francoe

-

Posts

243 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by francoe

-

Well I can understand what you are saying if we where quoting balances regarding interest. Quoting from the letter and all charges aside "Having calculated the balance that was with Black Horse (no balance figure quoted) I can confirm that you made payments totaling £22,2532.32(actual monies received regardless of when) Your agreement states that in order to to complete your obligation you are required to make a minimum amount of £25,053.40. If an arrears balance accrues on the account the total amount payable will adjust to reflect this as additional interest will become payable no mention of whether there was or that it did and no figure quoted)" I made my calculations based on original & copy statements to track payments made. I also last night went through all bank statements to cross check payments whether made by CHQ/DD or POS. My payment total amounts to sum of £22,832.32 , that is a difference of exactly £300.00. I found a payment made to Black Horse on the 15/12/2010 by POS. We can not talk about interest accruing on arrears until the wording of the letter is changed. Is this correct or am I getting something wrong? Thank you Sorry, edit to post The payment that was made on 15/12/2010 by POS was exactly £300.00 based on calculations Black Horse confirmed payments received £22,532.32 My actual payments made £22,832.32 there is a payment made by me from my bank which is missing of £300.00 as far as I understand thats before we start talking about balances

-

An update required after post from Nihilus I did not send out the LBA because of the reply I received from Black Horse(which is attached) I did not send LBA because of the wording of there reply but because it was close to resolving the issue of the fees. The only problem I need to resolve with Black Horse is the amount they say I have paid, up to the point of transfer to Skye loans as they have missed a payment.Once I have finalised the transferred balance I can then continue with Skye loans as this would make anything Skye Loans are quoting totally wrong. The outset of the original post was to get the charges refunded, the over payment and for a zero balance, account closed and finished with. So you see once I can resolve the missing payment issue and agree the transferred balance I can continue with Skye as Black Horse are only dealing with it up to the transfer point. Hope this make sense but I thought it was moving towards our aim. Thanks

-

Cheers for that Martin Letters on way then. Will update in a couple of weeks or sooner if I receive a reply

-

Unfortunately letter had to wait for me to get home. I have drafted LBA ready to post out tomorrow. the only question I have to ask is who am I sending it too, Black Horse or Skye. Reason for asking is that I received this letter yesterday. Thanks

-

Ok thanks Martin Back at work now so Mrs will have to type up & send Will post up update as soon as Thanks again

-

Hi Martin & all Nothing up since last post. 14 days finished on Wednesday just past. I need to get LBA sent could you possibly link me to a template if you are around.I Cant find it. Do not think I m lazy its just i dont have much time.I am a shopfitter by trade and my hours are very demanding leaving me very little time to sort things.I am home from London tonight & then have to leave for London again tomorrow at 5.30 ,a good 3 hr trip so could do with penning a letter tonight. Also regarding my previous post,I carry on with sending the LBA to Skye and completely ignore Black Horse. Thanks Rob

-

Thanks for the reply Martin. Will continue as is then. Will post up if anything does appear from Black Horse in the meantime. Thanks

-

As said a reply yesterday from Skye Loans This doesn't do much really except passing it back to Black Horse the original lender. How do I stand now with time lines and the like. Do I just wait for Black Horse or should I now be doing something else or do I take it that Skye hasn't really handled my complaint stick to the 14 day timeline and send an LBA. Thanks

-

OK Letter was away yesterday. Will post back when or if I receive a reply. Thanks for all help.

-

Ok thanks Martin But all reads ok with the way charges & interest have been written? This is my main concern that this is right from the start. Will amend FOS part & get this sent off Monday. Thanks again

-

Thanks for reply Martin I came across some old letters on a memory stick, could I merge this one with mine.In regards to the 14 day timeline and also the reference to the credit file? Apologies trying again Ok hows this read. Any alterations

-

ok martin wow quick reply. So I have to incorporate 14 day timeline.ok,will re-word that then. Is it correct otherwise? I mean,not including interest in the charges amount? Will re-word and re-post tomorrow. Thanks for quick reply

-

Ok I have managed to sit down and sort letter. Trying to fit this in between everything else. have attached my letter , how does this look? The total amount of charges is 597 + over payment of 278.26 making total of 875.26 CI is 629.22 based on the original loan agreement of 15.9% Making a total of 1504.48. As you will see I have not included the interest in my letter , is this correct?

