BRIGADIER2JCS

-

Posts

32,198 -

Joined

-

Last visited

-

Days Won

19

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by BRIGADIER2JCS

-

-

Hi

Just been asked to help a friend,

D, who has recieved a letter from Provident saying that as of the 22nd August

they sold the account to AK and BCW are managing the account.

This letter is dated the 17th october 2014.

Also recieved is a letter from AK, dated 17th october 2014,

saying the have purchased the account from provident and the outstanding balance is £xxx.

These I believe, and cant say way incase they are watching, have been printed from the same printer.

Also recieved is a letter dated the 14th october 2014 from BCW saying they are disapointed the situation remains unsolved.

this is also a Settlement Offer offering him a exceptional opportunity to settle on highly favorable terms

they are willing to accept under £500 less as long as its paid in 3 months and

they reserve the right to register a deafult on the account then the client will mark it as partily settled.

Highly favorable to them l see.

I have noted the dates they must think that we have a time machine due to the dates.

D has not got any paperwork for this account so l am SARing Provident and CCAing BCW and will go from there.

l have agreed to battle for him,

he is a Mental health patient and

l fight all his battles for him.

He has asked l dont scan or put copies of letters on here but said l can give necessary details to help with the issue.

Just looking to no if there is anything new with Provident and if l could get the debt wiped completely based on the extortinate rates.

Any advise based on this would be a help l have been out of the battle for a few yrs now.

It is accepted practice for a debt purchaser to send a notice of assignment on behalf of the original creditor.

DNs can be sent by the OC the assignee or both.

-

nice one, one up on them is good.

I've take to winding dca's up to the point of breaking, two of them owe my wife £25000 and lowell owe £10000 so far, i know we will never see the money, but i worked them into the same "tick box" type contract that the credit companys use, and one dca rather than sending me a curt few lines sent me a 2 pager with obvious panic in them... I will reveal all when i'm done with dealing with the dca's, but i have a double edged sword with lowell, they used my information illegally and i will have them over the coals one way or another.. I hate dca **** bags.

[removed]

fotl?

-

I was going for an administration job and reached the second stage of the recruitment/interview process, when the company suddenly turned around and stated that I would have to undergo a credit check.

I have been having a few debt problems on the count of my recent divorce from my ex-partner and had to take out a myriad of loans to keep my family home with 2 young children from going under.

The company realised my bad credit score and in the end did not offer me the job because of it. I am struggling to pay my rent on the low income job that I am currently doing which I have been in for the last 5 years.... it's not enough and then when there is a glimmer of hope, it got taken away just like that due to a credit check!

So I am desperate to know what other people's experiences with this kind of issue has been and the methods you have taken to move past this.

How has this affected you? Because quite frankly, it's affected me and the up keep of my children badly....

Hi welcome to CAG,

Your " credit score" has nothing to do with the rejection, it is a day to day representation of how a credit app may be viewed by a potential lender, it is not anything more than a personal indicator.

Your problem is I suspect more to do with the conduct of your credit accounts.

Were you told credit checks would be made when applying for this job?

-

What if they send me the same stuff with a correct address ?

If that bit is wrong most likely the rest is!

A recon agreement Must Have,

Your name and address at the inception of the agreement and the Creditors Name and address at inception.

All the Ts & Cs at inception and closure of the account.

Any material amendments to the Ts & Cs during the life of the agreement.

Any documents mentioned in the agreement.

A current (not historical) statement of the account.

Any part wrong or missing means the recon does not comply.

You have spotted 1 error so you just reply that the recon is of no merit.

-

1

1

-

-

Hi

I have a summons from county court business centre.

The amount is over 10 thou.

The fee is listed as £410.

is this the actual cost, or have the complainants added their own fee?

That is the court fee!

-

Another Lowell Lemon debt goes down!!

-

And letter this morning,

Pay 70% and have file marked as partial settled on CRA

If not heard from in 10 days as Brig said Hamptons Legal.

Am quaking in my boots ........

SO Bl**dy predictable new me they are joke, more mays, might, could threats to follow then probably an offer of a discount as it's nearly Christmas.!!

-

Been a while again

got surprise on my doorstep from Marlin Financial Services with a copy of my reconstitued agreement as HSBC Bank have been unable to supple the original. It's a 'reconstitued agreement' which means it doesn't have my signature, there's no payment terms and it has has my address from 3 years ago (when i took the credit card, I lived at a completely different address) writen with a pen. Will add a scan later, but in the meantime - what should I tell them ? Been out of the game for a while now

got surprise on my doorstep from Marlin Financial Services with a copy of my reconstitued agreement as HSBC Bank have been unable to supple the original. It's a 'reconstitued agreement' which means it doesn't have my signature, there's no payment terms and it has has my address from 3 years ago (when i took the credit card, I lived at a completely different address) writen with a pen. Will add a scan later, but in the meantime - what should I tell them ? Been out of the game for a while now

Hi, Well that recon fails at the first hurdle it Must have your address as at the date the agreement was signed.

