Showing results for tags 'charging'.

-

Hi, I wonder if anyone can help? Today I received a letter from Mortimer Clarke Solicitors acting on behalf of Cabot Financial and tyring to get a charging order for an unpaid debt. attached to the letter is copy of the county court judgement dated 6th July 2017 and a copy of the intermin charging order dated 7th September 2017 it states I have 14 days from the date of this to send in reconsideration and unless the judgement debtor o any other person files and serves their objection to the continuation of the charge in writing, within 28 days from the date of service fo the order, the application will be considered by a district Judge no later than 26th October 2017.. Firstly, I have no clue as to what this debt is for, had no clue that it had been to court (until today). The debt is for £4,895.22. What do I do? As in how do I go about finding out what this debt is for, overturning the judgement etc? Any help would be much appreciated. Many thanks Hannah

-

Hi I own a small company with 3 employees only been running since April this year I had booked a holiday and 4 days before I went away one of my employees left without warning. I had no choice but to contact my local agency to employ a temp worker to cover the period I was away 10 days in all . It was quite a straightforward process with just a couple of forms to fill in and sign one of which was thier terms of business . All done over the telephone with the forms being emailed back etc . I queried the hourly rate whilst on the telephone as it wasn't written anywhere (I have never used an agency before ) and the administrator put me through to another lady whom I assume was the manager she told me that the hourly rate was £12.80 for a min of 8 hours a day and then after that it was time and a half. The ten days would include 2 saturdays and a bank holiday . The agency asked me to pay up front as apparently they take a line of credit to ensure that each worker is paid but thier credit company wouldn't lend agaginst my company as it had been newly formed . I thought this was a bit strange and said no I'm not prepared to pay upfront but would pay for the first three days after they had been completed and then the remaining 7 days a couple of days after they had been completed which they agreed to . Due to the nature of the work I insisted that I must have the same person for the duration of the contract which again they agreed to. The agency worker turned up as arranged and I went on holiday.... after the first three days I received an invoice from the agency as promised but to my horror they had charged the whole of sat as time and a half. I queried this by email as I was away and corresponded with the lady who had told me about the hourly rate. When I asked why the whole of sat was charged as overtime her written reponse was sorry I didn't mention it but this practice is common knowledge within the industry everybody pays sat and bank holidays as overtime otherwise they wouldn't get people to work.so I replied that she knew I was a new customer she knew I was having the worker over the weekend and bank holiday so why not mention in the telephone call that sat and bank holidays are classed as overtime ?? To which she apologised again for not telling me but she thought I was not new . Thier terms of business says hourly rate etc to be agreed in writing I have nothing from them in writing stating what the hourly rate would be just the verbal confirmation during the telephone call backed up by her email apologising for not telling me about the changes on sat and bank holiday . I'm away on holiday and am panicking that if I kick up about the invoice that she will pull the worker and leave me in the right brown stuff. So against my better judgement I pay it but send an email complaining I'm not happy .To which I get no response So 4 days later I get a phone call from the agency saying the original worker is leaving today but he is going to be replaced by another worker who will be doing the rest of the week (3 days remaining )....as you can imagine I kick off big time especially after I'd gone to all the effort of insisting that I needed the same worker for the 10'days apparently the worker had been contacted by another employer that he Temps for and wanted to go and work for them apparently the agency can't stop him from doing this which again I was not told about especially as I had lengthy conversations with the agency about this . So I eventually agree to having the replacement guy and then when I speak with the new guy on the telephone in the evening he tells me that he can only do the last two days as he has commitments on the last day which apparently the agency knew about !! That is the final straw so I have cancelled the work for the last day as don't want to use the agency again as too much grief . I will be getting the invoice for the last period of work soon so would like to know if I can deduct the rate increase that I paid originally whilst I was away from the new invoice ,and go down the line I wasn't told it's not written down anywhere etc and can I do anything about having to cancel the last working day and being mucked around etc with different staff etc this company are a joke and I will never use them again Any thoughts greatly appreciated !!

Hi I own a small company with 3 employees only been running since April this year I had booked a holiday and 4 days before I went away one of my employees left without warning. I had no choice but to contact my local agency to employ a temp worker to cover the period I was away 10 days in all . It was quite a straightforward process with just a couple of forms to fill in and sign one of which was thier terms of business . All done over the telephone with the forms being emailed back etc . I queried the hourly rate whilst on the telephone as it wasn't written anywhere (I have never used an agency before ) and the administrator put me through to another lady whom I assume was the manager she told me that the hourly rate was £12.80 for a min of 8 hours a day and then after that it was time and a half. The ten days would include 2 saturdays and a bank holiday . The agency asked me to pay up front as apparently they take a line of credit to ensure that each worker is paid but thier credit company wouldn't lend agaginst my company as it had been newly formed . I thought this was a bit strange and said no I'm not prepared to pay upfront but would pay for the first three days after they had been completed and then the remaining 7 days a couple of days after they had been completed which they agreed to . Due to the nature of the work I insisted that I must have the same person for the duration of the contract which again they agreed to. The agency worker turned up as arranged and I went on holiday.... after the first three days I received an invoice from the agency as promised but to my horror they had charged the whole of sat as time and a half. I queried this by email as I was away and corresponded with the lady who had told me about the hourly rate. When I asked why the whole of sat was charged as overtime her written reponse was sorry I didn't mention it but this practice is common knowledge within the industry everybody pays sat and bank holidays as overtime otherwise they wouldn't get people to work.so I replied that she knew I was a new customer she knew I was having the worker over the weekend and bank holiday so why not mention in the telephone call that sat and bank holidays are classed as overtime ?? To which she apologised again for not telling me but she thought I was not new . Thier terms of business says hourly rate etc to be agreed in writing I have nothing from them in writing stating what the hourly rate would be just the verbal confirmation during the telephone call backed up by her email apologising for not telling me about the changes on sat and bank holiday . I'm away on holiday and am panicking that if I kick up about the invoice that she will pull the worker and leave me in the right brown stuff. So against my better judgement I pay it but send an email complaining I'm not happy .To which I get no response So 4 days later I get a phone call from the agency saying the original worker is leaving today but he is going to be replaced by another worker who will be doing the rest of the week (3 days remaining )....as you can imagine I kick off big time especially after I'd gone to all the effort of insisting that I needed the same worker for the 10'days apparently the worker had been contacted by another employer that he Temps for and wanted to go and work for them apparently the agency can't stop him from doing this which again I was not told about especially as I had lengthy conversations with the agency about this . So I eventually agree to having the replacement guy and then when I speak with the new guy on the telephone in the evening he tells me that he can only do the last two days as he has commitments on the last day which apparently the agency knew about !! That is the final straw so I have cancelled the work for the last day as don't want to use the agency again as too much grief . I will be getting the invoice for the last period of work soon so would like to know if I can deduct the rate increase that I paid originally whilst I was away from the new invoice ,and go down the line I wasn't told it's not written down anywhere etc and can I do anything about having to cancel the last working day and being mucked around etc with different staff etc this company are a joke and I will never use them again Any thoughts greatly appreciated !! -

My late mother had dementia. She was also quite secretive so I knew nothing of this story until just prior to her death. She owned a property and ran up large debts and was sued by the department store's legal dept. They appointed golden boys Restons who succeeded in getting a final charging order on the property in 2012 following a CCJ in 2011. She paid £67 per month until her death last year. The property is in the process of being sold but a lifetime mortgage has to be paid off first. Unfortunately Restons are being tardy in processing relinquishing the charging order but... The value of the debt is greater than the balance of the sale price after the mortgage has been paid off so what happens next? Is it down to Restons whether the charging order is waived at all or can they say no sale thanks? Can they insist that the whole debt is paid first before relinquishing? Does the balance become unsecured debt? Is there any come back on Restons if they refuse to give authority to relinquish the CO. Restons' client doesn't seem to want to know and if you have tried to get in touch with Restons then you'll know it is a total nightmare!

