Search the Community

Showing results for tags 'insurance'.

-

hi folks, in a bit of a predicament regarding an accident back in July 2016. I am insured through Allianz through safeguard for my motorhome insurance, back in July i had a buyer for it, so decided to use it one last time before parting with it. on my way home, passed through a town not far from my home address, is a narrow street, with cars parked down one side, in designated parking bays, but these take up half of the road lane, meaning anyone passing will have to straddle the other lane of the road, the wrong side, the other lane has double yellows, so no parking. This was the lane i was travelling along, when approaching near the end of line of parked cars, this driver decided not to wait or give way to avoid an accident, the road is clear to see if anything is coming, and parts where you can pull into to allow the oncoming traffic to carry on their journey. My motorhome at its widest point is just under 9ft wide, taking up its presence on the road, the main street is that narrow at points, it is not safe to pass, as their is just not enough room, when i realised this driver was not going to stop, i slammed on my brakes, almost at a standstill when he hit my mirror, smashed it, dented the door, and scrapped along the coach body of the motorhome. i pulled into the space right across the road from me, where he should have pulled into, he admitted he should have gave away, then saying he was as far over as he could go, meaning if one of the parked cars opened their door, he would have taken that off, as well as hitting me, exchanged details, to find out later he is disputing the claim saying it was my fault, when he was on my side of the road, nowhere for me to go to avoid him, other than mounting a pavement or driving into a building, one of the local businesses seen what happened and gave me his contact details for a witness. My problem now is, the insurance company say they have not received anything from him and him saying he has sent them it twice, and without this statement i would have to accept responsibility or go 50/50, i have even given them a dash cam vid of the road and where the accident happened, not a clip of the actual accident, but more to show the condition of the road, and space with passing cars in both directions, they are now saying that they can check this on google, and because the clip is not of the actual accident, it would not count. Now google cant show the road conditions, of passing cars, and the clip was done to prove this fact, seems to be a known area for this happening, informed them the repairs would not be done until it had being resolved. Recently got a call from the bodyshop saying the insurance company has now authorised the claim, and booked it in, i presumed it had now being resolved and the 3rd party had accepted responsibility, no letter, call or email from my insurance to tell me this, when it has not being resolved and i would have to pay the 300 excess, depending on how the 3rd party goes, it would be claimed back from their insurance. I feel now they have taken the upper hand and forced me into a position, where i have told them i will not accept any responsibility for the accident, and prepared to take it to court, where i was informed it would not go to court as the claim was under 1k and my only option is to accept a 50/50. I have also had a lot of out of pocket expense, as the motorhome is now not worth what i had a buyer for it last year, and as they have not got the witness statement, then i have no case to answer and will have to accept 50/50. I rang the motor legal protection i had on my policy, found out this is a complete waste of money as they offered no help at all, and said it would be better to just accept 50/50. i have being up a few times to see the witness, even leaving him a copy of the witness statement for him to sign, has asked me to come back for it next week, but if i have problems getting this off him where do i stand, what can i do, as it will also affect my future insurance, and for an accident where i was at no fault at all and thoughts on this would be greatly appreciated

-

Hi, I was living in France and had a French Mortgage for 200,000 Euros in 2009. Unfortunately I lost my job and I had to return to the UK, I paid what I could to the Bank over the next few years, but one day in 2012 the Bank informed me that the outstanding Mortgage was paid off by an insurance policy. I rented the house out to tenants after making enquiries and paying a Notaire to see if the house was actually mine, I was assured it was and assumed that I had taken a policy out at the time of purchase. Last year I agreed to sell the house to my tenant, it was then discovered that the insurance company Credit Logement had put a charge on the house in 2012 for the outstanding amount of the mortgage they paid off plus interest. I have been living in the UAE since 2010, and my tenant in my house in France since 2011. Neither of us had received any notification of any actions or judgements against me. I was totally unaware of any legal proceedings whatsoever as the papers were served to an address in the UK, I hadn't lived in since 2010. We are in a stalemate situation at the moment with the Insurance Company threatening to re-possess the house since May 2016 but have they have not made any moves to do so. The Paris High Court served a Judgement against me in March 2012 with the insurance Company putting a charge on the Property's Title in August 2012. Does anyone know if these outstanding debts have a Statute of Limitations? Any advice would be gratefully appreciated. Badhorsey

Hi, I was living in France and had a French Mortgage for 200,000 Euros in 2009. Unfortunately I lost my job and I had to return to the UK, I paid what I could to the Bank over the next few years, but one day in 2012 the Bank informed me that the outstanding Mortgage was paid off by an insurance policy. I rented the house out to tenants after making enquiries and paying a Notaire to see if the house was actually mine, I was assured it was and assumed that I had taken a policy out at the time of purchase. Last year I agreed to sell the house to my tenant, it was then discovered that the insurance company Credit Logement had put a charge on the house in 2012 for the outstanding amount of the mortgage they paid off plus interest. I have been living in the UAE since 2010, and my tenant in my house in France since 2011. Neither of us had received any notification of any actions or judgements against me. I was totally unaware of any legal proceedings whatsoever as the papers were served to an address in the UK, I hadn't lived in since 2010. We are in a stalemate situation at the moment with the Insurance Company threatening to re-possess the house since May 2016 but have they have not made any moves to do so. The Paris High Court served a Judgement against me in March 2012 with the insurance Company putting a charge on the Property's Title in August 2012. Does anyone know if these outstanding debts have a Statute of Limitations? Any advice would be gratefully appreciated. Badhorsey -

Why does my insurance company who gave me a quote, not allow me to pay monthly because I was truthful and said I had a CCJ,they didn't even do a credit search. My sister who is financially connected to me, got insurance from the same company, and got monthly payments. Surely if I didn't pay they could just cancel the insurance? Very frustrating

