Search the Community

Showing results for tags 'sar'.

-

I had been with Natwest for 22 years and had a black account with the Gold Advantage Charge card. I was advised to become a company as I would be delivering a service through several agencies. Unfortunately, due to exceptional circumstances and include a bad personal relationship left me in debt and I am about £8 -9k in mortgage arrears on a house I rent out and a personal overdraft that was £12k. In 6 months that OD was cleared and both business and personal accounts were in the black. The difficulty in meeting the mortgage department for an arrangement to be put in place was mainly because this period was over the summer, they would meet with me after 5pm and if I called at 4.45 they would not deal with me. I sent in 2 income/expenditure spreadsheets but they clearly didnt see them but I managed to set up a DD for the mortgage online and I met the deadline. That evening all three of my accounts were closed. I called the callcentre and they said they didnt have me on record. I tried to log a complaint and they were too busy on the Friday but promised they would be in touch the next day. They never did. As a prelude they stopped my access to online banking even though there was no way of spending money or transferring out into other accounts so it made knowing where I was financially and who had paid me and hadnt. The worst thing is that I couldnt operate, I need supplies, sundries and I was without any money to buy food or even some milk. I told Natwest this but they told me all my funds were transferred into the mortgage. It took a further 3 months to work out what had happened and the cause was not offered to me by the bank whose level of investigation was looking at the screen in front of them whilst on the phone. They hadnt cancelled the previous direct debit so every month the original arrangement would draw funds then the older previously arranged dd would be rejected. This was recorded as a default. I tried to make it clear to them there was an arrangement in place, it utilised a payment system set up and approved by the bank and it was their job to find out where the money was disappearing to every month for three months instead they left it to me. I complained about being oushed further into hardship by continued charges I had no way of keeping track of as the online facility had been taken away four months before they closed me down, failed to log 6 out of 8 attempts to complain and didnt care that I had not a penny for two weeks. They tried to issue a repossesion order and I wrote in to the lawyer to say that was illegal as the account was under dispute. In the meantime, I asked for SAR to get all the account information and after three months all I have is mortgage account copies. The lawyers are now calling me and I am sure its about instructing me to pay the arrears within the week or they would issue a repossession order on the house. They cancelled the direct debit that existed so I was conscious to keep puttting funds in every month but trying to function without a bank account lost me more money and irretrievably lost more clients. I am expecting a lump sum of money that will clear the arrears but the knock on effect meant that I was late paying my suppliers and one has taken a county court judgement out against me and bankruptcy is where I am at if I dont have some means of a reprieve. Yes, they said that if i didnt have an arrangement in place my account woud be closed and they talked about recovery. Sounded to me it was going to get better! The arrears werent as much as my overdraft which i cleared in less than 6 months and they had said the the charge card was a different legal entity and when I called the credit card company customer services before they closed my accounts they said that there wasnt any money owed and that it would be fully operational once the mortgage arrangement was in place. That wasn't true and I also lost my 36,000 reward points as I had no online access and frankly more serious things to worry about. i cant really afford a litigation lawyer at the moment and have little faith in the FSA from what I am reading. The banks replies to my complaints are to issues that weren't raised and they have not taken notice of my plea to allow me access to funds I had to eat and drink. I was not notified clearly that every account would be closed down and as far as I am concerned there was an arrangement in place that obviously isnt integrated into the RBS network as they couldn't see that the money had been taken from the holding account and HSBC provided a fast pay reference number. You cannot open another bank account if you have mortgage arrears is what every other bank told me but once I called the Business Debtline they advised me to walk into a bank and ask to open an account. Why didnt the other banks suggest this to me? A week after submitting an application form for a Cashminder account with the coop was i able to restart rebuiding what Natwest pulled down.