-

ok thanks will re-word letter to suit.I am using the ci spread.If I come across anything else will ask. Thanks

-

Thanks also Martin I am trying to get this sorted today I have re-typed letter but I do have a few more questions which hopefully I can get posted today. Thanks Ok Just finally sat down to have a look at the spreadsheets. Right I believe I am to use the CIS Version for my claim. Fine. My be sounding like a plum here but where would I get the APR from a Black Statement or the original contract? Also referring back to my original post I have made an extra installment payment how does this fit into the equation? Just a few more things to iron out on the letter. 1.This was a joint account with my wife,do I word the letter in the plural, as I am doing the letters I keep using the singular. 2.The loan was originally taken with Black Horse and was a secured loan, Skye now call it a Mortgage.Do I use the word secured loan or mortgage 3.Do I send this letter to Black Horse(the original lender) or Skye Loans (the new owner) or both. Hopefully this is the last of my questions, may seem trivial but want to get this right from the start and get this letter sent out. Thanks for your replies and time. 3

-

-

Hi Further to post a letter received during the whilst away. As advised by Skye charges have been reassigned to capital.

-

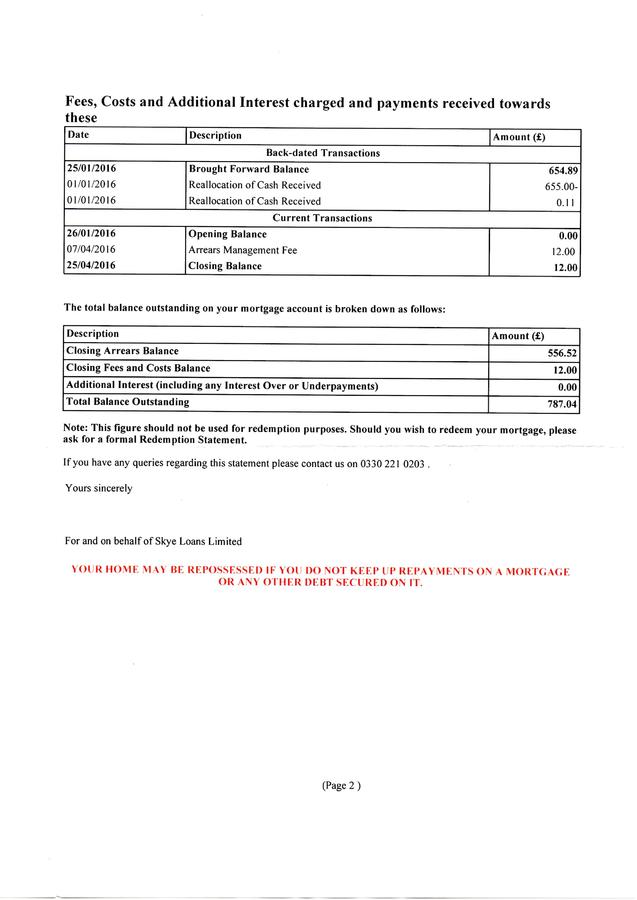

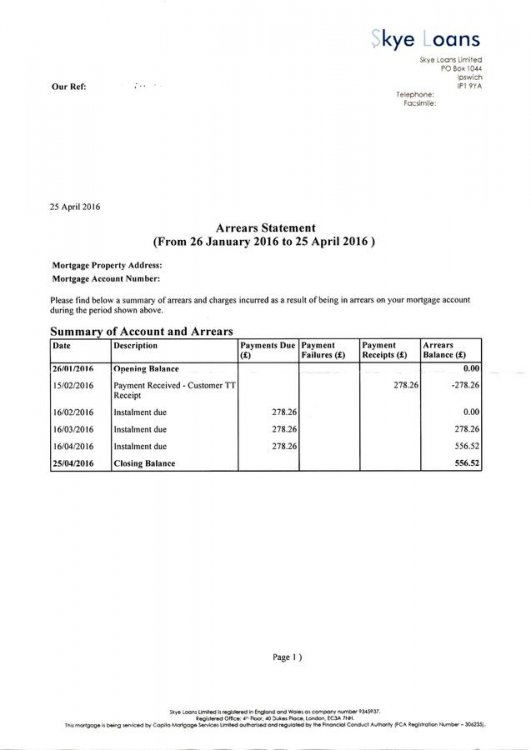

Hi I have recently finished paying a loan, originally with Black Horse now with Skye. I have made all contractual payments under this agreement. (well actually I overpaid by 1 instalment) 90 payments of 278.26 for agreement 91 payments of 278.26 made The balance of this account is now stands at 775.04 This amount derives from 15 charges of 25.00 & 7 charges of 30.00 A charge of 15.00 to change the date of the repayments. Also now a charge of 12.00 from Skye in March this year for an alleged instalment payment missed. All information is obtained from a SAR sent to Black Horse in February 2016. Skye took over receiving payments for this account in June 2015.At that point I had 7 payments to make, although due to a communication error with my other half 8 were made. All these payments made in full and on time. So as far as I was concerned this loan was finished, but was aware account had incurred charges during a bad period for us 2009-2011. I have never accepted these charges & made Black Horse aware of this & of our financial problems at that time hence paying for a date change in repayments to try and rectify problem but didn’t work & I continued to be charged. I have recently received a letter from Skye quoting that I have missed a payment of 278.26 in March and have subsequently been charged 12.00. Against better judgement a phoned Skye and asked how can I have missed payments when all contractual payments had been made +1. They hadn’t a