Search the Community

Showing results for tags 'limited'.

-

Hello, I just received email from Graham High Group Limited - Loss Adjusters that insurer approved our claim. Does Anyone know how long takes to have refund ? We have to pay our Contractor to start do works and no idea how long takes the payment process THANK YOU

Hello, I just received email from Graham High Group Limited - Loss Adjusters that insurer approved our claim. Does Anyone know how long takes to have refund ? We have to pay our Contractor to start do works and no idea how long takes the payment process THANK YOU -

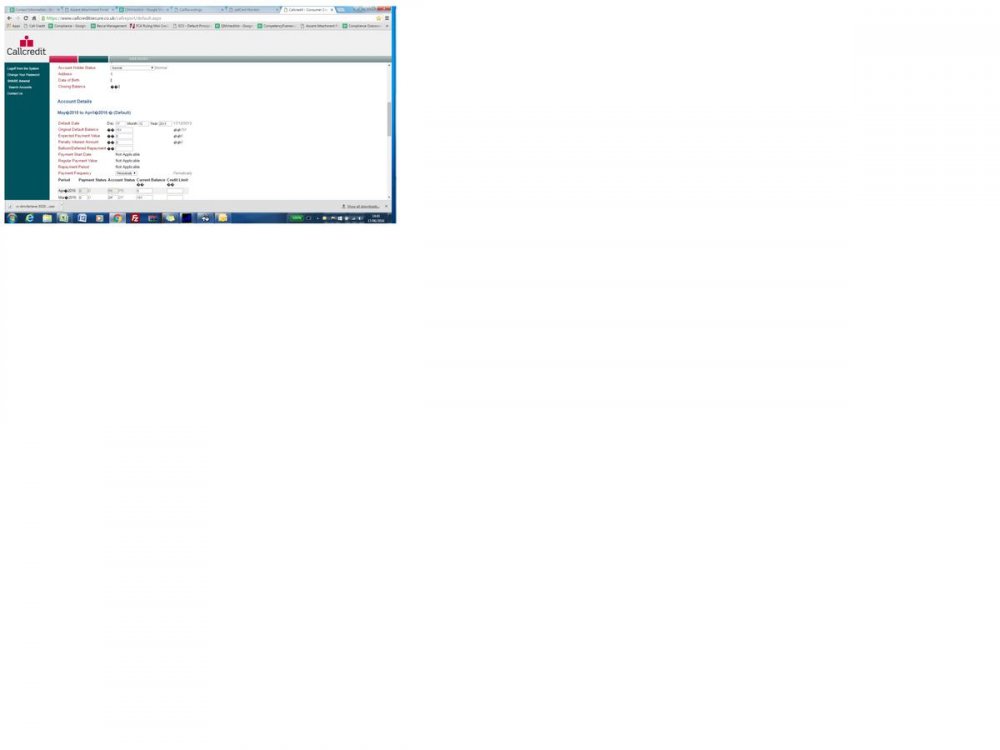

Hi All, New to the CAG and really need some experienced help with my ongoing battle with this company. I first submitted a Formal Complaint against Opos Limited in January 2016. This went to the Financial Ombudsman after I disagreed with their final response. The adjudicator advised that where Opos Limited is the debt collector and Kapama is the debt owner, he didn't think Opos Limited's collection practices were wrong, but he did advise me to send in a second complaint to Kapama about irresponsible lending. The original loan was for £100.00, and with charges etc. it ended up at £300.50. This is where things get interesting... I made a payment to Opos back on the 18th October 2014 for £149.45. When I looked at my credit report on Noddle, the 'Account Default Date' for this Minicredit loan was exactly the same I made a payment to Opos. When the adjudicator questioned them on this, apparently that date was incorrect and Minicredit defaulted me in November 2012. Please bear in mind that I actually took out the Minicredit loan in July 2013 so this definitely isn't correct! Anyway, to resolve the first complaint we agreed a settlement of £100.00 which I paid in full two days after the adjudicators decision. This was 22nd April 2016. Around the same time I sent the second complaint to Kapama for irresponsible lending. On receipt of my second complaint, Opos's Compliance Manager sent me an email on the verge of bribery saying that IF I withdrew my second complaint, she would remove the footprint of this loan from my credit file as a way of resolution. I got in touch with the adjudicator at the FOS about what they offered and he said he is personally going to call them and say it's unacceptable. Their compliance manager said she was going to update my credit file within 28 days since the settlement was received. I check on my credit report at the end of April and there is now new information... Account Default Date is 17th December 2013 with the account showing a balance of £51.45 outstanding? As you can imagine I am now fuming with this. So I phone them, and they make up some sorry excuse that they never received the settlement form (despite having an email from their compliance manager saying the account is settled). When I mentioned court they hung up on me so I emailed them with a furious message. I haven't been satisfied from the beginning that Minicredit defaulted me in the first place, so now I have opened a case with the Information Commissioners Office which they are investigating. On Wednesday 15th June 2016, I received a final response to my second complaint. This time they offered to refund around £50.00 as a gesture of goodwill and decided not to uphold my complaint. (I believe this is very weird considering they had already offered to remove the default without looking further into the complaint and have now offered a refund). They also said that they updated my credit file information through Callcredit and that this is not the same as Noddle and the information may not have shown on Noddle as it takes longer to update. I have not accepted this and again have put it in to the FOS. In response to their Final Complaint I asked a series of questions regarding the default, dates and why they have offered me the above but not upheld my complaint. They responded that they will liaise with the FOS and did not answer any of my questions. Yesterday I decided that I would pay for a subscription to Callcredit (Credit Compass) to see what my file on there shows in regards to this default seeing as this is where they say the updated the information. After looking everywhere for this account, it is NOT on there. Not in settled or outstanding. So I emailed the Compliance Manager again and said that this account is nowhere to be found and yet this is where they supposedly updated the information, and not through Noddle. She emailed me back with a screenshot of her computer with the screen showing my file details with the '£0' balance etc. (I think this could have been a big mistake for them) On that screenshot it shows Account Details 'May 2015 to April 2016'. It also looks like the boxes are available for them to amend themselves! I thought that they notified CRA's to enter personal information like that, I'm not sure if creditors are allowed to do this and are able to amend information freely themselves? What I really need some advice on is surely if Minicredit defaulted me, it would be a case of a name change on the account on my credit file back in 2013 or whatever date they supposedly defaulted me. Minicredit passed over their accounts in December 2014 and on that screenshot they're showing account details from May 2015!? I have phoned Callcredit and they asked me to send a copy of the default showing on Noddle, as well as copy of that screenshot they sent me. I have also fowarded this on to the ICO and FOS. I really apologise for the huge essay but I would like to share my story about these companies to you all. I would advise everyone that has had a default from this company to check the dates etc. If anyone can give me some advice I'd really appreciate it as I'm willing to go all the way with this. I've attached the screenshot for all of you to see. I have loads of emails for evidence and the responses so if you need to see them please let me know. I have probably missed a few things out but this is the main part of it all. Thanks