-

Looking for advice on this as I have only been made aware of S86D CCA. I have been on a DMP with Payplan for over 6 years. During this time Barclay's have continue to charge interest albeit at reduced rates on my two cards. I don't believe that they ever sent out a notice of arrears for the accounts at any time. With S86D in mind am I right in thinking that they therefore have not been entitled to charge interest. Whilst I have had AP markers for the entire period they have backdated defaults which will mean that they drop off within the next couple of months. I have received monthly statements from Barclays for the cards throughout so does this counteract the requirement for them to provide a notice of arrears. The interest would be sizeable and could wipe out the rest of my DMP which still has 5 months to run. I have found the below advice Arrears notice penalty Of course, when a trader provides credit, he or she accepts that the debtor may default, whether intentionally or not, or knowingly or not. Either way, the creditor is under a duty to provide the debtor with a notice stating that he or she is in arrears and exactly how much money is owed. Section 11 of the CCA 2006 amends the CCA 1974 by inserting a new section - 86D - that sets out the consequences for a creditor if he fails to notify as required by sections 86B or 86C. If the creditor fails to provide a notice when required to do so, then throughout the period of his failure (i.e. from the date that it was required to be given until the end of the day on which it is eventually provided), he is not entitled to enforce the agreement. In addition, the debtor or hirer is not liable to pay any interest that relates to the period of the creditor or owner’s failure,

Looking for advice on this as I have only been made aware of S86D CCA. I have been on a DMP with Payplan for over 6 years. During this time Barclay's have continue to charge interest albeit at reduced rates on my two cards. I don't believe that they ever sent out a notice of arrears for the accounts at any time. With S86D in mind am I right in thinking that they therefore have not been entitled to charge interest. Whilst I have had AP markers for the entire period they have backdated defaults which will mean that they drop off within the next couple of months. I have received monthly statements from Barclays for the cards throughout so does this counteract the requirement for them to provide a notice of arrears. The interest would be sizeable and could wipe out the rest of my DMP which still has 5 months to run. I have found the below advice Arrears notice penalty Of course, when a trader provides credit, he or she accepts that the debtor may default, whether intentionally or not, or knowingly or not. Either way, the creditor is under a duty to provide the debtor with a notice stating that he or she is in arrears and exactly how much money is owed. Section 11 of the CCA 2006 amends the CCA 1974 by inserting a new section - 86D - that sets out the consequences for a creditor if he fails to notify as required by sections 86B or 86C. If the creditor fails to provide a notice when required to do so, then throughout the period of his failure (i.e. from the date that it was required to be given until the end of the day on which it is eventually provided), he is not entitled to enforce the agreement. In addition, the debtor or hirer is not liable to pay any interest that relates to the period of the creditor or owner’s failure, -

Hi all So my dad is due to fly to Sweden next month, as his brother is in his final months of live, due to cancer. He booked a flight via Norwegian air for a return trip from Gatwick to Copenhagen for £106.90 on Monday the 17th. He got the confirmation email, so everything looked normal, until Wednesday, he got a series of flight confirmation emails, which listed changes to his flight. The first email was a series of cancellation/time changes, but also included: 2 x Checked baggage (10.00 GBP) 0.00 (0%) 20.00 2 x Upgrade fee (36.00 GBP) 0.00 (0%) 72.00 2 x Namechange fee (36.00 GBP) 0.00 (0%) 72.00 2 x Checked baggage (15.00 GBP) 0.00 (0%) 30.00 Fast track 0.00 (0%) 9.00 WCHR – Wheelchair (ramp) 0.00 (0%) 0.00 2 x Hearing impairments 0.00 (0%) 0.00 2 x Vision impairments 0.00 (0%) 0.00 WCHC – Wheelchair (seat) 0.00 (0%) 0.00 For a grand total of £289.90 The second email was the same thing, but the times were back to their originals, again, the same total price. Third email was the same upgrades/changes again, but also different flight times, with stop overs in Madrid for the return flight These changes were £629.80 Fourth and final email had the same types of changes, only for a lot more money (£1191.70) and included a whole bunch of random things like golf equipment etc. Checked baggage 0.00 (0%) 25.20 4 x Upgrade fee (36.00 GBP) 0.00 (0%) 144.00 Checked baggage 0.00 (0%) 16.80 Checked baggage 0.00 (0%) 43.00 2 x Namechange fee (36.00 GBP) 0.00 (0%) 72.00 2 x Seat reservation (10.00 GBP) 0.00 (0%) 20.00 Checked baggage 0.00 (0%) 32.00 Checked baggage 0.00 (0%) 15.00 2 x Golf equipment 0.00 (0%) 56.00 4 x Ski equipment 0.00 (0%) 112.00 2 x Fast track 0.00 (0%) 9.00 11x Excess baggage 0.00 (0%) 99.00 16x Excess baggage 0.00 (0%) 144.00 Windsurfing equipment 0.00 (0%) 38.00 Kite equipment 0.00 (0%) 38.00 Total Amount 0.00 1191.70 All of these individual charges have apparently been debited from his account. So he got in touch with Norwegian Air through their chat system and they were of zero use, basically telling him it wasn't them, it must have been him, or someone else. He got the same response from their phone line, that he's been hacked, or his account has been hacked and for him to go to his bank and the police. He doesn't even have an account with norwegian air, so could he or anyone make changes? He's going down to the police station and bank tomorrow about it, but has anyone else experienced anything like this?

Hi all So my dad is due to fly to Sweden next month, as his brother is in his final months of live, due to cancer. He booked a flight via Norwegian air for a return trip from Gatwick to Copenhagen for £106.90 on Monday the 17th. He got the confirmation email, so everything looked normal, until Wednesday, he got a series of flight confirmation emails, which listed changes to his flight. The first email was a series of cancellation/time changes, but also included: 2 x Checked baggage (10.00 GBP) 0.00 (0%) 20.00 2 x Upgrade fee (36.00 GBP) 0.00 (0%) 72.00 2 x Namechange fee (36.00 GBP) 0.00 (0%) 72.00 2 x Checked baggage (15.00 GBP) 0.00 (0%) 30.00 Fast track 0.00 (0%) 9.00 WCHR – Wheelchair (ramp) 0.00 (0%) 0.00 2 x Hearing impairments 0.00 (0%) 0.00 2 x Vision impairments 0.00 (0%) 0.00 WCHC – Wheelchair (seat) 0.00 (0%) 0.00 For a grand total of £289.90 The second email was the same thing, but the times were back to their originals, again, the same total price. Third email was the same upgrades/changes again, but also different flight times, with stop overs in Madrid for the return flight These changes were £629.80 Fourth and final email had the same types of changes, only for a lot more money (£1191.70) and included a whole bunch of random things like golf equipment etc. Checked baggage 0.00 (0%) 25.20 4 x Upgrade fee (36.00 GBP) 0.00 (0%) 144.00 Checked baggage 0.00 (0%) 16.80 Checked baggage 0.00 (0%) 43.00 2 x Namechange fee (36.00 GBP) 0.00 (0%) 72.00 2 x Seat reservation (10.00 GBP) 0.00 (0%) 20.00 Checked baggage 0.00 (0%) 32.00 Checked baggage 0.00 (0%) 15.00 2 x Golf equipment 0.00 (0%) 56.00 4 x Ski equipment 0.00 (0%) 112.00 2 x Fast track 0.00 (0%) 9.00 11x Excess baggage 0.00 (0%) 99.00 16x Excess baggage 0.00 (0%) 144.00 Windsurfing equipment 0.00 (0%) 38.00 Kite equipment 0.00 (0%) 38.00 Total Amount 0.00 1191.70 All of these individual charges have apparently been debited from his account. So he got in touch with Norwegian Air through their chat system and they were of zero use, basically telling him it wasn't them, it must have been him, or someone else. He got the same response from their phone line, that he's been hacked, or his account has been hacked and for him to go to his bank and the police. He doesn't even have an account with norwegian air, so could he or anyone make changes? He's going down to the police station and bank tomorrow about it, but has anyone else experienced anything like this? -

