1273

-

Posts

16 -

Joined

-

Last visited

-

I got two letter from Littlewoods stating that they they do not have a credit agreement and that they will not pursue the debts but every month they send a default letter...since. I wrote them and ask them to remove the default, but they just totally ignored me... What can i do to get the defaults removed?

-

Read this... was a court case 1 I, make this statement as my defence to the Claimant’s vague particulars of claim dated 27 October 2008. The Defendant respectfully seeks the courts permission upon clarification of the claimant’s case and disclosure of the necessary documents to amend this defence if required. 2 On the 19th May 2005, the Defendant signed an Application Form for a credit card facility to be provided by Claimant. (Exhibit 1) 3 Provision of this credit facility was dependant upon a satisfactory credit record being obtained by the Claimant from one or more Credit Reference Agencies, and upon other lending decision criteria. The Application Form was therefore a pre-contractual agreement to enter into a prospective full-regulated credit agreement with the Claimant in the event that the Defendant’s application was successful. 4 The Application Form contained a clause, which included the following statement - 'Please issue me with an additional Barclaycard for use on the account(s) to which this application relates. I accept to be bound by the Barclaycard Conditions of use'. As such, the application purports to bind the Defendant to the terms and conditions of any prospective credit agreement with the Claimant. 5 Section 59 (1) of the Consumer Credit Act 1974 states that 'an agreement is void if, and to the extent that, it purports to bind a person to enter as debtor or hirer into a prospective regulated agreement.’ The Defendant therefore contends that this pre-contractual document, not being a regulated credit agreement in itself, and insofar as it purports to bind the Defendant to the terms of an actual prospective regulated credit agreement, is void and of no effect. 6 The Defendant’s application for credit was successful and a line of credit was provided. However, no subsequent regulated credit agreement, fully setting out the proposed terms and conditions and containing all the terms, information and statutory statements as prescribed by the Consumer Credit Act, was ever provided by the Claimant for the Defendant to sign and agree to. The credit facility was therefore given with no agreement made for repayment. 7 I refer in this section to the alleged agreement exhibit A. 8 In respect of that which is denied, if the court should decide that the said agreement is not void by virtue of s59 (1): 9 it is respectfully submitted that the agreement is improperly executed because it is not in the prescribed format set out under The Consumer Credit (Agreements) Regulations 1983. The agreement was entered into before section 15 of the Consumer Credit Act 2006 came into force. Therefore, by way of schedule 3, s11 of the consumer credit act 2006, those sections otherwise repealed by the Consumer Credit Act 2006 section 15 remain in force. 10 Consequently, the court is precluded from issuing an enforcement order by way of s. 127 of the Consumer Credit Act 1974, since the document does not contain all the prescribed terms defined in the Consumer Credit (Agreements) Regulations 1983, these being defined by Reg 6(1) as being specified in Sch 6 to the Agreements Regulations for the purposes of s61 (1)(a) and s127 (3). (The omitted terms including Credit Limit, Rate of interest, and Payment terms under the Consumer Credit (Agreements) Regulations 1983 schedule 6. 11 Furthermore, the Defendant disputes the balance of the account, as during the period in which the account was operating The Claimant debited charges to the account in respect of purported breaches of contract on the part of the Defendant and also charged interest on the charges once applied. The Defendant understands that the Claimant will contend that the charges were debited in accordance with the terms of the contract between the Claimant and the Defendant and accordingly puts the Claimant to strict proof of such terms existence. The Defendant contends: a) No such contractual provision exists to allow Claimant to levy such charges; b) Where there is a contractual provision that permits the Claimant to levy such charges, this provision is unenforceable by virtue of the Unfair Terms in Consumer Contracts Regulations (1999) and the Common Law of penalty because they are a disproportionately high sum in compensation compared to the cost of the purported breach and are not a genuine pre-estimate of cost incurred by the Claimant; exceed any alleged actual loss to the Claimant in respect of any breaches of contract on the part of the Defendant; and are not intended to represent or are related to any alleged actual loss, but instead unduly enrich the Claimant, which exercises the contractual term in respect of such charges with a view to profit; and c) Accordingly the Defendant puts the Claimant to strict proof that every charge made to the account was valid and lawful. d) The Defendant has not been furnished with the requisite default notice in order for the Claimant to terminate the alleged agreement. e) And in any event, the Defendant avers that any Default or Termination Notice sent would have included penalty charges, invalidating that Notice as per Woodchester v lease. f) The Claimant contends that they have a claim to monies under an agreement between the defendant and the original creditor, the defendant seeks clarification of this fact and proof of legal assignment as required by Law of Property Act 1925 12 Accordingly, the Defendant puts the Claimant to strict proof that the agreement has been defaulted and terminated in accordance with s.88/s.98 CCA 1974 and the Consumer Credit (Enforcement, Default and Termination Notices) Regulations 1993. 13 Where the Defendant is unable to supply original signed certified copies of alleged Default Notices or Termination Notices, the Claimant pleads that the agreement has been unlawfully defaulted and terminated, in that, either; a) No Default Notice or Termination Notice has been issued, the Claimant being prepared to swear on oath that no such notice was sent or received at the time of default or termination; or b) Where the Defendant can show evidence that Default or Termination Notices were issued, such Notices are not accurate and fail to comply with s.88/s.98 CCA 1974 and the Consumer Credit (Enforcement, Default and Termination Notices) Regulations 1993, in that the Default and Termination amounts are incorrect as per paragraph 10(e) of this Statement. 14 The claimant respectfully requests that the court use its powers under section 141 of the consumer credit act to determine the rights of the parties. 15 For the reasons set out in this Defence, the Defendant’s position is that the Claimant’s Claim has no real prospect of success and discloses no reasonable grounds for it to be brought. The Defendant reserves the right to seek costs against the Claimant on the basis that such conduct is unreasonable and/or vexatious in bringing and/or pursuing this claim should the matter proceed to a full assessment.

