Search the Community

Showing results for tags 'application'.

-

Hi all, I have received a form N244A notice of hearing of application today for a hearing scheduled for 20 Oct 17. This is in relation to a Tomlin Order that i had been paying monthly since april 15. In may this year i was signed off from work due to ill health and only receive statutory sick pay at approx £400 per month. (i am still off work) I contacted all my creditors and informed them and all were happy with token payments (TPP set up via stepchange) I contacted pestons to tell them and offered them a reduced payment of £20 per month until i was back in work when i would continue with the agreed 200 a month. They wanted bank statements, employers letters, GP letters and various other bits of paper. i didn't supply them with any of it - they already have too much info on me in my opinion. This is the reason for the N244A arriving today. Can i apply to the court for a variation at this stage or have i missed the boat on that one? If so do i need to do anything or wait until the imminent CCJ is served on me? Any advice will be greatly appreciated.

Hi all, I have received a form N244A notice of hearing of application today for a hearing scheduled for 20 Oct 17. This is in relation to a Tomlin Order that i had been paying monthly since april 15. In may this year i was signed off from work due to ill health and only receive statutory sick pay at approx £400 per month. (i am still off work) I contacted all my creditors and informed them and all were happy with token payments (TPP set up via stepchange) I contacted pestons to tell them and offered them a reduced payment of £20 per month until i was back in work when i would continue with the agreed 200 a month. They wanted bank statements, employers letters, GP letters and various other bits of paper. i didn't supply them with any of it - they already have too much info on me in my opinion. This is the reason for the N244A arriving today. Can i apply to the court for a variation at this stage or have i missed the boat on that one? If so do i need to do anything or wait until the imminent CCJ is served on me? Any advice will be greatly appreciated. -

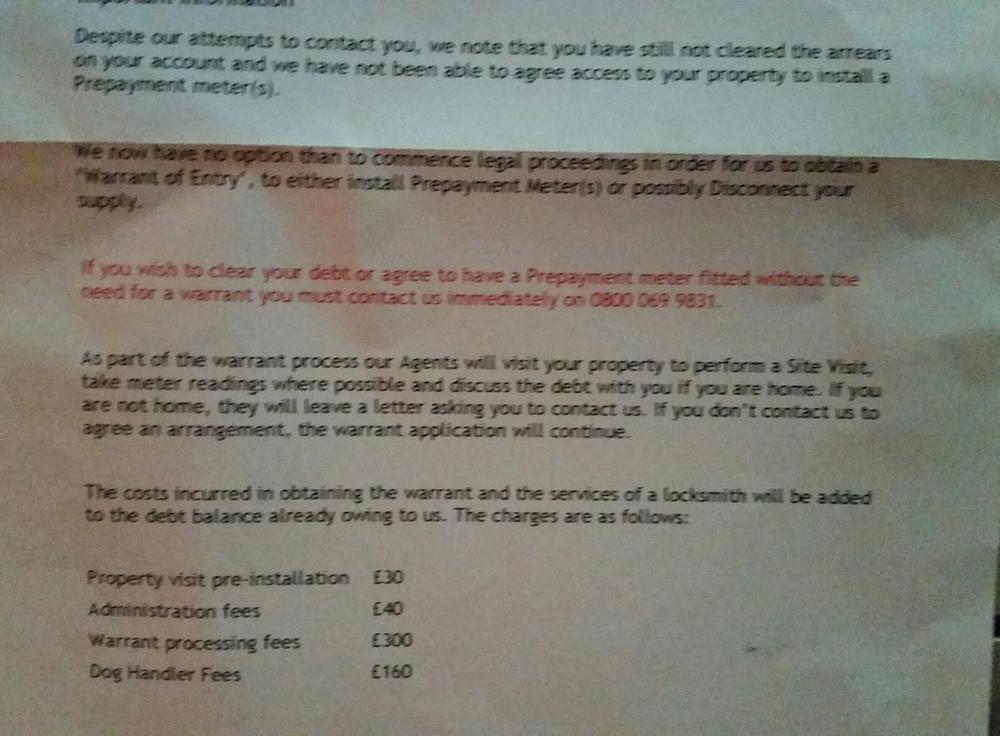

Hi folks, hope someone can give me some advice please. I missed a month's direct debit for my electricity supply from edf; they cancelled the direct debit and gradually I fell behind. I used their online chat application and 'spoke' to an operative - I said that as I'm paid weekly I'd be able to repay the outstanding amount at £25 per week, ie £100 every four weeks. The lady said I had to pay by direct debit, £100 a month I said I'd rather pay weekly and she said that she would note that on my account. I set up a standing order and have paid £25 every Friday for the last probably 4 months. The outstanding was about £400-ish, sorry I can't remember exactly. I started getting letters from edf saying I had this outstanding balance that needed to be paid off, then would come home from work to notes through the door from debt collectors saying they'd tried to gain access. This morning I had a letter through the post from Resolvecall saying that they are applying for a warrant to come into my home and fit a prepayment meter and the hearing is on 12 October at my local court house. The amount they say is outstanding is £431.41 I read the meter and sent it to edf last week to see where I was the bill was in the region of £600. Resolvecall letter is dated 25 September and I read the meter before that so their info is out of date. I'm paying this as quick as I can and now I'm worried sick. What should I do please? Thanks in advance

Hi folks, hope someone can give me some advice please. I missed a month's direct debit for my electricity supply from edf; they cancelled the direct debit and gradually I fell behind. I used their online chat application and 'spoke' to an operative - I said that as I'm paid weekly I'd be able to repay the outstanding amount at £25 per week, ie £100 every four weeks. The lady said I had to pay by direct debit, £100 a month I said I'd rather pay weekly and she said that she would note that on my account. I set up a standing order and have paid £25 every Friday for the last probably 4 months. The outstanding was about £400-ish, sorry I can't remember exactly. I started getting letters from edf saying I had this outstanding balance that needed to be paid off, then would come home from work to notes through the door from debt collectors saying they'd tried to gain access. This morning I had a letter through the post from Resolvecall saying that they are applying for a warrant to come into my home and fit a prepayment meter and the hearing is on 12 October at my local court house. The amount they say is outstanding is £431.41 I read the meter and sent it to edf last week to see where I was the bill was in the region of £600. Resolvecall letter is dated 25 September and I read the meter before that so their info is out of date. I'm paying this as quick as I can and now I'm worried sick. What should I do please? Thanks in advance -