Hi All Earlier this year I had a Final Charging Order applied for by my local Council to my local County Court. This secures a long-standing Council Tax debt from a past period of financial difficulty. I’ve no problem with that, it’s right and proper and appears to have been done procedurally correctly. The issue I have is that the Final Charging Order, issued by the County Court with a case number etc, has found its way to Registry Trust so is now listed on my credit file by the credit reference agencies. I’d always understood that credit reference agencies didn’t list council tax debt, so I’ve done a bit of research and made a few calls and I’m now in a position where I need some advice – hence my post here. I rang Registry Trust, the guy I spoke to said normally a charging order wouldn’t be listed but the info they get sent to upload from the County Court Money claim centre doesnt specify what the Judgement is - it just lists case number, amount, claimant & defendant names. He advised me to call the County Court Money claim centre, who have asked me to put my case to them in a letter or email. So what I’m looking to find out is: 1. What and where is the legislation or rules saying what Registry Trust should list? 2. How do I go about getting them to remove the record if it shouldn’t be there? 3. What about the credit reference agencies themselves, what and where is the legislation or rules saying what they can list? I dont want this blighting my file for 6 years if it shouldnt be there. Thanks in advance for any help

Hi All Earlier this year I had a Final Charging Order applied for by my local Council to my local County Court. This secures a long-standing Council Tax debt from a past period of financial difficulty. I’ve no problem with that, it’s right and proper and appears to have been done procedurally correctly. The issue I have is that the Final Charging Order, issued by the County Court with a case number etc, has found its way to Registry Trust so is now listed on my credit file by the credit reference agencies. I’d always understood that credit reference agencies didn’t list council tax debt, so I’ve done a bit of research and made a few calls and I’m now in a position where I need some advice – hence my post here. I rang Registry Trust, the guy I spoke to said normally a charging order wouldn’t be listed but the info they get sent to upload from the County Court Money claim centre doesnt specify what the Judgement is - it just lists case number, amount, claimant & defendant names. He advised me to call the County Court Money claim centre, who have asked me to put my case to them in a letter or email. So what I’m looking to find out is: 1. What and where is the legislation or rules saying what Registry Trust should list? 2. How do I go about getting them to remove the record if it shouldn’t be there? 3. What about the credit reference agencies themselves, what and where is the legislation or rules saying what they can list? I dont want this blighting my file for 6 years if it shouldnt be there. Thanks in advance for any help -

Hi All, I have been living in a private rented property for 14 months now. Up until today, both the letting agents and landlord have been spot on. Yesterday morning we woke to a broken double glazed window. This happened over night and was through no fault of our own as the tenant. I phoned the letting agents to be told "Sorry, glass is your problem to replace". My main concern was getting rid of the broken window and being secure so I had a company in to quote for a replacement. The fitters who came straight away said there are very obvious signs that the window has failed due to a manufacturing defect and has showed me how I can evidence this. He has also said he is willing to write a report confirming this with pictures and that Pilkington, the manufacturer will do the same. We have been good tenants, not over expecting, always paid on time and have looked after the place very well. The letting agents originally told the landlord that I broke the window so the landlord said it was my responsibility to change. I can understand that. If I had of broken it through my own fault, I would never expect them to pay to repair. I asked the letting agents to go back again and explain the situation clearly including that I will be able to supply professional evidence of no wrong doing on my behalf. Today I have had an email back stating that as a gesture of good will, the landlord will replace this one however in future it is my responsibility. Now, I do not want to sour my relationship with either the landlord or letting agents but to me this is not on. My contract does state; To keep the interior of the property (including glass in the windows and lock fastenings and fittings of the outer doors and windows) and the effects in as good and substantial repair and condition as at the date hereof (fair wear and tear excepted) and (where applicable) all electrical and other mechanical apparatus in good working order and to immediately replace broken glass upon the occurrence of any breakage However surely a failure through no fault of my own can be my responsibility? Some advice would be much appreciated.

Hi All, I have been living in a private rented property for 14 months now. Up until today, both the letting agents and landlord have been spot on. Yesterday morning we woke to a broken double glazed window. This happened over night and was through no fault of our own as the tenant. I phoned the letting agents to be told "Sorry, glass is your problem to replace". My main concern was getting rid of the broken window and being secure so I had a company in to quote for a replacement. The fitters who came straight away said there are very obvious signs that the window has failed due to a manufacturing defect and has showed me how I can evidence this. He has also said he is willing to write a report confirming this with pictures and that Pilkington, the manufacturer will do the same. We have been good tenants, not over expecting, always paid on time and have looked after the place very well. The letting agents originally told the landlord that I broke the window so the landlord said it was my responsibility to change. I can understand that. If I had of broken it through my own fault, I would never expect them to pay to repair. I asked the letting agents to go back again and explain the situation clearly including that I will be able to supply professional evidence of no wrong doing on my behalf. Today I have had an email back stating that as a gesture of good will, the landlord will replace this one however in future it is my responsibility. Now, I do not want to sour my relationship with either the landlord or letting agents but to me this is not on. My contract does state; To keep the interior of the property (including glass in the windows and lock fastenings and fittings of the outer doors and windows) and the effects in as good and substantial repair and condition as at the date hereof (fair wear and tear excepted) and (where applicable) all electrical and other mechanical apparatus in good working order and to immediately replace broken glass upon the occurrence of any breakage However surely a failure through no fault of my own can be my responsibility? Some advice would be much appreciated. -

