have received from Link Financial is enforceable. It is a £6k debt with Barclaycard. Please can somebody advise me how to upload this for somebody to check if it is enforceable? Thanks, -

Hi I've just received a 'Letter Of Claim' from Howard Cohen & Co. Solicitors stating their client as "HPH2 LTD (Ex Tesco Personal Finance PLC)" also referenced in the letter as "Hoist Portfolio Holding 2 Ltd" regarding it's 'intention to issue proceedings in the County Court'. It also says "Despite our client or it's agents, Robinson Way Limited..." I believe my first course of action is to issue a CCA Request to the debt collector / client? The problem is that I cant find a UK address for Hoist Portfolio Holding 2 LTD but have found a Jersey address. The UK arm appears to be Hoist Finance who in turn own Robinson Way. Which of these companies should I write to with the CCA request? It's in relation to an amount of c.£5,500 on a credit card agreement allegedly signed in April 2008 Thanks

Hi I've just received a 'Letter Of Claim' from Howard Cohen & Co. Solicitors stating their client as "HPH2 LTD (Ex Tesco Personal Finance PLC)" also referenced in the letter as "Hoist Portfolio Holding 2 Ltd" regarding it's 'intention to issue proceedings in the County Court'. It also says "Despite our client or it's agents, Robinson Way Limited..." I believe my first course of action is to issue a CCA Request to the debt collector / client? The problem is that I cant find a UK address for Hoist Portfolio Holding 2 LTD but have found a Jersey address. The UK arm appears to be Hoist Finance who in turn own Robinson Way. Which of these companies should I write to with the CCA request? It's in relation to an amount of c.£5,500 on a credit card agreement allegedly signed in April 2008 Thanks -

Hi im new to the forum I have recently stopped paying my loan, I recall the loan company sending me out my loan agreement and making me hand sign it in late 2016. If I was to do a CCA will they need to show the signed agreement?

.jpg.f47a48c30e96170c55f95f84f13d0e48.jpg)

.jpg.d129be8d5ac67a57ddec55f9b7677710.jpg)