-

Hello everyone, I took out a vehicle insurance online via one of the van insurance comparison sites beginning of this month and paid the deposit of around £250 upfront with the first instalment of £130 coming out shortly after on the 10th of Feb. Now, I just got home and had a letter (dated 20/02) from the insurance company, or rather the broker as it turns out, telling me that the insurer (they don't mention the name of the insurance company) advised them that my policy must be cancelled within the next 7 days. "This is because of where your vehicle is kept overnight". The vehicle is kept on the road overnight, as I indicated on the comparison site, which based on all the information I have given listed the different insurers and their premiums, from which I had chosen this one. The letter goes on to say that I urgently have to contact them so that they can place me with an alternative insurer. Now I have a few questions: 1. First of all, I think this smells very fishy and I have doubts that this is legal? 2. I provided all the information beforehand, based on which I was given a premium. If this would have been an issue they should have not let me take out the insurance in the first place? 3. The vehicle is kept on the road overnight. I did not lie. It's not like I said it's kept in a garage when in actual fact it isn't. I mean everyone keeps their vehicle on the road, or at least the majority of the population? This would mean they would only have a handful of customers? Again, another reason why I think it doesn't make any sense? 4. Do I have 7 days from date of receipt of this letter, ie from today until the policy would be cancelled? 5. If I don't agree with this and they cancel me completely or I want to leave them as this is not a very honest start with them, can I get my money back? I haven't even been with them for a month. My installment from the 10th should at least take me up to the 10th of March, not to mention my £250 deposit I paid at the outset? 6. The premium is set up to be paid monthly through a financing deal, which I signed. Am I now required to pay the full premium every month to the Finance guys, even if the brokers or I end up cancelling altogether? I would really appreciate if someone could explain the legalities of this all to me before I give them a call as I don't want to end up playing my cards wrong. Should I get legal help/advice to get my money back? Get in touch with watchdog? I am a bit at a loss with this as you can probably tell so any information would be greatly appreciated. Thanks a lot in advance!

Hello everyone, I took out a vehicle insurance online via one of the van insurance comparison sites beginning of this month and paid the deposit of around £250 upfront with the first instalment of £130 coming out shortly after on the 10th of Feb. Now, I just got home and had a letter (dated 20/02) from the insurance company, or rather the broker as it turns out, telling me that the insurer (they don't mention the name of the insurance company) advised them that my policy must be cancelled within the next 7 days. "This is because of where your vehicle is kept overnight". The vehicle is kept on the road overnight, as I indicated on the comparison site, which based on all the information I have given listed the different insurers and their premiums, from which I had chosen this one. The letter goes on to say that I urgently have to contact them so that they can place me with an alternative insurer. Now I have a few questions: 1. First of all, I think this smells very fishy and I have doubts that this is legal? 2. I provided all the information beforehand, based on which I was given a premium. If this would have been an issue they should have not let me take out the insurance in the first place? 3. The vehicle is kept on the road overnight. I did not lie. It's not like I said it's kept in a garage when in actual fact it isn't. I mean everyone keeps their vehicle on the road, or at least the majority of the population? This would mean they would only have a handful of customers? Again, another reason why I think it doesn't make any sense? 4. Do I have 7 days from date of receipt of this letter, ie from today until the policy would be cancelled? 5. If I don't agree with this and they cancel me completely or I want to leave them as this is not a very honest start with them, can I get my money back? I haven't even been with them for a month. My installment from the 10th should at least take me up to the 10th of March, not to mention my £250 deposit I paid at the outset? 6. The premium is set up to be paid monthly through a financing deal, which I signed. Am I now required to pay the full premium every month to the Finance guys, even if the brokers or I end up cancelling altogether? I would really appreciate if someone could explain the legalities of this all to me before I give them a call as I don't want to end up playing my cards wrong. Should I get legal help/advice to get my money back? Get in touch with watchdog? I am a bit at a loss with this as you can probably tell so any information would be greatly appreciated. Thanks a lot in advance! -

Hi all, I cancelled my vehicle insurance over the phone and was told that there was nothing more to pay, which surprised me as I thought there would be a cancellation fee, even though it was only 6 weeks until the policy ended. I then received a letter in PDF format via e-mail stating that I had cancelled my policy with a breakdown of how much I'd paid etc and then it stated that there was a NIL BALANCE. It was signed. I then received another letter in the same format telling me I had to pay a cancellation fee of over £150! I phoned them and they said that this was an error. 2 months later I received a letter from a "Solicitors" (DCA) saying that I owed this amount plus fees. I phoned them and explained, and then e-mailed them with the attached PDF stating I owed nothing. They then replied saying that because the letter stated at the bottom "this is subject to change" then the debt is enforceable but they would speak to the OC and get back to me. They have got back to me saying that the original letter was an error and that I do owe the amount stated. Here is a copy of my e-mails to them and the ones they have sent back. "Dear Ms XXXX * Further to your recent email, we have been in contact with the client and this is the response we have received:* * 'The letter attached to your original email was incorrect, this letter was followed by the attached letter advising of the outstanding balance'* * Please see attached document.* * You have an outstanding balance, therefore please contact us on 01707 XXXX to discuss payment methods, quoting your reference number:*XXXX Kind Regards, * Insurance Collections Bureau. " My reply to them. "Dear sirs, * I have spoken to my solicitor about this and showed him the attached. * He has advised me that, although the original creditor states it is an error, one cannot just send out a letter stating that there is no debt, and then simply decide that there is. The letter is signed and dated. * I therefore consider the matter closed and any further correspondence from you will incur a*charge of £12.50*for my time. However if you would like to discuss this further with my solicitor, Mr. Andrew XXXXXXXX, would you be happy to contact him directly in writing? * Regards, " Their reply: "Thank you for your recent email. With regards to this, I advise you or your solicitor to contact the client directly as we have advised you of their response, we will continue with our process until advised otherwise by the client.* Additionally, we do not have a contract with you, therefore you cannot charge us anything. Kind Regards," My question is, shall I ignore them for now? Or just send them an invoice straight away? I don't believe I owe them anything at all. Also I am considering sending them a section 40 notice (administration of justice act) but I will of course be sending that by recorded post.

-

Hi all just wondering about the doorstep collectors using their own cars and if standard insurance will be enough or will they need something like hire/reward policy. sorry if this has been asked before.

-

Hi there I have a question relating to a loan that I took in 2004 through Zenith Windows to install double glazing. But Zenith windows went into administration in 2010 I believe. Loan amount 5K. It is now paid off. How do I go about getting the PPI back from them and the unfair charges. Can anyone help please? Many thanks and much appreciated.

