sammyc1974_Derby

-

Posts

72 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by sammyc1974_Derby

-

-

Have a read of this it may help

-

Something you all might find useful.

http://www.oft.gov.uk/shared_oft/consumer_leaflets/credit/oft144.pdf

-

voda I did say it was off another thread and the author does say general rule of thumb. however when I used it to calculate another loan I have it was only 1p out.

I have just used both calculators,

Here's what i have put in

Total loan (car and Insuurances) £7464.00

Apr 30.7%

48 Monthly payments @ £256.20 (agreement says £255.30) dif 0.90p

Total Amount to Repay £12,297.52 (agreement says £12354.40)dif -56.88

Total Interest Charged £4,833.52 (agreement says £4890.40)diff -56.88.

They are undercharging me by 90pence a month, but have overcharged my interest,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,

So i am now thinking that possibly my calcs are still wrong, would someone else have a look............;-)

-

sol I've been told by a site team member agreement fee with interest is ok if written in your agreement in font that has the same size and prominence as all other t and c it's not ok if they have added it in before apr. I think the wilson case was like the 2nd example. however by my calculations which I will have to check the interest charged on mine is higher than that on my agreement. so as I have a final response from welcome and c case open with fos about this I'll prob just send to them

So how can we check if its been put in before the APR, Peter checked my agreement and said the apr is correct, I'm CONFUSED NOW

-

Does that mean I am finally interesting

Still something bugging me about all that...but leave that with me for now. Doing my CCA 101 still! Am kinda like a dog with a bone with something until I am satisfied

Not telling you to restart payments says to me, in their mind they are the start of a 'discussion' with you on this, no the end of one?

Cannot remember if you have already but have you complained to the head honcho at NU?

I think a complaint to the FSA from everyone that have not had the obligations of that Insurance Info (what did you cal it Mojo?) fulfilled....and maybe lots of angry letters to said head honcho ot NU too

After Mr P Sent me a letter telling me that they didn't charge interest on the acceptance fee and write back proving it, I had a response from my Calculations yesterday telling me they do charge interest on the acceptance fee, but there was nothing to tell me to carry on with my payments

-

Thats Fine

Do You Have The Nottingham Compliance Address

As This Is Mr P

What Did You Expect

Sorry , You Will Get To Know Him Better From The Forum

Yes i have the address, just get fed up of writing letters to them. Is there anything i can do regards to the payment they have taken.

-

Have a look at what i'm sending them and please give your input.

Thanks

24th March 2009

Account Number:

To whom it may concern

Point 1 My Wife has been through my loan statement that was sent to me on the 4th Feb 2009, All the Payments made to the account from myself have all be reconciled to my Bank Statements, except for one dated 06/05/2008 Adhoc Card Payment Credit £255.30, this payment left my bank account on the 7th May 2008 (statement No.14) which is so far correct, then on 09/05/2008 the loan statement reads O2 Payer Deceased Debit £255.30, So the payment was taken back from my loan account even though it has been debited from my bank account, I have enclosed a copy of the bank statement to back this up.

Point 2 I would like a full reason and understanding of why on the 27/03/2008 I had an HDPI fee charged to my account £17.73 and on the 02/11/2006 I had an ad Hoc Fee of £100 applied to my account could this be the option fee......................

Point 3 please could you give me full breakdowns including explanation as to why the following amounts were applied to my account:

26/02/2008

£19.98

30/01/2008

£19.41

16/01/2008

£16.70

29/11/2007

£25.00

26/11/2007

£12.26

13/11/2007

£10.00

25/10/2007

£10.00

25/10/2007

£12.01

25/09/2007

£6.94

19/09/2007

£10.00

14/09/2007

£10.00

10/09/2007

£10.00

05/09/2007

£10.00

04/09/2007

£20.00

28/08/2007

£5.56

24/08/2007

£10.00

23/08/2007

£10.00

16/08/2007

£10.00

14/08/2007

£10.00

14/08/2007

£20.00

23/07/2007

£5.62

26/07/2007

£5.33

25/05/2007

£7.10

27/03/2007

£10.00

14/02/2007

£20.00

14/12/2006

£20.00

02/11/2006

£100.00

It states on the bottom of the loan statement that capitalisation is interest, but how can I be charged so much interest when I have already been charged interest in the beginning, Charge for Credit includes the interest for the Car and the acceptance fee, Isn’t what you are doing called ‘Capitalising interest’ and is not advisable there are only certain situations that demand it be done. Please could you advise me of the reason why you as a company felt it necessary to capitalise interest on my account.