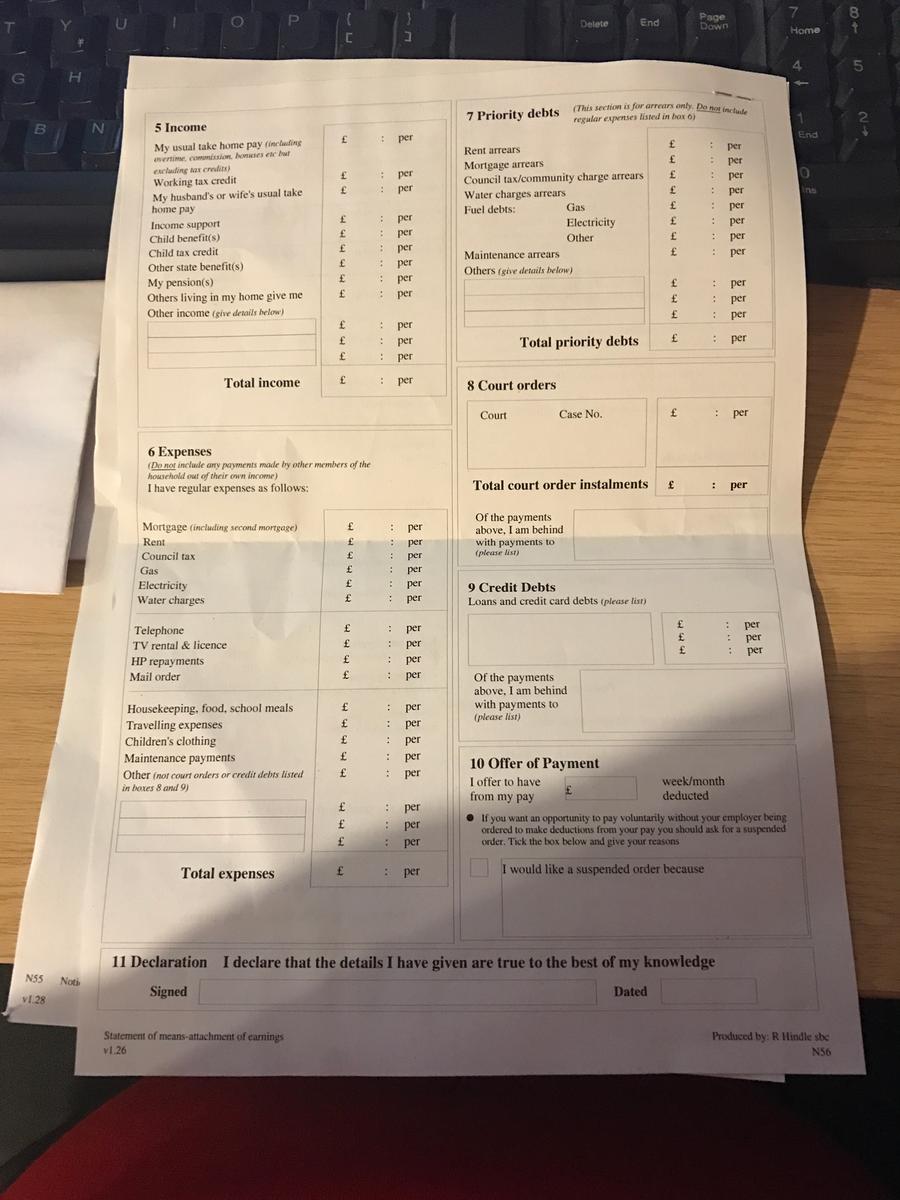

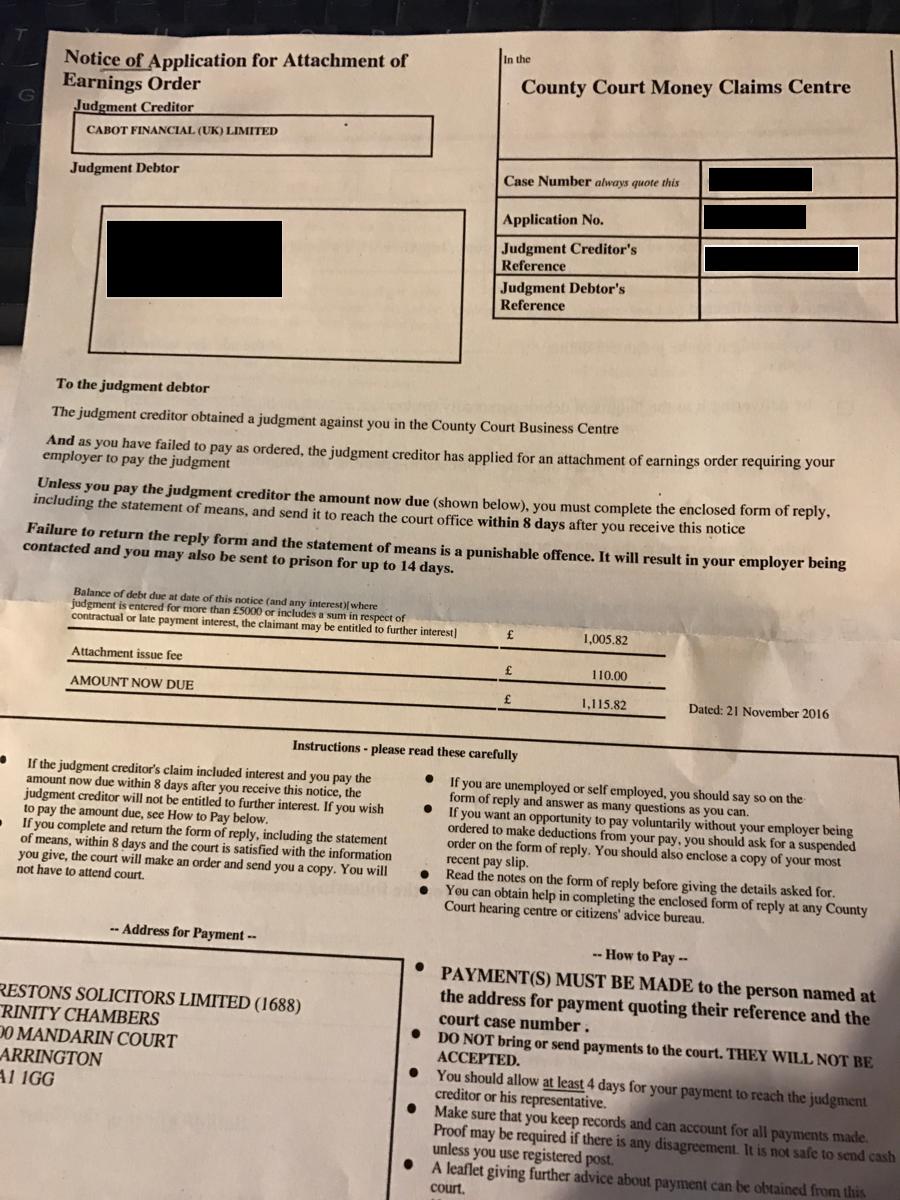

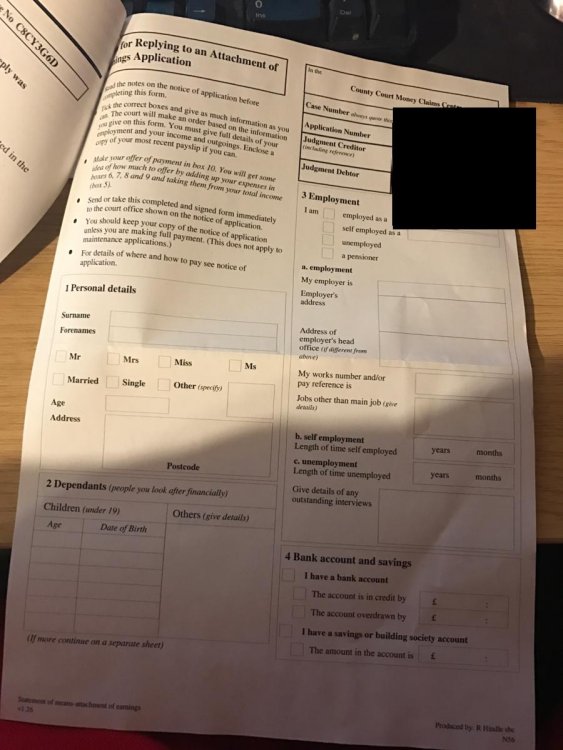

I have just gotten a Nottice of Application for Attachment of Earnings Order for a sum of just over £900 for CCJ issued in the CC busines Court Centre on behalf of Cabot Looking on my CC file i see a CCJ was obtained in summer 2015 for Cabot which after some research appears to be Welcome finance related. (i will contact Mortimer Clarke to confirm who the claimed creditor is but am pretty sure it isnt anyone else) It is the first time i have heard about this CCJ/debt. I returned my car to welcome finance in 2011 and changed address three times since then. I dont think ?I owed/owe them anything and I am not going to be paying £900 in any form if i can help it. I understood i had no debt to them but prior to returning the car under the agreement, I had had some arrears which i had cleared. My income is borderline for getting court fees paid An AOE could affect my job as i work for the government in a finance related role. I understand I can apply to have the CCJ put aside. I understand I could apply for a stay of the warrant I understand I can contact Welcome Finance for a Subject Access Request I have to reply to the application in eight days I don't think I had any PPI with Welcome Finance If I complete the N55 notice of AOE order Form do i make offer payment of an amount and then make the other application (vary warrant or overturn CCJ) or should i simply make an application to suspend and tick the box on the N55 saying I want to the order suspended because I have made that application. Or something else ? My income and expenditures are low and in the past i have made requests to vary judgements on grounds of low income that were accepted by courts after applying to stay warrant. but those were for debts i knew I owed and had had a chance to defend. Thank you in advance.

I have just gotten a Nottice of Application for Attachment of Earnings Order for a sum of just over £900 for CCJ issued in the CC busines Court Centre on behalf of Cabot Looking on my CC file i see a CCJ was obtained in summer 2015 for Cabot which after some research appears to be Welcome finance related. (i will contact Mortimer Clarke to confirm who the claimed creditor is but am pretty sure it isnt anyone else) It is the first time i have heard about this CCJ/debt. I returned my car to welcome finance in 2011 and changed address three times since then. I dont think ?I owed/owe them anything and I am not going to be paying £900 in any form if i can help it. I understood i had no debt to them but prior to returning the car under the agreement, I had had some arrears which i had cleared. My income is borderline for getting court fees paid An AOE could affect my job as i work for the government in a finance related role. I understand I can apply to have the CCJ put aside. I understand I could apply for a stay of the warrant I understand I can contact Welcome Finance for a Subject Access Request I have to reply to the application