Search the Community

Showing results for tags 'lloyds bank'.

-

I have an account with Lloyds, and have admittedly gone over the agreed overdraft a few times. after going through all my statements and calculating the total amount they've charged me, it comes to about £2000 in charges. I've already put in a claim and got the usual response back, however last month they removed my agreed overdraft limit of £500, and won't let me apply for another overdraft, so I opened a new account with a different bank. now I'm getting letters threatening me with court action because I'm £770 overdrawn. What should I do here? Try and agree a repayment plan with Lloyds to get the balance paid back? I do feel it's a little unfair seeing as I'd be a lot better off if their charges hadn't been so ridiculous. any help from anyone here would be great, thanks.

-

Had a claim upheld with LLoyds for PPI paid. I had, years ago, claimed on the policy and I knew that this would be taken off any redress but is it right they can charge you interest too? Claim paid out was for £8900 and the interest they have charged is £4400 on that! The claim would have come to nearly £11,000 so would have been some back if they hadn't charged all this interest!

Had a claim upheld with LLoyds for PPI paid. I had, years ago, claimed on the policy and I knew that this would be taken off any redress but is it right they can charge you interest too? Claim paid out was for £8900 and the interest they have charged is £4400 on that! The claim would have come to nearly £11,000 so would have been some back if they hadn't charged all this interest! -

Just checked my credit file today. Original Credit Card debt defaulted with OC December 2010 stopped paying monthly repayment plan last year so not SB. Debt passed to Cabot. Requested CCA - details not provided and unenforceable. Cabot have now entered another default status January 2016 ? Can they do this ? Thanks

-

Cabot/Restons - ClaimForm LLoyds Credit Card 'debt'

Tonster posted a topic in Financial Legal Issues

Issue Date on claim form 14th Jan, Particulars of Claim 1.The claimant claims payment of the overdue balance due from the Defendant under a contract between the Defendant and Lloyds Bank dated on or about the Jan ** 2002 2.and assigned to the Claimant on Jun ** 2014 in the sum of £11,***.** Particulars a/c no ************** Particulars a/c no ************** What is the value of the claim? £11K+ Is the claim for a current or credit/loan account or mobile phone account? Credit card When did you enter into the original agreement before or after 2007? 2002 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser (Cabot) Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Yes Why did you cease payments? Financial difficulties and increasing APR by the OC What was the date of your last payment? Feb 2012 Was there a dispute with the original creditor that remains unresolved? Yes, lack of prescribed terms in the signature document Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes I realise that as this is over £10K it may not be small claims track so any advice appreciated. AoS done today, intending to defend all. -

I am trying to help a relative who has received a claim out of the blue Name of the Claimant ? MFS Portfolio Ltd Date of issue 2/12/15 Date to submit defence = 4/1/16 [by 4pm 4th jan ] EDIT BY DX The claim was acknowledged online on 16/12/15 What is the claim for – The Claimant claims payment of the overdue balance due from the Defendant(s) under a contract contract between the Defendant(s) and Lloyds Bank dated on or about Sept 23 2009 and assigned to the claimant on 29 June 2015. Particulars a/c no xxxxxx Date 10/11/15 Default balance £18k Post Refrl Cr Nil Total £18k What is the value of the claim? £18k Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Loan a/c When did you enter into the original agreement before or after 2007? After (Sept 2009 is probably about right) Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? No Did you receive a Default Notice from the original creditor? Not aware of it Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? None Why did you cease payments? Reduction in income meant unable to afford payments any more What was the date of your last payment? It may have been around Sept 2011 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Tried to talk to the bank in the beginning but they were unhelpful. The bank took a payment out the person's bank account that was also with them at the time so the bank current account was closed and moved to stop that happening again I am going to go back to the sticky to see what else needs to be done. Probably be tomorrow now