All you do is reply that the recon is rejected as it does not comply with the requirements laid down for a reconstituted agreement.

DO NOT tell them why it does not comply.

-

Acknowledge the claim, state defending in full.

Your defence seems solid no enforceable CCA.

-

Could you point me to this, Brig? Hear it a lot but never see it. Some people are confused because Barclaycard used to use CS before selling debt to HFO.

What’s ‘Chis Lancasters’? Excuse my slowness. It’s early...

Lancaster Solicitors in Chiswick.

Google Cograd, there's some data re Concilian CS CCS is in the small print.

-

Yes, Brig, it’s all under the Concilian banner – totally non-transparent Malta-registered company. Nowt to do with Credit Solutions, as far as I know.

My finger is well and truly as close to their pulse as I can keep it, until they’re all de-licensed for good. Best place I find for a pulse is the neck

There's mention of Credit Solutions on one of their websites DB.

There's a fairly large law firm in Chis Lancasters.

-

Hopster v Egg

in Egg

?With the greatest of respect Brigadier you and the Site team are not singing off the same hymn sheet re. SB. Site Team - Would you agree with this ?I do not understand your post?

Has any member of the site team challenged or disputed the advice given?

Contradictory statements made by you have " muddied the waters " here.

So unless I'm missing something I can see no reason for your "comment".

-

And I predict that a company called Cograd Ltd will rise from this. Odd that Cograd Ltd doesn’t seem to be registered with the ICO, nor does it seem to have a consumer credit licence, yet its people and suppliers (ex-HFO/Rox) are all talking about databases and portfolios of accounts. How odd.

Oh, and it seems to operate from Chiswick. Can anyone think of any solicitors in Chiswick?

Concillian Group (CCS collect/credit solutions?

-

Thank you UncleBG.

I want to sleep at night....

I still to this day can't believe that I could have stayed in Dubai without a cold prison cell.

Does anyone have any good websites please for template letters?

layercake please keep the questions on the open forum.

In response tom your last PM on payments you will have to work out an I&E statement to see what you can reasonably afford to offer as monthly payments, but from what I gather from the information so far it is unlikely that

small monthly payments will be accepted.

It also appears that a " forthwith" order was made by the court, which went unchallenged hence the CO.

-

John,

Does she still have the goods in her possession? It would appear not from#post 1.

This may cause a problem as unsolicited good or not the would be a common duty of care to make sure that the items were returned.

I presume that the goods are no longer accessible?

-

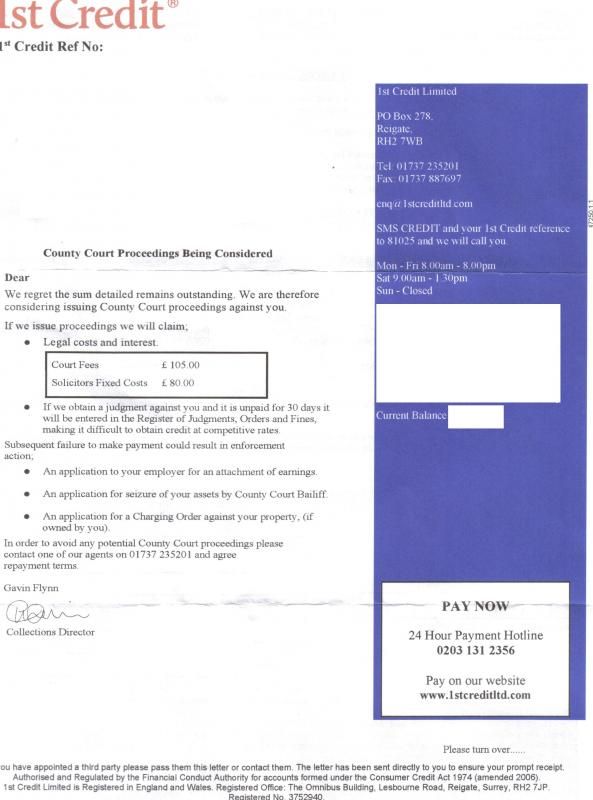

Hi All

Not been on here for a while, just need a bit off advice on this.

Its been very quiet from 1st Credit, until today when i received a threatagram through the post

.

.They actually want money of me in full or else

.

.Just a quick reminder this account was a Halifax account, then in 2012 they sold it to 1st Credit.

Here's what the letter said that came to me today.

So just need a bit of advice on what to do next.

Gazza

I take there is still no CCA around?

-

I am now being chased by MKRR.

They are insisting that when I informed them that the money paid in was a PPI refund I acknowledged the debt.

The agreement was taken out in 2006.

Their latest letter that arrived this week claims that due to MY misunderstanding of the situation they cannot assist me any further.

Reply to MKRR in a Formal Complaint.