in eight days I don't think I had any PPI with Welcome Finance If I complete the N55 notice of AOE order Form do i make offer payment of an amount and then make the other application (vary warrant or overturn CCJ) or should i simply make an application to suspend and tick the box on the N55 saying I want to the order suspended because I have made that application. Or something else ? My income and expenditures are low and in the past i have made requests to vary judgements on grounds of low income that were accepted by courts after applying to stay warrant. but those were for debts i knew I owed and had had a chance to defend. Thank you in advance. -

Hi I received a claim form last year with regard to an apparent arrow global debt I owe. The debt was bought from a halifax credit card. I did a CCA and CPR request to them straight away. There was then a stay on proceedings while they got the relevant documentation together. They have now submitted a notice of application to get the stay lifted and for summary judgement to be made against me. However they do not appear to attached terms and conditions to the credit agreement, just something entitled 'Key Financial Information'. Please see attached document. They have also not supplied a copy of the default notice, just a computer database entry of it. I am going to base a defence on the fact they have not complied with the CCA request, due to the missing terms and conditions. So have not complied with section 78 of the CCA. Also that they have not supplied a copy of the default notice, therefor cannot prove that a compliant default notice has been served, pursuant to sections 87 and 88 of the CCA. Please could you have a look at the three attachments and let me know what you think. credit agreement, terms and conditions(supposed), and default notice database entry. Thanks CCA return.pdf

Hi I received a claim form last year with regard to an apparent arrow global debt I owe. The debt was bought from a halifax credit card. I did a CCA and CPR request to them straight away. There was then a stay on proceedings while they got the relevant documentation together. They have now submitted a notice of application to get the stay lifted and for summary judgement to be made against me. However they do not appear to attached terms and conditions to the credit agreement, just something entitled 'Key Financial Information'. Please see attached document. They have also not supplied a copy of the default notice, just a computer database entry of it. I am going to base a defence on the fact they have not complied with the CCA request, due to the missing terms and conditions. So have not complied with section 78 of the CCA. Also that they have not supplied a copy of the default notice, therefor cannot prove that a compliant default notice has been served, pursuant to sections 87 and 88 of the CCA. Please could you have a look at the three attachments and let me know what you think. credit agreement, terms and conditions(supposed), and default notice database entry. Thanks CCA return.pdf -