I am trying to help a relative who has received a claim out of the blue Name of the Claimant ? MFS Portfolio Ltd Date of issue 2/12/15 Date to submit defence = 4/1/16 [by 4pm 4th jan ] EDIT BY DX The claim was acknowledged online on 16/12/15 What is the claim for – The Claimant claims payment of the overdue balance due from the Defendant(s) under a contract contract between the Defendant(s) and Lloyds Bank dated on or about Sept 23 2009 and assigned to the claimant on 29 June 2015. Particulars a/c no xxxxxx Date 10/11/15 Default balance £18k Post Refrl Cr Nil Total £18k What is the value of the claim? £18k Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Loan a/c When did you enter into the original agreement before or after 2007? After (Sept 2009 is probably about right) Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? No Did you receive a Default Notice from the original creditor? Not aware of it Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? None Why did you cease payments? Reduction in income meant unable to afford payments any more What was the date of your last payment? It may have been around Sept 2011 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Tried to talk to the bank in the beginning but they were unhelpful. The bank took a payment out the person's bank account that was also with them at the time so the bank current account was closed and moved to stop that happening again I am going to go back to the sticky to see what else needs to be done. Probably be tomorrow now -

I am starting a new thread on this as advised on my last thread, I have been re-paying a Lloyds Loan for years through Step-Change until just recently when things have deteriorated again the loan was originally taken out circa in 1997, after suddenly stopping my overdraft and pushing me further in to debt, Lloyds then basically force-sold me a "consolidation" re- loan, pushing the original loan from 7k to 15k, this was in 2007 I was sold PPI with the original loan, even though I was Self-Employed and PPI was not applicable, and the PPI continued on the consolidation Loan Following my last thread here, I have requested both Lloyds and Akinika (who the debt was passed on to a while ago) copy of agreement and statements etc Lloyds obliged pretty quickly and the PPI clearly states on it, but the agreement and statements are only related to the second "consolidation" loan, nothing about the original loan of 1997 How do I go about to request copies of the documents related to that without knowing the account details or number? And assuming I can obtain those, how do I then go about to hit them with a request to get repayment of PPI for the overall period? Any help appreciated here

-

Hi All This Is my first post and would greatly appreciate any advice. I have had a claim form from the county court business centre which says I owe £10,000 to capquest/drydens for a Lloyds credit card debt back in 2009. It also says I have been sent a default notice, which I have never received. Unfortunately my wife had a stroke at the time and I had to take time out to care for her. I was paying only token amounts. I am now employed part time and have managed to catch up with my mortgage, c/ tax arrears etc. I had set up a payment of £5 pcm with capquest. I wanted to do a direct debit, but capquest asked me to set up a automated card payment every month. I have found out that was stopped because my debit card was renewed I don't have any paperwork for the debt, should I request paperwork from capquest, the issue date was the 7th December. Any advice would be greatly appreciated. Best Regards Richard. I have already made a donation and will make more when I get the funds. What a fantastic site.

Hi All This Is my first post and would greatly appreciate any advice. I have had a claim form from the county court business centre which says I owe £10,000 to capquest/drydens for a Lloyds credit card debt back in 2009. It also says I have been sent a default notice, which I have never received. Unfortunately my wife had a stroke at the time and I had to take time out to care for her. I was paying only token amounts. I am now employed part time and have managed to catch up with my mortgage, c/ tax arrears etc. I had set up a payment of £5 pcm with capquest. I wanted to do a direct debit, but capquest asked me to set up a automated card payment every month. I have found out that was stopped because my debit card was renewed I don't have any paperwork for the debt, should I request paperwork from capquest, the issue date was the 7th December. Any advice would be greatly appreciated. Best Regards Richard. I have already made a donation and will make more when I get the funds. What a fantastic site. -

Following the recent successful outcome of a couple of PPI claims (that went on for ages!) I now realise that I have done nothing about the charges, so now I'm ready to get these claims started. 2 cards, lots of charges. Just want to make sure I get this right 1st time so have done may hours of research -So this is what I'm planning to do:- Fill out the CIsheet v101 with all the charges with a start date of the 1st charge, setting the interest rate to an average of their rate taken from my statements ' Put my claim to date as today Put the total amount of charges plus compound interest into the statintsheet v101 with a start date of today. Send my preliminary letter to Lloyds enclosing the CIsheet schedule of charges requesting a refund within 14 days after which time I will send a Letter before action to include the CIsheet and the statintsheet. I'm not expecting Lloyds to payout straight away, and realise I will probably have to start a county court claim, but I need to know I'm doing this claim correctly so any advise would be much appreciated. Thanks in advance