-

http://news.sky.com/story/car-insurance-costs-rising-five-times-faster-than-train-fares-10740471

-

I know many people here is not legal adviser, But The advice as I could get from this website always was more useful instead any lawyers or citizen advice bureau. Thank You My car Insurance payments: I insured my Second car since February 2016 for Premium: £1124.00 Sub Total before credit charge: £1124.00 Motor Premium Tax: £106.78 Total cash price: £1230.78 Total charge for credit: £111.28 Total amount payable for policy term: £1,342.06 In less of 20 days a Car accident happened Tried to get some advice from a legal firm about this case: I gave my case to a legal firm To advice me what they can do for me. But the company made a claim without any discussion, permission or confirmation. The third party gave a cheque for my car value to that unauthorised solicitor, But I never received the cheque, Because the firm tried to force me to sign a Client care pack. amended the contract and increased I did not provide my No claim bonus discount to them; ten days after the car accident they have amended the contract and increased my policy payment to 2367.94 I did not accept and send a complaint letter to them, They cancelled my policy and asked me to make a full payment as well. However, I paid them in full; They send a default notes to my credit report. The third party made claims against me to My insurance. My insurance informed me, they would like to settle the matter in 50/50, without accepting liability, if not, they would accept it in full. ( All communicate or conversation was by the emails and letters.) County Court Claim Letter After few months, from the Country Court, I received claims against myself letter under my name, to my address. I passed the letter to my Insurance by Email, And asked them if I need to respond to this letter!?; they told me, no, you don't need to do anything and when they settle the matters they will notifying me. CCJ On Credit Report Under my membership account with the credit expert and the Equifax, I informed about CCJ on my report but five days after the judgment date. My insurance forgot to respond to the court. They were apologising me. And told me they would remove the CCJ as soon as possible, because they did not update me on what's going on, and I could not trusting them anymore or take any risk, a day before the end of 28 days, I paid myself to the third party £3 039. I need help Because I was in a very hard situation during the last nine months. There are too many mistakes in my case from the beginning by my claim case worker. As she gave some comment without looking at the vehicle photo, and when I told her you could ask for the CCTV's Bus, she said, The third party representatives looked into this aspect of the claim and were advised that no footage was available. They did not tell me that I have to transfer my insurance to the other car. When I called them many times to talk with someone to explain to me, how they calculated the outstanding balance, if I need pay the full payment, need I pay the credit interest as well or APR? They did not tell me. They must have full responsibility for my accident and any matters as they promised me when we make a contract. I know under the credit agreement they should make a cleared about my policy or my credit agreement or any amended section in my contractor me as a customer. Many hours my time be wasted because They asked me to paid them in full. They did not respond to me when I asked them to make a clear the amount as they are asking me to pay, they wasted my time on the phone line in some hours, without providing me without any useful information. I paid them and asked them to remove the default from my credit report; I asked them by the phone and email, they did not accept and send a copy of the credit agreement act and told me you have breached our contract. The default on my credit report have not any good or any bad effect to that company, but the default have many effects on my daily life, Thus I don't want to accept any apologising from them, I Have some Question: I have got this insurance from 18 of February 2016 the accident happens on 11 of March they changed the policy on 24 of March Have I any right to not agree with the new agreement ( Agreement on 24 of March )or monthly payment plan? How should I receive the default notice when I had an accident, and I was not in any good situation? Because I paid and settled the country court claim against myself, They Own my money, is any way that they get the country court on their business credit report? This paragraph was in my insurance letter to me, What're means? I understand that you have satisfied the judgment of £3,093.53. You have the benefit of comprehensive insurance, for which you have paid the insurance premium. So, you should not be out of pocket any further. The accident was not my fault, Can I appeal to the court and defended myself? From the beginning, it is very clear as they don't want act for me. If they do act for me, what was the point for them? If I did not pay to them, by the law, have they any responsibility to acting behalf me or no? if the accident bee 50/50 what was the effect on my future insurance? which payment could I receive? and now I am 100% fault , what is the effect on my future insurance? which payment could I receive? Please Note: I have 11 years old no claim bonus discount as I used on my other car, I never have any accident before, and I have protected my no claim bonus for 2016-2017 not before.

I know many people here is not legal adviser, But The advice as I could get from this website always was more useful instead any lawyers or citizen advice bureau. Thank You My car Insurance payments: I insured my Second car since February 2016 for Premium: £1124.00 Sub Total before credit charge: £1124.00 Motor Premium Tax: £106.78 Total cash price: £1230.78 Total charge for credit: £111.28 Total amount payable for policy term: £1,342.06 In less of 20 days a Car accident happened Tried to get some advice from a legal firm about this case: I gave my case to a legal firm To advice me what they can do for me. But the company made a claim without any discussion, permission or confirmation. The third party gave a cheque for my car value to that unauthorised solicitor, But I never received the cheque, Because the firm tried to force me to sign a Client care pack. amended the contract and increased I did not provide my No claim bonus discount to them; ten days after the car accident they have amended the contract and increased my policy payment to 2367.94 I did not accept and send a complaint letter to them, They cancelled my policy and asked me to make a full payment as well. However, I paid them in full; They send a default notes to my credit report. The third party made claims against me to My insurance. My insurance informed me, they would like to settle the matter in 50/50, without accepting liability, if not, they would accept it in full. ( All communicate or conversation was by the emails and letters.) County Court Claim Letter After few months, from the Country Court, I received claims against myself letter under my name, to my address. I passed the letter to my Insurance by Email, And asked them if I need to respond to this letter!?; they told me, no, you don't need to do anything and when they settle the matters they will notifying me. CCJ On Credit Report Under my membership account with the credit expert and the Equifax, I informed about CCJ on my report but five days after the judgment date. My insurance forgot to respond to the court. They were apologising me. And told me they would remove the CCJ as soon as possible, because they did not update me on what's going on, and I could not trusting them anymore or take any risk, a day before the end of 28 days, I paid myself to the third party £3 039. I need help Because I was in a very hard situation during the last nine months. There are too many mistakes in my case from the beginning by my claim case worker. As she gave some comment without looking at the vehicle photo, and when I told her you could ask for the CCTV's Bus, she said, The third party representatives looked into this aspect of the claim and were advised that no footage was available. They did not tell me that I have to transfer my insurance to the other car. When I called them many times to talk with someone to explain to me, how they calculated the outstanding balance, if I need pay the full payment, need I pay the credit interest as well or APR? They did not tell me. They must have full responsibility for my accident and any matters as they promised me when we make a contract. I know under the credit agreement they should make a cleared about my policy or my credit agreement or any amended section in my contractor me as a customer. Many hours my time be wasted because They asked me to paid them in full. They did not respond to me when I asked them to make a clear the amount as they are asking me to pay, they wasted my time on the phone line in some hours, without providing me without any useful information. I paid them and asked them to remove the default from my credit report; I asked them by the phone and email, they did not accept and send a copy of the credit agreement act and told me you have breached our contract. The default on my credit report have not any good or any bad effect to that company, but the default have many effects on my daily life, Thus I don't want to accept any apologising from them, I Have some Question: I have got this insurance from 18 of February 2016 the accident happens on 11 of March they changed the policy on 24 of March Have I any right to not agree with the new agreement ( Agreement on 24 of March )or monthly payment plan? How should I receive the default notice when I had an accident, and I was not in any good situation? Because I paid and settled the country court claim against myself, They Own my money, is any way that they get the country court on their business credit report? This paragraph was in my insurance letter to me, What're means? I understand that you have satisfied the judgment of £3,093.53. You have the benefit of comprehensive insurance, for which you have paid the insurance premium. So, you should not be out of pocket any further. The accident was not my fault, Can I appeal to the court and defended myself? From the beginning, it is very clear as they don't want act for me. If they do act for me, what was the point for them? If I did not pay to them, by the law, have they any responsibility to acting behalf me or no? if the accident bee 50/50 what was the effect on my future insurance? which payment could I receive? and now I am 100% fault , what is the effect on my future insurance? which payment could I receive? Please Note: I have 11 years old no claim bonus discount as I used on my other car, I never have any accident before, and I have protected my no claim bonus for 2016-2017 not before. -

