ads_uk

-

Posts

858 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by ads_uk

-

Parents didn't take photos back in April - they have a crappy flip phone with no camera or access to internet. I went down today and their is signage that Blue Badge now have to pay. (I have a photo of that) Previously they didn't, as it was run by the local authority for 20+years

-

So I understand and can advise my parents. As to what reason are they out of time. Is it due to the fact that they have failed to mention "schedule 4 of The Protections of Freedoms Act 2012" and therefore forgo their rights to any such claim? Edited: found this - If PoFA isn’t used (either by choice of the parking company, or because they haven’t achieved the requirements), then the keeper could be held liable if the parking company can demonstrate on the balance of probabilities that they were the driver at the time. This could be achieved, for example, if the driver intentionally or unintentionally reveals they were, or if the parking company has photographic evidence. They would have a job as the keeper doesnt have a drivers license as it's a mobility vehicle

-

Hi All, On behalf of my parents: 1 Date of the infringement: 12/04/2021 2 Date on the NTK: 11/06/2021 3 Date received: 17/06/2021 4 Does the NTK mention schedule 4 of The Protections of Freedoms Act 2012? NO 5 Is there any photographic evidence of the event? YES – But time/date stamps not readable 6 Have you appealed? No Have you had a response? No 7 Who is the parking company? Excel Parking Services Ltd 8. Where exactly: Site/Name on PCN/NTK = Three Spires Shopping Centre Short Stay Car Parks, Lichfield, WS13 6JF Actual site name (wrote next to machine) = Short Stay Car Park, Backcester Lane Appeals body they operate under: IAS Mother is a Blue Badge holder (father is driver) with Mobility Vehicle in her name. Not a company secretary as indicated on the PCN/NTK. Car Park site was operated/ran by Lichfield Council for the past 20yrs+, up until the Shopping Centre has taken it back on as of 1st March - spoke to Shopping Centre Manager who confirmed that Excel did not change the signage until 23rd March. For the last 20yrs+, the parking has always been Free parking for disabled badge holders (also confirmed on Google Street View - dated Sep 2020). This was their first time out of the house since March 2020, mother is classed as vulnerable, she would of been able to go out in July 2020, but fell and broke her hip - hospital stays meant further Isolation periods upto announcement that everyone was back inside.. Parents did not pay the £1.00 and have received notice for £100. As you can see from date of incident to date of issue has been 60days. Excel state they have 60 days to obtain the information from DVLA as per the International Parking Community (IPC) There is also no notification on the Local Authority (Lichfield District Council) or any other site that states Blue Badge holders will have to pay following the transfer to Excel. Please note my parents are not tech savvy, do not use the internet or have smart phone (an old flip phone works for them) Additional note: I have today gone to the site to check the signage - whilst I was there 5 people had issues paying (not accepting money): One man rang the helpline was instructed to use the payment machine on the other level - which is closed off to the public, informed the representative who then stated to pay by to be informed to either pay by App or Online - he stated he did not have card, they hung up. A woman tried to pay online and via the App which refused the site code and name - same person stated it has been the same since they took over the site, when she's complained she has always been told to buy a Monthly Permit. PCN (NTK) - 17.06.2021_compressed.pdf

-

Do you think inconsistency in reporting go in my favour? Equifax - No default registered, shows missed payments Aug - Oct 20 & two different settlement dates Nov & Dec 20. Aug 20 & prior paid on time marker for both Experian - Default registered Feb 2020 TransUnion - Default registered Feb 2020

-

Response from Head of Complaints: Looking though some older emails: One of the cards I had requested a payment plan in October 2019, then 13th Nov 2019 I requested the same plan for the 2nd card but they said they needed an income & expenditure (despite me being the same person and the details were exactly the same as the other card) -- at this point neither cards were in Default. I continued to complain about the refusal of the plan due to the fact that they already had the information on 3rd Jan 2020 it was escalated to the complaints team and they replied on 15 Jan 2020 but still insisted on an I&E for the second card. At this time, due circumstances beyond my control, I requested that the payment plan be lowered to £5 pcm and this to be active on the 2nd card as well and provided a revised I&E. This resulted in the Plan will only be put into place if the account is default (letter issued 21 Jan 2020) - Default applied 22nd Feb. I am going to wait for the SAR, and read through everything as it will show the difficulty I faced with the company trying to put a payment plan into place. Then try contacting the Company Secretary (Rupert MacInnes) and then if that fails CEO (Lucy-Marie Hagues) I think I am now completely out of luck in regards to Charges and Fee's, unless "Lockdown March 2020" can assist with being unable to complain to FOS within 6mths as an exception?

-

Hi All I have two Capital One Default entries on my report (which has now been a factor in being turned down for a job) - both accounts were low credit limit @ £200 each. From October 2019 I entered into a bit of an issue with finances & family matters and neglected payment on the accounts until a payment plan was set up in Jan 2020 . (no excuse I know) The main condition of the Payment Plans was that they would have to put my accounts as Default on acceptance of the payment plan as this was the only way one could be setup(?). (Default applied 22 Feb 2020) This is despite their own website stating "Money worries can be confusing, but don't worry, you have options. There are 3 steps you should take to avoid late fees and reduce any damage to your credit rating." & "Have your credit file show that you're doing your best to get back on track" ref: https://www.capitalone.co.uk/support/struggling-with-money.jsf Fast forward, I won a PPI battle with another company and money from that paid off both CapOne cards in Nov 2020. Prior to Oct 19 - I've managed the accounts accordingly. Card A - Started 2015 - credit report shows 2 missed payments (Jun 15 / Sep 18*), then Oct 19 to Jan 20 missed payment prior to Default. Card B - Started 2018 - No Missed payments until Oct 19 to Jan 20 *Sep 18: two separate payments were mistakenly made on Card B. There were other missed payments which were never negatively recorded due to 1-2 days due to payment processing. However I did still incur Late Payment Fees & Over limit fees on BOTH accounts in the same Months - basically equating to £48 of charges in a month. (2 x Late Payment / 2 x Over limit @ £12) but this was never negatively recorded on profile as I did make the payments. My questions are as follows: Charges: When a complaint is summitted how should Capital One treat a complaint? Is it a 1-2-1 relationship (CapOne & Customer) or is the complaint based upon the individual accounts. I am awaiting my SAR which will give me details of all charges since 2015 (start dates) Default: When entering a Payment Plan, should a Default be immediately applied to an account with no "Notice of Default" being issued ie the cooling off period? Is it appropriate for a company to register a default and not a payment plan marker on a credit report? I remember reading somewhere within the CONC guidelines about treating a customer fairly, and not misleading them - wouldn't the immediate default 'vs' their blurb on the website about reducing damage to credit rating be classed as misleading and treating a customer unfairly? (PS the company has said they will review my job application if I could get amended to a non-default marker)

-

Update from FOS. They have sided with Tesco Bank. Their main reasoning for this is due to "floor limit's" Thee statement the FOS put is as follows: "Regardless of who the retailer is, it’s not unusual for stores to have the aforementioned ‘floor limit’ in place. And if the store doesn’t request authorisation from Tesco for the transaction to be approved then it doesn’t have the opportunity to decline it, and once the transaction goes through Tesco has an obligation to pay that amount even if it takes the consumer over the agreed limit. So based on the information that I currently have I can’t find that Tesco’s done anything wrong because it’s correctly applied the over limit charges as per the terms and condition of the credit card. And while these same terms and conditions state Tesco has the ability to stop transactions and prevent consumers going over their limit, again this is only possible if the retailer requests authorisation for the transaction. But there’s also no obligation on the business to stop these transactions, the terms and conditions say that it can or may stop them but don’t state that they will. It’s important to remember that ultimately it’s always the consumer’s responsibility to manage their account and make sure that they stay within the agreed credit limit. It’s not the business’ responsibility to manage the consumer’s account for them and stop them from going over the limit." If all merchants have floor limits then what's to say for example Currys having a floor limit of £500 and someone with a credit limit less that £500, does this mean the transaction goes through? It seems like this so called floor limit is an excuse for Tesco's to make money.