-

Hi I am having all sorts of issues with Lloyds Bank recently. November they bounced a cheque I paid in because the signature on the cheque did not match the issuing banks mandate - complained and was put through to a branch I did not bank at, bank did not take complaint seriously - complaint was upheld and compensation received. Last week tried to upgrade my account from Club Lloyds to a Club Lloyds Platinum, this was declined - complaint raised and told someone in Lloyds Bank has put a marker on the account, speak to Personal Lending Team. Personal Lending Team say speak to complaints team, complaints team say vice versa. How can the bank decline an upgrade for an account for the features I am going to pay for? Backwards banking... Yesterday 07/01/16 went to reduce my overdraft and it took the bank 45 minutes to do so by telephone as the advisor had to get higher authority to override to authorise a reduction in the overdraft. I also requested a cheque book, this was declined and advised this needs to be ordered in the branch? I have banked with Lloyds for 5 years with my account always in credit and used as my main bank account. Lloyds Bank have said they are going to be sending out a final response in regards to the recent complaint about the refusal to upgrade my account, any thing I can do? I am going to take this complaint forward to the FOS.

-

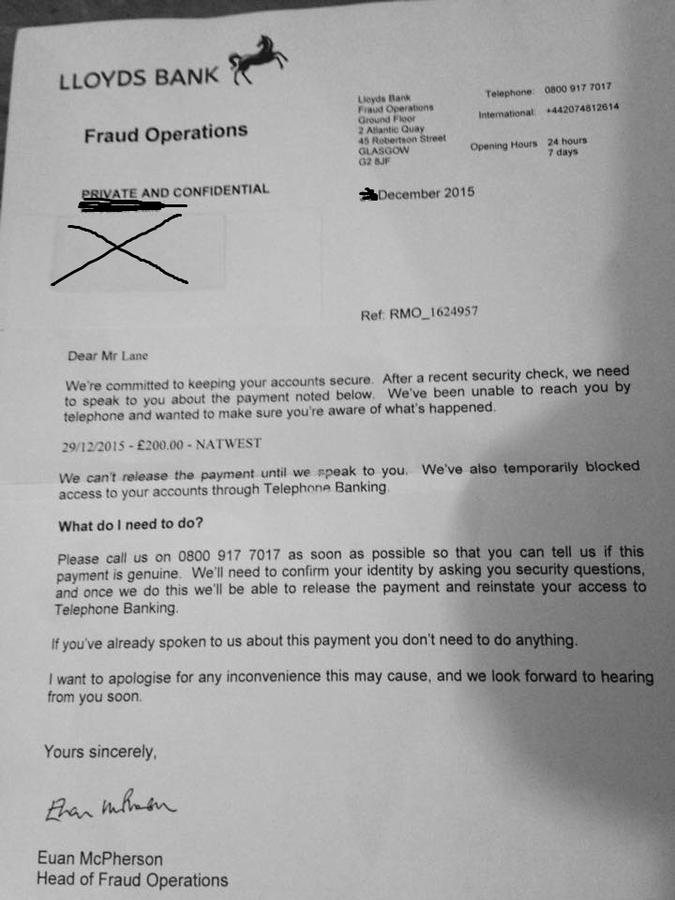

Just to let you know that there is a con going around at the moment. People receive the letter attached below. The free phone numbers in the letter don't belong to Lloyds. If you call them they will try to con you. Ignore or report if you receive one of these CON letters. Not sure if similar letters have been sent 'on behalf' of other banks.