@PANDORA_UK Hi there, I would like some advice please. Last week I purchased a 'Abundance Of Love' ring from Pandora UK on their online store for my daughters 16th birthday which is this coming Thursday. The cost in the sale was £19 plus £5 delivery. Today I received a parcel from Pandora. In the parcel is my invoice for the ring at £19 and delivery £5. However in the parcel there were two jewellery boxes. One had a necklace and pendant in. The other had 5 x Pandora charms in. After looking on the website I estimate the cost of this order around £300-£350. I like to think I am an honest person and although my dispatch note only said the ring I thought its only fair I ring and tell them about their error. I called and explained I ordered a £19 ring and have received over £300 of jewellery. They said once I send the jewellery back to them they will dispatch my ring. I said is there anyway around this as I would like the ring for my daughters birthday on Thursday. (ok its only £19 but should have been £45 - money is tight at the moment and this was going to be a special present for her) He put me on hold and said he spoke to his manager and no they couldnt do anything until I sent the parcel back. I said ok is a courier coming to collect it. He then said no you need to take it to the post office tomorrow and send it back to us recorded delivery! I kept very polite and said I rang you and was 100% honest when I could have just kept quiet and kept all this jewellery and now you are telling me that I have to take time out of work tomorrow to go into town to the postoffice and I have to pay to return it. He said yes or we cannot send out your original ring order. I asked to speak to management but suddenly no one was available. He said someone would call me right back but no one has. Am I right in being extremely angry that this is their mistake yet I have to pay for it? Can they make me? Am I within my rights to refuse to post it back at my expense? I am more then happy to have a courier come and collect it but I work from home and cannot easily get out to town for the postoffice during the week. I am so upset that I did the honest decent thing and now I am going to be out of pocket and my daughter will not have her birthday present. Any advice is appreciated. thank you

@PANDORA_UK Hi there, I would like some advice please. Last week I purchased a 'Abundance Of Love' ring from Pandora UK on their online store for my daughters 16th birthday which is this coming Thursday. The cost in the sale was £19 plus £5 delivery. Today I received a parcel from Pandora. In the parcel is my invoice for the ring at £19 and delivery £5. However in the parcel there were two jewellery boxes. One had a necklace and pendant in. The other had 5 x Pandora charms in. After looking on the website I estimate the cost of this order around £300-£350. I like to think I am an honest person and although my dispatch note only said the ring I thought its only fair I ring and tell them about their error. I called and explained I ordered a £19 ring and have received over £300 of jewellery. They said once I send the jewellery back to them they will dispatch my ring. I said is there anyway around this as I would like the ring for my daughters birthday on Thursday. (ok its only £19 but should have been £45 - money is tight at the moment and this was going to be a special present for her) He put me on hold and said he spoke to his manager and no they couldnt do anything until I sent the parcel back. I said ok is a courier coming to collect it. He then said no you need to take it to the post office tomorrow and send it back to us recorded delivery! I kept very polite and said I rang you and was 100% honest when I could have just kept quiet and kept all this jewellery and now you are telling me that I have to take time out of work tomorrow to go into town to the postoffice and I have to pay to return it. He said yes or we cannot send out your original ring order. I asked to speak to management but suddenly no one was available. He said someone would call me right back but no one has. Am I right in being extremely angry that this is their mistake yet I have to pay for it? Can they make me? Am I within my rights to refuse to post it back at my expense? I am more then happy to have a courier come and collect it but I work from home and cannot easily get out to town for the postoffice during the week. I am so upset that I did the honest decent thing and now I am going to be out of pocket and my daughter will not have her birthday present. Any advice is appreciated. thank you -

It would appear that Ebay is to start charging 20% VAT on fees when it changes it corporate structure later this year. Sellers with a turnover under £85,000 will not be affected. https://tamebay.com/2017/05/ebay-uk-spring-2017-seller-release-ebay-to-charge-vat-on-fees.html

-

Recently had a solicitors letter stating that a Charging Order was being sought on behalf of Hoist Portfolio Holding 2 Ltd. The amount is £9680. The District Judge will consider this case no later than 18/5/2017. I presume the amount owed is credit card debt - what should I do? Thanks in anticipation.

-

Hi, I have received an interim charging order after a judgement or order was given on the 19th January 2015 by the county court business centre. The application will be heard on the 3rd august 2015 at the county court in Kings Lynn. Is it too late for me to defend this? I received the judgement from the Nottingham County Court business centre in January, but as it was not signed by a judge and did not have my dob on the order I gave it no credence. Any advice on my next steps would be appreciated Many thanks.

Hi, I have received an interim charging order after a judgement or order was given on the 19th January 2015 by the county court business centre. The application will be heard on the 3rd august 2015 at the county court in Kings Lynn. Is it too late for me to defend this? I received the judgement from the Nottingham County Court business centre in January, but as it was not signed by a judge and did not have my dob on the order I gave it no credence. Any advice on my next steps would be appreciated Many thanks. -

I was advised by Citizen Advice Bureau to just admit a debt to the court paper. During the advice session they didn’t tell me I should ask for my credit agreement paper related to the debt with the OC and the authority of the DCA regarding to this debt (I did mention I own a debt to a company but I never heard of this DCA). I was told that there would be a hearing and the judge generally would allow me to pay monthly against my income. But the truth was that, the case just went through to the court clerk without a hearing and as a result, a CCJ against me straight away. I was ordered to pay in full without any chance to forward my financial details. The solicitor firm send me letter and they just wanted full amount and issued a charge for my home right away. The solicitor firm scared me to hell by claiming bailiff’s action and seizes of my home to make me homeless. I don’t even dare to open a window even its hot summer time nowadays. I tried to offer a monthly plan with the solicitor firm but in vain. Then suddenly, I received a letter from another solicitor firm (I would call it – B) telling me that they had taken over the original solicitor firm’s business and I must pay them money in full now. I had send numerous requests for any legal document so I could tell that my DCA (on the court form) would recognizes this arrangement, ‘B’ never answered my requests and they kept throwing me more thread. I had paid a monthly token to the old solicitor’s bank account on my own initial during the tangle with ‘B’. Then I stopped as I don’t hear anything back from the old solicitor firm. Lately I received a new thread from ‘B’, they are going to issue court order to seize my house unless I pay them. I am very scared !!! What should I do now and I have these questions : 1) ‘B’ uses roughly the same name as the old solicitor firm and it uses the same correspondence address too. But being a solicitor firm, they should know better about the legal issue. 2) Should I have a right to ask for an authority letter showing that the OC/DCA had given ‘B’ to collect the money? 3) I don’t know anything about ‘business taken over law’, but during a taken over, they should inform the court as well? I had asked my local court, ‘B’ didn’t file any paper to them about the take over. 4) If they issue order to seize of my home, could I appeal on the basis ‘B’ ignore my constant requests for proper paper about the authority of ‘B’ position to chase me money. ‘B’ kept chased me money and ordered me to pay into ‘B’ bank account not to my OC/DCA. 5) Would I look really bad at the hearing (if there’s any I could go to) as I know some court judge don’t like debtor at all? Please I really need advices here as I really don’t know what to do now! Thanks for all the help in advance.

-

Hi, Be really really grateful for any guidance. Some years ago , -2007/8/9 we got into big debt trouble, lost our business and the only thing we were able to keep, amazingly, was a 1 bed flat in my wife's name which at the time didn't really have any equity in it so wasn't much point in selling. CAG helped enormously, RMA from Amex dropped amongst other things and over time most have stopped pursuing us. However while I know there are sadder stories out there than ours the stress added up and we also split up with my wife keeping and living in the 1 bed flat. In 2014 MBNA produced a CCJ against my wife for €14000 on a credit card she had back in 2002. She made an arrangement to pay £100+ per month and understood it was interest free etc, doesn't seem to have had paperwork on it. She has never missed a payment and the balance is now £11,000 odd. They only assets she has in the world is the flat (interest only mortgage but a low interest rate) - about £40k equity and next year at 65 she must retire from the NHS (4 years service won't amount to much). So, having got through everything she is in pieces having received a letter from the Land registry saying that they have placed an interim charging order on the flat in favour of Arrow for the £11,000 balance. The letter seems to read that they automatically place the charging order if anyone asks for one and it is up to the owner to challenge in the courts to get it removed - Fait accompli! Or is it? Please can anyone help with advice because looking for information on the forum and elsewhere it seems the way the Land Registry is presenting the information is along the lines of - Its already done and dusted and no chance mate in getting it removed if you have a CCJ, where I am reading that the is a timescale where you can challenge the interim order and there are grounds for a challenge such as there being other creditors whose claims would be unfairly denied (not sure that is necessarily a good way forward) and another one which is that we are in the process of getting divorced, with solicitors instructed, having lived apart for more than 4 years (I am not claiming anything but nevertheless it might be grounds to put a spanner in the works). Finally, are we worrying too much about it? I don't at all like the idea of them making unsecured into secured but as long as they don't move to repossess and the £100 a month agreement stays in force interest free should we twitch too much? Is that naïve? By the way if anyone is wondering why I am writing on behalf of my wife when we are getting divorced we are still friends/care/and although the debt is in her name it came about when we were together so is joint really anyway. Thanks in advance and time for your replies.