-

Credit AGREEMENT -or- APPLICATION? RBS Advantage Card

1273 replied to diskmandave's topic in Royal Bank of Scotland

Can a Credit Card Application containing Key Financial Information (interest rates etc, loss and theft of card and genral information about missing payments and default charges be said to be an Consumer Credit Agreement. It also says 'once you have signed this agreement, you will have a short time to cancel it. We will send you the exact details of how and when you can do this.' There is no credit amount or credit limit. At the end it below my signature it says By signing this you authorise us when considering YOUR APPLICATION to gain additional relevant information, credit references, electoral role etc My signature is on the application form, and a section where they initial they recieved my proof of ID, not actually signing the agreement. It also has - we will tell you your credit limit when you first revieve your card. My question is can an application for a credit card, be used as a enforcable CCA?? -

scan0001.pdf here it is..

-

scan0001.pdf

-

This is it... Its my application.

-

Can a Credit Card Application containing Key Financial Information (interest rates etc, loss and theft of card and genral information about missing payments and default charges be said to be an Consumer Credit Agreement. It also says 'once you have signed this agreement, you will have a short time to cancel it. We will send you the exact details of how and when you can do this.' There is no credit amount or credit limit. At the end it below my signature it says By signing this you authorise us when considering YOUR APPLICATION to gain additional relevant information, credit references, electoral role etc My signature is on the application form, and a section where they initial they recieved my proof of ID, not actually signing the agreement. It also has - we will tell you your credit limit when you first revieve your card. My question is can an application for a credit card, be used as a enforcable CCA??