-

Hi All, I've had Lowell and Carter lodge a claim for £1,450 against me for an unpaid overdraft on behalf of Lloyds TSB in November. I acknowledged the claim online and later then submitted a defense to the tune of I do not recognise I owe this debt and that I am unable to defend myself unless proof of the debt is disclosed and that it is the claimants obligation to provided the defendant proof. The defense was accepted by the court and a DX was sent out to which I returned and opted yes to meditation and to allocate to my local county court. In the meantime I emailed Lowell and Carter about the fact they still have not provided any evidence that this debt even exists and that I am unwilling to enter any discussions or meditation until this is produced. A couple of days ago they e-mailed me back with this ------------------------------- Thank you for your email. We are seeking our client’s further instructions regarding your request for evidence however it is our understanding that it is the policy of the Original Creditor to provide its customers with agreements at the point of contract and statements throughout the duration of the account; consequently, you have previously been provided with validation of the debt and you are referred to your own records for the same. We trust this clarifies matters. Yours sincerely ------------------------------- This got my back up obviously as from my interpretation of this e-mail is it is up to me to seek this out myself so I e-mailed them back the below copying in the court e-mail with my claim number ------------------------------- Thank you for your response, I would like to remind you that it is not the original creditor trying to obtain a judgement against me through the small claims court. Are you telling me Is it your policy to take on instructions from your clients for commencement of legal proceedings without sight of any proof that the alleged debt is actually owed then? If I have been supplied with validation of the debt (To which I do not recall) Then I am sure that you will be able to speak to your client who sent this originally and reproduce this without a problem then proving to me and the court that this debt in fact exists as despite numerous requests I have yet to see it, and forgive me being the dubious person I am I fail to take your word for it that I have been 'provided with this before'. This is not the remit of either myself or the alleged original creditor (Lloyds) this is the responsibility of Lowell/Bryan Carter to prove beyond all doubt that this debt exists if you think I will be bullied into thinking any other way you are very mistaken. I await your response. I also trust this clarifies matters too. ------------------------------- I maybe should have been a bit more professional but they just seem to think it's okay to bully people into paying debts they potentially do not owe. Has anyone seen this before, do they have any proof on this debt? Surely they'd have this to hand if they did? Thanks!

-

I took a loan with Lloyds some years ago and the debt was passed to Lowell last year or so. They have been sending me letters I received court papers early December. I acknowledged them and spoke to them a couple of days ago as over Xmas I received a letter saying they would go for judgement if I didnt respond or pay by 6.1.16. I managed to get through to them yesterday after trying since Saturday. I was inclined to pay all the money ( with a loan from family ) as I have managed to clean up my credit file last couple years and dont want a CCJ. They said I could make an arragement to pay monthly and they would not get judgement. Is this true?

-

I thought I was nearly home free and clean but another has crawled out of the woodwork from Lowell's and the default will be six years old in May according to the credit report, They are currently at the stage of if I do not respond they will do a credit search to see if I have any assets such as property and evaluate my financial circumstances! I'm guessing that they are allowed to do this as they have bought the original agreement that says the company can credit check me? Do I just keep my head down and see what they do next or maybe try diversion tactics such as not known at this address? As ever all advice appreciated

-

I previously requested CCA details recently and received a reply advising that due to high volumes of requests that they would respond as soon as possible. 12+ days have now surpassed - do I chase again giving them another 12 days to respond or is there another letter that I send regarding failure to respond ? Cheers

-

Hi, I received the following email........I don't have a LLoyds account.....!!! Dear customer, For your protection, you must verify this activity before you can continue using your account. We will review the activity on your account with you and upon verification,and we will remove any restrictions placed on your account. Activate your account now > If you choose to ignore our request, you leave us no choice but to temporary suspend your account.Yours sincerely, Lloyds Banking Group Privacy | Site terms and conditions | Accessibility Information | Cookie notice| Site Map Lloyds Bank plc and Bank of Scotland plc (members of Lloyds Banking Group), are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Authorisation can be checked on the Financial Services Register at: www.fca.org.uk

-

Hi Having read through the Barclays thread on credit card reclaims I'm looking for similar experiences from Lloyds caggers, and not come across any so far, only PPI and bank charge reclaim. is that because recently there have not been any successful credit card reclaims with Lloyds:???:

-

Hi i would be grateful for any clarification other caggers can provide. LTSB Gold Service Payment application form circa 1990's. across the top of the application 'Lloyds Bank Gold Service Payment/Photo Card Application Form' underneath Credit agreement regulated by the Consumer Credit Act 1974. this is very confusing as part of the document states under 'Security' 'the overdraft facility made available under this agreement is unsecured and shall not be secured or treated as secured by virtue of any mortgage, charge or other security which i/we may have already given (or may in future give) to you. does this then mean that if there is a dispute that LTSB cannot enforce to change the 'unsecured' to 'secured' via a CCJ ? then further down it states 'to be considered for a Lloyds Bank Gold Service Payment Card you must sign in the box below' this implies to me the A4 form is an application form and not an agreement, however in the signature box it refers to 'this is a Credit Agreement regulated by the CCA' has anyone else come across this? and what is the position. Thank You

Hi i would be grateful for any clarification other caggers can provide. LTSB Gold Service Payment application form circa 1990's. across the top of the application 'Lloyds Bank Gold Service Payment/Photo Card Application Form' underneath Credit agreement regulated by the Consumer Credit Act 1974. this is very confusing as part of the document states under 'Security' 'the overdraft facility made available under this agreement is unsecured and shall not be secured or treated as secured by virtue of any mortgage, charge or other security which i/we may have already given (or may in future give) to you. does this then mean that if there is a dispute that LTSB cannot enforce to change the 'unsecured' to 'secured' via a CCJ ? then further down it states 'to be considered for a Lloyds Bank Gold Service Payment Card you must sign in the box below' this implies to me the A4 form is an application form and not an agreement, however in the signature box it refers to 'this is a Credit Agreement regulated by the CCA' has anyone else come across this? and what is the position. Thank You -

Hi. i had a Lloyds tsb credit card when they decide to sell tsb ,Lloyds Bank took the card over and that's where i get my statements from ,i pay them too, I have a problem now that Lloyds tsb are now flagging my account saying i have gone away ,i take that to be they are claiming, i do not live at the address they have on their files. It seems very strange to me, are they allwed to do this.

-

I am hoping someone can answer this Lloyds ppi question for me. Before I actually ask this is more so I understand than wanting help at this moment in time. The question I have is in regards to a Lloyds assit card that was taken out on 24 April 2001 I found some old statements and it had something called a CPP on it which disappeared around 2006 and ppi started to show instead on the statements. So my question (s) are: 1) What actually is CPP and how is it different to ppi? 2) If someone was claiming them been mis-sold (for whatever reason) would it be one claim for both or two separate claims? And a couple of unrelated questions: 1) Out of all the Credit ref companies which is the best between Noddle, Clearscore & Experian? The reason I ask is because on noddle it says that an account is open but on clearscore it says the account is closed and even though I just received my £2 report from Experian I don't understand what is open or closed on there. 2) If on my credit report it says that an account is settled and has a £0 balance by the original lender but DCA (Lowells) says there is still a balance owing. What does that mean? 3) On my credit report a DCA is shown to have updated three different times for the same account. On noodle it shows - 7th September (account open) On clearscore it says - 15th September (account closed) On Experian it says - 20th September (account open? not sure due to the fact I can't figure out how to read there paper reports) Which of those dates is the correct one? Also, can a DCA open and close the account like this? Thank you for any replies I may get and I do apologise for all the questions but I just want to get an idea how to understand all this and if I don't ask then I will never know.