Hi, Be really really grateful for any guidance. Some years ago , -2007/8/9 we got into big debt trouble, lost our business and the only thing we were able to keep, amazingly, was a 1 bed flat in my wife's name which at the time didn't really have any equity in it so wasn't much point in selling. CAG helped enormously, RMA from Amex dropped amongst other things and over time most have stopped pursuing us. However while I know there are sadder stories out there than ours the stress added up and we also split up with my wife keeping and living in the 1 bed flat. In 2014 MBNA produced a CCJ against my wife for €14000 on a credit card she had back in 2002. She made an arrangement to pay £100+ per month and understood it was interest free etc, doesn't seem to have had paperwork on it. She has never missed a payment and the balance is now £11,000 odd. They only assets she has in the world is the flat (interest only mortgage but a low interest rate) - about £40k equity and next year at 65 she must retire from the NHS (4 years service won't amount to much). So, having got through everything she is in pieces having received a letter from the Land registry saying that they have placed an interim charging order on the flat in favour of Arrow for the £11,000 balance. The letter seems to read that they automatically place the charging order if anyone asks for one and it is up to the owner to challenge in the courts to get it removed - Fait accompli! Or is it? Please can anyone help with advice because looking for information on the forum and elsewhere it seems the way the Land Registry is presenting the information is along the lines of - Its already done and dusted and no chance mate in getting it removed if you have a CCJ, where I am reading that the is a timescale where you can challenge the interim order and there are grounds for a challenge such as there being other creditors whose claims would be unfairly denied (not sure that is necessarily a good way forward) and another one which is that we are in the process of getting divorced, with solicitors instructed, having lived apart for more than 4 years (I am not claiming anything but nevertheless it might be grounds to put a spanner in the works). Finally, are we worrying too much about it? I don't at all like the idea of them making unsecured into secured but as long as they don't move to repossess and the £100 a month agreement stays in force interest free should we twitch too much? Is that naïve? By the way if anyone is wondering why I am writing on behalf of my wife when we are getting divorced we are still friends/care/and although the debt is in her name it came about when we were together so is joint really anyway. Thanks in advance and time for your replies. -

Going through the process of remortgaging my old house, and a question has come up from the conveyancers about a charging order. The wording from the land registry is: "Equitable charge created by an order nisi of the Luton County Court dated 22 July 1996 in favour of American Express Europe Limited." I have a vague memory of once having an American Express card, it obviously must be that though a Companies House search for the company name has it ceasing to exist on the 12th June 1996, probably is the American Express and they just changed their name. Otherwise, I have no more information to go on. After a lot of searching and reading up on this site it must have been in respect of a CCJ that had been granted at some point, but in the intervening 21 years if there was any paperwork, it has long since vanished. The conveyancers say that they need to contact the placers of the charge and ask them if they are happy deferring payment of that charge, but will check with their 'technical team'. Any advice on how to proceed? Thanks!

Going through the process of remortgaging my old house, and a question has come up from the conveyancers about a charging order. The wording from the land registry is: "Equitable charge created by an order nisi of the Luton County Court dated 22 July 1996 in favour of American Express Europe Limited." I have a vague memory of once having an American Express card, it obviously must be that though a Companies House search for the company name has it ceasing to exist on the 12th June 1996, probably is the American Express and they just changed their name. Otherwise, I have no more information to go on. After a lot of searching and reading up on this site it must have been in respect of a CCJ that had been granted at some point, but in the intervening 21 years if there was any paperwork, it has long since vanished. The conveyancers say that they need to contact the placers of the charge and ask them if they are happy deferring payment of that charge, but will check with their 'technical team'. Any advice on how to proceed? Thanks! -

Hi, It's a bit of a complicated issue, but I'll try to keep it concise. It's relating to my partners BC account, for which he put his head in the sand until 2014 as he assumed PayPlan had 'sorted it all out', since starting a DMP in mid 2006. I took over the issue in 2015, helping him, as we discovered BC failed to default the account in 2006 (and where still trashing his CRA files). The journey since has been frustrating to say the least.... ...I use 'I' in this context as I have been writing the letters etc on his behalf to try to get this sorted. I have a complaint with FOS, re Barclaycard failing to default a CC account in 2006 and adding interest between 2007-2016, at times as much as 17.9% whilst on a DMP. I raised complaint with BC in Early 2016, raising with FOS 6 months later (in time), BC refused to default account, and referred me to the FOS. FOS have now stated its both out of time, ie more than 6 years ago (only by BC using this as an excuse to stop the FOS investigation), and secondly the FOS adjudicator has stated it is fair, and in BC T&C that interest can be charged after the account is cancelled, as per T&C. ...my problem is that in 2 CCA requests no terms have ever been provided, the one copy I did receive with my DSAR does not reference interest under the section number the FOS states, oh and the FOS has actually failed to include a copy of the terms they are referencing! I intend to escalate to an Ombudsman, but need a little advice beforehand. My Q is: When a credit card is cancelled, by the creditor for the cause of 'my failure to meet minimum contractual repayments' (for 5 months), does this deem the contract to be terminated and thus no longer valid. Ie can BC legally charge interest if they have withdrawn credit facilities and 'cancelled' the account? (There are internal BC notes from DSAR which state account is closed in 2006) I always thought that when closing the account, withdrawing the card and stopping PPI etc then he contract was finished and interest could not be charged. (Oh and defaulted which is my main complaint to BC, the interest being charged is the second part of the complaint as I think this falls also under unfair treatment). History below: In summary, in 2006 default notice, not complied with (was in considerable financial difficulty), received a letter from BC stopping PPI as the account was cancelled. All credit facilities were revoked. DMP with Payplan started FIVE weeks after account cancelled. Then a 2nd default notice issued, after the first DMP payment, but before DMP accepted by BC . This too expired before BC accepted DMP. For one year interest was stopped, but then failed on 2 DMP payments , only managing a partial payment for both, in 2007. (DMP temporarily failed due to bullying from another creditor to make more payments to them outside of DMP!). Interest was restarted and never stopped despite numerous letters from PayPlan request that it is stopped - all letters were ignored. Between 2007 - 2016 made regular payments, and in Sept 2016 managed to pay off the remaining balance with a small PPI Claim received from another company. Between 2006-2014 buried head in the sand assuming PayPlan were working in best interests. Also assumed BC account was defaulted, all the others out of 13 creditors were defaulted between 2006-2009. In 2014/2015 realised both that BC was not defaulted and that wouldn't be getting the interest 'refunded' upon completion of DMP ( as promised by PayPlan - unfortunately only verbally!). This is when I intervened eventually leading to this Formal complaint to BC. any advice before I reject the ajudicators decision would be great. Me_too