-

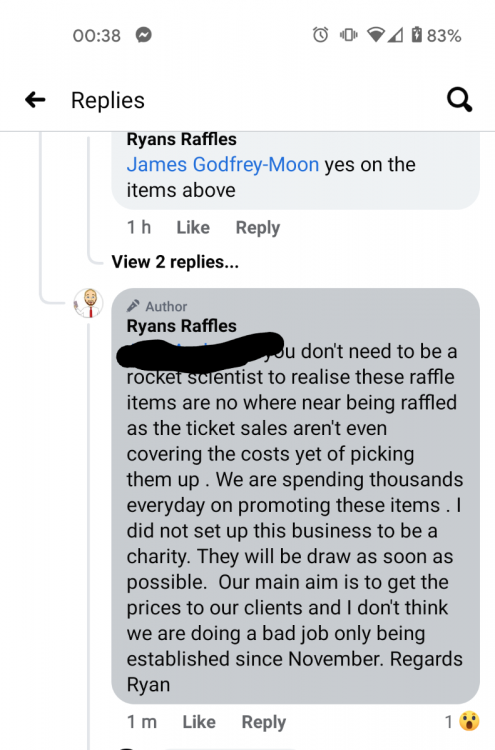

Terms and conditions state if less that 70% of tickets have been sold the a cash prize of 70% of ticket sales will be awarded. This was in the original and current terms & conditions. If a raffle has a Skill based element (question is required to be answered) and there is. Free entry route the Gambling Comission do not require it to be licensed. However, there have been users posting that they did the postal entries and not one of them has been awarded an entry ticket - he says they didn't do it correctly and deletes the comment. Requirement for postal is Postcard with name address, email, mobile and competiton name and answer. (Not hard is it?)

-

See attached The dates shown are competition start date and end date. I do not have screenshots from December as I didn't think anything was untoward. Entries purchased November for December (Christmas) Draws. After the draw date they were extended week by week but then exteded by 28days as we his new T & C's. Other people have also been impacted and posted asking when the tool sets, cars etc are going to be drawn only to have the comments deleted. He will reply sarcastically in the early hours and then delete his comments. (See also attached)

-

I invested £100 into the raffle site (I am on others which operate as expected and have won a few prizes) I've not invested anything further but others are still being fobbed off by this person. The site is called Ryan's Raffles https://ryansraffles.co.uk/ The Facebook page of which im blocked for commenting/messaging & leaving a review is: https://www.facebook.com/ryansraffle If you take a look at the reviews you can see how he's asked if there's an issue but then no response. Also shows negative review with other person who is experiencing the same.

-

The way the site is being run there are no intentions to hold the draws. Original T&C's permitted the operator of the site to extend the draws to the end of January. This date passed with each competition marked as Closed awaiting draw, only to have a new active timer for another 28 days - meaning they broke the original terms and conditions. Then 5th Feb, he updated the terms and conditions which now means he can extend to around May. Surely the original T&C's for competitions prior to 5th Feb change must be adhered to? Is there a governing body that monitors this, or can someone just create a site and have no intentions to hold draws & keep extending the draw date beyond the t&C's?

-

That's correct. Keeps extending. Past it's original T&C's - blocked from commenting / contacting the site/Facebook page. Owner of the Raffle site has multiple businesses (car sales & repairs are two)

-

Hi all Bit of advice please as I can not find anything on the internet relating to governance of online Raffle. The Gambling Comission do not require these such sites to be licensed if they offer a free entry route or a element of skill (such as answering a question correctly). Bank (starling) refusing to refund as MasterCard (who supply the debit card) state "When disputing transactions we have to follow specific rules set by MasterCard. Based on further investigation, we will unfortunately be unable to dispute these transactions at this time. This is because the service was provided by the merchant which entailed depositing of funds and facilitating wagering (buying raffles). As the merchant has provided this service, we have no chargeback rights to dispute this payment." my issue is with one site which looked at first legitimate but lots of things have happened since entering competitions: 1) Draw dates constantly extended. Original Draw dates December constantly changed again should of ended today but extended to march. 2) terms & conditions amended on 5th Feb which amended the Maximum extension period from 7 days + 4x7 days maximum extension to 28+ 4x28 days. 3) Messages, emails unanswered. Questions and comments about the draws deleted off Facebook & blocked from further commenting/messaging 4) positive reviews made by family members and employees of owners other companies 5) winners previously associated with the owners companies There is one negative review, bs people have commented on this stating the same issues but are blocked from writing a review but able to comment on the negative review (?) Any advice or is it a case of Action Fraud.