clue what anything was as they had only received a balance figure from Black Horse & said they would look into it. Another telephone call to Skye now reveals that this balance is made up of charges & interest. Some of the interest occurred from the start of the loan (draw down of funds in July 2008 & the 1st installment being paid in August 2008) and it was then pointed out that the amount owed now 775.04 is now capital. I repeated that I did not agree with the charges and would not be paying them and that I would be taken action to reclaim these charges & would send a letter this weekend. The only problem is what letter would I use to address this situation, it’s been quite some time since I tackled anything like this & I know things have changed somewhat as regarding reclaiming charges. I spent a little time looking at COBS(unfairness) is this a route to take & do I take up this fight with the original lender as I have read a post from Bankfodder regarding all duties still remain with them even if sold on. The reason I ask this is Skye told me to deal only with them and not with Black Horse. I work away from home during the week and can only deal with this at the weekend and as we all know these amounts soon start to get out of control so I need to deal with this as quickly as possible. If any info is required I have all letters statements and telephone transcripts. Any information or guidance is much appreciated. Thanks

-

MBNA CC debt, sold to Hillies, DLC issued court papers

francoe replied to francoe's topic in Financial Legal Issues

Hi Just an update. Have opted for a settlement at 50%. So no court no charging order debt gone.I consider this a victory others may not. A victory as we never denied the debt. Any way i have received a letter stating accepting my offer in full & final settlement of this matter. The only thing i am not sure about is that it is headed "Without Prejudice save As To Costs" I have found an explanation on net & it refers to what is known as a CalderBank Letter. So i am asking, if i make the payment i am not leaving myself open to any further action. Thanks R -

MBNA CC debt, sold to Hillies, DLC issued court papers

francoe replied to francoe's topic in Financial Legal Issues

Hi Andy Ah well this is where are defence will flaw.Way back in 2009 after getting trouble we were advised by cccs to what ever you do keep paying regular monthly payments.We were green. MBNA said in above posted letter to pay dlc/dtl at that address.Not wanting to miss a monthly payment we posted cheque with giro slip to dlc & continued to do so. We didnt actually receive a NOA from dlc whether this means anything. I have had NOA from other debtors last year that seem to be very informative. Oh well.Thinking we were doing the right thing by keeping regular payments it would appear we have hung ourselves. Another lesson learned.Dont pay. Thanks -