I had been with Natwest for 22 years and had a black account with the Gold Advantage Charge card. I was advised to become a company as I would be delivering a service through several agencies. Unfortunately, due to exceptional circumstances and include a bad personal relationship left me in debt and I am about £8 -9k in mortgage arrears on a house I rent out and a personal overdraft that was £12k. In 6 months that OD was cleared and both business and personal accounts were in the black. The difficulty in meeting the mortgage department for an arrangement to be put in place was mainly because this period was over the summer, they would meet with me after 5pm and if I called at 4.45 they would not deal with me. I sent in 2 income/expenditure spreadsheets but they clearly didnt see them but I managed to set up a DD for the mortgage online and I met the deadline. That evening all three of my accounts were closed. I called the callcentre and they said they didnt have me on record. I tried to log a complaint and they were too busy on the Friday but promised they would be in touch the next day. They never did. As a prelude they stopped my access to online banking even though there was no way of spending money or transferring out into other accounts so it made knowing where I was financially and who had paid me and hadnt. The worst thing is that I couldnt operate, I need supplies, sundries and I was without any money to buy food or even some milk. I told Natwest this but they told me all my funds were transferred into the mortgage. It took a further 3 months to work out what had happened and the cause was not offered to me by the bank whose level of investigation was looking at the screen in front of them whilst on the phone. They hadnt cancelled the previous direct debit so every month the original arrangement would draw funds then the older previously arranged dd would be rejected. This was recorded as a default. I tried to make it clear to them there was an arrangement in place, it utilised a payment system set up and approved by the bank and it was their job to find out where the money was disappearing to every month for three months instead they left it to me. I complained about being oushed further into hardship by continued charges I had no way of keeping track of as the online facility had been taken away four months before they closed me down, failed to log 6 out of 8 attempts to complain and didnt care that I had not a penny for two weeks. They tried to issue a repossesion order and I wrote in to the lawyer to say that was illegal as the account was under dispute. In the meantime, I asked for SAR to get all the account information and after three months all I have is mortgage account copies. The lawyers are now calling me and I am sure its about instructing me to pay the arrears within the week or they would issue a repossession order on the house. They cancelled the direct debit that existed so I was conscious to keep puttting funds in every month but trying to function without a bank account lost me more money and irretrievably lost more clients. I am expecting a lump sum of money that will clear the arrears but the knock on effect meant that I was late paying my suppliers and one has taken a county court judgement out against me and bankruptcy is where I am at if I dont have some means of a reprieve. Yes, they said that if i didnt have an arrangement in place my account woud be closed and they talked about recovery. Sounded to me it was going to get better! The arrears werent as much as my overdraft which i cleared in less than 6 months and they had said the the charge card was a different legal entity and when I called the credit card company customer services before they closed my accounts they said that there wasnt any money owed and that it would be fully operational once the mortgage arrangement was in place. That wasn't true and I also lost my 36,000 reward points as I had no online access and frankly more serious things to worry about. i cant really afford a litigation lawyer at the moment and have little faith in the FSA from what I am reading. The banks replies to my complaints are to issues that weren't raised and they have not taken notice of my plea to allow me access to funds I had to eat and drink. I was not notified clearly that every account would be closed down and as far as I am concerned there was an arrangement in place that obviously isnt integrated into the RBS network as they couldn't see that the money had been taken from the holding account and HSBC provided a fast pay reference number. You cannot open another bank account if you have mortgage arrears is what every other bank told me but once I called the Business Debtline they advised me to walk into a bank and ask to open an account. Why didnt the other banks suggest this to me? A week after submitting an application form for a Cashminder account with the coop was i able to restart rebuiding what Natwest pulled down. -

Hi all, Sorry for this but where is the appropriate sub-forum for BT complaints?

Hi all, Sorry for this but where is the appropriate sub-forum for BT complaints? -

The Barclays account in particular is dated 2000 . I have read that many of the agreements dated as far back as then do not have enough terms and conditions on the credit agreement and it is by a long way the most uncomprehensive agreement i have seen . Outside of that clutching at straws to be honest , like i said i would have settled them for her had they been able to meet me at a slightly lower per centage but my understanding is link are less likely to negotiate downwards than others.

The Barclays account in particular is dated 2000 . I have read that many of the agreements dated as far back as then do not have enough terms and conditions on the credit agreement and it is by a long way the most uncomprehensive agreement i have seen . Outside of that clutching at straws to be honest , like i said i would have settled them for her had they been able to meet me at a slightly lower per centage but my understanding is link are less likely to negotiate downwards than others. -

Today my gf has had back two letters, one from Mint & the other from Natwest after requests for CCA (mint) and SAR request with Natwest. Mint have stated the following: Does this mean I would also be unable to request SAR from Mint & reclaim PPI charges? As for Natwest, they have asked her to sign a form, provide evidence of identification "certified by a member of staff at any branch or a solicitor!" & "As the purpose of your request is unclear, we require some further information from you to help clarify what you are looking for" Are they for real? She'd have to take a day off work to be able to goto the bank just to get the ID authorised. I used the template letter from here & quoted 4 Credit Card account numbers and an insurance policy number.

Today my gf has had back two letters, one from Mint & the other from Natwest after requests for CCA (mint) and SAR request with Natwest. Mint have stated the following: Does this mean I would also be unable to request SAR from Mint & reclaim PPI charges? As for Natwest, they have asked her to sign a form, provide evidence of identification "certified by a member of staff at any branch or a solicitor!" & "As the purpose of your request is unclear, we require some further information from you to help clarify what you are looking for" Are they for real? She'd have to take a day off work to be able to goto the bank just to get the ID authorised. I used the template letter from here & quoted 4 Credit Card account numbers and an insurance policy number. -

Hi, I'm in a regulated tenancy. The rent's just gone up. The council, who pay my rent (I was on ESA in the SG long term, now I'm on GPC), are now complaining they overpaid on the old rent. They are threatening to suspend my HB claim or get the alleged overpayments back, presumably by underpaying the existing rent till they think we're square. They aren't offering any evidence of overpayment, however. My landlords, who have contacted them about this by email and ccd me on it, say the council always have been and are paying the correct rent, and have briefly broken down how the rent is arrived at for them. The council refuse to accept their figures and insist they've been overpaying. I want to see evidence of what they've been paying so I'd like to do a SAR; to whom should I address it please? I have the details of the head of housing benefit and they'd seem to be the right person. Perhaps you could either confirm that or make a better suggestion? Many thanks, SWLABR