Hi, It's a bit of a complicated issue, but I'll try to keep it concise. It's relating to my partners BC account, for which he put his head in the sand until 2014 as he assumed PayPlan had 'sorted it all out', since starting a DMP in mid 2006. I took over the issue in 2015, helping him, as we discovered BC failed to default the account in 2006 (and where still trashing his CRA files). The journey since has been frustrating to say the least.... ...I use 'I' in this context as I have been writing the letters etc on his behalf to try to get this sorted. I have a complaint with FOS, re Barclaycard failing to default a CC account in 2006 and adding interest between 2007-2016, at times as much as 17.9% whilst on a DMP. I raised complaint with BC in Early 2016, raising with FOS 6 months later (in time), BC refused to default account, and referred me to the FOS. FOS have now stated its both out of time, ie more than 6 years ago (only by BC using this as an excuse to stop the FOS investigation), and secondly the FOS adjudicator has stated it is fair, and in BC T&C that interest can be charged after the account is cancelled, as per T&C. ...my problem is that in 2 CCA requests no terms have ever been provided, the one copy I did receive with my DSAR does not reference interest under the section number the FOS states, oh and the FOS has actually failed to include a copy of the terms they are referencing! I intend to escalate to an Ombudsman, but need a little advice beforehand. My Q is: When a credit card is cancelled, by the creditor for the cause of 'my failure to meet minimum contractual repayments' (for 5 months), does this deem the contract to be terminated and thus no longer valid. Ie can BC legally charge interest if they have withdrawn credit facilities and 'cancelled' the account? (There are internal BC notes from DSAR which state account is closed in 2006) I always thought that when closing the account, withdrawing the card and stopping PPI etc then he contract was finished and interest could not be charged. (Oh and defaulted which is my main complaint to BC, the interest being charged is the second part of the complaint as I think this falls also under unfair treatment). History below: In summary, in 2006 default notice, not complied with (was in considerable financial difficulty), received a letter from BC stopping PPI as the account was cancelled. All credit facilities were revoked. DMP with Payplan started FIVE weeks after account cancelled. Then a 2nd default notice issued, after the first DMP payment, but before DMP accepted by BC . This too expired before BC accepted DMP. For one year interest was stopped, but then failed on 2 DMP payments , only managing a partial payment for both, in 2007. (DMP temporarily failed due to bullying from another creditor to make more payments to them outside of DMP!). Interest was restarted and never stopped despite numerous letters from PayPlan request that it is stopped - all letters were ignored. Between 2007 - 2016 made regular payments, and in Sept 2016 managed to pay off the remaining balance with a small PPI Claim received from another company. Between 2006-2014 buried head in the sand assuming PayPlan were working in best interests. Also assumed BC account was defaulted, all the others out of 13 creditors were defaulted between 2006-2009. In 2014/2015 realised both that BC was not defaulted and that wouldn't be getting the interest 'refunded' upon completion of DMP ( as promised by PayPlan - unfortunately only verbally!). This is when I intervened eventually leading to this Formal complaint to BC. any advice before I reject the ajudicators decision would be great. Me_too -

My partner has a bank loan which unfortunately due to the Recession and being self employed has been unable to make the monthly payments. Wrote to bank and they agreed monthly £1 payments till things picked up. They have asked for an update on finances and so we sent them a Personal Budget Sheet with a letter explaining that circumstances have not improved and this could be seen from my income and reduced expenditures sheet. They have written and said that because of excessive spending on my phone £45 per month and £250 per month for travel and vehicle costs that they cannot accept the £1 offering. How can this be so ridiculous. He has to use the phone to get any work and the fuel cost is only £60 ish pounds a week. This amount has to cover repairs on my 7 year old Van, RoadTax and Fuel which he obvioulsy has to spend in order to get to do the work as an Electrician. Any advice would be greatfully received ASAP PLEASE.

My partner has a bank loan which unfortunately due to the Recession and being self employed has been unable to make the monthly payments. Wrote to bank and they agreed monthly £1 payments till things picked up. They have asked for an update on finances and so we sent them a Personal Budget Sheet with a letter explaining that circumstances have not improved and this could be seen from my income and reduced expenditures sheet. They have written and said that because of excessive spending on my phone £45 per month and £250 per month for travel and vehicle costs that they cannot accept the £1 offering. How can this be so ridiculous. He has to use the phone to get any work and the fuel cost is only £60 ish pounds a week. This amount has to cover repairs on my 7 year old Van, RoadTax and Fuel which he obvioulsy has to spend in order to get to do the work as an Electrician. Any advice would be greatfully received ASAP PLEASE. -

Hi all! A long story short ( i have touched on it previously some time ago) im happy to expand on the details if you want. I have a charging order on my property, there is no CCJ and its not from a financial institution. Ex landlord who i rented a shop from and business collapsed. He wanted £15K from me i said no way so he got a charging order attahced in 2008. i paid a small amout of money each month but then stopped in 2009 and had last contact with him in 2010. Now he has suddenly had his solicitor write to me stating if i dont pay they will push for sale of the property. he wants £20K inc interest. even though he has a charge against my property is there a limitation on how long it can be chased? ie 6 years? i have heard that the court feels 6 years is enough time to chase? is this correct and would that tie in with why i have suddenly heard from the creditor? i thought there is a 12 year limitation on secured but would like clarification. There is no equity in the property - perhaps £5k but after fees etc there would be none so it seems pointless he is chasing all of a sudden? Is it a coincidence that its 6 years almost since last contact?? I have recently had a welcome charge removed from the property could they have looked and now think there is the equity available? there is no CCJ, im thinking maybe the order is interim? Help!!

-

hello, I do not know where to post this plea for help/advice. Recently dceided to sell my house & searches revealed a charge against my share in the property by CAPQUEST INVESTMENTS Ltd, I know this organisation has a reputation, from reading this site. I have lived in the property since 2004, still a small mortgage with GE Money I am pensioner so funds are restricted, any advice on how to establish what this charge relates to

-

.thumb.jpg.bf2f59e5260173230834ce3ad8015900.jpg) An interesting one that could end up with severe consequences if found out to be true.

An interesting one that could end up with severe consequences if found out to be true. -

Hi there, I have a problem with Hoover candy group and I don't know what to do . I bought a cooker/hob for my mother and within months it broke down. I called the engineer who came and said this hob is useless I will tell the company to sent a replacement. We waited and nothing came. When I called them they said the engineer has ordered a part when he told us you will get a replacement. We had to wait a month for the part(no cooker-no apologies). It was fixed after a month but the heat was really low. It broke down again nearly at the end of the year. The engineer came again(the same person) and after 5 minutes decided to leave and say the hob if fine. Now I keep receiving invoices from Hover Candy group of the amount of £64.50 for the call out even though the hob was still under manufactures warranty but the engineer is pretending the hob was fine and he was called for no reason and for that he is charging us the amount. I keep calling them to say that you need to come and inspect the hob as one of the plates is still not working and the rest are producing very low heat that you need at least two hours to make some pasta. I am at my end wits and i don't know what to do. Is there any suggestions? Anybody had the same issue? what do i do as i am not going to pay. Thank you in advance for taking the time to read my complaint.