Hi, I am in need of urgent advice. In April 2014 after losing a High Court case brought against myself and 8 others by our former employer, an interim charging order was made final. During the hearing I offered to pay the judgement debt (£8,000 + costs and interest of £120,000.00) by affordable monthly instalments of £100.00 but this was refused by the claimant who stated to the court that they had "no intention of applying for an order for sale but merely wanted to protect their interests". I subsequently made a number of instalment offers to the claimants but each offer was refused and indeed, my letters were often ignored by the claimant and their solicitor or they would take months to reply. In December 2016 I received a copy of an order issued by the High Court granting leave to the claimants to apply for an order for sale. The witness statement attached to the order was prepared by a solicitor who has subsequently been struck off for dishonesty and fraud! The statement also contain a number of factual mistakes and exaggerated the value of my home describing a different property to the one that I actually own. (using a Zoopla valuation as evidence of property value). The claimants issued their application for leave in the QBD of the High Court and the application was subsequently transferred to the Chancery Division where the order for leave was granted. the case was then transferred to the Central County court before being transferred again to Portsmouth County Court. At the hearing, the claimants failed to turn up and had written the day before to the court stating that they believed that they would not get a fair hearing (as one of my codefendant's partner had worked at the court 10 years previously!!!). The DJ was not impressed but would not dismissed the case as he believed that the claimants would only apply to reinstate proceedings. He subsequently transferred the proceedings to another County Court where the application will now be heard on 26th May (for directions). I am sorry that this preamble is so long winded! I need advice about what to do next. At the Portsmouth hearing the DJ alluded to the Human Rights Act (I assume he meant Article 8) although I am not sure how to use this during the hearing. My home is in joint names with my wife. My 20 year old daughter also resides with us. She is a full time university student and suffers with anxiety and dyslexsia. My wife works part time on a modest income. My income is also quite modest. The correct zoopla valuation for my home is £146K approx and my current interest only mortgage is £138K. After deduction of estate agents commission, solicitors and removal costs there is gross equity of about £2,000.00 (half of which presumably will have to be paid to my wife as she is not a party to the proceedings). The High court have never determined what my financial interest in the property actually is My interest only mortgage ends in about 6 years and, as I cannot afford to repay the loan, my family and I will have to move (possibly to a shared ownership property). I would welcome any advice and assistance that any cagger's can give to me about how to deal with this upcoming hearing (assuming that the claimant's turn up this time). In anticipation I appreciate any help that can be provided to me.

-

My Daughter has be hassled by Shoosmiths/ARC over an alleged debt with Egg, this started in March 2011 several DCA's have written and to each we have sent a S78 request, and had nothing returned other than a blank 'example' agreement. A couple of years ago Shoosmiths issued court papers to which I filed a defence on her behalf, pointing out that S78 had not been complied with and that a multitude of DCA's and solicitors had written a range of letters alleging debts but for a number of varying amounts. Shoosmiths responded by withdrawing the court application, out off the blue today we get a letter threatening an application for Summary Judgment, and wanting us to set up an agreement for repayment with them. My Daughter had a nervous breakdown several years ago 2007/8 and genuinely has no recollection of these debts and I have been managing them on her behalf, in may cases PPI has more than covered the debt but Shoosmiths have been particularly difficult to deal with and if this is a genuine debt then it will almost certainly have PPI attached to it, but apart from a bare minimum of information they have given me nothing to work with. I feel like calling their bluff, but the amount they are claiming is around £2k0 and if genuine is not a single debt but a number rolled into one, or has a significant amount of charges added. What would be my best course of action? Thanks in advance.

My Daughter has be hassled by Shoosmiths/ARC over an alleged debt with Egg, this started in March 2011 several DCA's have written and to each we have sent a S78 request, and had nothing returned other than a blank 'example' agreement. A couple of years ago Shoosmiths issued court papers to which I filed a defence on her behalf, pointing out that S78 had not been complied with and that a multitude of DCA's and solicitors had written a range of letters alleging debts but for a number of varying amounts. Shoosmiths responded by withdrawing the court application, out off the blue today we get a letter threatening an application for Summary Judgment, and wanting us to set up an agreement for repayment with them. My Daughter had a nervous breakdown several years ago 2007/8 and genuinely has no recollection of these debts and I have been managing them on her behalf, in may cases PPI has more than covered the debt but Shoosmiths have been particularly difficult to deal with and if this is a genuine debt then it will almost certainly have PPI attached to it, but apart from a bare minimum of information they have given me nothing to work with. I feel like calling their bluff, but the amount they are claiming is around £2k0 and if genuine is not a single debt but a number rolled into one, or has a significant amount of charges added. What would be my best course of action? Thanks in advance.

-

Hi all, It would be literally life changing if you can help with this one! Last year I checked my credit file and found I had a CCJ. The claimant was the managing agents for a flat I owned, the amount £1314 and it was registered in November 2012. Being a bit worried about the word CCJ I paid it immediately (Dec '14) and then set about investigating it. It turned out that despite notifying them of a change in correspondence address (I moved out and tenant moved in), they had been writing to the flat to notify me that my standing order for ground rent wasn't set up properly (I think after changing bank accounts). The tenant, I'm sure thinking he was being helpful, kept my post safe for me until he moved out!! The pile was nearly 1m high when I eventually reclaimed it! After a bit of internet investigation I figured I had grounds to have the Judgement Set Aside by Consent - I spoke to the claimant and they agreed to have it set aside they got their solicitors to issue a "Consent Order". I sent this with the correct forms and my own explanation of events to the courts along with £50. After 10 days or so I received a letter back from the courts telling me that my application had been rejected as the judge felt my application amounted to "credit repair". It went on to say that the judgement was paid and would be marked satisfied on my credit file. Fair enough I thought... That was until I recently applied for a mortgage and the underwriter informed me that I was "out of policy" until the debt had been cleared for at least 3 years. You can imagine how frustrated I am now with hindsight that the judge had felt it necessary to reject my application. Why would ANYONE want a judgement set aside if it wasn't to repair or reset their credit?! Surely he should of considered the facts rather than base his decision on opinion?! I paid a debt as soon as I found out about it and I've ended up with a 3 year sentence - you'd get as much for aggravated assault! I've spoken to the court again and despite it being longer than 7 days, I can apparently fill in a different form and send another £50 to appeal the judgement. My question, albeit a little long-winded, is: what chance have I got of winning an appeal? I don't want to throw another £50 at this and end up with the same result BUT if I knew I could get it set aside, I'd happily pay a hell of a lot more! If someone thinks they might be able to help, I'd happily pass on any documentation I have. Thanks.