Hi, I'm in a regulated tenancy. The rent's just gone up. The council, who pay my rent (I was on ESA in the SG long term, now I'm on GPC), are now complaining they overpaid on the old rent. They are threatening to suspend my HB claim or get the alleged overpayments back, presumably by underpaying the existing rent till they think we're square. They aren't offering any evidence of overpayment, however. My landlords, who have contacted them about this by email and ccd me on it, say the council always have been and are paying the correct rent, and have briefly broken down how the rent is arrived at for them. The council refuse to accept their figures and insist they've been overpaying. I want to see evidence of what they've been paying so I'd like to do a SAR; to whom should I address it please? I have the details of the head of housing benefit and they'd seem to be the right person. Perhaps you could either confirm that or make a better suggestion? Many thanks, SWLABR -

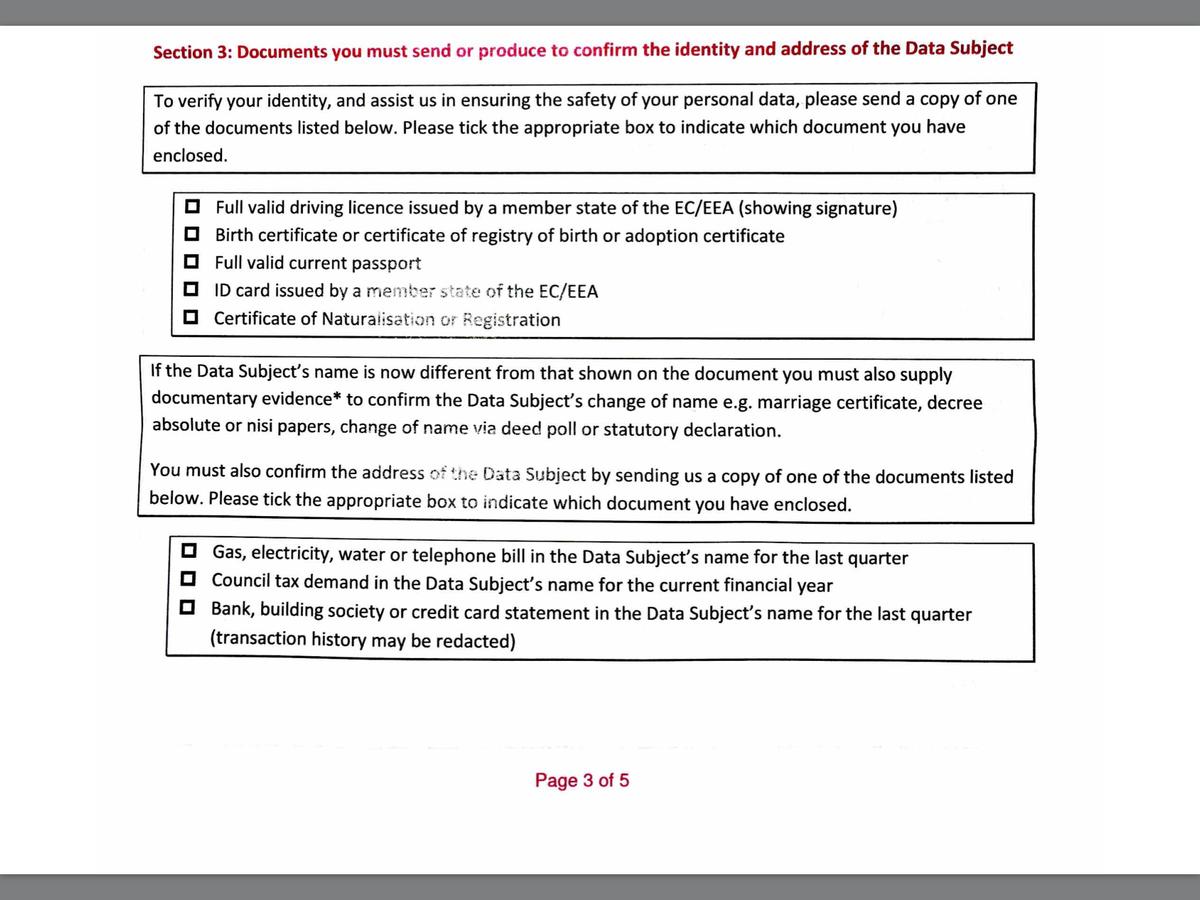

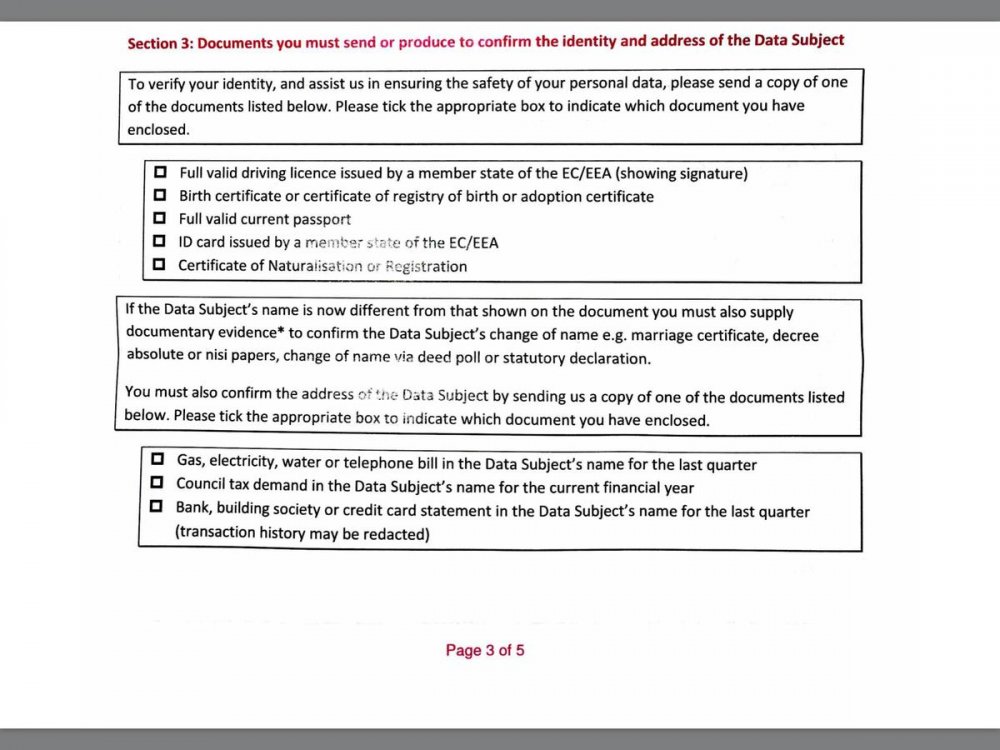

I've just sent off (with the £10 postal order) a Formal DSAR request to 1st Crud. All info required to be supplied, including a signature was provided in my formal and detailed letter. I've just received one of their 'please fill out this 5 page form' before we are obliged to do anything, however I'm not happy with what they are requesting I provide. There is no way I am ever going to provide them a copy of my driving licence, or bank statements and I'm back on here for some advice. I've been completing DSAR requests for approx 10 years, and apart from (almost) starting legal action with BC whilst some have been a struggle to get all info from and in a timely manner most have been compliant and not made me jump through too many hoops. (Oh apart from the DWP completely ignoring me for over 2 months! Still ongoing - but I class them in a different category to the CC companies and DCAs etc). Have the rules changed? I am now legally obliged to provide any of the following on the attached picture? Considering I've lived at the same address for over 10 years, and they've contacted me for 3-4 different companies at this same address, and threatened legal action to me at the same address, and supplied alleged CCA agreements, I would think that they should be fairly confident of my identity? Can I take this route, or will they likely play up and delay provision even though I don't (I think) have to legally provide the documents they have requested I send? Thanks ME_TOO