Have you had render by the The Wall Coating Company (TWCC). Did you get a 20 year insurance policy for the work? Your insurance policy may be worthless. I contracted with the The Wall Coating Company who (6 months and many many problems later) completed the work and sent a Guarantee certificate and an Insurance Policy Document. My insurance policy policy stated that contractor was WCC Systems Ltd. The contract, work and payments are all to The Wall Coating Company, so who is WCC Systems Ltd? I have been told that The Wall Coating Company is a trading name of WCC Systems Ltd and they, but neither I, the broker and the Insurance company have any paperwork that shows that. The address and phone numbers for the Wall Coating Company are totally different to WCC Systems Ltd. I queried this with the Policy Broker and they confirmed that, because of the different names on the different paperwork, the Insurance Policy is (or could potentially be) invalid. After some discussion, the broker will be sorting out he situation by amending the policy document to reflect that The Wall Coating Company is the trading name of WCC Systems Ltd. So. Have you had render done by The Wall Coating Company (TWCC)? Take a close look at the part of the Insurance Policy Document which states who the Contractor is. If it says WCC Systems LTD and your guarantee certificate is by The Wall Coating Company, it may be invalid. If anyone is thinking of contracting with The Wall Coating Company, be prepared for poor quality render (wonky, corners uneven, not level, not straight etc.) with the render dropped over your brand new windows and your paving slabs. Then be prepared for 6 months of trying to get the render to be put right. Eventually you may get hold of the Director Michael Richard ACKROYD who will deny any problems, accuse you of nit-picking and nagging and then threaten to send a team to remove the render from your walls.

Have you had render by the The Wall Coating Company (TWCC). Did you get a 20 year insurance policy for the work? Your insurance policy may be worthless. I contracted with the The Wall Coating Company who (6 months and many many problems later) completed the work and sent a Guarantee certificate and an Insurance Policy Document. My insurance policy policy stated that contractor was WCC Systems Ltd. The contract, work and payments are all to The Wall Coating Company, so who is WCC Systems Ltd? I have been told that The Wall Coating Company is a trading name of WCC Systems Ltd and they, but neither I, the broker and the Insurance company have any paperwork that shows that. The address and phone numbers for the Wall Coating Company are totally different to WCC Systems Ltd. I queried this with the Policy Broker and they confirmed that, because of the different names on the different paperwork, the Insurance Policy is (or could potentially be) invalid. After some discussion, the broker will be sorting out he situation by amending the policy document to reflect that The Wall Coating Company is the trading name of WCC Systems Ltd. So. Have you had render done by The Wall Coating Company (TWCC)? Take a close look at the part of the Insurance Policy Document which states who the Contractor is. If it says WCC Systems LTD and your guarantee certificate is by The Wall Coating Company, it may be invalid. If anyone is thinking of contracting with The Wall Coating Company, be prepared for poor quality render (wonky, corners uneven, not level, not straight etc.) with the render dropped over your brand new windows and your paving slabs. Then be prepared for 6 months of trying to get the render to be put right. Eventually you may get hold of the Director Michael Richard ACKROYD who will deny any problems, accuse you of nit-picking and nagging and then threaten to send a team to remove the render from your walls. -

In November someone drove into me and my car was written off. At the scene they admitted responsibility and I got the contact details of a witness who verified this. Following the crash the 3rd party decided to contest their liability which delayed my payout and meant that the case remained open, meaning that in the eyes of any prospective insurers I may possibly have been the guilty party... This meant that I couldn't afford to insure the car I'd been offered the use of over Xmas (thank you Ella Mullin x) so I had no wheels during the holiday period. All of this was bad enough but now... they've finally accepted liability, paid me out and I've got my ncd back again yet... I'm still being quoted twice as much for my insurance. I'm furious! I'm the injured party but my premiums have doubled - is this legal?

-

For many years I've religiously renewed my breakdown coverage because it's very cheap - £15. During that period I think I've used them only once before, but recently I punctured five miles from home. Ordinarily I would put the spare on myself but, Sod's Law, only that morning had lent someone my repair kit and didn't have it back yet. Rather than walk home, I decided to use breakdown. When I rang, they told me they couldn't find my details and said I hadn't renewed, but I was adamant that I had. They agreed to send someone in good faith providing my details could be clarified (I was also given the impression that if there had been a problem with the renewal, it could be rectified). As it was, it took them four hours to get to me (had I known it would be that long, I'd have walked home!). This prompted them to, the following day, ring me and offer £50 compensation. Now I've received a threatening letter saying I didn't renew and they want paying for everything. I'm assuming they mean the £50 and the cost of the (third party) breakdown guy. They haven't put a figure on this but I dread to think what it is. Having now checked, I found that I haven't a renewal policy. Further investigation shows that I sent them a cheque (which I have proof off) but, again Sod's Law kicking in, the £15 cheque that was subsequently cashed on my bank statement, and that I therefore assumed was for the renewal, was actually a late cheque that I'd written three months earlier, cashed late. So what now? I know that I sent them the cheque, so feel like I'm being punished because they lost the cheque. I know that I won't be able to afford whatever figure they come out with, and most certainly wouldn't have willy nilly rang for a breakdown guy to come out had I not thought I had coverage. Thanks in advance.