Hi there, I have a problem with Hoover candy group and I don't know what to do . I bought a cooker/hob for my mother and within months it broke down. I called the engineer who came and said this hob is useless I will tell the company to sent a replacement. We waited and nothing came. When I called them they said the engineer has ordered a part when he told us you will get a replacement. We had to wait a month for the part(no cooker-no apologies). It was fixed after a month but the heat was really low. It broke down again nearly at the end of the year. The engineer came again(the same person) and after 5 minutes decided to leave and say the hob if fine. Now I keep receiving invoices from Hover Candy group of the amount of £64.50 for the call out even though the hob was still under manufactures warranty but the engineer is pretending the hob was fine and he was called for no reason and for that he is charging us the amount. I keep calling them to say that you need to come and inspect the hob as one of the plates is still not working and the rest are producing very low heat that you need at least two hours to make some pasta. I am at my end wits and i don't know what to do. Is there any suggestions? Anybody had the same issue? what do i do as i am not going to pay. Thank you in advance for taking the time to read my complaint. -

At the beginning of October I booked a one night stay at the Black Horse Hotel in Otley via Laterooms for the night of 15/10/2016 at a cost of £80. The terms of booking are payment on arrival and if you cancel less than two days before arrival you forfeit the cost of the first night’s stay. On 13/10/2016 a pending transaction of £80 showed up on my account On arrival at the hotel I was asked to pay, which I did. This resulted in a second pending transaction of £80 appearing on my account, which, when combined with the £80 from two days earlier reduced the available balance by a total of £160. Effectively, in terms of my available balance, what they’ve done is charged me a cancellation fee two days before I was booked in case I didn't show, charged me again for accommodation when I checked in but not refunded me the cancellation fee at the same time. The manager was unavailable at check-in I was assured they would be around in the morning. Unfortunately, in the morning, the manager refused to speak to me directly but said, via a member of staff that; it was just how the Laterooms did things, it wasn’t them that had taken the money, that it was security in case I didn’t turn up and that it didn’t matter because the money hadn’t left my account. Fortunately this hasn’t caused me any problems (at least not yet) because the balance in my account is high enough to cover both payments but I’m annoyed at being deprived of the ability to spend my own money and it certainly would have caused me problems if it had been nearer the end of the month. Leaving aside the dubious morality of the hotel’s behaviour have they actually done anything legally wrong or actionable? I suspect not because, when the transactions go through the £80 reserved on 13/10/2016 will be cancelled and I will have made no loss. The only thing perhaps is that, although on 13th it was certain that I was going to be liable to pay the hotel £80, either for accommodation if I turned up or cancellation if I didn’t, neither of those events could happen before 15th so it was only on 15th that my card should have been processed PendingTrans.pdf

At the beginning of October I booked a one night stay at the Black Horse Hotel in Otley via Laterooms for the night of 15/10/2016 at a cost of £80. The terms of booking are payment on arrival and if you cancel less than two days before arrival you forfeit the cost of the first night’s stay. On 13/10/2016 a pending transaction of £80 showed up on my account On arrival at the hotel I was asked to pay, which I did. This resulted in a second pending transaction of £80 appearing on my account, which, when combined with the £80 from two days earlier reduced the available balance by a total of £160. Effectively, in terms of my available balance, what they’ve done is charged me a cancellation fee two days before I was booked in case I didn't show, charged me again for accommodation when I checked in but not refunded me the cancellation fee at the same time. The manager was unavailable at check-in I was assured they would be around in the morning. Unfortunately, in the morning, the manager refused to speak to me directly but said, via a member of staff that; it was just how the Laterooms did things, it wasn’t them that had taken the money, that it was security in case I didn’t turn up and that it didn’t matter because the money hadn’t left my account. Fortunately this hasn’t caused me any problems (at least not yet) because the balance in my account is high enough to cover both payments but I’m annoyed at being deprived of the ability to spend my own money and it certainly would have caused me problems if it had been nearer the end of the month. Leaving aside the dubious morality of the hotel’s behaviour have they actually done anything legally wrong or actionable? I suspect not because, when the transactions go through the £80 reserved on 13/10/2016 will be cancelled and I will have made no loss. The only thing perhaps is that, although on 13th it was certain that I was going to be liable to pay the hotel £80, either for accommodation if I turned up or cancellation if I didn’t, neither of those events could happen before 15th so it was only on 15th that my card should have been processed PendingTrans.pdf -

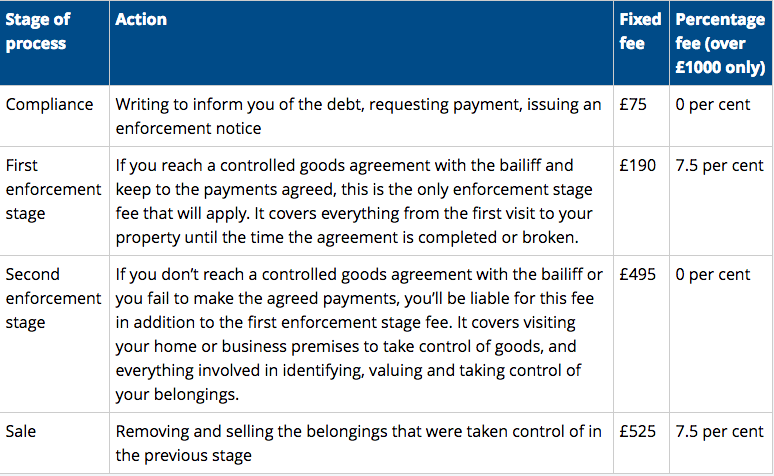

Hi all, I would really appreciate some advice. My business partner and I run a small business, and cashflow is very delicate. Some time ago we got in some money trouble and an invoice was sold to a debt recovery company. We managed to pay it off (or so we thought), but unfortunately my business partner is a bit scatternbrained with numbers, and paid the incorrect amount. The total outstanding debt was £5,723.96. My business partner sent them a transfer of £5,700, accidentally leaving off the £23.96. My business partner had some fees he wanted to dispute - The debt recovery company then sent a follow up email saying all prior fees are legitimate, and that "I have checked your account and can see we are still awaiting a payment of £23.96. I am assured this will be paid in due course, and this case can then be closed.". My business partner forgot to respond to the email (stupid, I know), and three weeks later (yesterday) they send a hired thug to our place of business, while customers were there, demanding the £23.96 plus a £1111.87 enforcement charge. He said that unless we paid that to him on the spot, he would confiscate goods that he valued to the sum of £8000. The £5,723.96 sum had a high court writ, which comes with a cap on fees of this nature that can be charged, as illustrated by the table below: The bailiff claimed to be able to charge for both stage two and three whether or not he actually had to carry out stage three. I pointed out that I was perfectly willing to pay the debt and the enforcement fee on the spot, which meant that he did not have the right to charge a "sale" enforcement fee, but he refused to drop it, saying I either pay exactly what he is demanding, or he starts ripping equipment out of the walls there and then. I had no choice but to pay the entire sum, and did so. There is no doubt in my mind that this is illegal and extortion, and in fact the bailiff himself used the very word "extortionate" when explaining the situation he was putting us in. My question to you is which regulatory body can I bring this to the attention of, are there any court cases setting a precedent in these situations, and are there guidelines that prevent bailiffs from charging huge bills for debts as low as £23? Even the £495 bill is entirely unfair, and clearly taking advantage of an admin error made by a small business. The law was not written to allow them to do this, and it puts our business at risk. Any advice on putting this right would be massively appreciated. Thanks a lot.