-

thanks

-

hi all. bit of advice please. I had a Three contract up until November last year. At £11pcm for 24mths. Paid every month on time via their online portal. When I ported over, I received a letter from Three thanking me for being a customer blah blah blah.. It also said IF I owed anything a final bill will be sent. No final bill ever received - I get a phone call around the first week in December form an Indian sounding man who was extremly difficult to understand. Said he was calling from Three, and wanted me to confirm my details - something of which I didnt as something didnt sit right. He said I could log into my account and review my bill as I owed money and then hung up. After the call I thought I'd best log into my account just in case. Couldnt log in. Account access denied. Logged on to chat - they said as I ported over and I was no longer a customer my access was suspended. Couple of weeks later I had another call from a local area number and answered again it was some Indian guy telling me I owed money, wanting me to confirm details. I refused and he said details will be sent out to me to my email on account and my home address as it was important. Once again nothing.. 15th Dec I received an email from PastDue in my name RE Three. Email stated they were contacting me about Three an I should receive a letter soon regards to this matter. Says about visiting their website. 22nd Jan another email form Pastdue. Stating they have yet to receive a response to the letter, and they had already sent me an email about this. We will continue to contact you until this matter is resolved. Again asks me to login. 23rd Jan letter received dated 13th Jan. Titled "We are here to help keep your Three Services" Claiming I owed "Airetime Balance £201.43" and contract period was 26/11/2019 to 25/11/2020 States "We have been appointed by Three to recover the amount of £201.43. If you pay this amount in full Three may be able to waive the cancellation fee and reconnect their service for you" - what cancellation fee / re connection??? I ended the contract giving the 30days notice and paying the last bill.. Then the normal crap about its important to pay. If I'm experiencing difficulties etc. Now both December and January Credit reports from ClearScore, Credit Karma, Credit Expert, Totally Money and Equifax all show Three as Closed and balance as Zero. (Date Satisfied /closed 17th Nov, bal 0, last updated 30th Nov) I've had nothing from Three. As far as I'm concerned I owe nothing as no final bill and no access to the portal. Should I email PastDue and do a prove it & attach proof of Credit Reports being £0 or do I do something else?

-

Ah right. So that could have a negative impact. His 2 CC defaults are still with FOS for PPI so he's hoping they will be word clean. As always thanks for your time

-

Nope. It's only showing missing payments. No default at all

-

Thanks for reply. AT time loan issued he was in debt for around £1.5k. CRA's around time loan issued show that only 4 credit cards (2 went to default in jun 19) a Paypal Credit account and a ShopDirect - all within 20% of credit limit on each. (and Car Insurance paid mthly) Since loan issued he took out a Everyday loan which has another 20mths to go, but has been paid on time without any missed or negative marker. No defaults were ever recorded on his closed accounts.

-

I would like some advice please. Trying to resolve an issue friend has got, and I'm a bit stumped. They have a 12mth loan account June 2018, but have never paid a penny towards it for some reason. As of today the Debt is not defaulted only shows as Missed Payments. Not once have they been chased for the loan, there's no record of contact or letters within their DSAR relating to collections - it just seems that the account fell off the radar. Now they are in a position to pay this debt in full, however they have spoken to the lender who has apologised about the lack of contact - and has stated they are prepared to reduce the amount owing by 20% (£450-ish) as a Partial Settlement. They do have 2 x default markers on their CRA which will be updated to satisfied (?) as they both now have a zero balance and a loan which has no negative markers. Should they take this offer of Partial Settlement - is there quite a negative impact to their CRA if they did, they are hoping to secure Car finance in the new year.