Hi all, It would be literally life changing if you can help with this one! Last year I checked my credit file and found I had a CCJ. The claimant was the managing agents for a flat I owned, the amount £1314 and it was registered in November 2012. Being a bit worried about the word CCJ I paid it immediately (Dec '14) and then set about investigating it. It turned out that despite notifying them of a change in correspondence address (I moved out and tenant moved in), they had been writing to the flat to notify me that my standing order for ground rent wasn't set up properly (I think after changing bank accounts). The tenant, I'm sure thinking he was being helpful, kept my post safe for me until he moved out!! The pile was nearly 1m high when I eventually reclaimed it! After a bit of internet investigation I figured I had grounds to have the Judgement Set Aside by Consent - I spoke to the claimant and they agreed to have it set aside they got their solicitors to issue a "Consent Order". I sent this with the correct forms and my own explanation of events to the courts along with £50. After 10 days or so I received a letter back from the courts telling me that my application had been rejected as the judge felt my application amounted to "credit repair". It went on to say that the judgement was paid and would be marked satisfied on my credit file. Fair enough I thought... That was until I recently applied for a mortgage and the underwriter informed me that I was "out of policy" until the debt had been cleared for at least 3 years. You can imagine how frustrated I am now with hindsight that the judge had felt it necessary to reject my application. Why would ANYONE want a judgement set aside if it wasn't to repair or reset their credit?! Surely he should of considered the facts rather than base his decision on opinion?! I paid a debt as soon as I found out about it and I've ended up with a 3 year sentence - you'd get as much for aggravated assault! I've spoken to the court again and despite it being longer than 7 days, I can apparently fill in a different form and send another £50 to appeal the judgement. My question, albeit a little long-winded, is: what chance have I got of winning an appeal? I don't want to throw another £50 at this and end up with the same result BUT if I knew I could get it set aside, I'd happily pay a hell of a lot more! If someone thinks they might be able to help, I'd happily pass on any documentation I have. Thanks. -

Hello I'm looking for advise. I live overseas for past 10 years. Yesterday at a friends address in UK where I receive my bank statements a letter arrived looking official. At my request my friend opened it. It is a Notice of Application for Attachments of Earnings Order. Judgement Creditor: Hoist Portfolio Holding 2 Limited. In the: Country Court Money Claims Centre. Amount 3,975.28 GB. The Judgement Debtor is under my maiden name and I've since been married, divorced and re-married. I have never heard of this company and no of no debt to them. They are not listed on companies house, but from research it seems they are linked to Robinson Way a DCA. There is no contact telephone number and only instruction to pay Howard Cohen & Co Solicitors, based in Leeds. Again they are not registered on Companies House. The form looks official with case number and reference number. The document is dated 17th May 2017 and says payment required in 8 days of notice or further action including a possible 14 days prison. I am very concerned especially as this is now logged at a friends address, where i have never lived but do get my UK bank statements sent to. Any advise gratefully received.

Hello I'm looking for advise. I live overseas for past 10 years. Yesterday at a friends address in UK where I receive my bank statements a letter arrived looking official. At my request my friend opened it. It is a Notice of Application for Attachments of Earnings Order. Judgement Creditor: Hoist Portfolio Holding 2 Limited. In the: Country Court Money Claims Centre. Amount 3,975.28 GB. The Judgement Debtor is under my maiden name and I've since been married, divorced and re-married. I have never heard of this company and no of no debt to them. They are not listed on companies house, but from research it seems they are linked to Robinson Way a DCA. There is no contact telephone number and only instruction to pay Howard Cohen & Co Solicitors, based in Leeds. Again they are not registered on Companies House. The form looks official with case number and reference number. The document is dated 17th May 2017 and says payment required in 8 days of notice or further action including a possible 14 days prison. I am very concerned especially as this is now logged at a friends address, where i have never lived but do get my UK bank statements sent to. Any advise gratefully received. -

Hi, first post on something I need a little help on please. I receieved a court claim about a credit card I took out 14 years ago but I had kept no records of it. I did a CPR and CCA request to get some documentation. What they sent through was a copy of the application form. All my details were legible within the white boxes of the form, strangely legible when compared to the rest of the form, but the surrounding areas with their information is illegible and very grey and pixalated. You can make out my signature, but not the date. They also sent me some terms and conditions as a separate photocopy. Am I right in thinking that pre 2007 it has to contain proof that the t's & c's were signed by me for it to be enforceable? I came across an old post in the forum about a similar issue and I'll quote it below, but does this apply too:

-

Thought it time I paid off and ditched my Vanquis card. Do not get me wrong it has been great with my credit profile. Had it for about three years, never missed a payment and have a Three Grand credit limit. So much for customer loyalty though, they point blank would not negotiate the APR, 59.9% So yesterday applied for a BarclayCard, eligibility checker stated 95% chance of being accepted. Went through the application, Digitally signed for it to come back as referred. Strange as 12 months ago did the same with Capital One and was instantly accepted with a two grand credit limit. Never missed any payment with any of my credit obligations for the last three years. Credit scores from the credit agencies mean SFA as each credit company have their own lending criteria. Now i know this is simply the automatic computer process wanting manual intervention from a human being. This was not an outright No and will be probably be accepted, But: What causes these referrals as a matter of interest??

-

I purchase a car on 29th Sept 2016 from a garage in Surrey. The car is a "lemon" when I went on the companies house to see where to send my letter of complaint under the Consumer Credit Act 1985 I found that it was dissolved in Nov 2016. I downloaded the DS01 form and found that it had been signed and dated 22 August 2016. It means that the garage sold me a car when it should not have been trading under that name. Am I right ? They may have got away with me claiming my money back from their Limited Company but has the director been acting according to the Law ? If not , who should I notify so that he gets prosecuted ? Companies House ? The Inland Revenue ? Your valuable expert advice is appreciated . Many thanks !!