-

Credit Card-MBNA -Account start date 05/2006, defaulted -06/2010 at £6550. Noddle currently shows that I owe : £5250. I found a letter dated 01/09/2010 from Experto Credite advising me that Varde Investments(Ireland) Limited has bought the interest of MBNA Europe Banks Limited and they are legal owner of my account. ‘Under the terms of assignment Experto Credite Ltd has been appointed by Varde to recover any and all outstanding sums.’ I paid Experto Credite £20 on monthly basis until Aktiv Capital contacted me to inform me that they have taken over my account. They agreed to the £1 monthly payment in 2013 (which was agreed with Experto Credite already I think) and since then I have been paying it. I noticed just recently that on my Noddle report instead of Activ Capital, PRA Group UK has taken place as a lender.The last letter I received before I moved away in 2013 was from Aktiv Kapital ltd. I have been paying them £1 for more than 2 years. Now I want to update them about my new address and request CCA but they are no longer Aktiv Kapital ltd. They are PRA ltd. They probably sent me a letter to notify me at my old address... Their bank details are still the same so my £1 has been going to them and they update my Credit record file regularly. I called the Aktiv Kapital telephone number from the letter I last received in 2013 but PRA answered. I did not introduce myself - just asked them to who to write and they explained to write to PRA in Scotland not to Aktiv Kapital in Bromley. Who should I address the letter to: PRA or Aktiv Kapital or both? What do you think? My address: Their address: Aktiv Kapital(UK)Ltd/ PRA ltd 2 The Cross Kilmarnock Scotland KA1 1LR Date: Dear Sir or Madam, .................. or My address: Their address: Aktiv Kapital Ltd 2 The Cross Kilmarnock Scotland KA1 1LR Date: Dear Sir or Madam, .....................

-

Hello, Can anyone please help me, I have received a claim form from Northampton County Court Business Centre. It is an old Simply Be debt, seems to be with ME III now, no idea who they are. Amount Claimed is: £1181 - this includes costs (their legal costs)

Hello, Can anyone please help me, I have received a claim form from Northampton County Court Business Centre. It is an old Simply Be debt, seems to be with ME III now, no idea who they are. Amount Claimed is: £1181 - this includes costs (their legal costs) -

Cabot Financial (Europe) Limited have left a footprint on my credit search file that says 'Customer Management' id like to know if this is going to be visible to lenders or if this particular search would be only visible to myself? It came about as i called them and asked the outstanding balance on a very old debt. There is no evidence of them within my file as this particular arranged payment fell of the credit report 2 years ago so it is only this particular search now. Thanks

Cabot Financial (Europe) Limited have left a footprint on my credit search file that says 'Customer Management' id like to know if this is going to be visible to lenders or if this particular search would be only visible to myself? It came about as i called them and asked the outstanding balance on a very old debt. There is no evidence of them within my file as this particular arranged payment fell of the credit report 2 years ago so it is only this particular search now. Thanks -

County claim form sent issue date 6th Jan 2016 from County Court Business Centre, Northamptom. Claimant: Cabot Financial (UK) Limited 1 Kings Hill Ave Kings Hill Kent ME19 4UA Claimed amount 280 + fees (25 court + 50 legal) = 355 Signed Wright Hassall Capital One original creditor nearly 6 years ago with a registered default notice. Apparently they sold the debt to Cabot without my knowledge. 1. Is this a legit CC claim, it's all printed, no pen signature or court stamp, just laser printed image of the TCC and text (it does have moneyclaim.gov.uk password but never checked it for authenticity)? 2. Will they have the original credit agreement and if they do or don't would I have time to obtain this feedback of information under CCA request? 3. I never received or in receipt of any "notice of the assignment", how could they prove otherwise? 4. REF: Firm Name: Cabot Financial (UK) Limited Interim Permissions Reference Number: 472690 Current status: Lapsed a) Consumer credit business: Entering into a regulated credit agreement as lender; and exercising, or having the right to exercise, the lender's rights and duties under a regulated credit agreement. Inactive 28/02/2015 b) Credit brokerage: Credit broking Or Credit broking limited to credit intermediation Inactive 28/02/2015 c) Debt administration: Debt administration Inactive 28/02/2015 d) Debt collecting: Debt collecting Inactive 28/02/2015 e) Debt-Adjusting on a Commercial Basis: Debt adjusting on a commercial basis Inactive 28/02/2015 If they don't have "permission" to conduct debt chasing activities how are they able to conduct debt chasing activities on me via a CC claim? 5. What position do I hold that will throw out this case in court? Any other help or advice will be greatly appreciated. Thank you in advance.

County claim form sent issue date 6th Jan 2016 from County Court Business Centre, Northamptom. Claimant: Cabot Financial (UK) Limited 1 Kings Hill Ave Kings Hill Kent ME19 4UA Claimed amount 280 + fees (25 court + 50 legal) = 355 Signed Wright Hassall Capital One original creditor nearly 6 years ago with a registered default notice. Apparently they sold the debt to Cabot without my knowledge. 1. Is this a legit CC claim, it's all printed, no pen signature or court stamp, just laser printed image of the TCC and text (it does have moneyclaim.gov.uk password but never checked it for authenticity)? 2. Will they have the original credit agreement and if they do or don't would I have time to obtain this feedback of information under CCA request? 3. I never received or in receipt of any "notice of the assignment", how could they prove otherwise? 4. REF: Firm Name: Cabot Financial (UK) Limited Interim Permissions Reference Number: 472690 Current status: Lapsed a) Consumer credit business: Entering into a regulated credit agreement as lender; and exercising, or having the right to exercise, the lender's rights and duties under a regulated credit agreement. Inactive 28/02/2015 b) Credit brokerage: Credit broking Or Credit broking limited to credit intermediation Inactive 28/02/2015 c) Debt administration: Debt administration Inactive 28/02/2015 d) Debt collecting: Debt collecting Inactive 28/02/2015 e) Debt-Adjusting on a Commercial Basis: Debt adjusting on a commercial basis Inactive 28/02/2015 If they don't have "permission" to conduct debt chasing activities how are they able to conduct debt chasing activities on me via a CC claim? 5. What position do I hold that will throw out this case in court? Any other help or advice will be greatly appreciated. Thank you in advance. -

Hello again, I had a loan taken on 2008 (paid full in 3 years) with OCEAN MONEY LIMITED, who was the lender BUT website doesn't exist any more and the address from the contract Pacific House, Relay Point, Wilnecote, Staffordshire, United Kingdom, B77 5PA checking ROYAL MAIL belongs TO ALDI SHOP. On company house putting Company registration number - account is still open and states address above but its ALDI SHOP THERE On my agreement i have that OCEAN MONEY is a member of the Ocean Finance & Mortgages Limited Group (IS OR WAS ON 2008) - now I don't have idea where to send, which address and to whose attention ? Any idea?