Point 4 if you look back at my notes you should see that I complained regarding the interest on the acceptance fee, I received a response from Mr Palmer which stated that you do not charge interest on the acceptance fee and that if I had evidence in which to prove you had charged me interest on my acceptance fee then I was to send it to yourselves, which I did, Yesterday I received a letter responding to my calculations stating that you do charge interest on the acceptance fee, I find this quite laughable as the first response had come from your legal compliance officer and the second had come from a compliance officer, so which one of the two are correct, both responses have been forwarded to the FOS as I feel this is not a correct a full response to my complaint.

Point 5 I asked in a previous correspondence if the insurances on my account could be refunded and cancelled as I felt that they were not necessary , At the time of purchase I was told I would have to have it as if the car was to be written off then my normal car insurance would not cover the outstanding finance , The breakdown insurance we were told that we would need this as if the car became faulty then this would cover it, Well the car did become faulty when I rang welcome finance and told them I was given the number for welcome insurances, the lady I spoke to their told me to take it to a garage and find out what is wrong then give us a call back and we will see if it is covered. We paid for this out of our own pocket.

Now from the beginning of these so called policies I have not been given any policy numbers, documentation or contact numbers, so I do not know who the policies are with what is covered and how long they run for, So as I have not been given this information I think it only fair that I am given a full refund of insurances, interest charged and interest accrued on what I have already paid, if you cannot do this then please provide me with the Name of the Companies whom I am insured with and their contact details, so that I can get a full refund. By law you have to provide me with my insurers details.

I would like to make you aware that my account will remain in dispute until you have looked at all points in this letter and taken the actions necessary to correct them, As they are all errors on your behalf, Please find the recap below this statement.

Point 1 The balance on my account has been incorrect since 09/05/08; because a payment was credited to my account then it was wrongfully debited. As you will see on the bank statement this payment was paid to yourselves on the 7/05/08. Bank Statement No 14 (included as proof).

Point 2 What is a HDPI fee and why it has been charged to my account at £17.76, what was I charged £100.00 for on the 02/11/06; a full explanation must be provided.

Point 3 Charges listed above must be given a full explanation as to what the charges were and why they were charged, where interest has been charged a full explanation must be given to why you felt it necessary to Capitalise on the interest as this can only be done in situations that demand it.

Point 4 Two responses sent from you regarding interest being charged on the acceptance fee, both responses give different verdicts, which is the correct verdict the one from the Legal Compliance Officer Mr Palmer or the one from the Compliance officer.

Point 5 Please refund all of the insurances, interest charged and interest accrued on them to date, if this cannot be done then please forward details of the insurers to myself.

I look forward to your response within 14 working days.

Many Thanks

-

But i made payment with my card and it went from the bank ok, which is fine. its just that they have had the payment from me, credited it to my account then a couple of days later, debited it from my account so it looks like no payment was made. The description they have given it is as follows:

09/05/08 O2 Payer Deceased Debit £255.30 £8582.84

-

I am just in the process of writing a letter, so i would like to know whether i need to tell them they have stolen from me or not.

-

OK on the 6th May 2008 i made a debit card payment for 255.30 which went through ok, (bank statement as proof) My balance went from £8577.84 to £8327.54.

On the 9th May 2008 this payment was debited back to my welcome account so my balance went from £8327.54 to £8577.84.

So I am asking is this classed as theft

-

Hi Sammy

Just A Bit Confused As To Your Question

Take Your Time

OK on the 6th May 2008 i made a debit card payment for 255.30 which went through ok, (bank statement as proof) My balance went from £8577.84 to £8327.54.