I've just sent off (with the £10 postal order) a Formal DSAR request to 1st Crud. All info required to be supplied, including a signature was provided in my formal and detailed letter. I've just received one of their 'please fill out this 5 page form' before we are obliged to do anything, however I'm not happy with what they are requesting I provide. There is no way I am ever going to provide them a copy of my driving licence, or bank statements and I'm back on here for some advice. I've been completing DSAR requests for approx 10 years, and apart from (almost) starting legal action with BC whilst some have been a struggle to get all info from and in a timely manner most have been compliant and not made me jump through too many hoops. (Oh apart from the DWP completely ignoring me for over 2 months! Still ongoing - but I class them in a different category to the CC companies and DCAs etc). Have the rules changed? I am now legally obliged to provide any of the following on the attached picture? Considering I've lived at the same address for over 10 years, and they've contacted me for 3-4 different companies at this same address, and threatened legal action to me at the same address, and supplied alleged CCA agreements, I would think that they should be fairly confident of my identity? Can I take this route, or will they likely play up and delay provision even though I don't (I think) have to legally provide the documents they have requested I send? Thanks ME_TOO

-

A while ago we had HMRC chasing us for a Tax Credit over-payment. We paid it in the end to get them off our backs but I still suspect there was a mistake made somewhere. I'm not looking for help on this one but I thought folks might like to know that there is an online SAR form on the HMRC website... https://www.gov.uk/guidance/hmrc-subject-access-request Here's the acknowledgement: Thank you for your email. We will process your Subject Access Request (SAR) as soon as we can. I should explain that under the terms of the Data Protection Act we have 40 calendar days to deal with this SAR. For further information on this please go to: www.hmrc.gov.uk/freedom/foi-01.htm If you have any further queries please write to: Freedom of Information Unit, 100 Parliament Street, London, SW1A 2BQ. I'll let you know how I get on.

-

I am about to send a SAR to a health insurance Company who have prevaricated, back tracked on their agreement and generally caused unneccessary pain and anxiety before during and after an operation. Should I be able to get details of conversations, messages etc between the surgeons dealing with the Insurance company or just communications between the Company and me? It would help if I knew what to expect to get from them.