-

Looking for some help Had a lloyds bank account a few years ago which was in agreed overdraft I moved house and informed all my creditors lloyds decided to cancel overdraft and ask for money back letters were sent to old address so they say and I was defaulted I honestly never received it and only knew about a year later when I checked my credit file and paid account off. I have asked them to for a copy of the notice which they say they haven't got but their computer says it was sent they won't remove default but I was never given opportunity to pay off. Do they have to keep copies of default notice Thanks

-

Bran Carter sent me an account review letter a couple of days ago advising me to contact them by phone to discuss my "proposed repayment plan"

-

Hello, I wonder if anybody could help me. I came to the site from Google as I typed in some information relating to Cabot Financial and a Claim Form and somebody had already posted a thread a long time ago. I tried to follow the thread but I got really confused. I am feeling quite stressed about this issue so that may be why I found it hard to follow, so I appreciate if this sounds familiar to you already but I may need some step by step help. I would be so thankful in return. A few years ago I went travelling and I missed some payments on a Lloyds Bank Student Credit Card (£500 limit) and they labelled it as 'Default'. My mother had moved address while I was travelling and so I failed to receive any letters from them about this. I have no legal experience and stupidly thought that because it stated the account was 'Satisfied' the payment must then be erased and my punishment must be the 6 year Default on my credit file. I therefore pretty much forgot about it and carried on with life. I signed up for Experian Credit Report about a year or so ago. Suddenly I started receiving letters from a company called CABOT FINANCIAL about a debt I had to pay them. I stupidly ignored the letters as I hadn't heard anything about the Lloyds debt in years and so didn't understand why I had to pay another company a debt from years ago, plus I couldn't afford to pay them the £663 they wanted. I heard something years ago about if they are not able to contact you personally and get a response then they cannot claim anything from you. Eg. Never answering the phone or replying to letters. I now realise this is not the case as I have received a COURT CLAIM FORM from CABOT FINANCIAL. This is what appears on my credit file. LLOYDS BANK CREDIT CARD Default Date 27/01/2012 Default Balance £663 BALANCE: £0 CABOT FINANCIAL (UK) LTD Default Date 27/01/2012 (They certainly did not contact me until the last 1/2 years but the date isn't shown) Default Balance £663 1st Question: Can I have two DEFAULTS on my credit file for the same amount? Eg. Both Lloyds and Cabot for the one debt I had. 2nd Question: Can anyone help me to respond to the CLAIM FORM from the COUNTY COURT BUSINESS CENTRE. (Details below) CLAIMANT: CABOT FINANCIAL (UK) LIMITED ISSUE DATE: 15TH SEPTEMBER 2015 PARTICULARS OF CLAIM: Defendant entered into a credit agreement described by the original creditor as LLOYDS BANK CREDIT CARD and having account number **************. The claimant, a UK limited company is the assignee and legal owner of all rights previously enjoyed by the original creditor. Amount Claimed: £663 Court Fee: £60 Legal Representatives: £70 Total Account: £796 Do I acknowledge it, defend, contest it? I cannot afford to pay it. I am off sick due to anxiety and depression and only get £315 a month. I also have a Lloyds Current Account that has just defaulted due to not being able to pay and I have a £3000 Halifax bank Overdraft which is nearing the limit. I wish I hadn't buried my head in the sand but the anxiety stopped me opening the letters and these things don't go away. Sorry for the long post. I really would appreciate any help and advice you can give. If you need any further information please feel free to ask. Thankyou.