-

Good morning, My 18 yr old daughter took out a policy with 'MyPolicy' car insurance 8 months ago when she passed her test. They seemed the best price at the time but have cost dearly over the 8months, mainly in charges for extra miles. a few weeks ago she was involved in an accident which wasn't her fault, the other driver admitted blame immediately. The claim has been settled and they have sent the cheque. Now, the problem is the charges they want to slap on her. Her car was a write off so she is going to buy her brother's car. They want to charge her £150 for a new black box and £100 to change the details on the policy to the new car. This sounds totally unreasonable to me and is a loss on her part seeing as the accident wasn't her fault. Baring in mind the black box only cost £50 to fit when she first took out the policy. She's young and inexperienced and doesn't know what to say on the phone. Last time I tried, they wouldn't speak to me, but surely if she gives her permission that should be fine? I need to fight her corner for her as I can be stronger on the phone. I need some advice as this charging can't be right. It's a total rip off to me. Any advice would be greatly appreciated.

Good morning, My 18 yr old daughter took out a policy with 'MyPolicy' car insurance 8 months ago when she passed her test. They seemed the best price at the time but have cost dearly over the 8months, mainly in charges for extra miles. a few weeks ago she was involved in an accident which wasn't her fault, the other driver admitted blame immediately. The claim has been settled and they have sent the cheque. Now, the problem is the charges they want to slap on her. Her car was a write off so she is going to buy her brother's car. They want to charge her £150 for a new black box and £100 to change the details on the policy to the new car. This sounds totally unreasonable to me and is a loss on her part seeing as the accident wasn't her fault. Baring in mind the black box only cost £50 to fit when she first took out the policy. She's young and inexperienced and doesn't know what to say on the phone. Last time I tried, they wouldn't speak to me, but surely if she gives her permission that should be fine? I need to fight her corner for her as I can be stronger on the phone. I need some advice as this charging can't be right. It's a total rip off to me. Any advice would be greatly appreciated. -

Hello All! Wondering if anyone can give me some advice please. I live in a flat where I am using it for an online business however it's presently dormant and has been since the start. There are no goods involved, it's just a free website. I had to register this under my home address however I am wondering if this would have an effect on the communal buildings insurance policy I have? (residential) Would it void it? Please can someone who know this get back to me.. Regards

-

Hello Friends, Are Insurance companies allowed to sell policies to people who are not eligible? I had bought MMS homeowner policy in Dec-15 and when I went to claim today, they refused saying that I was not holding mortgage in Dec-15. I had a mortgage in Feb-16. i had taken this income protection policy in Dec-15 in advance so as to protect me from commitments of mortgage. How was I wrong in that? I don't remember what questions the seller (ActiveQuotes) asked me when selling this policy with regards to my eligibility. Its possible that because I was going to have a mortgage soon, just waiting for exchange to happen, I would have said that I have a mortgage. However, that is speculative. If it was so mandatory should they not have asked documents to prove my current mortgage. They did not give me insurance initially in Sept-15 as I was still in probation and had not covered six months with my current employment. So should they not have checked for my mortgage as well. And given that I anyway soon became mortgage owner, do I not come under the cover. Excerpt from the Policy: You are eligible to take out this cover if you are: Living in the UK. Named as a person responsible for a mortgage or named as owner of your primary residence. Does this clause mean that I could not have bought the policy? Any ideas on this, please. Can the insurance companies sell such important policies without checks and only to leave the person stranded when he needs it?

-

Hi everyone, I'm new here I was involved in a lorry crash in early October and the lorry driver admitted full liability, so this is not in dispute. The original arrangement to sort out the mess to my car (he squashed the side of it) was to deal with it all privately through his own company. I was given details of who I should contact to arrange this. I thought this was a good idea becuase I thought if I went through my own insurance to sort it out with their insurance company, I would probably end up with a premium hike. I was keen to avoid that, so I just reported the accident instead and decided to do it all privately. I was contacted shortly after the accident by a claims management company who asked to do their own assessment on my car to ascertain the extent of damage. I had already done one of my own, got a quote for the damage. The quote itself cost £30. I told the claims management company that I needed my own garage to do the work because I was on a PCP Agreement and the terms stipulated that my own garage should do any repairs, preferably, to ensure original parts were used for replacements. I had to agree to the claims management company to do their own too. I was quite cross to see the Agent looking over my car in the forecourt of my house without having first knocked on my door. I noticed him out of the window. After he came and went, I had first told him about the Quote I already had paid for from my own garage - making it clear to him that those repairs would need to be done, not any revised work they might consider necessary instead. He said he would contact my garage for a copy of that. A few weeks later I got a call from another guy from the same claims management company who virtually accused me of having diddled the quote, asking for more work than was necessary - a complete re-spray - which was not necessary. I told him in no uncertain terms that the garage I got the quote from was bona fide and had a duty of care not to over-stipulate the work required by law when I checked it later, after the call, a re-spray wasn't even listed on it. I rang him again and told him that what was on that quote was the work I needed doing and they THEY would be paying for it. That was all there was to it, as far as I was concerned. He then told me that when he had contacted my garage for the quote, my garage had since refused to do this work for me - even though they had not told me personally about that decision. I rang them myself and they told me that they had said nothing of the kind but they did need a work repairs number to authorise payment from this claims management company or they could not begin work without it. I rang back the claim management guy what the outcome was at the claims management company and he agreed to go ahead with it all. I then put all this in writing this time, asking him specifically to reassure me that they would provide a works repair number to my garage to do the repairs, as per the quote they had originally given me. I also said in my email that the work may not be in full and final settlement if they discovered more needed to be done down the line and to confirm that they understood this. I did not get this, just a go ahead to book the garage. Since then I have done nothing at all to get the car repaired. I have been borrowing cars in my job lent to me by other clients, so my car has not been used much. However, I have been thinking about all of this and feel distinctly uneasy about going through this claims management company who are billing the company direct and leaving their own insurance company out of it. I feel now, given the messing about, the implied accusations, that the claims management company and my garage could easily cook up a deal behind my back to do less than was on the quote - so that the company pays less, but I don't get a comparable car back to what it was like before the crash. I now feel I want to chuck in all these behind the scenes arrangements, get in touch with their own insurance company and get them to instigate the repairs. I still don't intend to get my own insurance company involved though. Do you think I am being paranoid or do you think I am being set up for a fall? The works quote my garage compiled for the £30 charge is around £4300 worth of damage with a list of work to be carried out (and says nothing about a re-spray). My car is quite new and was not written off by the claim's management guy that looked over the car, even though it was officially worth £6800 at the time of the accident. The claims management company who are dealing with this on behalf of the lorry driver's company has issued a 'retail' works reference (not an insurance one). NB: Another thing I do not like about this private arrangement is that there are too many parties involved - the lorry driver's company, a company they speak to about repairs, the repair's department claim's management company (who also apparently work for the insurance company who they are not involving). It all seems too complicated to me. The last thing I want is to be taken for a ride and shafted in some way. Any advice from those who might be able to offer sound, constructive advice about this please?