Perhaps as follows:

Private & Confidential

FAO: Ms Sara Lambert

CEO the Compello Group

Same address as MKRR

Date:

Ref: use theirs

Dear Ms Lambert

I refer you to a letter from MKRR dated xx.xx.xxxx regarding an alleged debt originating from an account with Welcome Finance. Please not I do not acknowledge any debt to any company within the Compello Group

MKRR is claiming that a refund of PPI payments by the original creditor paid to this account restarted the 6 year period set down in the Limitations Act 1980 as you must be well aware this type of refund is not an admission of liability nor is a payment made by me and therefore has n effect on the becoming statute barred.

MKRR is making an unreasonable and unnecessary number of telephone calls to my number to an extent that this now amounts to harassment.

You are reminded of the 2014 Appeal Court Judgement in Roberts - v - BOS which laid down what amounts to harassment once a creditor has been informed in writing that contact by telephone must cease.

The alleged debt became statute barred some 18 months ago and I restate for clarification and for the avoidance of any misunderstanding; This alleged debt is Statute Barred and I will not now nor at any time in the future make any payment or offer of payment.

I now suggest that Compello/MKRR closes the file on this matter immediately and confirms in writing that it has done so, failure to do Will result in the matter being referred to the FCA and a complaint being made to the Financial Ombudsman Service.

This is my final response.

Use signed for post: Check delivery date:

-

Yes portsmouth had its own registration, dont quite follow the logic of the Act which seems to say you can unless there has been a change of keeper or keepers address you dont have to go to the council to get it taxed you can do at a post office within 14 days of the tax expiring but dont see anything about allowing the vehicle to used or kept on the highway (33c?) without diplaying a valid tax disc?

It was an implicit agreement rather than an explicit statement as a new driver in the early 60's buying a different car when the old one died it was always understood that there was a 14 day period of grace but the tax would be back dated to the start of the month.

-

I didn't write to DCA, just spoke on the phone. Was advised not to put anything in writing so I telephoned them and told them to send me everything they had relating to this debt. I didn't admit to owning the debt. CDW are acting as a debt collector, the same collecting laws apply to them. Before accepting any ownership of the debt you want all the information they hold. If it reads anything like I got off the DCA good luck trying to work it out!

The advice given re telephoning a DCA is wrong, all communication must be kept in writing, keeping a checkable paper trail, DCAs have a habit of not having any record of calls.

-

Start the ball rolling by making a Formal Complaint to AVON

google the UK MD/CEO and address the complaint to that person.

Inform Sigma Red that the alleged account with Avon is fraudulent and no liability is accepted,

demand that SR communicates in writing only by Royal Mail,

no phone calls, e-mails or text messages.

Tis has happened before with Avon " recruiters" I'm told building their paper pyramids.

Use signed for post and check delivery.

-

I have an old Cap One debt which becomes SB in about 3 months.

Over the years it's been passed to a number of DCA.

I have sent CCA requests and about a year ago received a dodgy copy of an agreement

and a statement of account.

After receiving this I sent an 'in dispute' letter. Haven't heard anything until

last week when I received a letter from Drydensdalefairfax offering to accept a reduced payment if I settle.

This week I've received a letter advising they have been instructed by Arrow Global to commrnce legal proceedings if I don't .

I believe AG and Drydensdalefairfax are probably all part of the same company .

Not sure if I should call their bluff and ignore the letter or send a further CCA request and maybe a SAR. Thank you

DF is a law practice with a core business of debt collection and is regulated by the Solicitors Regulation Authority.

-

Hi guys,

Only about 8 months now until its well and truely statute barred YIPPEEE.

Will it become statute barred at the 6 year birthday of the default or from the first missed payment, if its the latter then its only around 6 months even better?

Ive had numerous letters from all sorts of collectors, usual threat o grams - but all of them have the wrong amount by 9 k. they have a zero missing so it looks like they arent pushing too hard to collect for just 1k. Even the default amount is incorrect on my credit file.

My wife still gets text msgs for mrs linda harris on her phone and to call urgently (like .... we will).

BTW this default hasnt hurt my rating that badly as ive purchased two cars on credit since the default went on or its down to the low amount the default actually lists that maybe the reason - mind boggles.

For CC which is a simple contract the clock started ticking from the date of the missed payment after which No further payment or unequivocal written acknowledgment of the debt was made.

The default remains on file until the 6th anniversary of the default date.

-

Turkey not happy, ammo drops, attacks in Canada.

The Terrorist are in every part of Europe and North America/Canada as well as Asia and Africa service personnel are at risk everywhere and so are civil police officers.

As the status is classed " a clear and present threat"!

-

[quote=Ell

Thanks ELL I missed that post!

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

Cabot/Restons County Court claim form received for debt I don't owe!

in Financial Legal Issues

Posted

Going back to the early-mid 2000s it was common practice for catalogue companies to "open a credit account" on acceptance of the 1st order from a customer.