Hello, I wonder if anybody could help me. I came to the site from Google as I typed in some information relating to Cabot Financial and a Claim Form and somebody had already posted a thread a long time ago. I tried to follow the thread but I got really confused. I am feeling quite stressed about this issue so that may be why I found it hard to follow, so I appreciate if this sounds familiar to you already but I may need some step by step help. I would be so thankful in return. A few years ago I went travelling and I missed some payments on a Lloyds Bank Student Credit Card (£500 limit) and they labelled it as 'Default'. My mother had moved address while I was travelling and so I failed to receive any letters from them about this. I have no legal experience and stupidly thought that because it stated the account was 'Satisfied' the payment must then be erased and my punishment must be the 6 year Default on my credit file. I therefore pretty much forgot about it and carried on with life. I signed up for Experian Credit Report about a year or so ago. Suddenly I started receiving letters from a company called CABOT FINANCIAL about a debt I had to pay them. I stupidly ignored the letters as I hadn't heard anything about the Lloyds debt in years and so didn't understand why I had to pay another company a debt from years ago, plus I couldn't afford to pay them the £663 they wanted. I heard something years ago about if they are not able to contact you personally and get a response then they cannot claim anything from you. Eg. Never answering the phone or replying to letters. I now realise this is not the case as I have received a COURT CLAIM FORM from CABOT FINANCIAL. This is what appears on my credit file. LLOYDS BANK CREDIT CARD Default Date 27/01/2012 Default Balance £663 BALANCE: £0 CABOT FINANCIAL (UK) LTD Default Date 27/01/2012 (They certainly did not contact me until the last 1/2 years but the date isn't shown) Default Balance £663 1st Question: Can I have two DEFAULTS on my credit file for the same amount? Eg. Both Lloyds and Cabot for the one debt I had. 2nd Question: Can anyone help me to respond to the CLAIM FORM from the COUNTY COURT BUSINESS CENTRE. (Details below) CLAIMANT: CABOT FINANCIAL (UK) LIMITED ISSUE DATE: 15TH SEPTEMBER 2015 PARTICULARS OF CLAIM: Defendant entered into a credit agreement described by the original creditor as LLOYDS BANK CREDIT CARD and having account number **************. The claimant, a UK limited company is the assignee and legal owner of all rights previously enjoyed by the original creditor. Amount Claimed: £663 Court Fee: £60 Legal Representatives: £70 Total Account: £796 Do I acknowledge it, defend, contest it? I cannot afford to pay it. I am off sick due to anxiety and depression and only get £315 a month. I also have a Lloyds Current Account that has just defaulted due to not being able to pay and I have a £3000 Halifax bank Overdraft which is nearing the limit. I wish I hadn't buried my head in the sand but the anxiety stopped me opening the letters and these things don't go away. Sorry for the long post. I really would appreciate any help and advice you can give. If you need any further information please feel free to ask. Thankyou. -

Hello, I am after some advise please to help with my defence as to whether I can seek and obtain copies of any transactions relating to my load account with Lloyds prior to the sale to Cabot and if whether the sell price can be admissible in the balance I should be paying to Cabot as opposed to what they've put claim in for. Recently been served with a CCJ for defaulting on installment repayment for an unsecured loan I obtained from Lloyds TSB in 1994. The agreement of sale points to this taking place in Oct of 2012. I need advise also on how and if I qualify for PPI , as this can perhaps be what I can repay the outstanding amount owed. The loan was unsecured.

Hello, I am after some advise please to help with my defence as to whether I can seek and obtain copies of any transactions relating to my load account with Lloyds prior to the sale to Cabot and if whether the sell price can be admissible in the balance I should be paying to Cabot as opposed to what they've put claim in for. Recently been served with a CCJ for defaulting on installment repayment for an unsecured loan I obtained from Lloyds TSB in 1994. The agreement of sale points to this taking place in Oct of 2012. I need advise also on how and if I qualify for PPI , as this can perhaps be what I can repay the outstanding amount owed. The loan was unsecured. -

I'm new here so I apologise if I'm posting this in the wrong section. My wife and I purchased a business a few years ago that we closed earlier this year. The seller tricked us into buying the business by inflating the figures and we fell for it. Anyway.. we have lost our entire life savings trying to keep it going and earlier this year when we had no money left we had no choice but to walk away as we could not find a buyer after trying so hard to sell it for over a year. We have a business loan for £45k with Lloyds which we have personally guaranteed (I've been told the PG is watertight). We also have a £4k overdraft. They've sent us a formal demand for the loan and overdraft. I called them last week to set up a payment plan and I was told that they would contact us back. I wanted to know if anyone has been in a situation where Lloyds have accepted a payment plan for this kind of situation or will they force me to sell my house in order to pay them? I'm quite worried as I really don't want to move. My wife and I are currently working but we have only been working for 6 weeks so we will not have the right paperwork to remortgage the house.