-

So i'm having a bit of a dispute with our house insurance, long story short, my husband didn't close the shower screen properly and left the bathroom with shower running for a period of time, I walked into my kitchen to find it had all collected into a bubble and burst through a hole in the ceiling causing damage to the walls, floor and plaster. Insurance told us we could claim through our escape of water and had to give them two itemized insurance quotes. We massively struggled to get these quotes with several traders not turning up or wanting to charge a fee to produce them, we asked if the insurance company could send out someone to quote and fix - they said no, we asked for a list of their preferred suppliers and was told they didn't have one. Eventually they told us they would send a loss adjuster out with a view to offer a cash settlement. Whilst waiting for the loss adjuster we had another leak when using the shower and it became apparent that the bath was coming away from the wall when we were using it causing the seal to break and the water to escape down the side, this was confirmed when we got a plumber out through our boiler cover insurance. So we resealed the bath but again the bath would move so in order to prevent more damage whilst waiting for the loss adjuster we stopped using the shower and stuck to baths only. We're still having to do this months later. The loss adjuster came, had no details of our claim as his system had crashed, he spent 5 minutes in the kitchen looking at the hole went into the bathroom, didn't ask us to remove the bath panel or look under the bath. He took some photos and left. We were then offered a settlement of just over £600 out of which a £250 escape of water excess was to be deducted. None of the works included in his scheduled involved fixing the issue with the bath. So we queried it. They've taken our query as a complaint and issued us with a final response claiming the loss adjuster took photos of the toilet which he claims was the root of the leak and we were negligent in fixing it hence as it must have been leaking a lengthy period as evidence by rust on the pipes (our pipes are all plastic so zero rust and 100% never been a leak) so they are refusing to pay out for any bathroom works. We've subsequently had 3 different plumbers out to the house for quote all which have been in the region of around £1700 and all the works listed are the same, all state that no evidence of a leak to the toilet and that significant removal and refitting of the bathroom suite and wet-wall will be needed to remedy the bath issue and the joist which has been soaked along with the fixing of the ceiling and flooring. The insurance company won't entertain these quotes or letters of evidence nor will the entertain the photos i've taken myself of the damage in particular behind the toilet which clearly shows plastic pipes and no rust anywhere there or under the bath. They've refused to let us see the report written by the loss adjuster or the photos taken and refuse to comment on how he could accurately know the issue when he didn't even look under the bath. They wont enter into a dialogue with us and have told us as they issued their final response we have to take it to the ombudsman if im not happy. Does anyone have any experience of this or words of advice on how to approach it with the ombudsman? what more evidence should I need or be gathering in order to support my complaint? I'm quite sure the insurance company are taking the **** in their offer but i've never had to make an insurance claim before so i'm not sure if this is normal or if i'm expecting too much?

So i'm having a bit of a dispute with our house insurance, long story short, my husband didn't close the shower screen properly and left the bathroom with shower running for a period of time, I walked into my kitchen to find it had all collected into a bubble and burst through a hole in the ceiling causing damage to the walls, floor and plaster. Insurance told us we could claim through our escape of water and had to give them two itemized insurance quotes. We massively struggled to get these quotes with several traders not turning up or wanting to charge a fee to produce them, we asked if the insurance company could send out someone to quote and fix - they said no, we asked for a list of their preferred suppliers and was told they didn't have one. Eventually they told us they would send a loss adjuster out with a view to offer a cash settlement. Whilst waiting for the loss adjuster we had another leak when using the shower and it became apparent that the bath was coming away from the wall when we were using it causing the seal to break and the water to escape down the side, this was confirmed when we got a plumber out through our boiler cover insurance. So we resealed the bath but again the bath would move so in order to prevent more damage whilst waiting for the loss adjuster we stopped using the shower and stuck to baths only. We're still having to do this months later. The loss adjuster came, had no details of our claim as his system had crashed, he spent 5 minutes in the kitchen looking at the hole went into the bathroom, didn't ask us to remove the bath panel or look under the bath. He took some photos and left. We were then offered a settlement of just over £600 out of which a £250 escape of water excess was to be deducted. None of the works included in his scheduled involved fixing the issue with the bath. So we queried it. They've taken our query as a complaint and issued us with a final response claiming the loss adjuster took photos of the toilet which he claims was the root of the leak and we were negligent in fixing it hence as it must have been leaking a lengthy period as evidence by rust on the pipes (our pipes are all plastic so zero rust and 100% never been a leak) so they are refusing to pay out for any bathroom works. We've subsequently had 3 different plumbers out to the house for quote all which have been in the region of around £1700 and all the works listed are the same, all state that no evidence of a leak to the toilet and that significant removal and refitting of the bathroom suite and wet-wall will be needed to remedy the bath issue and the joist which has been soaked along with the fixing of the ceiling and flooring. The insurance company won't entertain these quotes or letters of evidence nor will the entertain the photos i've taken myself of the damage in particular behind the toilet which clearly shows plastic pipes and no rust anywhere there or under the bath. They've refused to let us see the report written by the loss adjuster or the photos taken and refuse to comment on how he could accurately know the issue when he didn't even look under the bath. They wont enter into a dialogue with us and have told us as they issued their final response we have to take it to the ombudsman if im not happy. Does anyone have any experience of this or words of advice on how to approach it with the ombudsman? what more evidence should I need or be gathering in order to support my complaint? I'm quite sure the insurance company are taking the **** in their offer but i've never had to make an insurance claim before so i'm not sure if this is normal or if i'm expecting too much? -

Hi I took out a Barclays Income Protection insurance around 2008. http://www.barclays.co.uk/Insurance/Incomeinsurance/IncomeInsurance/P1242614107744 Barclays stopped selling this policy years ago. This was a policy that covered me for sickness and unemployment. I paid around a £100 a month and would get around £2000 a month in the event of making a claim for up to 2 years. I have been paying this policy for the last six 7 years. I was recently made unemployed due to a disagreement with my employer (over 7 years working there) - without going into details I was being asked to act immorally. I sought legal advice. It was clear the relationship had broken down. I did not resign, I was not fired - but a settlement agreement was put in place, which i decided to accept rather than going down the long and painful road of employment tribunals. Even if i had gone down a employment triberinal route - as I have read it, the polciy still would not have covered me as this would have been considered me resigning. The law around this was updated around this in 2010 in the Equality Act and further changes were recommended in 2013. Since I took out the policy i have never been contacted by Barclays with any statements or policy changes etc. I pay my money and they have been silent. When I signed up to the agreement I specifically asked about “Compromise Agreements” and was told that these were covered, as this is what had happened to me at a previous company. These are now called "settlement agreements" and widly used by employers for senior managers to deal with someone leaving. I feel I was mis-sold this policy and that I want to claim back my premiums i have paid to date. it would have been impossible for me to make a claim. If settlement agreements are now the norm and the policy does not cover it - it is worthless. I am wondering what the best course of action is - would this type of policy fall under PPI or is it something else ? Thanks in advance Simon

