Ollieogb

-

Posts

13 -

Joined

-

Last visited

-

I have an old HSBC credit card debt for £7000. I received default notice back in 2010 and was paying £1 a month, until last year when I received a letter from HSBC confirming they cannot provide CCA and debt unenforceable, so I stopped payment. Moorcroft are now chasing for repayment plan. Is there a standard letter I can send them to say no cca and confirmed unenforceable so go away do not harass or do I just ignore. I dont have means to repay. I'm a carer for wife, so not working, my daughter has serious mental health issues, my mother has dementia and much of her support also fall on me, my father has passed away this August, and father in law losing sight. Do I tell them this.

-

yes still m&s

-

I have been making £1 a month payments to an M&S Credit Card debt since 2009. These were stopped in Nov 19 and CCA request and DSAR submitted. The credit card was initially an old M&S chargecard. I have been sent the attached CCA documentation for the credit card. Can I have an opinion whether this constitutes an enforceable document. M&S_CCA_Jan20.pdf

-

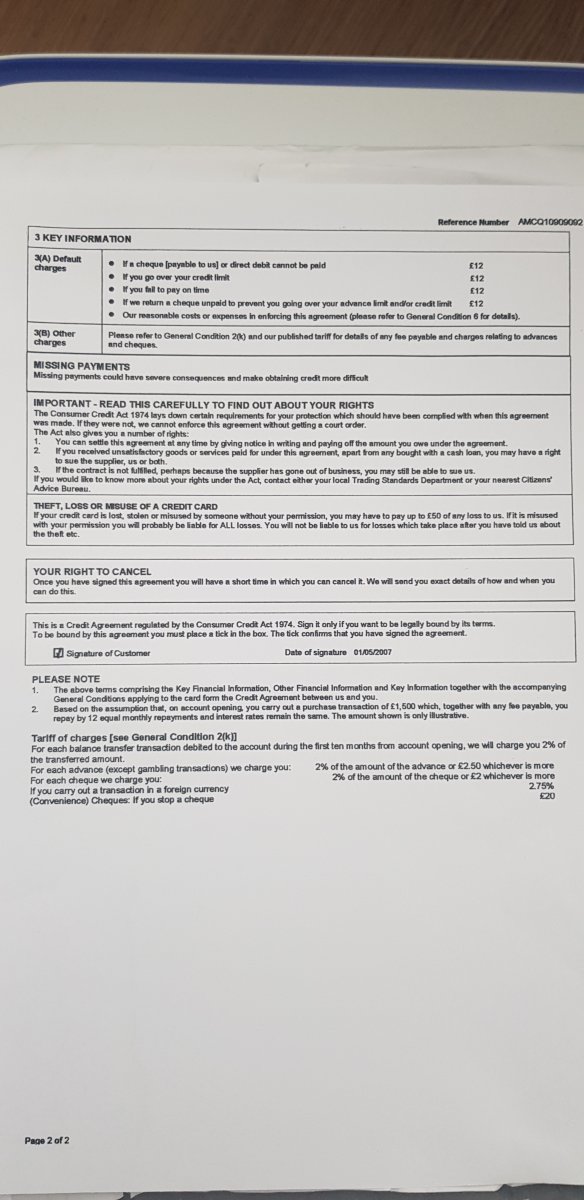

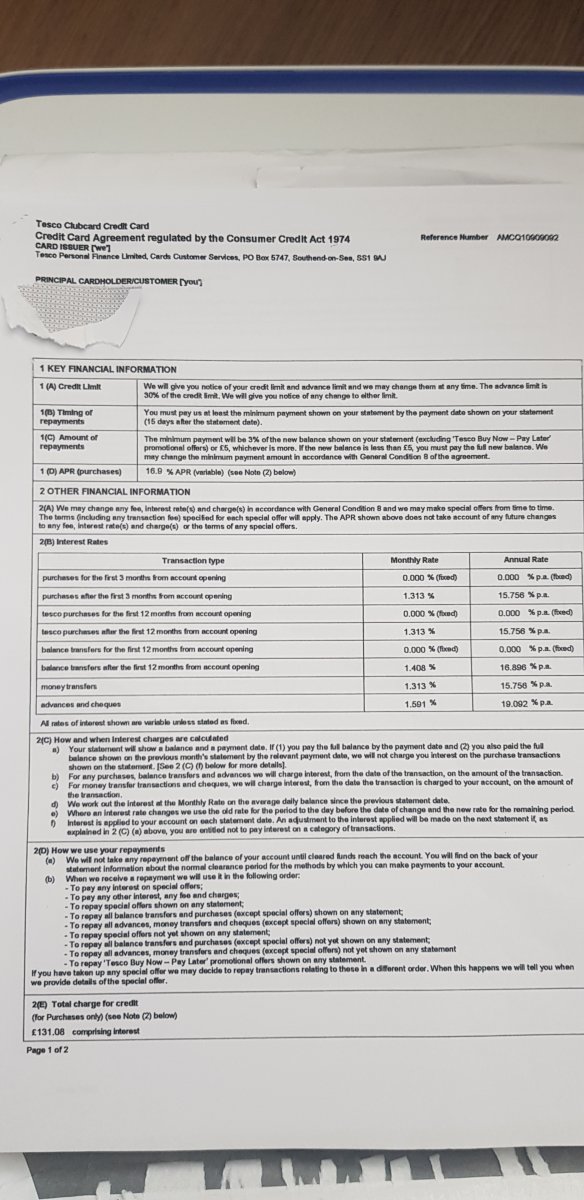

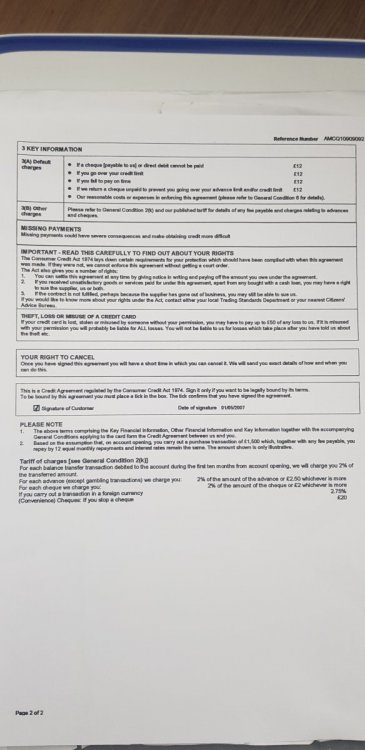

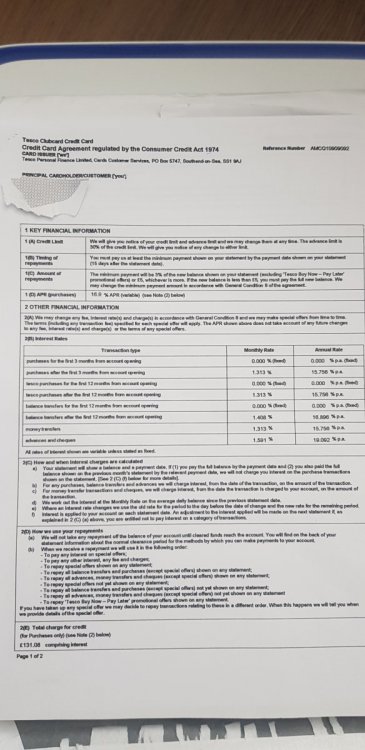

Can anyone confirm if the attached CCA is enforceable. Relates to a Tesco Credit Card acquired in May 2007 online. The debt has been purchased by Intrum.

-

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Defence was submitted on time, so waiting to hear now. Can I just double check re PRA cover letter in #17, is it best not to reply at all or should I just confirm in response to their 'if you disagree...'. comment "As you will be aware I have submitted my defence of your claim to the court" -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Thank you and Andy for swift response. I have one question re defence. One point In one of the no paperwork defence points states - on the alternative, as the Claimant claims to be an assignee of a debt, it is denied that the claimant has the right to lay claim due to contraventions of S136 Law of Property Act and S82A of CCA 1974. My Question is what does this mean/say? I just like to make sure i understand what I'm putting in if challenged. -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Docs attached. Really need to get this done today, if anyone could get back to me id be really grateful. q1 is cca valid given signature and terms not on same document and paras 4 to 18 not included? q2 are the assignments correct format. ive read should be from assignor and assignee? q3 assgnments don't show movement from mbna to varde should there be another assignment? q4 I have paid £1 a month which was amount initially agreed should my defence continue to be along lines of missing documentation or should I include commentary that £1 was the agreement entered into, financial circumstances unchanged, they have confirmed to continue with agreed amount if cant pay more, they were aware of circumstances when debt purchased etc? q5 cca shows credit limit of £11500 they have not confirmed how this has become £18k q6 should I respond to their letter from complaints and disputes? q7 their letter confirms all on hold for 30 days should I make point they haven't withdrawn from ccj activity so very sneaky of them, and that their 'we're here to help' approach contradicts with their actions. PRA scanned docs.pdf -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Thanks I'd drawn up defence based on missing documentation from the help you referred me to. However today I have received a copy of the signed section of cca which appears separate to the t&cs. On a separate page are terms 1 to 3, terms 4 to 19 are not attached and on this page . it states "The rest of your terms and conditions (paras 4 to 19) can be found in the full copy (which we must give to you under the CCA 1974) which is attached.' Question Is this enforceable I seem to recall reading the T&Cs and signature should all be on the same page. There are no interest rates showing and the credit limit showing is 11500 so below the amount claimed. No default notice has been sent. They have sent what they say are notices of assignment but I'm not clear what these should look like. Also the Aktiv Kapital states purchased from Varde Investments (Ireland) and not from mbna. This suggests should be another assignment from mbna to Varde - would you agree? -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Understand. I'm still going to send a defence, just wondered if there were defence templates. -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Received a response from PRA, looks standard confirming they've requested CCA from MBNA and advising me it can be a reconstituted copy of original. They say they've suspended all collection activity but not had anything from court. I need to send defence next week. Are there any templates for this or tips. -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Date is 21/2/17. Don't know re 19 + 14. I think it's 5 + 14 for acknowledging by I.e 12/3/17 (I have acknowledged already defend all) plus further 14 for defence I.e by 26/3/17 ? If you count 21/2 as day 1 then dates become 11/3/17 to acknowledge by and 25/3/17 for defence but I'm no expert. -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Thank you for swift response. I assume I request notice of assignments for MBNA to activ then activ to PRA. I do recall a number of calls I had with Activ saying I hadn't been informed they had taken it on from MBNA back in 2012. -

PRA Group Claimform - MBNA [old abbey card] credit card 'debt'

Ollieogb replied to Ollieogb's topic in Financial Legal Issues

Name of the Claimant ? PRA Group(UK) Limited Date of issue – 21/2/2017 Date of acknowledge = 11.03.2017 Date to submit defence = 24.03.2017 What is the claim for – 1.The Claimant claims the sum of £19k for debt and interest. 2.On xx/xx/03 the defendant entered into an agreement with MBNA for a credit card under reference xxxxxxxxxxxxxxxx. 3.On xx/xx/10 the defendant defaulted on the agreement with an outstanding balance of £18k. 4.On xx/xx/12 the debt of £18k assigned to Aktiv Capital Portfolio AS, Oslo, Zug branch, who itself assigned the debt to PRA Group (UK) Ltd on Xx/xx/14. Notices of assignment were sent to the defendant in accordance with S136 Law of Property Act 1925. 5.Payments of Xx.00 received up to xx/9/16 AND THE CLAIMANT CLAIMS 1. The sum of £18k 2. Statutory interest pursuant to section 69 of the County Courts Act 1984 at a rate of 8.00% per annum from xx/9/16 to xx/2/17 600 and thereafter at a daily rate of 3.97 until judgement or sooner payment. What is the value of the claim? 19700 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Credit Card When did you enter into the original agreement before or after 2007? Before Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes, not sure if Notice of assignment received from either Aktiv or PRA but might have. Did you receive a Default Notice from the original creditor? Think so Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No, not that I recall Why did you cease payments? Redundancy and drop in income. What was the date of your last payment? I don't recall, I entered into £1 a month Mon payment agreement following support from debt charity. Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management icon plan? Yes and have made £1 monthly payments since 2010 -

This is my first post so hope format is ok. I took out MBNA credit card (as Abbey National member) over 10 years ago following a change in financial circumstances was unable to make the repayments. I entered into an agreement to pay £1 a month to MBNA and a number of other creditors in 2010. My total unsecured debt is over £50k, and debt to MBNA was approx £16k. This debt was moved on to Aktiv Capital then to PRA Group. I have made these £1 payments since 2010 to all 3 organisations (I believe there may also have been another company in between MBNA and Aktiv but can't find details to confirm) Early this year I received a request from PRA litigation dept requesting payment of outstanding sum on an Abbey National card card or offer of repayment plan. The debt appears larger than I recall at 18600 appx. I responded to confirm circumstances unchanged and couldn't pay the o/s balance. I also requested they send me a copy of the CCA, as they were vague on start date. They have not sent the CCA but have issue court proceedings. I have completed and Back of service and confirmed I intend to defend all of the claim. I gather from forums I now need to issue a CPR, but I'm unsure which CPR to refer to. I've seen ref to CPR 18 but also CPR 31. Which should I refer to and is there a template letter I can refer to or use. At this point it appears to be in house PRA litigation taking action and not solicitor on their behalf so should I send CPR to the litigation department plus separate request to PRA for CCA. Its not clear on court N1 which address I send CPR to as address is PRA Bromley but litigation dept letter came from Scotland address. Any guidance would be appreciated.