-

My first time using a forum ever, wish i had done this sooner .... ill try and explain best i can. had a Lloyds bank account roughly 5 years ago, changed bank accounts since and thought nothing of it. I then received a County Court Claim form on 28th April 2015 then a letter from Bryan Carter Solicitors on 29th april 2015 out of the blue saying i owe £270 The claim form states : Particulars of claim The claimants claim is for the sum of 181.10, being monies due from the defendant to the claimant under an agreement regulated by the consumer credit act 1974 between the defendant and Lloyds. Under account reference XXXXXXXX and assigned to the claimant on 03/07/13, notice of which has been given the the defendant (Ive never received this) the defendant failed to maintain contractual repayment under the terms of the agreement and a default notice has been served which has not been complied with (again not received) And the claimant claims 181.10 the claimant also claims statutory interest pursuant to s.69 of the country act 1984 at a rate of 8% per annum from the date of assignment of the agreement to date but limited to a maximum of one year and a maximum of 1000 amounting to 14.49 in brief i replied to the court and sent in a defence stating that i had never received the default notice nor any other correspondence before the claim form and that i had requested a copy of the credit agreement including the £1.00 payment but no reply . (i sent them recorded delivery and have the signature as proof they were received) They offered mediation to which i said yes but when i spoke to the mediation team it wasn't suitable as i had still not received a copy of the agreement i had requested for a second time. the last reply i got from bryan carter was on 17th july 2015: "we confirm we are taking further instruction from our client in regards to your request for documentation under the consumer credit act 1974 and we will revert back to you in due course. We confirm the production of these documents at a later date will rectify any earlier breaches." Then on the 11/8/2015 i received notice of allocation to the small claims track (hearing) My hearing is on the 16th October and i need to put in a witness statement 2 weeks before that... ... i dont know where to start with it? and also after reading a few other threads i think i should have asked for CPR 31.14 at the beginning but i didnt:| its really weighing heavy on my mind now and just want to get this statement in and let the court decide its not a very large amount i keep thinking i should just give in and pay (not that i have that to hand) but then i think why should i when i dont have any information about this debt??? any help would be so much appriciated!!!

My first time using a forum ever, wish i had done this sooner .... ill try and explain best i can. had a Lloyds bank account roughly 5 years ago, changed bank accounts since and thought nothing of it. I then received a County Court Claim form on 28th April 2015 then a letter from Bryan Carter Solicitors on 29th april 2015 out of the blue saying i owe £270 The claim form states : Particulars of claim The claimants claim is for the sum of 181.10, being monies due from the defendant to the claimant under an agreement regulated by the consumer credit act 1974 between the defendant and Lloyds. Under account reference XXXXXXXX and assigned to the claimant on 03/07/13, notice of which has been given the the defendant (Ive never received this) the defendant failed to maintain contractual repayment under the terms of the agreement and a default notice has been served which has not been complied with (again not received) And the claimant claims 181.10 the claimant also claims statutory interest pursuant to s.69 of the country act 1984 at a rate of 8% per annum from the date of assignment of the agreement to date but limited to a maximum of one year and a maximum of 1000 amounting to 14.49 in brief i replied to the court and sent in a defence stating that i had never received the default notice nor any other correspondence before the claim form and that i had requested a copy of the credit agreement including the £1.00 payment but no reply . (i sent them recorded delivery and have the signature as proof they were received) They offered mediation to which i said yes but when i spoke to the mediation team it wasn't suitable as i had still not received a copy of the agreement i had requested for a second time. the last reply i got from bryan carter was on 17th july 2015: "we confirm we are taking further instruction from our client in regards to your request for documentation under the consumer credit act 1974 and we will revert back to you in due course. We confirm the production of these documents at a later date will rectify any earlier breaches." Then on the 11/8/2015 i received notice of allocation to the small claims track (hearing) My hearing is on the 16th October and i need to put in a witness statement 2 weeks before that... ... i dont know where to start with it? and also after reading a few other threads i think i should have asked for CPR 31.14 at the beginning but i didnt:| its really weighing heavy on my mind now and just want to get this statement in and let the court decide its not a very large amount i keep thinking i should just give in and pay (not that i have that to hand) but then i think why should i when i dont have any information about this debt??? any help would be so much appriciated!!!