Hi I took out a Barclays Income Protection insurance around 2008. http://www.barclays.co.uk/Insurance/Incomeinsurance/IncomeInsurance/P1242614107744 Barclays stopped selling this policy years ago. This was a policy that covered me for sickness and unemployment. I paid around a £100 a month and would get around £2000 a month in the event of making a claim for up to 2 years. I have been paying this policy for the last six 7 years. I was recently made unemployed due to a disagreement with my employer (over 7 years working there) - without going into details I was being asked to act immorally. I sought legal advice. It was clear the relationship had broken down. I did not resign, I was not fired - but a settlement agreement was put in place, which i decided to accept rather than going down the long and painful road of employment tribunals. Even if i had gone down a employment triberinal route - as I have read it, the polciy still would not have covered me as this would have been considered me resigning. The law around this was updated around this in 2010 in the Equality Act and further changes were recommended in 2013. Since I took out the policy i have never been contacted by Barclays with any statements or policy changes etc. I pay my money and they have been silent. When I signed up to the agreement I specifically asked about “Compromise Agreements” and was told that these were covered, as this is what had happened to me at a previous company. These are now called "settlement agreements" and widly used by employers for senior managers to deal with someone leaving. I feel I was mis-sold this policy and that I want to claim back my premiums i have paid to date. it would have been impossible for me to make a claim. If settlement agreements are now the norm and the policy does not cover it - it is worthless. I am wondering what the best course of action is - would this type of policy fall under PPI or is it something else ? Thanks in advance Simon -

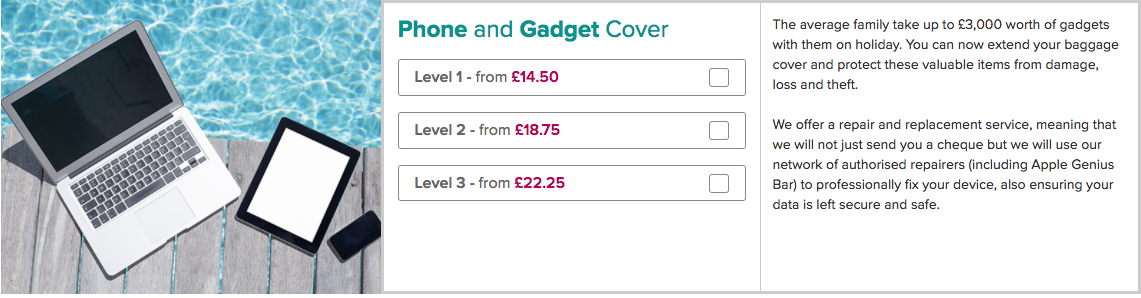

Hi there, Apologies if this is in the wrong section, but it seemed most appropriate. In October I went on holiday to India. Before I went I took out "gold" cover travel insurance with Cover For You. While I was on holiday my mobile phone was stolen from my bag. I reported it to the police, got a police report, immediately had it blocked by my phone company and did all the right things. However, on contacting the people administering the insurance, it turns out that mobile phones are not included in the insurance and that it is required to take out additional gadget insurance to cover phones. Now my phone was a brand new iPhone 7 that I'd had for 3 weeks. If it had been at all clear that it was excluded when buying my insurance, I would have taken the additional gadget insurance. But I remember going through the form application and when additional gadget insurance came up, it said this (I have recreated the insurance application and the screen is exactly as it was when I ordered): I remember thinking - I am not taking up to £3k, my baggage cover is up to £2k, so I don't need to "extend" it. And carried on. Maybe that was naive of me, maybe it was my fault for not examining it more closely, but the wording appears misleading to me. Then when I looked at the key facts, there is no information at all that gadgets are excluded from baggage allowance. In fact it states exclusion includes when: The loss, theft or damage to Valuables and electronic/other equipment occurs whilst not being carried in your hand luggage while You are travelling on Public transport or on an aircraft. This is in the personal baggage section. The reference to electronic equipment in that section again reinforced for me the idea that gadgets were covered up to the value of the personal baggage allowance. I would like to ask opinions on whether I have grounds for complaint here. I feel like I was mislead when buying the insurance and that it should be much much clearer that gadgets, including mobile phones, are excluded from personal baggage allowance and that it's essential to take out additional gadget insurance. Thanks in advance you your thoughts. [Just realised this should be in the insurance section - could an admin move it for me? Very sorry.)

-

Hey all, Looks like this forum is the answer to all my problems.To be honest would like to thanks dx100 uk & Martin 2006 for all their support in answering all the queries posted.This forum certainly points you in the right direction. So to begin with Admiral insurance i received the renewals pack for my multi car insurance ,the price they quoted me looked too high,so like usual i rang them to check if it was their best quote, i told them i got a quote elsewere which was 2200 ,my quote was 2500 ,so the gentlemen applied some discounts and quoted me a little above 2200 (wish i had said 1200). Now the interesting part on my renewals which i noticed was that the cars were kept at my old address although i had called to change my address a couple of times,once i asked the advisor why this was as such he said theagent might not have changed this and would need to check further ,so when he put this address in where i was living it bought the quote of 2200 to 1100 (Lucky me) which i was pleased with. However my concern here is i am with them from over 7 years & have changed the address twice in a year & also have changed the car ,i queried this with the advisor that if the "Post code where kept" hasnt been changed over this year then its not my fault and i had paid the wrong premium during this address change to which he replied he will have to check the call(i remember calling & changing my address in june which he confirmed) He further advised he will have to go through the call log & will come back to me with an outcome. Now i know they will try to put this on me saying i have not updated the details & its my fault which i dont think it is coz as soon as i moved to a different address i had called the insurance to change this & the agent has onfirmed. I just want to check what the insurance company can do in this case to prevent them from giving me a refund? i m sure they have their own tactics in relaying this back and putting this on my head Shall i complaint? Will they accept their liability? what should i wary of when they call me back? how shall i proceed? Any help or direction is much appreciated again As always many thanks again

-

I had very bad experience with FOS at the adjudicator level AND ombudsman level: the adjudicator appeared to have limited legal knowledge related to my complaint and sometimes even came across short of common sense. The ombudsman made her decision on her obviously incorrect assumption which was absolutely false. When I pointed it out a senior level for review, FOS wrote to me saying her mistake was unimportant and thus upheld her decision. I am now thinking to escalate my complaint to the highest level. However, FOS services seemed unacceptable given that they should work for facts and justice. . Now I start to understand why banks these days are so keen to ask you to approach FOS once disputes arisen. The services I have received from FOS was simply an insult to its name. I will tell you how one of the biggest home insurance providers have dealt with me. My lease-hold flat has been insured with it for many years. In the policy renewal documents I received in 2012, 2011, and 2010, the covering letter states 'Please note, any changes to the policy wording are detailed overleaf'. You turn the page around and It is a nearly blank page overleaf without any DETAILED changes, except the wording quoted as below: The above quoted identical wording was certainly from the same template, appearing in all the renewal documents in 2010,2011,and 2012. It is a common sense and an industrial practice that banks would have to highlight the important product information in their correspondence. Plus, the covering letter itself clearly states that any changes will be detailed overleaf, where no detailed information was given. As no document entitled 'Your Home policy document changes' was enclosed with other renewal documents or received separately in 2010,2011, and 2012, I was made genuinely to believe that my policy terms remain unchanged in 2010, 2011, and 2012. In 2015, I had a claim for lease related dispute, which the insurer refused. The insurer said that the cover to lease disputes had been removed since may 2010 according to the renewal documents it sent to me in May 2010. Its allegation was totally untrue. Given that my renewal documents was made under the same template in three years, I believe the template was very likely used to produce some of your renewal documents too. Now, can you please check if the quoted wording appears in your insurance renewal document for year 2010, 2011, and 2012? If so, can you please let me know whether you have received the document ' Your Home policy document changes' attached to your renewal documents? Please help me fight for consumer rights!

-

In the latest statement, Philip Hammond announced increase in Insurance premium tax to 12.5% from June 2017. Given that Insurers also like to include other premium increases, people are likely to see average increases on Insurances of 20% or more. With average Car Insurance premiums now £700, i could see this rising by at least another £100. Then add on increases to other Insurances bought by households and you could see an extra £300 to £400 in annual budget taken by Insurances. Because VAT is 20% currently. Philip Hammond used this as a reason to justify increasing Insurance Premium Tax, suggesting that people were already getting a discounted tax rate. I am not sure people will see it in the same way. Is buying Insurance the same as buying any other consumer product ? Given that Car Insurance is a legal requirement and not optional, i would argue that tax should not be paid on the compulsory third party liability element of the policy.

-

Hello insurance specialists, I wonder if you can help me please? I'm executor for my mother and am trying to renew cover for her house. It's been empty since she went into a care home about 3 years ago and we're currently trying to sell it. Probate came through in August. I rang Swinton who have been insuring the house through Towergate and they say nobody wants to quote now, because of the length of time the house has been empty. Does anyone know of other companies who would look at this please? Many thanks, HB

Hello insurance specialists, I wonder if you can help me please? I'm executor for my mother and am trying to renew cover for her house. It's been empty since she went into a care home about 3 years ago and we're currently trying to sell it. Probate came through in August. I rang Swinton who have been insuring the house through Towergate and they say nobody wants to quote now, because of the length of time the house has been empty. Does anyone know of other companies who would look at this please? Many thanks, HB -

My OH's elderly parents have Home Insurance policy with RSA through Lloyds bank. In July 2015 one of their patio doors glass shattered and had to be replaced. They submitted a claim and glass was eventually replaced (3 weeks) by Evander Glazing, who assumed it was due to direct sunlight / heat. Whilst replacing it the glass shattered again therefore replaced on 2nd attempt. Today the same glass shattered again. My question is, would the replacement glass be under any sort of guarantee? Thank-you

My OH's elderly parents have Home Insurance policy with RSA through Lloyds bank. In July 2015 one of their patio doors glass shattered and had to be replaced. They submitted a claim and glass was eventually replaced (3 weeks) by Evander Glazing, who assumed it was due to direct sunlight / heat. Whilst replacing it the glass shattered again therefore replaced on 2nd attempt. Today the same glass shattered again. My question is, would the replacement glass be under any sort of guarantee? Thank-you -

We recently had a flood upstairs and our downstairs room was destroyed. We've had no claims insurance for more than 10 years. We put in a claim to our insurance company who were dragging their heals ( like they do) they came and asses the damage and we thought the claim was going through. Then out of the blue we were sent a letter by a different insurance company stating we had to renew our policy. My husband had insured is twice by accident for home and content insurance!!! He called the other insurance company and told them about the flood - they asked if we had any other insurance company and he said no, but he wasn't really listening to the questions properly either. Straight away they stop all claims and sent it to the investigation team.! The same underwriter looked at both cases and the second insurance company said they've rejected the claim due to fraud and the 1st insurance company who took 4-5 weeks to come to this conclusion And informed me today they also stop the claim for fraud! This was a genuine mistake - getting two policies (why didn't they tell us) and not telling each insurance company about each other. He thought they were the same company!!! We now can't get any compensation for £4000 worth of loss....my house is a mess and I've waited 8 weeks for them to come to this decision. With 4 kids running around it's quite dangerous now Can anyone help or advise on what to do? Will this effect future insurance? Have I got a leg to stand on at all?

We recently had a flood upstairs and our downstairs room was destroyed. We've had no claims insurance for more than 10 years. We put in a claim to our insurance company who were dragging their heals ( like they do) they came and asses the damage and we thought the claim was going through. Then out of the blue we were sent a letter by a different insurance company stating we had to renew our policy. My husband had insured is twice by accident for home and content insurance!!! He called the other insurance company and told them about the flood - they asked if we had any other insurance company and he said no, but he wasn't really listening to the questions properly either. Straight away they stop all claims and sent it to the investigation team.! The same underwriter looked at both cases and the second insurance company said they've rejected the claim due to fraud and the 1st insurance company who took 4-5 weeks to come to this conclusion And informed me today they also stop the claim for fraud! This was a genuine mistake - getting two policies (why didn't they tell us) and not telling each insurance company about each other. He thought they were the same company!!! We now can't get any compensation for £4000 worth of loss....my house is a mess and I've waited 8 weeks for them to come to this decision. With 4 kids running around it's quite dangerous now Can anyone help or advise on what to do? Will this effect future insurance? Have I got a leg to stand on at all?