Hi all, I would really appreciate some advice. My business partner and I run a small business, and cashflow is very delicate. Some time ago we got in some money trouble and an invoice was sold to a debt recovery company. We managed to pay it off (or so we thought), but unfortunately my business partner is a bit scatternbrained with numbers, and paid the incorrect amount. The total outstanding debt was £5,723.96. My business partner sent them a transfer of £5,700, accidentally leaving off the £23.96. My business partner had some fees he wanted to dispute - The debt recovery company then sent a follow up email saying all prior fees are legitimate, and that "I have checked your account and can see we are still awaiting a payment of £23.96. I am assured this will be paid in due course, and this case can then be closed.". My business partner forgot to respond to the email (stupid, I know), and three weeks later (yesterday) they send a hired thug to our place of business, while customers were there, demanding the £23.96 plus a £1111.87 enforcement charge. He said that unless we paid that to him on the spot, he would confiscate goods that he valued to the sum of £8000. The £5,723.96 sum had a high court writ, which comes with a cap on fees of this nature that can be charged, as illustrated by the table below: The bailiff claimed to be able to charge for both stage two and three whether or not he actually had to carry out stage three. I pointed out that I was perfectly willing to pay the debt and the enforcement fee on the spot, which meant that he did not have the right to charge a "sale" enforcement fee, but he refused to drop it, saying I either pay exactly what he is demanding, or he starts ripping equipment out of the walls there and then. I had no choice but to pay the entire sum, and did so. There is no doubt in my mind that this is illegal and extortion, and in fact the bailiff himself used the very word "extortionate" when explaining the situation he was putting us in. My question to you is which regulatory body can I bring this to the attention of, are there any court cases setting a precedent in these situations, and are there guidelines that prevent bailiffs from charging huge bills for debts as low as £23? Even the £495 bill is entirely unfair, and clearly taking advantage of an admin error made by a small business. The law was not written to allow them to do this, and it puts our business at risk. Any advice on putting this right would be massively appreciated. Thanks a lot.

-

Good evening I am hoping somebody can help me with advise. My wife currently owns a house with her mum. Her mum moved out about 9 years ago when she remarried and instead of selling my wife went onto the mortgage and became 50% owner. they have had an offer on the house and are in the process of selling. The solicitor today rang to say we they aware of a charging order in mother in laws name. She didn't have a clue about it but so far has managed to find out the following: The DCA is Cabot. They have said that she needs to speak with the Solicitors 'Wright Hassall' (seems a really apt name!!!!) She contacted solicitors and they have said that the original debt was with Egg (apparently. Until MIL said she has never had an egg credit card, they mentioned two other potential creditors it could be) The charging order was on the 16/12/2013 for a fee of £6,113.25. The last payment (or default, she can't remember) on this account is 02/07/2007. The account balance was £5066.25 She has never had a credit card so obviously wants to dispute this in its entirety. She didn't live at the address the letters were sent to so was unaware of the judgements. I have told her that she needs to request a CCA from the solicitors etc. The problem is, the house sell. Obviously they don't want to pay this, but will not be able to sell the house if they dispute it. Can they dispute it retrospectively? really really really appreciate the advice given

Good evening I am hoping somebody can help me with advise. My wife currently owns a house with her mum. Her mum moved out about 9 years ago when she remarried and instead of selling my wife went onto the mortgage and became 50% owner. they have had an offer on the house and are in the process of selling. The solicitor today rang to say we they aware of a charging order in mother in laws name. She didn't have a clue about it but so far has managed to find out the following: The DCA is Cabot. They have said that she needs to speak with the Solicitors 'Wright Hassall' (seems a really apt name!!!!) She contacted solicitors and they have said that the original debt was with Egg (apparently. Until MIL said she has never had an egg credit card, they mentioned two other potential creditors it could be) The charging order was on the 16/12/2013 for a fee of £6,113.25. The last payment (or default, she can't remember) on this account is 02/07/2007. The account balance was £5066.25 She has never had a credit card so obviously wants to dispute this in its entirety. She didn't live at the address the letters were sent to so was unaware of the judgements. I have told her that she needs to request a CCA from the solicitors etc. The problem is, the house sell. Obviously they don't want to pay this, but will not be able to sell the house if they dispute it. Can they dispute it retrospectively? really really really appreciate the advice given -

I am currently trying to get information from Hillesden regarding a HP agreement I took out in 2001 with Associates Capital for a car. This agreement was taken over by Welcome Finance. Prior to this change I contacted Associates and told them I could no longer afford the car due to personal circumstances at the time, and asked them to collect as I had the car for 2 years which was half the HP agreement timescale. They never collected the car. I contacted Welcome after the change and told them the same, that I could no longer afford the car and to collect. Again they did not but wanted me to take out a new agreement with them to re-finance the car. I refused to do this. After checking my credit report, Hillesden Securities now 'own' this alleged debt. I checked my credit report last month and this account was defaulted as an HP agreement. This month, however, they have defaulted me for the same amount and changed the type of default to a loan account. Can they do this? Anyone? The information is lodged with Callcredit reference agency, on two other reference agency files it shows as a HP agreement. Please let me know what you think before I write to Callcredit and Hillesden

I am currently trying to get information from Hillesden regarding a HP agreement I took out in 2001 with Associates Capital for a car. This agreement was taken over by Welcome Finance. Prior to this change I contacted Associates and told them I could no longer afford the car due to personal circumstances at the time, and asked them to collect as I had the car for 2 years which was half the HP agreement timescale. They never collected the car. I contacted Welcome after the change and told them the same, that I could no longer afford the car and to collect. Again they did not but wanted me to take out a new agreement with them to re-finance the car. I refused to do this. After checking my credit report, Hillesden Securities now 'own' this alleged debt. I checked my credit report last month and this account was defaulted as an HP agreement. This month, however, they have defaulted me for the same amount and changed the type of default to a loan account. Can they do this? Anyone? The information is lodged with Callcredit reference agency, on two other reference agency files it shows as a HP agreement. Please let me know what you think before I write to Callcredit and Hillesden -

Hi, Had a letter today from DLC regarding an outstanding CCJ, in that letter they are stating that it is currently being enforced by way of a charging order. Now I've done a bit of research and it appears that they are stating they have a charging order against my property. The thing is I live in rented accomodation and havent had a mortgaged property of any sort since 2009, this is now owned by the local council who bought it following repossesion. My question is, are DLC being fraudulent by claiming a charging order exists or does one still exist at my old property. For reference the property was repossessed in 2009 the CCJ was September 2010 although I only became aware of the CCJ recently following a check of my credit file and have had no paperwork regarding it to date until this letter. They clearly have my current address as the letter was sent directly there and not forwarded, I have lived at two other addresses since 2009! So they are tracking my current details. The letter goes on to state they are putting the matter in the hands of Cabot financial and that their solicitors will be in contact with me regarding further enforcement. Question is 1) Do they have a charging order? 2) How can they enforce one if they do as I do not own any property. and 3) Do I do something about the issues if they are being dishonest? The CCJ will be off the records in September and although not statute barred I believe it is much more difficult to follow up/enforce once that date passes. Please correct me if i'm wrong. Any help would be greatly appreciated. Thanks

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS