Hi there,

Firstly, thanks for all your resources on this website, it has been very informative.

I wanted to ask a question as I wasn't really sure how to proceed with Motormile Finance in my particular situation.

So the long story short is:

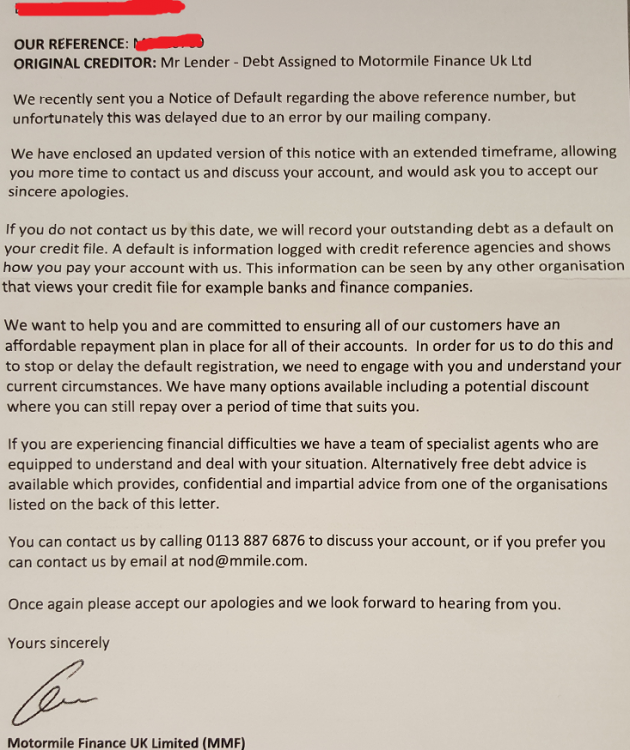

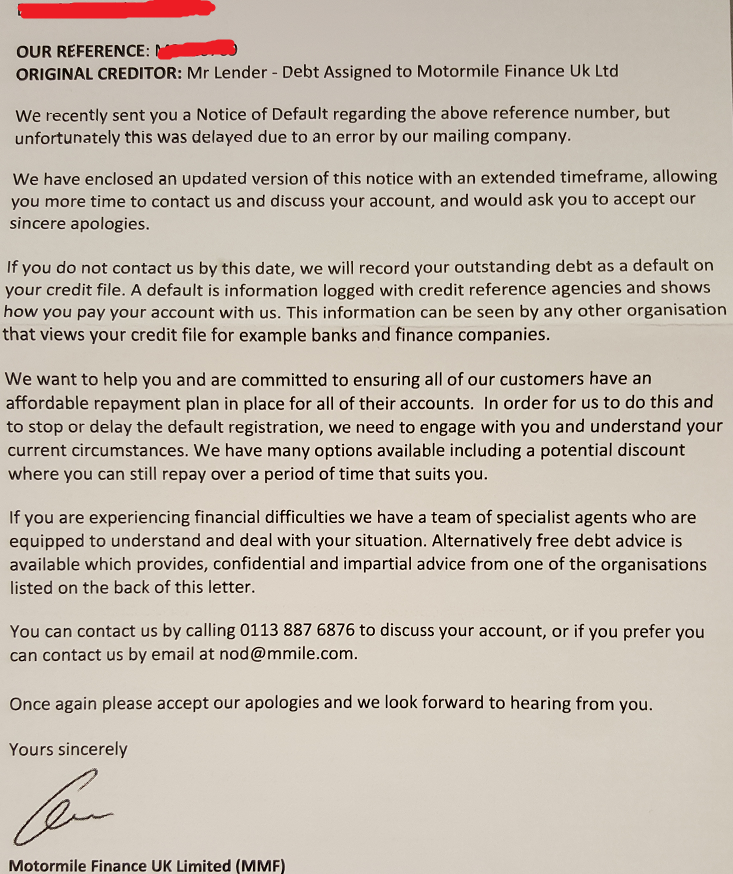

I received a letter the other day from Motormile, chasing debt from an old Payday loan going back to early 2013.

As the letter was threatening with default action (see "Attachment 1"),

I was curious as to why there were no other letters coming through with warnings.