On the 9th May 2008 this payment was debited back to my welcome account so my balance went from £8327.54 to £8577.84.

So I am asking is this classed as theft

-

Sorry i meant wrongfully deducted the money, which as far as i can see means that my balance has been wrong by 255.30 since 9th may 2008.

By wrong i mean it should be less than what it is............

-

I'm just putting another letter together, I had my statement of account sent and i have noticed that a payment i made to welcome using my debit card (that was sucessful bank statement as proof) on the 6th May 2008 was then debited to my welcome account on the 9th may 2008, so is this classed as theft on there behalf as they have wrongfully taken the money back......

PLEASE HELP,

:mad::mad:Sorry i meant wrongfully deducted the money, which as far as i can see means that my balance has been wrong by 255.30 since 9th may 2008.

-

I'm just putting another letter together, I had my statement of account sent and i have noticed that a payment i made to welcome using my debit card (that was sucessful bank statement as proof) on the 6th May 2008 was then debited to my welcome account on the 9th may 2008, so is this classed as theft on there behalf as they have wrongfully taken the money back......

PLEASE HELP,

:mad::mad: -

Just a very quick question, we purchased our car on the 9/9/2006, from ucan, our finance was done through welcome which we didn't know, now looking at the sales receipt the date is 09/09/2006, the finance agreemnt is date by the sales guy 13/09/2006....does this make any difference as we took the finance out on the 09/09/06 not 13/09/2006

-

Sammy, i think he was referring to my agreement.

Felix

Yeah i was having a moment.....................

-

Hi

Sorry have quite a lot to look at misssed yours

-

Peter

I also posted a letter on here last night that i recieved from Mr P and its states that the is no insurance charged on the acceptance fee.....

-

Peter,

I've rescanned the agreement should be better now.

Thanks

http://i722.photobucket.com/albums/ww223/1sammyc1974/Page2of2003.jpg

Peter

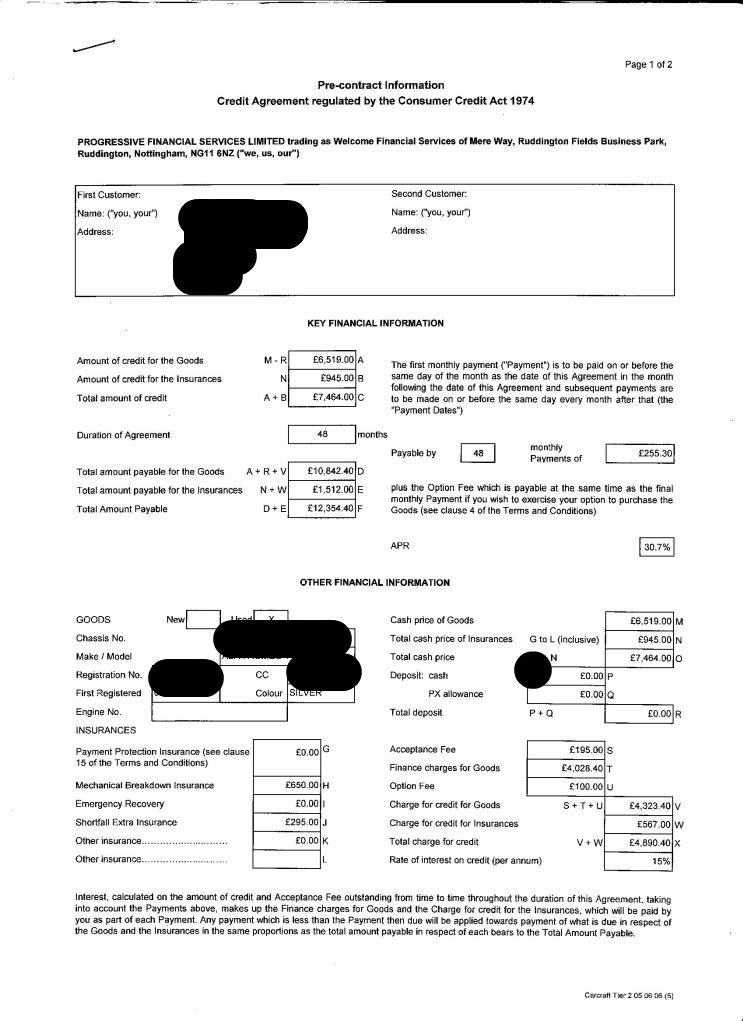

could you have a look at this i know its the pre contractual agreement, the figures are identical to credit agreement, i've used this as the credit agreement won't scan properly as its only a copy..