-

Unenforceable agreements under the Consumer Credit Act

1273 replied to Stub001's topic in General Debt Issues

Can a Credit Card Application containing Key Financial Information (interest rates etc, loss and theft of card and genral information about missing payments and default charges be said to be an Consumer Credit Agreement. It also says 'once you have signed this agreement, you will have a short time to cancel it. We will send you the exact details of how and when you can do this.' There is no credit amount or credit limit. At the end it below my signature it says By signing this you authorise us when considering YOUR APPLICATION to gain additional relevant information, credit references, electoral role etc My signature is on the application form, and a section where they initial they recieved my proof of ID, not actually signing the agreement. It also has - we will tell you your credit limit when you first revieve your card. My question is can an application for a credit card, be used as a enforcable CCA?? -

Can a Credit Card Application containing Key Financial Information (interest rates etc, loss and theft of card and genral information about missing payments and default charges be said to be an Consumer Credit Agreement. It also says 'once you have signed this agreement, you will have a short time to cancel it. We will send you the exact details of how and when you can do this.' There is no credit amount or credit limit. At the end it below my signature it says By signing this you authorise us when considering YOUR APPLICATION to gain additional relevant information, credit references, electoral role etc The only signature on the form is mine. (except when they initial my proofs of address and identification) It also has - we will tell you your credit limit when you first revieve your card. My question is can an application for a credit card, be used as a enforcable CCA??

-

Can a Credit Card Application containing Key Financial Information (interest rates etc, loss and theft of card and genral information about missing payments and default charges be said to be an Consumer Credit Agreement. It also says 'once you have signed this agreement, you will have a short time to cancel it. We will send you the exact details of how and when you can do this.' There is no credit amount or credit limit. At the end it below my signature it says By signing this you authorise us when considering YOUR APPLICATION to gain additional relevant information, credit references, electoral role etc The application form only has my signature... It also has - we will tell you your credit limit when you first revieve your card. My question is can an application for a credit card, be used as a enforcable CCA??

-

Credit Card agreement request template - COURT CLAIM

1273 replied to saitken's topic in Financial Legal Issues

Can a Credit Card Application containing Key Financial Information (interest rates etc, loss and theft of card and genral information about missing payments and default charges be said to be an Consumer Credit Agreement. It also says 'once you have signed this agreement, you will have a short time to cancel it. We will send you the exact details of how and when you can do this.' There is no credit amount or credit limit. At the end it below my signature it says By signing this you authorise us when considering YOUR APPLICATION to gain additional relevant information, credit references, electoral role etc It also has - we will tell you your credit limit when you first revieve your card. My question is can an application for a credit card, be used as a enforcable CCA?? -

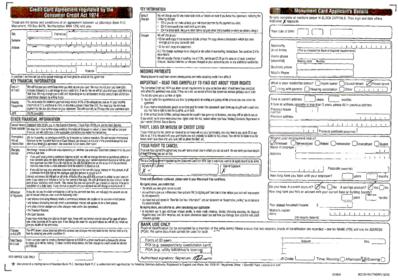

Please Check Out My Cca From Monument

1273 replied to ANDREAMOUR's topic in Debt Collection Agencies

Can a Credit Card Application containing Key Financial Information (interest rates etc, loss and theft of card and genral information about missing payments and default charges be said to be an Consumer Credit Agreement. It also says 'once you have signed this agreement, you will have a short time to cancel it. We will send you the exact details of how and when you can do this.' There is no credit amount or credit limit. At the end it below my signature it says By signing this you authorise us when considering YOUR APPLICATION to gain additional relevant information, credit references, electoral role etc It also has - we will tell you your credit limit when you first revieve your card. My question is can an application for a credit card, be used as a enforcable CCA?? Shouldnt it be a seperate document form the Application Form??? -

Please Check Out My Cca From Monument

1273 replied to ANDREAMOUR's topic in Debt Collection Agencies

They sent me a letter saying its enforcable and attached some terms and conditions which they say is up to date. Check this out. This is the application form/reply card I completed. It has no credit amount or credit limt etc. It is a good CCA?

-

Got this from Monument. Its a reply card/ application from. Look closely at it and give me some advice

-

Please Check Out My Cca From Monument

1273 replied to ANDREAMOUR's topic in Debt Collection Agencies

I recieved these documents from Monument please have a look on the and give me your opinion on the matter. They sent me this letter: I got an application form that they claim is enforceable: They attached terms and conditions to the application form: What should I do next?? Help.. please,,,