I am about to send a SAR to a health insurance Company who have prevaricated, back tracked on their agreement and generally caused unneccessary pain and anxiety before during and after an operation. Should I be able to get details of conversations, messages etc between the surgeons dealing with the Insurance company or just communications between the Company and me? It would help if I knew what to expect to get from them. -

Hi I sent a SAR to Halifax on 13th December but have so far received no reply. Is it advisable to send them a letter regarding this? Other creditors were sent SAR's the same time and I have received them. Many thanks

-

Hello All I made this SAR request to the Energy Ombudsman (E-O) as I wanted to see what Npower submitted to them as evidence to back up their response to my complaint with them. Npower are reknowned for saying they have done everything correctly but not substantiating anything with hard evidence. My questions are: 1) There are some emails between Npower and the E-O where the NPower's persons details (name number email etc) have been redacted. Is this permitted? Why? 2) The E-O hasn't sent me any evidence from Npower to substantiate their response to my complaint (but they did include the emails I sent them as evidence) . Should they withhold this from me in SAR request? As this was the purpose of me making the request in the first place. 3) Can I do anything about the above to get the info I was after in the first place? Many thanks in advance Jimbo

Hello All I made this SAR request to the Energy Ombudsman (E-O) as I wanted to see what Npower submitted to them as evidence to back up their response to my complaint with them. Npower are reknowned for saying they have done everything correctly but not substantiating anything with hard evidence. My questions are: 1) There are some emails between Npower and the E-O where the NPower's persons details (name number email etc) have been redacted. Is this permitted? Why? 2) The E-O hasn't sent me any evidence from Npower to substantiate their response to my complaint (but they did include the emails I sent them as evidence) . Should they withhold this from me in SAR request? As this was the purpose of me making the request in the first place. 3) Can I do anything about the above to get the info I was after in the first place? Many thanks in advance Jimbo -

I know that my telecommunications provider has been overcharging me but not by how much and over what period (they acknowledge as much but are being awkward in (not) helping me arrive at the amount they have overcharged, for me to reclaim and have said they will arrive at "an arbitrary sum" of their own if I am unable to provide them with full details of dates and amounts). So I sent them a properly worded SAR but they have replied with an in-house "SUBJECT ACCESS REQUEST FORM" for me to fill in (which suggests they receive a few requests) and told me I must return it to their "Legal Team", directly. 1) Do I have to complete their form or can I insist they respond to my formal SAR, as already provided to them? 2) Is it for me to approach their legal team or is it for them to pass the request over to it? Thanks in advance for any help and advice.

-

I need some advice as to what I should do... here are the details of my situation. I purchased in to a property scheme run by a vendor in Nov 2008 , where you pay the vendor £2000 and for this they find a buy to let property for you where the rent covers the mortgage payment , the vendor takes care of the purchase of the property, they take care of the solicitor, all the management, (renting, any bills) all bills after two years you have the option to sell the property or to continue to use their services. The Solicitor used was in this with the vendor, the valuation from the surveyor showed that the property was worth more than what I was paying After three months after purchasing the property, the rents stopped coming in I started to chase the vendor who told me they were having some cash flow problems and I will get the rents to cover the mortgage, this went on for a two to three months and soon the vendor had disappeared. I visited the property I had purchased and asked the tenant for the rent and to pay me directly, and found out that that the rent came very short of the monthly mortgage payment , I got a local estate to come and value the property and they valued it less than £120K of the purchase price. I went to the police and told them about this, they said there is nothing they can do as this is a civil case I then instructed a solicitor to investigate and their findings showed that the property was bought and sold in a very short period less than a month, where the price sold at was over inflated by 120k, without any work done to the property. I told the mortgage company and told them there is no way I can afford the to pay the mortgage, this was around June 2009, The mortgage company repossessed the property and sold it in 2010, this is where the shortfall of 110K is. The conveyancing solicitor was part of a fraud, the solicitor is now no longer around, they were an LLP and I have tried to take them to court and sue them and claim damages from their indemnity insurance, but the indemnity insurers have said they will not cover this as this was a fraudulent act intentionally done by the solicitor. Now the bank has passed the debt to a number of debt collectors , this is the third one who is contacting me. To make things even worse, at the time, back in 2008 I actually bought three properties via this vendor, so I actually have three mortgage shortfalls that I need to deal with. I have been living with a lot of stress ever since this has happened, it is really getting me down, has affected my whole life, mentally, physically, affecting my family. I feel I have been let down by the whole system, I purchased these properties in good faith, thinking this will be an investment for the future but in reality it has been nothing but a nightmare. I need to find out what I can do to stop the debt or not pay the shortfall the debt collectors are asking for. Can anyone help and point me in the right direction