I checked my e-mail and it turns out there's countless e-mails in my spam from Motormile from late 2013 onwards.

The e-mails are all the usual ones described in this forum:

initial discount offers on the debt,

then about a year and half of doorstep agent threats,

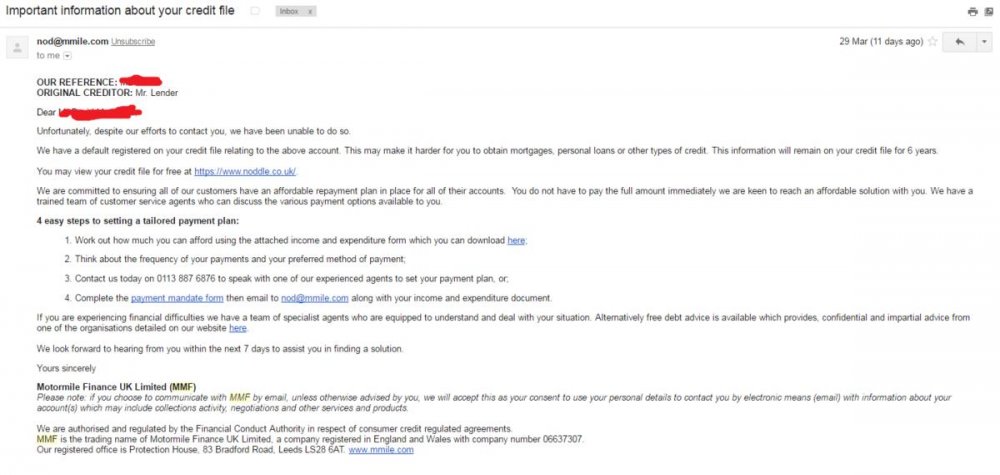

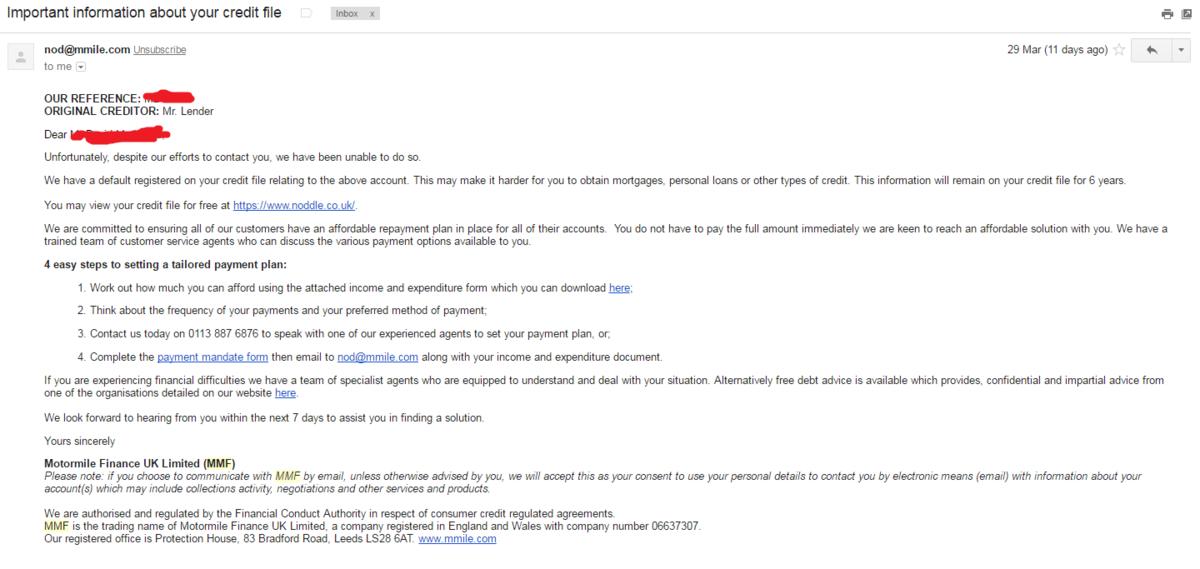

and the most recent one was an e-mail about a default, sent 11 days ago.

This e-mail is attached as "Attachment 2".