-

Hi, I have been a member for years, but this is my first post. My husband has received a letter from UCS, stating that they have been instructed by UK Parking Limited, for a PCN in (afaik) a private car park. It states that UKPL wrote to him & that we did not respond & therefore cannot appeal. We have had no correspondence from them, And I presume that they would have had to write with date & time stamped photographic proof? They are stating that we were parked after the expired time on a P&D ticket and the original charge was £100 and they have added a £60 Admin Fee. They have threatened him with a solicitor, if he either does not pay, or does not say who was driving the car, if it wasn`t him. They are also trying to use scare tactics by quoting the case of Parking Eye V Beavis. The letter then goes on to "advise" us not to believe information given on the interent, and to gain legal advice. I have been trying to find an email contact for them, so that I have a paper trail & also because I do not want to speak to them (hubbie doesn`t have time due to work, so I am dealing with it). I wanted to email this - Pls can anyone advise if it is acceptable to send? Hello, I am contacting you as my husband was sent a letter from you, saying that UK Parking Limited had instructed you to contact him, due to non payment of a parking charge notice. The reference number is - ******** We have not received anything in writing from UK Parking Limited and I presume that they have to contact us with evidence of any wrong doing, such as timed & dated photographs. I am sure that as a legitimate company, you wouldn't expect anyone to make payment without such proof. I presume that you will be contacting them to send us the relevant information before you proceed. Yours sincerely, Our 14 days to respond is up tomorrow (well today as it is now gone midnight!) Thanks & Kind Regards

Hi, I have been a member for years, but this is my first post. My husband has received a letter from UCS, stating that they have been instructed by UK Parking Limited, for a PCN in (afaik) a private car park. It states that UKPL wrote to him & that we did not respond & therefore cannot appeal. We have had no correspondence from them, And I presume that they would have had to write with date & time stamped photographic proof? They are stating that we were parked after the expired time on a P&D ticket and the original charge was £100 and they have added a £60 Admin Fee. They have threatened him with a solicitor, if he either does not pay, or does not say who was driving the car, if it wasn`t him. They are also trying to use scare tactics by quoting the case of Parking Eye V Beavis. The letter then goes on to "advise" us not to believe information given on the interent, and to gain legal advice. I have been trying to find an email contact for them, so that I have a paper trail & also because I do not want to speak to them (hubbie doesn`t have time due to work, so I am dealing with it). I wanted to email this - Pls can anyone advise if it is acceptable to send? Hello, I am contacting you as my husband was sent a letter from you, saying that UK Parking Limited had instructed you to contact him, due to non payment of a parking charge notice. The reference number is - ******** We have not received anything in writing from UK Parking Limited and I presume that they have to contact us with evidence of any wrong doing, such as timed & dated photographs. I am sure that as a legitimate company, you wouldn't expect anyone to make payment without such proof. I presume that you will be contacting them to send us the relevant information before you proceed. Yours sincerely, Our 14 days to respond is up tomorrow (well today as it is now gone midnight!) Thanks & Kind Regards -

Hi I am the executor for my late mother's estate and we are in the process of selling her house. We have hit an obstacle in that there is a secured loan which was paid off in the early '90s but it is still listed as outstanding on the title deeds. The loan was with Cedar Holdings Limited, which is now a dormant company and comes under Black Horse Finance Management. I have called them today and been given a number for their secured legal department in Cardiff, but the number is constantly engaged. We are trying to get proof that the loan has actually been repaid, can anyone give me any advice on the best way to take this forward, apart from trying to call them constantly? Any help would be greatly appreciated!! Thank you!!

Hi I am the executor for my late mother's estate and we are in the process of selling her house. We have hit an obstacle in that there is a secured loan which was paid off in the early '90s but it is still listed as outstanding on the title deeds. The loan was with Cedar Holdings Limited, which is now a dormant company and comes under Black Horse Finance Management. I have called them today and been given a number for their secured legal department in Cardiff, but the number is constantly engaged. We are trying to get proof that the loan has actually been repaid, can anyone give me any advice on the best way to take this forward, apart from trying to call them constantly? Any help would be greatly appreciated!! Thank you!! -

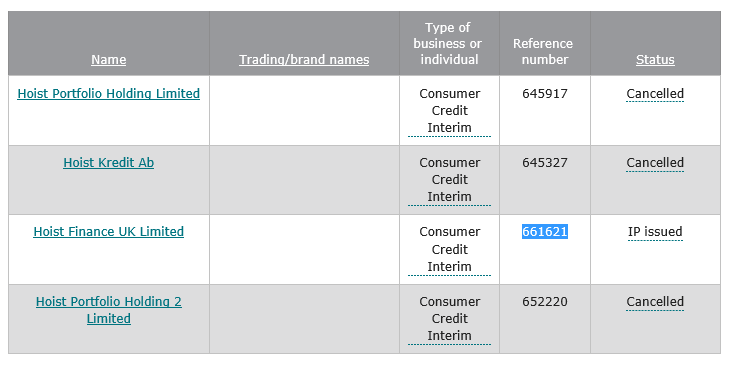

Upon checking the new FCA Public Register which is listing "Interim Permissions" in its transitional role from the OFT, I find that Hoist wildcard returns 4 results : Hoist Portfolio Holding Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Portfolio Holding 2 Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Kredit Ab (Presumably Swedish Parent Company) - IP CANCELLED Hoist Finance UK Limited - Reference Number 661621 - IP ISSUED Having received a letter from Robinson Way (As we know now owned by Hoist Finance UK Limited) they state that they have purchased an account from MKDP LLP (Compello - Hoist Director is director of Compello also). They state quite clearly and unambiguously that the alleged new beneficial owner of the account is Hoist Portfolio 2 Limited, who clearly are not registered nor authorised to engage in CC activity, and as such cannot legally instruct their associate company Robinson Way to attempt any form of recovery on their behalf. This latest threat to the consumer has all the hallmarks and modus operandi of the last bunch of cowboys who fought their corner for so long and then voluntarily surrendered their licences. I'm not mentioning names, but everyone knows whom I'm referring to. This is now the same old story, one director pulling the strings with an absolute labyrinth of companies who are nothing more than a file on a shelf and a brass plate on an accountants door, representing the fiddles of the strings. I'm making it my business to enquire with the FCA as to the status of Hoist Portfolio 2 Holding Limited just to see and hear from them directly their legal status. They would probably just BS consumers and say "oh well we're all part of the same group" blah blah blah - now where have I heard that before - sounds familiar. Would appreciate all your comments on this matter. Ive been in Court before with people as a MacKenzie Friend against the last mob who tried to collect accounts whilst unauthorised and tried to wriggle with intertwined companies. The Judge generally sees right through it.

Upon checking the new FCA Public Register which is listing "Interim Permissions" in its transitional role from the OFT, I find that Hoist wildcard returns 4 results : Hoist Portfolio Holding Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Portfolio Holding 2 Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Kredit Ab (Presumably Swedish Parent Company) - IP CANCELLED Hoist Finance UK Limited - Reference Number 661621 - IP ISSUED Having received a letter from Robinson Way (As we know now owned by Hoist Finance UK Limited) they state that they have purchased an account from MKDP LLP (Compello - Hoist Director is director of Compello also). They state quite clearly and unambiguously that the alleged new beneficial owner of the account is Hoist Portfolio 2 Limited, who clearly are not registered nor authorised to engage in CC activity, and as such cannot legally instruct their associate company Robinson Way to attempt any form of recovery on their behalf. This latest threat to the consumer has all the hallmarks and modus operandi of the last bunch of cowboys who fought their corner for so long and then voluntarily surrendered their licences. I'm not mentioning names, but everyone knows whom I'm referring to. This is now the same old story, one director pulling the strings with an absolute labyrinth of companies who are nothing more than a file on a shelf and a brass plate on an accountants door, representing the fiddles of the strings. I'm making it my business to enquire with the FCA as to the status of Hoist Portfolio 2 Holding Limited just to see and hear from them directly their legal status. They would probably just BS consumers and say "oh well we're all part of the same group" blah blah blah - now where have I heard that before - sounds familiar. Would appreciate all your comments on this matter. Ive been in Court before with people as a MacKenzie Friend against the last mob who tried to collect accounts whilst unauthorised and tried to wriggle with intertwined companies. The Judge generally sees right through it.

-

I am in the process of suing a limited company that owes me £16,000. They admit they owe the amount but just wont pay. My problem is that the companies registered office is at a firm of accountants. Do I have my court summons issued to there or to the home address of the director I have been dealing with. If I win the case and I have to send in bailiffs there would be no sense in using the registered office. Anyone help me? David Prince

-

Absolute Locate aka Global Debt Recovery Limited

InfoGeek posted a topic in Debt Collection Agencies

Had a letter earlier this week from: Absolute Locate Dear Mr x We require your assistance to verify information on behalf of a client. This is part of an investigation we are currently conducting Please contact ect ect No, I have not responded, and don't intend too. Letter states this registered office is for a Nat Bourner Huddersfeild HD2 1GN CCL 579084 DPLN ZA019311 Having done some homework and looking on this group, they are not who they say they are First off, the CCL 579084 is incorrect, Consumer credit number 579084 is for a Natalie Alice Bunyer not Nat Bourner as stated in this letter (She has married, but not changed the name) She also resides in Surrey not Huddersfeild this information is therefore falsely registered and constitutes either fraud and or deception. these people are in fact: Global Debt Recovery Limited Milbourne House 66-70 Coombe Rd New Malden, Greater London KT3 4QW I am assuming that their client will be: FV-1 INC of 25 CABOT SQUARE, CANARY WHARF, LONDON E14 4QA if you take a look here at: mylawer co uk - restriction of debt collectors They have already broken the following guidelines 1 Those contacting debtors not making clear who they are, who they work for, what their role is, what the purpose of the contact is 2 Not informing the debtor when their case has been passed on to a different debt collector 3 Passing on debtor details to debt management companies without the debtors informed prior consent i.e FV-1 INC will have passed any alleged debt onto Absolute Locate, who in turn will then pass that onto Global Debt Recovery Limited and all without my informed prior consent, add to that Absolute Locate is just a dummy office which IMO amounts to deception. Adding to this, they would’ve already broken the Data Protection Act by passing my details on. I will post more when I receive their first letter. But as you can see from my tone, I am not going to be messed with by idiots, I will be going straight for the jugular Ps. If (big IF) there is a debt, if would’ve to be more than 8 years old or more, so Statue Barred. -

Civil Enforcement Limited claim issued at CCBC It's been acknowledged and notified will defend via NCOL The POC is for 'Outstanding Debt and Damages'and a note 'I will provide the defendant separate detailed particulars within 14 days of service of the claim form' The detailed particulars of claim were received on day 12. They mention Vine v Waltham Forest (2000) 4 ER 169 - When defendant parked they accepted by their conduct the conditions of parking They also point to case of Parking Eye V Beavis Supreme Court Ruling (establish legality of car park operators to charge...) They have added a 'Statement of Truth' and it's signed by their solicitor. They have attached a Schedule of Information which indicates the Site Details and Registration etc the Summary of Terms states it's a Maximum Parking Allowance exceeded I am helping the defendant with this as they have tried to deal with Civil Enforcement directly but got nowhere. The 'Incident' was on 08/04/2015 it's a 5 hour 'stay' but the defendant was over stayed by over 2 hours. The site has a cinema and number of eateries, they were parked for those purposes. I have looked at Received Court Papers From A Private parking Speculative invoice?? I will continue to hunt the threads but a defence needs to be prepared, I am going to see the site as I am pretty sure the sinage is rather poor however I wanted to check the following: If the ANPR camera is located at the 'entrance' to the car park even though you would need to drive over 100m to reach the 1st 'space' (or notice) does the parking notice not need to be displayed at the ANPR site?? Any other threads or specific help would be much appreciated.

Civil Enforcement Limited claim issued at CCBC It's been acknowledged and notified will defend via NCOL The POC is for 'Outstanding Debt and Damages'and a note 'I will provide the defendant separate detailed particulars within 14 days of service of the claim form' The detailed particulars of claim were received on day 12. They mention Vine v Waltham Forest (2000) 4 ER 169 - When defendant parked they accepted by their conduct the conditions of parking They also point to case of Parking Eye V Beavis Supreme Court Ruling (establish legality of car park operators to charge...) They have added a 'Statement of Truth' and it's signed by their solicitor. They have attached a Schedule of Information which indicates the Site Details and Registration etc the Summary of Terms states it's a Maximum Parking Allowance exceeded I am helping the defendant with this as they have tried to deal with Civil Enforcement directly but got nowhere. The 'Incident' was on 08/04/2015 it's a 5 hour 'stay' but the defendant was over stayed by over 2 hours. The site has a cinema and number of eateries, they were parked for those purposes. I have looked at Received Court Papers From A Private parking Speculative invoice?? I will continue to hunt the threads but a defence needs to be prepared, I am going to see the site as I am pretty sure the sinage is rather poor however I wanted to check the following: If the ANPR camera is located at the 'entrance' to the car park even though you would need to drive over 100m to reach the 1st 'space' (or notice) does the parking notice not need to be displayed at the ANPR site?? Any other threads or specific help would be much appreciated. -

Hi I have a long running problem with a local limited company. His latest attempt to get out of it is to resign as sole director and let the company get struck off, its now showing proposal to strike off! He has over £3000 of my money and the asset how do I deal with this, can I still take the company to court? I was hoping the fact he isn't winding the company up "properly" and taken all the assets and capital out of the company would mean he is guilty of wrongful trading and that I could go after him personally? Or am I best trying to get the faulty goods back and cutting my losses? Urgent advice please!

Hi I have a long running problem with a local limited company. His latest attempt to get out of it is to resign as sole director and let the company get struck off, its now showing proposal to strike off! He has over £3000 of my money and the asset how do I deal with this, can I still take the company to court? I was hoping the fact he isn't winding the company up "properly" and taken all the assets and capital out of the company would mean he is guilty of wrongful trading and that I could go after him personally? Or am I best trying to get the faulty goods back and cutting my losses? Urgent advice please! -

Hi, this is one of two claims I currently have going against me. Both of which are close to statute barred. This is my bigger worry of the two as this one is only statute barred if you go from the date the last payment was made, however it is not quite six years statute barred if it goes from the date the first payment was missed. Name of the Claimant ? Arrow Global Guernsey Limited Date of issue – 11/12/15 Date to submit defence = 12th Jan (33 days in total) - What is the claim for – The claimant claims payment of the overdue balance from the Defendant(s) and MBNA dated on or about October 06 2003 and assigned to the claimant on Dec 20 2001 Particulars a/c no. 444444444555555555 Date :18/11/2015 Item: Default Balance Value: £8200 Post Refrl Cr: Nil Total: £8200ish What is the value of the claim? £8200ish Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Credit card When did you enter into the original agreement before or after 2007? before Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? yes , I received a notice dated 09th march 2010 Did you receive a Default Notice from the original creditor? yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? I dont think so Why did you cease payments? Did a CCA request as I couldn't keep up with payments. I took nearly three months to receive a signature document so account was placed in dispute and payments ceased What was the date of your last payment? 02 december 09 Was there a dispute with the original creditor that remains unresolved? yes, following my CCA request I received a photocopy of a tear off slip with my name on and on the rear of the photocopy was a photocopy of terms and conditions, although they are the same size which makes it look as though they are from the same tear off slip I noticed they have different document reference numbers and dont believe the photocopy of the rear I received was the true rear. Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? no

Hi, this is one of two claims I currently have going against me. Both of which are close to statute barred. This is my bigger worry of the two as this one is only statute barred if you go from the date the last payment was made, however it is not quite six years statute barred if it goes from the date the first payment was missed. Name of the Claimant ? Arrow Global Guernsey Limited Date of issue – 11/12/15 Date to submit defence = 12th Jan (33 days in total) - What is the claim for – The claimant claims payment of the overdue balance from the Defendant(s) and MBNA dated on or about October 06 2003 and assigned to the claimant on Dec 20 2001 Particulars a/c no. 444444444555555555 Date :18/11/2015 Item: Default Balance Value: £8200 Post Refrl Cr: Nil Total: £8200ish What is the value of the claim? £8200ish Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Credit card When did you enter into the original agreement before or after 2007? before Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? yes , I received a notice dated 09th march 2010 Did you receive a Default Notice from the original creditor? yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? I dont think so Why did you cease payments? Did a CCA request as I couldn't keep up with payments. I took nearly three months to receive a signature document so account was placed in dispute and payments ceased What was the date of your last payment? 02 december 09 Was there a dispute with the original creditor that remains unresolved? yes, following my CCA request I received a photocopy of a tear off slip with my name on and on the rear of the photocopy was a photocopy of terms and conditions, although they are the same size which makes it look as though they are from the same tear off slip I noticed they have different document reference numbers and dont believe the photocopy of the rear I received was the true rear. Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? no -

I parked at private car park of my solicitor with his permission. However, I did not display visitor's pass, as I only went there to sign a document and was seen straight away. I never received ticket, app. 10 days later, I've received a letter from company called Private Parking Solutions (London) Ltd. with PCN. The letter was sent later then it was dated. I wrote to them and asked my solicitor to write to them as well, which he has done. Never the less, they rejected my explanations and told me that I must pay or could appeal to IAS, which is independent authority. This company IAS accepts only online appeals, and hence I completed the form and was waiting to their decision. I never received any reply from them. On Saturday I received a letter from debt collection agency UCS, which demands now £160.00 ( initial fine was £100.00 or £60.00 if paid within 14 days and I started appeal within that period). The letter is stating that my appeal was rejected. That "Independent Adjudicators" are actually a private company number 08248531. I feel as they all part of the same gang and only interested to get as much as they can away with. IAS has no telephone number and I could only email them via their website, but since I did not receive any respond from them in the past, I am not sure they will bother with replying to me now. I will really appreciate if somebody could advise me if I have to pay PCN if I parked on private car park with owner's permission? And also even if PCN is valid, how should I deal with the fact that no reply was sent to me and that Independent Adjudicators are private company not some sort of authorities? Is it even legal? Could anybody advise me? I went to sign some documents by a notary and parked outside his office on their car park, which he allows me, but usually I ask for a visitor pass. However, on that date I saw him straight away and hence did not bother with a pass. A couple of weeks later I received a letter from London Parking Solutions with PCN. I appealed and also asked the notary, who is also the owner of that LLP to write to them, which he did. They ignored his plea and rejected my appeal, I appeal to ISA, never received any reply from them, and on Saturday received a letter from UCS, debt collection agency stating that my appeal was rejected and now I have to pay additional administration fee or they take me to court. I email them about never receiving ISA decision, but how can I proof it? Also they never provided any evidences of how long I was parked there etc. Should I pay whole amount or offer £60.00 on basis that as far as I know my case is still on hold and only by receiving this letter I became aware that the Private Parking Solutions are still demanding their fee?

-

I have been issued a County Court Business Centre Claim form (Northampton unit) from Hoist at a St Helier, Jersey address. It is dated 7 Jan 15 and concerns £7043 (against an old credit card?) plus a further 3379.60 interest . The claim say that that amount due is from 6 Jan 2010 and I certainly haven't been in contact with them in the meantime. Does this mean that it actually covered by the statute limitation of 6 years (out by a day?) and they trying it on? Can I request cancellation under the limitation and also as I am uncertain as to the actual debt itself can I request proof of the original agreement and signature? And also proof that I have contacted or paid anything in the elapsed 6 years? I unfortunately only have till 21 Jan to reply to the court so any help appreciated. Thanks

I have been issued a County Court Business Centre Claim form (Northampton unit) from Hoist at a St Helier, Jersey address. It is dated 7 Jan 15 and concerns £7043 (against an old credit card?) plus a further 3379.60 interest . The claim say that that amount due is from 6 Jan 2010 and I certainly haven't been in contact with them in the meantime. Does this mean that it actually covered by the statute limitation of 6 years (out by a day?) and they trying it on? Can I request cancellation under the limitation and also as I am uncertain as to the actual debt itself can I request proof of the original agreement and signature? And also proof that I have contacted or paid anything in the elapsed 6 years? I unfortunately only have till 21 Jan to reply to the court so any help appreciated. Thanks -

checking my credit file on noddle and it shows a debt just over 1k the lender being 1st credit. the account start date is 24/08/2009 but the account history only shows from may 2015 to Oct 2015 all of which are shown as defaults. however the default date is shown as 28/03/2014, probably when 1st credit took over the debt. i don't have any clue as to who the original lender was but suspect it was a payday loan probably defaulted on it soon after it was taken out. the problem i have is if i did default soon after the loan was taken then it should rightly almost be statute barred. if i contact them to find out more do i risk restarting everything again?

-

Good evening all, I would be grateful for any advice that may be offered for the following case that I am pursuing through the Small Claims court. I have changed the exact dates, but the rest of the details are accurate: On 15 November 2013, I found a website offering for sale some consumer electronics. It was a computer peripheral (offered as a kit or fully assembled) that would enable me to expand my fledgling prototyping business. After many calls and emails with the Company Director, I went ahead with ordering an assembled and calibrated unit for the sum of £1000.00 (including courier delivery). The sale was agreed specifically for an assembled and calibrated unit, to be delivered within 10days. The director emailed after 11 days to state that he was waiting for parts and that I should receive the unit soon. Queue excuse again a few days later, but the Director offers to deliver the unit to me personally. After much chasing, a tracking number is received, but no goods. On querying with the Couriers, they state that the goods were never collected because no-one was ever found at the collection address. Repeat this cycle for approximately 6 months, at which point I contact Solicitors for advice. They do a search and advise me that CompanyA has been dissolved on the 22 June 2014 (effective 15/06/2014). No legal recourse as there is no legal entity to pursue. News to me. I complain to Companies House (CH), but am told that I had 3months to object to the Dissolution and that's that. They advise to continue communicating in the hope that the goods will arrive. The Director keeps up the promises and the goods never arrive. A request is submitted for delivery of the goods or full refund of the purchase price. This is ignored. The Director eventually ignores my emails and phone calls. The Director randomly emails me with another false Tracking Number in September 2014, to which I respond that I know he is making false statements and that I have reported him to the authorities. He replies to say 'sorry to hear but understandable. Machine will be sent soon'. I complain to Trading Standards (TS) and the Police Fraud squad (AF) and am advised that although I have no legal recourse, I should still pursue the matter by persisting in asking where the goods are/when they will arrive. AF advises that I should not under any circumstances give this individual any more money if he gets back in touch. Following the dissolution of CompanyA, I go back to his website where I find he is offering the same goods and services, but now under CompanyB. The terms and conditions on the website are still listed as CompanyA. I get back in touch with TS and AF and complain again, also contacting CH to report what I believe was Phoenix Company action. No further action by CH as he applied for Voluntary Dissolution. No further communication with the Director is received until February 2015 when he comes back on the scene, apologising and saying that's it's been all a big mix up and that CompanyB is now responsible for delivering the order. Again, news to me. I consider that maybe he is serious following the AF/TS complaints and is going to deliver the goods. On reading back through the correspondence, he does state that it is his intention to close the company 'within the next three months', but not that he has already filed the application. In hindsight, it is clearly his intent to close the company before he even resumes contact. Further, he states in a later email, that only those who have opted to NOT receive a machine would have received a copy of the DS01. Alarm bells ring and on checking, I find that he has an active application for dissolution. I am just in time to register an objection which is upheld. I notify the Director of my objection and continue to appeal to him for mediation, compromise... a solution. He repeatedly requests to discuss things over the phone and after a few weeks of waffle, I decline further contact by phone. I challenge him with regards to the DS01 and he emails a copy through, stating that he has never hidden this from me and that I should have received one in the post. No proof is provided, no communication is received from this Director or his Companies by post. Ever. I make him aware that I am contemplating legal action. His response is that CompanyB is ONLY fulfilling the orders. When I challenge his handling of the situation, his response is to ask if I want to invest £3000.00 in his business. I ignore this. A 'Notice Before Action' (NBA) is issued to his business address and home address. The home address one is signed for, the business address one is returned a month later, uncollected. He acknowledges receipt of the Notice. He misses the deadline to respond to the NBA. He later offers that funds are low, so he would not challenge legal action. He also asks that, given my history, would I be interested in an investment opportunity? I lodge a further complaint with the Director, who ignores the complaint and instead offers 49% of his business for £5000.00 and states he would then be able to issue my refund. (?) I again complain to CH. After objecting to dissolution for 6+ months, I progress to legal action. On legal advice, the Solicitor questions the ProForma, the only document I have with an order number on it. I question if it is acceptable proof of purchase and he agrees that it is. It is unclear who the liability for the ProForma is with - I assume it is with the Company. Solicitor advises naming Director and Company jointly, which I do. On investigation since submitting the Claim: The Director is sole member and sole Director of Companies A, B and C. (You cannot deal with anyone else in the company other than him: He is a one man band.) I find that the Director's DOB on the Certificates of Incorporation are listed differently between CompanyA and CompanyB. CompanyC is registered with incorrect Director's contact details. Director is later removed and reinstated with contact details for CompanyB's business address. CompanyB and C share the same trading address. The Director alleges that CompanyB and the unit are closed, but on investigation, I am told that the named unit is occupied with an active lease and no notice of termination. CompanyA's application for Dissolution was dated 3 months and two days after I sent the payment (17/02/14 and 15/11/13 resp). Granted he has not (to my knowledge) traded within that 3 month period prior to the application - I question whether there is an indication, seeing as how there were 2 days between sending the money and making the decision to no longer trade; that there was an intent to take the money without ever fulfilling the order. This would seem to be corroborated by not being notified of the Dissolution of CompanyA. CompanyA and the Director are repeatedly named in a user forum specific to this industry that I recently find. There are numerous complaints almost identical to my own. It appears that previous legal action has been settled in mediation with questionable/pitiful results. No accounts have been submitted for any Company. Only one return is ever filed for CompanyA, and all documents show as Outstanding (that's not for performance) with CH. As all have been/ are being Voluntarily Dissolved, CH will not take further action, even in light of his failure to notify Creditors and suspicions of sharp practice. These are stated offences in the Companies Act 2006. The Solictor's reaction to the ProForma bugs me. There is a logo that states CompanyA, but the only mention of LTD is under his name as Director of CompanyA Ltd. There is no inclusion of the Company Number and no VAT details. The office address is both the Company's address and the Director's home address. No invoice or receipt is ever received from CompanyA. I only have email confirmation that the Director received the money. Is the ProForma proof of an agreement between the company and myself, or the Director and myself? I call HMRC for clarification, they advise that the ProForma I originally received is not a recognised Invoice. It is considered to be a quote for goods and services. They cannot comment on whether the agreement is with the individual or the company. CH advise they cannot comment on the legality of the document, but based on my continued evidence and pending court case, the objections are being upheld pending Judgement. Director contacts me to complain that I have named him personally as a Defendant. I ask him who received the original payment. He does not respond. The Director has just defended the claim against himself, but nothing has been received for the company. Default Judgement has been removed now that his defense has been submitted. His defense is that the order is with the Company and that I already know this as I am objecting to it's Dissolution with CH. He states that he has sent me the DS01, (which he did, but only after I demanded a copy of it (and months after the application was submitted)). Whilst I have continually tried to be reasonable, his persistent evasion of any credible information leads me to believe that he is either incompetent or blatantly defrauding his customers. I only have his word that the goods exist and that the agreement is with the Company. As you can imagine, after 2 years+ of outright deceit, I am very suspicious of anything he states. I believe that I am waiting for a question pack from MCOL in order to progress to Judgement, but am concerned that the debt is going to be lumped on the Company and he'll close it without paying. Actually, I think it's obvious that he has been trading whilst insolvent, but I do not know what further powers (as a Creditor) I have to prove/charge him as personally liable. Was I wrong to name him as a Defendant in the first place? The claim covers the basic facts, but I am concerned because of the preconceived response to Director's liability in these situations. I don't want to waste the Court's time, but I do want to submit as much documentary evidence as possible for the Judgement. Is anyone able to offer any further advice? Many thanks in advance for your help.

Good evening all, I would be grateful for any advice that may be offered for the following case that I am pursuing through the Small Claims court. I have changed the exact dates, but the rest of the details are accurate: On 15 November 2013, I found a website offering for sale some consumer electronics. It was a computer peripheral (offered as a kit or fully assembled) that would enable me to expand my fledgling prototyping business. After many calls and emails with the Company Director, I went ahead with ordering an assembled and calibrated unit for the sum of £1000.00 (including courier delivery). The sale was agreed specifically for an assembled and calibrated unit, to be delivered within 10days. The director emailed after 11 days to state that he was waiting for parts and that I should receive the unit soon. Queue excuse again a few days later, but the Director offers to deliver the unit to me personally. After much chasing, a tracking number is received, but no goods. On querying with the Couriers, they state that the goods were never collected because no-one was ever found at the collection address. Repeat this cycle for approximately 6 months, at which point I contact Solicitors for advice. They do a search and advise me that CompanyA has been dissolved on the 22 June 2014 (effective 15/06/2014). No legal recourse as there is no legal entity to pursue. News to me. I complain to Companies House (CH), but am told that I had 3months to object to the Dissolution and that's that. They advise to continue communicating in the hope that the goods will arrive. The Director keeps up the promises and the goods never arrive. A request is submitted for delivery of the goods or full refund of the purchase price. This is ignored. The Director eventually ignores my emails and phone calls. The Director randomly emails me with another false Tracking Number in September 2014, to which I respond that I know he is making false statements and that I have reported him to the authorities. He replies to say 'sorry to hear but understandable. Machine will be sent soon'. I complain to Trading Standards (TS) and the Police Fraud squad (AF) and am advised that although I have no legal recourse, I should still pursue the matter by persisting in asking where the goods are/when they will arrive. AF advises that I should not under any circumstances give this individual any more money if he gets back in touch. Following the dissolution of CompanyA, I go back to his website where I find he is offering the same goods and services, but now under CompanyB. The terms and conditions on the website are still listed as CompanyA. I get back in touch with TS and AF and complain again, also contacting CH to report what I believe was Phoenix Company action. No further action by CH as he applied for Voluntary Dissolution. No further communication with the Director is received until February 2015 when he comes back on the scene, apologising and saying that's it's been all a big mix up and that CompanyB is now responsible for delivering the order. Again, news to me. I consider that maybe he is serious following the AF/TS complaints and is going to deliver the goods. On reading back through the correspondence, he does state that it is his intention to close the company 'within the next three months', but not that he has already filed the application. In hindsight, it is clearly his intent to close the company before he even resumes contact. Further, he states in a later email, that only those who have opted to NOT receive a machine would have received a copy of the DS01. Alarm bells ring and on checking, I find that he has an active application for dissolution. I am just in time to register an objection which is upheld. I notify the Director of my objection and continue to appeal to him for mediation, compromise... a solution. He repeatedly requests to discuss things over the phone and after a few weeks of waffle, I decline further contact by phone. I challenge him with regards to the DS01 and he emails a copy through, stating that he has never hidden this from me and that I should have received one in the post. No proof is provided, no communication is received from this Director or his Companies by post. Ever. I make him aware that I am contemplating legal action. His response is that CompanyB is ONLY fulfilling the orders. When I challenge his handling of the situation, his response is to ask if I want to invest £3000.00 in his business. I ignore this. A 'Notice Before Action' (NBA) is issued to his business address and home address. The home address one is signed for, the business address one is returned a month later, uncollected. He acknowledges receipt of the Notice. He misses the deadline to respond to the NBA. He later offers that funds are low, so he would not challenge legal action. He also asks that, given my history, would I be interested in an investment opportunity? I lodge a further complaint with the Director, who ignores the complaint and instead offers 49% of his business for £5000.00 and states he would then be able to issue my refund. (?) I again complain to CH. After objecting to dissolution for 6+ months, I progress to legal action. On legal advice, the Solicitor questions the ProForma, the only document I have with an order number on it. I question if it is acceptable proof of purchase and he agrees that it is. It is unclear who the liability for the ProForma is with - I assume it is with the Company. Solicitor advises naming Director and Company jointly, which I do. On investigation since submitting the Claim: The Director is sole member and sole Director of Companies A, B and C. (You cannot deal with anyone else in the company other than him: He is a one man band.) I find that the Director's DOB on the Certificates of Incorporation are listed differently between CompanyA and CompanyB. CompanyC is registered with incorrect Director's contact details. Director is later removed and reinstated with contact details for CompanyB's business address. CompanyB and C share the same trading address. The Director alleges that CompanyB and the unit are closed, but on investigation, I am told that the named unit is occupied with an active lease and no notice of termination. CompanyA's application for Dissolution was dated 3 months and two days after I sent the payment (17/02/14 and 15/11/13 resp). Granted he has not (to my knowledge) traded within that 3 month period prior to the application - I question whether there is an indication, seeing as how there were 2 days between sending the money and making the decision to no longer trade; that there was an intent to take the money without ever fulfilling the order. This would seem to be corroborated by not being notified of the Dissolution of CompanyA. CompanyA and the Director are repeatedly named in a user forum specific to this industry that I recently find. There are numerous complaints almost identical to my own. It appears that previous legal action has been settled in mediation with questionable/pitiful results. No accounts have been submitted for any Company. Only one return is ever filed for CompanyA, and all documents show as Outstanding (that's not for performance) with CH. As all have been/ are being Voluntarily Dissolved, CH will not take further action, even in light of his failure to notify Creditors and suspicions of sharp practice. These are stated offences in the Companies Act 2006. The Solictor's reaction to the ProForma bugs me. There is a logo that states CompanyA, but the only mention of LTD is under his name as Director of CompanyA Ltd. There is no inclusion of the Company Number and no VAT details. The office address is both the Company's address and the Director's home address. No invoice or receipt is ever received from CompanyA. I only have email confirmation that the Director received the money. Is the ProForma proof of an agreement between the company and myself, or the Director and myself? I call HMRC for clarification, they advise that the ProForma I originally received is not a recognised Invoice. It is considered to be a quote for goods and services. They cannot comment on whether the agreement is with the individual or the company. CH advise they cannot comment on the legality of the document, but based on my continued evidence and pending court case, the objections are being upheld pending Judgement. Director contacts me to complain that I have named him personally as a Defendant. I ask him who received the original payment. He does not respond. The Director has just defended the claim against himself, but nothing has been received for the company. Default Judgement has been removed now that his defense has been submitted. His defense is that the order is with the Company and that I already know this as I am objecting to it's Dissolution with CH. He states that he has sent me the DS01, (which he did, but only after I demanded a copy of it (and months after the application was submitted)). Whilst I have continually tried to be reasonable, his persistent evasion of any credible information leads me to believe that he is either incompetent or blatantly defrauding his customers. I only have his word that the goods exist and that the agreement is with the Company. As you can imagine, after 2 years+ of outright deceit, I am very suspicious of anything he states. I believe that I am waiting for a question pack from MCOL in order to progress to Judgement, but am concerned that the debt is going to be lumped on the Company and he'll close it without paying. Actually, I think it's obvious that he has been trading whilst insolvent, but I do not know what further powers (as a Creditor) I have to prove/charge him as personally liable. Was I wrong to name him as a Defendant in the first place? The claim covers the basic facts, but I am concerned because of the preconceived response to Director's liability in these situations. I don't want to waste the Court's time, but I do want to submit as much documentary evidence as possible for the Judgement. Is anyone able to offer any further advice? Many thanks in advance for your help. -

Hi Guys, A claim with an employment tribunal has been going through, and on Friday 15th 2016, and agreement was arranged as an out of court settlement to pay a fixed sum of £9,000 by Friday 22nd 2016. I have now been informed that the company is unable to make the payment as it does not have the available funds in the bank. the company is still active, does anybody know what I should be doing to get the funds paid? The agreement was set through ACAS. Thanks Guys

Hi Guys, A claim with an employment tribunal has been going through, and on Friday 15th 2016, and agreement was arranged as an out of court settlement to pay a fixed sum of £9,000 by Friday 22nd 2016. I have now been informed that the company is unable to make the payment as it does not have the available funds in the bank. the company is still active, does anybody know what I should be doing to get the funds paid? The agreement was set through ACAS. Thanks Guys -

Hi and thanks for looking at this thread. I am about to defend a claim from an old Sainsburys credit card debt which has literally just become statute barred...I hope! Name of the Claimant Arrow Global Limited Date of issue – 30th Nov 2015 Date to submit defence = 4pm 01 Jan16 (33 days in total) - What is the claim for – 1. The claim is for the sum of £7000 in respect of monies owing by the defendant on a credit agreement held by the defendant with Sainsburys Bank PLC under account number 44444455555 upon which the defendant failed to maintain payments. 2,A Default notice was served upon which the defendant and has not been complied with. 3 By virtue of a sale agreement between Sainsburys bank PLC and the claimant, the claim vested in the claimant who has a genuine interest. The defendant has been notified of the assignment by letter. What is the value of the claim £8000 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account - Credit card When did you enter into the original agreement before or after 2007/ - before Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. -- debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Not sure Did you receive a Default Notice from the original creditor? yes, notice dated 11th feb 2010 Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? I dont think so but couldnt be 100% sure Why did you cease payments? - first payment missed 24th November 2009 What was the date of your last payment? last payment made 24th October 2009 Was there a dispute with the original creditor that remains unresolved? sent CCA request which took 3 months to arrive. The document they sent had a signature on but it was really just confirming personal details and my signature on the bottom. On the rear of the photocopy they sent me were some reconstructed terms and conditions. I placed the account in dispute and stopped payments. I also asked for a photocopy of the actual rear of the document but one was never sent to me. Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? no