-

READ MORE HERE: https://www.gov.uk/government/publications/armed-forces-veterans-badge-application-form

READ MORE HERE: https://www.gov.uk/government/publications/armed-forces-veterans-badge-application-form -

I am currently living apart from my wife. We are planning to get divorced,but have not begun proceedings, yet. Neither are we legally separated. However, all expenses are currently separate. For the purpose of completing the tax credit application form, would I be considered single or married?

-

Supply start date Feb 2014 Dispute raised March 2014 based on start of contract meter reading and inaccurate bill. September 2014 Court date set for warrant application and stated to court the warrant process was being misused and the account was in dispute warrant declined as there was no need to attend my meter for any works or service. After the declined warrant application I agreed to have smart meters fitted and debt would be refreshed due to inaccuracy on contract start date. Debt has never been wiped as agreed, so account remains in dispute. The engineers came and declared it unsafe to sit a smart meter due to age of current gas meter, they wanted to replace the meter due to age but due to location would need to consult with national grid as walls needed to be knocked through etc etc and pipes re piped. Nothing materialised, I changed my supplier however as I have discovered today only the electric went through. I was unaware that the supplier was still supplying me and assumed I was on a dual fuel tariff with new supplier however it's electric only. I have today been issued with a notice to obtain a warrant due to debt of £3500. Last meter reading was September 2014. Have bot been provided with an accurate bill in this time. The meter still awaits replacement. Any advice on how to proceed? Upon phoning them They are adamant they either need 50 % payment or they will fit a pre payment meter and deduct 20% of every top up for the debt. I'm happy to have a repayment meter however the amount of debt is not correct

Supply start date Feb 2014 Dispute raised March 2014 based on start of contract meter reading and inaccurate bill. September 2014 Court date set for warrant application and stated to court the warrant process was being misused and the account was in dispute warrant declined as there was no need to attend my meter for any works or service. After the declined warrant application I agreed to have smart meters fitted and debt would be refreshed due to inaccuracy on contract start date. Debt has never been wiped as agreed, so account remains in dispute. The engineers came and declared it unsafe to sit a smart meter due to age of current gas meter, they wanted to replace the meter due to age but due to location would need to consult with national grid as walls needed to be knocked through etc etc and pipes re piped. Nothing materialised, I changed my supplier however as I have discovered today only the electric went through. I was unaware that the supplier was still supplying me and assumed I was on a dual fuel tariff with new supplier however it's electric only. I have today been issued with a notice to obtain a warrant due to debt of £3500. Last meter reading was September 2014. Have bot been provided with an accurate bill in this time. The meter still awaits replacement. Any advice on how to proceed? Upon phoning them They are adamant they either need 50 % payment or they will fit a pre payment meter and deduct 20% of every top up for the debt. I'm happy to have a repayment meter however the amount of debt is not correct

-

Hi folks, i need somebody to inform me what the empty spaces are needing as ive re read this block several times and its not clear to me.

Hi folks, i need somebody to inform me what the empty spaces are needing as ive re read this block several times and its not clear to me.

-

Hi All, I am in a bit of a pickle at the moment, I felt I was finally able to afford my council flat that I have lived in for over 15 years, I put in my first RTB application March 2015, and a valuation was done for the property, after the valuation came out, I found that I was not able to afford it even after the London discounts so I didn’t take up the offer, fast track November 2016, the same year I made another application and this time around the price of the flat had reduced by £100k as per the new valuation done in November 2016, so I took up the offer, applied for a mortgage and got it approved etc, to my horror council wrote to me last week saying that they have now revised the offer from the council where they have changed all the figures and have now decided to use the first valuation which is 100k more than the second one. I am a little lost now and do now know what to do. I am already out of pocket after spending on solicitors and mortgage brokers. Thanks in advance.

Hi All, I am in a bit of a pickle at the moment, I felt I was finally able to afford my council flat that I have lived in for over 15 years, I put in my first RTB application March 2015, and a valuation was done for the property, after the valuation came out, I found that I was not able to afford it even after the London discounts so I didn’t take up the offer, fast track November 2016, the same year I made another application and this time around the price of the flat had reduced by £100k as per the new valuation done in November 2016, so I took up the offer, applied for a mortgage and got it approved etc, to my horror council wrote to me last week saying that they have now revised the offer from the council where they have changed all the figures and have now decided to use the first valuation which is 100k more than the second one. I am a little lost now and do now know what to do. I am already out of pocket after spending on solicitors and mortgage brokers. Thanks in advance. -

Will not name the company (for now) it's the procedure I am trying to understand. No outstanding amount on account (may be a variation on the amount used due to estimated readings but it wouldn't be a lot but essentially all bills have been paid, nothing was outstanding until now. Utility company write stating that they need to check the meter for safety reasons and quote 'Must Inspect' G4S are those wanting to read the meter, however some years before a member of g4s threatened the householder at the time that if they didn't let them in they'd get a warrant and break in....this from a meter reader and before any ''must inspect' notices had been issued, meter reader dispensed, complaint made with the householder stating any further visits for meter read would need to be anyone other than G4S... Fast Forward a couple of years to end of 2016, Must Inspect letters sent, but these were from G4S and were ignored (see above) Utility company write stating they must be contacted within 7 days to make an appt to check the meter or action will be taken, they were contacted about 14 days later and put on notice that both the utility company and the service distribution company had been in the property just 2 months earlier due to a power outage and where the meter had been checked/ main fuse taken out, tested, put back in, sealed and the road dug up for a week (generators etc) both the distribution company and the utility company had been in and checked the meter safety etc.... At around the same time a letter from G4S arrives stating the householder needs to get in touch as they needed to visually check the meter, the utility company were called again (not G4S) and the same conversation again (paragraph above) and they said not to worry, they'd get it dropped etc. Fast forward to this year, utility company process a bill, usual bill, standing charge and usage..10 days later the householder goes to pay the bill, but when going to notices a further charge of in excess of £50 ....there is nothing on the bill or the account to show as to why the additional price so a call was placed to the Utility company and where they stated 'oh, thats for the warrant application fee' Discussion ensues, they stated they could see contact had been made (as per their and G4's requests) but that the meter still needed to be checked???? The time difference between the letter requesting contact to the time the warrant application fee was applied to the account was 75 days ... G4S requested to remove the application, they state it can only come from the utility company and that as they had heard nothing the warrant application was still to go ahead. Utility company contacted again, complaint raised to a different department and where they appeared to be less than helpful, householder felt somewhat threatened/intimidated (they're registered disabled both physically and mental health) utility company are aware of the status re disabled (householder is registered for priority assistance should there be a outage) They refused to remove the fee, said it still applied, they could see that contact had been made when requested but that G4S needed to check the meter, they acknowledged that the property had been visited by them and the distribution company but still the meter needed to be checked as they'd tried for some time now (yes but it had been checked) Utility company seemed altogether oblivious to any of the points raised re: 1:/Why the fee had been added when no notification as to a court date for the application had been made and that had not the householder queried the additional fee on their newest bill they would have been oblivious to the date at court to see a warrant (only 3 weeks from the time of the fee being added (so not long to go now for the householder) 2:/ Why the utility company acknowledged that when requested they be contacted that they were contacted which in essence nullifies their 'if you dont contact us we'll do......) and where situation explained and they appeared to have accepted it that they then reverse that acceptance. 3:/ Why the extra fee levied does not correspond to their online 'charges' for the same 'application' 4:/ Why they or agents acting on their behalf (G4S) took (a) 75 days to apply the fee and presumably make an application to the court and why they did not inform the householder when the court date was or indeed what court it was to be at? 5:/ Why when they can see both themselves and the distribution company have been in the property and at the meter (checked/resaled/) previous to their warrant threats that this appears not to register with them --- The final contact from the elongated and somewhat intimidating/threatening Utility company wasa followed up by an email to the householder stating 'thanks but we're not withdrawing the warrant and that g4s would still need to attend. ... Further to that, there are a couple of other points to ponder and as yet the householder has not put this to the utility company and any advice confirmation (if applicable) be given. 1:/ G4S as a meter reading company no longer exist, they were sold with the sale complete in January 17, so any court application and when G4S were called a few days ago and where they answered the call as G4S and spoke regarding a reference number on their letter from last year? would need to be from the American company that purchased G4S? 2:/ The legal requirement to inspect a meter was repealed in 2016, becoming defunct from April 1st 2016 , yet 9 months later the Utility company in their letters stated they are 'required by law to check 'your' meter every two years and where you are required to allow them access. I have read the repeal on Ofgem's site, it's quite clear. (they also state somewhere that any utility company using the 2year argument post April 2016 would be pursued Calls to the Utility Company were recorded and they were informed as much, I've listened to some of them, they're dreadful listening and I as an individual could clearly hear the distress in the householders voice and also detect the undeniable intimidatory tone from the Utility company employees The Householder going to court would be detrimental to their health, physically difficult, mentally pretty much impossible but court they will go, better to be avoided but when the above is the situation any homeonwer/tenant would want to protect their home from what is pretty much unlawful entry. Deb Any thoughts ? views? re the Must Inspect repeal?

-

Hi, I am currently representing my daughter on the McKenzie friend basis in her claim for unfair dismissal on the grounds of discrimination ( pregancy ) We have followed all the procedures through ACAS and we are currently taking her employer through the Employment Tribunal, which has taking about seven months to get to a Trial which has been listed for next week 4/5th February 2016, this was after a previous hearing. Today i receive a letter from the Tribunal stating that the trial might be postponed on the grounds that despite knowing for a number of months that in any event, the trial would be considered by a panel rather than a single judge because it is a discrimination case, to use this as a reason, and so late in the day does not add up, they would have known months in advance that a panel would need to be assigned, so in using this has delayed even further. The Tribunal are also aware that the Respondents are in abuse of process as they have failed to abide the previous order for them to provide a trial bundle, witness statements and further and better particulars in readiness for the trial next week? Because of this we made an application for the Tribunal to make an unless order for this evidence to be giving as all of it is central to the claim and it had been previously ordered. We have also written to the other side and in anticipating the Tribunal not making the unless order, which seems very reasonable, by stating that we would provide our own trial bundle and giving them seven days to object. Since all of this has happened in the last couple of days, the Tribunal as it would appear are bending over backwards in allowing the previous orders be breached and ignored and they have also giving the Respondents more time to defend a claim that evidently cannot be defended because of the circumstances which led to my daughter being dismissed. Whilst i am not legally qualified as to adjudge it would a appear that (a) she has been denied the right to a fair hearing because her opponents have abused orders which if followed would have allowed the trial to proceed and ( b) the Tribunal could have not only made the request for that evidence to be disclosed, in postponing the trial next week, giving those facts and the excuse of needing a panel, which would have been knowledge as soon as pleadings were made, i feel this is unequal and unfair as the Tribunal are not only allowing orders to be breached, they are also giving the Respondents more time to further breach the orders. My daughter i feel has a very strong case and my theory is that because of the strength of her case, the opponents and the tribunal are doing everything in their power to keep this matter out of court. It is hard enough and most times financially impossible for pregnant woman to establish unfair dismissal claims because they are pregnant, the Tribunal who should protect, if my experiences are anything to go on make it even more difficult by allowing employers the right to ignore orders and as in this case give further encouragement for this to happen again by postponing without reason or justification. Any help would be greatly appreciated by this angry dad:mad2:

Hi, I am currently representing my daughter on the McKenzie friend basis in her claim for unfair dismissal on the grounds of discrimination ( pregancy ) We have followed all the procedures through ACAS and we are currently taking her employer through the Employment Tribunal, which has taking about seven months to get to a Trial which has been listed for next week 4/5th February 2016, this was after a previous hearing. Today i receive a letter from the Tribunal stating that the trial might be postponed on the grounds that despite knowing for a number of months that in any event, the trial would be considered by a panel rather than a single judge because it is a discrimination case, to use this as a reason, and so late in the day does not add up, they would have known months in advance that a panel would need to be assigned, so in using this has delayed even further. The Tribunal are also aware that the Respondents are in abuse of process as they have failed to abide the previous order for them to provide a trial bundle, witness statements and further and better particulars in readiness for the trial next week? Because of this we made an application for the Tribunal to make an unless order for this evidence to be giving as all of it is central to the claim and it had been previously ordered. We have also written to the other side and in anticipating the Tribunal not making the unless order, which seems very reasonable, by stating that we would provide our own trial bundle and giving them seven days to object. Since all of this has happened in the last couple of days, the Tribunal as it would appear are bending over backwards in allowing the previous orders be breached and ignored and they have also giving the Respondents more time to defend a claim that evidently cannot be defended because of the circumstances which led to my daughter being dismissed. Whilst i am not legally qualified as to adjudge it would a appear that (a) she has been denied the right to a fair hearing because her opponents have abused orders which if followed would have allowed the trial to proceed and ( b) the Tribunal could have not only made the request for that evidence to be disclosed, in postponing the trial next week, giving those facts and the excuse of needing a panel, which would have been knowledge as soon as pleadings were made, i feel this is unequal and unfair as the Tribunal are not only allowing orders to be breached, they are also giving the Respondents more time to further breach the orders. My daughter i feel has a very strong case and my theory is that because of the strength of her case, the opponents and the tribunal are doing everything in their power to keep this matter out of court. It is hard enough and most times financially impossible for pregnant woman to establish unfair dismissal claims because they are pregnant, the Tribunal who should protect, if my experiences are anything to go on make it even more difficult by allowing employers the right to ignore orders and as in this case give further encouragement for this to happen again by postponing without reason or justification. Any help would be greatly appreciated by this angry dad:mad2: -

I moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out. I don't live in Scotland anymore. Is it possible to submit a summary application by post or electronically? moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out can someone please suggest a solicitor that can submit the summary application on my behalf and elp handle the process?

I moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out. I don't live in Scotland anymore. Is it possible to submit a summary application by post or electronically? moved out of a rented property in Aberdeen on the 15th of September 2016. It was a short assured tenancy for 6 months My landlord did not secure my deposit of £650 in any deposit scheme and only returned part of it (£500). I would like to submit a summary application for the remainder of the deposit and compensation but have only 6 more days to do this as it will soon be 3 months since I moved out can someone please suggest a solicitor that can submit the summary application on my behalf and elp handle the process? -

First I've heard of this, I haven't received anything else regarding this matter, isn't this something that I have to attend court for? if so why wasn't nothing stated nor issued to me? I have to pay £1005.82+£110 fee within 8 days to a company I don't even know about? or even know what money they are trying to get from me? Over the past few years I've been working hard to pay back things i genuinely do owe, and for this to pop up is just annoying.. I work a part time 30 hour a week job, any ideas? Obviously if the debt is true I'll pay, but from how long ago could it go back to?

First I've heard of this, I haven't received anything else regarding this matter, isn't this something that I have to attend court for? if so why wasn't nothing stated nor issued to me? I have to pay £1005.82+£110 fee within 8 days to a company I don't even know about? or even know what money they are trying to get from me? Over the past few years I've been working hard to pay back things i genuinely do owe, and for this to pop up is just annoying.. I work a part time 30 hour a week job, any ideas? Obviously if the debt is true I'll pay, but from how long ago could it go back to?

-

After one applies for jobseekers allowance, they are invited to their first appointment to sign their application. If there are topics that need to be expanded, or for example special circumstances that cannot be answered with a simple yes/no, can one attach a written statement to be sent to the decision makers? Thanks

-

I have received a letter this morning at my rented address for a notice of application for attachment of earnings order from Cabot Financial (UK) Ltd. I migrated to Australia in 2011 but had to return in Aug 2015 due to visa refusal but although this letter has a case number and application number as well as a judgement creditors reference I actually have no idea what this debt is supposed to be for as this is the first correspondence I have received at this address and I have been here since August 2015. It says unless I pay the judgement creditor within 8 days I must complete the enclosed form of reply including the statement of means and send it to the court office within 8 days after receiving this notice. I'm not sure what this debt is for which is my main concern as there is no reference to it nor what date this judgment was carried out. It says the address for payment is Restons Solicitors Limited Warrington and that's about as much as I know

I have received a letter this morning at my rented address for a notice of application for attachment of earnings order from Cabot Financial (UK) Ltd. I migrated to Australia in 2011 but had to return in Aug 2015 due to visa refusal but although this letter has a case number and application number as well as a judgement creditors reference I actually have no idea what this debt is supposed to be for as this is the first correspondence I have received at this address and I have been here since August 2015. It says unless I pay the judgement creditor within 8 days I must complete the enclosed form of reply including the statement of means and send it to the court office within 8 days after receiving this notice. I'm not sure what this debt is for which is my main concern as there is no reference to it nor what date this judgment was carried out. It says the address for payment is Restons Solicitors Limited Warrington and that's about as much as I know -

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance

Hi, someone can help ! Over the weekend I put in an offer to rent a property, and was given a date as to when i could move in providing referencing went through ok etc etc. The problem now is that my boss, who is my referrer, is now on holiday and wont be able to sign anything until he is back. I need to move out and into a new place before he is back. Perhaps naively, I actually thought that they would simply call or email him and ask to confirm any details that I put down, he is contactable this way, but wont be able to print and sign anything off before he gets back. Which leaves me in a bit of a pickle. I can move my stuff out and and move somewhere else, but once ive moved somewhere else I wont be able to (or want to for that matter) move my belongings again. The lettings company charged me £400 pretty much immediately, and i am wondering if i am within my right to ask for a refund. I didnt sign anything when i sent over the £400. No checks have been made as yet, i found this all out just now as ive received the landlord hub referencing form. thanks in advance -

I failed the PIP medical (by a mere few points). I'd gone through the Mandatory Reconsideration and had posted the paperwork to lodge an appeal before the imposed deadline. On chasing this up, I found that the appeal paperwork had not been received by the tribunal. Thankfully, I had help from a welfare rights worker at my local housing association, who contacted the tribunal and managed to fax them a copy of said paperwork. It's really lucky that I chased this up. They will now process my application and get back to me with a date (hopefully not too far into the future). Please, please, please keep on top of your paperwork. I'm sure it's very rare for important letters to disappear in the post, but it does happen. If you have someone to help you, ask them to confirm that everything is proceeding as expected. If I hadn't asked my welfare rights worker if they'd received any news, I'd be none the wiser and my appeal would be going nowhere.

- 4 replies

-

- 1

-

-

- apparently

- appeal

- (and 2 more)

-

I'm looking for some advice please . I recently applied for a mortgage, and was asked initially over the phone "have you ever had any CCJS or IVAS". The answer was and is no. I was given an agreement in principle. This has now progressed to full application stage , after passing a full credit check. I have received a check list to sign and return to the lender. One of the first questions asks "Have you ever been subject to county court judgements (CCJs) , defaults or a repossession"? Is this asking if I have had a CCJ, county court default judgement or county court repossession order?, or is it asking if I have ever had credit defaults? The answer to that is yes, all unsecured, all now off my file and statute barred. After an initial panic I believe it is all County Court order related but I would like your opinions please.