Thanks

In advance

-

Andie.

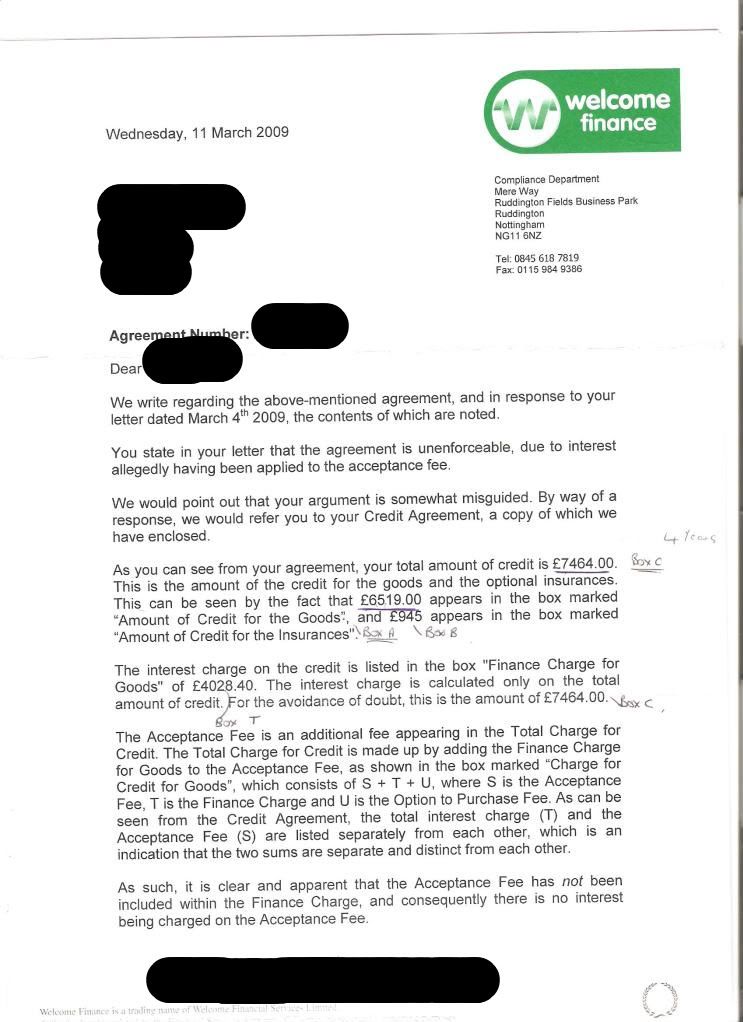

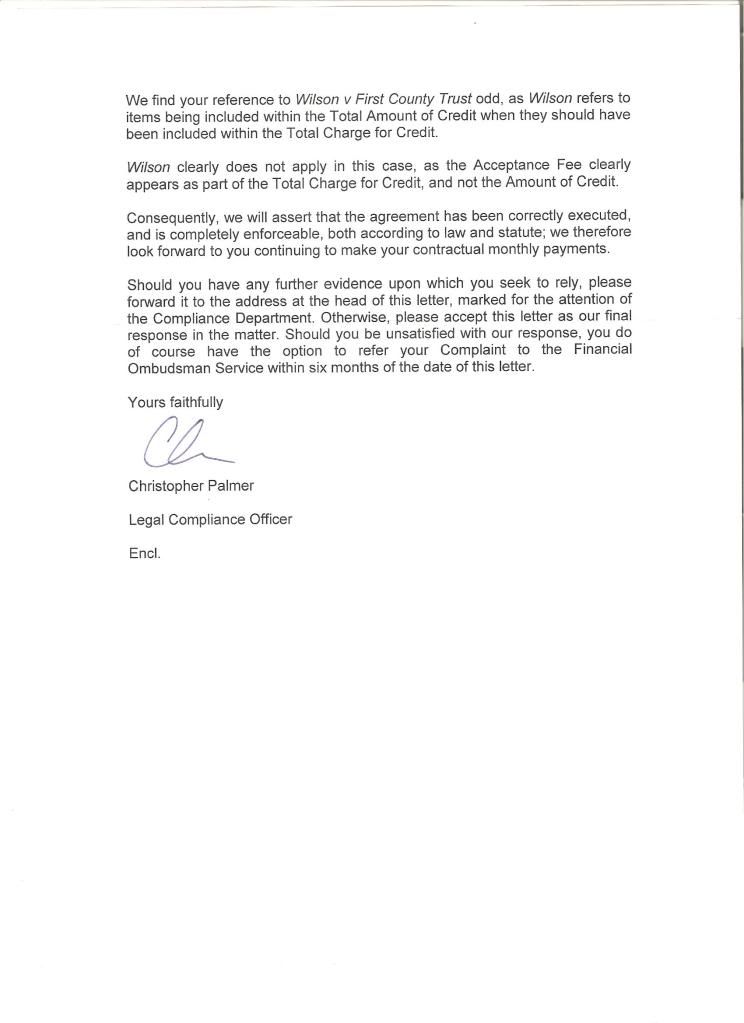

Take a look at the letter i recieved from Mr p, They're his words not mine, pay special attention to last Paragraph on 1st page....

Let me know what you think..

http://i722.photobucket.com/albums/ww223/1sammyc1974/Page2of2004.jpg

http://i722.photobucket.com/albums/ww223/1sammyc1974/Page2of2005.jpg

-

Post,

I've sent you a PM.

-

Peter,

I've rescanned the agreement should be better now.

Thanks

http://i722.photobucket.com/albums/ww223/1sammyc1974/Page2of2003.jpg

would someone please have a check of my agreement as now i know that the interest can be charged on the acceptance fee i need to know if everything else is ok,

-

Peter,

I've rescanned the agreement should be better now.

Thanks

http://i722.photobucket.com/albums/ww223/1sammyc1974/Page2of2003.jpg

-

So what happens if the apr and the interest per anum on agreement don't add up.......... Apr 30.7% Interest Per Anum 15%, So if the Interest Per Anum is 15% Shouldnt the APR be 30% or if the APR is 30.7% the shouldnt the interest per anum be 15.35%, doing the calculations they have used the 15% per anum so doesn't that make my APR out by .7%?????????????????????

I also wrote and complained about the interest on the acceptance fee and i was told that none had been charged, so if it is a corect practice why didn't they just write back to me and say that they are allowed to do this, but Mr Palmer asked for further evidence that i wish to rely on, which i have now sent.... But no reply

{kind=link}

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

Welcome Finance - This company needs to be banned.

in Welcome Finance

Posted

My comlpaint is now with the FOS and welcome are well aware of this, well i had a call on my mobile last night it went, Hello is ****** there please, I said whose speaking please, he said its Tom, I said Tom From ???, He said oh its a social call, and I said what on his wifes mobile..He stuttered for a while and said If you can get him to call me back, I said inconnection with, He stuttered and said he'll know who it is....is he there, I said No and put the phone down.

I did a trace on the number this morning and it is welcome, but they are answering the phone stating who is speaking and not the company.....The woman i spoke to this morning said she couldn't speak to me as i'm not the account holder, all she said was that they wanted an update as to what was happening with the FOS ??????? so if i could get ***** to ring then that would be great, I explained to her that they were not supposed to be calling us and that the account was on hold as i had filed another Complaint...She insisted i get my husband to ring back and i said that i will get him to ring when i recieve a response to my letter dated 31st March, she got really snotty and put the phone down....I then rang the FOS to let them now that welcome had been ringing us and the nice lady said ring them and tell them to put the account on hold...So i rang the snotty girl at welcome back told her what the fos had said and she took the complaint number and their phone number and said i'll update the account...