-

I initially had a credit card debt with MBNA which was then sold onto Max Recovery Limited. When the debt was originally sold it was under an IVA. Now the IVA has since been cancelled, so I have started written communication with Max Recovery Limited. As I understand it, when a debt has been sold on, there should be a Deed of Assignment to prove that Max Recovery Limited own the debt. I have asked for this document on 3 occasions Max Recovery Limited has not acknowledge this requests. To date Max Recovery Limited has sent the debt onto their own DCA a firm called Drysdenfairfax Solicitors for collection.Again, I asked their DCA for proof their client owns the debt, Drysden have not complied. I reported Drysden to the Solicitors Regulation Authority over the matter, the SRA said Drysden hasn't done anything wrong. So my question is this; because Max Recovery Limited have failed to provide proof they have purchased the debts, can they persue me for it!?

-

Hi I received a letter in September from Hoist Portfolio Holding 2 Limited stating the following and that I was to make payments to Robinson way. The first paragraph of the letter is as follows. " We are writing to notify you that MKDP LLP has assigned all of it's respective rights, titles and interest in respect of the above referenced account (Ex Welcome Finance Limited) to Hoist Portfolio Holding Limited effective 10/08/2015. The balance they say is £17580.00." This was a loan that I took out with Welcome Finance and was secured on my home which was subsequently repossessed in October 2010. Further down the letter it states that I should check my credit file and that this account will currently be showing under the name of MKDP LLP. However when I check my credit report (Both Experian and Noddle) there is no mention of this debt in either my Active, Default or settled accounts. When I spoke to Robinson way about this account, I said I would speak to Step Change and this gave me 30 days grace. However the time has now come when they will be contacting me again by phone. Before I speak to them I would like to know where I stand as if it was still a debt surely it would appear on my credit file. I look forward to some advice on this matter. Regards Kim Kitchener

Hi I received a letter in September from Hoist Portfolio Holding 2 Limited stating the following and that I was to make payments to Robinson way. The first paragraph of the letter is as follows. " We are writing to notify you that MKDP LLP has assigned all of it's respective rights, titles and interest in respect of the above referenced account (Ex Welcome Finance Limited) to Hoist Portfolio Holding Limited effective 10/08/2015. The balance they say is £17580.00." This was a loan that I took out with Welcome Finance and was secured on my home which was subsequently repossessed in October 2010. Further down the letter it states that I should check my credit file and that this account will currently be showing under the name of MKDP LLP. However when I check my credit report (Both Experian and Noddle) there is no mention of this debt in either my Active, Default or settled accounts. When I spoke to Robinson way about this account, I said I would speak to Step Change and this gave me 30 days grace. However the time has now come when they will be contacting me again by phone. Before I speak to them I would like to know where I stand as if it was still a debt surely it would appear on my credit file. I look forward to some advice on this matter. Regards Kim Kitchener -

Good morning. Unfortunately, on 03/10/2015 i was issued a Parking Charge Notice by Parking Control Management (UK) Limited for the sum of £60.00 whilst I was parked on a private car park. I had appealed on the grounds that the signs had been vandalised which of course was rejected by PCM and decided to follow it through with another appeal to The Independent Appeals Service and also this was dismissed. I have left it whilst seeking advice but PCM have now referred it over to Debt Recovery Plus Limited who are chasing me for the amount of £160.00 I'm not the best when it comes to this sort of stuff, and hope someone would be able to advise me further about the whole situation and where I stand. I have linked in an album as there are too many images to display on here of my PCN, Evidence and also the appeal that i submitted to TheIAS which can be viewed here: http://imgur.com/a/Eld1V Any help would be greatly appreciated as I do not want to pay these people a penny as they do not deserve it.

Good morning. Unfortunately, on 03/10/2015 i was issued a Parking Charge Notice by Parking Control Management (UK) Limited for the sum of £60.00 whilst I was parked on a private car park. I had appealed on the grounds that the signs had been vandalised which of course was rejected by PCM and decided to follow it through with another appeal to The Independent Appeals Service and also this was dismissed. I have left it whilst seeking advice but PCM have now referred it over to Debt Recovery Plus Limited who are chasing me for the amount of £160.00 I'm not the best when it comes to this sort of stuff, and hope someone would be able to advise me further about the whole situation and where I stand. I have linked in an album as there are too many images to display on here of my PCN, Evidence and also the appeal that i submitted to TheIAS which can be viewed here: http://imgur.com/a/Eld1V Any help would be greatly appreciated as I do not want to pay these people a penny as they do not deserve it. -

Good evening, I wondered if you could help me. I have received a county court claim form for a credit card debt. The credit card was capital one and the debt was passed to various solicitors over the years. The debt is now with Capquest and they have instructed Drydens Fairfax to manage the matter. This credit card was taken out over 6 years ago, however I believe the last payment made could be around the 5 or 6 year mark which if over 6 could make the debt statute barred. I have tried to find old paperwork to try and see when I last made payment but can't and I no longer bank with the particular bank from which the payments will have been made. I know I haven't made any payment since May 2010 and could be earlier. The issue date on the Claim a Form is 03 December 2015 and I know I have to comply with timescales. I cannot afford to have a CCJ registered against me as I am looking to purchase a house next year. I haven't received anything from anyone about this debt for around 4 years until a week or so ago when I got a letter from Drydens. They threatened legal action if I didn't contact them within 14 days. I contacted them within this period and emailed for more information. They emailed back to request a paragraph from me to confirm that I was happy to correspond via email I did this, received no further response apart from the Claim Form. I don't know what to do for the best. The debt is in excess of £2500. I also cannot find out when my last payment was. I don't know where to start. Do I acknowledge regardless? Do I attempt to defend with no evidence unless they can prove otherwise? I look forward to receiving your help Thank you

Good evening, I wondered if you could help me. I have received a county court claim form for a credit card debt. The credit card was capital one and the debt was passed to various solicitors over the years. The debt is now with Capquest and they have instructed Drydens Fairfax to manage the matter. This credit card was taken out over 6 years ago, however I believe the last payment made could be around the 5 or 6 year mark which if over 6 could make the debt statute barred. I have tried to find old paperwork to try and see when I last made payment but can't and I no longer bank with the particular bank from which the payments will have been made. I know I haven't made any payment since May 2010 and could be earlier. The issue date on the Claim a Form is 03 December 2015 and I know I have to comply with timescales. I cannot afford to have a CCJ registered against me as I am looking to purchase a house next year. I haven't received anything from anyone about this debt for around 4 years until a week or so ago when I got a letter from Drydens. They threatened legal action if I didn't contact them within 14 days. I contacted them within this period and emailed for more information. They emailed back to request a paragraph from me to confirm that I was happy to correspond via email I did this, received no further response apart from the Claim Form. I don't know what to do for the best. The debt is in excess of £2500. I also cannot find out when my last payment was. I don't know where to start. Do I acknowledge regardless? Do I attempt to defend with no evidence unless they can prove otherwise? I look forward to receiving your help Thank you