MBNA CC debt, sold to Hillies, DLC issued court papers

francoe replied to francoe's topic in Financial Legal Issues

Forgot the letter template that was used for the NOA. Why have they not sent a copy of the letter.Does this mean anything? Thanks -

MBNA CC debt, sold to Hillies, DLC issued court papers

francoe replied to francoe's topic in Financial Legal Issues

Hi cb We are in between posts i was busy typing but thats exactly right but at the time i went with what i was told to do.MBNA told me to pay dlc/dtl at that address.So i did. -

MBNA CC debt, sold to Hillies, DLC issued court papers

francoe replied to francoe's topic in Financial Legal Issues

Ok So reverting back to their covering letter They have sent me 1.A copy of the agreement (posted in previous posts) 2.T& C s from a period when account was defaulted (not when account was requested) 3.A default notice. 4.A notice of assignment TEMPLATE. 5.Statements from MBNA 6.Statement of account showing payments following assignment.(see attachment/date) So my interest lies in the notice of assignment.Why a template letter an not with all information?(see attachment) As i imagine, if i said i did not receive a noa why did i start paying dlc? Well after instruction from MBNA (see attachment) but is this a notice of assignment?Note date. And then a letter from dlc. Apart from the question of the agreement being enforceable l i feel this case lies in the assignment or am i totally wrong. I believe this will go to court & need to have my house in order. Hi Andy any advice! -

MBNA CC debt, sold to Hillies, DLC issued court papers

francoe replied to francoe's topic in Financial Legal Issues

Hi again Back from a break with DLC. Right just an update as DLC have decided to answer my defence that was filed in November 2013. I have attached a copy of the cover letter which outlines there intention along with supplying me with copies of alot of paperwork which dosnt really mean much.Except possibly one. Just to recap the claim was thus 1.The Claiments Claim is in respect of a credit facility xxxxxxxxxxxx,provided by MBNA at the defendants request on the xxxxxx 2.Failure to meet requests for payment resulted in the account being defaulted. 3.On xx/xx/xxxx, all legal and beneficial interest for the monies was assigned to hillesden securities ltd. 4.The defendant was duly notified in writing of the assignment and that a balance of xxxx.xx was due. 5.The balance of xxxx.xx remains owing from the defendant. My defence was thus Paragraph 1 is admitted in regards to entering into an agreement with MBNA for a credit facility. Paragraph 2 is denied as MBNA did not serve Default Notice. Paragraph 3/4/5 are denied as yet the claimant has failed to serve a Notice of Assignment in accordance with s136 Law of Property act 1925 and therefore yet to prove they are entitled to bring this claim. On receipt of this claim i requested a section 78 request from the claimant dated xx/xx/xxxx sent recorded delivery & signed for on the xx/xx/xxxx. The claimant has yet to reply. Therefore the claimant is put to strict proof to: (a) Show how the defendant has entered into an agrrement with the claimant; and (b) Show how the defendant has reached the amount claimed for; and © Show how the claimant has the legal right,either under statute or equity to issue a claim. As per civil procedure rule 16.5(4),it is expected that the claimant prove the allegation that the money is owed. On the alternative, if the claimant is an assignee of a debt, it is denied that the claimant has the right to lay a claim due to contraventions of section 136 of the law of property act and section 82a of the consumer credit act 1974. Until such the claimant can comply with my request for a copy of the agreement/default notice it relies upon, they are prevented from enforcing or requesting any relief as pursuant to the cca 1974. By reason of the facts and matters set out above,it is denied that the claimant is entitled to the relief claimed or any relief. So here is their response. -

MBNA CC debt, sold to Hillies, DLC issued court papers

francoe replied to francoe's topic in Financial Legal Issues

Cheers Andy Thanks for all your advice. Your av would suggest you are looking much better now! Cheers R