I need some advice as to what I should do... here are the details of my situation. I purchased in to a property scheme run by a vendor in Nov 2008 , where you pay the vendor £2000 and for this they find a buy to let property for you where the rent covers the mortgage payment , the vendor takes care of the purchase of the property, they take care of the solicitor, all the management, (renting, any bills) all bills after two years you have the option to sell the property or to continue to use their services. The Solicitor used was in this with the vendor, the valuation from the surveyor showed that the property was worth more than what I was paying After three months after purchasing the property, the rents stopped coming in I started to chase the vendor who told me they were having some cash flow problems and I will get the rents to cover the mortgage, this went on for a two to three months and soon the vendor had disappeared. I visited the property I had purchased and asked the tenant for the rent and to pay me directly, and found out that that the rent came very short of the monthly mortgage payment , I got a local estate to come and value the property and they valued it less than £120K of the purchase price. I went to the police and told them about this, they said there is nothing they can do as this is a civil case I then instructed a solicitor to investigate and their findings showed that the property was bought and sold in a very short period less than a month, where the price sold at was over inflated by 120k, without any work done to the property. I told the mortgage company and told them there is no way I can afford the to pay the mortgage, this was around June 2009, The mortgage company repossessed the property and sold it in 2010, this is where the shortfall of 110K is. The conveyancing solicitor was part of a fraud, the solicitor is now no longer around, they were an LLP and I have tried to take them to court and sue them and claim damages from their indemnity insurance, but the indemnity insurers have said they will not cover this as this was a fraudulent act intentionally done by the solicitor. Now the bank has passed the debt to a number of debt collectors , this is the third one who is contacting me. To make things even worse, at the time, back in 2008 I actually bought three properties via this vendor, so I actually have three mortgage shortfalls that I need to deal with. I have been living with a lot of stress ever since this has happened, it is really getting me down, has affected my whole life, mentally, physically, affecting my family. I feel I have been let down by the whole system, I purchased these properties in good faith, thinking this will be an investment for the future but in reality it has been nothing but a nightmare. I need to find out what I can do to stop the debt or not pay the shortfall the debt collectors are asking for. Can anyone help and point me in the right direction -

Sorry if this is in the wrong section . I would like to send a subject access request to a housing association but i am not sure on how to proceed. We think there has been some major mistakes [ deliberate ] in procedure in dealing with complaints & we feel that there is cover up being covered up . Who do we SAR What legally can can we request , we would really like internal cross department communications if possible but all data held on this case is our aim. Apologies if this sounds stupid but we really have no idea on the SAR procedure & how to obtain all information & data that pertains to us . Thanks in advance Snowy .

-

Good Afternoon, Apologies if this is in the wrong forum. I'm about to send off a SAR with regards to a problem with AMEX and Allied International and a breach of DPA, amongst other issues. Allied International are purporting to be representing AMEX as an agent and as such are effectively working on behalf of AMEX. With this in mind, will a SAR sent to AMEX be enough to gain access to Allied International actions taken on behalf of AMEX? Thanks in advance.

-

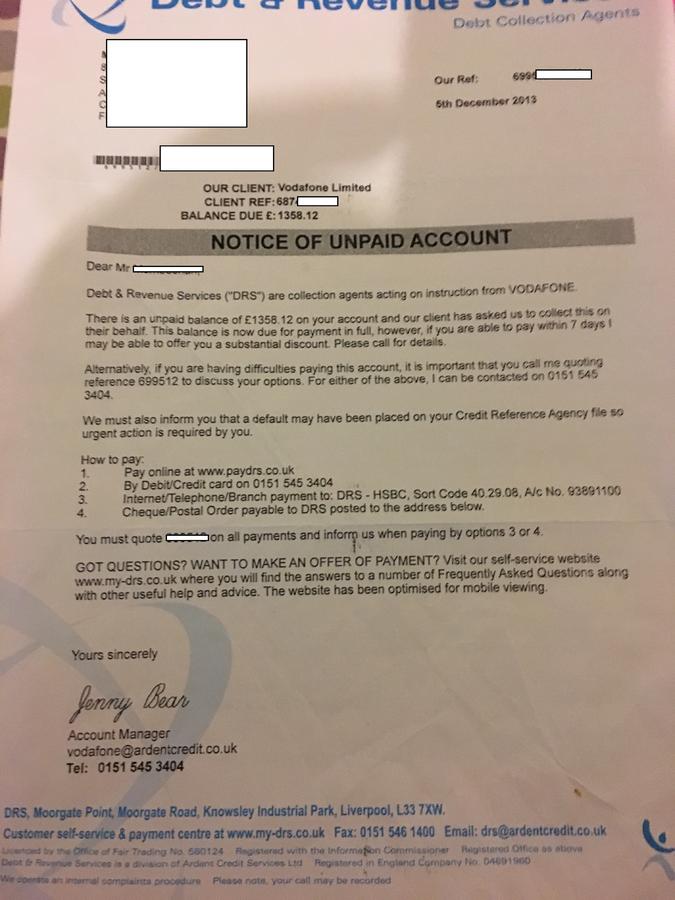

Need some advice on dealing with Vodafone. I submitted a SAR request asking for all the usual (Contract Details, Pricing Structure, Allowance, statement.. the works) and eventually received less of a "Data Subject Access Request" but more a summary of screen notes: For instance I called to change my address and this is what they have given me in the SAR Now I agree, it notifys me of an address change, and could be considered screen notes however WHERE IS THE ACTUAL DATA? Changed address to what??? Now I know where I changed the address to as I have a tenancy agreement and could prove that however subsequently the following happens: So I asked for a Signed copy of my default notice from the CS Agent who sent my SAR: Now I was extremely confused because I knew that I 100% hadn't received the note at my new address however until just shortly I had lost all hope then suddenly while speaking to the new owners of my old address, they informed me that they did indeed have a pile of old mail for me in their cupboard: Incase you haven't guessed THIS WAS SENT TO MY OLD ADDRESS DESPITE ME CHANGING IT

Need some advice on dealing with Vodafone. I submitted a SAR request asking for all the usual (Contract Details, Pricing Structure, Allowance, statement.. the works) and eventually received less of a "Data Subject Access Request" but more a summary of screen notes: For instance I called to change my address and this is what they have given me in the SAR Now I agree, it notifys me of an address change, and could be considered screen notes however WHERE IS THE ACTUAL DATA? Changed address to what??? Now I know where I changed the address to as I have a tenancy agreement and could prove that however subsequently the following happens: So I asked for a Signed copy of my default notice from the CS Agent who sent my SAR: Now I was extremely confused because I knew that I 100% hadn't received the note at my new address however until just shortly I had lost all hope then suddenly while speaking to the new owners of my old address, they informed me that they did indeed have a pile of old mail for me in their cupboard: Incase you haven't guessed THIS WAS SENT TO MY OLD ADDRESS DESPITE ME CHANGING IT

-

I requested a SAR from Arrow Global: template removed - dx read out rules please} This morning, I received a thinner-than-expected package containing some computer printouts and some copy letters (not all I sent). Within was also their statement: Data subject requests under the Data Protection Act 1998 do not entitle a data subject to gain access to all documents they care to mention nor even to all documents which may be relevant to them. The purpose of a data subject access request is to enable the individual to check whether the data controller's processing of his personal data unlawfully infringes his privacy. It is not an automatic key to any information, readily accessible or not, of matters in which he may be named or involved. Therefore we have conducted a proportionate search for personal data relating to you. Can anyone tell me if this is correct. I wanted everything they hold about me, including correspondence between them and MBNA. Many thanks for your help.

I requested a SAR from Arrow Global: template removed - dx read out rules please} This morning, I received a thinner-than-expected package containing some computer printouts and some copy letters (not all I sent). Within was also their statement: Data subject requests under the Data Protection Act 1998 do not entitle a data subject to gain access to all documents they care to mention nor even to all documents which may be relevant to them. The purpose of a data subject access request is to enable the individual to check whether the data controller's processing of his personal data unlawfully infringes his privacy. It is not an automatic key to any information, readily accessible or not, of matters in which he may be named or involved. Therefore we have conducted a proportionate search for personal data relating to you. Can anyone tell me if this is correct. I wanted everything they hold about me, including correspondence between them and MBNA. Many thanks for your help. -

Hello, Its my first time when i am trying to claim my PPI - can someone help me where to send complains I had a few store cards, all now closed and all information are from my Equifax account DEBENHAMS 2009 - 2013 - NewDay MONSOON 2007 - 2012 - NewDay TOP SHOP - account closed 2009 - GE Money River Island - NewDay NEXT - (2006 - 2012) I had as well Personal loan from Ocean money and again I dont have idea which address to use? Any help will be appreciated

Hello, Its my first time when i am trying to claim my PPI - can someone help me where to send complains I had a few store cards, all now closed and all information are from my Equifax account DEBENHAMS 2009 - 2013 - NewDay MONSOON 2007 - 2012 - NewDay TOP SHOP - account closed 2009 - GE Money River Island - NewDay NEXT - (2006 - 2012) I had as well Personal loan from Ocean money and again I dont have idea which address to use? Any help will be appreciated -

Hello again, I had a loan taken on 2008 (paid full in 3 years) with OCEAN MONEY LIMITED, who was the lender BUT website doesn't exist any more and the address from the contract Pacific House, Relay Point, Wilnecote, Staffordshire, United Kingdom, B77 5PA checking ROYAL MAIL belongs TO ALDI SHOP. On company house putting Company registration number - account is still open and states address above but its ALDI SHOP THERE On my agreement i have that OCEAN MONEY is a member of the Ocean Finance & Mortgages Limited Group (IS OR WAS ON 2008) - now I don't have idea where to send, which address and to whose attention ? Any idea?

-

Hi Guys Im trying to be proactive regarding some letters im receiving from Cabot but i cannot find a recent SAR address for MBNA? Does this one look current? I found it on thread dated from 2007, thats my only concern. MBNA Europe Bank Ltd PO Box 1004 Chester Business Park Wrexham Road Chester CH4 9WW

-

as above, CCA'd egg on 16/07/08. They responded with an unsigned agreement and nothing else, no terms, no other info. Wrote back to them to tell them account in dispute as they have failed to provide etc. put in the dispute letter the usual about "you may not pass this account on" etc but they've completely ignored it and sent a letter back saying the account is now closed and will be passed to a DCA for collection what do I do now?

-

Barclays- SAR and CCA? Dear Cagers, As mentioned in another post I have 4+ debts which I desperately want to sort out ASAP. I want to start with Barclays and I will rely on your amazing help I have seen you have given to other desperate people. Please be aware that I am very inexperienced in dealing with creditors, DCA etc... The situation: Barclays current account: Opened 11-12 years ago. I use this account to transfer £4 each month from another account to be able to pay my debts -£1 to each of 4 debtors. This is including paying £1 each month to my Barclays unsecured loan (£1 payment agreed in 2013 via CDCS)... My account is in ‘working’ condition but I can see online that my address, telephone number and e-mail are marked as unknown –I guess they have found out that I don’t live at the last address provided to them. My e-mail and the telephone number have not been changed though but they have deleted them from ‘my details’ file... Barclaycard- Credit card: CLOSED by Barclaycard years ago (opened around 2004-2005,closed-unknown when and why). Never had any late payments etc.. . I have overpaid £10 to the card and never received them back. No documentation with me to prove that but I am sure about the above. Barclays Unsecured loan: Information on Noddle about my unsecured loan: Barclays Bank Plc Account start date: ‘Summer’ 2007 Opening balance £ 20,000 Regular payment £ 385 Repayment frequency :Monthly Date of default: ‘Summer’ 2010 Default balance : £14,000 Currently owning : under £13,000 Originally taken in 2007 for £20K as far as I remember to be repaid in 4 years-maybe 5 years!?. I was supposed to pay £385 a month. I paid £385 a month for over 2 years until November 2009. I applied for the loan online through my current bank account online page and I remember that the money was transferred very quickly to my Barclays current account. I don’t have any paperwork of terms & conditions or signed agreement. I am not sure if I was provided with any anyway. Maybe I just ticked these as ‘read’ online without reading them to be honest. The loan was spent on an unsuccessful business. In October 2009 I became very ill and had to leave the country for treatment. I did not pay anything to them for around 6 months while abroad in hospital. I returned to England in June 2010. I discussed with them my situation (conversations over the phone) and was paying them reduced payments (as much as I can) but they did not agree to reduced payments and did not care and kept adding fines and fees. I don’t remember receiving anything in writing from them-most of the conversations were happening over the phone, any correspondence I might have had is lost. I received a letter from CDCS (Central Debt Collection Services- Parent Company: Barclays Plc. Information about them here : http://www.humberdebt.co.uk/help-with-central-debt-collection-services-debt-debt-management-and-debt-advice/ ) in 2013 agreeing to my £1 monthly payment offered to them. Prior to that I was paying them higher amounts. After that I never received anything from them, then I moved address and never contacted to update address as I did not have a permanent place of stay. Please give me advice what to do? I guess once I provide them with an address they may issue CCJ (non registered yet on Noddle)... I remember taking the loan but I have not got any documentation etc.. . and have not got a clue how much fines , interest and charges they have added to my unsecured loan. ..Is the right thing to request SAR and CCA to Barclays? I think that it is necessary to recover all the information (statements, charges, interest, ppi and other insurance, applications, correspondence for loan, credit card and current account, telephone conversations) before discussing any repayment or settlements with them? Will SAR provide me with statements for my current account as I will need these for proof of payments for different debts as well? https://www.apply.barclays.co.uk/forms/subject-access-request?execution=e1s1 Do you suggest to apply via post or using their online system above? Do you think that the best is to close my Barclays current account first and then start communicating about the unsecured loan with them? Is it true that once I have requested SAR and/or CCA there is a big chance interest and fines to apply to my account again and to be asked to pay more than the token monthly payment? Your help is much appreciated.

-

Hi, Need some advice. I sent Vanquis a DSAR request over 4 months ago. I enclosed a £10 cheque which was duly cashed however they failed to provide me with any of the reqested documents (CCA, Terms & Conditions, Default Notices, Deed of assignment etc) I received a 3 page letter consisting of a demand for a further £1 for CCA and a 2 page document consisting of an abreviated table of transactions (I believe this is supposed to constitute a statement) Can someone confirm to me whether the £10 paid for the sar superceeds the requirement for an additional £1 for the cca. My understanding was the £10 sar fee covers ALL docs & data. Thanks

-

On 4th February I sent the Co-operative Bank a SAR. The first letter they sent was asking for more information. Following my reply they today sent another letter stating that they sold the debt to Fredrickson International so they are now the data holders and not the data controllers and do not have to send me the information that they hold on me. They also kept the £10.00 fee. Can anyone advise if this is correct please? Thank you.

-

What address should I use for a SAR? Confused over Leeds / Chester / elsewhere.

-

First post, so hoping I've followed all the recommendations. Would appreciate some advice following a recent SAR request I sent to NatWest. Used the template from the CAG library to send a SAR to NatWest and they've called today to ask exactly what I was looking for. Not very good at being forceful on the phone, so rather than saying "everything I asked for in writing", I explained I needed transactions and credit agreements. They are supposed to send me a list of transactions for all of my accounts that I will then comb through for any reclaimable charges and supply me details of the department that may be able to locate my agreements. They are also sending back the £10 fee. I have the following defaulted from Natwest (all have fallen off my credit report in the last 2 years). Fell into problems in 2009 and have been making token payements on and off since: a non SB unsecured loan (post April 2007) - £16k outstanding Overdraft - £304 outstanding Credit Card (pre April 2007) - £3k outstanding Just wondering if I should have demanded more or if transactions and an attempt to find my agreements is a good start. Have just started to tidy up the mess from numerous debts. Natwest is the most complicated, largest amount I owe and surprisingly haven't chased, just send statements. They have used DCA in the past but seem to still own the debts Can anyone advise. Thanks