-

An update. Complaint has gone into FoS, yet to be assigned a case number. Whilst I've been waiting I contacted the company (Morrisons) where she purchased fuel. Two replies came back, both stating that when purchasing from a Kiosk, it's an online transaction, not pre-authorised and also that you need to have sufficient funds available else the card will be declined. With this, I went back to Tesco, as it made the statement they based the rejection for refund completely untrue. I also added that a section of their own T&C's states "In certain circumstances, we'll need to suspend or restrict the use of your card. We'll only do this for a good reason, including when: (d) The transaction would take you over your limit or you are already over limit" In less than 24hrs they responded with yet another excuse not to refund: "After looking at the further information you provided, my decision remains unchanged. The reason for this is Tesco Bank can decline transactions that would take you over your agreed credit limit if we receive an authorisation request from the retailer. However, retailers have a floor limit and the merchant can approve a transaction that is lower than this limit without the authorisation request being sent to us. It is therefore not possible for us decline every transaction that may exceed your limit." So they are saying that, you've tried your hardest to prove us wrong, lets try it this way; it's the Merchants issue, not theirs; despite Morrisions saying the funds must be available they deny this; you can run up a debt with Tesco Bank as they don't hold you to a credit limit. How can a company be so underhanded and lie, cheat and steal. Not abide by their own T&C's Surely this contravenes some sort of code of ethics/standards? Has anyone come across this before?

-

DSAR Sent. She received details of this payment arrangement and it doesn't still seem right. OverDue amount: £87 Overlimit amount: £55 Proposed plan = £25.00 for the next 4 months. After the 4 months the account will be in Arrears by £110 which would require a lump sum? Current Credit Limit = £250 Current Balance = £305 Now, my maths tell me that £25 x 4 = £100, deduct that from the Balance and then that leaves £205, £45 below the Credit Limit. So why would a lump sum be required? This is what I'm not understanding.

-

Hi ya. Little update She received a default notice for £302. (C/Limit of £250) In arrears total £83.00 She rang them as they were supposed to put her on the COVID payment break freeze thing. They said a freeze was applied 6th July but as it's gone past the 90 days, collection letters commence - she pointed out that 90days would mean Oct. Bit of a track back by the agent who said the account was placed on a temp hold whilst complaint was investigated and not the covid freeze (despite originally stating that she was struggling back in June) Now this is the part I'm having trouble understanding. The agent has told her to prevent the account being Terminated & Defaulted she would need to do an arrangement. For some stupid reason she's told them she can afford £25 pcm. They have told her that based on that they will freeze the account at 0% interest and not accrue any charges. Now for the bit i dont understand - they have the arrangement would be £25 pcm, then she would have to pay £110 lump sum to clear the arrears. She did not understand this and neither do I - the agent stated that the system generates the minimum payment (£25) due and they can not do anything about that, so the £110 will be the arrears of the minimum payment due. Surely if she accepts this £25pcm for 4mths would bring the balance below the £250 credit limit - so no arrears outstanding. - the person is insistent that their calculator is right. She has asked for it to be put in writing before she accepts -- she said she told the agent multiple times that she did not understand, and that the agent was insistent of accepting. in the end the agent agreed to place the account on hold for 20days so the information could be sent through. Am I missing something on the lumpsum / arrears - if a repay plan is in place at £25 and is paid monthly, then how can arrears increase? That would mean that she would need to pay £50+ pcm to clear arrears? Once this letter comes through I'm going to DSar them for the telephone call, as Tesco state all calls are recorded as she should not be pushed into accepting something she didnt understand.

-

You said FOS don't rarely side with the consumer. Then again it costs nothing to try.

-

Best tell her the bad news that she's going to have to pay it. Cheers for your help

-

Do I need to reply to them or is it now FOS. The kiosk bit is a bit of lie. Ive gone to a garage kiosk and purchased fuel before and tried to pay with the wrong card and the card gets rejected if there is insufficient funds available.