Due to getting this letter and checking those e-mails,

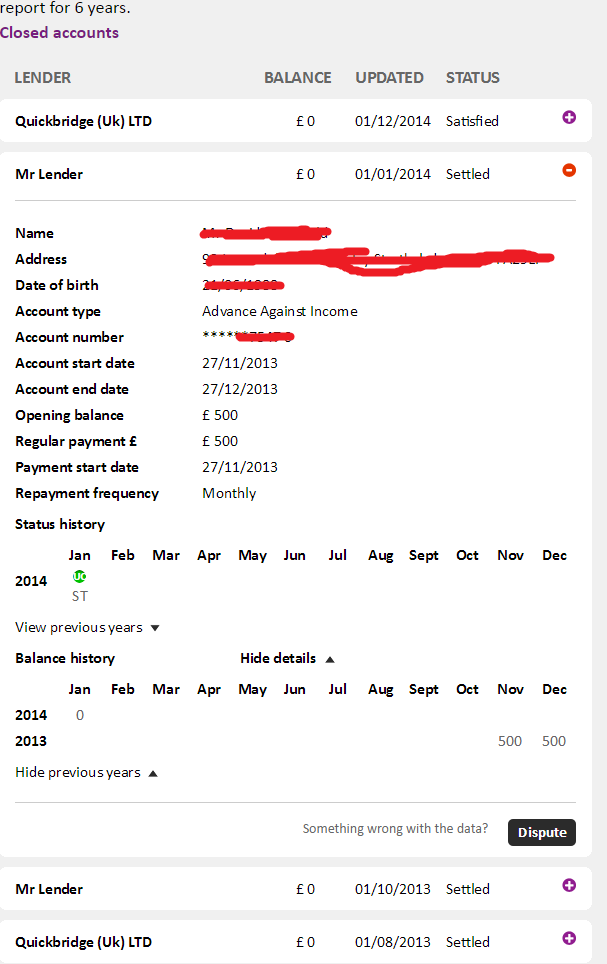

I have decided to check my credit rating on various credit checking sites to see where things were at (including Equifax).

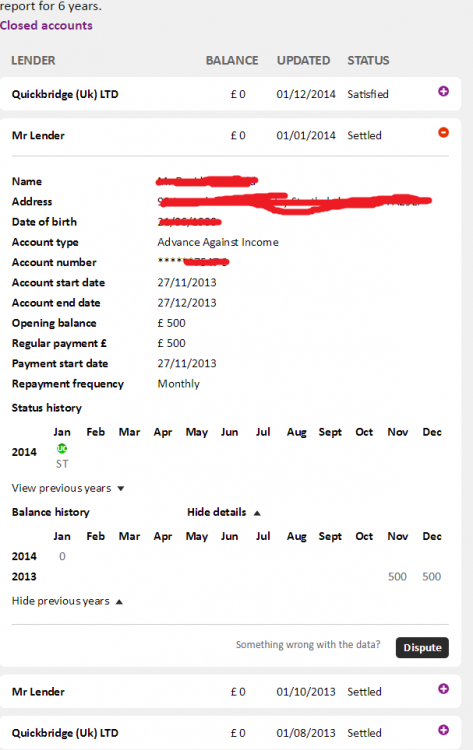

As shown in "Attachment 3", the last thing every recorded anywhere on my credit history

for Mr Lender was on January 2014 as "Settled" and I appear to have no defaults with them

- at some point they must have just sold my outstanding balance over to Motormile.

My question is:

If the original lender has never defaulted me (surprisingly),

can Motormile go ahead and create that default on their behalf.

From what I have read on here,

Motormile can not update the dates of existing defaults

- But I'm not sure whether or not they can create a default if the original lender never created one?

Note: In the attached e-mail they say they have a "default registered against you"

(which isn't true, at least yet)

and in the letter they say they will default me later this month if a resolution isn't met.

P.S: I know I really should have dealt with this debt back in the day instead of letting the problem "vanish".

I guess I am very apprehensive about getting in touch with Motormile

and paying off this large debt from many years ago,

back when I was stupid and desperate enough to take out a payday loan.

Thanks in advance for all advice on how to move forward!